Management Accounting Project Report

VerifiedAdded on 2022/11/14

|14

|3542

|252

AI Summary

This Management Accounting Project Report includes schedules, activities, and resource drivers used in blending, custard tart, and other activities. It covers traditional and activity-based costing systems, management accounting factors, benefits, costs, and limitations. The report also provides references for further reading.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Management Accounting

1

Project Report: Management Accounting

1

Project Report: Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

2

Contents

Answer 1, 2, 3 and 4.........................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Schedule 3.....................................................................................................................3

Schedule 4.....................................................................................................................4

Schedule 5.....................................................................................................................6

Schedule 6.....................................................................................................................7

Answer 5...........................................................................................................................8

Answer 6...........................................................................................................................8

Answer 7...........................................................................................................................9

Answer 8 and 9.................................................................................................................9

Introduction...................................................................................................................9

Traditional costing system..........................................................................................10

Activity based costing system....................................................................................10

Management accounting factor...................................................................................11

Benefit, cost and limitations.......................................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

2

Contents

Answer 1, 2, 3 and 4.........................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Schedule 3.....................................................................................................................3

Schedule 4.....................................................................................................................4

Schedule 5.....................................................................................................................6

Schedule 6.....................................................................................................................7

Answer 5...........................................................................................................................8

Answer 6...........................................................................................................................8

Answer 7...........................................................................................................................9

Answer 8 and 9.................................................................................................................9

Introduction...................................................................................................................9

Traditional costing system..........................................................................................10

Activity based costing system....................................................................................10

Management accounting factor...................................................................................11

Benefit, cost and limitations.......................................................................................12

Conclusion..................................................................................................................12

References.......................................................................................................................13

Management Accounting

3

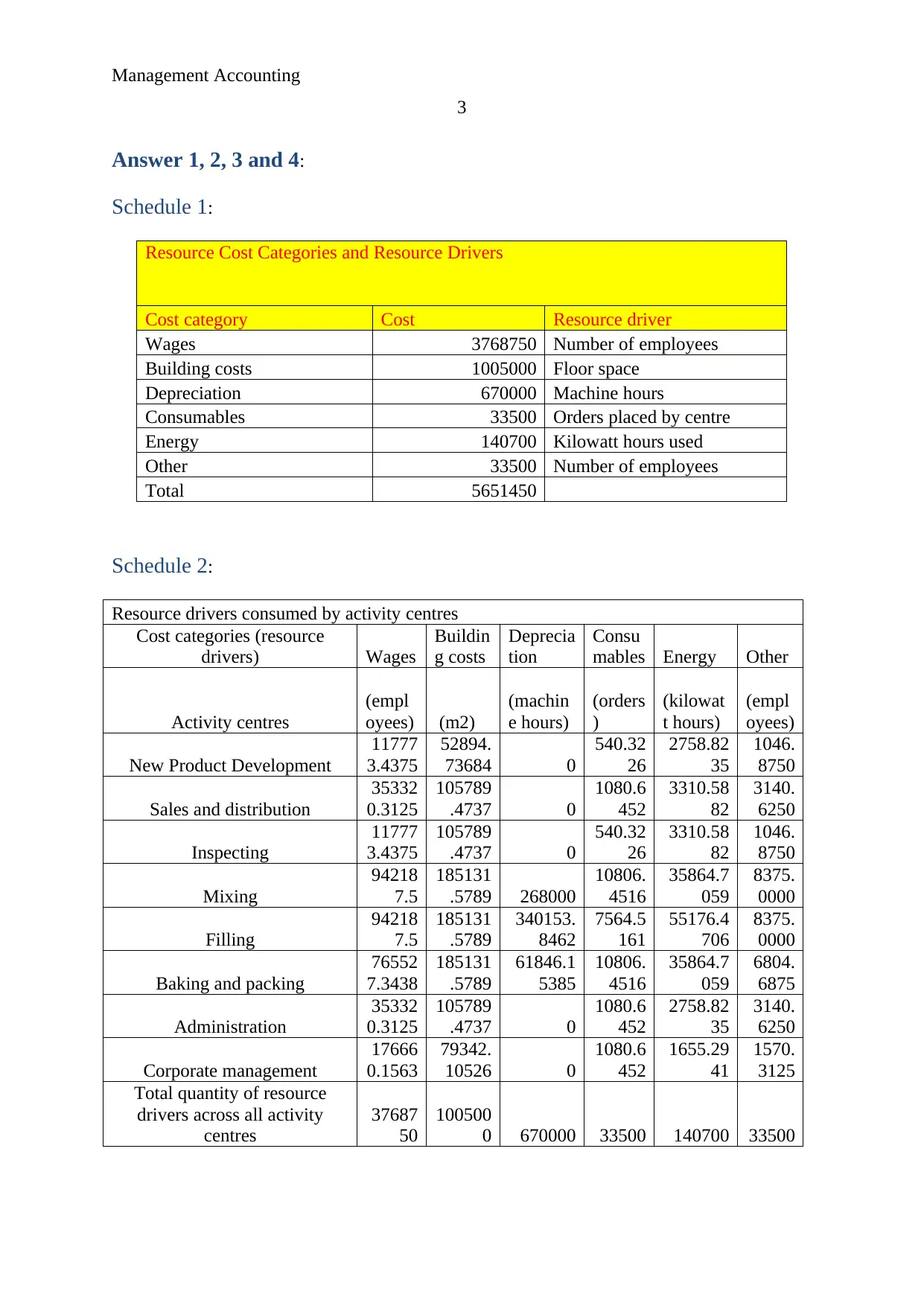

Answer 1, 2, 3 and 4:

Schedule 1:

Resource Cost Categories and Resource Drivers

Cost category Cost Resource driver

Wages 3768750 Number of employees

Building costs 1005000 Floor space

Depreciation 670000 Machine hours

Consumables 33500 Orders placed by centre

Energy 140700 Kilowatt hours used

Other 33500 Number of employees

Total 5651450

Schedule 2:

Resource drivers consumed by activity centres

Cost categories (resource

drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres

(empl

oyees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product Development

11777

3.4375

52894.

73684 0

540.32

26

2758.82

35

1046.

8750

Sales and distribution

35332

0.3125

105789

.4737 0

1080.6

452

3310.58

82

3140.

6250

Inspecting

11777

3.4375

105789

.4737 0

540.32

26

3310.58

82

1046.

8750

Mixing

94218

7.5

185131

.5789 268000

10806.

4516

35864.7

059

8375.

0000

Filling

94218

7.5

185131

.5789

340153.

8462

7564.5

161

55176.4

706

8375.

0000

Baking and packing

76552

7.3438

185131

.5789

61846.1

5385

10806.

4516

35864.7

059

6804.

6875

Administration

35332

0.3125

105789

.4737 0

1080.6

452

2758.82

35

3140.

6250

Corporate management

17666

0.1563

79342.

10526 0

1080.6

452

1655.29

41

1570.

3125

Total quantity of resource

drivers across all activity

centres

37687

50

100500

0 670000 33500 140700 33500

3

Answer 1, 2, 3 and 4:

Schedule 1:

Resource Cost Categories and Resource Drivers

Cost category Cost Resource driver

Wages 3768750 Number of employees

Building costs 1005000 Floor space

Depreciation 670000 Machine hours

Consumables 33500 Orders placed by centre

Energy 140700 Kilowatt hours used

Other 33500 Number of employees

Total 5651450

Schedule 2:

Resource drivers consumed by activity centres

Cost categories (resource

drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres

(empl

oyees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product Development

11777

3.4375

52894.

73684 0

540.32

26

2758.82

35

1046.

8750

Sales and distribution

35332

0.3125

105789

.4737 0

1080.6

452

3310.58

82

3140.

6250

Inspecting

11777

3.4375

105789

.4737 0

540.32

26

3310.58

82

1046.

8750

Mixing

94218

7.5

185131

.5789 268000

10806.

4516

35864.7

059

8375.

0000

Filling

94218

7.5

185131

.5789

340153.

8462

7564.5

161

55176.4

706

8375.

0000

Baking and packing

76552

7.3438

185131

.5789

61846.1

5385

10806.

4516

35864.7

059

6804.

6875

Administration

35332

0.3125

105789

.4737 0

1080.6

452

2758.82

35

3140.

6250

Corporate management

17666

0.1563

79342.

10526 0

1080.6

452

1655.29

41

1570.

3125

Total quantity of resource

drivers across all activity

centres

37687

50

100500

0 670000 33500 140700 33500

Management Accounting

4

Schedule 3:

Activities and resource drivers used - Blending

Activity

Percentage of

labour time

Percentage of

floor space

Percentage of

machine hours Energy

Consu

mable

Ot

he

r

Set up Mixer 94218.75 9256.5789 0 0 0

83

7.5

Weigh and

Sort

Ingredients 94218.75 9256.5789 0 0 0

83

7.5

Load mixer 376875 129592.1053 268000

35864.

70588

10806.

45161

33

50

Operate mixer 188437.5 9256.5789 0 0 0

16

75

Unload and

Clean mixer 94218.75 9256.5789 0 0 0

83

7.5

Move to

Filling room 94218.75 18513.1579 0 0 0

83

7.5

Total 942187.5 185131.5789 268000

35864.

70588

10806.

45161

83

75

Schedule 4:

List of activities

Activity

Activ

ity

cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

1766

60

Assigned directly to

products

Process

receivables

1755

81 No. of invoices 3400 invoices

51.641

5

Process payables

1149

28 No. of purchase orders 1700

purchase

orders

67.604

7

Production

planning

1755

81

No. of production

schedules 670

productio

n

schedules

262.06

12

Reports to Health

Dept

2246

1 No. of reports 67 reports

335.23

88

Process sales

order

2991

57 No. of sales orders 2680

sales

orders

111.62

57

Dispatch sales

order

1641

75 No. of dispatches 1700

dispatche

s

96.573

5

New Product

Development

1177

73

Assigned directly to

new products lines

Inspect filling 8854 No. of batches 670 batches 132.15

4

Schedule 3:

Activities and resource drivers used - Blending

Activity

Percentage of

labour time

Percentage of

floor space

Percentage of

machine hours Energy

Consu

mable

Ot

he

r

Set up Mixer 94218.75 9256.5789 0 0 0

83

7.5

Weigh and

Sort

Ingredients 94218.75 9256.5789 0 0 0

83

7.5

Load mixer 376875 129592.1053 268000

35864.

70588

10806.

45161

33

50

Operate mixer 188437.5 9256.5789 0 0 0

16

75

Unload and

Clean mixer 94218.75 9256.5789 0 0 0

83

7.5

Move to

Filling room 94218.75 18513.1579 0 0 0

83

7.5

Total 942187.5 185131.5789 268000

35864.

70588

10806.

45161

83

75

Schedule 4:

List of activities

Activity

Activ

ity

cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

1766

60

Assigned directly to

products

Process

receivables

1755

81 No. of invoices 3400 invoices

51.641

5

Process payables

1149

28 No. of purchase orders 1700

purchase

orders

67.604

7

Production

planning

1755

81

No. of production

schedules 670

productio

n

schedules

262.06

12

Reports to Health

Dept

2246

1 No. of reports 67 reports

335.23

88

Process sales

order

2991

57 No. of sales orders 2680

sales

orders

111.62

57

Dispatch sales

order

1641

75 No. of dispatches 1700

dispatche

s

96.573

5

New Product

Development

1177

73

Assigned directly to

new products lines

Inspect filling 8854 No. of batches 670 batches 132.15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

5

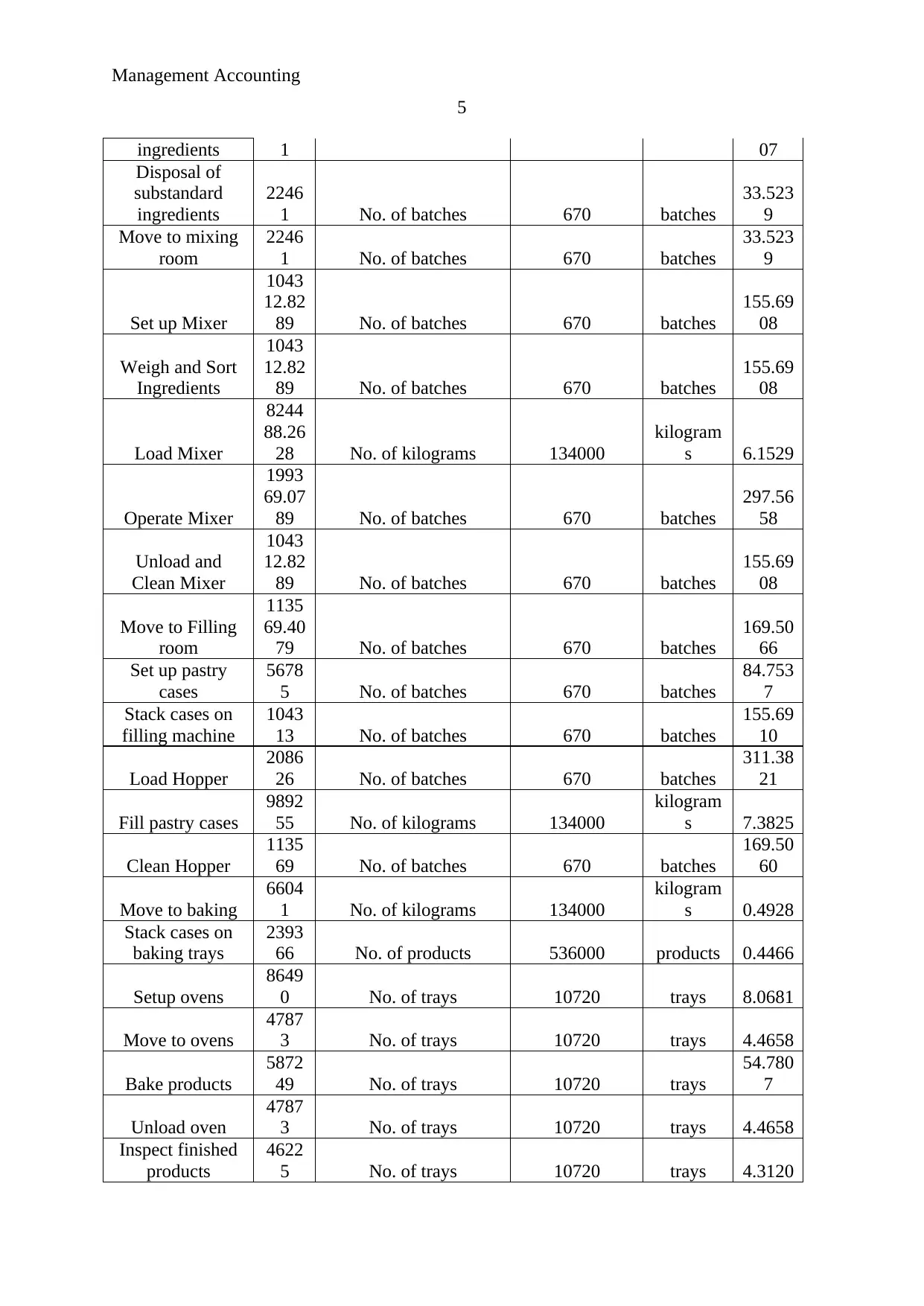

ingredients 1 07

Disposal of

substandard

ingredients

2246

1 No. of batches 670 batches

33.523

9

Move to mixing

room

2246

1 No. of batches 670 batches

33.523

9

Set up Mixer

1043

12.82

89 No. of batches 670 batches

155.69

08

Weigh and Sort

Ingredients

1043

12.82

89 No. of batches 670 batches

155.69

08

Load Mixer

8244

88.26

28 No. of kilograms 134000

kilogram

s 6.1529

Operate Mixer

1993

69.07

89 No. of batches 670 batches

297.56

58

Unload and

Clean Mixer

1043

12.82

89 No. of batches 670 batches

155.69

08

Move to Filling

room

1135

69.40

79 No. of batches 670 batches

169.50

66

Set up pastry

cases

5678

5 No. of batches 670 batches

84.753

7

Stack cases on

filling machine

1043

13 No. of batches 670 batches

155.69

10

Load Hopper

2086

26 No. of batches 670 batches

311.38

21

Fill pastry cases

9892

55 No. of kilograms 134000

kilogram

s 7.3825

Clean Hopper

1135

69 No. of batches 670 batches

169.50

60

Move to baking

6604

1 No. of kilograms 134000

kilogram

s 0.4928

Stack cases on

baking trays

2393

66 No. of products 536000 products 0.4466

Setup ovens

8649

0 No. of trays 10720 trays 8.0681

Move to ovens

4787

3 No. of trays 10720 trays 4.4658

Bake products

5872

49 No. of trays 10720 trays

54.780

7

Unload oven

4787

3 No. of trays 10720 trays 4.4658

Inspect finished

products

4622

5 No. of trays 10720 trays 4.3120

5

ingredients 1 07

Disposal of

substandard

ingredients

2246

1 No. of batches 670 batches

33.523

9

Move to mixing

room

2246

1 No. of batches 670 batches

33.523

9

Set up Mixer

1043

12.82

89 No. of batches 670 batches

155.69

08

Weigh and Sort

Ingredients

1043

12.82

89 No. of batches 670 batches

155.69

08

Load Mixer

8244

88.26

28 No. of kilograms 134000

kilogram

s 6.1529

Operate Mixer

1993

69.07

89 No. of batches 670 batches

297.56

58

Unload and

Clean Mixer

1043

12.82

89 No. of batches 670 batches

155.69

08

Move to Filling

room

1135

69.40

79 No. of batches 670 batches

169.50

66

Set up pastry

cases

5678

5 No. of batches 670 batches

84.753

7

Stack cases on

filling machine

1043

13 No. of batches 670 batches

155.69

10

Load Hopper

2086

26 No. of batches 670 batches

311.38

21

Fill pastry cases

9892

55 No. of kilograms 134000

kilogram

s 7.3825

Clean Hopper

1135

69 No. of batches 670 batches

169.50

60

Move to baking

6604

1 No. of kilograms 134000

kilogram

s 0.4928

Stack cases on

baking trays

2393

66 No. of products 536000 products 0.4466

Setup ovens

8649

0 No. of trays 10720 trays 8.0681

Move to ovens

4787

3 No. of trays 10720 trays 4.4658

Bake products

5872

49 No. of trays 10720 trays

54.780

7

Unload oven

4787

3 No. of trays 10720 trays 4.4658

Inspect finished

products

4622

5 No. of trays 10720 trays 4.3120

Management Accounting

6

Disposal of

substandard

product

2246

1 No. of trays 10720 trays 2.0952

Move to truck

5713

0 No. of trays 10180

Finished

trays 5.6120

* All

Calculations to 4

decimal places

“??” indicates that

these figures must be

calculated.

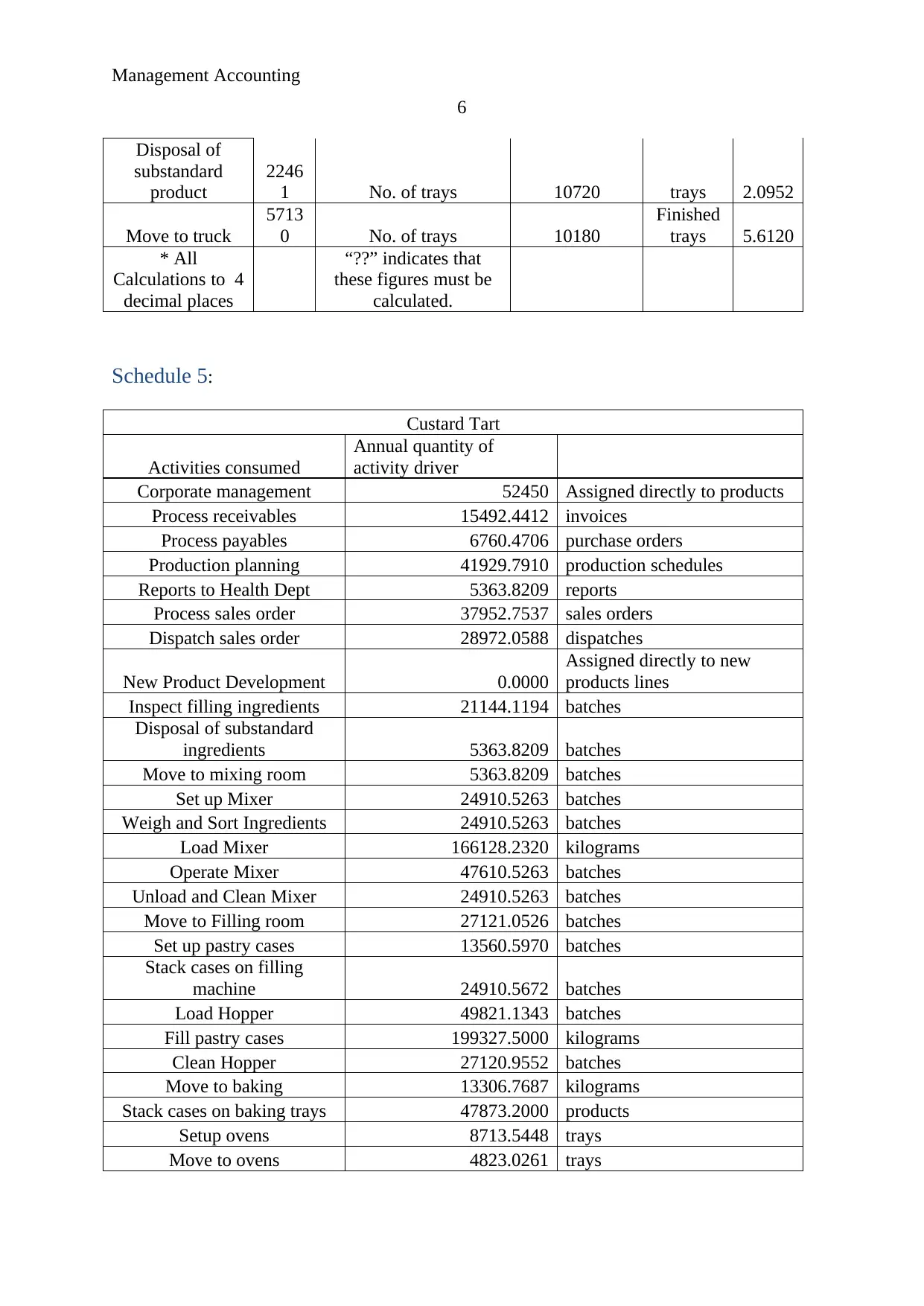

Schedule 5:

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 52450 Assigned directly to products

Process receivables 15492.4412 invoices

Process payables 6760.4706 purchase orders

Production planning 41929.7910 production schedules

Reports to Health Dept 5363.8209 reports

Process sales order 37952.7537 sales orders

Dispatch sales order 28972.0588 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 21144.1194 batches

Disposal of substandard

ingredients 5363.8209 batches

Move to mixing room 5363.8209 batches

Set up Mixer 24910.5263 batches

Weigh and Sort Ingredients 24910.5263 batches

Load Mixer 166128.2320 kilograms

Operate Mixer 47610.5263 batches

Unload and Clean Mixer 24910.5263 batches

Move to Filling room 27121.0526 batches

Set up pastry cases 13560.5970 batches

Stack cases on filling

machine 24910.5672 batches

Load Hopper 49821.1343 batches

Fill pastry cases 199327.5000 kilograms

Clean Hopper 27120.9552 batches

Move to baking 13306.7687 kilograms

Stack cases on baking trays 47873.2000 products

Setup ovens 8713.5448 trays

Move to ovens 4823.0261 trays

6

Disposal of

substandard

product

2246

1 No. of trays 10720 trays 2.0952

Move to truck

5713

0 No. of trays 10180

Finished

trays 5.6120

* All

Calculations to 4

decimal places

“??” indicates that

these figures must be

calculated.

Schedule 5:

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 52450 Assigned directly to products

Process receivables 15492.4412 invoices

Process payables 6760.4706 purchase orders

Production planning 41929.7910 production schedules

Reports to Health Dept 5363.8209 reports

Process sales order 37952.7537 sales orders

Dispatch sales order 28972.0588 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 21144.1194 batches

Disposal of substandard

ingredients 5363.8209 batches

Move to mixing room 5363.8209 batches

Set up Mixer 24910.5263 batches

Weigh and Sort Ingredients 24910.5263 batches

Load Mixer 166128.2320 kilograms

Operate Mixer 47610.5263 batches

Unload and Clean Mixer 24910.5263 batches

Move to Filling room 27121.0526 batches

Set up pastry cases 13560.5970 batches

Stack cases on filling

machine 24910.5672 batches

Load Hopper 49821.1343 batches

Fill pastry cases 199327.5000 kilograms

Clean Hopper 27120.9552 batches

Move to baking 13306.7687 kilograms

Stack cases on baking trays 47873.2000 products

Setup ovens 8713.5448 trays

Move to ovens 4823.0261 trays

Management Accounting

7

Bake products 59163.1455 trays

Unload oven 4823.0261 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 6060.9430 Finished trays

Direct Materials 1

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 700

Annual Volume 108000

* All Calculations to 4

decimal places

Total Indirect Cost 995888.8953

Per Unit Indirect cost 9.2212

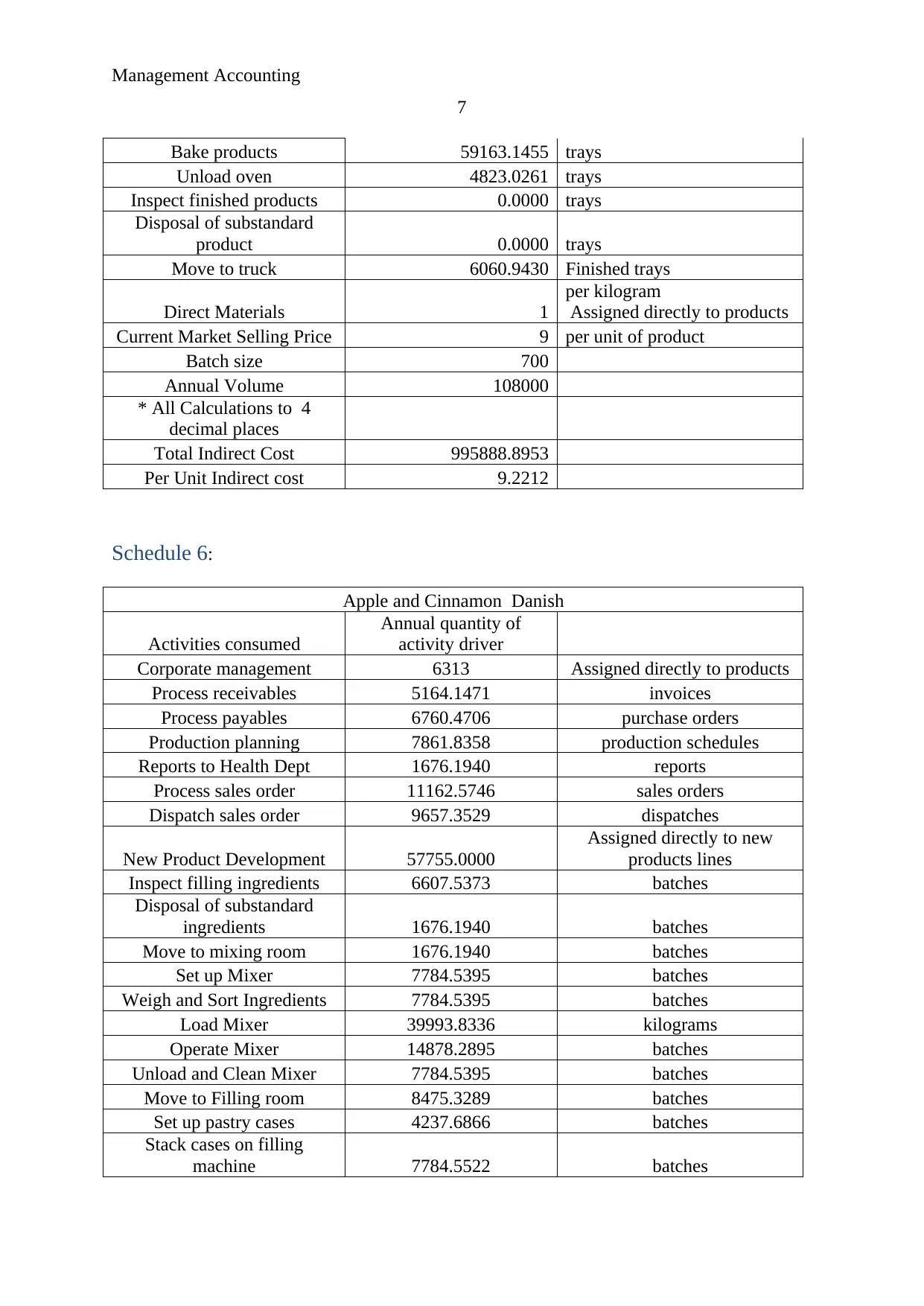

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 6313 Assigned directly to products

Process receivables 5164.1471 invoices

Process payables 6760.4706 purchase orders

Production planning 7861.8358 production schedules

Reports to Health Dept 1676.1940 reports

Process sales order 11162.5746 sales orders

Dispatch sales order 9657.3529 dispatches

New Product Development 57755.0000

Assigned directly to new

products lines

Inspect filling ingredients 6607.5373 batches

Disposal of substandard

ingredients 1676.1940 batches

Move to mixing room 1676.1940 batches

Set up Mixer 7784.5395 batches

Weigh and Sort Ingredients 7784.5395 batches

Load Mixer 39993.8336 kilograms

Operate Mixer 14878.2895 batches

Unload and Clean Mixer 7784.5395 batches

Move to Filling room 8475.3289 batches

Set up pastry cases 4237.6866 batches

Stack cases on filling

machine 7784.5522 batches

7

Bake products 59163.1455 trays

Unload oven 4823.0261 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 6060.9430 Finished trays

Direct Materials 1

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 700

Annual Volume 108000

* All Calculations to 4

decimal places

Total Indirect Cost 995888.8953

Per Unit Indirect cost 9.2212

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 6313 Assigned directly to products

Process receivables 5164.1471 invoices

Process payables 6760.4706 purchase orders

Production planning 7861.8358 production schedules

Reports to Health Dept 1676.1940 reports

Process sales order 11162.5746 sales orders

Dispatch sales order 9657.3529 dispatches

New Product Development 57755.0000

Assigned directly to new

products lines

Inspect filling ingredients 6607.5373 batches

Disposal of substandard

ingredients 1676.1940 batches

Move to mixing room 1676.1940 batches

Set up Mixer 7784.5395 batches

Weigh and Sort Ingredients 7784.5395 batches

Load Mixer 39993.8336 kilograms

Operate Mixer 14878.2895 batches

Unload and Clean Mixer 7784.5395 batches

Move to Filling room 8475.3289 batches

Set up pastry cases 4237.6866 batches

Stack cases on filling

machine 7784.5522 batches

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

8

Load Hopper 15569.1045 batches

Fill pastry cases 47986.2500 kilograms

Clean Hopper 8475.2985 batches

Move to baking 3203.4813 kilograms

Stack cases on baking trays 5984.1500 products

Setup ovens 2178.3862 trays

Move to ovens 1205.7565 trays

Bake products 14790.7864 trays

Unload oven 1205.7565 trays

Inspect finished products 1164.2491 trays

Disposal of substandard

product 565.7155 trays

Move to truck 1459.1159 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 12.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 318821.8602

Per Unit Indirect cost 11.5935

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 5651450

2 Total Annual Units produced 500000

3 Per Unit Indirect Cost 11.3029

4 Cost For Custard Tart 1220713.2 995888.8953

224824.304

7

5

Cost for Apple and Cinnamon

Dash 146937.7 318821.8602

-

171884.160

2

Answer 5:

On the basis of above calculations, it has been measured that the product cost of from

traditional costing system and activity based costing system is different. The reason behind

difference in the cost is due to the different process and consideration of both the accounting

system.

8

Load Hopper 15569.1045 batches

Fill pastry cases 47986.2500 kilograms

Clean Hopper 8475.2985 batches

Move to baking 3203.4813 kilograms

Stack cases on baking trays 5984.1500 products

Setup ovens 2178.3862 trays

Move to ovens 1205.7565 trays

Bake products 14790.7864 trays

Unload oven 1205.7565 trays

Inspect finished products 1164.2491 trays

Disposal of substandard

product 565.7155 trays

Move to truck 1459.1159 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 12.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 318821.8602

Per Unit Indirect cost 11.5935

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 5651450

2 Total Annual Units produced 500000

3 Per Unit Indirect Cost 11.3029

4 Cost For Custard Tart 1220713.2 995888.8953

224824.304

7

5

Cost for Apple and Cinnamon

Dash 146937.7 318821.8602

-

171884.160

2

Answer 5:

On the basis of above calculations, it has been measured that the product cost of from

traditional costing system and activity based costing system is different. The reason behind

difference in the cost is due to the different process and consideration of both the accounting

system.

Management Accounting

9

Answer 6:

On the basis of above calculations, it has been measured that the product cost of

Custard Tart is overstated whereas the product cost of Apple and Cinnamon Dash is

understated on the basis of comparison with traditional costing system. the reason behind

overstate and understate cost is difference between the costing system.. Calculations of the

same are as follows:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773 7821758.01

5 Cost for Apple and Cinnamon Dash 1173565.217 581870.7269

591694.490

5

Answer 7:

On the basis of the study, it has been observed that there are various difference which

has occurred into the business in last 15 years. These changes have occurred due to the

following reasons:

1. Material cost is one of the important reasons. Along with the time, the material cost of

the company has been improved and it has affected over the cost structure of the

company.

2. The production process of the company has also impacted over the production cost

and process of the business.

3. Further, labour cost is also one of the important reasons. Along with the time, the

labour cost of the company has been improved and it has affected over the cost

structure of the company (Bhimani, Horngren, Datar and Foster, 2009).

4. Further, the fixed cost such as higher electricity cost, machinery cost, depreciation etc

has also improve the cost level of the business.

Answer 8 and 9:

Introduction:

9

Answer 6:

On the basis of above calculations, it has been measured that the product cost of

Custard Tart is overstated whereas the product cost of Apple and Cinnamon Dash is

understated on the basis of comparison with traditional costing system. the reason behind

overstate and understate cost is difference between the costing system.. Calculations of the

same are as follows:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 10796800

2 Total Annual Units produced 230000

3 Per Unit Indirect Cost 46.9426087

4 Cost For Custard Tart 9623234.783 1801476.773 7821758.01

5 Cost for Apple and Cinnamon Dash 1173565.217 581870.7269

591694.490

5

Answer 7:

On the basis of the study, it has been observed that there are various difference which

has occurred into the business in last 15 years. These changes have occurred due to the

following reasons:

1. Material cost is one of the important reasons. Along with the time, the material cost of

the company has been improved and it has affected over the cost structure of the

company.

2. The production process of the company has also impacted over the production cost

and process of the business.

3. Further, labour cost is also one of the important reasons. Along with the time, the

labour cost of the company has been improved and it has affected over the cost

structure of the company (Bhimani, Horngren, Datar and Foster, 2009).

4. Further, the fixed cost such as higher electricity cost, machinery cost, depreciation etc

has also improve the cost level of the business.

Answer 8 and 9:

Introduction:

Management Accounting

10

Costing is a strategy or a system that is utilizes by organizations to collect, evaluate,

distribute and manage the expense to every asset driver and every component of costing and

overheads in an production organization. Costing method must be successful as a compelling

and huge costing strategy which offers the required information, certainty sheet and data to

the administrators and the organization for dealing with the orders, diminishing the waste and

limiting the expense.

Costing systems are constantly utilized by each manufacturing house to improve the

benefits and limit the expenses to accomplish the objectives and upgrade the value of the

manufacturing house. This report has been set up to examine the exchanging costing strategy

and movement costing technique (Drury, 2013). This report delineates about the inadequacies

of both the systems.

The case study of Centuria Company has been studied. The company is operating

since last 15 years in the market and producing various products in the market. the company

is using traduitional costing system from last 15 years to manage the cost of the company.

Howevre, along with the time, the management of the company is seeking changes. Hence,

the company is planning to adopt activity based costing.

Traditional costing system:

Traditional costing framework is one of the most used and oldest method among each

of the strategies of cost accounting method. This system is utilized by the manufacturing

house and organizations to identify classify and allocate the expense to each cost driver and

component of cost accounting system. This procedure does not investigate the complexity

data of the manufacturing house. It assigns all the expense to the cost centre as per the normal

rate of overhead. This technique recommends the organization to draw all the indirect

overhead and other overhead expense into the manufacturing division. This strategy just uses

one cost driver to apply all the expense similarly to each item.

The principle deficiency with this strategy is its technique for appointing cost. It

allocates the whole indirect expense under the manufacturing head and it has an effect over

the expense of manufacturing by expanding it. This system impacts the choice of the

management in regards to the cost (Garrison et al, 2010). In ABC costing method, the cost is

allocated to the production department on the basis of the cost centres.

10

Costing is a strategy or a system that is utilizes by organizations to collect, evaluate,

distribute and manage the expense to every asset driver and every component of costing and

overheads in an production organization. Costing method must be successful as a compelling

and huge costing strategy which offers the required information, certainty sheet and data to

the administrators and the organization for dealing with the orders, diminishing the waste and

limiting the expense.

Costing systems are constantly utilized by each manufacturing house to improve the

benefits and limit the expenses to accomplish the objectives and upgrade the value of the

manufacturing house. This report has been set up to examine the exchanging costing strategy

and movement costing technique (Drury, 2013). This report delineates about the inadequacies

of both the systems.

The case study of Centuria Company has been studied. The company is operating

since last 15 years in the market and producing various products in the market. the company

is using traduitional costing system from last 15 years to manage the cost of the company.

Howevre, along with the time, the management of the company is seeking changes. Hence,

the company is planning to adopt activity based costing.

Traditional costing system:

Traditional costing framework is one of the most used and oldest method among each

of the strategies of cost accounting method. This system is utilized by the manufacturing

house and organizations to identify classify and allocate the expense to each cost driver and

component of cost accounting system. This procedure does not investigate the complexity

data of the manufacturing house. It assigns all the expense to the cost centre as per the normal

rate of overhead. This technique recommends the organization to draw all the indirect

overhead and other overhead expense into the manufacturing division. This strategy just uses

one cost driver to apply all the expense similarly to each item.

The principle deficiency with this strategy is its technique for appointing cost. It

allocates the whole indirect expense under the manufacturing head and it has an effect over

the expense of manufacturing by expanding it. This system impacts the choice of the

management in regards to the cost (Garrison et al, 2010). In ABC costing method, the cost is

allocated to the production department on the basis of the cost centres.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

11

Through breaking down the contextual analysis of Centuria Company, it has been

recognized that the traditional costing framework isn't agreeable to the organization. Because

of this costing technique, organization has faced numerous issues, for example, decrease in

benefits, low support and different issues. It has been discovered that this method don't give

the precise figures to the management thus that the process and strategies of the business

could be manipulated.

Activity based costing system:

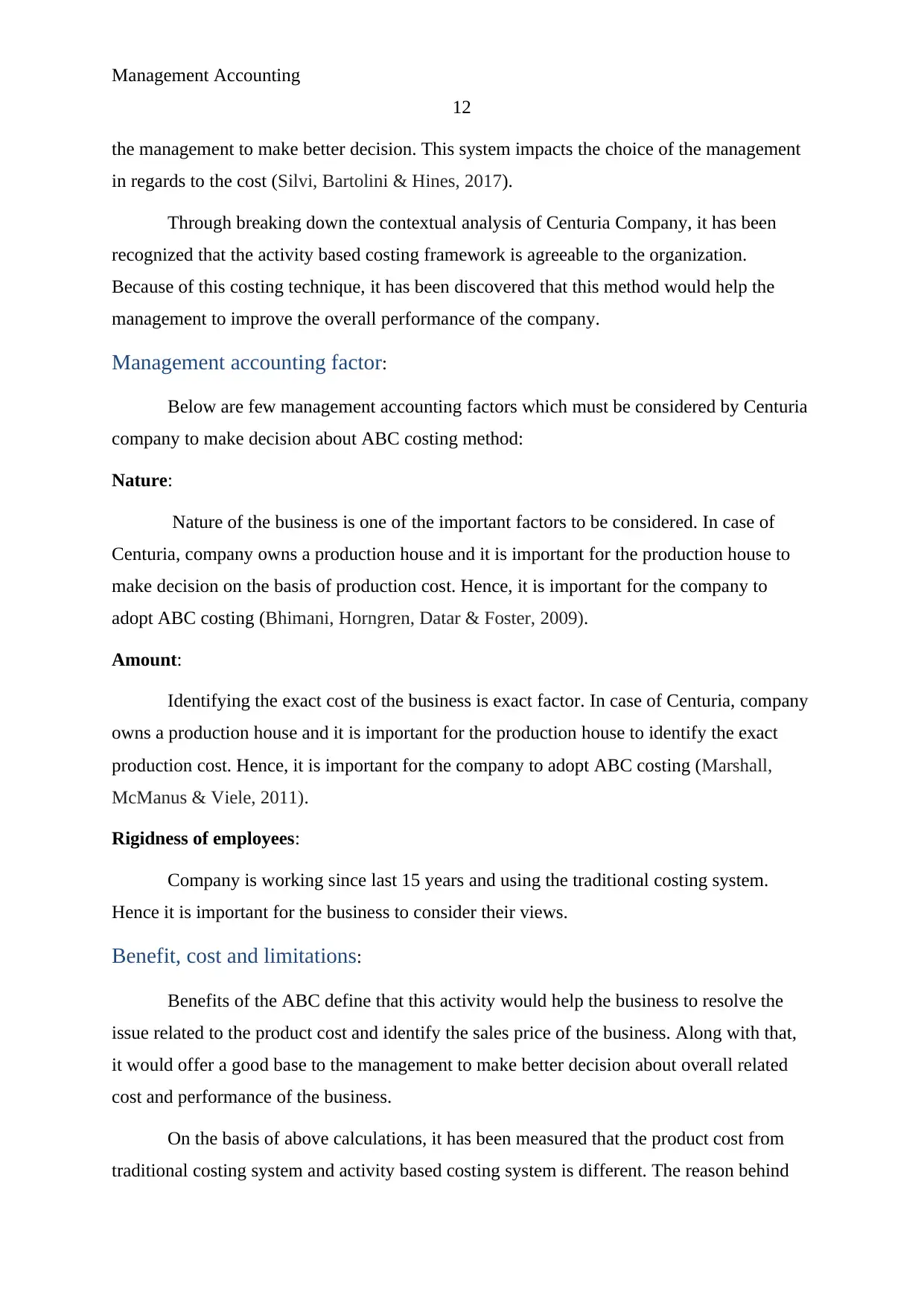

Activity based costing framework is one of the newest method among each of the

strategies of cost accounting method. This system is utilized by the manufacturing house and

organizations to identify classify and allocate the expense to each cost driver and component

of cost accounting system (Rasiah, 2011). This procedure investigates the complexity data of

the manufacturing house. It assigns all the expense to the cost centre as per their contribution.

This technique recommends the organization to draw all the indirect overhead and other

overhead expense into the manufacturing division on the basis of cost centre and their

allocated rate. This strategy takes the concern over all the cost drivers.

(Weygandt, Kimmel & Kieso, 2015)

The principle deficiency with this strategy is its complexity for appointing cost. It

allocates the whole indirect expense on the basis of their cost centre which makes it easier for

11

Through breaking down the contextual analysis of Centuria Company, it has been

recognized that the traditional costing framework isn't agreeable to the organization. Because

of this costing technique, organization has faced numerous issues, for example, decrease in

benefits, low support and different issues. It has been discovered that this method don't give

the precise figures to the management thus that the process and strategies of the business

could be manipulated.

Activity based costing system:

Activity based costing framework is one of the newest method among each of the

strategies of cost accounting method. This system is utilized by the manufacturing house and

organizations to identify classify and allocate the expense to each cost driver and component

of cost accounting system (Rasiah, 2011). This procedure investigates the complexity data of

the manufacturing house. It assigns all the expense to the cost centre as per their contribution.

This technique recommends the organization to draw all the indirect overhead and other

overhead expense into the manufacturing division on the basis of cost centre and their

allocated rate. This strategy takes the concern over all the cost drivers.

(Weygandt, Kimmel & Kieso, 2015)

The principle deficiency with this strategy is its complexity for appointing cost. It

allocates the whole indirect expense on the basis of their cost centre which makes it easier for

Management Accounting

12

the management to make better decision. This system impacts the choice of the management

in regards to the cost (Silvi, Bartolini & Hines, 2017).

Through breaking down the contextual analysis of Centuria Company, it has been

recognized that the activity based costing framework is agreeable to the organization.

Because of this costing technique, it has been discovered that this method would help the

management to improve the overall performance of the company.

Management accounting factor:

Below are few management accounting factors which must be considered by Centuria

company to make decision about ABC costing method:

Nature:

Nature of the business is one of the important factors to be considered. In case of

Centuria, company owns a production house and it is important for the production house to

make decision on the basis of production cost. Hence, it is important for the company to

adopt ABC costing (Bhimani, Horngren, Datar & Foster, 2009).

Amount:

Identifying the exact cost of the business is exact factor. In case of Centuria, company

owns a production house and it is important for the production house to identify the exact

production cost. Hence, it is important for the company to adopt ABC costing (Marshall,

McManus & Viele, 2011).

Rigidness of employees:

Company is working since last 15 years and using the traditional costing system.

Hence it is important for the business to consider their views.

Benefit, cost and limitations:

Benefits of the ABC define that this activity would help the business to resolve the

issue related to the product cost and identify the sales price of the business. Along with that,

it would offer a good base to the management to make better decision about overall related

cost and performance of the business.

On the basis of above calculations, it has been measured that the product cost from

traditional costing system and activity based costing system is different. The reason behind

12

the management to make better decision. This system impacts the choice of the management

in regards to the cost (Silvi, Bartolini & Hines, 2017).

Through breaking down the contextual analysis of Centuria Company, it has been

recognized that the activity based costing framework is agreeable to the organization.

Because of this costing technique, it has been discovered that this method would help the

management to improve the overall performance of the company.

Management accounting factor:

Below are few management accounting factors which must be considered by Centuria

company to make decision about ABC costing method:

Nature:

Nature of the business is one of the important factors to be considered. In case of

Centuria, company owns a production house and it is important for the production house to

make decision on the basis of production cost. Hence, it is important for the company to

adopt ABC costing (Bhimani, Horngren, Datar & Foster, 2009).

Amount:

Identifying the exact cost of the business is exact factor. In case of Centuria, company

owns a production house and it is important for the production house to identify the exact

production cost. Hence, it is important for the company to adopt ABC costing (Marshall,

McManus & Viele, 2011).

Rigidness of employees:

Company is working since last 15 years and using the traditional costing system.

Hence it is important for the business to consider their views.

Benefit, cost and limitations:

Benefits of the ABC define that this activity would help the business to resolve the

issue related to the product cost and identify the sales price of the business. Along with that,

it would offer a good base to the management to make better decision about overall related

cost and performance of the business.

On the basis of above calculations, it has been measured that the product cost from

traditional costing system and activity based costing system is different. The reason behind

Management Accounting

13

difference in the cost is due to the different process and consideration by both the accounting

system (Drury, 2013).

Lastly, the main limitation of the company is its complexity and few errors related to

the process. It sometimes manipulate the management to make wrong decisions.

Conclusion:

Through considering the calculations over company, it has been recognized that

various issues are faced by the company due to backward costing system, If company adopts

the new costing system then it would not only improve the profitability level of the business

but also it would help the business to make better decision for the company’s betterment.

Hence, Centuria company is recommended to make the changes in the costing system

and adopt ABC costing method to improve the overall performance of the company.

13

difference in the cost is due to the different process and consideration by both the accounting

system (Drury, 2013).

Lastly, the main limitation of the company is its complexity and few errors related to

the process. It sometimes manipulate the management to make wrong decisions.

Conclusion:

Through considering the calculations over company, it has been recognized that

various issues are faced by the company due to backward costing system, If company adopts

the new costing system then it would not only improve the profitability level of the business

but also it would help the business to make better decision for the company’s betterment.

Hence, Centuria company is recommended to make the changes in the costing system

and adopt ABC costing method to improve the overall performance of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

14

References:

Bhimani, A., Horngren, C. T., Datar, S. M., & Foster, G. (2009). Management and cost

accounting (Vol. 1). Pearson Education.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Marshall, D. H., McManus, W. W., & Viele, D. F. (2011). Accounting. McGraw-Hill Irwin,.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Silvi, R., Bartolini, M., & Hines, P. (2017). Strategic cost management and lean thinking: A

framework for management accounting.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

14

References:

Bhimani, A., Horngren, C. T., Datar, S. M., & Foster, G. (2009). Management and cost

accounting (Vol. 1). Pearson Education.

DRURY, C. M. (2013). Management and cost accounting. Springer.

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Marshall, D. H., McManus, W. W., & Viele, D. F. (2011). Accounting. McGraw-Hill Irwin,.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Silvi, R., Bartolini, M., & Hines, P. (2017). Strategic cost management and lean thinking: A

framework for management accounting.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.