Management Accounting Project Report: Answers, Schedules, and List of Activities

VerifiedAdded on 2022/10/19

|15

|3715

|233

AI Summary

This project report covers various topics related to management accounting, including answers, schedules, and a list of activities. It includes information on resource cost categories and drivers, activities and resource drivers used in blending, a list of activities and their associated costs, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Management Accounting

1

Project Report: Management Accounting

1

Project Report: Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

2

Contents

Answer 1:..........................................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Answer 2:..........................................................................................................................4

Schedule 3.....................................................................................................................4

Answer 3:..........................................................................................................................4

Schedule 4:....................................................................................................................4

Answer 4:..........................................................................................................................6

Schedule 5:....................................................................................................................6

Schedule 6:....................................................................................................................7

Answer 5:..........................................................................................................................8

Answer 6:..........................................................................................................................8

Answer 7:..........................................................................................................................9

Answer 8 and 9:..............................................................................................................10

Introduction:...............................................................................................................10

Traditional costing system:.........................................................................................10

Deficiencies in traditional costing system:.................................................................11

Activity based costing:...............................................................................................11

Importance of activity based costing system:.............................................................11

Why should ABC adopted:.........................................................................................12

Benefit, cost and limitations of ABC:.........................................................................12

Conclusion......................................................................................................................13

2

Contents

Answer 1:..........................................................................................................................3

Schedule 1.....................................................................................................................3

Schedule 2.....................................................................................................................3

Answer 2:..........................................................................................................................4

Schedule 3.....................................................................................................................4

Answer 3:..........................................................................................................................4

Schedule 4:....................................................................................................................4

Answer 4:..........................................................................................................................6

Schedule 5:....................................................................................................................6

Schedule 6:....................................................................................................................7

Answer 5:..........................................................................................................................8

Answer 6:..........................................................................................................................8

Answer 7:..........................................................................................................................9

Answer 8 and 9:..............................................................................................................10

Introduction:...............................................................................................................10

Traditional costing system:.........................................................................................10

Deficiencies in traditional costing system:.................................................................11

Activity based costing:...............................................................................................11

Importance of activity based costing system:.............................................................11

Why should ABC adopted:.........................................................................................12

Benefit, cost and limitations of ABC:.........................................................................12

Conclusion......................................................................................................................13

Management Accounting

3

References.......................................................................................................................14

3

References.......................................................................................................................14

Management Accounting

4

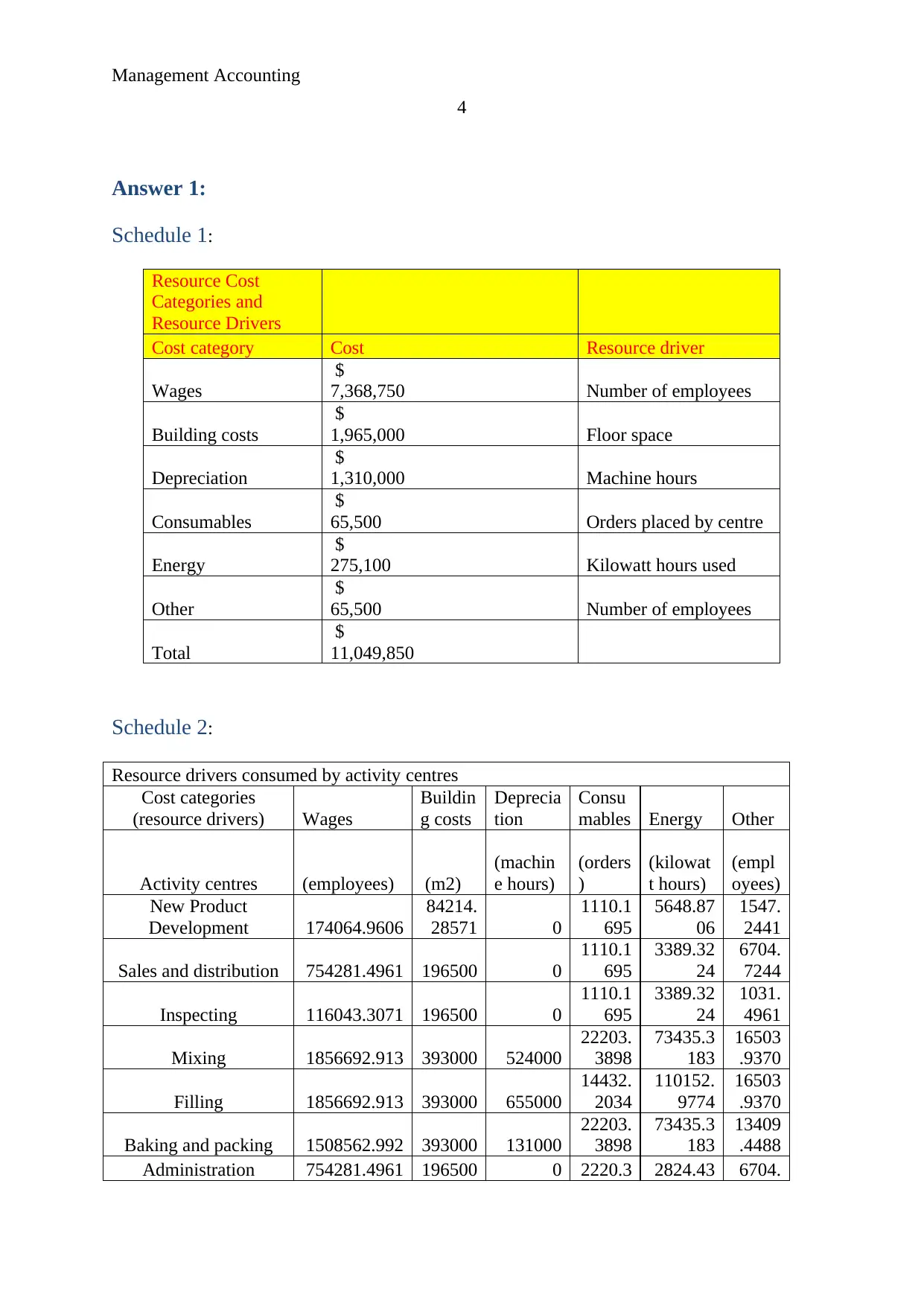

Answer 1:

Schedule 1:

Resource Cost

Categories and

Resource Drivers

Cost category Cost Resource driver

Wages

$

7,368,750 Number of employees

Building costs

$

1,965,000 Floor space

Depreciation

$

1,310,000 Machine hours

Consumables

$

65,500 Orders placed by centre

Energy

$

275,100 Kilowatt hours used

Other

$

65,500 Number of employees

Total

$

11,049,850

Schedule 2:

Resource drivers consumed by activity centres

Cost categories

(resource drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres (employees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product

Development 174064.9606

84214.

28571 0

1110.1

695

5648.87

06

1547.

2441

Sales and distribution 754281.4961 196500 0

1110.1

695

3389.32

24

6704.

7244

Inspecting 116043.3071 196500 0

1110.1

695

3389.32

24

1031.

4961

Mixing 1856692.913 393000 524000

22203.

3898

73435.3

183

16503

.9370

Filling 1856692.913 393000 655000

14432.

2034

110152.

9774

16503

.9370

Baking and packing 1508562.992 393000 131000

22203.

3898

73435.3

183

13409

.4488

Administration 754281.4961 196500 0 2220.3 2824.43 6704.

4

Answer 1:

Schedule 1:

Resource Cost

Categories and

Resource Drivers

Cost category Cost Resource driver

Wages

$

7,368,750 Number of employees

Building costs

$

1,965,000 Floor space

Depreciation

$

1,310,000 Machine hours

Consumables

$

65,500 Orders placed by centre

Energy

$

275,100 Kilowatt hours used

Other

$

65,500 Number of employees

Total

$

11,049,850

Schedule 2:

Resource drivers consumed by activity centres

Cost categories

(resource drivers) Wages

Buildin

g costs

Deprecia

tion

Consu

mables Energy Other

Activity centres (employees) (m2)

(machin

e hours)

(orders

)

(kilowat

t hours)

(empl

oyees)

New Product

Development 174064.9606

84214.

28571 0

1110.1

695

5648.87

06

1547.

2441

Sales and distribution 754281.4961 196500 0

1110.1

695

3389.32

24

6704.

7244

Inspecting 116043.3071 196500 0

1110.1

695

3389.32

24

1031.

4961

Mixing 1856692.913 393000 524000

22203.

3898

73435.3

183

16503

.9370

Filling 1856692.913 393000 655000

14432.

2034

110152.

9774

16503

.9370

Baking and packing 1508562.992 393000 131000

22203.

3898

73435.3

183

13409

.4488

Administration 754281.4961 196500 0 2220.3 2824.43 6704.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

5

390 53 7244

Corporate

management 348129.9213

112285

.7143 0

1110.1

695

2824.43

53

3094.

4882

Total quantity of

resource drivers across

all activity centres 7368750

196500

0 1310000 65500 275100 65500

Answer 2:

Schedule 3:

Activities and resource drivers used - Blending

Activity

Percentage of

labour time

Percentage

of floor

space

Percentage of

machine hours

Energ

y

Consu

mable Other

Stack cases on

baking trays 464173.2283 98250.0000 0 0 0

4125.

98425

Setup ovens 185669.2913 19650.0000 0 0 0

1650.

3937

Move to

ovens 92834.64567 19650.0000 0 0 0

825.1

9685

Bake products 928346.4567 196500.0000 524000

73435.

31828

22203.

38983

8251.

9685

Unload oven 92834.64567 19650.0000 0 0 0

825.1

9685

Move to truck 92834.64567 39300.0000 0 0 0

825.1

9685

Total 1856692.913 393000 524000

73435.

31828

22203.

38983

16503

.937

Answer 3:

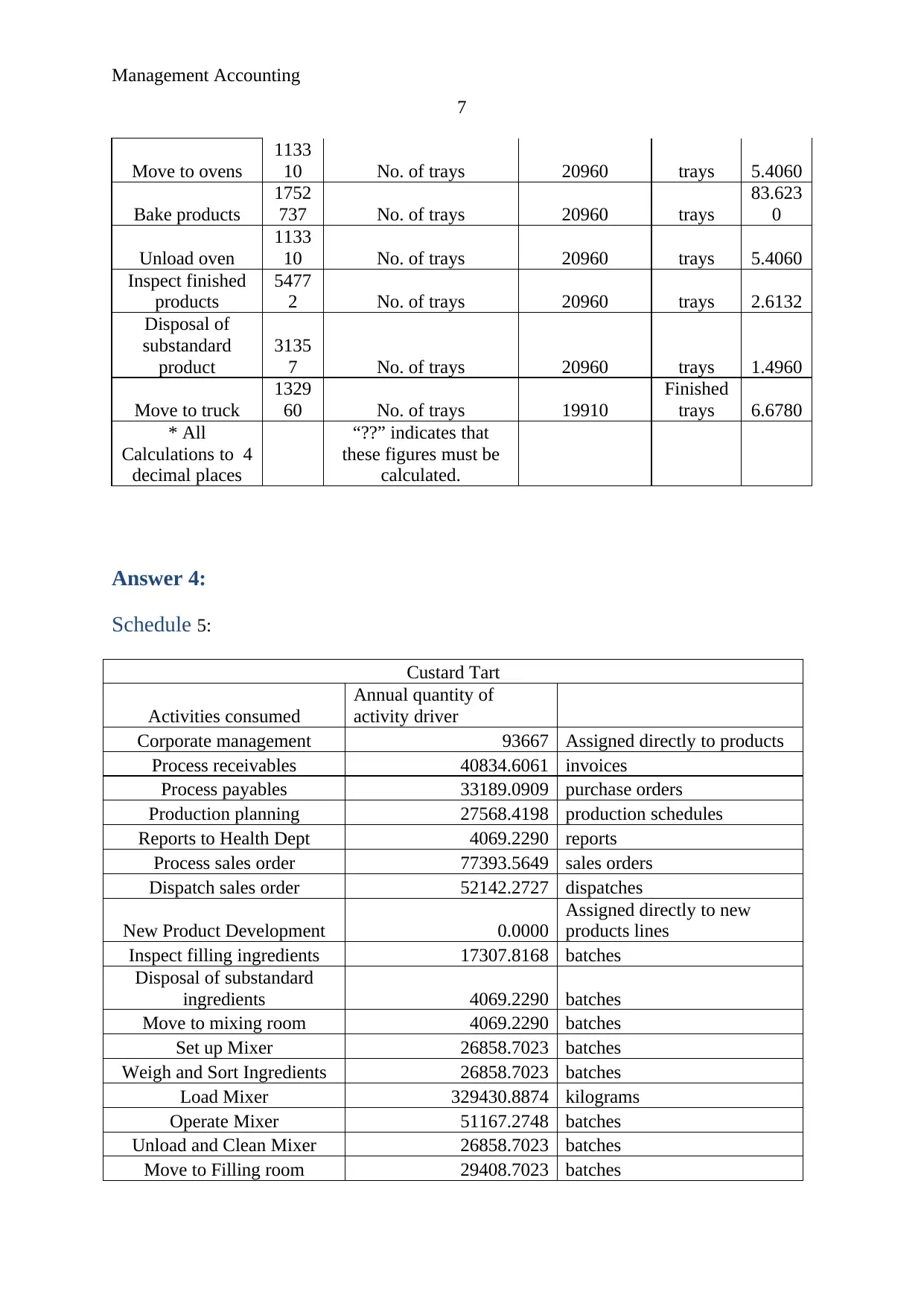

Schedule 4:

List of activities

Activity

Activ

ity

cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

3481

30

Assigned directly to

products

Process

receivables

3850

12 No. of invoices 6600 invoices

58.335

2

5

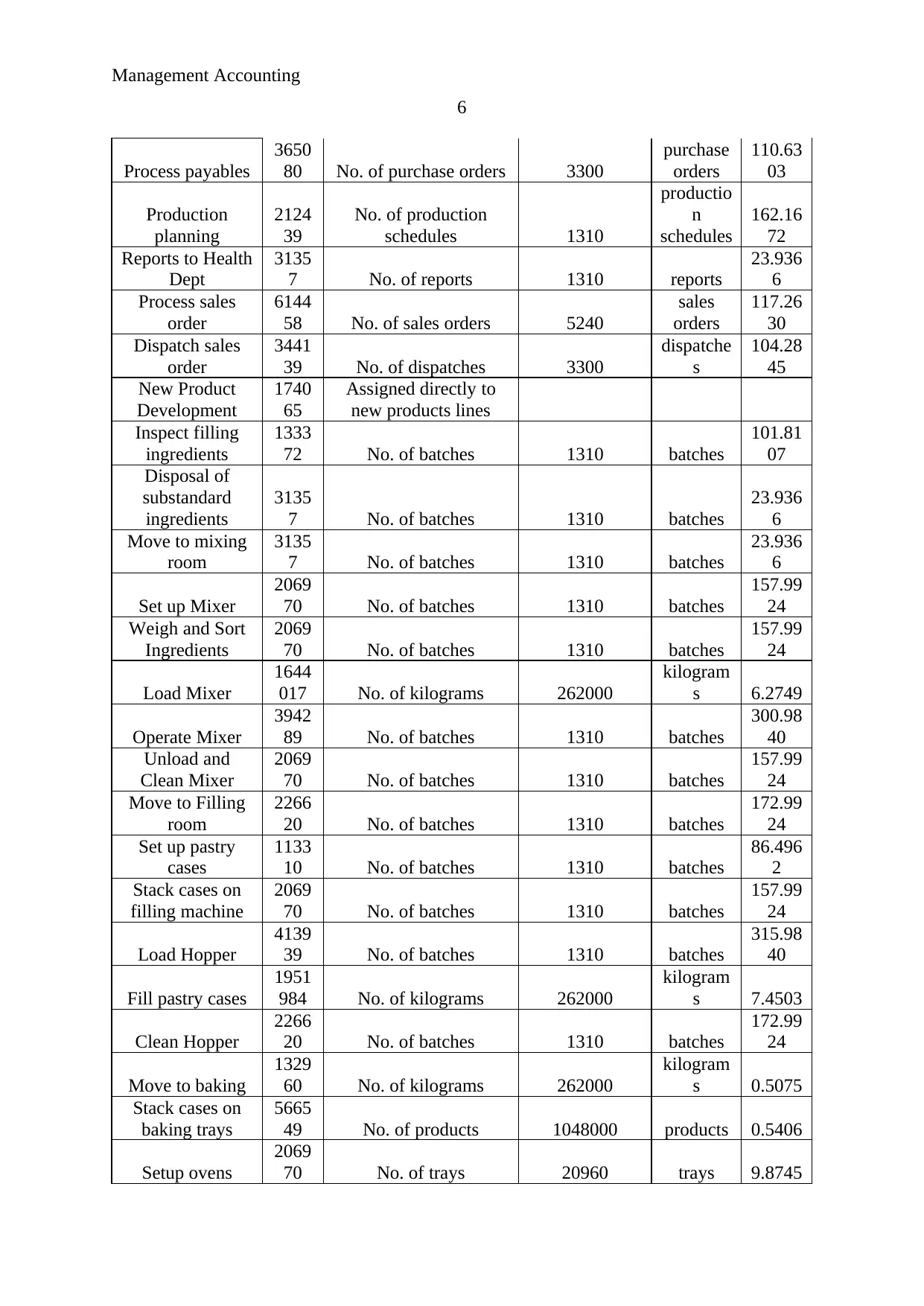

390 53 7244

Corporate

management 348129.9213

112285

.7143 0

1110.1

695

2824.43

53

3094.

4882

Total quantity of

resource drivers across

all activity centres 7368750

196500

0 1310000 65500 275100 65500

Answer 2:

Schedule 3:

Activities and resource drivers used - Blending

Activity

Percentage of

labour time

Percentage

of floor

space

Percentage of

machine hours

Energ

y

Consu

mable Other

Stack cases on

baking trays 464173.2283 98250.0000 0 0 0

4125.

98425

Setup ovens 185669.2913 19650.0000 0 0 0

1650.

3937

Move to

ovens 92834.64567 19650.0000 0 0 0

825.1

9685

Bake products 928346.4567 196500.0000 524000

73435.

31828

22203.

38983

8251.

9685

Unload oven 92834.64567 19650.0000 0 0 0

825.1

9685

Move to truck 92834.64567 39300.0000 0 0 0

825.1

9685

Total 1856692.913 393000 524000

73435.

31828

22203.

38983

16503

.937

Answer 3:

Schedule 4:

List of activities

Activity

Activ

ity

cost Activity driver

Annual

quantity of

activity driver

Cost

per

Driver

Corporate

management

3481

30

Assigned directly to

products

Process

receivables

3850

12 No. of invoices 6600 invoices

58.335

2

Management Accounting

6

Process payables

3650

80 No. of purchase orders 3300

purchase

orders

110.63

03

Production

planning

2124

39

No. of production

schedules 1310

productio

n

schedules

162.16

72

Reports to Health

Dept

3135

7 No. of reports 1310 reports

23.936

6

Process sales

order

6144

58 No. of sales orders 5240

sales

orders

117.26

30

Dispatch sales

order

3441

39 No. of dispatches 3300

dispatche

s

104.28

45

New Product

Development

1740

65

Assigned directly to

new products lines

Inspect filling

ingredients

1333

72 No. of batches 1310 batches

101.81

07

Disposal of

substandard

ingredients

3135

7 No. of batches 1310 batches

23.936

6

Move to mixing

room

3135

7 No. of batches 1310 batches

23.936

6

Set up Mixer

2069

70 No. of batches 1310 batches

157.99

24

Weigh and Sort

Ingredients

2069

70 No. of batches 1310 batches

157.99

24

Load Mixer

1644

017 No. of kilograms 262000

kilogram

s 6.2749

Operate Mixer

3942

89 No. of batches 1310 batches

300.98

40

Unload and

Clean Mixer

2069

70 No. of batches 1310 batches

157.99

24

Move to Filling

room

2266

20 No. of batches 1310 batches

172.99

24

Set up pastry

cases

1133

10 No. of batches 1310 batches

86.496

2

Stack cases on

filling machine

2069

70 No. of batches 1310 batches

157.99

24

Load Hopper

4139

39 No. of batches 1310 batches

315.98

40

Fill pastry cases

1951

984 No. of kilograms 262000

kilogram

s 7.4503

Clean Hopper

2266

20 No. of batches 1310 batches

172.99

24

Move to baking

1329

60 No. of kilograms 262000

kilogram

s 0.5075

Stack cases on

baking trays

5665

49 No. of products 1048000 products 0.5406

Setup ovens

2069

70 No. of trays 20960 trays 9.8745

6

Process payables

3650

80 No. of purchase orders 3300

purchase

orders

110.63

03

Production

planning

2124

39

No. of production

schedules 1310

productio

n

schedules

162.16

72

Reports to Health

Dept

3135

7 No. of reports 1310 reports

23.936

6

Process sales

order

6144

58 No. of sales orders 5240

sales

orders

117.26

30

Dispatch sales

order

3441

39 No. of dispatches 3300

dispatche

s

104.28

45

New Product

Development

1740

65

Assigned directly to

new products lines

Inspect filling

ingredients

1333

72 No. of batches 1310 batches

101.81

07

Disposal of

substandard

ingredients

3135

7 No. of batches 1310 batches

23.936

6

Move to mixing

room

3135

7 No. of batches 1310 batches

23.936

6

Set up Mixer

2069

70 No. of batches 1310 batches

157.99

24

Weigh and Sort

Ingredients

2069

70 No. of batches 1310 batches

157.99

24

Load Mixer

1644

017 No. of kilograms 262000

kilogram

s 6.2749

Operate Mixer

3942

89 No. of batches 1310 batches

300.98

40

Unload and

Clean Mixer

2069

70 No. of batches 1310 batches

157.99

24

Move to Filling

room

2266

20 No. of batches 1310 batches

172.99

24

Set up pastry

cases

1133

10 No. of batches 1310 batches

86.496

2

Stack cases on

filling machine

2069

70 No. of batches 1310 batches

157.99

24

Load Hopper

4139

39 No. of batches 1310 batches

315.98

40

Fill pastry cases

1951

984 No. of kilograms 262000

kilogram

s 7.4503

Clean Hopper

2266

20 No. of batches 1310 batches

172.99

24

Move to baking

1329

60 No. of kilograms 262000

kilogram

s 0.5075

Stack cases on

baking trays

5665

49 No. of products 1048000 products 0.5406

Setup ovens

2069

70 No. of trays 20960 trays 9.8745

Management Accounting

7

Move to ovens

1133

10 No. of trays 20960 trays 5.4060

Bake products

1752

737 No. of trays 20960 trays

83.623

0

Unload oven

1133

10 No. of trays 20960 trays 5.4060

Inspect finished

products

5477

2 No. of trays 20960 trays 2.6132

Disposal of

substandard

product

3135

7 No. of trays 20960 trays 1.4960

Move to truck

1329

60 No. of trays 19910

Finished

trays 6.6780

* All

Calculations to 4

decimal places

“??” indicates that

these figures must be

calculated.

Answer 4:

Schedule 5:

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 93667 Assigned directly to products

Process receivables 40834.6061 invoices

Process payables 33189.0909 purchase orders

Production planning 27568.4198 production schedules

Reports to Health Dept 4069.2290 reports

Process sales order 77393.5649 sales orders

Dispatch sales order 52142.2727 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 17307.8168 batches

Disposal of substandard

ingredients 4069.2290 batches

Move to mixing room 4069.2290 batches

Set up Mixer 26858.7023 batches

Weigh and Sort Ingredients 26858.7023 batches

Load Mixer 329430.8874 kilograms

Operate Mixer 51167.2748 batches

Unload and Clean Mixer 26858.7023 batches

Move to Filling room 29408.7023 batches

7

Move to ovens

1133

10 No. of trays 20960 trays 5.4060

Bake products

1752

737 No. of trays 20960 trays

83.623

0

Unload oven

1133

10 No. of trays 20960 trays 5.4060

Inspect finished

products

5477

2 No. of trays 20960 trays 2.6132

Disposal of

substandard

product

3135

7 No. of trays 20960 trays 1.4960

Move to truck

1329

60 No. of trays 19910

Finished

trays 6.6780

* All

Calculations to 4

decimal places

“??” indicates that

these figures must be

calculated.

Answer 4:

Schedule 5:

Custard Tart

Activities consumed

Annual quantity of

activity driver

Corporate management 93667 Assigned directly to products

Process receivables 40834.6061 invoices

Process payables 33189.0909 purchase orders

Production planning 27568.4198 production schedules

Reports to Health Dept 4069.2290 reports

Process sales order 77393.5649 sales orders

Dispatch sales order 52142.2727 dispatches

New Product Development 0.0000

Assigned directly to new

products lines

Inspect filling ingredients 17307.8168 batches

Disposal of substandard

ingredients 4069.2290 batches

Move to mixing room 4069.2290 batches

Set up Mixer 26858.7023 batches

Weigh and Sort Ingredients 26858.7023 batches

Load Mixer 329430.8874 kilograms

Operate Mixer 51167.2748 batches

Unload and Clean Mixer 26858.7023 batches

Move to Filling room 29408.7023 batches

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

8

Set up pastry cases 14704.3511 batches

Stack cases on filling

machine 26858.7023 batches

Load Hopper 53717.2748 batches

Fill pastry cases 391141.8321 kilograms

Clean Hopper 29408.7023 batches

Move to baking 26642.7481 kilograms

Stack cases on baking trays 113309.8425 products

Setup ovens 20736.4665 trays

Move to ovens 11352.6083 trays

Bake products 175608.2051 trays

Unload oven 11352.6083 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 14023.8910 Finished trays

Direct Materials 3

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 1300

Annual Volume 210000

* All Calculations to 4

decimal places

Total Indirect Cost 1733750.662

Per Unit Indirect cost 8.2560

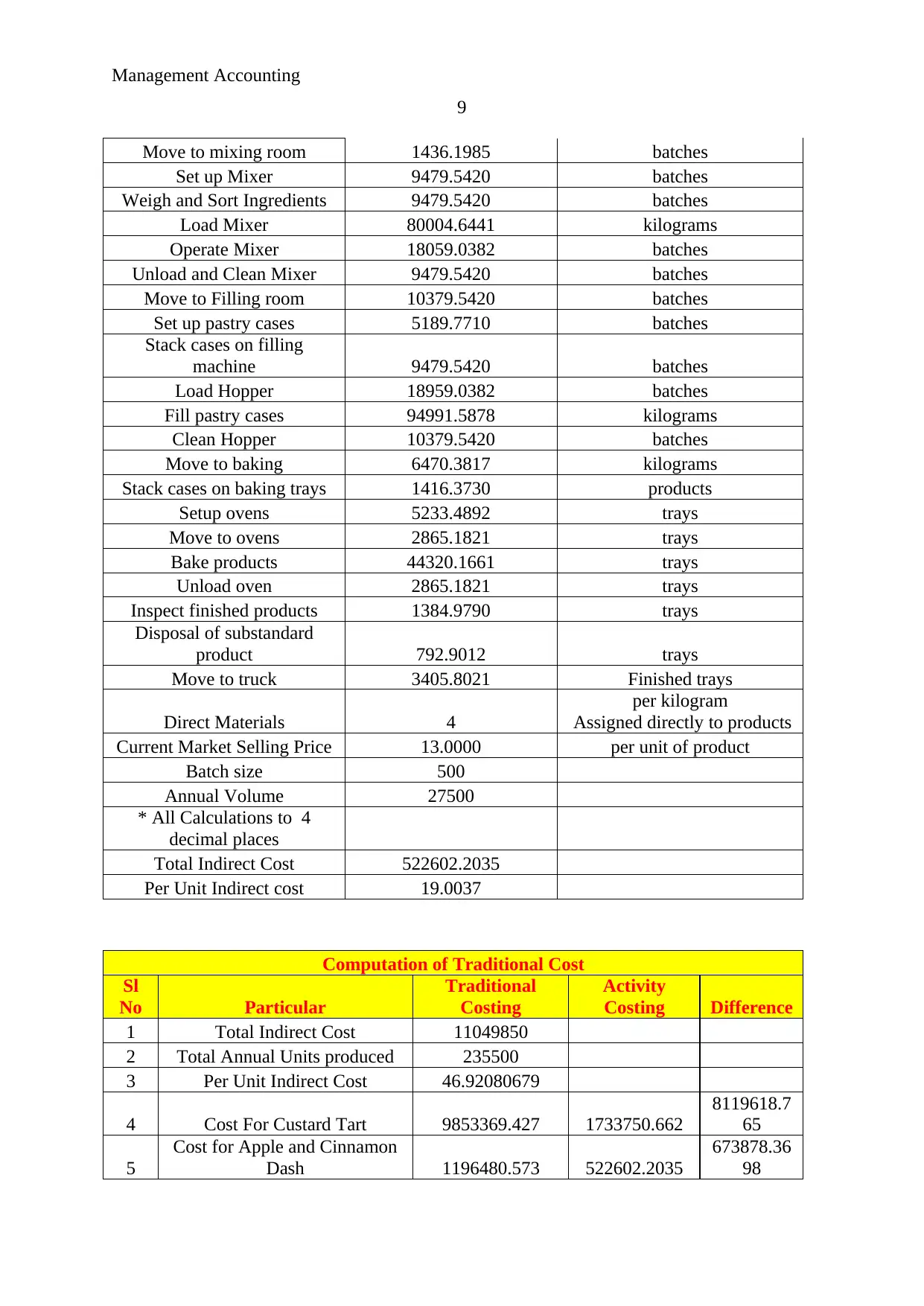

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 11374 Assigned directly to products

Process receivables 11667.0303 invoices

Process payables 11063.0303 purchase orders

Production planning 11351.7023 production schedules

Reports to Health Dept 1675.5649 reports

Process sales order 23452.5954 sales orders

Dispatch sales order 10428.4545 dispatches

New Product Development 87973.0000

Assigned directly to new

products lines

Inspect filling ingredients 6108.6412 batches

Disposal of substandard

ingredients 1436.1985 batches

8

Set up pastry cases 14704.3511 batches

Stack cases on filling

machine 26858.7023 batches

Load Hopper 53717.2748 batches

Fill pastry cases 391141.8321 kilograms

Clean Hopper 29408.7023 batches

Move to baking 26642.7481 kilograms

Stack cases on baking trays 113309.8425 products

Setup ovens 20736.4665 trays

Move to ovens 11352.6083 trays

Bake products 175608.2051 trays

Unload oven 11352.6083 trays

Inspect finished products 0.0000 trays

Disposal of substandard

product 0.0000 trays

Move to truck 14023.8910 Finished trays

Direct Materials 3

per kilogram

Assigned directly to products

Current Market Selling Price 9 per unit of product

Batch size 1300

Annual Volume 210000

* All Calculations to 4

decimal places

Total Indirect Cost 1733750.662

Per Unit Indirect cost 8.2560

Schedule 6:

Apple and Cinnamon Danish

Activities consumed

Annual quantity of

activity driver

Corporate management 11374 Assigned directly to products

Process receivables 11667.0303 invoices

Process payables 11063.0303 purchase orders

Production planning 11351.7023 production schedules

Reports to Health Dept 1675.5649 reports

Process sales order 23452.5954 sales orders

Dispatch sales order 10428.4545 dispatches

New Product Development 87973.0000

Assigned directly to new

products lines

Inspect filling ingredients 6108.6412 batches

Disposal of substandard

ingredients 1436.1985 batches

Management Accounting

9

Move to mixing room 1436.1985 batches

Set up Mixer 9479.5420 batches

Weigh and Sort Ingredients 9479.5420 batches

Load Mixer 80004.6441 kilograms

Operate Mixer 18059.0382 batches

Unload and Clean Mixer 9479.5420 batches

Move to Filling room 10379.5420 batches

Set up pastry cases 5189.7710 batches

Stack cases on filling

machine 9479.5420 batches

Load Hopper 18959.0382 batches

Fill pastry cases 94991.5878 kilograms

Clean Hopper 10379.5420 batches

Move to baking 6470.3817 kilograms

Stack cases on baking trays 1416.3730 products

Setup ovens 5233.4892 trays

Move to ovens 2865.1821 trays

Bake products 44320.1661 trays

Unload oven 2865.1821 trays

Inspect finished products 1384.9790 trays

Disposal of substandard

product 792.9012 trays

Move to truck 3405.8021 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 522602.2035

Per Unit Indirect cost 19.0037

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 11049850

2 Total Annual Units produced 235500

3 Per Unit Indirect Cost 46.92080679

4 Cost For Custard Tart 9853369.427 1733750.662

8119618.7

65

5

Cost for Apple and Cinnamon

Dash 1196480.573 522602.2035

673878.36

98

9

Move to mixing room 1436.1985 batches

Set up Mixer 9479.5420 batches

Weigh and Sort Ingredients 9479.5420 batches

Load Mixer 80004.6441 kilograms

Operate Mixer 18059.0382 batches

Unload and Clean Mixer 9479.5420 batches

Move to Filling room 10379.5420 batches

Set up pastry cases 5189.7710 batches

Stack cases on filling

machine 9479.5420 batches

Load Hopper 18959.0382 batches

Fill pastry cases 94991.5878 kilograms

Clean Hopper 10379.5420 batches

Move to baking 6470.3817 kilograms

Stack cases on baking trays 1416.3730 products

Setup ovens 5233.4892 trays

Move to ovens 2865.1821 trays

Bake products 44320.1661 trays

Unload oven 2865.1821 trays

Inspect finished products 1384.9790 trays

Disposal of substandard

product 792.9012 trays

Move to truck 3405.8021 Finished trays

Direct Materials 4

per kilogram

Assigned directly to products

Current Market Selling Price 13.0000 per unit of product

Batch size 500

Annual Volume 27500

* All Calculations to 4

decimal places

Total Indirect Cost 522602.2035

Per Unit Indirect cost 19.0037

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 11049850

2 Total Annual Units produced 235500

3 Per Unit Indirect Cost 46.92080679

4 Cost For Custard Tart 9853369.427 1733750.662

8119618.7

65

5

Cost for Apple and Cinnamon

Dash 1196480.573 522602.2035

673878.36

98

Management Accounting

10

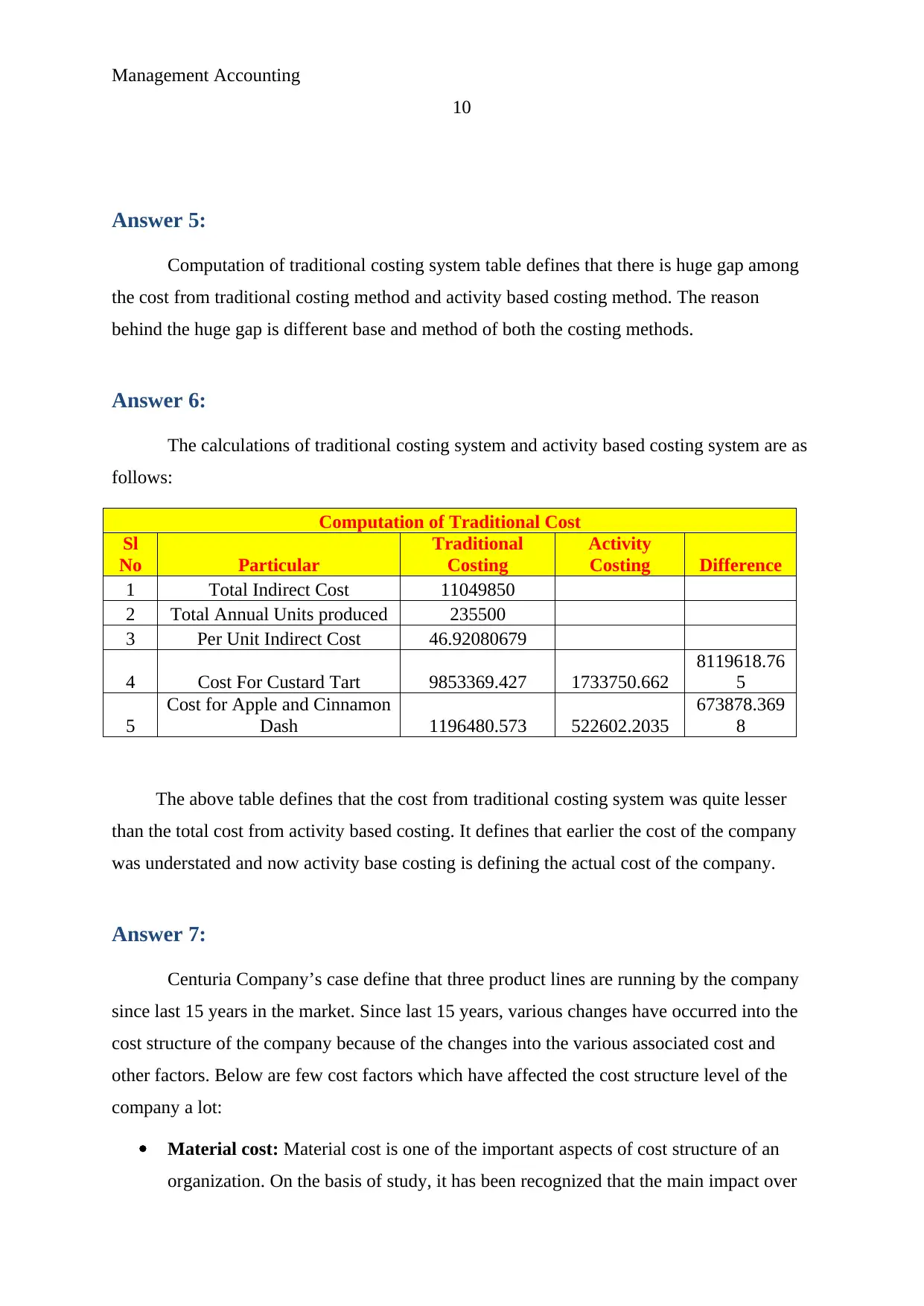

Answer 5:

Computation of traditional costing system table defines that there is huge gap among

the cost from traditional costing method and activity based costing method. The reason

behind the huge gap is different base and method of both the costing methods.

Answer 6:

The calculations of traditional costing system and activity based costing system are as

follows:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 11049850

2 Total Annual Units produced 235500

3 Per Unit Indirect Cost 46.92080679

4 Cost For Custard Tart 9853369.427 1733750.662

8119618.76

5

5

Cost for Apple and Cinnamon

Dash 1196480.573 522602.2035

673878.369

8

The above table defines that the cost from traditional costing system was quite lesser

than the total cost from activity based costing. It defines that earlier the cost of the company

was understated and now activity base costing is defining the actual cost of the company.

Answer 7:

Centuria Company’s case define that three product lines are running by the company

since last 15 years in the market. Since last 15 years, various changes have occurred into the

cost structure of the company because of the changes into the various associated cost and

other factors. Below are few cost factors which have affected the cost structure level of the

company a lot:

Material cost: Material cost is one of the important aspects of cost structure of an

organization. On the basis of study, it has been recognized that the main impact over

10

Answer 5:

Computation of traditional costing system table defines that there is huge gap among

the cost from traditional costing method and activity based costing method. The reason

behind the huge gap is different base and method of both the costing methods.

Answer 6:

The calculations of traditional costing system and activity based costing system are as

follows:

Computation of Traditional Cost

Sl

No Particular

Traditional

Costing

Activity

Costing Difference

1 Total Indirect Cost 11049850

2 Total Annual Units produced 235500

3 Per Unit Indirect Cost 46.92080679

4 Cost For Custard Tart 9853369.427 1733750.662

8119618.76

5

5

Cost for Apple and Cinnamon

Dash 1196480.573 522602.2035

673878.369

8

The above table defines that the cost from traditional costing system was quite lesser

than the total cost from activity based costing. It defines that earlier the cost of the company

was understated and now activity base costing is defining the actual cost of the company.

Answer 7:

Centuria Company’s case define that three product lines are running by the company

since last 15 years in the market. Since last 15 years, various changes have occurred into the

cost structure of the company because of the changes into the various associated cost and

other factors. Below are few cost factors which have affected the cost structure level of the

company a lot:

Material cost: Material cost is one of the important aspects of cost structure of an

organization. On the basis of study, it has been recognized that the main impact over

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management Accounting

11

the cost structure of an organization is material cost. Hence, changes into material

cost have affected cost structure level at a great extent.

Labour cost: Labour cost is one of the highest and used aspects of cost structure of

an organization. On the basis of study, it has been recognized that the labour cost has

improved a lot in the market from last 15 years (Bhimani, Horngren, Datar & Foster,

2018). Hence, changes into labour cost have affected cost structure level at a great

extent.

High fixed cost: Further the study defines that along with the changes into the

process and machineries, the fixed cost level of the company get also change. On the

basis of study, it has been recognized that the high cost level have affected the

performance of the company at great extent. Hence, changes into fixed cost have

affected cost structure level at a great extent.

Inflation rate: Lastly, inflation rate is the main aspect which affects the cost level of

the business. On the basis of study, it has been recognized that the main impact over

the cost structure of an organization is inflation rate. Hence, changes into inflation

rate have affected cost structure level at a great extent.

Answer 8 and 9:

Introduction:

Costing system is a technique which is used in manufacturing and other organizations

to gather the data and identify the total cost associated with the total production level of the

business. Mainly there are 2 ways to calculate the same: activity based costing and traditional

costing system. Traditional costing system is the oldest technique to calculate the production

cost. Activity based costing is the refined version of traditional costing in which each cost is

allocated on different basis to production department.

In the case, Centuria Company is a manufacturing company and it is manufacturing 3

different products since last 15 years in the market. The company was following the

traditional costing system but now it has been found that there is huge difference between the

costs from traditional costing system in activity based costing. Hence, the company is looking

forward the make the changes in costing system of the company.

11

the cost structure of an organization is material cost. Hence, changes into material

cost have affected cost structure level at a great extent.

Labour cost: Labour cost is one of the highest and used aspects of cost structure of

an organization. On the basis of study, it has been recognized that the labour cost has

improved a lot in the market from last 15 years (Bhimani, Horngren, Datar & Foster,

2018). Hence, changes into labour cost have affected cost structure level at a great

extent.

High fixed cost: Further the study defines that along with the changes into the

process and machineries, the fixed cost level of the company get also change. On the

basis of study, it has been recognized that the high cost level have affected the

performance of the company at great extent. Hence, changes into fixed cost have

affected cost structure level at a great extent.

Inflation rate: Lastly, inflation rate is the main aspect which affects the cost level of

the business. On the basis of study, it has been recognized that the main impact over

the cost structure of an organization is inflation rate. Hence, changes into inflation

rate have affected cost structure level at a great extent.

Answer 8 and 9:

Introduction:

Costing system is a technique which is used in manufacturing and other organizations

to gather the data and identify the total cost associated with the total production level of the

business. Mainly there are 2 ways to calculate the same: activity based costing and traditional

costing system. Traditional costing system is the oldest technique to calculate the production

cost. Activity based costing is the refined version of traditional costing in which each cost is

allocated on different basis to production department.

In the case, Centuria Company is a manufacturing company and it is manufacturing 3

different products since last 15 years in the market. The company was following the

traditional costing system but now it has been found that there is huge difference between the

costs from traditional costing system in activity based costing. Hence, the company is looking

forward the make the changes in costing system of the company.

Management Accounting

12

Traditional costing system:

Traditional costing method is the oldest and most used cost accounting method. In this

method, all the cost related to the production and services are allocated to the production

house on the basis of one base only. Only one base is used in this accounting method to

allocate the cost of the company. This method mainly talks that whatever cost has incurred in

the company during the production process is ultimately been recovered by the final products

of the company equally (Hansen, Mowen and Madison, 2010). This strategy is useful to only

those organizations which are producing single product and doesn’t involved in much non

operating expenses. In case of more than 1 product production, it becomes difficult for the

organization to make decision that ho much cost is involved in producing 1 product line.

Deficiencies in traditional costing system:

There are various deficiencies involved with the traditional costing system. Most

importantly, in this system all the cost related to the production and services are allocated to

the production house on the basis of one base only. Because of it, it becomes difficult for the

organization to make decision that ho much cost is involved in producing 1 product line.

Further, it also influences the management of the company to make wrong decisions on the

basis of wrong data calculated (Horngren, 2009).

In case of Centuria company, traditional costing system is used by the company from

last 15 years but the calculations explains that the cost calculated by the company through

traditional costing system in underrated which has affected over the financial statement and

decisions of the management.

Activity based costing:

Activity based costing method is refined version of cost accounting method. In this

method, all the cost related to the production and services are allocated to the production

house on the basis of cost centre. Each expenses or cost is allocated in this accounting

method on the basis of the allocated centre to allocate the cost of the company. This method

mainly talks that each cost which has incurred in the company during the production process

is different and hence the treatment of each of the cost must be done accordingly (Horngren,

2009). This strategy is useful to each manufacturing organizations which are producing

12

Traditional costing system:

Traditional costing method is the oldest and most used cost accounting method. In this

method, all the cost related to the production and services are allocated to the production

house on the basis of one base only. Only one base is used in this accounting method to

allocate the cost of the company. This method mainly talks that whatever cost has incurred in

the company during the production process is ultimately been recovered by the final products

of the company equally (Hansen, Mowen and Madison, 2010). This strategy is useful to only

those organizations which are producing single product and doesn’t involved in much non

operating expenses. In case of more than 1 product production, it becomes difficult for the

organization to make decision that ho much cost is involved in producing 1 product line.

Deficiencies in traditional costing system:

There are various deficiencies involved with the traditional costing system. Most

importantly, in this system all the cost related to the production and services are allocated to

the production house on the basis of one base only. Because of it, it becomes difficult for the

organization to make decision that ho much cost is involved in producing 1 product line.

Further, it also influences the management of the company to make wrong decisions on the

basis of wrong data calculated (Horngren, 2009).

In case of Centuria company, traditional costing system is used by the company from

last 15 years but the calculations explains that the cost calculated by the company through

traditional costing system in underrated which has affected over the financial statement and

decisions of the management.

Activity based costing:

Activity based costing method is refined version of cost accounting method. In this

method, all the cost related to the production and services are allocated to the production

house on the basis of cost centre. Each expenses or cost is allocated in this accounting

method on the basis of the allocated centre to allocate the cost of the company. This method

mainly talks that each cost which has incurred in the company during the production process

is different and hence the treatment of each of the cost must be done accordingly (Horngren,

2009). This strategy is useful to each manufacturing organizations which are producing

Management Accounting

13

products. This strategy helps the management to make decision and improve the performance

of the company.

Importance of activity based costing system:

There are various deficiencies involved with the activity based costing system. Most

importantly, in this system all the cost related to the production and services are allocated to

the production house on the basis of cost centre which makes it difficult for the management

to identify that which cost is related to which cost centre. Because of it, it is a complex

process. Further, it also impact over the profitability level of the company.

In case of Centuria company, traditional costing system is used by the company from

last 15 years but because of wrong calculations and wrong production cost, it is

recommended to the company to switch to activity based costing in order to make better

decision and improve the overall performance of the company.

Why should ABC adopted:

There are various factors which must be determined by the company before making

any decision about the adoption of activity based costing. Few of them are as follows:

The study defines that the total production cost of the company is understated. Hence,

in order to identify and collect the correct information and production cost, it is

important for the business to switch to activity based costing.

Activity based costing makes sure that the relevant cost is allocated to relevant

department so that it becomes easier for the management to decide better sales price

and improve the performance of the company (Silvi, Bartolini and Hines, 2012).

Activity based costing would help the business to set the competitive prices n the

market.

Activity based costing would also make sure that the overall production process and

profitability level of the business could be improved in the market.

Benefit, cost and limitations of ABC:

Benefits: Main benefits of ABC are as follows:

It would help the management to identify the actual production cost.

13

products. This strategy helps the management to make decision and improve the performance

of the company.

Importance of activity based costing system:

There are various deficiencies involved with the activity based costing system. Most

importantly, in this system all the cost related to the production and services are allocated to

the production house on the basis of cost centre which makes it difficult for the management

to identify that which cost is related to which cost centre. Because of it, it is a complex

process. Further, it also impact over the profitability level of the company.

In case of Centuria company, traditional costing system is used by the company from

last 15 years but because of wrong calculations and wrong production cost, it is

recommended to the company to switch to activity based costing in order to make better

decision and improve the overall performance of the company.

Why should ABC adopted:

There are various factors which must be determined by the company before making

any decision about the adoption of activity based costing. Few of them are as follows:

The study defines that the total production cost of the company is understated. Hence,

in order to identify and collect the correct information and production cost, it is

important for the business to switch to activity based costing.

Activity based costing makes sure that the relevant cost is allocated to relevant

department so that it becomes easier for the management to decide better sales price

and improve the performance of the company (Silvi, Bartolini and Hines, 2012).

Activity based costing would help the business to set the competitive prices n the

market.

Activity based costing would also make sure that the overall production process and

profitability level of the business could be improved in the market.

Benefit, cost and limitations of ABC:

Benefits: Main benefits of ABC are as follows:

It would help the management to identify the actual production cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting

14

ABC would improve the profitability and performance level of the company.

It would improve the decision making process of the business.

Activity based costing would help the business to set the competitive prices n the

market (Rasiah, 2011).

Cost: Computation of traditional costing system table defines that there is huge gap among

the cost from traditional costing method and activity based costing method. The reason

behind the huge gap is different base and method of both the costing methods. In order to

identify the perfect cost of the production, ABC must be adopted by the company.

Limitations: Limitations of ABC are as follows:

Few errors are associated with the ABC method.

It is bit complex.

manipulated the decision of management

It might impact negatively on the performance of the company (Rasiah, 2011).

Conclusion:

Centuria company is following traditional costing system from last 15 years but the

calculations explains that the cost calculated by the company through traditional costing

system in underrated which has affected over the financial statement and decisions of the

management. To recommend, the company should switch to activity based costing in order to

make better decision and improve the overall performance of the company.

14

ABC would improve the profitability and performance level of the company.

It would improve the decision making process of the business.

Activity based costing would help the business to set the competitive prices n the

market (Rasiah, 2011).

Cost: Computation of traditional costing system table defines that there is huge gap among

the cost from traditional costing method and activity based costing method. The reason

behind the huge gap is different base and method of both the costing methods. In order to

identify the perfect cost of the production, ABC must be adopted by the company.

Limitations: Limitations of ABC are as follows:

Few errors are associated with the ABC method.

It is bit complex.

manipulated the decision of management

It might impact negatively on the performance of the company (Rasiah, 2011).

Conclusion:

Centuria company is following traditional costing system from last 15 years but the

calculations explains that the cost calculated by the company through traditional costing

system in underrated which has affected over the financial statement and decisions of the

management. To recommend, the company should switch to activity based costing in order to

make better decision and improve the overall performance of the company.

Management Accounting

15

References:

Bhimani, A., Horngren, C. T., Datar, S. M., and Foster, G. (2018). Management and cost

accounting (Vol. 1). Pearson Education.

Hansen, D. R., Mowen, M. M., and Madison, T. (2010). Cornerstones of cost

accounting. Issues in Accounting Education, 25(4), 790-791.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Silvi, R., Bartolini, M., and Hines, P. (2012). Strategic cost management and lean thinking: A

framework for management accounting.

15

References:

Bhimani, A., Horngren, C. T., Datar, S. M., and Foster, G. (2018). Management and cost

accounting (Vol. 1). Pearson Education.

Hansen, D. R., Mowen, M. M., and Madison, T. (2010). Cornerstones of cost

accounting. Issues in Accounting Education, 25(4), 790-791.

Horngren, C. T. (2009). Cost accounting: A managerial emphasis, 13/e. Pearson Education

India.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Silvi, R., Bartolini, M., and Hines, P. (2012). Strategic cost management and lean thinking: A

framework for management accounting.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.