Examination of Partnership Taxation and Fringe Benefit Tax (FBT) Law

VerifiedAdded on 2023/04/25

|11

|2214

|288

Report

AI Summary

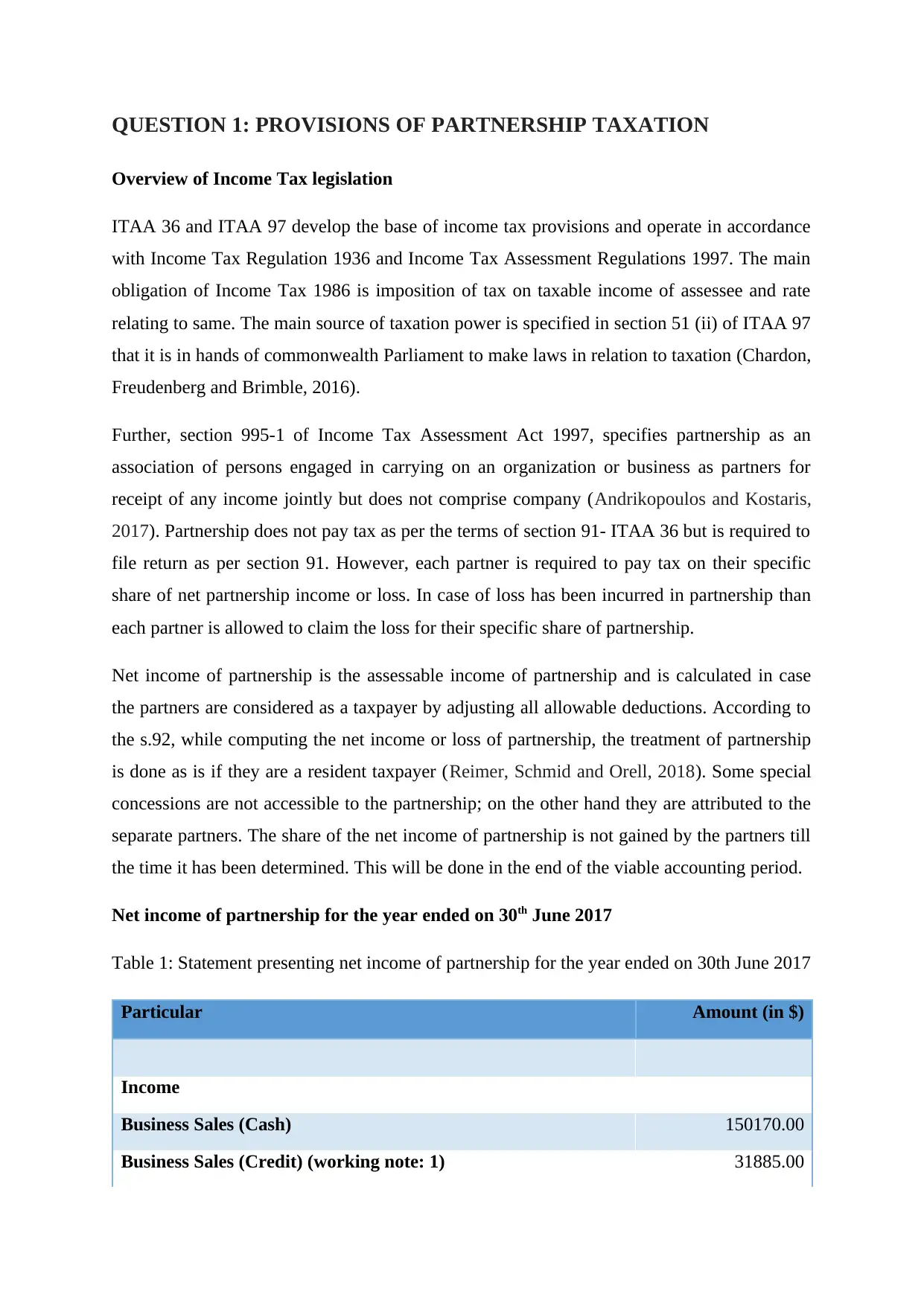

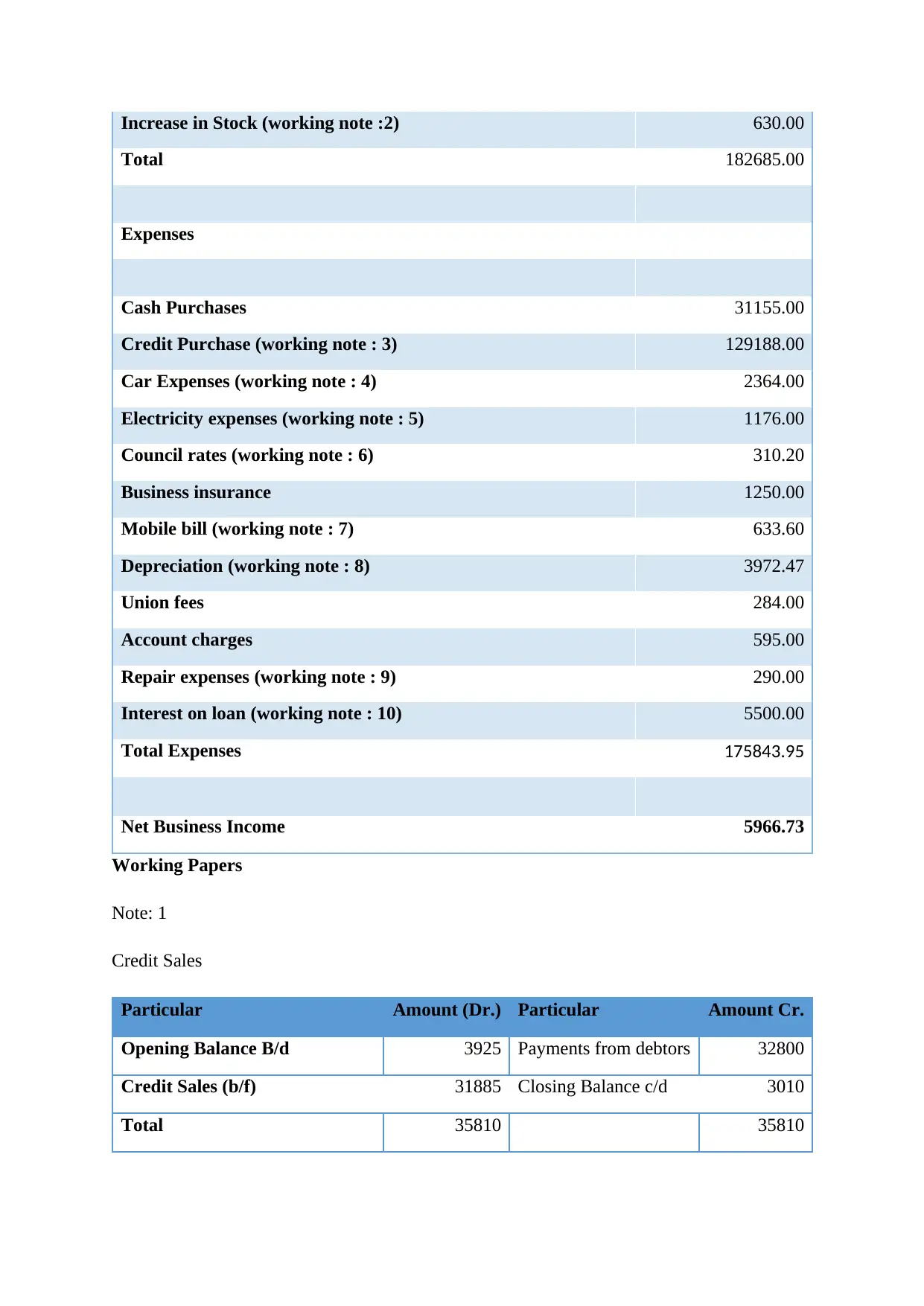

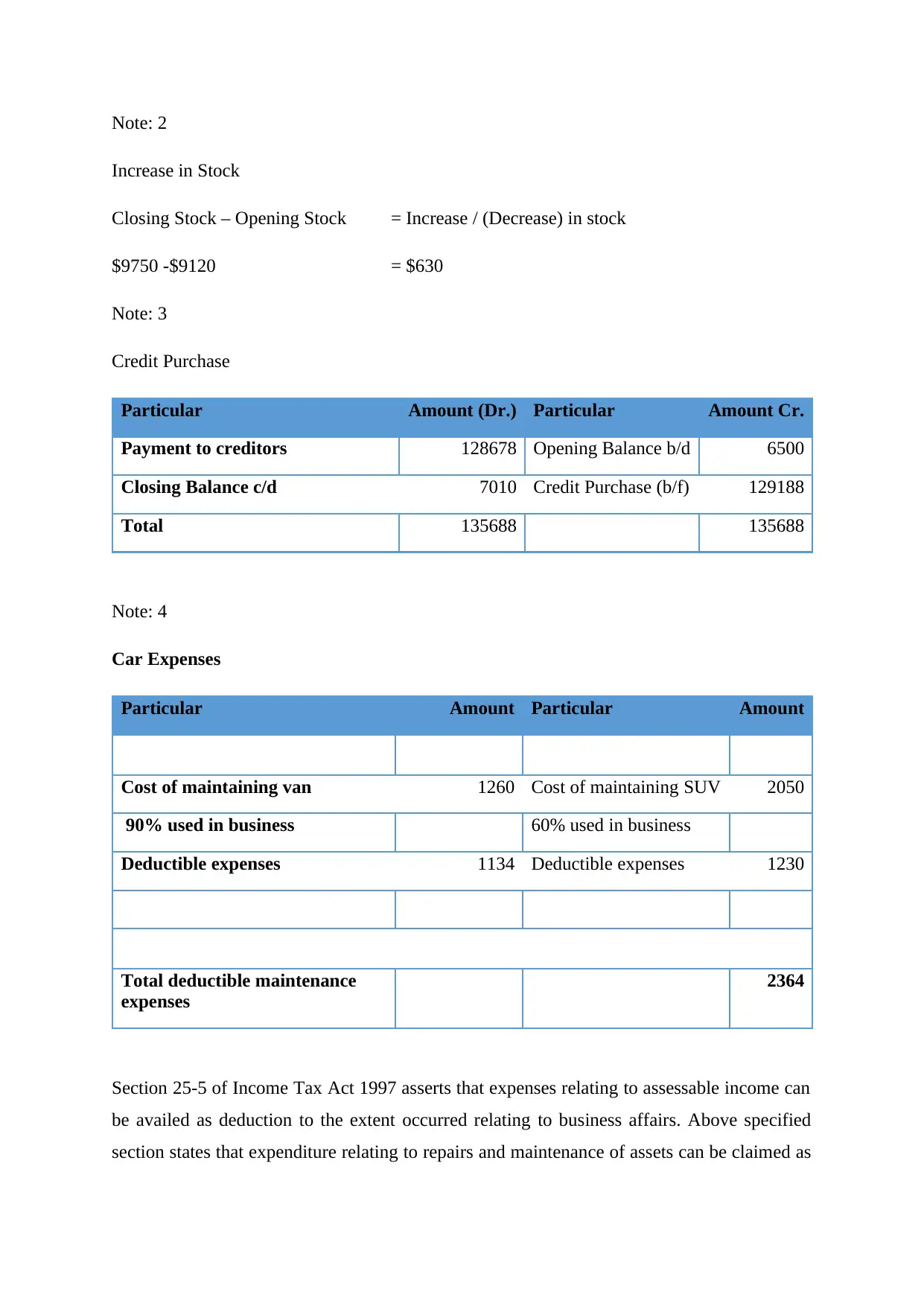

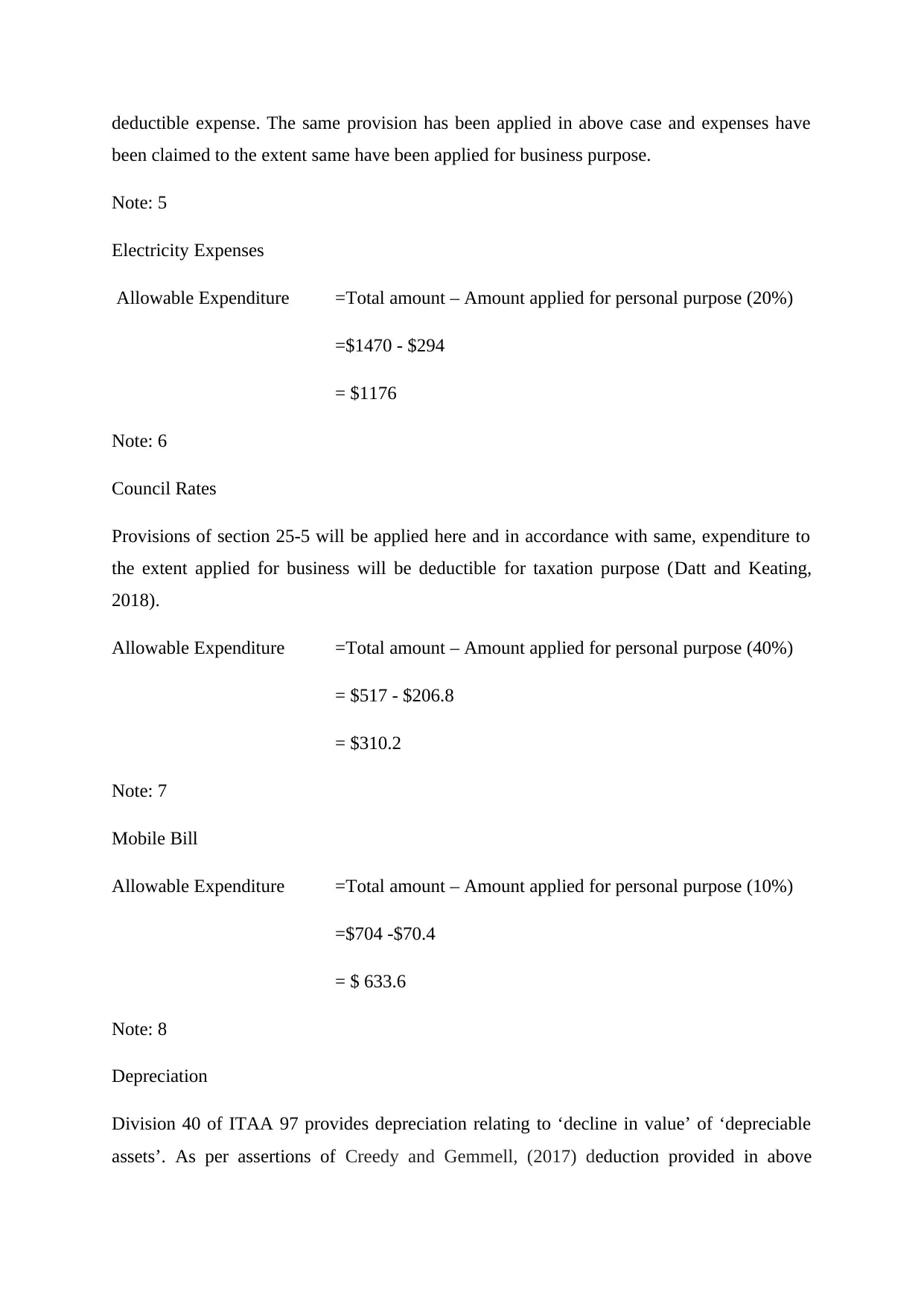

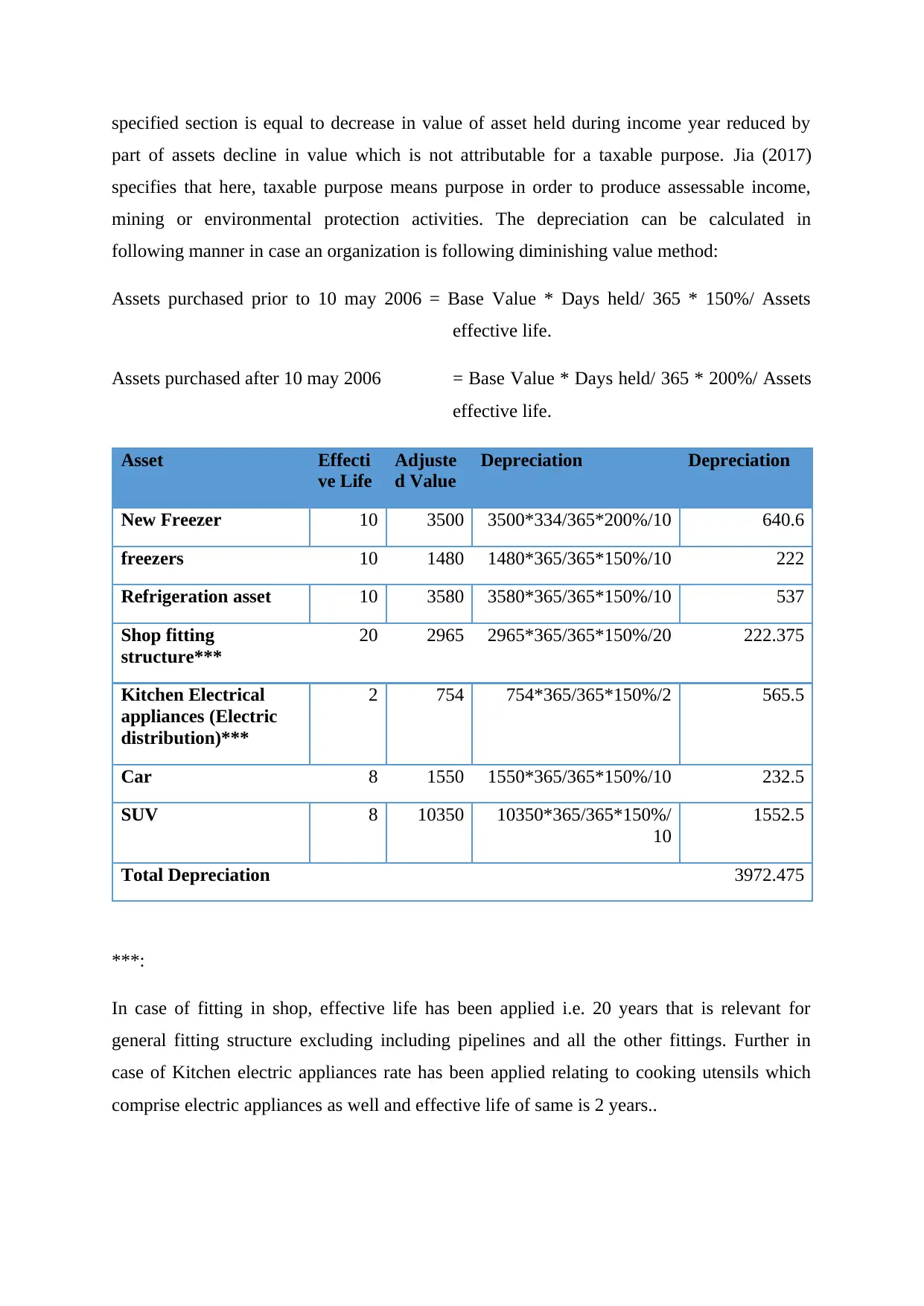

This report provides a detailed analysis of partnership taxation and Fringe Benefit Tax (FBT) provisions under Australian taxation law. It begins with an overview of income tax legislation, specifically ITAA 36 and ITAA 97, and their application to partnerships. The report includes a calculation of net partnership income, considering various income and expense items with detailed working notes explaining the treatment of items such as credit sales, stock adjustments, car expenses, electricity expenses, and depreciation. It also addresses the deductibility of repair expenses and interest on loans. Furthermore, the report examines the provisions of FBT, explaining its chargeability, valuation, and consequences for employers, including calculations for school fee payments and accommodation benefits. The analysis incorporates relevant sections of the Income Tax Assessment Act and Fringe Benefit Tax Assessment Act, along with references to case law and scholarly articles to support its conclusions. Desklib provides access to this and other solved assignments for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.