Taxation Law: Case Study on Partnership Income and Fringe Benefits

VerifiedAdded on 2023/04/21

|11

|2304

|498

Case Study

AI Summary

This case study delves into two primary taxation issues. The first concerns the calculation of net income from a partnership, considering various receipts and outgoings, and applying relevant sections of the ITAA 1936 and ITAA 1997 to determine assessable income and permissible deductions. Expenses such as drawings, shop painting, and refrigerator motor replacement are analyzed for their deductibility based on whether they are capital or private in nature. The second issue focuses on the fringe benefit consequences for an employer providing benefits to an employee, including school fees and housing. The analysis involves applying the FBTAA 1986 to determine the taxable value of these benefits, considering expense payment fringe benefits and housing fringe benefits, and exploring potential reductions in tax liability through employee contributions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Applications:..........................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Rule:.......................................................................................................................................7

Applications:..........................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

The current issue is based on ascertaining the net income obtained from the

partnership during the relevant income year.

Rule:

As per “division 5 of the ITAA 1936” partnership is not treated as the separate legal

unit based on the general law and they are not required to pay taxes. “Section 91 of the ITAA

1997” requires the taxpayers to file return so that they can reveal the allocation of profit

among the stakeholders1. As defined in “sec 92, ITA Act 1997” income or loss is allocated

among the partners which attracts tax liabilities. Citing “section 995-1(1)” partnership refers

to carrying of business to earn profit. Income obtained from partnership is either treated as

statutory and ordinary income.

As per “section 6-5(4)” and “section 6-10 (3), ITAA 1997” a taxpayer is believed to

have obtained the income as and when directed by the taxpayer. Referring to “sec 6-5, ITA

Act 1997” large part of the taxpayer’s income is classified as ordinary income. The

commissioner in “Scott v CT (1935)” stated that necessary principles must be applied to

determine the receipts as the ordinary income2. Similarly, under “section 6-5, ITA Act 1997”

business receipts are treated as income according to ordinary concepts.

1 Burton, Mark. "Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy." eJTR 16 (2018): 2.

2 Gideon, Michael. "Do individuals perceive income tax rates correctly?." Public Finance

Review 45.1 (2017): 97-117.

Answer to question 1:

Issues:

The current issue is based on ascertaining the net income obtained from the

partnership during the relevant income year.

Rule:

As per “division 5 of the ITAA 1936” partnership is not treated as the separate legal

unit based on the general law and they are not required to pay taxes. “Section 91 of the ITAA

1997” requires the taxpayers to file return so that they can reveal the allocation of profit

among the stakeholders1. As defined in “sec 92, ITA Act 1997” income or loss is allocated

among the partners which attracts tax liabilities. Citing “section 995-1(1)” partnership refers

to carrying of business to earn profit. Income obtained from partnership is either treated as

statutory and ordinary income.

As per “section 6-5(4)” and “section 6-10 (3), ITAA 1997” a taxpayer is believed to

have obtained the income as and when directed by the taxpayer. Referring to “sec 6-5, ITA

Act 1997” large part of the taxpayer’s income is classified as ordinary income. The

commissioner in “Scott v CT (1935)” stated that necessary principles must be applied to

determine the receipts as the ordinary income2. Similarly, under “section 6-5, ITA Act 1997”

business receipts are treated as income according to ordinary concepts.

1 Burton, Mark. "Interpreting the Australian Income Tax Definition of Ordinary Income:

Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth

Century Linguistic Philosophy." eJTR 16 (2018): 2.

2 Gideon, Michael. "Do individuals perceive income tax rates correctly?." Public Finance

Review 45.1 (2017): 97-117.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

“Section 8-1 of ITA Act 1997” permits the taxpayer from obtaining permissible

deduction relating to outgoings or expenses sustained while generating assessable income or

sustained during the process of generating assessable profits3. While the negative limbs of

“sec 8-1 (2), ITA Act 1997” prohibits a person from obtaining permissible deduction relating

to outgoings that carry the nature of private, domestic or capital type.

The ATO states that the taxpayers are permitted to instantly write-off for assets that

costs below 20,000. On the other hand, allows the taxpayers to obtain permissible deduction

for repairs. “Subsection 25-10 (1), ITA Act 1997” permits the taxpayer from obtaining

deduction for repairs that requires remedying the deterioration, defects or damage on the

property4. However, the taxpayers are denied deduction for repairs that are extensive or

capital in nature. Similarly, in “FC of T v Western Suburbs Cinemas (1952)” the taxpayer

was denied deduction for initial repairs because it amounted to capital in nature.

Application:

Denial and Olivia are carrying on the partnership business and reported certain

receipts as well as outgoings. The partnership derived receipts through sales and debtor’s

receipts. Referring to “section 6-5, ITA Act 1997” the sales receipts and payments from

debtors should be classified as income based on ordinary concepts which is included for

assessment of partnership income.

The partners reported drawings from the partnership that amounted to $5600, $6000.

They further reported the drawings of $3,200 that was related to private purpose of the

partners. Referring to “section 8-1 (2), ITA Act 1997”, drawings made by the partners does

3 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

4 Black, Duncan. The incidence of income taxes. Routledge, 2018.

“Section 8-1 of ITA Act 1997” permits the taxpayer from obtaining permissible

deduction relating to outgoings or expenses sustained while generating assessable income or

sustained during the process of generating assessable profits3. While the negative limbs of

“sec 8-1 (2), ITA Act 1997” prohibits a person from obtaining permissible deduction relating

to outgoings that carry the nature of private, domestic or capital type.

The ATO states that the taxpayers are permitted to instantly write-off for assets that

costs below 20,000. On the other hand, allows the taxpayers to obtain permissible deduction

for repairs. “Subsection 25-10 (1), ITA Act 1997” permits the taxpayer from obtaining

deduction for repairs that requires remedying the deterioration, defects or damage on the

property4. However, the taxpayers are denied deduction for repairs that are extensive or

capital in nature. Similarly, in “FC of T v Western Suburbs Cinemas (1952)” the taxpayer

was denied deduction for initial repairs because it amounted to capital in nature.

Application:

Denial and Olivia are carrying on the partnership business and reported certain

receipts as well as outgoings. The partnership derived receipts through sales and debtor’s

receipts. Referring to “section 6-5, ITA Act 1997” the sales receipts and payments from

debtors should be classified as income based on ordinary concepts which is included for

assessment of partnership income.

The partners reported drawings from the partnership that amounted to $5600, $6000.

They further reported the drawings of $3,200 that was related to private purpose of the

partners. Referring to “section 8-1 (2), ITA Act 1997”, drawings made by the partners does

3 Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

4 Black, Duncan. The incidence of income taxes. Routledge, 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

not qualifies for permissible deduction under the negative limbs because it amounted to

private in nature.

The ATO states that the taxpayers are permitted to instantly write-off for assets that

costs below 20,000. The partnership during the income year bought an air condition which

amounted to $1200. The base value of asset is within $20,000 and the partnership can choose

to instantly write off as the permissible deduction.

The partnership incurred outgoings for painting the shop and replacement of motor in

refrigerator. Citing the case of “FC of T v Western Suburbs Cinemas (1952)” the expenses

on shop painting and refrigerator motor replacement amounted to capital outgoing which is

non-deductible under “sect 25-10, ITA Act 1997”. The computation of partnership income is

given below together with the working paper;

not qualifies for permissible deduction under the negative limbs because it amounted to

private in nature.

The ATO states that the taxpayers are permitted to instantly write-off for assets that

costs below 20,000. The partnership during the income year bought an air condition which

amounted to $1200. The base value of asset is within $20,000 and the partnership can choose

to instantly write off as the permissible deduction.

The partnership incurred outgoings for painting the shop and replacement of motor in

refrigerator. Citing the case of “FC of T v Western Suburbs Cinemas (1952)” the expenses

on shop painting and refrigerator motor replacement amounted to capital outgoing which is

non-deductible under “sect 25-10, ITA Act 1997”. The computation of partnership income is

given below together with the working paper;

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 150170

Debtors Cash payments (Notes 1) 33715

Total Receipts 183885

Expenses Eligble for Deductions

Electricity Bill 1176

Council rates (Notes 6) 310.2

Business Insurance 1250

Mobile Bills (Notes 6) 633.6

Union Bills 284

Account Charges 595

Repair Expenses 1490

Loan Expenses (Notes 4) 5500

Purchase of Fixed Asset 3500

Cost of Sales (Notes 3) 30525

Van (Notes 5) 1134

SUV (Notes 5) 1230

Repayment to Creditors (Notes 2) 128168

Installation of Air-Condition 1200

Depreciation Expenses(Notes 7) 726.2

New Restaurant Freezer 3500

Total Expenses Eligible for Deductions 181222

Net Income From Partnership 2663

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3500

Less: Trade In Value @ 500 3000 333 547.4

Air Conditions installation 1200 272 178.8

Total Depreciation 726.2

Working papers

Notes 7

Particulars Amount ($)

Receipts

Business sales 150170

Debtors Cash payments (Notes 1) 33715

Total Receipts 183885

Expenses Eligble for Deductions

Electricity Bill 1176

Council rates (Notes 6) 310.2

Business Insurance 1250

Mobile Bills (Notes 6) 633.6

Union Bills 284

Account Charges 595

Repair Expenses 1490

Loan Expenses (Notes 4) 5500

Purchase of Fixed Asset 3500

Cost of Sales (Notes 3) 30525

Van (Notes 5) 1134

SUV (Notes 5) 1230

Repayment to Creditors (Notes 2) 128168

Installation of Air-Condition 1200

Depreciation Expenses(Notes 7) 726.2

New Restaurant Freezer 3500

Total Expenses Eligible for Deductions 181222

Net Income From Partnership 2663

Computation of Partnership Net Income

For the year ended 30th June 2017

Working Papers:

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3500

Less: Trade In Value @ 500 3000 333 547.4

Air Conditions installation 1200 272 178.8

Total Depreciation 726.2

Working papers

Notes 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Notes 1

Debtors at 1st July 2016 3925

Debtors Cash Payments 32800

Debtors at 30th June 2017 3010

Debtors Net 33715

Notes 2

Creditors at 1st July 2016 6500

Add: Repayment to Creditors 128678

Less: Creditors at 30 June 2017 7010

Creditors Net 128168

Notes 3

Cost of Sales

Stock on 1st July 2016 9120

Add: Purchase 31155

Less: Stock on 30th June 2017 9750

Notes 4 30525

Loan Repayment

Business Loan 8500

Less: Reduction of loan 3000

Net Loan Re-Payment 5500

Notes 5

Cost of Maintainance

Van 1260

Less: Business use 90% 1134

SUV 2050

Less: Business use 60% 1230

Total cost of Maintainance 2364

Notes 6

Mobile Bills 704

Less: 90% Business Use 633.6

Electricity Expenses 1470

Less: 80% Business Use 1176

Council Rates 517

Less: 60% Business Use 310.2

Notes 1

Debtors at 1st July 2016 3925

Debtors Cash Payments 32800

Debtors at 30th June 2017 3010

Debtors Net 33715

Notes 2

Creditors at 1st July 2016 6500

Add: Repayment to Creditors 128678

Less: Creditors at 30 June 2017 7010

Creditors Net 128168

Notes 3

Cost of Sales

Stock on 1st July 2016 9120

Add: Purchase 31155

Less: Stock on 30th June 2017 9750

Notes 4 30525

Loan Repayment

Business Loan 8500

Less: Reduction of loan 3000

Net Loan Re-Payment 5500

Notes 5

Cost of Maintainance

Van 1260

Less: Business use 90% 1134

SUV 2050

Less: Business use 60% 1230

Total cost of Maintainance 2364

Notes 6

Mobile Bills 704

Less: 90% Business Use 633.6

Electricity Expenses 1470

Less: 80% Business Use 1176

Council Rates 517

Less: 60% Business Use 310.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Conclusion:

On a conclusive note, the net income from the partnership amounted to $2,663 and the

same has been included for assessment purpose under “section 6-5, ITA Act 1997” as income

according to the ordinary concepts.

Answer to question 2:

Issues:

The current issue here is based on determining the fringe benefit consequences for the

employer of John relating to the receipt of fringe benefit under FBTAA 1986.

Rule:

Fringe benefit is representing the payment made the employee that is different from

wages and salary. As per FBTAA 1986 benefits given to employee as the part of employment

constitutes fringe benefit5. The tax liability paying the fringe benefit arises falls on the

employer irrespective whether the employer is sole trader partnership, trustee, government or

corporation.

“Section 20 of FBTAA1986” defines the expense payment fringe benefit. An expense

payment fringe benefit might originate when the employer pays the third party to satisfy the

outgoings occurred by the employee6. The chargeable value of the expense payment fringe

5 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13.3 (2015):

819.

6 Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

Conclusion:

On a conclusive note, the net income from the partnership amounted to $2,663 and the

same has been included for assessment purpose under “section 6-5, ITA Act 1997” as income

according to the ordinary concepts.

Answer to question 2:

Issues:

The current issue here is based on determining the fringe benefit consequences for the

employer of John relating to the receipt of fringe benefit under FBTAA 1986.

Rule:

Fringe benefit is representing the payment made the employee that is different from

wages and salary. As per FBTAA 1986 benefits given to employee as the part of employment

constitutes fringe benefit5. The tax liability paying the fringe benefit arises falls on the

employer irrespective whether the employer is sole trader partnership, trustee, government or

corporation.

“Section 20 of FBTAA1986” defines the expense payment fringe benefit. An expense

payment fringe benefit might originate when the employer pays the third party to satisfy the

outgoings occurred by the employee6. The chargeable value of the expense payment fringe

5 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13.3 (2015):

819.

6 Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

8TAXATION LAW

benefit happens when the employer reimburses or pays the outgoings. There are situations

where the tax liability of fringe benefit expenses can be lowered if the employer makes

contributions towards the fringe benefit costs.

Denoting “subparagraph 65A (ii), FBTAA 1986” payment of expenses payment

fringe benefit is permitted for reduction in tax liability for the employer given the child fees

occurred is in relation to the full time child’s education of employee7. As held in “J & G

Knowles v FCT (2000)” the recipient expenses hold material and sufficient relation among

the employees benefit and occupation.

Accordingly, “section 25, FBTAA 1986” states that a housing fringe benefit denotes

a situation where the employee is offered with the rights of using the house as the employee’s

general residential place. The taxable value of the housing fringe benefit is determined by

referring to the market value of the unit of housing given by the employer to an employee

lowered by any sum of recipient rent that are in effect of the rental accommodation.

Applications:

Accordingly, in the case of John, the employer pays the child school fees that

amounted to $15,000. Citing the “sec 20, FBTAA 1986” the expense payment fringe benefit

arises here for the employer of John because the expenses were incurred by the employee to

satisfy the third party payment. Citing the judgement of “J & G Knowles v FCT (2000)” the

expenses of John’s employer hold material and sufficient relation among the employee

benefit and occupation8. Therefore, John would be liable for FBT however he can reduce the

7 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52.11 (2018): 608.

8 Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human

benefit happens when the employer reimburses or pays the outgoings. There are situations

where the tax liability of fringe benefit expenses can be lowered if the employer makes

contributions towards the fringe benefit costs.

Denoting “subparagraph 65A (ii), FBTAA 1986” payment of expenses payment

fringe benefit is permitted for reduction in tax liability for the employer given the child fees

occurred is in relation to the full time child’s education of employee7. As held in “J & G

Knowles v FCT (2000)” the recipient expenses hold material and sufficient relation among

the employees benefit and occupation.

Accordingly, “section 25, FBTAA 1986” states that a housing fringe benefit denotes

a situation where the employee is offered with the rights of using the house as the employee’s

general residential place. The taxable value of the housing fringe benefit is determined by

referring to the market value of the unit of housing given by the employer to an employee

lowered by any sum of recipient rent that are in effect of the rental accommodation.

Applications:

Accordingly, in the case of John, the employer pays the child school fees that

amounted to $15,000. Citing the “sec 20, FBTAA 1986” the expense payment fringe benefit

arises here for the employer of John because the expenses were incurred by the employee to

satisfy the third party payment. Citing the judgement of “J & G Knowles v FCT (2000)” the

expenses of John’s employer hold material and sufficient relation among the employee

benefit and occupation8. Therefore, John would be liable for FBT however he can reduce the

7 White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52.11 (2018): 608.

8 Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

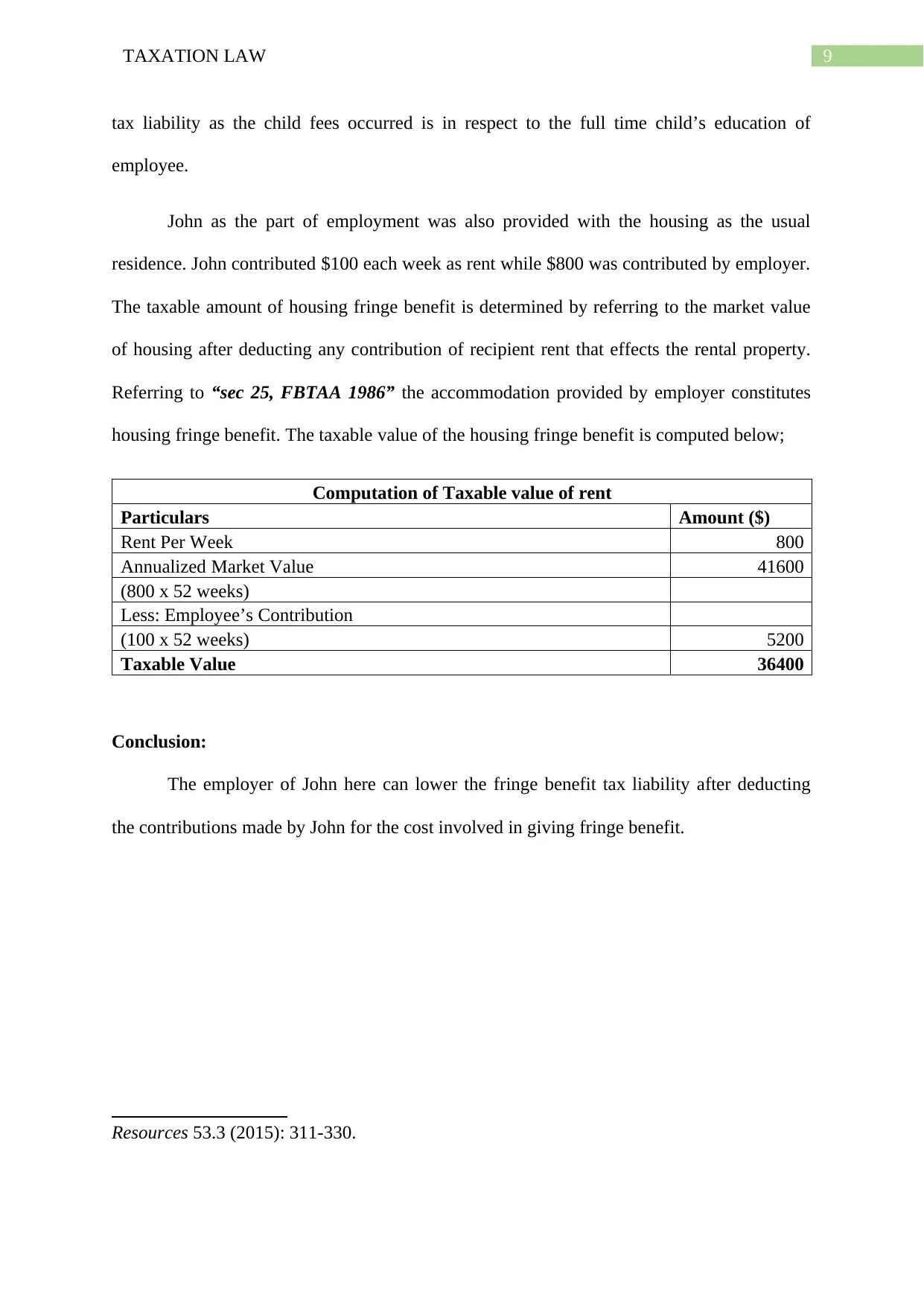

tax liability as the child fees occurred is in respect to the full time child’s education of

employee.

John as the part of employment was also provided with the housing as the usual

residence. John contributed $100 each week as rent while $800 was contributed by employer.

The taxable amount of housing fringe benefit is determined by referring to the market value

of housing after deducting any contribution of recipient rent that effects the rental property.

Referring to “sec 25, FBTAA 1986” the accommodation provided by employer constitutes

housing fringe benefit. The taxable value of the housing fringe benefit is computed below;

Computation of Taxable value of rent

Particulars Amount ($)

Rent Per Week 800

Annualized Market Value 41600

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5200

Taxable Value 36400

Conclusion:

The employer of John here can lower the fringe benefit tax liability after deducting

the contributions made by John for the cost involved in giving fringe benefit.

Resources 53.3 (2015): 311-330.

tax liability as the child fees occurred is in respect to the full time child’s education of

employee.

John as the part of employment was also provided with the housing as the usual

residence. John contributed $100 each week as rent while $800 was contributed by employer.

The taxable amount of housing fringe benefit is determined by referring to the market value

of housing after deducting any contribution of recipient rent that effects the rental property.

Referring to “sec 25, FBTAA 1986” the accommodation provided by employer constitutes

housing fringe benefit. The taxable value of the housing fringe benefit is computed below;

Computation of Taxable value of rent

Particulars Amount ($)

Rent Per Week 800

Annualized Market Value 41600

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5200

Taxable Value 36400

Conclusion:

The employer of John here can lower the fringe benefit tax liability after deducting

the contributions made by John for the cost involved in giving fringe benefit.

Resources 53.3 (2015): 311-330.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Black, Duncan. The incidence of income taxes. Routledge, 2018.

Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

Burton, Mark. "Interpreting the Australian Income Tax Definition of Ordinary Income: Ritual

Incantation Or Analysis, When Examined through the Lens of Early Twentieth Century

Linguistic Philosophy." eJTR 16 (2018): 2.

Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human

Resources 53.3 (2015): 311-330.

Gideon, Michael. "Do individuals perceive income tax rates correctly?." Public Finance

Review 45.1 (2017): 97-117.

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13.3 (2015):

819.

White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52.11 (2018): 608.

References:

Black, Duncan. The incidence of income taxes. Routledge, 2018.

Braverman, Daniel, Stephen Marsden, and Kerrie Sadiq. "Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules." J. Austl. Tax'n17

(2015): 1.

Buenker, John D. The Income Tax and the Progressive Era. Routledge, 2018.

Burton, Mark. "Interpreting the Australian Income Tax Definition of Ordinary Income: Ritual

Incantation Or Analysis, When Examined through the Lens of Early Twentieth Century

Linguistic Philosophy." eJTR 16 (2018): 2.

Cortis, Natasha, and Christine Eastman. "Salary sacrificing in A ustralia: are patterns of

uptake and benefit different in the not‐for‐profit sector?." Asia Pacific Journal of Human

Resources 53.3 (2015): 311-330.

Gideon, Michael. "Do individuals perceive income tax rates correctly?." Public Finance

Review 45.1 (2017): 97-117.

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13.3 (2015):

819.

White, Judy, and Adele Townsend. "Deductibility of employee travel expenses: The ATO's

guidance." Taxation in Australia52.11 (2018): 608.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.