Recording Business Transaction: Journal, Ledger, Trial Balance, Income Statement, Balance Sheet

VerifiedAdded on 2023/06/15

|15

|2057

|241

AI Summary

This report explains how to record business transactions in the journal, prepare general ledgers, formulate the trial balance, construct the income statement, and provide details of the balance sheet. It also covers determining accounting ratios and explaining the impact of Covid-19 on business profits. The report includes examples and explanations to help readers understand the concepts better.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transaction

Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

PART A ..........................................................................................................................................3

a) Record the enterprise proceedings in the journal...............................................................3

b) Prepare general ledgers......................................................................................................5

c) Formulate the Trial Balance...............................................................................................9

d) Construct the Income Statement........................................................................................9

e) Provide details of the Balance Sheet................................................................................10

f) Determine what are drawings and explain it to Linda......................................................11

PART B .........................................................................................................................................11

a) Determine the Accounting Ratios of the Business...........................................................11

b) Explain the impact of Covid-19 on the profits of the business........................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

PART A ..........................................................................................................................................3

a) Record the enterprise proceedings in the journal...............................................................3

b) Prepare general ledgers......................................................................................................5

c) Formulate the Trial Balance...............................................................................................9

d) Construct the Income Statement........................................................................................9

e) Provide details of the Balance Sheet................................................................................10

f) Determine what are drawings and explain it to Linda......................................................11

PART B .........................................................................................................................................11

a) Determine the Accounting Ratios of the Business...........................................................11

b) Explain the impact of Covid-19 on the profits of the business........................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The business transactions refer to the happenings in the business which is related to either

its operations or non-operations which help the business in earning a revenue. These transactions

are recorded in the books of accounts of the business and determines how a business is doing

financially (PURI, and SINGH, 2021). These transactions may occur in the business when they

sell its products and services in the market of when it acquires raw materials from the markets.

These transactions are recorded and summaries to determine the profit or loss earned by the

business in a given period of time which is called the accounting period or fiscal period. This

report highlights how these transactions are recorded and summarised in the defined accounting

period and shows how different financial statements are prepared in the business.

TASK

PART A

a) Record the enterprise proceedings in the journal

JOURNAL ENTRIES

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business being started with cash, flat and a car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(goods of the firm i.e., furniture being purchased on

credit from Home ltd.)

5400

5400

04/10/21 Computer

Printer

Bank

800

200

1000

The business transactions refer to the happenings in the business which is related to either

its operations or non-operations which help the business in earning a revenue. These transactions

are recorded in the books of accounts of the business and determines how a business is doing

financially (PURI, and SINGH, 2021). These transactions may occur in the business when they

sell its products and services in the market of when it acquires raw materials from the markets.

These transactions are recorded and summaries to determine the profit or loss earned by the

business in a given period of time which is called the accounting period or fiscal period. This

report highlights how these transactions are recorded and summarised in the defined accounting

period and shows how different financial statements are prepared in the business.

TASK

PART A

a) Record the enterprise proceedings in the journal

JOURNAL ENTRIES

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business being started with cash, flat and a car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(goods of the firm i.e., furniture being purchased on

credit from Home ltd.)

5400

5400

04/10/21 Computer

Printer

Bank

800

200

1000

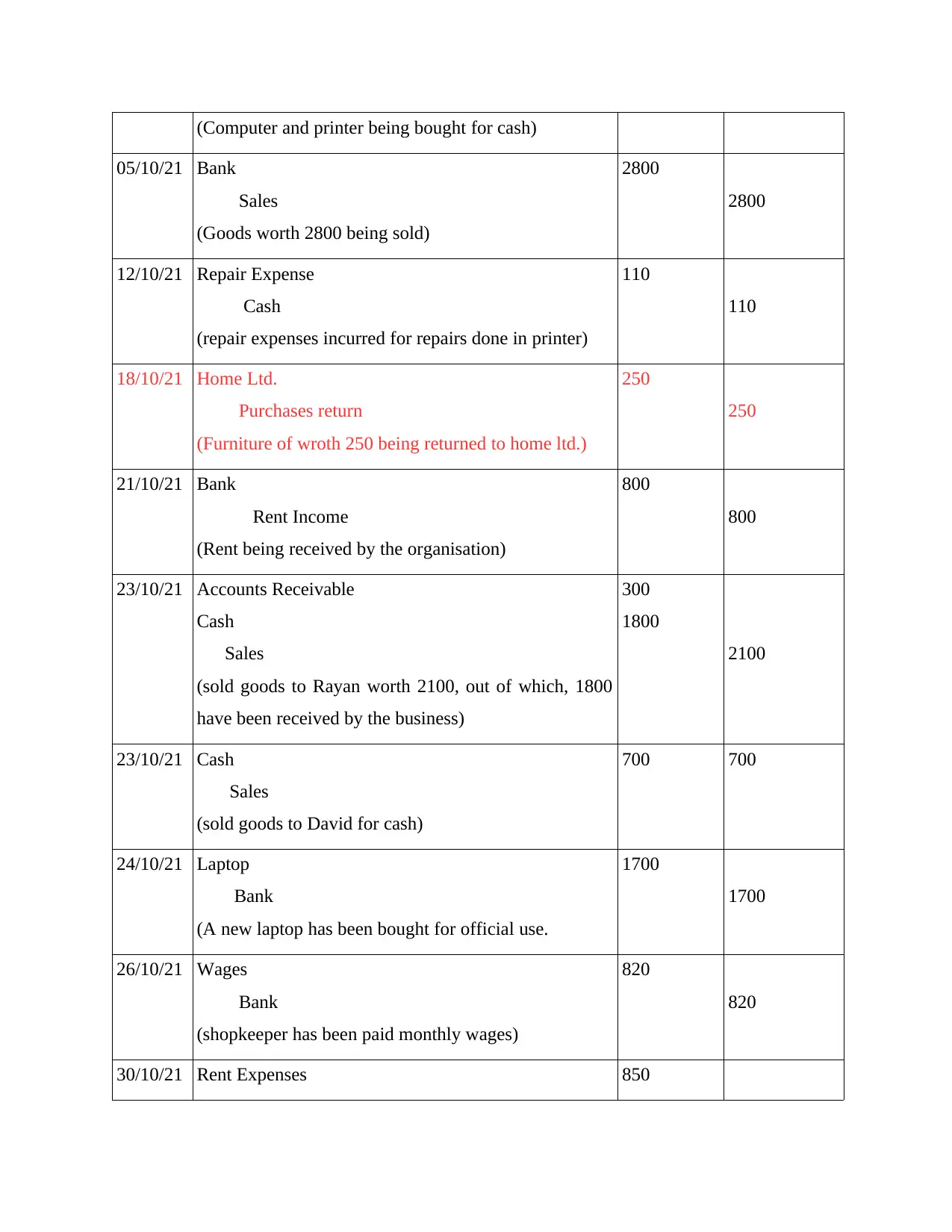

(Computer and printer being bought for cash)

05/10/21 Bank

Sales

(Goods worth 2800 being sold)

2800

2800

12/10/21 Repair Expense

Cash

(repair expenses incurred for repairs done in printer)

110

110

18/10/21 Home Ltd.

Purchases return

(Furniture of wroth 250 being returned to home ltd.)

250

250

21/10/21 Bank

Rent Income

(Rent being received by the organisation)

800

800

23/10/21 Accounts Receivable

Cash

Sales

(sold goods to Rayan worth 2100, out of which, 1800

have been received by the business)

300

1800

2100

23/10/21 Cash

Sales

(sold goods to David for cash)

700 700

24/10/21 Laptop

Bank

(A new laptop has been bought for official use.

1700

1700

26/10/21 Wages

Bank

(shopkeeper has been paid monthly wages)

820

820

30/10/21 Rent Expenses 850

05/10/21 Bank

Sales

(Goods worth 2800 being sold)

2800

2800

12/10/21 Repair Expense

Cash

(repair expenses incurred for repairs done in printer)

110

110

18/10/21 Home Ltd.

Purchases return

(Furniture of wroth 250 being returned to home ltd.)

250

250

21/10/21 Bank

Rent Income

(Rent being received by the organisation)

800

800

23/10/21 Accounts Receivable

Cash

Sales

(sold goods to Rayan worth 2100, out of which, 1800

have been received by the business)

300

1800

2100

23/10/21 Cash

Sales

(sold goods to David for cash)

700 700

24/10/21 Laptop

Bank

(A new laptop has been bought for official use.

1700

1700

26/10/21 Wages

Bank

(shopkeeper has been paid monthly wages)

820

820

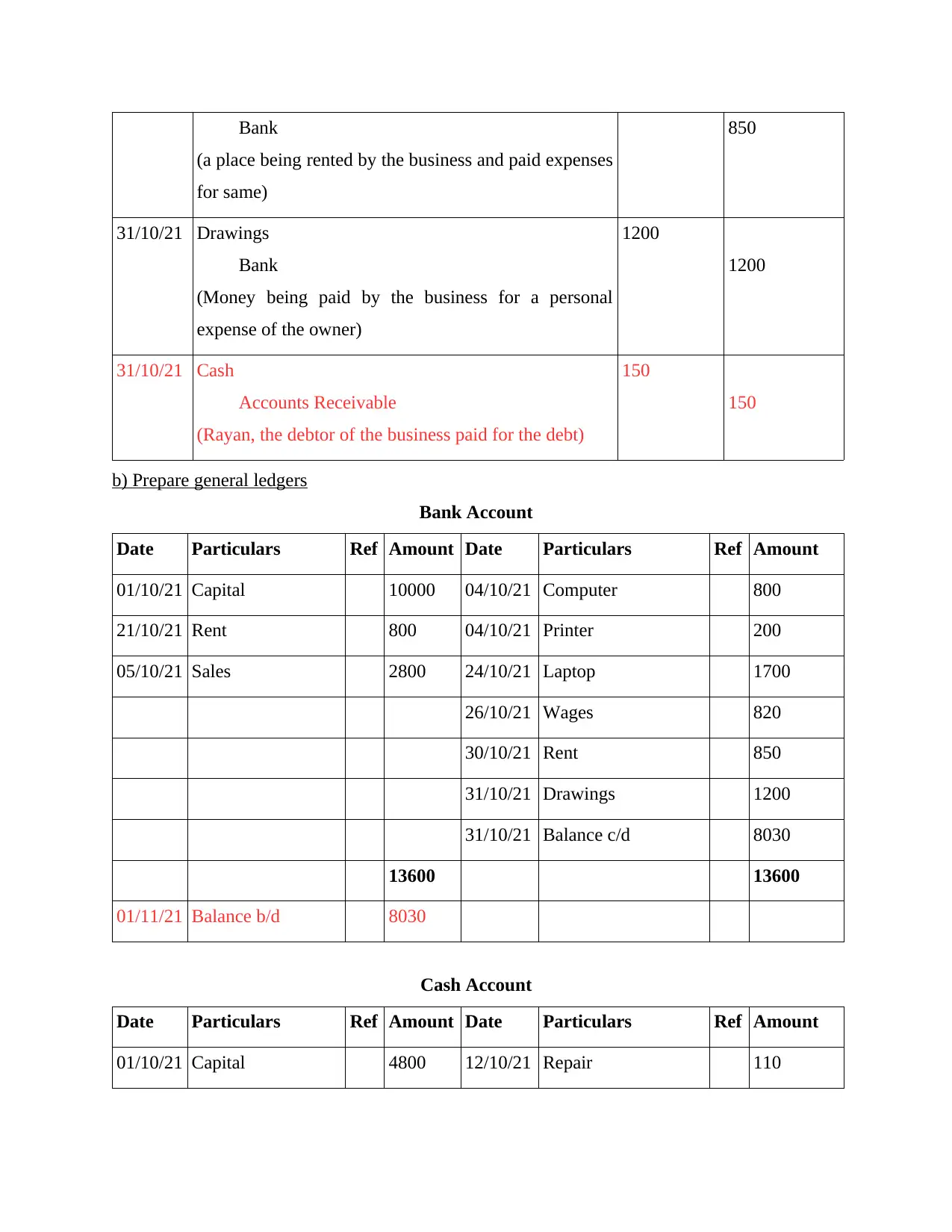

30/10/21 Rent Expenses 850

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Bank

(a place being rented by the business and paid expenses

for same)

850

31/10/21 Drawings

Bank

(Money being paid by the business for a personal

expense of the owner)

1200

1200

31/10/21 Cash

Accounts Receivable

(Rayan, the debtor of the business paid for the debt)

150

150

b) Prepare general ledgers

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

01/11/21 Balance b/d 8030

Cash Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 4800 12/10/21 Repair 110

(a place being rented by the business and paid expenses

for same)

850

31/10/21 Drawings

Bank

(Money being paid by the business for a personal

expense of the owner)

1200

1200

31/10/21 Cash

Accounts Receivable

(Rayan, the debtor of the business paid for the debt)

150

150

b) Prepare general ledgers

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

01/11/21 Balance b/d 8030

Cash Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 4800 12/10/21 Repair 110

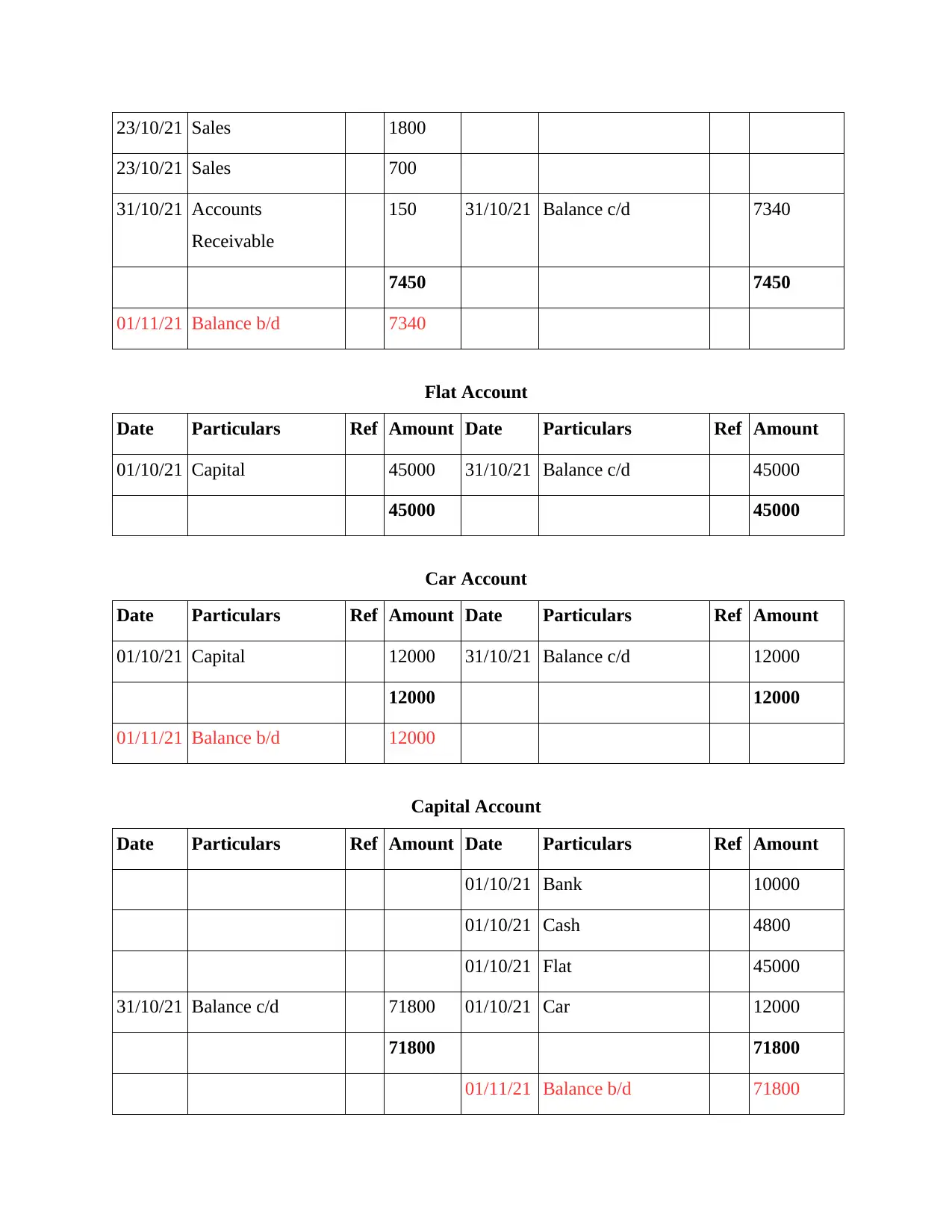

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Accounts

Receivable

150 31/10/21 Balance c/d 7340

7450 7450

01/11/21 Balance b/d 7340

Flat Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

Car Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Bank 10000

01/10/21 Cash 4800

01/10/21 Flat 45000

31/10/21 Balance c/d 71800 01/10/21 Car 12000

71800 71800

01/11/21 Balance b/d 71800

23/10/21 Sales 700

31/10/21 Accounts

Receivable

150 31/10/21 Balance c/d 7340

7450 7450

01/11/21 Balance b/d 7340

Flat Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

Car Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Bank 10000

01/10/21 Cash 4800

01/10/21 Flat 45000

31/10/21 Balance c/d 71800 01/10/21 Car 12000

71800 71800

01/11/21 Balance b/d 71800

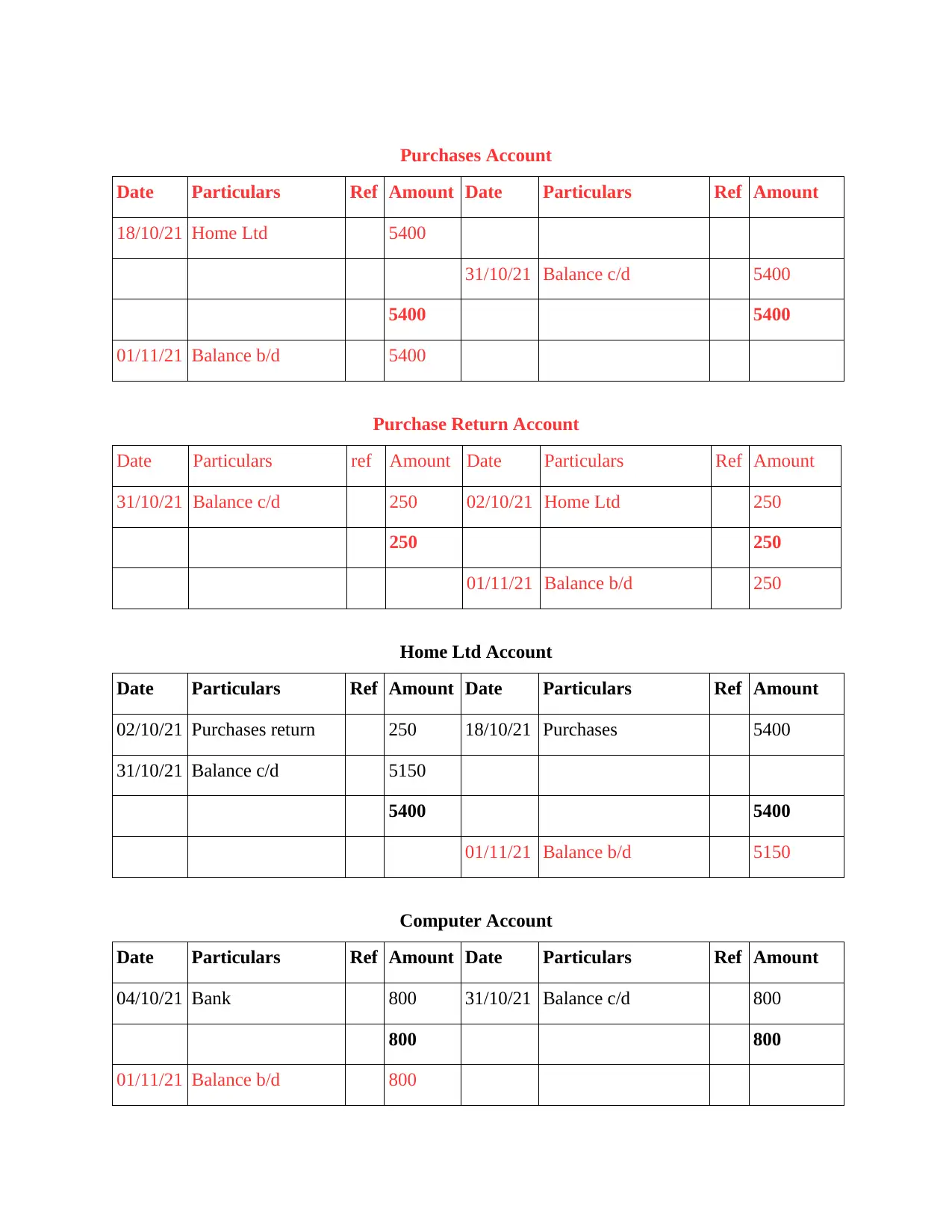

Purchases Account

Date Particulars Ref Amount Date Particulars Ref Amount

18/10/21 Home Ltd 5400

31/10/21 Balance c/d 5400

5400 5400

01/11/21 Balance b/d 5400

Purchase Return Account

Date Particulars ref Amount Date Particulars Ref Amount

31/10/21 Balance c/d 250 02/10/21 Home Ltd 250

250 250

01/11/21 Balance b/d 250

Home Ltd Account

Date Particulars Ref Amount Date Particulars Ref Amount

02/10/21 Purchases return 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

Date Particulars Ref Amount Date Particulars Ref Amount

18/10/21 Home Ltd 5400

31/10/21 Balance c/d 5400

5400 5400

01/11/21 Balance b/d 5400

Purchase Return Account

Date Particulars ref Amount Date Particulars Ref Amount

31/10/21 Balance c/d 250 02/10/21 Home Ltd 250

250 250

01/11/21 Balance b/d 250

Home Ltd Account

Date Particulars Ref Amount Date Particulars Ref Amount

02/10/21 Purchases return 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

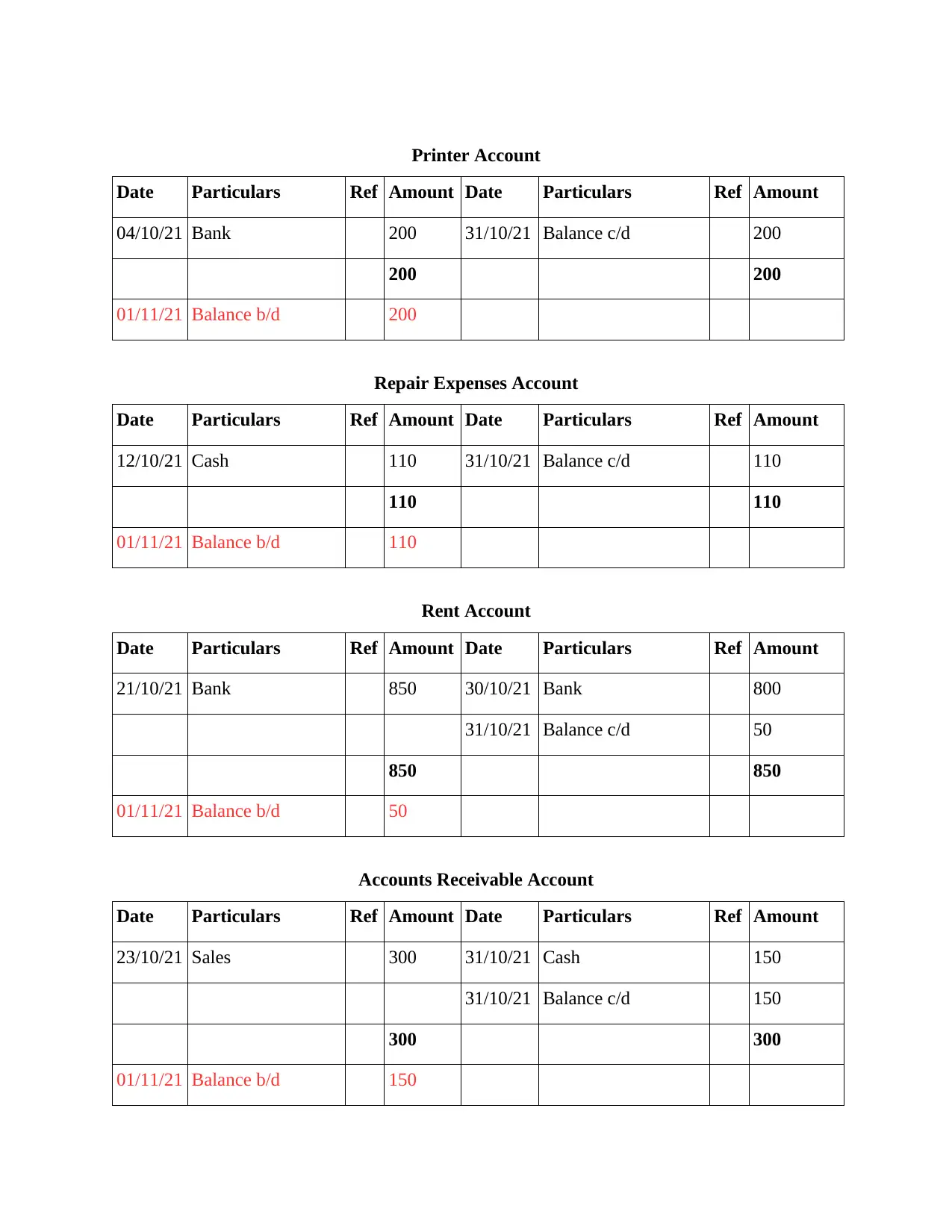

Printer Account

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 200 31/10/21 Balance c/d 200

200 200

01/11/21 Balance b/d 200

Repair Expenses Account

Date Particulars Ref Amount Date Particulars Ref Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars Ref Amount Date Particulars Ref Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Accounts Receivable Account

Date Particulars Ref Amount Date Particulars Ref Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 200 31/10/21 Balance c/d 200

200 200

01/11/21 Balance b/d 200

Repair Expenses Account

Date Particulars Ref Amount Date Particulars Ref Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars Ref Amount Date Particulars Ref Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Accounts Receivable Account

Date Particulars Ref Amount Date Particulars Ref Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

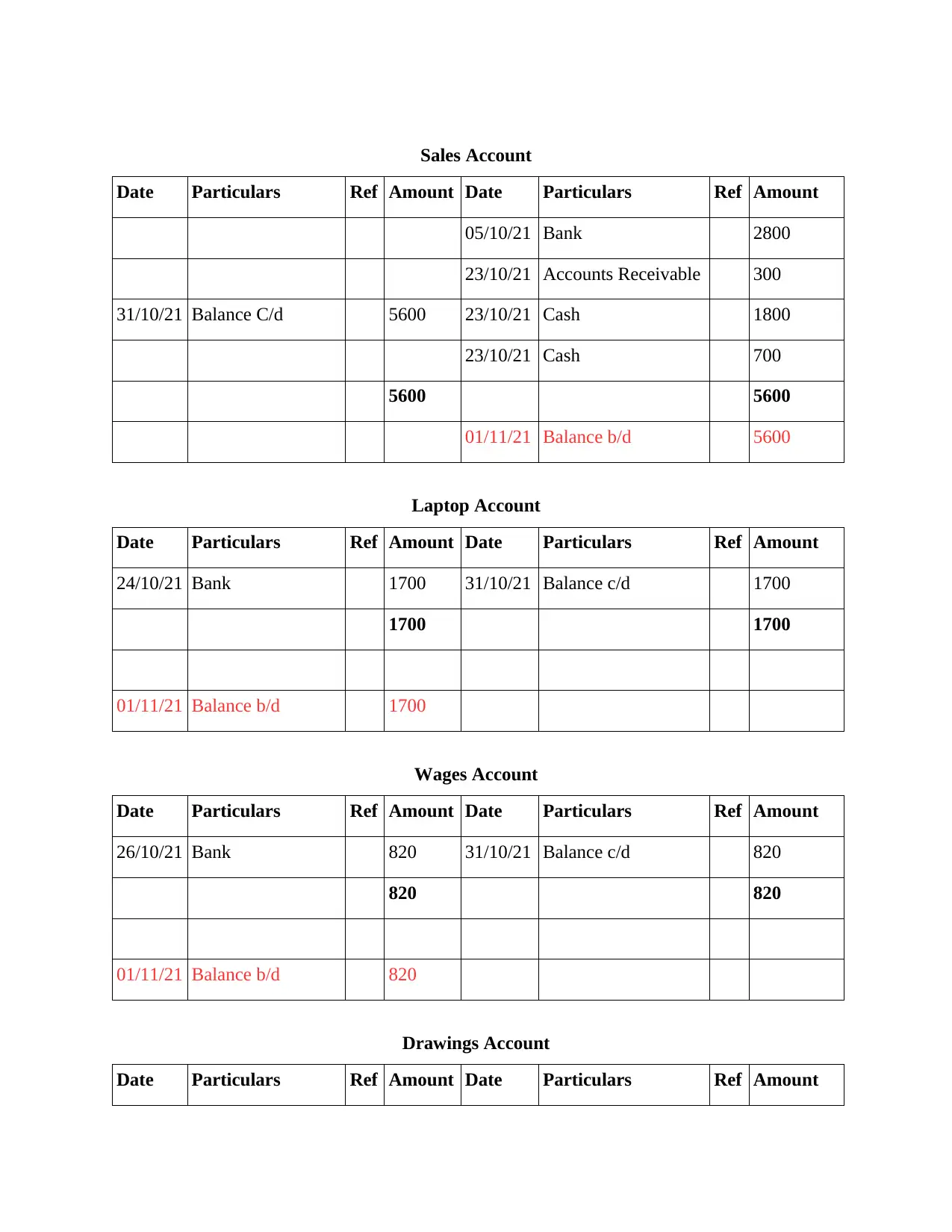

Sales Account

Date Particulars Ref Amount Date Particulars Ref Amount

05/10/21 Bank 2800

23/10/21 Accounts Receivable 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars Ref Amount Date Particulars Ref Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars Ref Amount Date Particulars Ref Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars Ref Amount Date Particulars Ref Amount

Date Particulars Ref Amount Date Particulars Ref Amount

05/10/21 Bank 2800

23/10/21 Accounts Receivable 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars Ref Amount Date Particulars Ref Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars Ref Amount Date Particulars Ref Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars Ref Amount Date Particulars Ref Amount

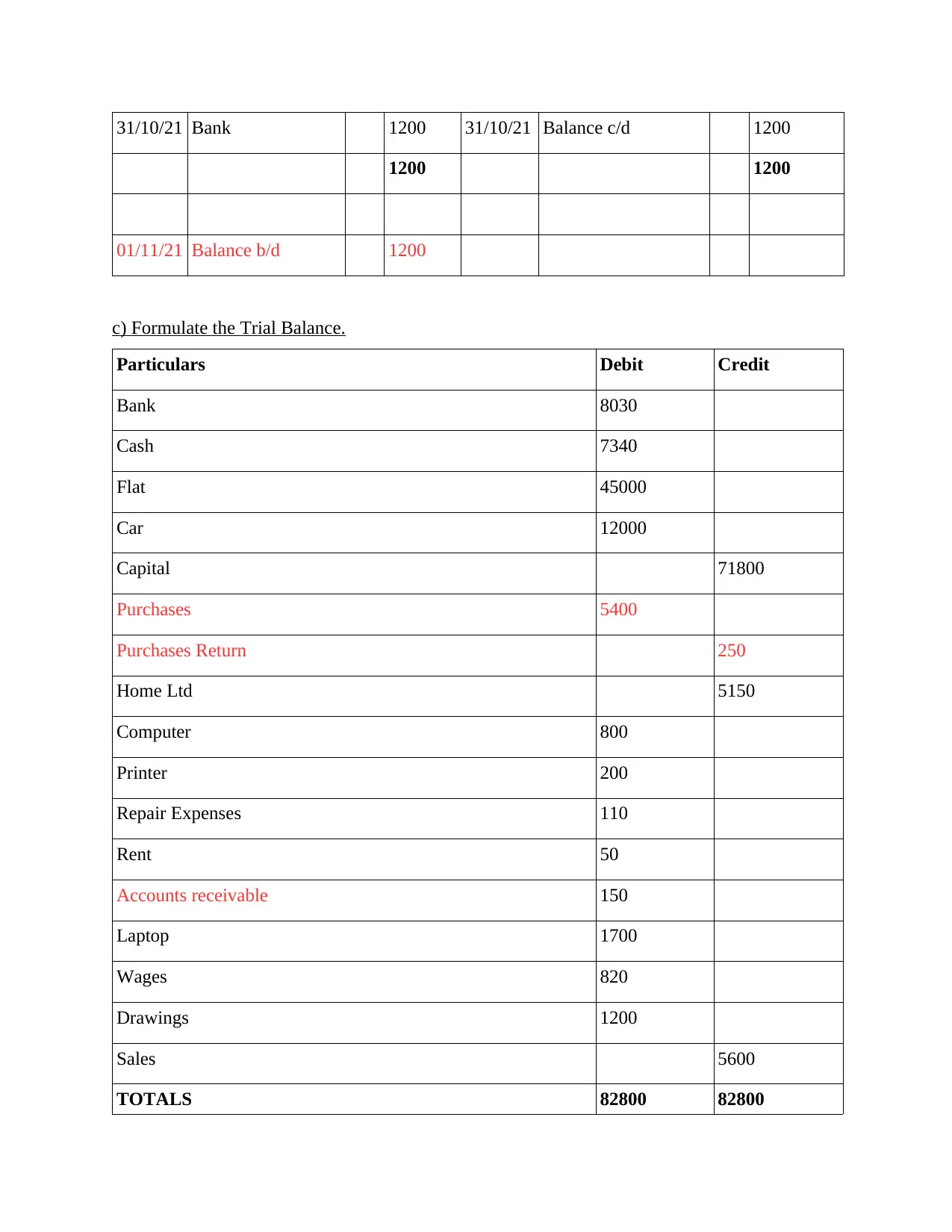

31/10/21 Bank 1200 31/10/21 Balance c/d 1200

1200 1200

01/11/21 Balance b/d 1200

c) Formulate the Trial Balance.

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5400

Purchases Return 250

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Accounts receivable 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTALS 82800 82800

1200 1200

01/11/21 Balance b/d 1200

c) Formulate the Trial Balance.

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5400

Purchases Return 250

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Accounts receivable 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTALS 82800 82800

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

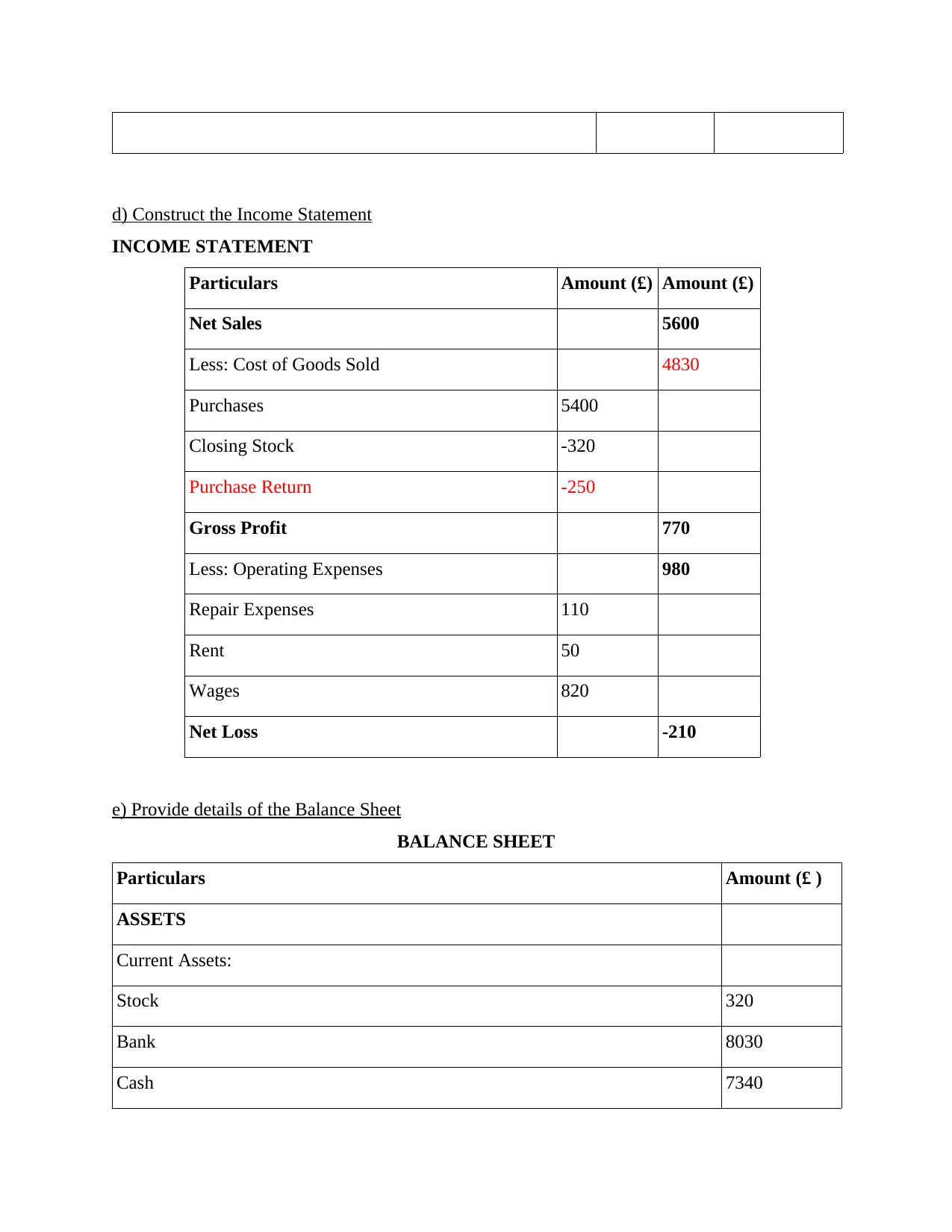

d) Construct the Income Statement

INCOME STATEMENT

Particulars Amount (£) Amount (£)

Net Sales 5600

Less: Cost of Goods Sold 4830

Purchases 5400

Closing Stock -320

Purchase Return -250

Gross Profit 770

Less: Operating Expenses 980

Repair Expenses 110

Rent 50

Wages 820

Net Loss -210

e) Provide details of the Balance Sheet

BALANCE SHEET

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

INCOME STATEMENT

Particulars Amount (£) Amount (£)

Net Sales 5600

Less: Cost of Goods Sold 4830

Purchases 5400

Closing Stock -320

Purchase Return -250

Gross Profit 770

Less: Operating Expenses 980

Repair Expenses 110

Rent 50

Wages 820

Net Loss -210

e) Provide details of the Balance Sheet

BALANCE SHEET

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

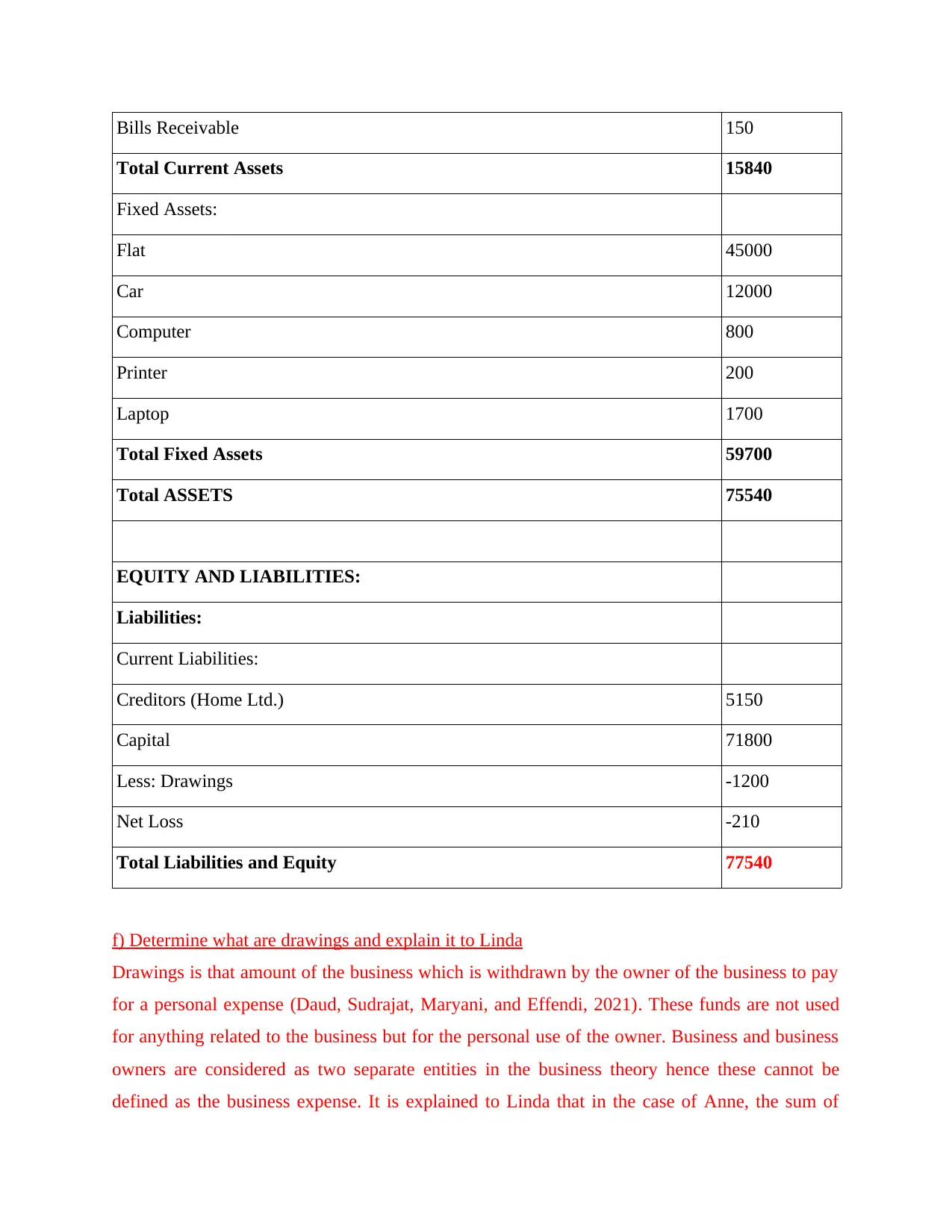

Bills Receivable 150

Total Current Assets 15840

Fixed Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

Laptop 1700

Total Fixed Assets 59700

Total ASSETS 75540

EQUITY AND LIABILITIES:

Liabilities:

Current Liabilities:

Creditors (Home Ltd.) 5150

Capital 71800

Less: Drawings -1200

Net Loss -210

Total Liabilities and Equity 77540

f) Determine what are drawings and explain it to Linda

Drawings is that amount of the business which is withdrawn by the owner of the business to pay

for a personal expense (Daud, Sudrajat, Maryani, and Effendi, 2021). These funds are not used

for anything related to the business but for the personal use of the owner. Business and business

owners are considered as two separate entities in the business theory hence these cannot be

defined as the business expense. It is explained to Linda that in the case of Anne, the sum of

Total Current Assets 15840

Fixed Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

Laptop 1700

Total Fixed Assets 59700

Total ASSETS 75540

EQUITY AND LIABILITIES:

Liabilities:

Current Liabilities:

Creditors (Home Ltd.) 5150

Capital 71800

Less: Drawings -1200

Net Loss -210

Total Liabilities and Equity 77540

f) Determine what are drawings and explain it to Linda

Drawings is that amount of the business which is withdrawn by the owner of the business to pay

for a personal expense (Daud, Sudrajat, Maryani, and Effendi, 2021). These funds are not used

for anything related to the business but for the personal use of the owner. Business and business

owners are considered as two separate entities in the business theory hence these cannot be

defined as the business expense. It is explained to Linda that in the case of Anne, the sum of

1200 which have been paid by the business were the drawings done by Anne from the business

as these were paid from the business bank account for the holiday trip of Anne York.

PART B

a) Determine the Accounting Ratios of the Business

Net Profit Margin = (Net profit / Net Sales) * 100 = (- 210 / 5600) * 100 = - 3.75 %

Gross Profit Margin = (Gross Profit / Net Sales) * 100 = (770 / 5600) * 100 = 13.75 %

Current Ratio = Current Assets / Current Liabilities (Wiratama, and Asri, 2020) =

15480 / 5150 = 3.01

Acid Test ratio = (Current Assets – Stock) / Current Liabilities = (15480 – 320) / 5150 =

2.94

Accounts Receivable Collection Period = (Average Debtors / Net Sales) * 365 = (150 /

5600) * 365 = 9.78 Days

Accounts Payable Payment Period = (Average Creditors / Net Purchases) * 365 =

(5150 / 5150) * 365 = 365 Days

Interpretation: From the above calculation of ratios of Anne, it can be seen that the organisation

of Anne is not performing well when compared to the ratios of the competitors. It can be seen

that the competitors of the business are earning more profits at a less expenditure. The current

assets of these businesses are high in comparison to Anne's business. This creates a bad condition

for the business as it impacts the short term liquidity positions of the business (Yang, 2021). But

Anne's asset employment is better than most of the businesses which creates better hope for the

business.

b) Explain the impact of Covid-19 on the profits of the business

The Covid-19 pandemic has created chaos among the world and particularly in the business

world as the businesses, to cut the costs, reduced their production in the times of uncertainty

(Heister, Kaufman, and Yuthas, 2021). The business in the case have seen greater losses in the

business due to reduced demand in the marketplace. The decrease in the market interactions of

the business of Anne have decreased their sales revenue and in turn its profits have turned into

losses. It is advised to Anne that she should focus on covering up these losses in the year 2021 if

she wants to reach no profit-no loss condition. After that she can work on the production and

as these were paid from the business bank account for the holiday trip of Anne York.

PART B

a) Determine the Accounting Ratios of the Business

Net Profit Margin = (Net profit / Net Sales) * 100 = (- 210 / 5600) * 100 = - 3.75 %

Gross Profit Margin = (Gross Profit / Net Sales) * 100 = (770 / 5600) * 100 = 13.75 %

Current Ratio = Current Assets / Current Liabilities (Wiratama, and Asri, 2020) =

15480 / 5150 = 3.01

Acid Test ratio = (Current Assets – Stock) / Current Liabilities = (15480 – 320) / 5150 =

2.94

Accounts Receivable Collection Period = (Average Debtors / Net Sales) * 365 = (150 /

5600) * 365 = 9.78 Days

Accounts Payable Payment Period = (Average Creditors / Net Purchases) * 365 =

(5150 / 5150) * 365 = 365 Days

Interpretation: From the above calculation of ratios of Anne, it can be seen that the organisation

of Anne is not performing well when compared to the ratios of the competitors. It can be seen

that the competitors of the business are earning more profits at a less expenditure. The current

assets of these businesses are high in comparison to Anne's business. This creates a bad condition

for the business as it impacts the short term liquidity positions of the business (Yang, 2021). But

Anne's asset employment is better than most of the businesses which creates better hope for the

business.

b) Explain the impact of Covid-19 on the profits of the business

The Covid-19 pandemic has created chaos among the world and particularly in the business

world as the businesses, to cut the costs, reduced their production in the times of uncertainty

(Heister, Kaufman, and Yuthas, 2021). The business in the case have seen greater losses in the

business due to reduced demand in the marketplace. The decrease in the market interactions of

the business of Anne have decreased their sales revenue and in turn its profits have turned into

losses. It is advised to Anne that she should focus on covering up these losses in the year 2021 if

she wants to reach no profit-no loss condition. After that she can work on the production and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales of the business to earn a little profit in the year 2022. The ratio investigation of fo Anne

displays the concern is handling in various losing and the concern has to focus on delivery

behind its operating cost. So, it can be terminated from the preceding discourse that Anne should

retool the concern scheme that they are having and direction on amended keeping in the market.

CONCLUSION

The above-mentioned report can be concluded by mentioning that accounting transactions

recording is an important aspect in the field of business as these helps the business to determine

the profits and financial performance of the business. The above report shows recordings of

different business transactions in the books of accounts and then summarising these in the

financial statements of the business. It also highlights the ratio analysis following the

interpretation of the these.

displays the concern is handling in various losing and the concern has to focus on delivery

behind its operating cost. So, it can be terminated from the preceding discourse that Anne should

retool the concern scheme that they are having and direction on amended keeping in the market.

CONCLUSION

The above-mentioned report can be concluded by mentioning that accounting transactions

recording is an important aspect in the field of business as these helps the business to determine

the profits and financial performance of the business. The above report shows recordings of

different business transactions in the books of accounts and then summarising these in the

financial statements of the business. It also highlights the ratio analysis following the

interpretation of the these.

REFERENCES

Books and Journals

PURI, N. and SINGH, H., 2021. Current Trends in Finance in the Context of Adoption of

Principle-Based Accounting Standards in Accounting Education. Financial Intelligence

in Human Resources Management: New Directions and Applications for Industry 4.0.

Daud, Z.M., Sudrajat, J., Maryani, D. and Effendi, M.S., 2021, August. Android-Based Online

Inventory Information System Design for Micro, Small and Medium Enterprises

(MSMEs). In 2021 IEEE International Conference on Electronic Technology,

Communication and Information (ICETCI) (pp. 366-371). IEEE.

Yang, J., 2021, March. Network Security and Prevention of Accounting Information System in

the Era of Big Data. In The International Conference on Cyber Security Intelligence

and Analytics (pp. 856-860). Springer, Cham.

Heister, S., Kaufman, M. and Yuthas, K., 2021. Blockchain and the Future of Business Data

Analytics. Journal of Emerging Technologies in Accounting. 18(1). pp.87-98.

Books and Journals

PURI, N. and SINGH, H., 2021. Current Trends in Finance in the Context of Adoption of

Principle-Based Accounting Standards in Accounting Education. Financial Intelligence

in Human Resources Management: New Directions and Applications for Industry 4.0.

Daud, Z.M., Sudrajat, J., Maryani, D. and Effendi, M.S., 2021, August. Android-Based Online

Inventory Information System Design for Micro, Small and Medium Enterprises

(MSMEs). In 2021 IEEE International Conference on Electronic Technology,

Communication and Information (ICETCI) (pp. 366-371). IEEE.

Yang, J., 2021, March. Network Security and Prevention of Accounting Information System in

the Era of Big Data. In The International Conference on Cyber Security Intelligence

and Analytics (pp. 856-860). Springer, Cham.

Heister, S., Kaufman, M. and Yuthas, K., 2021. Blockchain and the Future of Business Data

Analytics. Journal of Emerging Technologies in Accounting. 18(1). pp.87-98.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.