Recording Business Transactions: Journal Entries, Ledgers, Trial Balance, Income Statement and Balance Sheet

VerifiedAdded on 2023/06/14

|14

|2084

|398

AI Summary

This report includes the preparation of financial statements which start from passing journal entries, preparing ledger accounts, trial balance, profitability statement and balance sheet of Anne York who is a businesswoman and running a business of furniture. Calculation of ratios are also included in this report. Interpretation of ratios is done considering competitor and COVID-19 impact on the entity.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transaction

Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

Assessment II...................................................................................................................................1

Part A...............................................................................................................................................1

(a) Journal books including the record of business transactions. ...............................................1

(b) Ledgers Accounts of Anne York Business............................................................................3

(c) Preparation of Trial Balance as on 31st October 2021..........................................................7

(d) Income Statement for the period ended 31st October 2021..................................................7

(e) Statement of Financial Position.............................................................................................8

(f) Letter addressed to Anne........................................................................................................9

PART B............................................................................................................................................9

(a) Calculation of Accounting Ratios of Anne Business: -.........................................................9

(b) Interpretation of ratios calculated above considering competitor and covid 19 impact on

the entity......................................................................................................................................9

CONCLUSION..............................................................................................................................10

References:.....................................................................................................................................11

INTRODUCTION...........................................................................................................................1

Assessment II...................................................................................................................................1

Part A...............................................................................................................................................1

(a) Journal books including the record of business transactions. ...............................................1

(b) Ledgers Accounts of Anne York Business............................................................................3

(c) Preparation of Trial Balance as on 31st October 2021..........................................................7

(d) Income Statement for the period ended 31st October 2021..................................................7

(e) Statement of Financial Position.............................................................................................8

(f) Letter addressed to Anne........................................................................................................9

PART B............................................................................................................................................9

(a) Calculation of Accounting Ratios of Anne Business: -.........................................................9

(b) Interpretation of ratios calculated above considering competitor and covid 19 impact on

the entity......................................................................................................................................9

CONCLUSION..............................................................................................................................10

References:.....................................................................................................................................11

INTRODUCTION

Business transactions are defined as the activities of flow of money or products or

services in a business organisation which take place among two or more people. These

transactions are necessary for businesses to record them in the books and there are several steps

in the process of recording transactions which include journal entry, preparation of ledgers and

completion of books of account (Karamchandani and Srivastava 2020). This report include the

preparation of financial statements which start from passing journal entries, preparing ledger

accounts, trial balance, profitability statement and balance sheet of Anne york who is a

businesswoman and running a business of furniture. Along with this, it also include a letter

addressing to Anne which clarify her related to the drawings which had drawn from the funds of

business unit along with providing answer to her query which she has raised for holidays taken

by her. Calculation of ratios are also included in this report.

Assessment II

Part A

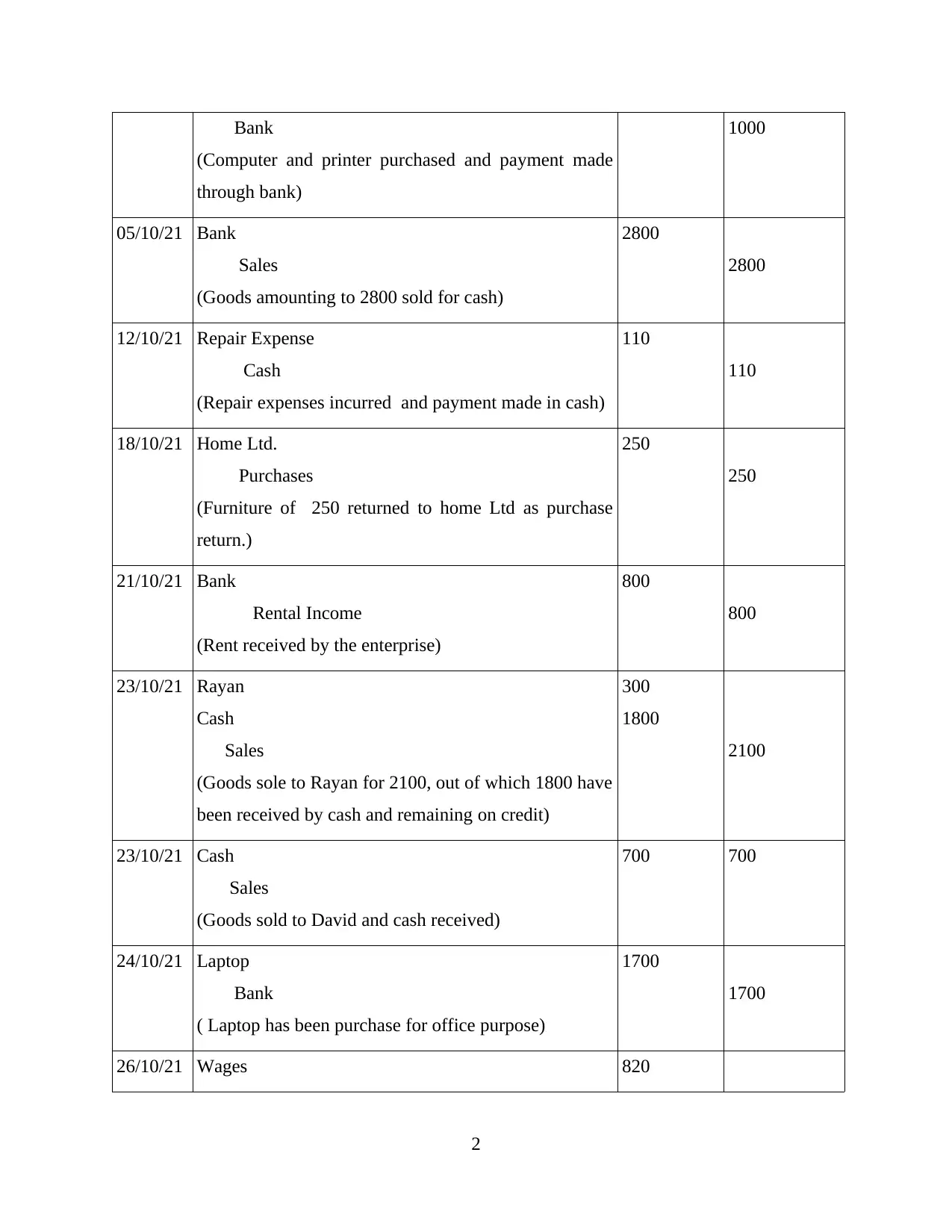

(a) Journal books including the record of business transactions.

JOURNAL ENTRIES IN BOOKS

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business started with bank, cash, flat and car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(Goods purchased on credit from Home Ltd.)

5400

5400

04/10/21 Computer

Printer

800

200

1

Business transactions are defined as the activities of flow of money or products or

services in a business organisation which take place among two or more people. These

transactions are necessary for businesses to record them in the books and there are several steps

in the process of recording transactions which include journal entry, preparation of ledgers and

completion of books of account (Karamchandani and Srivastava 2020). This report include the

preparation of financial statements which start from passing journal entries, preparing ledger

accounts, trial balance, profitability statement and balance sheet of Anne york who is a

businesswoman and running a business of furniture. Along with this, it also include a letter

addressing to Anne which clarify her related to the drawings which had drawn from the funds of

business unit along with providing answer to her query which she has raised for holidays taken

by her. Calculation of ratios are also included in this report.

Assessment II

Part A

(a) Journal books including the record of business transactions.

JOURNAL ENTRIES IN BOOKS

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business started with bank, cash, flat and car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(Goods purchased on credit from Home Ltd.)

5400

5400

04/10/21 Computer

Printer

800

200

1

Bank

(Computer and printer purchased and payment made

through bank)

1000

05/10/21 Bank

Sales

(Goods amounting to 2800 sold for cash)

2800

2800

12/10/21 Repair Expense

Cash

(Repair expenses incurred and payment made in cash)

110

110

18/10/21 Home Ltd.

Purchases

(Furniture of 250 returned to home Ltd as purchase

return.)

250

250

21/10/21 Bank

Rental Income

(Rent received by the enterprise)

800

800

23/10/21 Rayan

Cash

Sales

(Goods sole to Rayan for 2100, out of which 1800 have

been received by cash and remaining on credit)

300

1800

2100

23/10/21 Cash

Sales

(Goods sold to David and cash received)

700 700

24/10/21 Laptop

Bank

( Laptop has been purchase for office purpose)

1700

1700

26/10/21 Wages 820

2

(Computer and printer purchased and payment made

through bank)

1000

05/10/21 Bank

Sales

(Goods amounting to 2800 sold for cash)

2800

2800

12/10/21 Repair Expense

Cash

(Repair expenses incurred and payment made in cash)

110

110

18/10/21 Home Ltd.

Purchases

(Furniture of 250 returned to home Ltd as purchase

return.)

250

250

21/10/21 Bank

Rental Income

(Rent received by the enterprise)

800

800

23/10/21 Rayan

Cash

Sales

(Goods sole to Rayan for 2100, out of which 1800 have

been received by cash and remaining on credit)

300

1800

2100

23/10/21 Cash

Sales

(Goods sold to David and cash received)

700 700

24/10/21 Laptop

Bank

( Laptop has been purchase for office purpose)

1700

1700

26/10/21 Wages 820

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Bank

(Payment made to shopkeeper in cash amounting to

820 as wages)

820

30/10/21 Rent Expenses

Bank

(An office premises being rented by entity for which

rent has been paid for cash)

850

850

31/10/21 Drawings

Bank

(Amount withdraw from the business for personal use

by the proprietor)

1200

1200

31/10/21 Cash

Rayan

(Rayan a debtor of organisation of the entity paid their

debt)

150

150

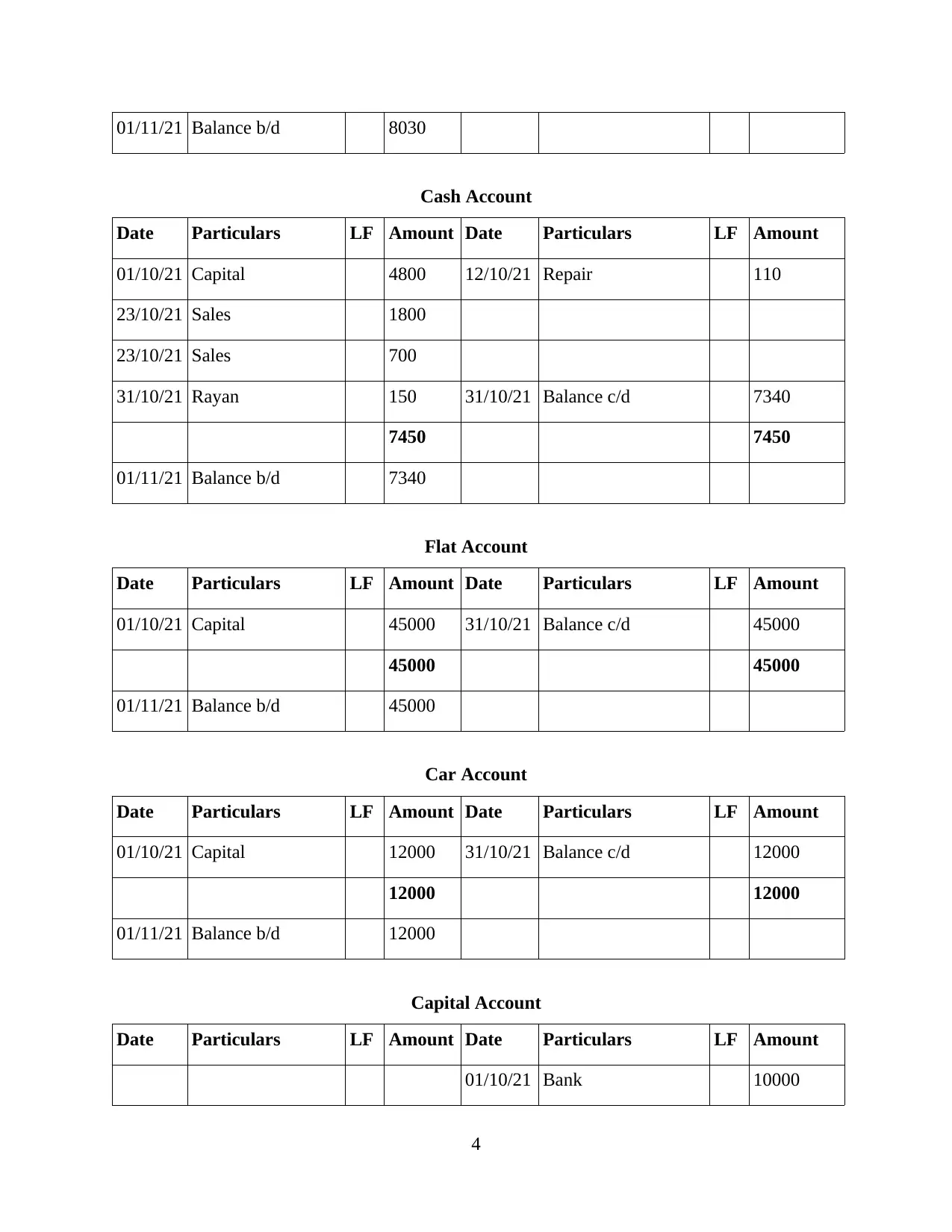

(b) Ledgers Accounts of Anne York Business

Bank Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

3

(Payment made to shopkeeper in cash amounting to

820 as wages)

820

30/10/21 Rent Expenses

Bank

(An office premises being rented by entity for which

rent has been paid for cash)

850

850

31/10/21 Drawings

Bank

(Amount withdraw from the business for personal use

by the proprietor)

1200

1200

31/10/21 Cash

Rayan

(Rayan a debtor of organisation of the entity paid their

debt)

150

150

(b) Ledgers Accounts of Anne York Business

Bank Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

3

01/11/21 Balance b/d 8030

Cash Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 4800 12/10/21 Repair 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

7450 7450

01/11/21 Balance b/d 7340

Flat Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

01/11/21 Balance b/d 45000

Car Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

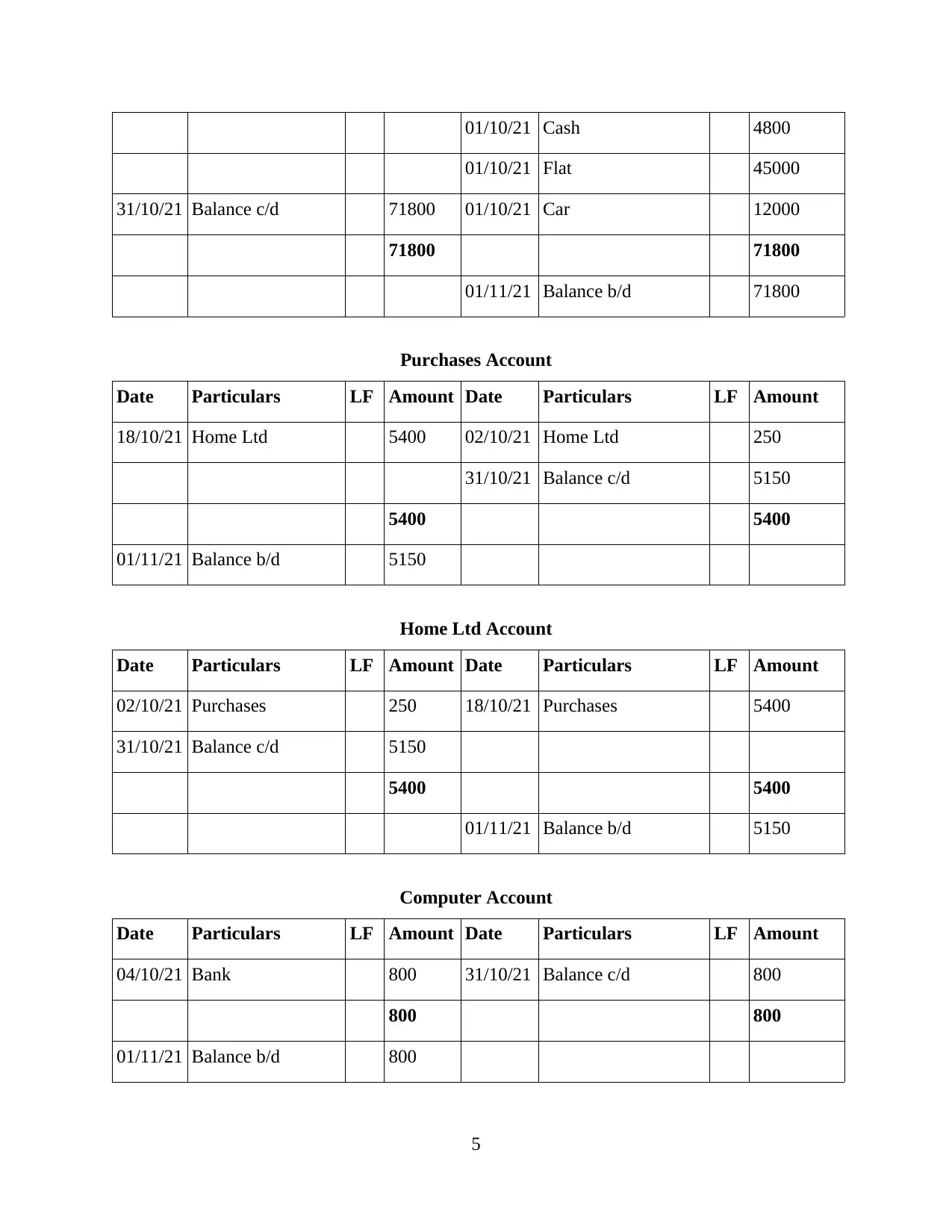

Capital Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Bank 10000

4

Cash Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 4800 12/10/21 Repair 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

7450 7450

01/11/21 Balance b/d 7340

Flat Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

01/11/21 Balance b/d 45000

Car Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

Capital Account

Date Particulars LF Amount Date Particulars LF Amount

01/10/21 Bank 10000

4

01/10/21 Cash 4800

01/10/21 Flat 45000

31/10/21 Balance c/d 71800 01/10/21 Car 12000

71800 71800

01/11/21 Balance b/d 71800

Purchases Account

Date Particulars LF Amount Date Particulars LF Amount

18/10/21 Home Ltd 5400 02/10/21 Home Ltd 250

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Home Ltd Account

Date Particulars LF Amount Date Particulars LF Amount

02/10/21 Purchases 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars LF Amount Date Particulars LF Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

5

01/10/21 Flat 45000

31/10/21 Balance c/d 71800 01/10/21 Car 12000

71800 71800

01/11/21 Balance b/d 71800

Purchases Account

Date Particulars LF Amount Date Particulars LF Amount

18/10/21 Home Ltd 5400 02/10/21 Home Ltd 250

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Home Ltd Account

Date Particulars LF Amount Date Particulars LF Amount

02/10/21 Purchases 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars LF Amount Date Particulars LF Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Printer Account

Date Particulars LF Amount Date Particulars LF Amount

04/10/21 Bank 200 31/10/21 Balance c/d 200

200 200

01/11/21 Balance b/d 200

Repair Account

Date Particulars LF Amount Date Particulars LF Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars LF Amount Date Particulars LF Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Rayan Account

Date Particulars LF Amount Date Particulars LF Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

6

Date Particulars LF Amount Date Particulars LF Amount

04/10/21 Bank 200 31/10/21 Balance c/d 200

200 200

01/11/21 Balance b/d 200

Repair Account

Date Particulars LF Amount Date Particulars LF Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars LF Amount Date Particulars LF Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Rayan Account

Date Particulars LF Amount Date Particulars LF Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

6

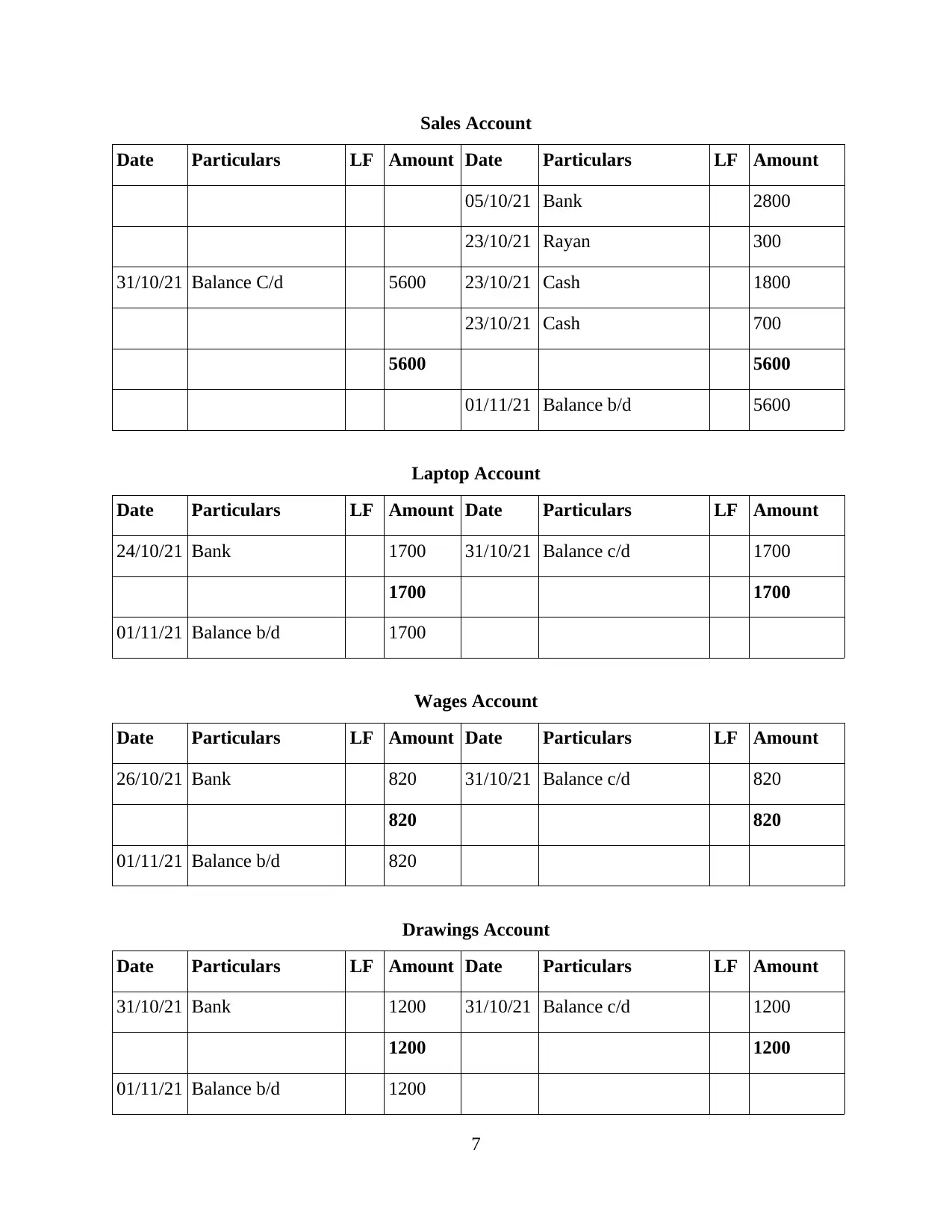

Sales Account

Date Particulars LF Amount Date Particulars LF Amount

05/10/21 Bank 2800

23/10/21 Rayan 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars LF Amount Date Particulars LF Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars LF Amount Date Particulars LF Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars LF Amount Date Particulars LF Amount

31/10/21 Bank 1200 31/10/21 Balance c/d 1200

1200 1200

01/11/21 Balance b/d 1200

7

Date Particulars LF Amount Date Particulars LF Amount

05/10/21 Bank 2800

23/10/21 Rayan 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars LF Amount Date Particulars LF Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars LF Amount Date Particulars LF Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars LF Amount Date Particulars LF Amount

31/10/21 Bank 1200 31/10/21 Balance c/d 1200

1200 1200

01/11/21 Balance b/d 1200

7

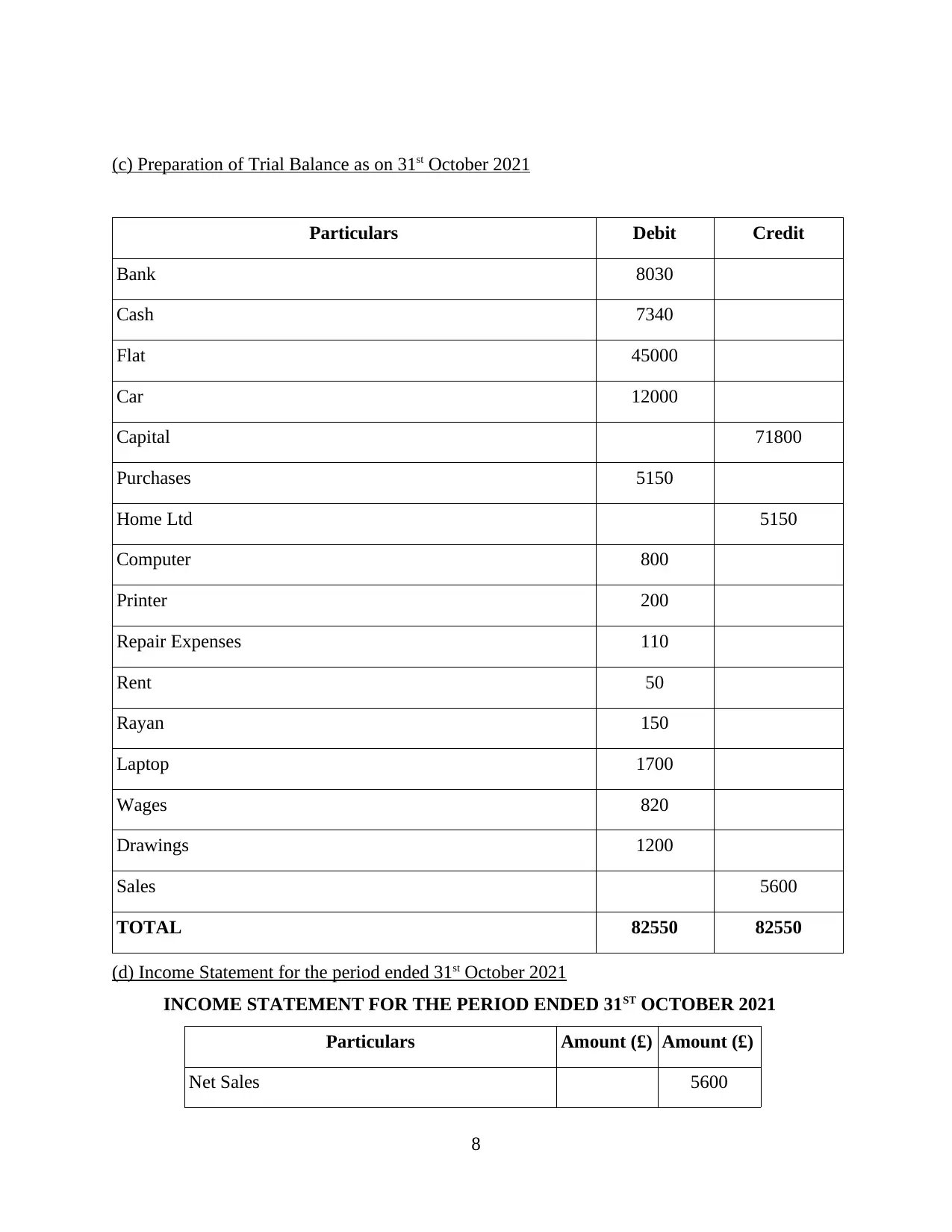

(c) Preparation of Trial Balance as on 31st October 2021

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5150

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Rayan 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTAL 82550 82550

(d) Income Statement for the period ended 31st October 2021

INCOME STATEMENT FOR THE PERIOD ENDED 31ST OCTOBER 2021

Particulars Amount (£) Amount (£)

Net Sales 5600

8

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5150

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Rayan 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTAL 82550 82550

(d) Income Statement for the period ended 31st October 2021

INCOME STATEMENT FOR THE PERIOD ENDED 31ST OCTOBER 2021

Particulars Amount (£) Amount (£)

Net Sales 5600

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

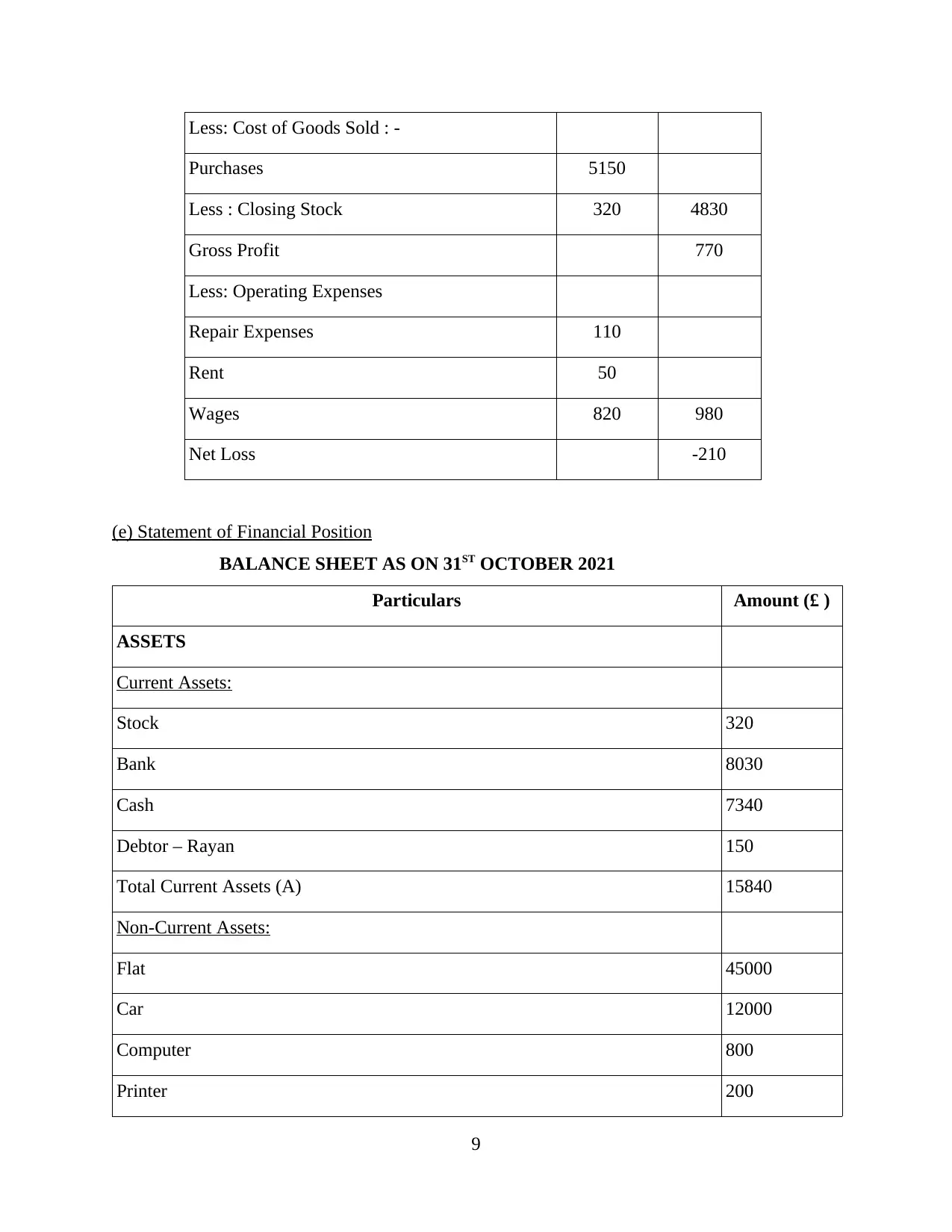

Less: Cost of Goods Sold : -

Purchases 5150

Less : Closing Stock 320 4830

Gross Profit 770

Less: Operating Expenses

Repair Expenses 110

Rent 50

Wages 820 980

Net Loss -210

(e) Statement of Financial Position

BALANCE SHEET AS ON 31ST OCTOBER 2021

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

Debtor – Rayan 150

Total Current Assets (A) 15840

Non-Current Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

9

Purchases 5150

Less : Closing Stock 320 4830

Gross Profit 770

Less: Operating Expenses

Repair Expenses 110

Rent 50

Wages 820 980

Net Loss -210

(e) Statement of Financial Position

BALANCE SHEET AS ON 31ST OCTOBER 2021

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

Debtor – Rayan 150

Total Current Assets (A) 15840

Non-Current Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

9

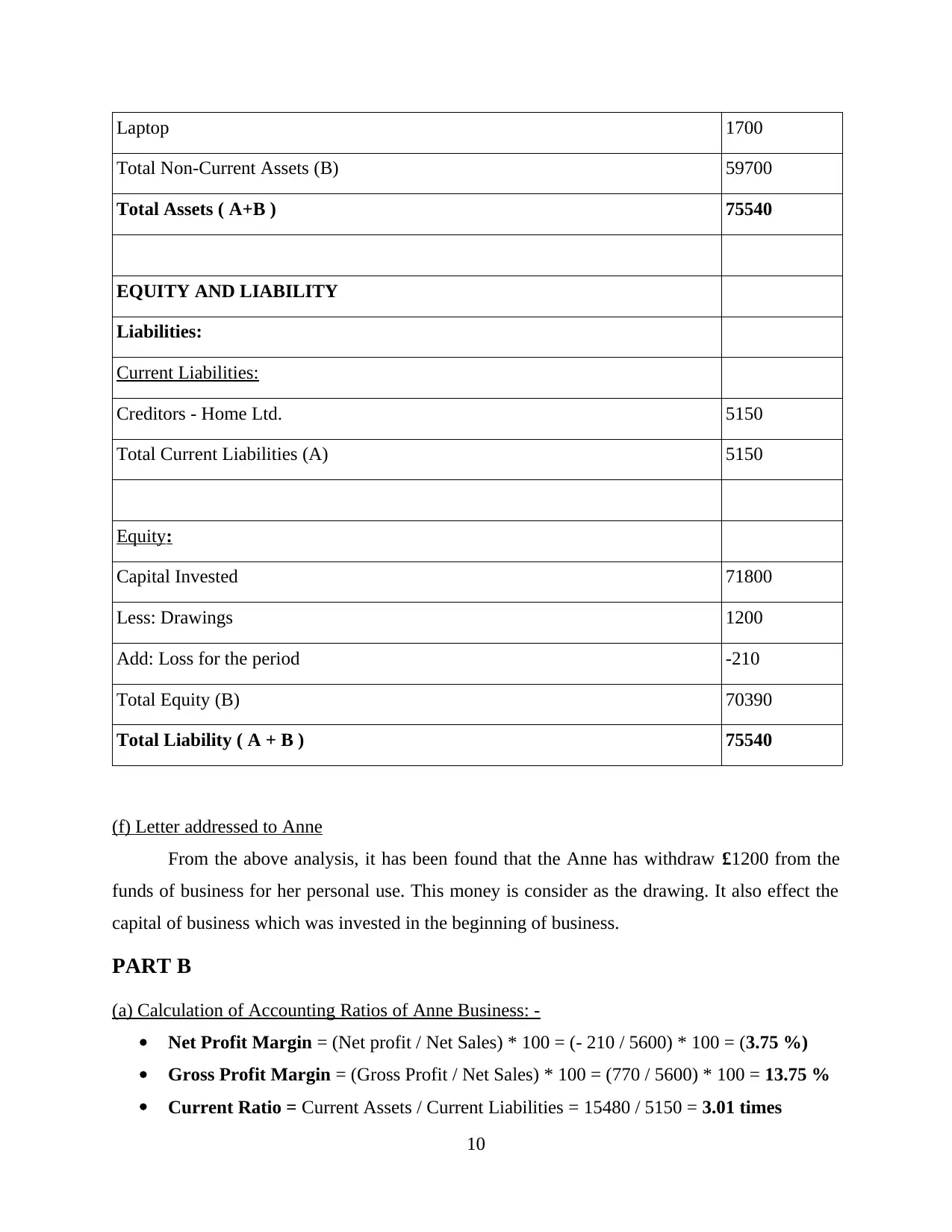

Laptop 1700

Total Non-Current Assets (B) 59700

Total Assets ( A+B ) 75540

EQUITY AND LIABILITY

Liabilities:

Current Liabilities:

Creditors - Home Ltd. 5150

Total Current Liabilities (A) 5150

Equity:

Capital Invested 71800

Less: Drawings 1200

Add: Loss for the period -210

Total Equity (B) 70390

Total Liability ( A + B ) 75540

(f) Letter addressed to Anne

From the above analysis, it has been found that the Anne has withdraw £1200 from the

funds of business for her personal use. This money is consider as the drawing. It also effect the

capital of business which was invested in the beginning of business.

PART B

(a) Calculation of Accounting Ratios of Anne Business: -

Net Profit Margin = (Net profit / Net Sales) * 100 = (- 210 / 5600) * 100 = (3.75 %)

Gross Profit Margin = (Gross Profit / Net Sales) * 100 = (770 / 5600) * 100 = 13.75 %

Current Ratio = Current Assets / Current Liabilities = 15480 / 5150 = 3.01 times

10

Total Non-Current Assets (B) 59700

Total Assets ( A+B ) 75540

EQUITY AND LIABILITY

Liabilities:

Current Liabilities:

Creditors - Home Ltd. 5150

Total Current Liabilities (A) 5150

Equity:

Capital Invested 71800

Less: Drawings 1200

Add: Loss for the period -210

Total Equity (B) 70390

Total Liability ( A + B ) 75540

(f) Letter addressed to Anne

From the above analysis, it has been found that the Anne has withdraw £1200 from the

funds of business for her personal use. This money is consider as the drawing. It also effect the

capital of business which was invested in the beginning of business.

PART B

(a) Calculation of Accounting Ratios of Anne Business: -

Net Profit Margin = (Net profit / Net Sales) * 100 = (- 210 / 5600) * 100 = (3.75 %)

Gross Profit Margin = (Gross Profit / Net Sales) * 100 = (770 / 5600) * 100 = 13.75 %

Current Ratio = Current Assets / Current Liabilities = 15480 / 5150 = 3.01 times

10

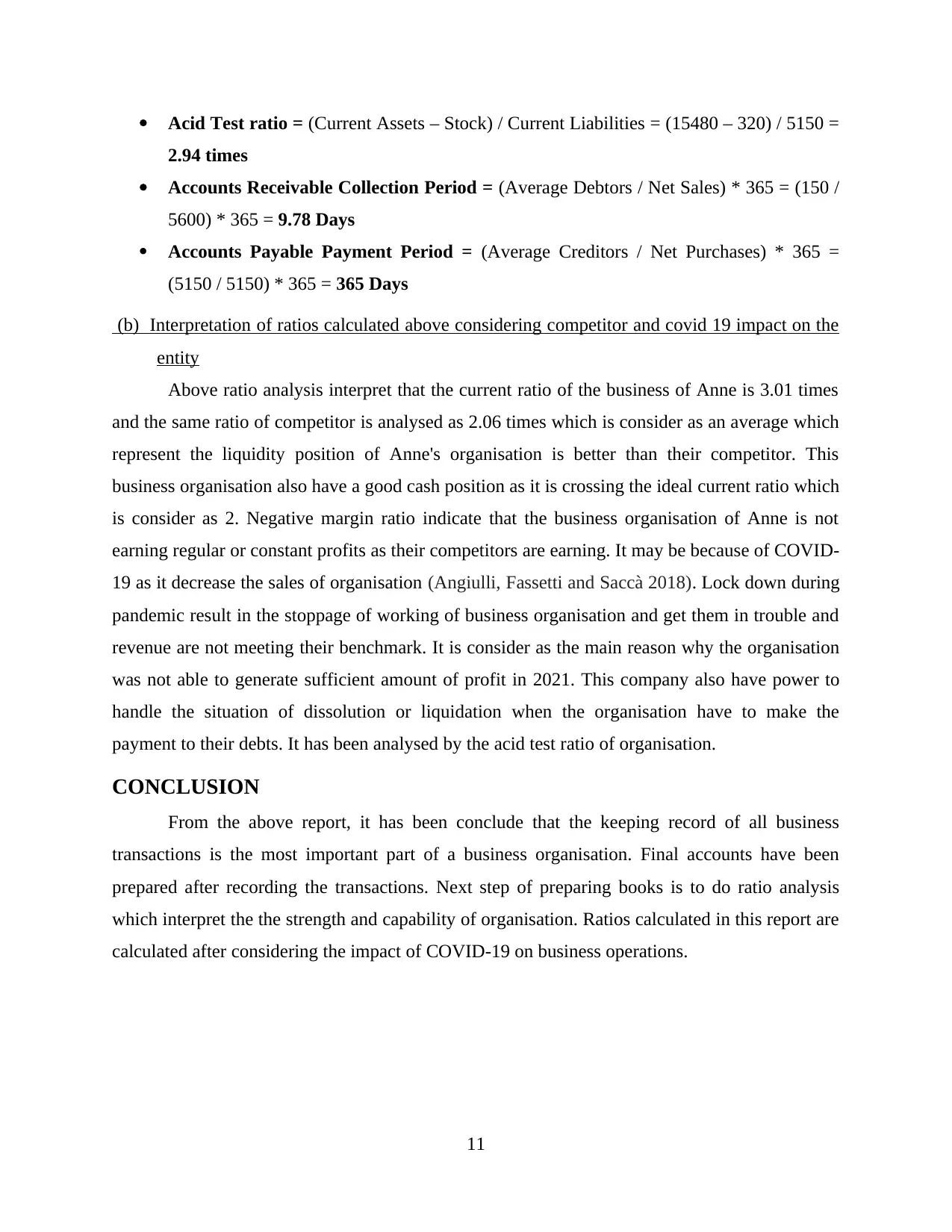

Acid Test ratio = (Current Assets – Stock) / Current Liabilities = (15480 – 320) / 5150 =

2.94 times

Accounts Receivable Collection Period = (Average Debtors / Net Sales) * 365 = (150 /

5600) * 365 = 9.78 Days

Accounts Payable Payment Period = (Average Creditors / Net Purchases) * 365 =

(5150 / 5150) * 365 = 365 Days

(b) Interpretation of ratios calculated above considering competitor and covid 19 impact on the

entity

Above ratio analysis interpret that the current ratio of the business of Anne is 3.01 times

and the same ratio of competitor is analysed as 2.06 times which is consider as an average which

represent the liquidity position of Anne's organisation is better than their competitor. This

business organisation also have a good cash position as it is crossing the ideal current ratio which

is consider as 2. Negative margin ratio indicate that the business organisation of Anne is not

earning regular or constant profits as their competitors are earning. It may be because of COVID-

19 as it decrease the sales of organisation (Angiulli, Fassetti and Saccà 2018). Lock down during

pandemic result in the stoppage of working of business organisation and get them in trouble and

revenue are not meeting their benchmark. It is consider as the main reason why the organisation

was not able to generate sufficient amount of profit in 2021. This company also have power to

handle the situation of dissolution or liquidation when the organisation have to make the

payment to their debts. It has been analysed by the acid test ratio of organisation.

CONCLUSION

From the above report, it has been conclude that the keeping record of all business

transactions is the most important part of a business organisation. Final accounts have been

prepared after recording the transactions. Next step of preparing books is to do ratio analysis

which interpret the the strength and capability of organisation. Ratios calculated in this report are

calculated after considering the impact of COVID-19 on business operations.

11

2.94 times

Accounts Receivable Collection Period = (Average Debtors / Net Sales) * 365 = (150 /

5600) * 365 = 9.78 Days

Accounts Payable Payment Period = (Average Creditors / Net Purchases) * 365 =

(5150 / 5150) * 365 = 365 Days

(b) Interpretation of ratios calculated above considering competitor and covid 19 impact on the

entity

Above ratio analysis interpret that the current ratio of the business of Anne is 3.01 times

and the same ratio of competitor is analysed as 2.06 times which is consider as an average which

represent the liquidity position of Anne's organisation is better than their competitor. This

business organisation also have a good cash position as it is crossing the ideal current ratio which

is consider as 2. Negative margin ratio indicate that the business organisation of Anne is not

earning regular or constant profits as their competitors are earning. It may be because of COVID-

19 as it decrease the sales of organisation (Angiulli, Fassetti and Saccà 2018). Lock down during

pandemic result in the stoppage of working of business organisation and get them in trouble and

revenue are not meeting their benchmark. It is consider as the main reason why the organisation

was not able to generate sufficient amount of profit in 2021. This company also have power to

handle the situation of dissolution or liquidation when the organisation have to make the

payment to their debts. It has been analysed by the acid test ratio of organisation.

CONCLUSION

From the above report, it has been conclude that the keeping record of all business

transactions is the most important part of a business organisation. Final accounts have been

prepared after recording the transactions. Next step of preparing books is to do ratio analysis

which interpret the the strength and capability of organisation. Ratios calculated in this report are

calculated after considering the impact of COVID-19 on business operations.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

Books and Journals

Angiulli, F., Fassetti, F., and Saccà, D., 2018, June. Achieving service accountability through

blockchain and digital identity. In International Conference on Advanced Information

Systems Engineering (pp. 16-23). Springer, Cham.

Karamchandani, A., and Srivastava, R.K., 2020. Perception-based model for analyzing the

impact of enterprise blockchain adoption on SCM in the Indian service

industry. International Journal of Information Management. 52. p.102019.

Menna, F., Agrafiotis, P. and Georgopoulos, A., 2018. State of the art and applications in

archaeological underwater 3D recording and mapping. Journal of Cultural

Heritage. 33. pp.231-248.

Müßigmann, B., von der Gracht, H. and Hartmann, E., 2020. Blockchain technology in

logistics and supply chain management—A bibliometric literature review from 2016

to January 2020. IEEE Transactions on Engineering Management. 67(4). pp.988-

1007.

Pasala, S., Pavani, V., and Narayana, V.L., 2020. Identification of attackers using blockchain

transactions using cryptography methods. Journal of Critical Reviews. 7(6). pp.368-

375.

Perez, M.R.L., Gerardo, B. and Medina, R., 2018, November. Modified sha256 for securing

online transactions based on blockchain mechanism. In 2018 IEEE 10th International

Conference on Humanoid, Nanotechnology, Information Technology, Communication

and Control, Environment and Management (HNICEM) (pp. 1-5). IEEE.

Rimba, P., Tran, A.B., and Xu, X., 2020. Quantifying the cost of distrust: Comparing

blockchain and cloud services for business process execution. Information Systems

Frontiers. 22(2). pp.489-507.

12

Books and Journals

Angiulli, F., Fassetti, F., and Saccà, D., 2018, June. Achieving service accountability through

blockchain and digital identity. In International Conference on Advanced Information

Systems Engineering (pp. 16-23). Springer, Cham.

Karamchandani, A., and Srivastava, R.K., 2020. Perception-based model for analyzing the

impact of enterprise blockchain adoption on SCM in the Indian service

industry. International Journal of Information Management. 52. p.102019.

Menna, F., Agrafiotis, P. and Georgopoulos, A., 2018. State of the art and applications in

archaeological underwater 3D recording and mapping. Journal of Cultural

Heritage. 33. pp.231-248.

Müßigmann, B., von der Gracht, H. and Hartmann, E., 2020. Blockchain technology in

logistics and supply chain management—A bibliometric literature review from 2016

to January 2020. IEEE Transactions on Engineering Management. 67(4). pp.988-

1007.

Pasala, S., Pavani, V., and Narayana, V.L., 2020. Identification of attackers using blockchain

transactions using cryptography methods. Journal of Critical Reviews. 7(6). pp.368-

375.

Perez, M.R.L., Gerardo, B. and Medina, R., 2018, November. Modified sha256 for securing

online transactions based on blockchain mechanism. In 2018 IEEE 10th International

Conference on Humanoid, Nanotechnology, Information Technology, Communication

and Control, Environment and Management (HNICEM) (pp. 1-5). IEEE.

Rimba, P., Tran, A.B., and Xu, X., 2020. Quantifying the cost of distrust: Comparing

blockchain and cloud services for business process execution. Information Systems

Frontiers. 22(2). pp.489-507.

12

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.