Recording Business Transactions: Journal Entries, General Ledgers, Trial Balance, Income Statement, and Balance Sheet

VerifiedAdded on 2023/06/12

|18

|2423

|210

AI Summary

This report explains the process of recording business transactions through journal entries, preparing general ledgers, trial balance, income statement, and balance sheet. It also includes a letter explaining the reasons behind drawings made by Anne, calculation of accounting ratios, and the impact of COVID-19 on business profits. The report provides useful guidance for effective planning and handling of issues and problems.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RECORDING

BUSINESS

TRANSACTIONS

BUSINESS

TRANSACTIONS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

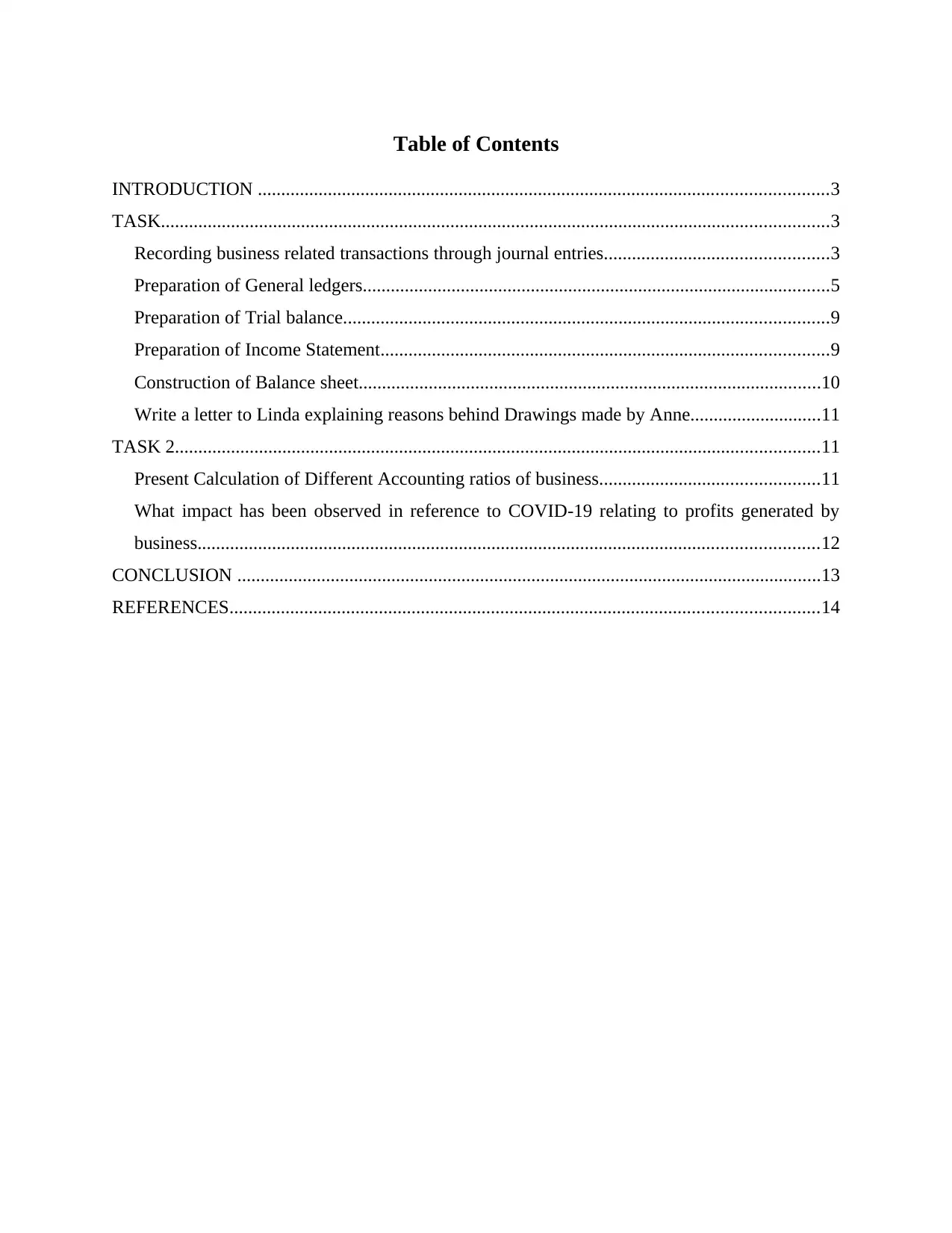

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

Recording business related transactions through journal entries................................................3

Preparation of General ledgers....................................................................................................5

Preparation of Trial balance........................................................................................................9

Preparation of Income Statement................................................................................................9

Construction of Balance sheet...................................................................................................10

Write a letter to Linda explaining reasons behind Drawings made by Anne............................11

TASK 2..........................................................................................................................................11

Present Calculation of Different Accounting ratios of business...............................................11

What impact has been observed in reference to COVID-19 relating to profits generated by

business.....................................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

TASK...............................................................................................................................................3

Recording business related transactions through journal entries................................................3

Preparation of General ledgers....................................................................................................5

Preparation of Trial balance........................................................................................................9

Preparation of Income Statement................................................................................................9

Construction of Balance sheet...................................................................................................10

Write a letter to Linda explaining reasons behind Drawings made by Anne............................11

TASK 2..........................................................................................................................................11

Present Calculation of Different Accounting ratios of business...............................................11

What impact has been observed in reference to COVID-19 relating to profits generated by

business.....................................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The report prepared below reflects how business transactions helps in carrying out

activities and operations in a company (Burke, 2019). It can be defined as a process that involves

various steps such as at initial step it explains examining of transactions occurred and in what

ways they are going to affect the organisation. Further it involves which accounts must be

credited and what must be debited. It also explains basic accounting procedure that determines

nature of transactions so far recorded. Transactions are said to be recorded in form of journals

that help to have a clearer picture as where the cash has been used and what are the areas that

contributed in generation of cash. It is helpful in preparation of financial records and statements

that reflect profit earned, revenue generated and incurred losses from transactions. Ratio analysis

also helps to calculate financial values through which useful interpretations could be made. It

also helps to examine the effect and impact observed by company due to unpredictable condition

of COVID-19. It also provides useful guidance that states ideas that would help to give effective

plans for handling such issues and problems (Lang and et.al., 2018).

TASK

Recording business related transactions through journal entries.

JOURNAL ENTRIES

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business commenced with Bank, cash, flat and car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(Purchase of furniture processed on credit from

Home Ltd.)

5400

5400

04/10/21 Computer 800

The report prepared below reflects how business transactions helps in carrying out

activities and operations in a company (Burke, 2019). It can be defined as a process that involves

various steps such as at initial step it explains examining of transactions occurred and in what

ways they are going to affect the organisation. Further it involves which accounts must be

credited and what must be debited. It also explains basic accounting procedure that determines

nature of transactions so far recorded. Transactions are said to be recorded in form of journals

that help to have a clearer picture as where the cash has been used and what are the areas that

contributed in generation of cash. It is helpful in preparation of financial records and statements

that reflect profit earned, revenue generated and incurred losses from transactions. Ratio analysis

also helps to calculate financial values through which useful interpretations could be made. It

also helps to examine the effect and impact observed by company due to unpredictable condition

of COVID-19. It also provides useful guidance that states ideas that would help to give effective

plans for handling such issues and problems (Lang and et.al., 2018).

TASK

Recording business related transactions through journal entries.

JOURNAL ENTRIES

Date Particulars Debit Credit

01/10/21 Bank

Cash

Flat

Car

Capital

(Business commenced with Bank, cash, flat and car)

10000

4800

45000

12000

71800

02/10/21 Purchases

Home Ltd

(Purchase of furniture processed on credit from

Home Ltd.)

5400

5400

04/10/21 Computer 800

Printer

Bank

(Purchase of computer and printer made in exchange

of cash)

200

1000

05/10/21 Bank

Sales

(Sale of goods being made for 2800)

2800

2800

12/10/21 Repair Expense

Cash

(Repair expenses charged for printer (Kim and et.al.,

2020)

110

110

18/10/21 Home Ltd.

Purchases

(Furniture retuned to Home Ltd. having Worth of

250)

250

250

21/10/21 Bank

Rent income

(Rent of 800 collected by company)

800

800

23/10/21 Rayan

Cash

Sales

(Sale of goods made to Rayan having worth 2100

where 1800 have been collected by organisation

(Massaro, 2021)

300

1800

2100

23/10/21 Cash

Sales

(Sale of goods made for cash to David)

700

700

24/10/21 Laptop

Bank

1700

1700

Bank

(Purchase of computer and printer made in exchange

of cash)

200

1000

05/10/21 Bank

Sales

(Sale of goods being made for 2800)

2800

2800

12/10/21 Repair Expense

Cash

(Repair expenses charged for printer (Kim and et.al.,

2020)

110

110

18/10/21 Home Ltd.

Purchases

(Furniture retuned to Home Ltd. having Worth of

250)

250

250

21/10/21 Bank

Rent income

(Rent of 800 collected by company)

800

800

23/10/21 Rayan

Cash

Sales

(Sale of goods made to Rayan having worth 2100

where 1800 have been collected by organisation

(Massaro, 2021)

300

1800

2100

23/10/21 Cash

Sales

(Sale of goods made for cash to David)

700

700

24/10/21 Laptop

Bank

1700

1700

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(New laptop being purchased by company for official

purposes)

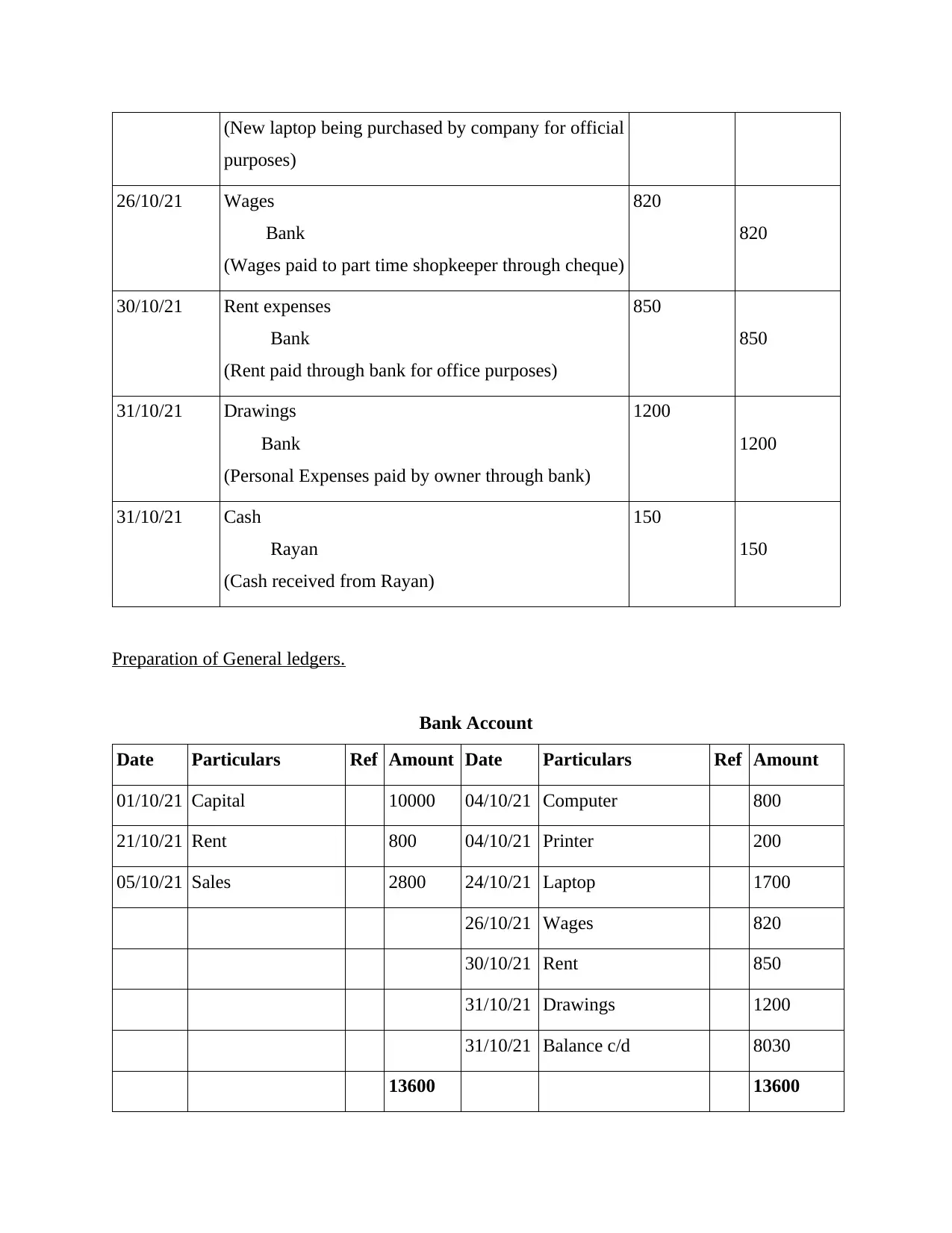

26/10/21 Wages

Bank

(Wages paid to part time shopkeeper through cheque)

820

820

30/10/21 Rent expenses

Bank

(Rent paid through bank for office purposes)

850

850

31/10/21 Drawings

Bank

(Personal Expenses paid by owner through bank)

1200

1200

31/10/21 Cash

Rayan

(Cash received from Rayan)

150

150

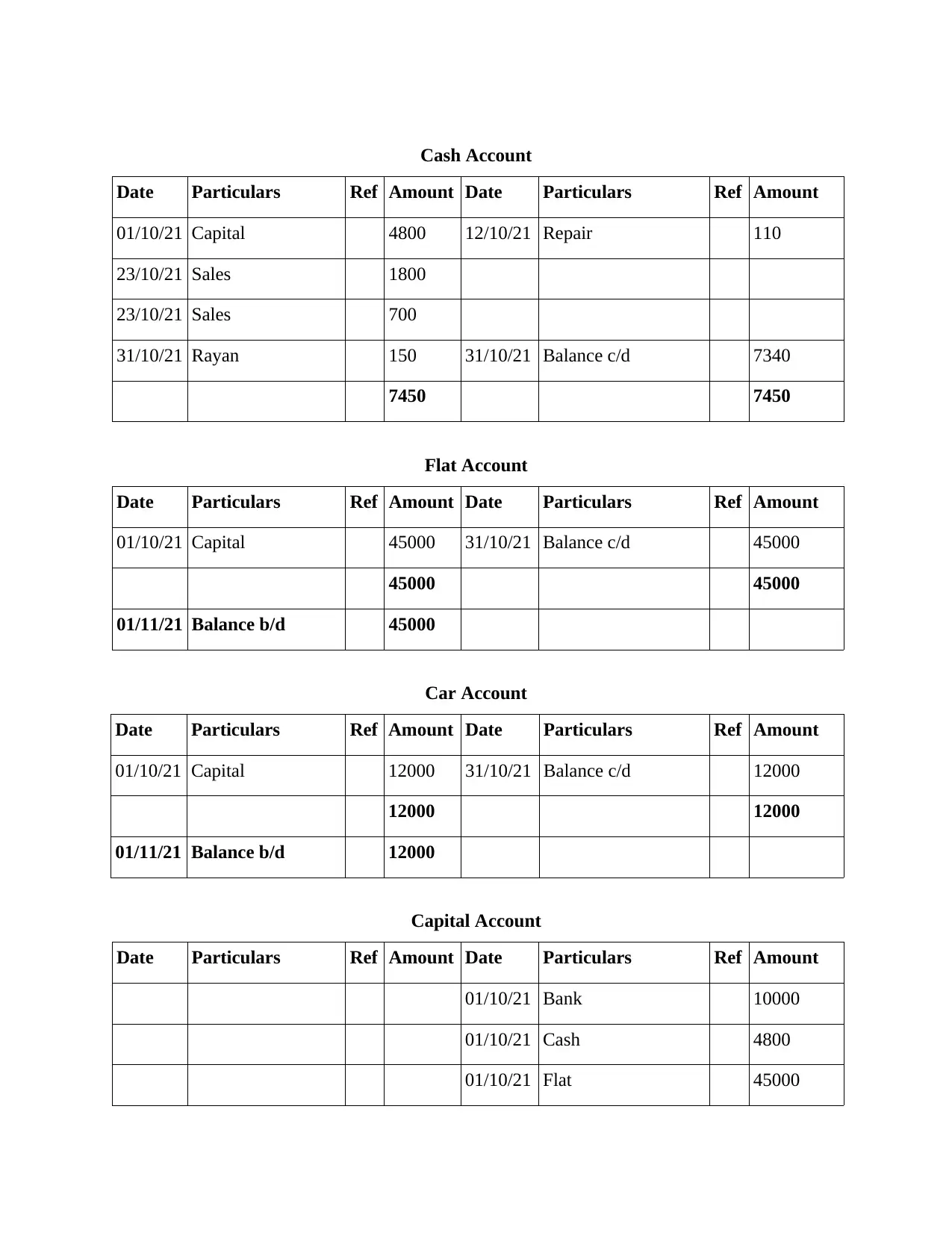

Preparation of General ledgers.

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

purposes)

26/10/21 Wages

Bank

(Wages paid to part time shopkeeper through cheque)

820

820

30/10/21 Rent expenses

Bank

(Rent paid through bank for office purposes)

850

850

31/10/21 Drawings

Bank

(Personal Expenses paid by owner through bank)

1200

1200

31/10/21 Cash

Rayan

(Cash received from Rayan)

150

150

Preparation of General ledgers.

Bank Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 10000 04/10/21 Computer 800

21/10/21 Rent 800 04/10/21 Printer 200

05/10/21 Sales 2800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

13600 13600

Cash Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 4800 12/10/21 Repair 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

7450 7450

Flat Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

01/11/21 Balance b/d 45000

Car Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Bank 10000

01/10/21 Cash 4800

01/10/21 Flat 45000

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 4800 12/10/21 Repair 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

7450 7450

Flat Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

45000 45000

01/11/21 Balance b/d 45000

Car Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

12000 12000

01/11/21 Balance b/d 12000

Capital Account

Date Particulars Ref Amount Date Particulars Ref Amount

01/10/21 Bank 10000

01/10/21 Cash 4800

01/10/21 Flat 45000

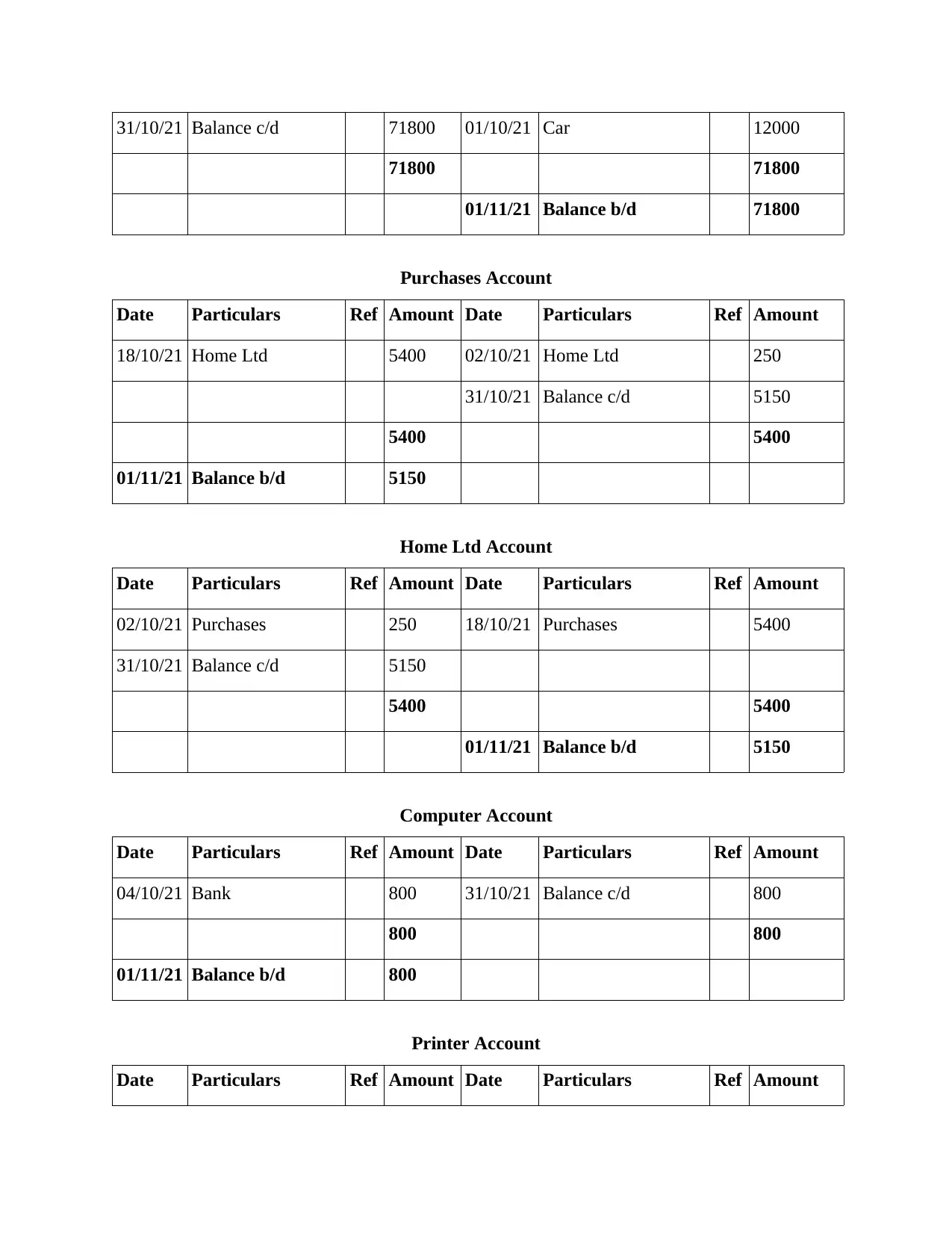

31/10/21 Balance c/d 71800 01/10/21 Car 12000

71800 71800

01/11/21 Balance b/d 71800

Purchases Account

Date Particulars Ref Amount Date Particulars Ref Amount

18/10/21 Home Ltd 5400 02/10/21 Home Ltd 250

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Home Ltd Account

Date Particulars Ref Amount Date Particulars Ref Amount

02/10/21 Purchases 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

Printer Account

Date Particulars Ref Amount Date Particulars Ref Amount

71800 71800

01/11/21 Balance b/d 71800

Purchases Account

Date Particulars Ref Amount Date Particulars Ref Amount

18/10/21 Home Ltd 5400 02/10/21 Home Ltd 250

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Home Ltd Account

Date Particulars Ref Amount Date Particulars Ref Amount

02/10/21 Purchases 250 18/10/21 Purchases 5400

31/10/21 Balance c/d 5150

5400 5400

01/11/21 Balance b/d 5150

Computer Account

Date Particulars Ref Amount Date Particulars Ref Amount

04/10/21 Bank 800 31/10/21 Balance c/d 800

800 800

01/11/21 Balance b/d 800

Printer Account

Date Particulars Ref Amount Date Particulars Ref Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

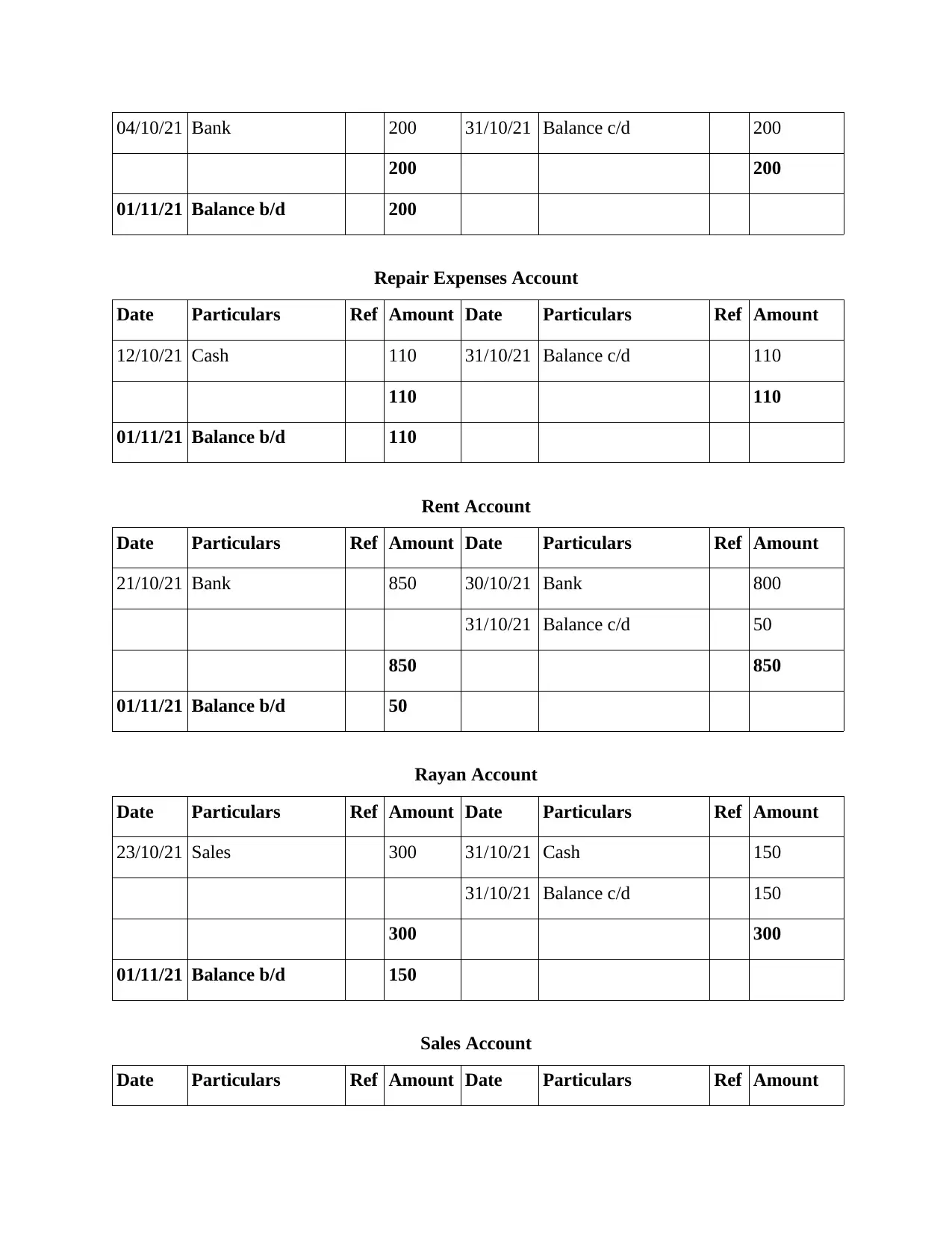

04/10/21 Bank 200 31/10/21 Balance c/d 200

200 200

01/11/21 Balance b/d 200

Repair Expenses Account

Date Particulars Ref Amount Date Particulars Ref Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars Ref Amount Date Particulars Ref Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Rayan Account

Date Particulars Ref Amount Date Particulars Ref Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

Sales Account

Date Particulars Ref Amount Date Particulars Ref Amount

200 200

01/11/21 Balance b/d 200

Repair Expenses Account

Date Particulars Ref Amount Date Particulars Ref Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

110 110

01/11/21 Balance b/d 110

Rent Account

Date Particulars Ref Amount Date Particulars Ref Amount

21/10/21 Bank 850 30/10/21 Bank 800

31/10/21 Balance c/d 50

850 850

01/11/21 Balance b/d 50

Rayan Account

Date Particulars Ref Amount Date Particulars Ref Amount

23/10/21 Sales 300 31/10/21 Cash 150

31/10/21 Balance c/d 150

300 300

01/11/21 Balance b/d 150

Sales Account

Date Particulars Ref Amount Date Particulars Ref Amount

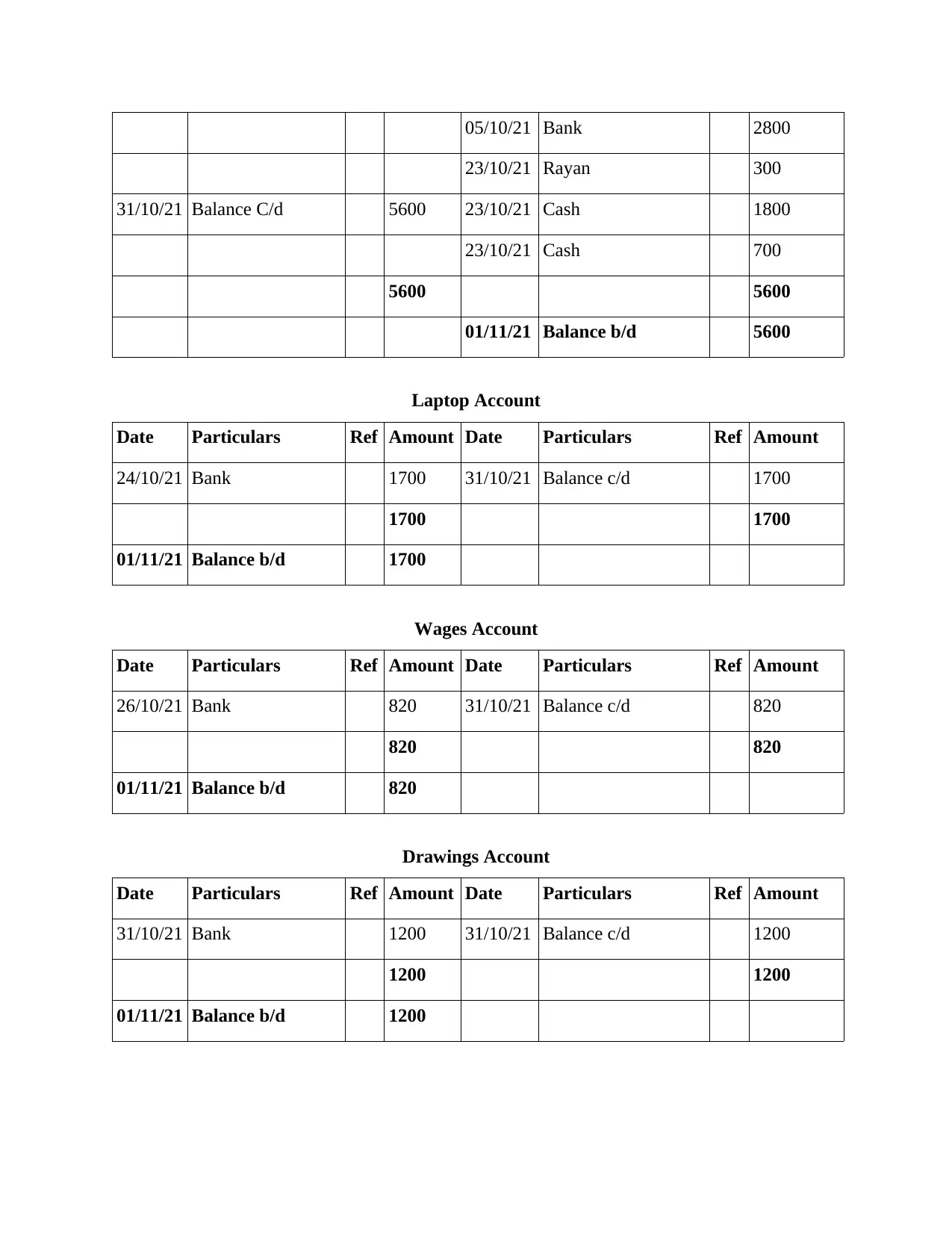

05/10/21 Bank 2800

23/10/21 Rayan 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars Ref Amount Date Particulars Ref Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars Ref Amount Date Particulars Ref Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/10/21 Bank 1200 31/10/21 Balance c/d 1200

1200 1200

01/11/21 Balance b/d 1200

23/10/21 Rayan 300

31/10/21 Balance C/d 5600 23/10/21 Cash 1800

23/10/21 Cash 700

5600 5600

01/11/21 Balance b/d 5600

Laptop Account

Date Particulars Ref Amount Date Particulars Ref Amount

24/10/21 Bank 1700 31/10/21 Balance c/d 1700

1700 1700

01/11/21 Balance b/d 1700

Wages Account

Date Particulars Ref Amount Date Particulars Ref Amount

26/10/21 Bank 820 31/10/21 Balance c/d 820

820 820

01/11/21 Balance b/d 820

Drawings Account

Date Particulars Ref Amount Date Particulars Ref Amount

31/10/21 Bank 1200 31/10/21 Balance c/d 1200

1200 1200

01/11/21 Balance b/d 1200

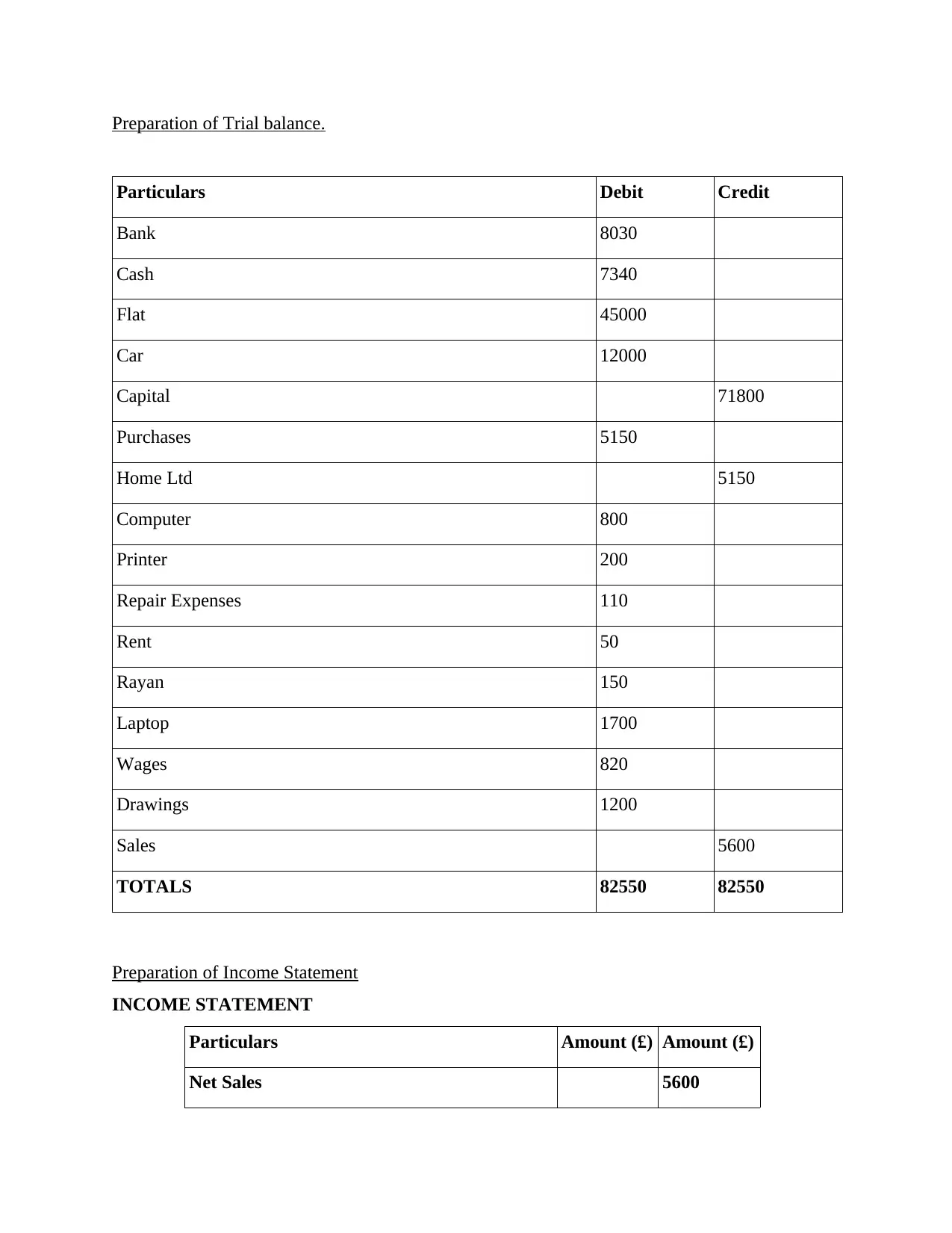

Preparation of Trial balance.

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5150

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Rayan 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTALS 82550 82550

Preparation of Income Statement

INCOME STATEMENT

Particulars Amount (£) Amount (£)

Net Sales 5600

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Purchases 5150

Home Ltd 5150

Computer 800

Printer 200

Repair Expenses 110

Rent 50

Rayan 150

Laptop 1700

Wages 820

Drawings 1200

Sales 5600

TOTALS 82550 82550

Preparation of Income Statement

INCOME STATEMENT

Particulars Amount (£) Amount (£)

Net Sales 5600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

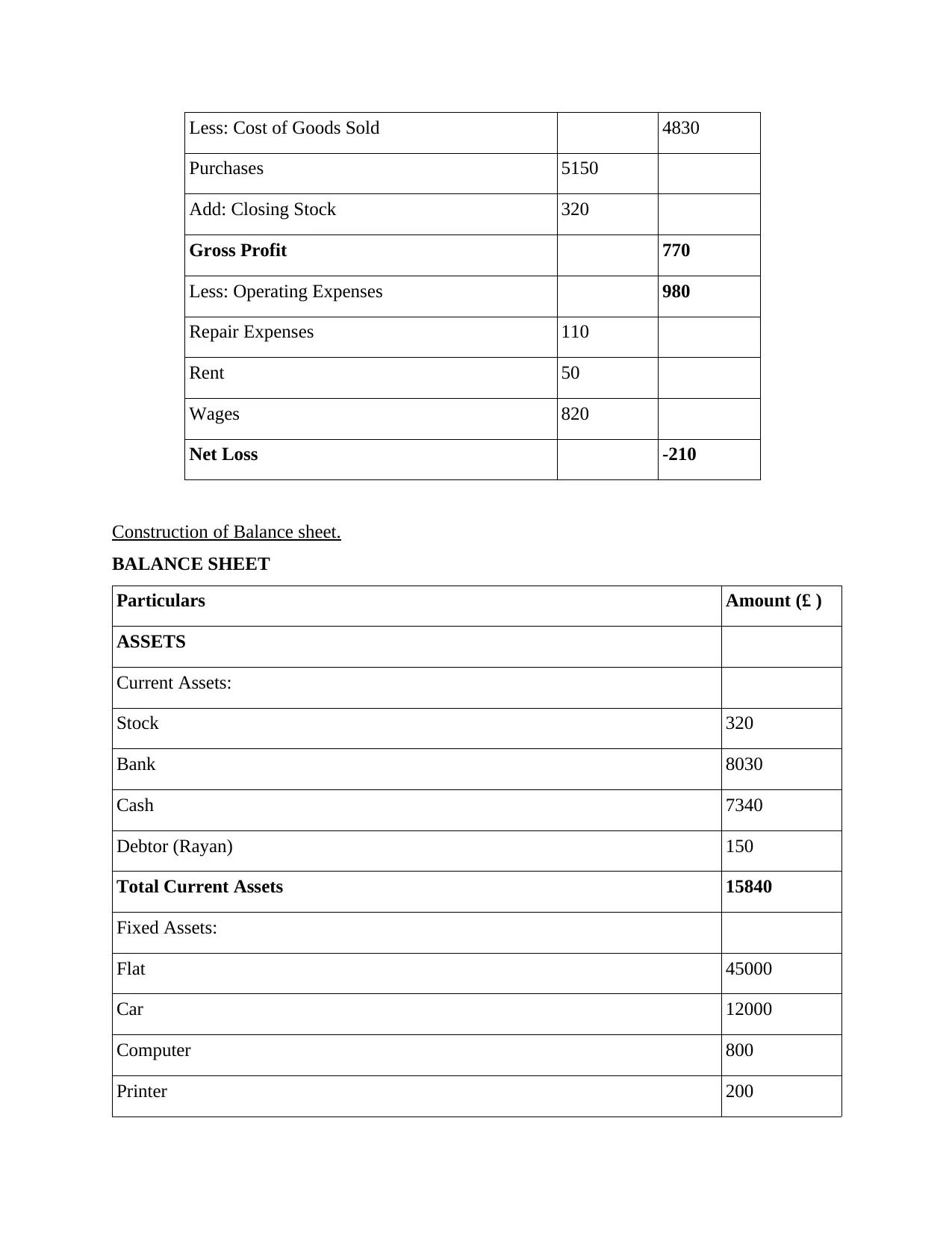

Less: Cost of Goods Sold 4830

Purchases 5150

Add: Closing Stock 320

Gross Profit 770

Less: Operating Expenses 980

Repair Expenses 110

Rent 50

Wages 820

Net Loss -210

Construction of Balance sheet.

BALANCE SHEET

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

Debtor (Rayan) 150

Total Current Assets 15840

Fixed Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

Purchases 5150

Add: Closing Stock 320

Gross Profit 770

Less: Operating Expenses 980

Repair Expenses 110

Rent 50

Wages 820

Net Loss -210

Construction of Balance sheet.

BALANCE SHEET

Particulars Amount (£ )

ASSETS

Current Assets:

Stock 320

Bank 8030

Cash 7340

Debtor (Rayan) 150

Total Current Assets 15840

Fixed Assets:

Flat 45000

Car 12000

Computer 800

Printer 200

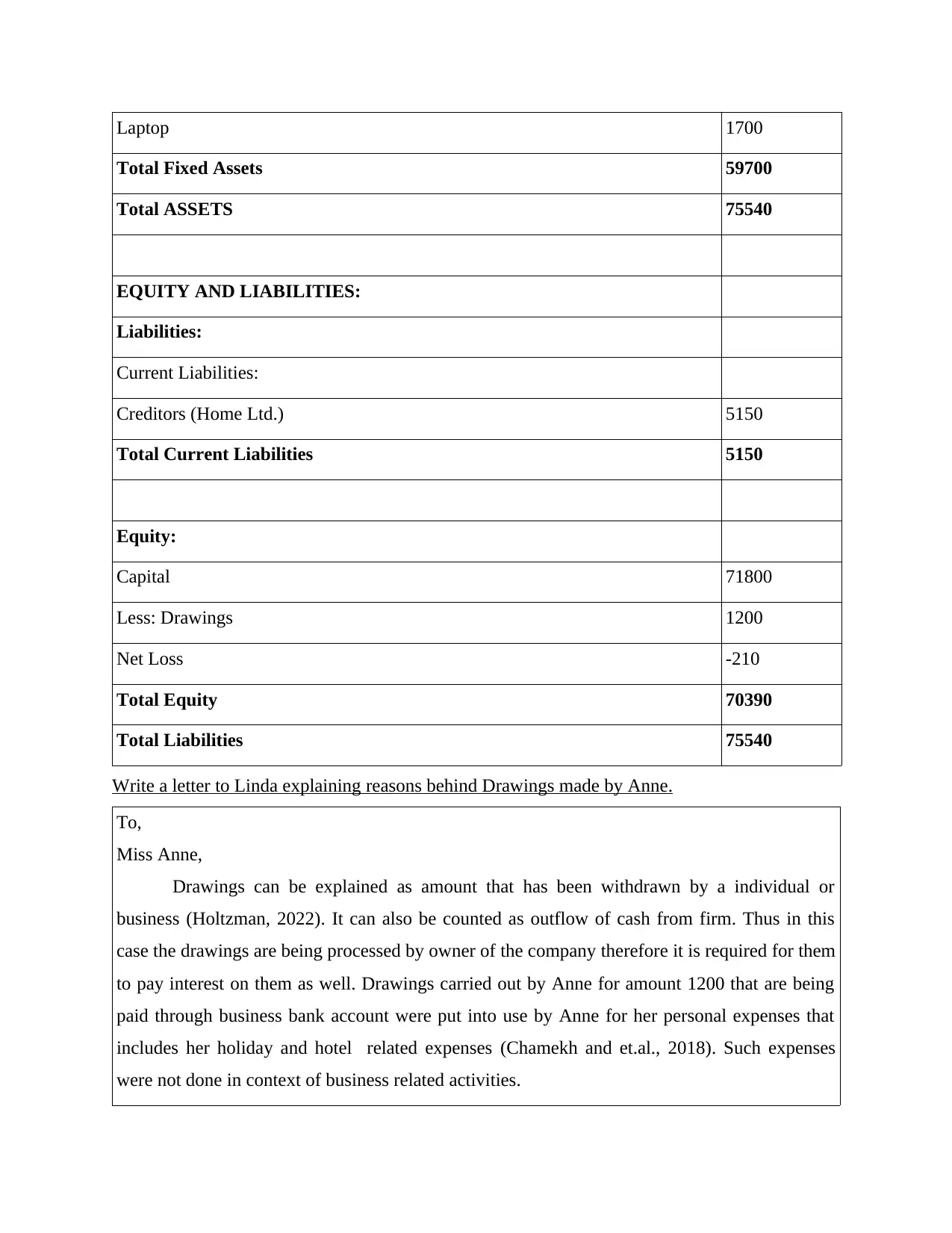

Laptop 1700

Total Fixed Assets 59700

Total ASSETS 75540

EQUITY AND LIABILITIES:

Liabilities:

Current Liabilities:

Creditors (Home Ltd.) 5150

Total Current Liabilities 5150

Equity:

Capital 71800

Less: Drawings 1200

Net Loss -210

Total Equity 70390

Total Liabilities 75540

Write a letter to Linda explaining reasons behind Drawings made by Anne.

To,

Miss Anne,

Drawings can be explained as amount that has been withdrawn by a individual or

business (Holtzman, 2022). It can also be counted as outflow of cash from firm. Thus in this

case the drawings are being processed by owner of the company therefore it is required for them

to pay interest on them as well. Drawings carried out by Anne for amount 1200 that are being

paid through business bank account were put into use by Anne for her personal expenses that

includes her holiday and hotel related expenses (Chamekh and et.al., 2018). Such expenses

were not done in context of business related activities.

Total Fixed Assets 59700

Total ASSETS 75540

EQUITY AND LIABILITIES:

Liabilities:

Current Liabilities:

Creditors (Home Ltd.) 5150

Total Current Liabilities 5150

Equity:

Capital 71800

Less: Drawings 1200

Net Loss -210

Total Equity 70390

Total Liabilities 75540

Write a letter to Linda explaining reasons behind Drawings made by Anne.

To,

Miss Anne,

Drawings can be explained as amount that has been withdrawn by a individual or

business (Holtzman, 2022). It can also be counted as outflow of cash from firm. Thus in this

case the drawings are being processed by owner of the company therefore it is required for them

to pay interest on them as well. Drawings carried out by Anne for amount 1200 that are being

paid through business bank account were put into use by Anne for her personal expenses that

includes her holiday and hotel related expenses (Chamekh and et.al., 2018). Such expenses

were not done in context of business related activities.

TASK 2

Present Calculation of Different Accounting ratios of business.

Net Profit Margin = ( Net profit / Net Sales ) * 100 = ( - 210 / 5600 ) * 100 = - 3.75 %

Gross Profit Margin = ( Gross Profit / Net Sales) * 100 = ( 770 / 5600 ) * 100 = 13.75

%

Current Ratio = Current Assets / Current Liabilities (Wiratama, and Asri, 2020) =

15480 / 5150 = 3.01

Acid Test ratio = ( Current Assets – Stock ) / Current Liabilities = ( 15480 – 320 ) /

5150 = 2.94

Accounts Receivable Collection Period = ( Average Debtors / Net Sales ) * 365 =

( 150 / 5600 ) * 365 = 9.78 Days

Accounts Payable Payment Period = ( Average Creditors / Net Purchases ) * 365 =

( 5150 / 5150 ) * 365 = 365 Days

Interpretation: The above made calculations reflect various type of Ratios of Anne. With the

help of them it can be interpreted that the business is not at a good position. Whereas when

compared to its competitors it can be observed that they are earning more profits and incurring

less costs/ losses which help them to facilitate development and expansion. The competitors of

Anne can be observed to have high margin of current assets available with them that makes their

liquidity better than running business of Anne in short run. Anne's acquired assets is better than

other companies working in the same area of industry but it is suggested that it must work

consistently on front foot for better results. Net profit margin helps to calculate profit generated

by company and revenues earned so far (Das and Dutta, 2020). Gross profit margin can be

explained as deviation between cost incurred in sale of goods and revenue generated in the

process. Current ratio is amount of current assets in relation with current liabilities thus ratio

observed above is 3.01 that indicates that it is a profitable situation. Acid test ratio helps to asses

comparison of company's short term assets towards its short term liabilities. Account receivable

collection period can be defined as a tool that helps to measure the number of days demanded by

Present Calculation of Different Accounting ratios of business.

Net Profit Margin = ( Net profit / Net Sales ) * 100 = ( - 210 / 5600 ) * 100 = - 3.75 %

Gross Profit Margin = ( Gross Profit / Net Sales) * 100 = ( 770 / 5600 ) * 100 = 13.75

%

Current Ratio = Current Assets / Current Liabilities (Wiratama, and Asri, 2020) =

15480 / 5150 = 3.01

Acid Test ratio = ( Current Assets – Stock ) / Current Liabilities = ( 15480 – 320 ) /

5150 = 2.94

Accounts Receivable Collection Period = ( Average Debtors / Net Sales ) * 365 =

( 150 / 5600 ) * 365 = 9.78 Days

Accounts Payable Payment Period = ( Average Creditors / Net Purchases ) * 365 =

( 5150 / 5150 ) * 365 = 365 Days

Interpretation: The above made calculations reflect various type of Ratios of Anne. With the

help of them it can be interpreted that the business is not at a good position. Whereas when

compared to its competitors it can be observed that they are earning more profits and incurring

less costs/ losses which help them to facilitate development and expansion. The competitors of

Anne can be observed to have high margin of current assets available with them that makes their

liquidity better than running business of Anne in short run. Anne's acquired assets is better than

other companies working in the same area of industry but it is suggested that it must work

consistently on front foot for better results. Net profit margin helps to calculate profit generated

by company and revenues earned so far (Das and Dutta, 2020). Gross profit margin can be

explained as deviation between cost incurred in sale of goods and revenue generated in the

process. Current ratio is amount of current assets in relation with current liabilities thus ratio

observed above is 3.01 that indicates that it is a profitable situation. Acid test ratio helps to asses

comparison of company's short term assets towards its short term liabilities. Account receivable

collection period can be defined as a tool that helps to measure the number of days demanded by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a customer to pay back its credit amount back to organisation. Account payable payment period

can further be described as average time taken by a firm to cover its accounts payable.

What impact has been observed in reference to COVID-19 relating to profits generated by

business.

The impact of pandemic has been uncontrollable in every sector of the economy and

industries as well (Górski, Bednarski and Chaczko, 2018). It has affected every company

whether small or large in adverse ways i.e. decreased the amount of profits earned and additional

revenues that were being generated . It can be recommended after assessment of conditions

prevailing in the economy that special care must be taken for managing labour scale in post

corona situations (Gupta, 2018). There are several new and modified ideas that can be adopted

by business for bringing the growth and expansion of company back on track with an urge to

increase profitability. If the market gets back to normal conditions and the situation is being in

normal stages it would be easy for firm to carry out its work efficiently and effectively. It would

thus be helpful for organisation to plan accordingly and predict what is the desirable demand of

people present in marketplace and what could be the possible ways for fulfilling such needs

(Hakak and et.al., 2020).

can further be described as average time taken by a firm to cover its accounts payable.

What impact has been observed in reference to COVID-19 relating to profits generated by

business.

The impact of pandemic has been uncontrollable in every sector of the economy and

industries as well (Górski, Bednarski and Chaczko, 2018). It has affected every company

whether small or large in adverse ways i.e. decreased the amount of profits earned and additional

revenues that were being generated . It can be recommended after assessment of conditions

prevailing in the economy that special care must be taken for managing labour scale in post

corona situations (Gupta, 2018). There are several new and modified ideas that can be adopted

by business for bringing the growth and expansion of company back on track with an urge to

increase profitability. If the market gets back to normal conditions and the situation is being in

normal stages it would be easy for firm to carry out its work efficiently and effectively. It would

thus be helpful for organisation to plan accordingly and predict what is the desirable demand of

people present in marketplace and what could be the possible ways for fulfilling such needs

(Hakak and et.al., 2020).

CONCLUSION

From the above asserted report it can be concluded that Recording business transaction is

a process of multiple steps that includes the type of transactions being recorded in a company

and how they would affect the working of company. It is useful to keep a books of accounts that

helps in recording transaction of monetary nature which would help to assess liquidity and

positioning of business in market and what could be the possible ways that would contribute in

improving them. With the help of report managers, investors and even the owner can assess its

working and profitability scale. It reflects the calculation of ratios, preparation of journal

accounts, ledger and balance sheet as well. It helps to understand what amount of current assets

are available with the company and the amount of debts & liabilities it has to cover. It is helpful

to understand the impact of COVID- 19 and how companies can plan its operations keeping

them in mind for better results.

From the above asserted report it can be concluded that Recording business transaction is

a process of multiple steps that includes the type of transactions being recorded in a company

and how they would affect the working of company. It is useful to keep a books of accounts that

helps in recording transaction of monetary nature which would help to assess liquidity and

positioning of business in market and what could be the possible ways that would contribute in

improving them. With the help of report managers, investors and even the owner can assess its

working and profitability scale. It reflects the calculation of ratios, preparation of journal

accounts, ledger and balance sheet as well. It helps to understand what amount of current assets

are available with the company and the amount of debts & liabilities it has to cover. It is helpful

to understand the impact of COVID- 19 and how companies can plan its operations keeping

them in mind for better results.

REFERENCES

Books and Journals

Burke, T., 2019. Blockchain in food traceability. In Food traceability (pp. 133-143). Springer,

Cham.

Chamekh and et.al., 2018, June. Secured distributed IoT based supply chain architecture.

In 2018 IEEE 27th International Conference on Enabling Technologies: Infrastructure

for Collaborative Enterprises (WETICE) (pp. 199-202). IEEE.

Das, D. and Dutta, A., 2020. Bitcoin’s energy consumption: Is it the Achilles heel to miner’s

revenue?. Economics Letters. 186. p.108530.

Górski, T., Bednarski, J. and Chaczko, Z., 2018, December. Blockchain-based renewable energy

exchange management system. In 2018 26th International Conference on Systems

Engineering (ICSEng) (pp. 1-6). IEEE.

Gupta, S., 2018. Driving digital strategy: A guide to reimagining your business. Harvard

Business Press.

Hakak and et.al., 2020. Securing smart cities through blockchain technology: Architecture,

requirements, and challenges. IEEE Network. 34(1). pp.8-14.

Holtzman, M.P., 2022. FASB Streamlines Income Tax Accounting. The CPA Journal. 92(1/2).

pp.54-56.

Kim and et.al., 2020. Permissionless and permissioned, technology-focused and business needs-

driven: Understanding the hybrid opportunity in blockchain through a case study of

Insolar. IEEE Transactions on Engineering Management.

Lang and et.al., 2018. Fundamentals of transfer pricing: a practical guide. Kluwer Law

International BV.

Massaro, M., 2021. Digital transformation in the healthcare sector through blockchain

technology. Insights from academic research and business developments. Technovation,

p.102386.

Books and Journals

Burke, T., 2019. Blockchain in food traceability. In Food traceability (pp. 133-143). Springer,

Cham.

Chamekh and et.al., 2018, June. Secured distributed IoT based supply chain architecture.

In 2018 IEEE 27th International Conference on Enabling Technologies: Infrastructure

for Collaborative Enterprises (WETICE) (pp. 199-202). IEEE.

Das, D. and Dutta, A., 2020. Bitcoin’s energy consumption: Is it the Achilles heel to miner’s

revenue?. Economics Letters. 186. p.108530.

Górski, T., Bednarski, J. and Chaczko, Z., 2018, December. Blockchain-based renewable energy

exchange management system. In 2018 26th International Conference on Systems

Engineering (ICSEng) (pp. 1-6). IEEE.

Gupta, S., 2018. Driving digital strategy: A guide to reimagining your business. Harvard

Business Press.

Hakak and et.al., 2020. Securing smart cities through blockchain technology: Architecture,

requirements, and challenges. IEEE Network. 34(1). pp.8-14.

Holtzman, M.P., 2022. FASB Streamlines Income Tax Accounting. The CPA Journal. 92(1/2).

pp.54-56.

Kim and et.al., 2020. Permissionless and permissioned, technology-focused and business needs-

driven: Understanding the hybrid opportunity in blockchain through a case study of

Insolar. IEEE Transactions on Engineering Management.

Lang and et.al., 2018. Fundamentals of transfer pricing: a practical guide. Kluwer Law

International BV.

Massaro, M., 2021. Digital transformation in the healthcare sector through blockchain

technology. Insights from academic research and business developments. Technovation,

p.102386.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.