The Effects of Corporate Tax Reduction on Foreign Investment

VerifiedAdded on 2023/01/19

|8

|3296

|71

Report

AI Summary

This report provides an in-depth analysis of the relationship between corporate tax reduction and foreign investment inflows. It begins by defining corporate income tax and its variations across different countries, including a sample calculation. The report then explores the global trend of corporate tax reduction, examining the factors that influence multinational companies' decisions to shift operations to lower-tax jurisdictions, such as tax policies, opaqueness, patent regimes, and capital gain tax structures. It provides examples of major companies like Starbucks, Amazon, and Google and their tax planning strategies. The report further details the corporate tax regimes of countries like the United Kingdom, Ireland, Portugal, and Italy, including their tax rates, incentives, and double tax avoidance agreements. The report concludes with a discussion of the impact of these tax policies on foreign investment and economic growth.

Reduction in Corporate Tax and Foreign Investment inflow

Introduction

Corporate Income Tax is the rate of tax levied on Business Corporation for the profits earned

during the relevant year. The rate varies from country to country ranging from zero corporate

tax as levied by UAE to 40-50% levied by different countries. The tax is generally levied on

the actual profits as computed under the Income Tax regime of different countries. A sample

computation of corporate Income tax is presented here-in-under:

Profit earned during the year as per books of account: $100 Mio.

Profit earned during the year as per Income-tax account: $80 Mio.

Tax Rate: 25%

Corporate Income Tax= Profit earned during the year as per Income-tax account* Tax Rate

Corporate Income Tax=$ 80 Mio* 25%= $ 20 Mio.( Subject to surcharge and cess, if any).

Further, other types of tax that are levied on enterprise range from Goods and Service Tax,

Dividend distribution Tax, Withholding tax etc.

Corporate Taxation

Recently, many countries around the world has been on a shopping spree by reducing the

corporate of taxation with some countries having a basic tax rate of zero percent. Further, the

impact of such corporate tax reduction entails company to shift their head operations into

lower tax and entail the advantage of favourable tax policies.

In addition, not only the corporate taxation policy of the country determines the rationale for

shifting of enterprise to a lower tax jurisdiction, there are various other parameters that needs

to be analysed to determine the reason for multi giants to set up their operation in the tax

jurisdiction:

(a) Opaqueness of the country i.e. maintaining of secrecy and privacy and non-sharing of

information with other countries of operation of the company;

(b) Patent Box Regime: Laws of the country favouring the establishment and registration of

patents, copyright, trademark etc;

(c) Cost of establishing the organisation in the jurisdiction in comparison with the benefits.

Further, a comparison of cost and benefit analysis needs to be compared;

(d) Capital Gain tax regime of the country along with nil tax on capital gain. For instance,

economies like India have dual tax classification wherein tax rate on capital gain is lower

than normal business income;

(e) Structure of company that can be operated in the country. Example in the form of

partnership, company etc.

The aforesaid factors also play a critical role in determining the rationale for attracting

investment in the foreign jurisdiction.

Introduction

Corporate Income Tax is the rate of tax levied on Business Corporation for the profits earned

during the relevant year. The rate varies from country to country ranging from zero corporate

tax as levied by UAE to 40-50% levied by different countries. The tax is generally levied on

the actual profits as computed under the Income Tax regime of different countries. A sample

computation of corporate Income tax is presented here-in-under:

Profit earned during the year as per books of account: $100 Mio.

Profit earned during the year as per Income-tax account: $80 Mio.

Tax Rate: 25%

Corporate Income Tax= Profit earned during the year as per Income-tax account* Tax Rate

Corporate Income Tax=$ 80 Mio* 25%= $ 20 Mio.( Subject to surcharge and cess, if any).

Further, other types of tax that are levied on enterprise range from Goods and Service Tax,

Dividend distribution Tax, Withholding tax etc.

Corporate Taxation

Recently, many countries around the world has been on a shopping spree by reducing the

corporate of taxation with some countries having a basic tax rate of zero percent. Further, the

impact of such corporate tax reduction entails company to shift their head operations into

lower tax and entail the advantage of favourable tax policies.

In addition, not only the corporate taxation policy of the country determines the rationale for

shifting of enterprise to a lower tax jurisdiction, there are various other parameters that needs

to be analysed to determine the reason for multi giants to set up their operation in the tax

jurisdiction:

(a) Opaqueness of the country i.e. maintaining of secrecy and privacy and non-sharing of

information with other countries of operation of the company;

(b) Patent Box Regime: Laws of the country favouring the establishment and registration of

patents, copyright, trademark etc;

(c) Cost of establishing the organisation in the jurisdiction in comparison with the benefits.

Further, a comparison of cost and benefit analysis needs to be compared;

(d) Capital Gain tax regime of the country along with nil tax on capital gain. For instance,

economies like India have dual tax classification wherein tax rate on capital gain is lower

than normal business income;

(e) Structure of company that can be operated in the country. Example in the form of

partnership, company etc.

The aforesaid factors also play a critical role in determining the rationale for attracting

investment in the foreign jurisdiction.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Major Companies which profited from such Corporate Tax Planning

Multinational companies all around the world have had complicated tax structures that have

highlighted a number of tax avoiding issues. For instance, Star bucks in 2012 had sales of

approximately £400m in UK, but paid no corporation tax to UK, as they transferred some

money to their Dutch sister company as royalty payment in furtherance of paying high

interest rates to borrow from other parts of the business. Another example is that of Amazon

who reported a tax expense of £1.8m, while having sales of £3.35bn in UK in 2011 by

reporting sales through a Luxembourg based unit. Similarly, Google paid £6m in tax, while

having sales of £395m in 2011, by channeling its income via Ireland and Bermuda. The

French government demanded €1bn from Google, and also highlighted the issue of how the

internet giant was avoiding tax in France and was of the view that it must not be acceptable

and 49 efforts must be made to harmonize the tax structure.

In addition, companies like those that Apple Inc. has been charged with complain from many

countries of paying nil or zero withholding tax. Also. Many giant software companies like

Google, Yahoo etc has been very agile in shifting their tax base to lower tax jurisdiction to

benefit from reduced corporate taxation.

Countries which have reduced Corporate Rate of Taxation

United Kingdom: One of the major countries of Europe which is compliant with IFRS/

GAAP and IAS, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has planned to reduce its

corporate tax rate to 17% by 1st April, 2020 from 19% currently and much higher rate

previously. The said action has been taken by the country to make it investment attractive,

inflow of foreign funds and rapid growth of Economy. Further, United Kingdom is currently

undergoing a drastic phase of Brexit which is lower down its economic growth on year on

year basis. Further, the tax is levied on world-wide profits and gains with credit for overseas

tax paid.

In addition, taxable income in United Kingdom is imposed on trading income, several non-

trading income in basket form and capital gains. Thus, the country does not distinguish

between capital gain and corporate income.

Other incentives that are offered by the tax jurisdiction encompass the following:

Qualifying capital expenditure on plant and machinery shall be allowed to be written

down at 8% and 6% in current year. An alternative is also provided in the form of written

down value method at the flat rate of 18%;

Full deduction is permitted for first GBP of qualifying expenses during the year;

Exemption of receipt of dividend to most dividend receipt and distributions unless

received by a bank, an insurance company or other financial trade;

Gain or loss on the substantial holding both in UK and foreign countries are exempt

under the participation exemption scheme and Parent Subsidiary directive;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Trading losses can be set-off against the profit without any restriction;

Losses can be carried forward indefinitely.

Multinational companies all around the world have had complicated tax structures that have

highlighted a number of tax avoiding issues. For instance, Star bucks in 2012 had sales of

approximately £400m in UK, but paid no corporation tax to UK, as they transferred some

money to their Dutch sister company as royalty payment in furtherance of paying high

interest rates to borrow from other parts of the business. Another example is that of Amazon

who reported a tax expense of £1.8m, while having sales of £3.35bn in UK in 2011 by

reporting sales through a Luxembourg based unit. Similarly, Google paid £6m in tax, while

having sales of £395m in 2011, by channeling its income via Ireland and Bermuda. The

French government demanded €1bn from Google, and also highlighted the issue of how the

internet giant was avoiding tax in France and was of the view that it must not be acceptable

and 49 efforts must be made to harmonize the tax structure.

In addition, companies like those that Apple Inc. has been charged with complain from many

countries of paying nil or zero withholding tax. Also. Many giant software companies like

Google, Yahoo etc has been very agile in shifting their tax base to lower tax jurisdiction to

benefit from reduced corporate taxation.

Countries which have reduced Corporate Rate of Taxation

United Kingdom: One of the major countries of Europe which is compliant with IFRS/

GAAP and IAS, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has planned to reduce its

corporate tax rate to 17% by 1st April, 2020 from 19% currently and much higher rate

previously. The said action has been taken by the country to make it investment attractive,

inflow of foreign funds and rapid growth of Economy. Further, United Kingdom is currently

undergoing a drastic phase of Brexit which is lower down its economic growth on year on

year basis. Further, the tax is levied on world-wide profits and gains with credit for overseas

tax paid.

In addition, taxable income in United Kingdom is imposed on trading income, several non-

trading income in basket form and capital gains. Thus, the country does not distinguish

between capital gain and corporate income.

Other incentives that are offered by the tax jurisdiction encompass the following:

Qualifying capital expenditure on plant and machinery shall be allowed to be written

down at 8% and 6% in current year. An alternative is also provided in the form of written

down value method at the flat rate of 18%;

Full deduction is permitted for first GBP of qualifying expenses during the year;

Exemption of receipt of dividend to most dividend receipt and distributions unless

received by a bank, an insurance company or other financial trade;

Gain or loss on the substantial holding both in UK and foreign countries are exempt

under the participation exemption scheme and Parent Subsidiary directive;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Trading losses can be set-off against the profit without any restriction;

Losses can be carried forward indefinitely.

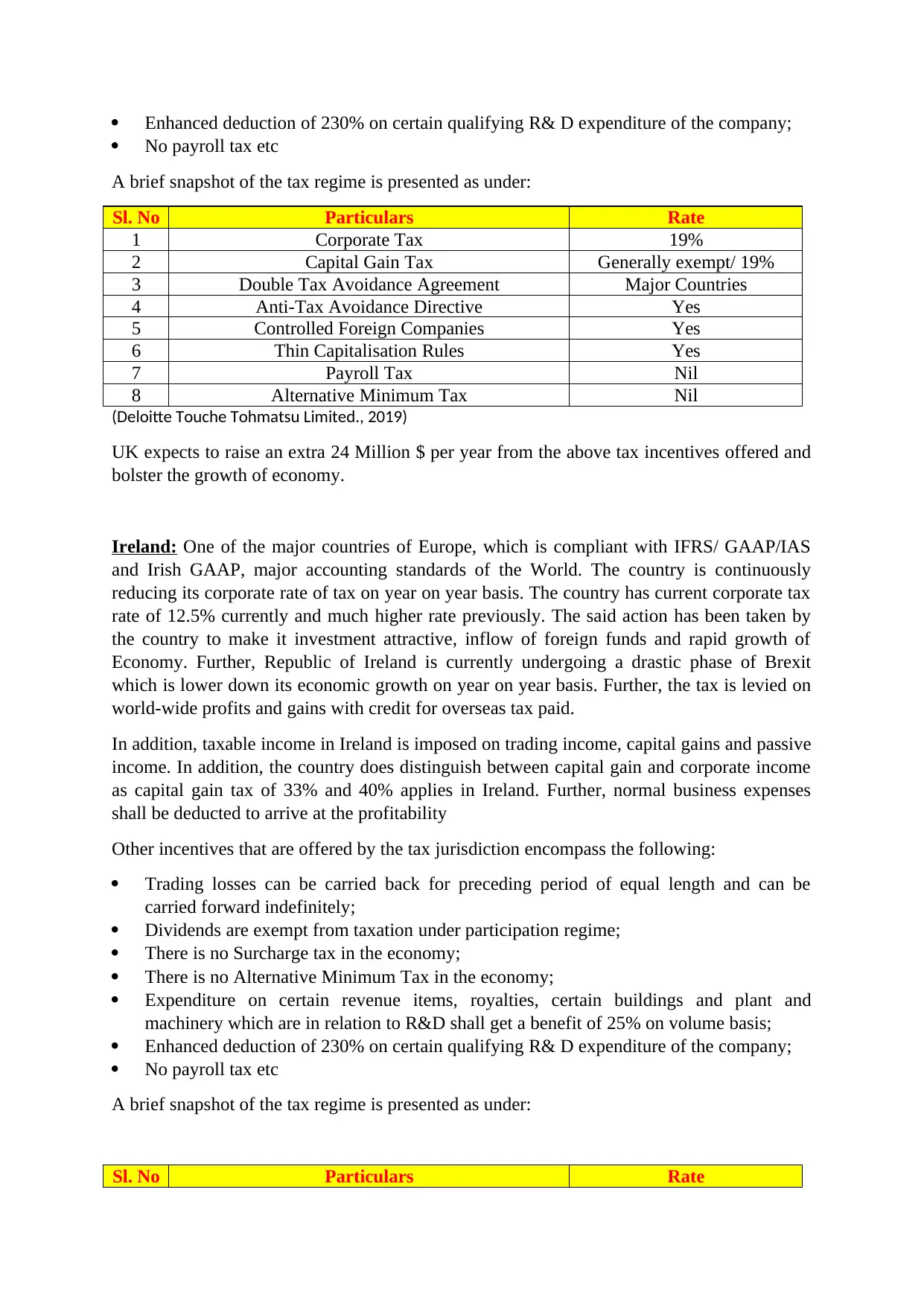

Enhanced deduction of 230% on certain qualifying R& D expenditure of the company;

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 19%

2 Capital Gain Tax Generally exempt/ 19%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited., 2019)

UK expects to raise an extra 24 Million $ per year from the above tax incentives offered and

bolster the growth of economy.

Ireland: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS

and Irish GAAP, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has current corporate tax

rate of 12.5% currently and much higher rate previously. The said action has been taken by

the country to make it investment attractive, inflow of foreign funds and rapid growth of

Economy. Further, Republic of Ireland is currently undergoing a drastic phase of Brexit

which is lower down its economic growth on year on year basis. Further, the tax is levied on

world-wide profits and gains with credit for overseas tax paid.

In addition, taxable income in Ireland is imposed on trading income, capital gains and passive

income. In addition, the country does distinguish between capital gain and corporate income

as capital gain tax of 33% and 40% applies in Ireland. Further, normal business expenses

shall be deducted to arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for preceding period of equal length and can be

carried forward indefinitely;

Dividends are exempt from taxation under participation regime;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Expenditure on certain revenue items, royalties, certain buildings and plant and

machinery which are in relation to R&D shall get a benefit of 25% on volume basis;

Enhanced deduction of 230% on certain qualifying R& D expenditure of the company;

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 19%

2 Capital Gain Tax Generally exempt/ 19%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited., 2019)

UK expects to raise an extra 24 Million $ per year from the above tax incentives offered and

bolster the growth of economy.

Ireland: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS

and Irish GAAP, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has current corporate tax

rate of 12.5% currently and much higher rate previously. The said action has been taken by

the country to make it investment attractive, inflow of foreign funds and rapid growth of

Economy. Further, Republic of Ireland is currently undergoing a drastic phase of Brexit

which is lower down its economic growth on year on year basis. Further, the tax is levied on

world-wide profits and gains with credit for overseas tax paid.

In addition, taxable income in Ireland is imposed on trading income, capital gains and passive

income. In addition, the country does distinguish between capital gain and corporate income

as capital gain tax of 33% and 40% applies in Ireland. Further, normal business expenses

shall be deducted to arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for preceding period of equal length and can be

carried forward indefinitely;

Dividends are exempt from taxation under participation regime;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Expenditure on certain revenue items, royalties, certain buildings and plant and

machinery which are in relation to R&D shall get a benefit of 25% on volume basis;

Enhanced deduction of 230% on certain qualifying R& D expenditure of the company;

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

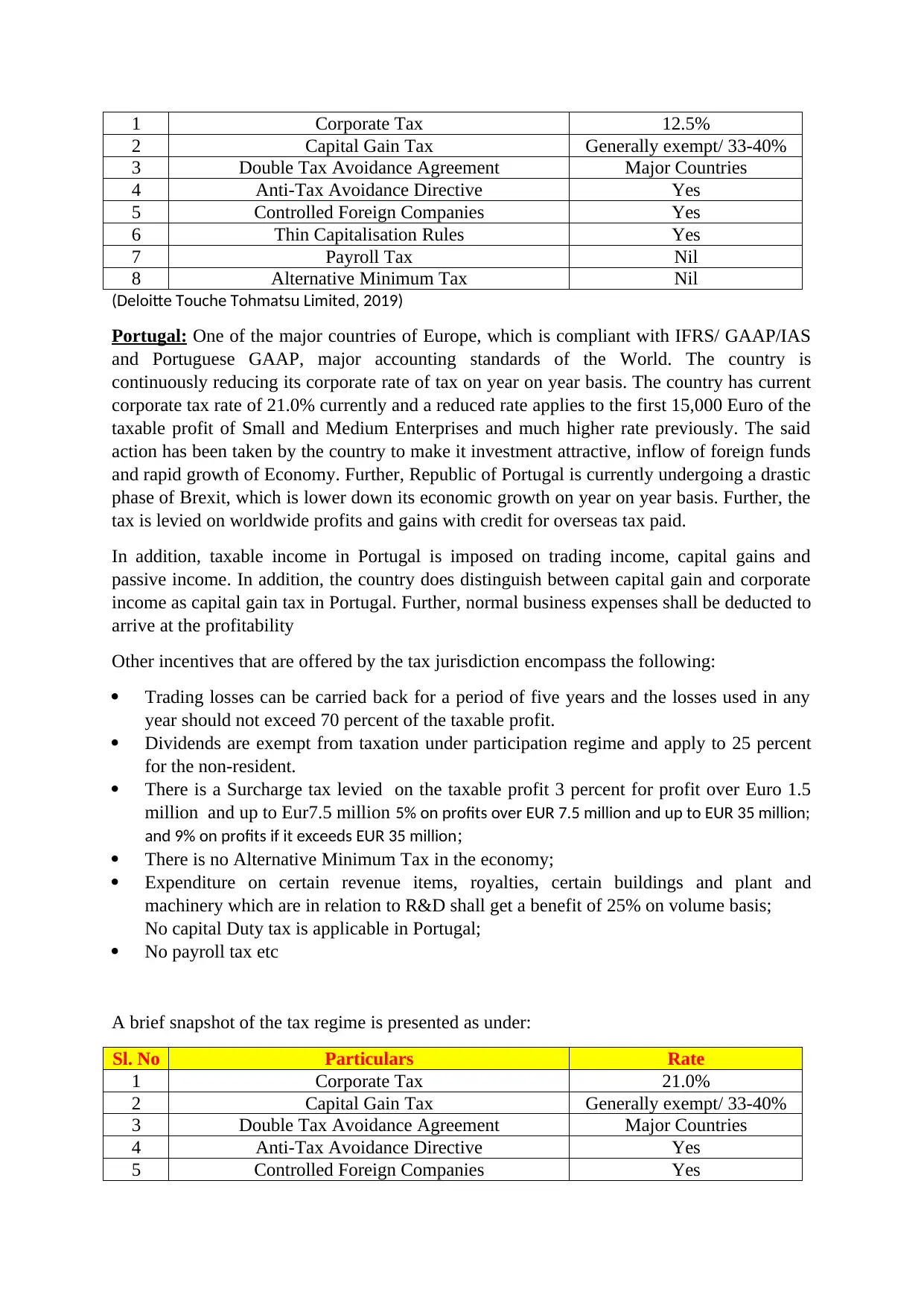

1 Corporate Tax 12.5%

2 Capital Gain Tax Generally exempt/ 33-40%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited, 2019)

Portugal: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS

and Portuguese GAAP, major accounting standards of the World. The country is

continuously reducing its corporate rate of tax on year on year basis. The country has current

corporate tax rate of 21.0% currently and a reduced rate applies to the first 15,000 Euro of the

taxable profit of Small and Medium Enterprises and much higher rate previously. The said

action has been taken by the country to make it investment attractive, inflow of foreign funds

and rapid growth of Economy. Further, Republic of Portugal is currently undergoing a drastic

phase of Brexit, which is lower down its economic growth on year on year basis. Further, the

tax is levied on worldwide profits and gains with credit for overseas tax paid.

In addition, taxable income in Portugal is imposed on trading income, capital gains and

passive income. In addition, the country does distinguish between capital gain and corporate

income as capital gain tax in Portugal. Further, normal business expenses shall be deducted to

arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for a period of five years and the losses used in any

year should not exceed 70 percent of the taxable profit.

Dividends are exempt from taxation under participation regime and apply to 25 percent

for the non-resident.

There is a Surcharge tax levied on the taxable profit 3 percent for profit over Euro 1.5

million and up to Eur7.5 million 5% on profits over EUR 7.5 million and up to EUR 35 million;

and 9% on profits if it exceeds EUR 35 million;

There is no Alternative Minimum Tax in the economy;

Expenditure on certain revenue items, royalties, certain buildings and plant and

machinery which are in relation to R&D shall get a benefit of 25% on volume basis;

No capital Duty tax is applicable in Portugal;

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 21.0%

2 Capital Gain Tax Generally exempt/ 33-40%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

2 Capital Gain Tax Generally exempt/ 33-40%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited, 2019)

Portugal: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS

and Portuguese GAAP, major accounting standards of the World. The country is

continuously reducing its corporate rate of tax on year on year basis. The country has current

corporate tax rate of 21.0% currently and a reduced rate applies to the first 15,000 Euro of the

taxable profit of Small and Medium Enterprises and much higher rate previously. The said

action has been taken by the country to make it investment attractive, inflow of foreign funds

and rapid growth of Economy. Further, Republic of Portugal is currently undergoing a drastic

phase of Brexit, which is lower down its economic growth on year on year basis. Further, the

tax is levied on worldwide profits and gains with credit for overseas tax paid.

In addition, taxable income in Portugal is imposed on trading income, capital gains and

passive income. In addition, the country does distinguish between capital gain and corporate

income as capital gain tax in Portugal. Further, normal business expenses shall be deducted to

arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for a period of five years and the losses used in any

year should not exceed 70 percent of the taxable profit.

Dividends are exempt from taxation under participation regime and apply to 25 percent

for the non-resident.

There is a Surcharge tax levied on the taxable profit 3 percent for profit over Euro 1.5

million and up to Eur7.5 million 5% on profits over EUR 7.5 million and up to EUR 35 million;

and 9% on profits if it exceeds EUR 35 million;

There is no Alternative Minimum Tax in the economy;

Expenditure on certain revenue items, royalties, certain buildings and plant and

machinery which are in relation to R&D shall get a benefit of 25% on volume basis;

No capital Duty tax is applicable in Portugal;

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 21.0%

2 Capital Gain Tax Generally exempt/ 33-40%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited., 2019)

Italy: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS and

Italian GAAP, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has current corporate tax

rate of 24.0% currently and much higher rate previously. The said action has been taken by

the country to make it investment attractive, inflow of foreign funds and rapid growth of

Economy and there is no foreign exchange restrictions for transfer to funds to other major

countries and the non-residents can easily hold the foreign currency inside and outside the

country. However, there is one condition to the rule that the fund held outside the country or

transferred in the country without bank intermediary must be declared the same for the

taxable income purpose. Further, Republic of Italy is currently undergoing a drastic phase of

Brexit, which is lower down its economic growth on year on year basis. Further, the tax is

levied on worldwide profits and gains with credit for overseas tax paid.

In addition, taxable income in Italy is imposed on trading income, capital gains and passive

income i.e dividends, interest and royalties. Taxable income is also based on the income,

which is arrived at after certain adjustments done with the income part .Also; the country

does not do any distinguishment between capital gain and corporate income as both are

charged at the same rate of 24% of the corporate income tax. . Further, normal business

expenses shall be deducted to arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for preceding period of equal length and can be

carried forward indefinitely;

Dividends paid to domestic shareholder are subject to tax regime of 1.20 percent and 26

percent if the dividend is distributed to the non resident.;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

There is no Branch remittance Tax.

There is no capital acquisition tax

Deductions on certain employment income, contribution towards social security scheme

dependents deductions are also available in computing taxable income.

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 24.0%

2 Capital Gain Tax 20%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited., 2019)

Italy: One of the major countries of Europe, which is compliant with IFRS/ GAAP/IAS and

Italian GAAP, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country has current corporate tax

rate of 24.0% currently and much higher rate previously. The said action has been taken by

the country to make it investment attractive, inflow of foreign funds and rapid growth of

Economy and there is no foreign exchange restrictions for transfer to funds to other major

countries and the non-residents can easily hold the foreign currency inside and outside the

country. However, there is one condition to the rule that the fund held outside the country or

transferred in the country without bank intermediary must be declared the same for the

taxable income purpose. Further, Republic of Italy is currently undergoing a drastic phase of

Brexit, which is lower down its economic growth on year on year basis. Further, the tax is

levied on worldwide profits and gains with credit for overseas tax paid.

In addition, taxable income in Italy is imposed on trading income, capital gains and passive

income i.e dividends, interest and royalties. Taxable income is also based on the income,

which is arrived at after certain adjustments done with the income part .Also; the country

does not do any distinguishment between capital gain and corporate income as both are

charged at the same rate of 24% of the corporate income tax. . Further, normal business

expenses shall be deducted to arrive at the profitability

Other incentives that are offered by the tax jurisdiction encompass the following:

Trading losses can be carried back for preceding period of equal length and can be

carried forward indefinitely;

Dividends paid to domestic shareholder are subject to tax regime of 1.20 percent and 26

percent if the dividend is distributed to the non resident.;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

There is no Branch remittance Tax.

There is no capital acquisition tax

Deductions on certain employment income, contribution towards social security scheme

dependents deductions are also available in computing taxable income.

No payroll tax etc

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 24.0%

2 Capital Gain Tax 20%

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited, 2019)

Finland: One of the major countries of Europe, which is compliant with IFRS/ Finnish

GAAP and IAS, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country corporate tax rate is 20%

. The said action has been taken by the country to make it investment attractive, inflow of

foreign funds and rapid growth of Economy. Further, in Finland resident are taxed on the

basis of worldwide income and non residents are only taxed on the basis of Finnish source of

income on the basis of their permanent establishment in finland.Further, the tax is levied on

world-wide profits and gains with credit for overseas tax paid.

In addition, taxable income in United Kingdom is imposed on trading income, several non-

trading income in basket form and capital gains. The expense, which the company incur in to

generate profit, is deducted to arrive at the taxable income.

Other incentives that are offered by the tax jurisdiction encompass the following:

Qualifying capital expenditure on plant and machinery shall be allowed to be written

down at 8% and 6% in current year. An alternative is also provided in the form of written

down value method at the flat rate of 18%;

Payment of interest to the non residents are generally exempt from tax;

Exemption of receipt of dividend to most Finnish resident received from another Finnish

company with few certain exceptions, only the dividend received from all other countries

are taxable in nature;

Capital gain is generally treated as the ordinary income and taxed at the normal corporate

rate of 20 percent .However certain gains are exempt if they do satisfy certain criteria;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Trading losses can be set-off against the profit without any restriction;

Losses can be carried forward for a period of 10 years but the carry back in losses are not

permitted.

Payment of foreign tax by the Finland residents may be credited against Finnish tax

assessed but the credit can be availed only up to the amount of tax payable in Finland

and the rest amount can be carried in forward for a period of five years.;

No payroll tax etc

No technical service fees are levied.

No Branch remittance tax.

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 20%

2 Capital Gain Tax Generally exempt/

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

(Deloitte Touche Tohmatsu Limited, 2019)

Finland: One of the major countries of Europe, which is compliant with IFRS/ Finnish

GAAP and IAS, major accounting standards of the World. The country is continuously

reducing its corporate rate of tax on year on year basis. The country corporate tax rate is 20%

. The said action has been taken by the country to make it investment attractive, inflow of

foreign funds and rapid growth of Economy. Further, in Finland resident are taxed on the

basis of worldwide income and non residents are only taxed on the basis of Finnish source of

income on the basis of their permanent establishment in finland.Further, the tax is levied on

world-wide profits and gains with credit for overseas tax paid.

In addition, taxable income in United Kingdom is imposed on trading income, several non-

trading income in basket form and capital gains. The expense, which the company incur in to

generate profit, is deducted to arrive at the taxable income.

Other incentives that are offered by the tax jurisdiction encompass the following:

Qualifying capital expenditure on plant and machinery shall be allowed to be written

down at 8% and 6% in current year. An alternative is also provided in the form of written

down value method at the flat rate of 18%;

Payment of interest to the non residents are generally exempt from tax;

Exemption of receipt of dividend to most Finnish resident received from another Finnish

company with few certain exceptions, only the dividend received from all other countries

are taxable in nature;

Capital gain is generally treated as the ordinary income and taxed at the normal corporate

rate of 20 percent .However certain gains are exempt if they do satisfy certain criteria;

There is no Surcharge tax in the economy;

There is no Alternative Minimum Tax in the economy;

Trading losses can be set-off against the profit without any restriction;

Losses can be carried forward for a period of 10 years but the carry back in losses are not

permitted.

Payment of foreign tax by the Finland residents may be credited against Finnish tax

assessed but the credit can be availed only up to the amount of tax payable in Finland

and the rest amount can be carried in forward for a period of five years.;

No payroll tax etc

No technical service fees are levied.

No Branch remittance tax.

A brief snapshot of the tax regime is presented as under:

Sl. No Particulars Rate

1 Corporate Tax 20%

2 Capital Gain Tax Generally exempt/

3 Double Tax Avoidance Agreement Major Countries

4 Anti-Tax Avoidance Directive Yes

5 Controlled Foreign Companies Yes

6 Thin Capitalisation Rules Yes

7 Payroll Tax Nil

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8 Alternative Minimum Tax Nil

(Deloitte Touche Tohmatsu Limited, 2019)

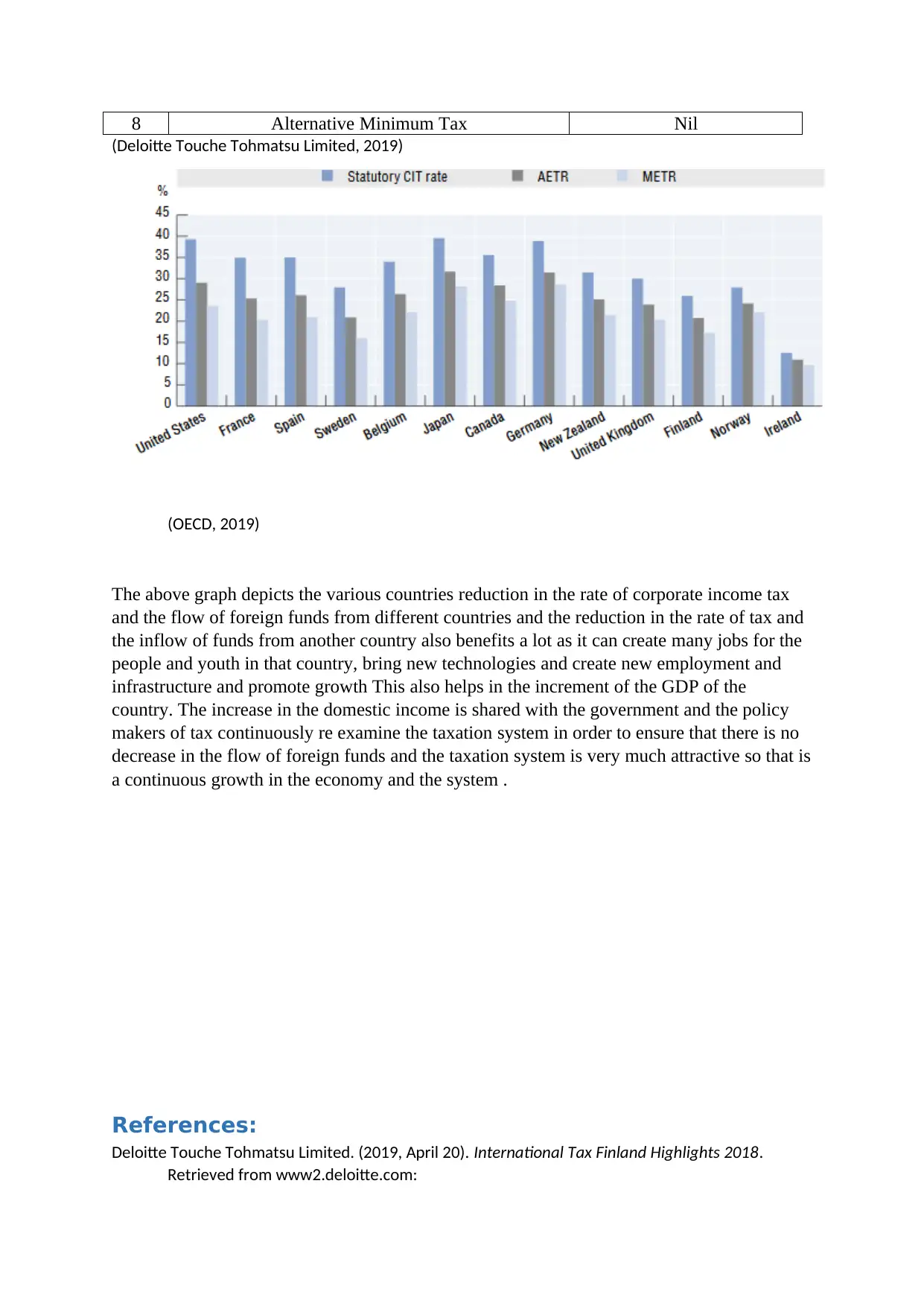

(OECD, 2019)

The above graph depicts the various countries reduction in the rate of corporate income tax

and the flow of foreign funds from different countries and the reduction in the rate of tax and

the inflow of funds from another country also benefits a lot as it can create many jobs for the

people and youth in that country, bring new technologies and create new employment and

infrastructure and promote growth This also helps in the increment of the GDP of the

country. The increase in the domestic income is shared with the government and the policy

makers of tax continuously re examine the taxation system in order to ensure that there is no

decrease in the flow of foreign funds and the taxation system is very much attractive so that is

a continuous growth in the economy and the system .

References:

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Finland Highlights 2018.

Retrieved from www2.deloitte.com:

(Deloitte Touche Tohmatsu Limited, 2019)

(OECD, 2019)

The above graph depicts the various countries reduction in the rate of corporate income tax

and the flow of foreign funds from different countries and the reduction in the rate of tax and

the inflow of funds from another country also benefits a lot as it can create many jobs for the

people and youth in that country, bring new technologies and create new employment and

infrastructure and promote growth This also helps in the increment of the GDP of the

country. The increase in the domestic income is shared with the government and the policy

makers of tax continuously re examine the taxation system in order to ensure that there is no

decrease in the flow of foreign funds and the taxation system is very much attractive so that is

a continuous growth in the economy and the system .

References:

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Finland Highlights 2018.

Retrieved from www2.deloitte.com:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

finlandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Finland Highlights 2018.

Retrieved from www2.deloitte.com:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

finlandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Ireland Highlights 2018.

Retrieved from www2.deloitte.com/:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

irelandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). nternational Tax Italy Highlights 2018. Retrieved

from www2.deloitte.com/:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

italyhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Portugal Highlights 2018.

Retrieved from /www2.deloitte.com:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

portugalhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). www2.deloitte.com. Retrieved from

International Tax United Kingdom Highlights 2019:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

unitedkingdomhighlights-2019.pdf

OECD. (2019, April 20). Tax Effects on Foreign Direct Investment. Retrieved from www.oecd.org/:

https://www.oecd.org/investment/investment-policy/40152903.pdf

finlandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Finland Highlights 2018.

Retrieved from www2.deloitte.com:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

finlandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Ireland Highlights 2018.

Retrieved from www2.deloitte.com/:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

irelandhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). nternational Tax Italy Highlights 2018. Retrieved

from www2.deloitte.com/:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

italyhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). International Tax Portugal Highlights 2018.

Retrieved from /www2.deloitte.com:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

portugalhighlights-2018.pdf

Deloitte Touche Tohmatsu Limited. (2019, April 20). www2.deloitte.com. Retrieved from

International Tax United Kingdom Highlights 2019:

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

unitedkingdomhighlights-2019.pdf

OECD. (2019, April 20). Tax Effects on Foreign Direct Investment. Retrieved from www.oecd.org/:

https://www.oecd.org/investment/investment-policy/40152903.pdf

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.