Evaluation of Remuneration Structure of Woodside Petroleum and Santos

VerifiedAdded on 2023/06/07

|28

|6167

|289

AI Summary

The report evaluates the remuneration structure of Woodside Petroleum and its competitor, Santos in the Australian market. It analyses the effectiveness of control systems within companies and reviews the details of remuneration committee and membership. The report also analyses the allocation of executive remuneration and the mix of performance measures used.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report is concerned with evaluating the remuneration structure of Woodside

Petroleum and its competitor, Santos in the Australian market. It has been evaluated that the

presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. it is

inherent that Woodside Petroleum has maintained an effective remuneration structure in line

with its overall financial performance. However, deficiencies could be observed in the executive

remuneration structure of Santos because of the poor financial health in the Australian market.

The net income of Woodside has increased coupled with fall in outstanding shares for

Woodside and the situation is just the opposite for Santos due to negative net income. Hence, the

returns of the shareholders are maximised for Woodside Petroleum. It needs to be also seen that

there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million.

Executive Summary:

The current report is concerned with evaluating the remuneration structure of Woodside

Petroleum and its competitor, Santos in the Australian market. It has been evaluated that the

presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. it is

inherent that Woodside Petroleum has maintained an effective remuneration structure in line

with its overall financial performance. However, deficiencies could be observed in the executive

remuneration structure of Santos because of the poor financial health in the Australian market.

The net income of Woodside has increased coupled with fall in outstanding shares for

Woodside and the situation is just the opposite for Santos due to negative net income. Hence, the

returns of the shareholders are maximised for Woodside Petroleum. It needs to be also seen that

there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million.

2MANAGERIAL ACCOUNTING

Table of Contents

1. Introduction:................................................................................................................................3

2. Review of topic and review of literature:....................................................................................3

2.1 Executive performance and remuneration in public companies:...........................................3

2.2 Effectiveness of control systems within companies:.............................................................5

3. Company reviews:.......................................................................................................................6

3.1 Details of remuneration committee and membership:...........................................................6

3.2 Allocation of executive remuneration:..................................................................................8

3.3 Mix of performance measures used:....................................................................................11

3.4 Company performance versus executive pay:.....................................................................17

4. Summary of findings:................................................................................................................19

5. Analysis and comparison of remuneration methods used:........................................................20

5.1 Best result in terms of shareholder returns:.........................................................................20

5.2 Best result in short-term:.....................................................................................................21

5.3 Best result in long-term:......................................................................................................22

6. Conclusion:................................................................................................................................23

References:....................................................................................................................................24

Table of Contents

1. Introduction:................................................................................................................................3

2. Review of topic and review of literature:....................................................................................3

2.1 Executive performance and remuneration in public companies:...........................................3

2.2 Effectiveness of control systems within companies:.............................................................5

3. Company reviews:.......................................................................................................................6

3.1 Details of remuneration committee and membership:...........................................................6

3.2 Allocation of executive remuneration:..................................................................................8

3.3 Mix of performance measures used:....................................................................................11

3.4 Company performance versus executive pay:.....................................................................17

4. Summary of findings:................................................................................................................19

5. Analysis and comparison of remuneration methods used:........................................................20

5.1 Best result in terms of shareholder returns:.........................................................................20

5.2 Best result in short-term:.....................................................................................................21

5.3 Best result in long-term:......................................................................................................22

6. Conclusion:................................................................................................................................23

References:....................................................................................................................................24

3MANAGERIAL ACCOUNTING

1. Introduction:

The report aims in identifying the role of remuneration, which is depicted in the annual

report of an organisation. Remuneration report is mainly depicted in the annual report as per the

rulings of Companies Act, where the organisation needs to detect all the remuneration that has

been provided to the directors of the company. Remuneration report also allows the investors to

understand the level of income, which is generated by the directors of the company during

declining profit and improving earnings. The report mainly exists to evaluate the remuneration

report of Woodside Petroleum for the fiscal year of 2017. Further evaluation on the company is

conducted in the overall assessment where its remuneration report is analysed, while other

financial performance measures are also taken into consideration. With the summary of findings

and the comparison of the remuneration report, the assessment portrays the company’s

performance over the fiscal years.

2. Review of topic and review of literature:

2.1 Executive performance and remuneration in public companies:

Both executive performance evaluation and remuneration in public companies are

depicted in the annual report of the organisation. The remuneration report depicted in the

financial statement directly indicates the level of bonuses and monetary benefits that has been

provided to the directors and executives of the organisation. This identified remuneration system

is adequately evaluated by the auditors and regulator to identify whether the organisation is

correctly providing remunerations to its directors and executives. In this context, Riaz, et al.,

(2015) stated that organisation with the help of remuneration report is able to detect the level of

1. Introduction:

The report aims in identifying the role of remuneration, which is depicted in the annual

report of an organisation. Remuneration report is mainly depicted in the annual report as per the

rulings of Companies Act, where the organisation needs to detect all the remuneration that has

been provided to the directors of the company. Remuneration report also allows the investors to

understand the level of income, which is generated by the directors of the company during

declining profit and improving earnings. The report mainly exists to evaluate the remuneration

report of Woodside Petroleum for the fiscal year of 2017. Further evaluation on the company is

conducted in the overall assessment where its remuneration report is analysed, while other

financial performance measures are also taken into consideration. With the summary of findings

and the comparison of the remuneration report, the assessment portrays the company’s

performance over the fiscal years.

2. Review of topic and review of literature:

2.1 Executive performance and remuneration in public companies:

Both executive performance evaluation and remuneration in public companies are

depicted in the annual report of the organisation. The remuneration report depicted in the

financial statement directly indicates the level of bonuses and monetary benefits that has been

provided to the directors and executives of the organisation. This identified remuneration system

is adequately evaluated by the auditors and regulator to identify whether the organisation is

correctly providing remunerations to its directors and executives. In this context, Riaz, et al.,

(2015) stated that organisation with the help of remuneration report is able to detect the level of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGERIAL ACCOUNTING

income that is distributed to directors and executives of the organisation. The level of

remuneration that is provided to the directors is considered to be as bonuses for the efforts

delivered by the Managing Directors. On the other hand, Hooghiemstra, Kuang and Qin (2017)

argued that investors are able to evaluate the loopholes in the current accounting system of

organisations, when they are able to identify that high remunerations are provided to director

while the organisation is making losses.

The remuneration report directly involved different types of methods that are used by the

organisation in paying the directives and executives. There are two different levels of payment

such as share-based payments and monetary payments. The organisation mainly provide share

based payment to the director and executive for long duration, while restricting the level of trees

that could be conducted for a particular period. This eventually helps in supporting the overall

share value of the organisation if the directors and executive think of selling their portion of

shares. Furthermore, the monetary benefit that is provided by the organisation is mainly for the

services that were conducted during the fiscal year. The bonuses are based on future share based

payments, which are provided to the executive for their services during the fiscal year.

According to Faghani, Monem and Ng (2015), the remuneration provided by the company to the

executive is based on the performance evaluation, which is conducted on annual basis to identify

the most efficient executive of the company. Moreover, Riaz, et al., (2015) indicated that

motivating the executive with monetary benefits for an effort during the fiscal year eventually

helps in improving the motivation level of employees. Therefore, with the remuneration report,

the organisation is able to detect the level of expenses that is conducted on executives and

directors for their initiatives. This eventually allows the investors to detect the level of expenses

income that is distributed to directors and executives of the organisation. The level of

remuneration that is provided to the directors is considered to be as bonuses for the efforts

delivered by the Managing Directors. On the other hand, Hooghiemstra, Kuang and Qin (2017)

argued that investors are able to evaluate the loopholes in the current accounting system of

organisations, when they are able to identify that high remunerations are provided to director

while the organisation is making losses.

The remuneration report directly involved different types of methods that are used by the

organisation in paying the directives and executives. There are two different levels of payment

such as share-based payments and monetary payments. The organisation mainly provide share

based payment to the director and executive for long duration, while restricting the level of trees

that could be conducted for a particular period. This eventually helps in supporting the overall

share value of the organisation if the directors and executive think of selling their portion of

shares. Furthermore, the monetary benefit that is provided by the organisation is mainly for the

services that were conducted during the fiscal year. The bonuses are based on future share based

payments, which are provided to the executive for their services during the fiscal year.

According to Faghani, Monem and Ng (2015), the remuneration provided by the company to the

executive is based on the performance evaluation, which is conducted on annual basis to identify

the most efficient executive of the company. Moreover, Riaz, et al., (2015) indicated that

motivating the executive with monetary benefits for an effort during the fiscal year eventually

helps in improving the motivation level of employees. Therefore, with the remuneration report,

the organisation is able to detect the level of expenses that is conducted on executives and

directors for their initiatives. This eventually allows the investors to detect the level of expenses

5MANAGERIAL ACCOUNTING

and determine whether the remuneration amount is feasible and viable for the directors or

executives.

2.2 Effectiveness of control systems within companies:

Presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. Scott

(2015) mentioned that without the presence of adequate control system within the organisation

the management is not able to exercise decisions, which could improve productivity and

efficiency of the company. Without the presence of an adequate control system businesses are

not able to develop and execute strategic plans, which helps in generating higher revenue in the

end. Therefore, it could be understood that organisations using the control system are able to

fulfil their objectives and obtain sustainable growth by adequately utilising the available

resources. The organisation also needs to have an adequate internal control system to support the

legal and regulatory standards that has been imposed by the adequate authorities. Hence, it could

be understood that without the presence of effective control system organisations are not able to

operate their 100%, which directly affects their capability to reach higher levels of revenue and

income (Argyris, 2017).

There are different benefits of an effective control system, which can be used by the

organisation to improve the timing of their decision making process. Furthermore, an effective

control system would increase the quality of information that can be received by different

departments of the organisation (Kerzner and Kerzner, 2017). This eventually helps in

minimising the lead-time that is taken for transferring data from one department to other. This

and determine whether the remuneration amount is feasible and viable for the directors or

executives.

2.2 Effectiveness of control systems within companies:

Presence of an effective control system within the organisation is essential, as it helps in

improving the efficiency of the employees and reduces the level of slack conducted by the

workforce. Without an efficient control, system organisations are not able to reduce the level of

unethical practice within the organisation and control the attributes of their workforce. Scott

(2015) mentioned that without the presence of adequate control system within the organisation

the management is not able to exercise decisions, which could improve productivity and

efficiency of the company. Without the presence of an adequate control system businesses are

not able to develop and execute strategic plans, which helps in generating higher revenue in the

end. Therefore, it could be understood that organisations using the control system are able to

fulfil their objectives and obtain sustainable growth by adequately utilising the available

resources. The organisation also needs to have an adequate internal control system to support the

legal and regulatory standards that has been imposed by the adequate authorities. Hence, it could

be understood that without the presence of effective control system organisations are not able to

operate their 100%, which directly affects their capability to reach higher levels of revenue and

income (Argyris, 2017).

There are different benefits of an effective control system, which can be used by the

organisation to improve the timing of their decision making process. Furthermore, an effective

control system would increase the quality of information that can be received by different

departments of the organisation (Kerzner and Kerzner, 2017). This eventually helps in

minimising the lead-time that is taken for transferring data from one department to other. This

6MANAGERIAL ACCOUNTING

adequate effectiveness would eventually help in reducing the time taken for the decision making

process, which increases their operating conditions This improvement in the control system

would eventually allow the organisation to successfully complete the financial report on time

without delay. Furthermore, organisations with the help of the control system are able to design

and maintain adequate executive performance and reward system, which could be used for

motivating employees. This kind of systems is eventually helpful to motivate the workforce and

minimise the employee turnover ratio of an organisation. Sayles (2017) stated that with the use

of adequate reward system organisations are able to maximize the output of a workforce present

within the company. Therefore, it can be understood that within an effective control systems the

organisation is set on right track, where the operations and efficiency would eventually improve.

3. Company reviews:

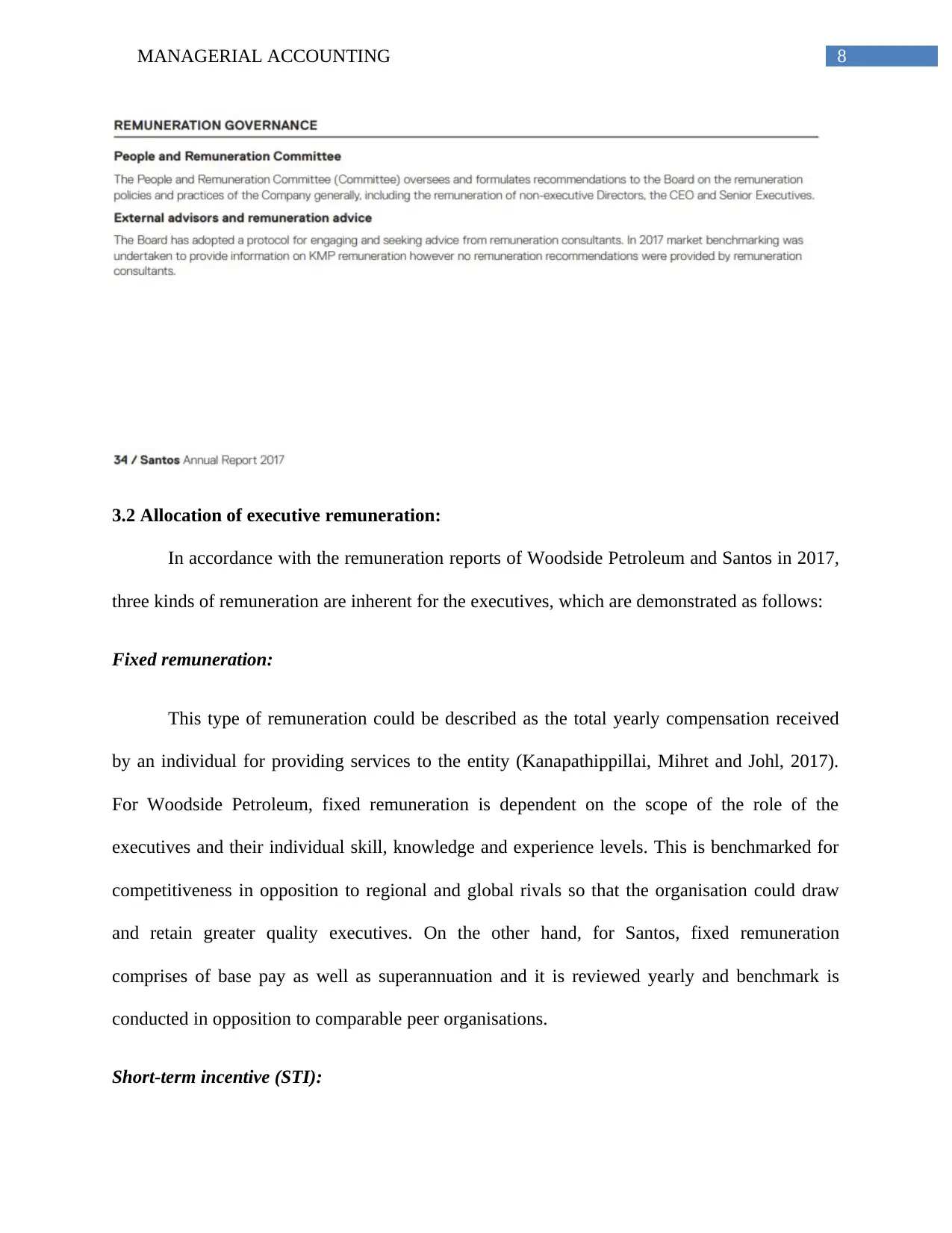

3.1 Details of remuneration committee and membership:

After critical evaluation of the annual report of Woodside Petroleum in 2017, no

disclosures have been made regarding the number of members present in the remuneration

committee, while for Santos, three members are present in the remuneration committee of the

organisation. The remuneration committee is accountable for reviewing as well as

recommending the board regarding the remuneration policy of the organisation while assessing

its efficiency and compliance with the relevant standards (Beaumont, Clarkson and Tutticci,

2018). Moreover, another responsibility of these committees is to review and recommend the

individual levels of remuneration related to the key personnel of the two organisations. The

memberships of the committees and their chairpersons would be determined based on the

business situations by the respective boards (Scott, 2015).

adequate effectiveness would eventually help in reducing the time taken for the decision making

process, which increases their operating conditions This improvement in the control system

would eventually allow the organisation to successfully complete the financial report on time

without delay. Furthermore, organisations with the help of the control system are able to design

and maintain adequate executive performance and reward system, which could be used for

motivating employees. This kind of systems is eventually helpful to motivate the workforce and

minimise the employee turnover ratio of an organisation. Sayles (2017) stated that with the use

of adequate reward system organisations are able to maximize the output of a workforce present

within the company. Therefore, it can be understood that within an effective control systems the

organisation is set on right track, where the operations and efficiency would eventually improve.

3. Company reviews:

3.1 Details of remuneration committee and membership:

After critical evaluation of the annual report of Woodside Petroleum in 2017, no

disclosures have been made regarding the number of members present in the remuneration

committee, while for Santos, three members are present in the remuneration committee of the

organisation. The remuneration committee is accountable for reviewing as well as

recommending the board regarding the remuneration policy of the organisation while assessing

its efficiency and compliance with the relevant standards (Beaumont, Clarkson and Tutticci,

2018). Moreover, another responsibility of these committees is to review and recommend the

individual levels of remuneration related to the key personnel of the two organisations. The

memberships of the committees and their chairpersons would be determined based on the

business situations by the respective boards (Scott, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

The remuneration committees of both the organisations hold time to time meetings in a

specific financial period depending on both external and internal situations. Moreover, both the

organisations use independent consultants in order to gather professional advice related to

executive remuneration as well as other matters associated remuneration and there is direct

relationship between these services and the remuneration committees (Goh and Gupta, 2016).

The chairpersons of the committee are engaged in evaluating the associations and costs to be

incurred for the management consultants. Finally, it has been identified that the remuneration

committees of both organisations obtain recommendations from their consultants to adhere to the

“Corporations Act 2001”.

The remuneration committees of both the organisations hold time to time meetings in a

specific financial period depending on both external and internal situations. Moreover, both the

organisations use independent consultants in order to gather professional advice related to

executive remuneration as well as other matters associated remuneration and there is direct

relationship between these services and the remuneration committees (Goh and Gupta, 2016).

The chairpersons of the committee are engaged in evaluating the associations and costs to be

incurred for the management consultants. Finally, it has been identified that the remuneration

committees of both organisations obtain recommendations from their consultants to adhere to the

“Corporations Act 2001”.

8MANAGERIAL ACCOUNTING

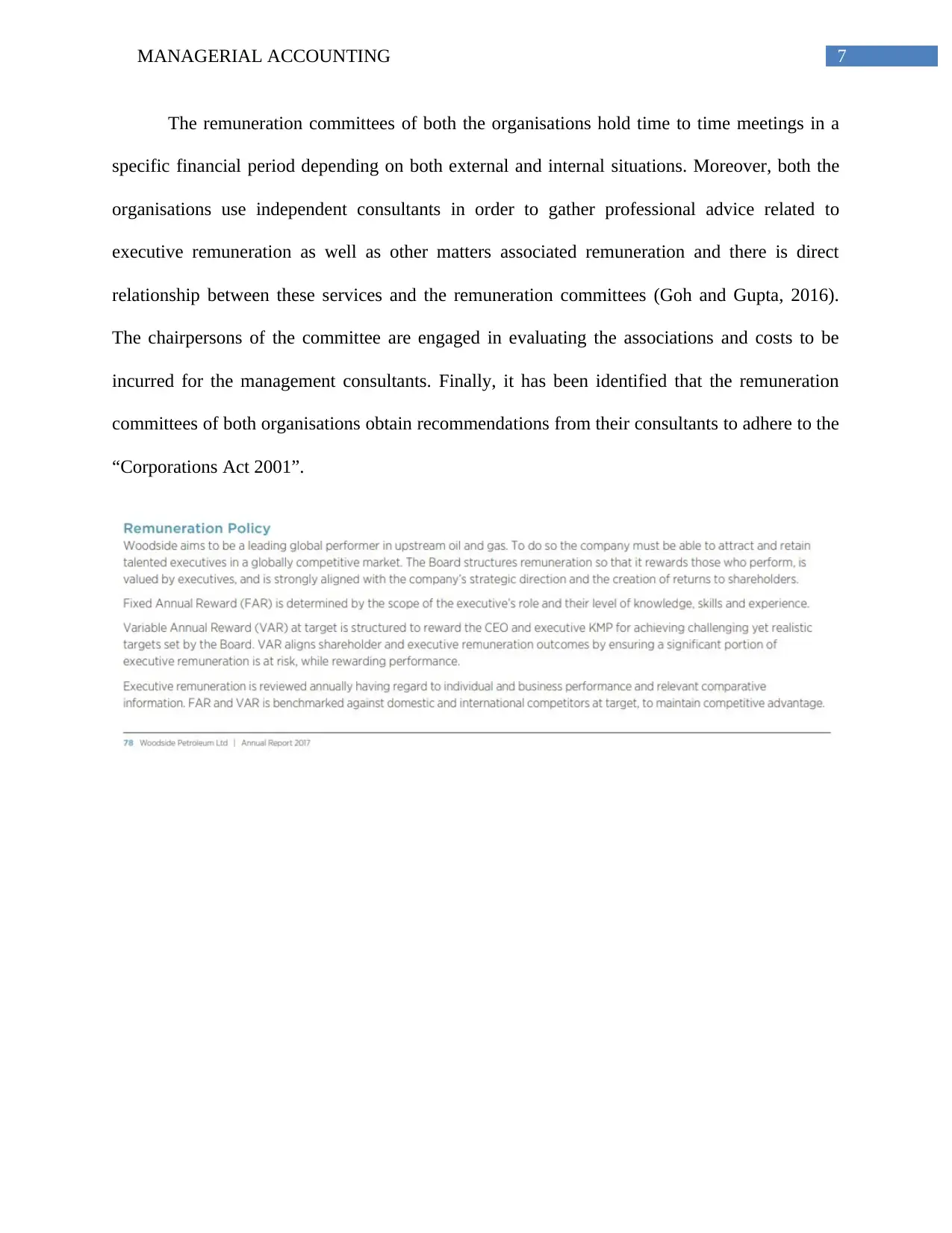

3.2 Allocation of executive remuneration:

In accordance with the remuneration reports of Woodside Petroleum and Santos in 2017,

three kinds of remuneration are inherent for the executives, which are demonstrated as follows:

Fixed remuneration:

This type of remuneration could be described as the total yearly compensation received

by an individual for providing services to the entity (Kanapathippillai, Mihret and Johl, 2017).

For Woodside Petroleum, fixed remuneration is dependent on the scope of the role of the

executives and their individual skill, knowledge and experience levels. This is benchmarked for

competitiveness in opposition to regional and global rivals so that the organisation could draw

and retain greater quality executives. On the other hand, for Santos, fixed remuneration

comprises of base pay as well as superannuation and it is reviewed yearly and benchmark is

conducted in opposition to comparable peer organisations.

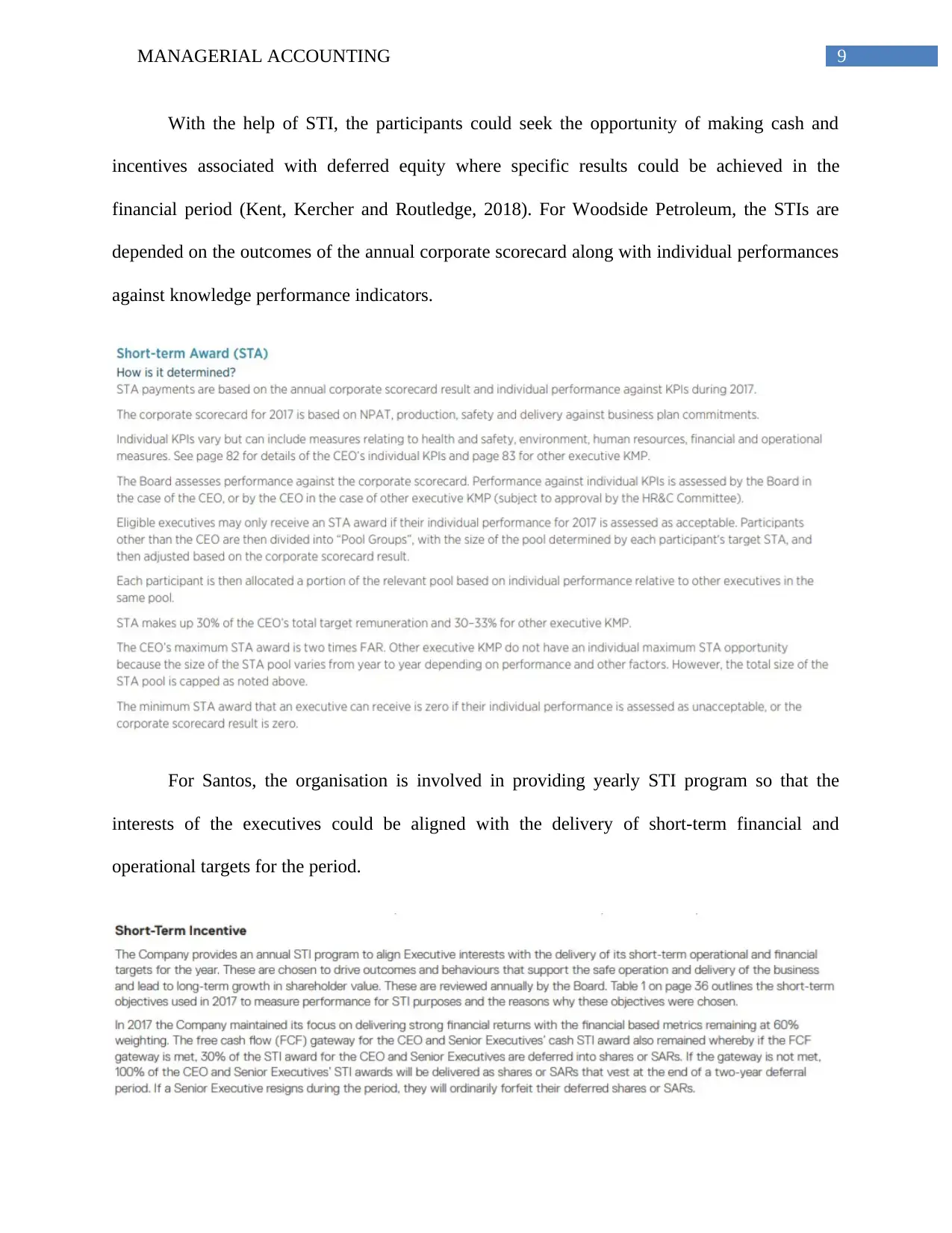

Short-term incentive (STI):

3.2 Allocation of executive remuneration:

In accordance with the remuneration reports of Woodside Petroleum and Santos in 2017,

three kinds of remuneration are inherent for the executives, which are demonstrated as follows:

Fixed remuneration:

This type of remuneration could be described as the total yearly compensation received

by an individual for providing services to the entity (Kanapathippillai, Mihret and Johl, 2017).

For Woodside Petroleum, fixed remuneration is dependent on the scope of the role of the

executives and their individual skill, knowledge and experience levels. This is benchmarked for

competitiveness in opposition to regional and global rivals so that the organisation could draw

and retain greater quality executives. On the other hand, for Santos, fixed remuneration

comprises of base pay as well as superannuation and it is reviewed yearly and benchmark is

conducted in opposition to comparable peer organisations.

Short-term incentive (STI):

9MANAGERIAL ACCOUNTING

With the help of STI, the participants could seek the opportunity of making cash and

incentives associated with deferred equity where specific results could be achieved in the

financial period (Kent, Kercher and Routledge, 2018). For Woodside Petroleum, the STIs are

depended on the outcomes of the annual corporate scorecard along with individual performances

against knowledge performance indicators.

For Santos, the organisation is involved in providing yearly STI program so that the

interests of the executives could be aligned with the delivery of short-term financial and

operational targets for the period.

With the help of STI, the participants could seek the opportunity of making cash and

incentives associated with deferred equity where specific results could be achieved in the

financial period (Kent, Kercher and Routledge, 2018). For Woodside Petroleum, the STIs are

depended on the outcomes of the annual corporate scorecard along with individual performances

against knowledge performance indicators.

For Santos, the organisation is involved in providing yearly STI program so that the

interests of the executives could be aligned with the delivery of short-term financial and

operational targets for the period.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10MANAGERIAL ACCOUNTING

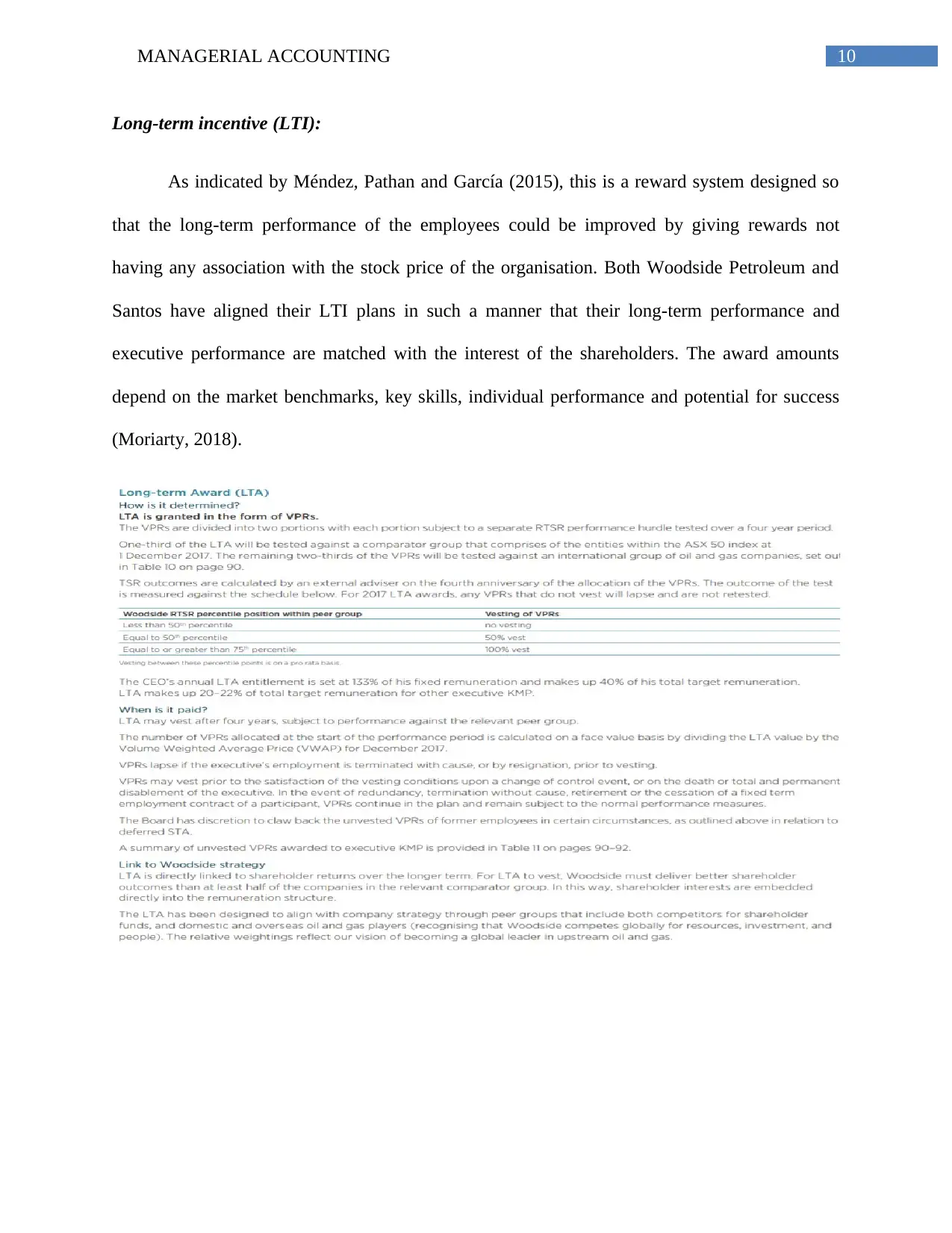

Long-term incentive (LTI):

As indicated by Méndez, Pathan and García (2015), this is a reward system designed so

that the long-term performance of the employees could be improved by giving rewards not

having any association with the stock price of the organisation. Both Woodside Petroleum and

Santos have aligned their LTI plans in such a manner that their long-term performance and

executive performance are matched with the interest of the shareholders. The award amounts

depend on the market benchmarks, key skills, individual performance and potential for success

(Moriarty, 2018).

Long-term incentive (LTI):

As indicated by Méndez, Pathan and García (2015), this is a reward system designed so

that the long-term performance of the employees could be improved by giving rewards not

having any association with the stock price of the organisation. Both Woodside Petroleum and

Santos have aligned their LTI plans in such a manner that their long-term performance and

executive performance are matched with the interest of the shareholders. The award amounts

depend on the market benchmarks, key skills, individual performance and potential for success

(Moriarty, 2018).

11MANAGERIAL ACCOUNTING

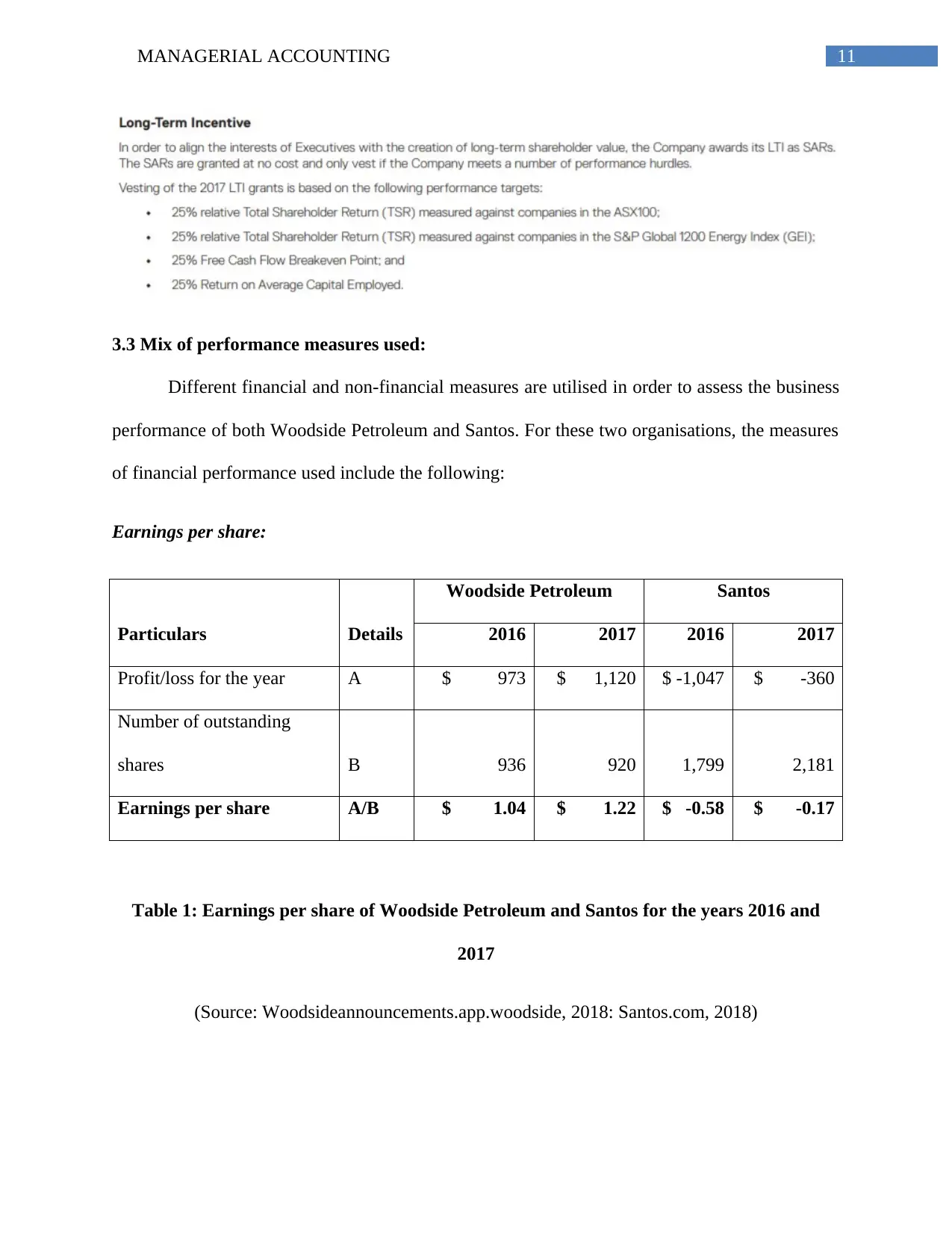

3.3 Mix of performance measures used:

Different financial and non-financial measures are utilised in order to assess the business

performance of both Woodside Petroleum and Santos. For these two organisations, the measures

of financial performance used include the following:

Earnings per share:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Profit/loss for the year A $ 973 $ 1,120 $ -1,047 $ -360

Number of outstanding

shares B 936 920 1,799 2,181

Earnings per share A/B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Table 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

3.3 Mix of performance measures used:

Different financial and non-financial measures are utilised in order to assess the business

performance of both Woodside Petroleum and Santos. For these two organisations, the measures

of financial performance used include the following:

Earnings per share:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Profit/loss for the year A $ 973 $ 1,120 $ -1,047 $ -360

Number of outstanding

shares B 936 920 1,799 2,181

Earnings per share A/B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Table 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

12MANAGERIAL ACCOUNTING

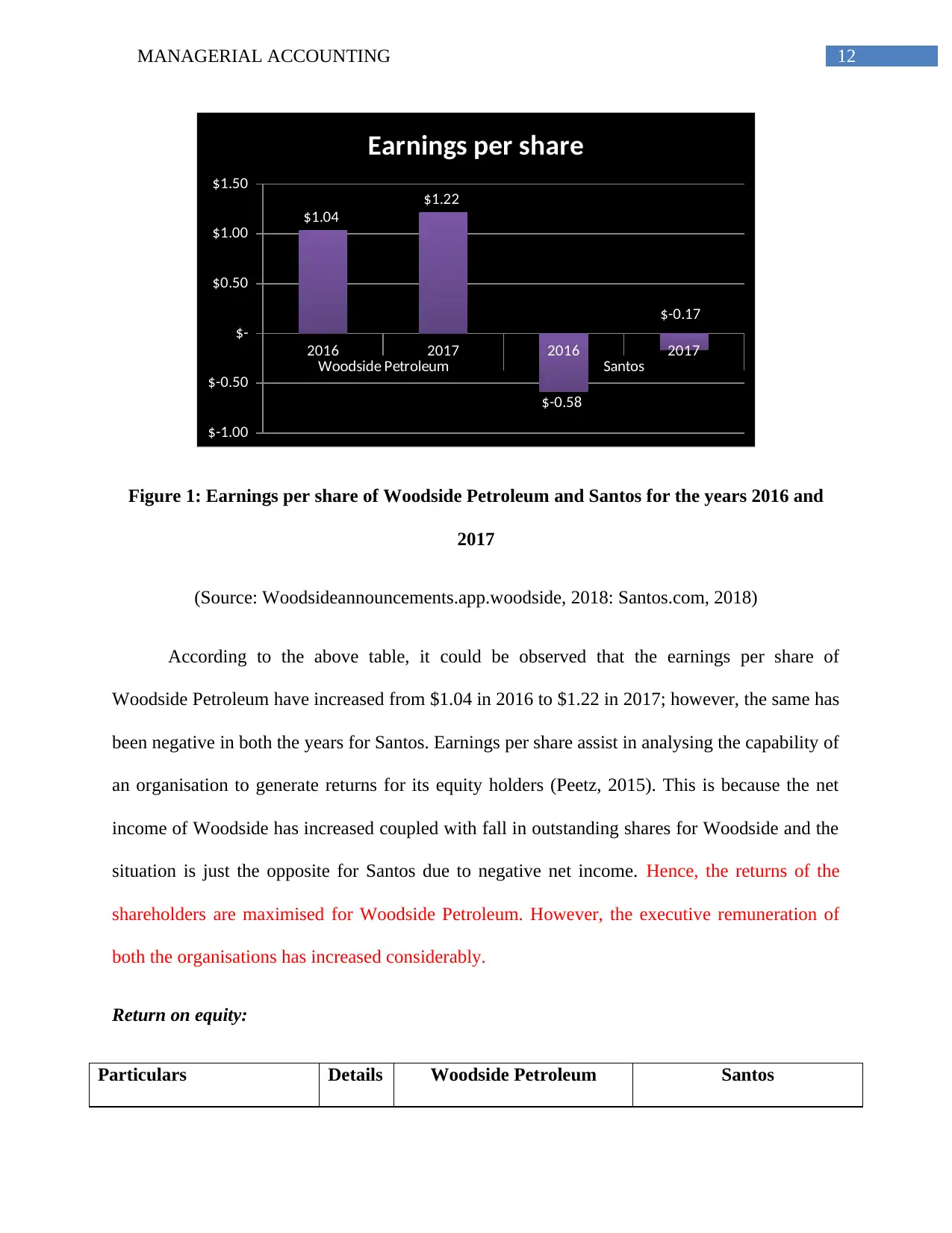

2016 2017 2016 2017

Woodside Petroleum Santos

$-1.00

$-0.50

$-

$0.50

$1.00

$1.50

$1.04

$1.22

$-0.58

$-0.17

Earnings per share

Figure 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

According to the above table, it could be observed that the earnings per share of

Woodside Petroleum have increased from $1.04 in 2016 to $1.22 in 2017; however, the same has

been negative in both the years for Santos. Earnings per share assist in analysing the capability of

an organisation to generate returns for its equity holders (Peetz, 2015). This is because the net

income of Woodside has increased coupled with fall in outstanding shares for Woodside and the

situation is just the opposite for Santos due to negative net income. Hence, the returns of the

shareholders are maximised for Woodside Petroleum. However, the executive remuneration of

both the organisations has increased considerably.

Return on equity:

Particulars Details Woodside Petroleum Santos

2016 2017 2016 2017

Woodside Petroleum Santos

$-1.00

$-0.50

$-

$0.50

$1.00

$1.50

$1.04

$1.22

$-0.58

$-0.17

Earnings per share

Figure 1: Earnings per share of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

According to the above table, it could be observed that the earnings per share of

Woodside Petroleum have increased from $1.04 in 2016 to $1.22 in 2017; however, the same has

been negative in both the years for Santos. Earnings per share assist in analysing the capability of

an organisation to generate returns for its equity holders (Peetz, 2015). This is because the net

income of Woodside has increased coupled with fall in outstanding shares for Woodside and the

situation is just the opposite for Santos due to negative net income. Hence, the returns of the

shareholders are maximised for Woodside Petroleum. However, the executive remuneration of

both the organisations has increased considerably.

Return on equity:

Particulars Details Woodside Petroleum Santos

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGERIAL ACCOUNTING

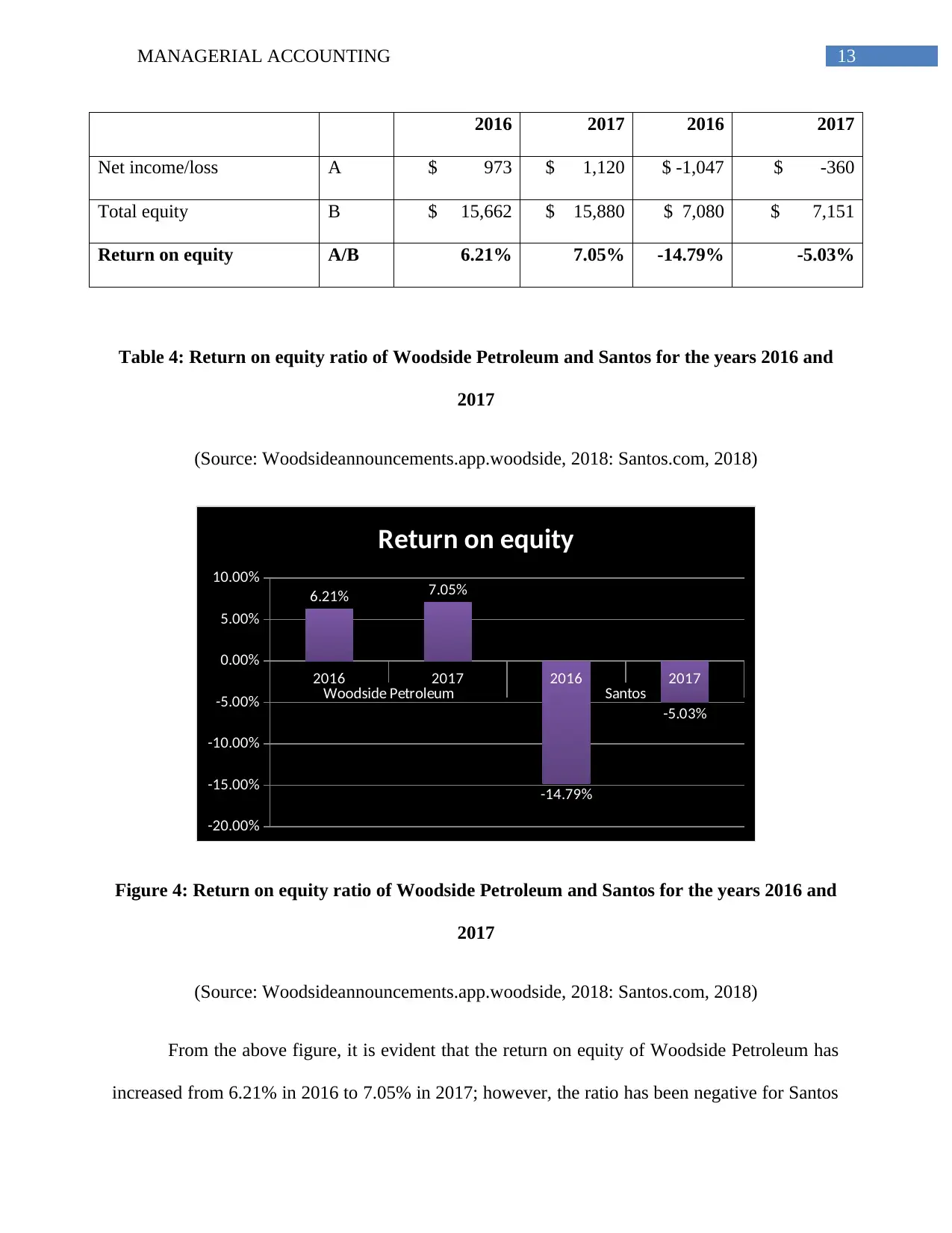

2016 2017 2016 2017

Net income/loss A $ 973 $ 1,120 $ -1,047 $ -360

Total equity B $ 15,662 $ 15,880 $ 7,080 $ 7,151

Return on equity A/B 6.21% 7.05% -14.79% -5.03%

Table 4: Return on equity ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

2016 2017 2016 2017

Woodside Petroleum Santos

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

6.21% 7.05%

-14.79%

-5.03%

Return on equity

Figure 4: Return on equity ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

From the above figure, it is evident that the return on equity of Woodside Petroleum has

increased from 6.21% in 2016 to 7.05% in 2017; however, the ratio has been negative for Santos

2016 2017 2016 2017

Net income/loss A $ 973 $ 1,120 $ -1,047 $ -360

Total equity B $ 15,662 $ 15,880 $ 7,080 $ 7,151

Return on equity A/B 6.21% 7.05% -14.79% -5.03%

Table 4: Return on equity ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

2016 2017 2016 2017

Woodside Petroleum Santos

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

6.21% 7.05%

-14.79%

-5.03%

Return on equity

Figure 4: Return on equity ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

From the above figure, it is evident that the return on equity of Woodside Petroleum has

increased from 6.21% in 2016 to 7.05% in 2017; however, the ratio has been negative for Santos

14MANAGERIAL ACCOUNTING

in 2016 and in 2017, the trend is similar as well. According to Price (2018), return on equity

measures the rate of return that the shareholders expect to earn from their investments made in

the organisation. In other words, it signifies the capability of the organisation to increase returns

on investments collected from the shareholders (Qu, et al., 2018). For Woodside, increased net

income has helped the organisation in providing adequate return on investment to the

shareholders. However, the negative net income has barred the ability of Santos to provide any

return on investment to its shareholders.

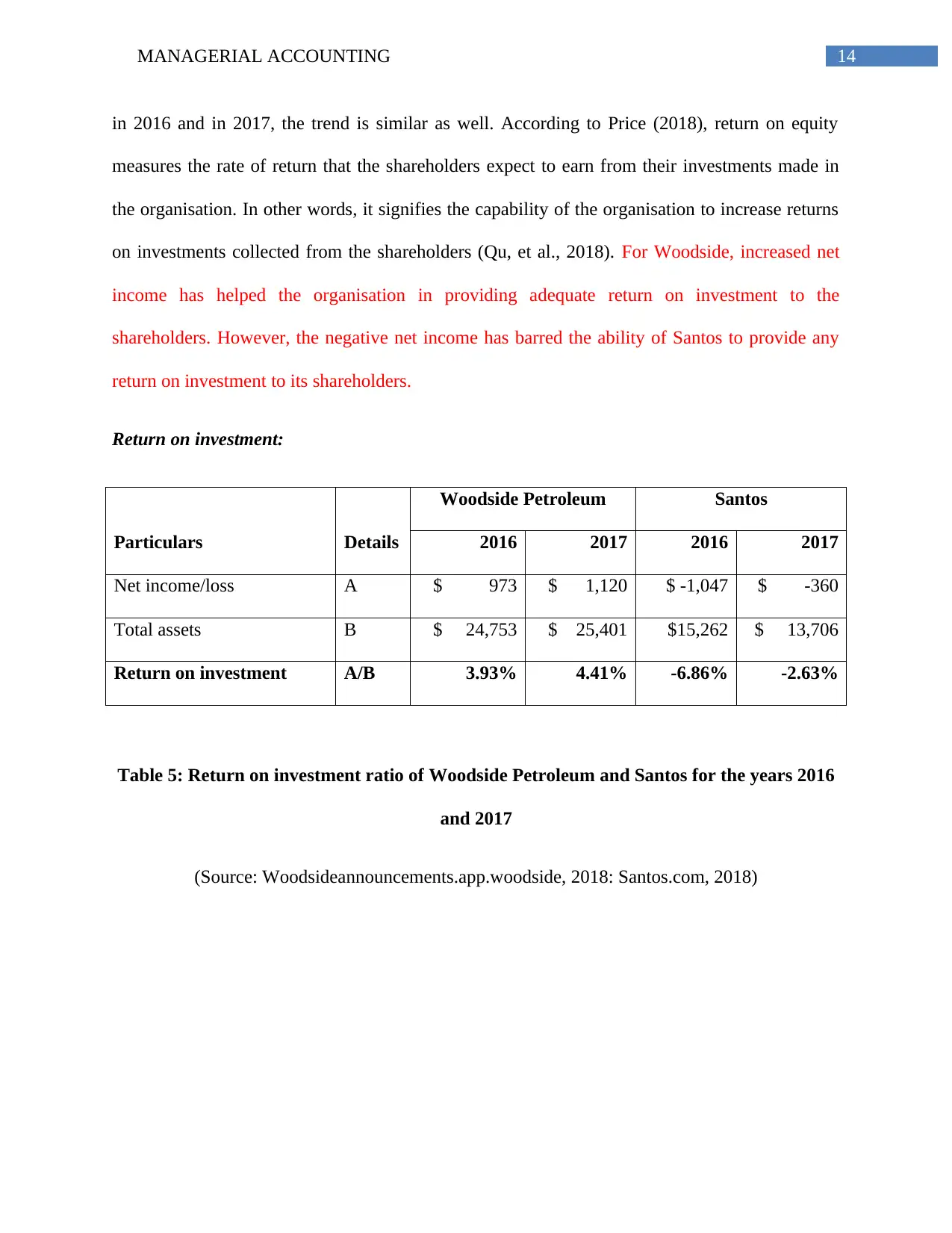

Return on investment:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Net income/loss A $ 973 $ 1,120 $ -1,047 $ -360

Total assets B $ 24,753 $ 25,401 $15,262 $ 13,706

Return on investment A/B 3.93% 4.41% -6.86% -2.63%

Table 5: Return on investment ratio of Woodside Petroleum and Santos for the years 2016

and 2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

in 2016 and in 2017, the trend is similar as well. According to Price (2018), return on equity

measures the rate of return that the shareholders expect to earn from their investments made in

the organisation. In other words, it signifies the capability of the organisation to increase returns

on investments collected from the shareholders (Qu, et al., 2018). For Woodside, increased net

income has helped the organisation in providing adequate return on investment to the

shareholders. However, the negative net income has barred the ability of Santos to provide any

return on investment to its shareholders.

Return on investment:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Net income/loss A $ 973 $ 1,120 $ -1,047 $ -360

Total assets B $ 24,753 $ 25,401 $15,262 $ 13,706

Return on investment A/B 3.93% 4.41% -6.86% -2.63%

Table 5: Return on investment ratio of Woodside Petroleum and Santos for the years 2016

and 2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

15MANAGERIAL ACCOUNTING

2016 2017 2016 2017

Woodside Petroleum Santos

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

3.93% 4.41%

-6.86%

-2.63%

Return on investment

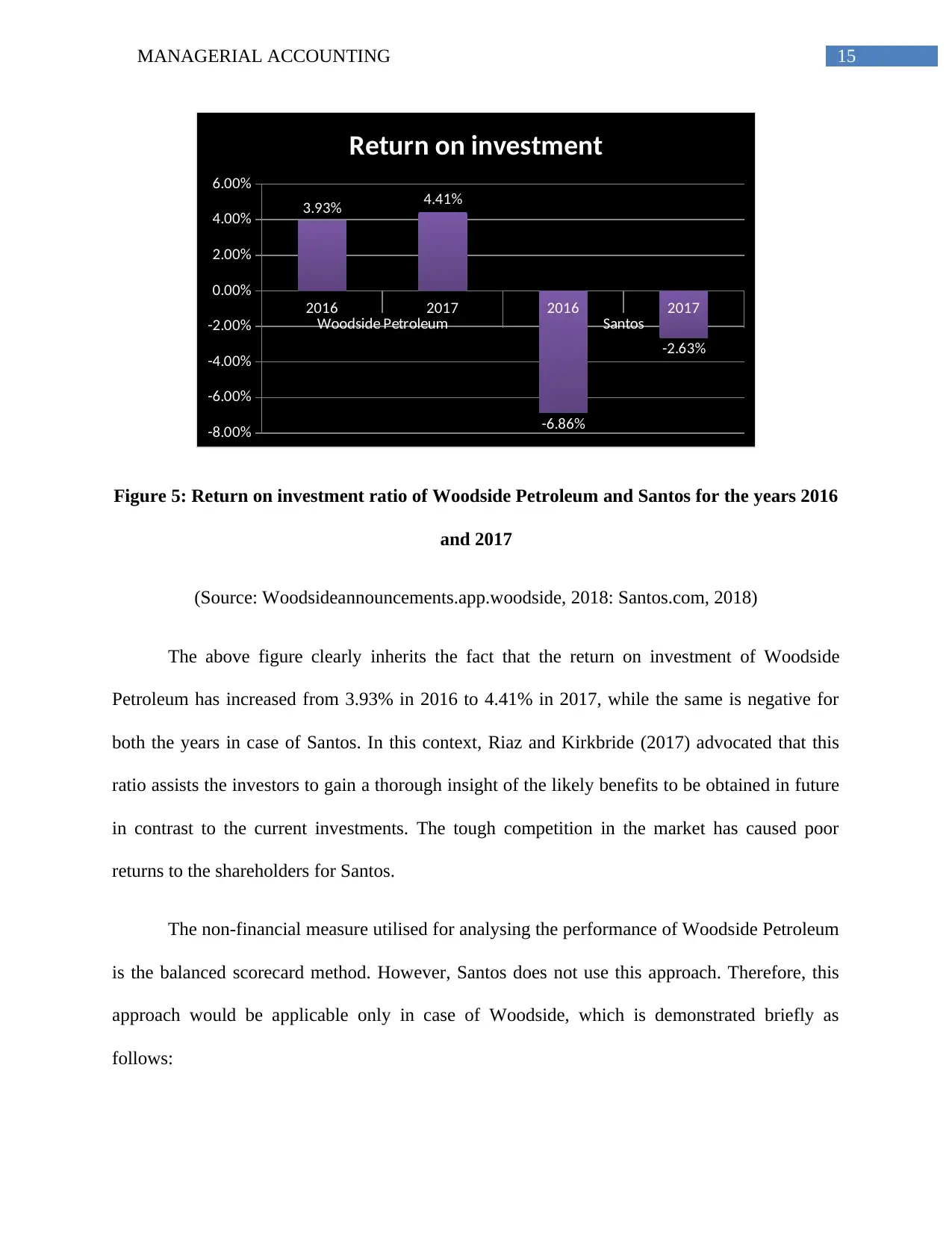

Figure 5: Return on investment ratio of Woodside Petroleum and Santos for the years 2016

and 2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

The above figure clearly inherits the fact that the return on investment of Woodside

Petroleum has increased from 3.93% in 2016 to 4.41% in 2017, while the same is negative for

both the years in case of Santos. In this context, Riaz and Kirkbride (2017) advocated that this

ratio assists the investors to gain a thorough insight of the likely benefits to be obtained in future

in contrast to the current investments. The tough competition in the market has caused poor

returns to the shareholders for Santos.

The non-financial measure utilised for analysing the performance of Woodside Petroleum

is the balanced scorecard method. However, Santos does not use this approach. Therefore, this

approach would be applicable only in case of Woodside, which is demonstrated briefly as

follows:

2016 2017 2016 2017

Woodside Petroleum Santos

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

3.93% 4.41%

-6.86%

-2.63%

Return on investment

Figure 5: Return on investment ratio of Woodside Petroleum and Santos for the years 2016

and 2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

The above figure clearly inherits the fact that the return on investment of Woodside

Petroleum has increased from 3.93% in 2016 to 4.41% in 2017, while the same is negative for

both the years in case of Santos. In this context, Riaz and Kirkbride (2017) advocated that this

ratio assists the investors to gain a thorough insight of the likely benefits to be obtained in future

in contrast to the current investments. The tough competition in the market has caused poor

returns to the shareholders for Santos.

The non-financial measure utilised for analysing the performance of Woodside Petroleum

is the balanced scorecard method. However, Santos does not use this approach. Therefore, this

approach would be applicable only in case of Woodside, which is demonstrated briefly as

follows:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16MANAGERIAL ACCOUNTING

Financial perspective:

Woodside has an objective of reducing its business expenses. This is achieved by

increasing productivity and optimising the business processes. For this, the organisation has

designed a five-year plan and the implementation process is conducted in separate steps.

Moreover, it is seen to be engaged in greater return activities so that the overall profits could be

increased. Lastly, the risks are minimised by transferring from net profit to portfolio broadening

of fee-related products. This would assist in providing protection to the bank (Riaz, Ray and Ray,

2015).

Customer perspective:

Woodside has formulated a long-term plan so that sufficient customers could be

ensured for positive financial performance. It has kept aside considerable amount of funds for

research and development to gain additional knowledge about the customers for meeting their

needs in a better manner (Riaz, Ray and Ray, 2015).

Internal processes perspective:

After identification of customer needs, Woodside is involved in cross-selling of

products because it has the availability of proactive staffs. This has been possible due to the

strong interpersonal relationships maintained by the employees with the customers.

Learning and growth perspective:

Balanced scorecard is used so that additional motivation could be provided to the

employees in order to ensure positive work results. In addition, resources are assigned in those

areas having the potential of fetching maximum profits.

Financial perspective:

Woodside has an objective of reducing its business expenses. This is achieved by

increasing productivity and optimising the business processes. For this, the organisation has

designed a five-year plan and the implementation process is conducted in separate steps.

Moreover, it is seen to be engaged in greater return activities so that the overall profits could be

increased. Lastly, the risks are minimised by transferring from net profit to portfolio broadening

of fee-related products. This would assist in providing protection to the bank (Riaz, Ray and Ray,

2015).

Customer perspective:

Woodside has formulated a long-term plan so that sufficient customers could be

ensured for positive financial performance. It has kept aside considerable amount of funds for

research and development to gain additional knowledge about the customers for meeting their

needs in a better manner (Riaz, Ray and Ray, 2015).

Internal processes perspective:

After identification of customer needs, Woodside is involved in cross-selling of

products because it has the availability of proactive staffs. This has been possible due to the

strong interpersonal relationships maintained by the employees with the customers.

Learning and growth perspective:

Balanced scorecard is used so that additional motivation could be provided to the

employees in order to ensure positive work results. In addition, resources are assigned in those

areas having the potential of fetching maximum profits.

17MANAGERIAL ACCOUNTING

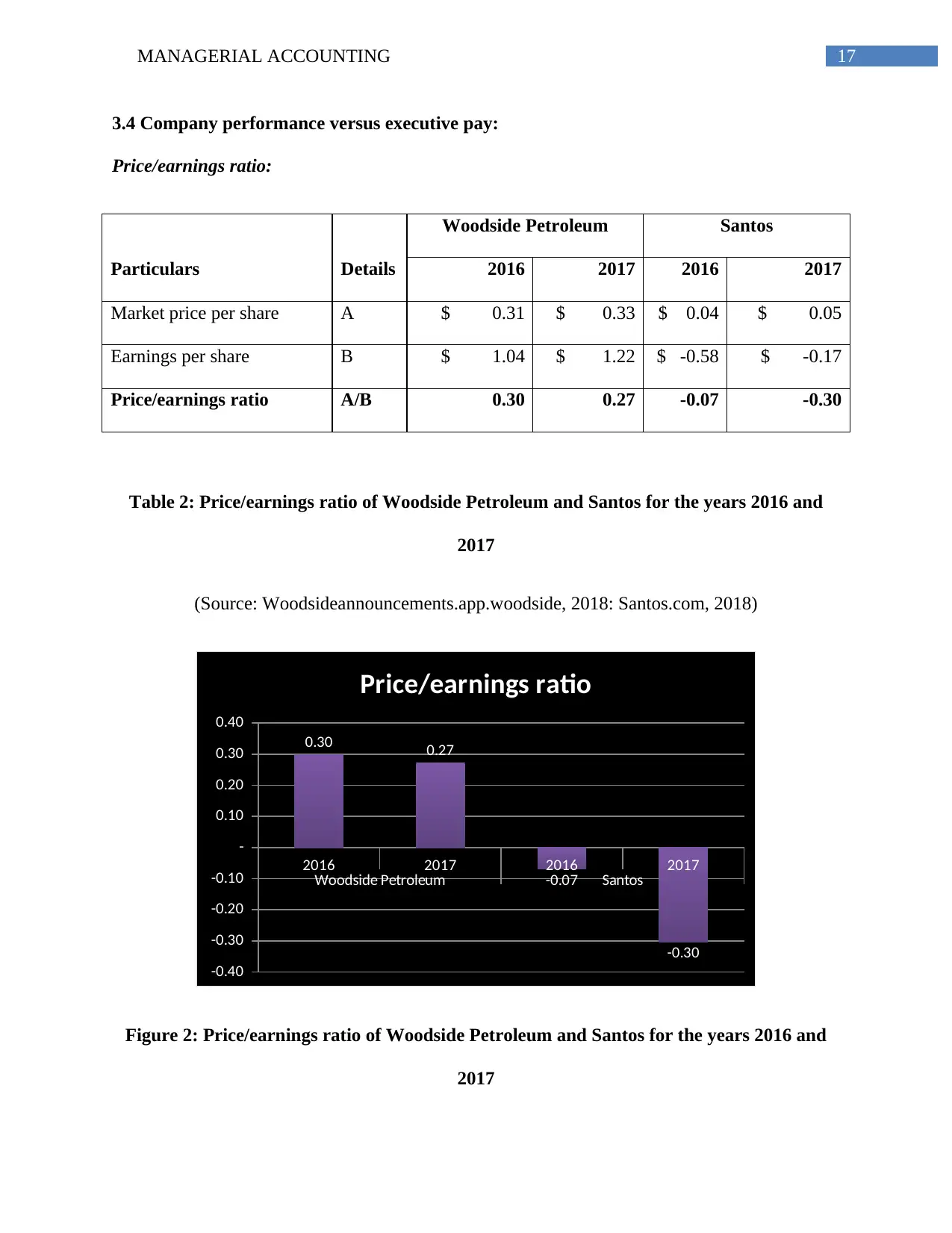

3.4 Company performance versus executive pay:

Price/earnings ratio:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Market price per share A $ 0.31 $ 0.33 $ 0.04 $ 0.05

Earnings per share B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Price/earnings ratio A/B 0.30 0.27 -0.07 -0.30

Table 2: Price/earnings ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

2016 2017 2016 2017

Woodside Petroleum Santos

-0.40

-0.30

-0.20

-0.10

-

0.10

0.20

0.30

0.40

0.30 0.27

-0.07

-0.30

Price/earnings ratio

Figure 2: Price/earnings ratio of Woodside Petroleum and Santos for the years 2016 and

2017

3.4 Company performance versus executive pay:

Price/earnings ratio:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Market price per share A $ 0.31 $ 0.33 $ 0.04 $ 0.05

Earnings per share B $ 1.04 $ 1.22 $ -0.58 $ -0.17

Price/earnings ratio A/B 0.30 0.27 -0.07 -0.30

Table 2: Price/earnings ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

2016 2017 2016 2017

Woodside Petroleum Santos

-0.40

-0.30

-0.20

-0.10

-

0.10

0.20

0.30

0.40

0.30 0.27

-0.07

-0.30

Price/earnings ratio

Figure 2: Price/earnings ratio of Woodside Petroleum and Santos for the years 2016 and

2017

18MANAGERIAL ACCOUNTING

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

According to the above figure, it has been identified that there has been slight decline in

price/earnings ratio for Woodside, while the same is negative for Santos. The standard ratio is

considered to be above 1 (Riaz, et al., 2015). However, the future earnings are expected to

increase for Woodside in future. Therefore, it could be said that the executive remuneration of

the organisation is in line with the financial performance.

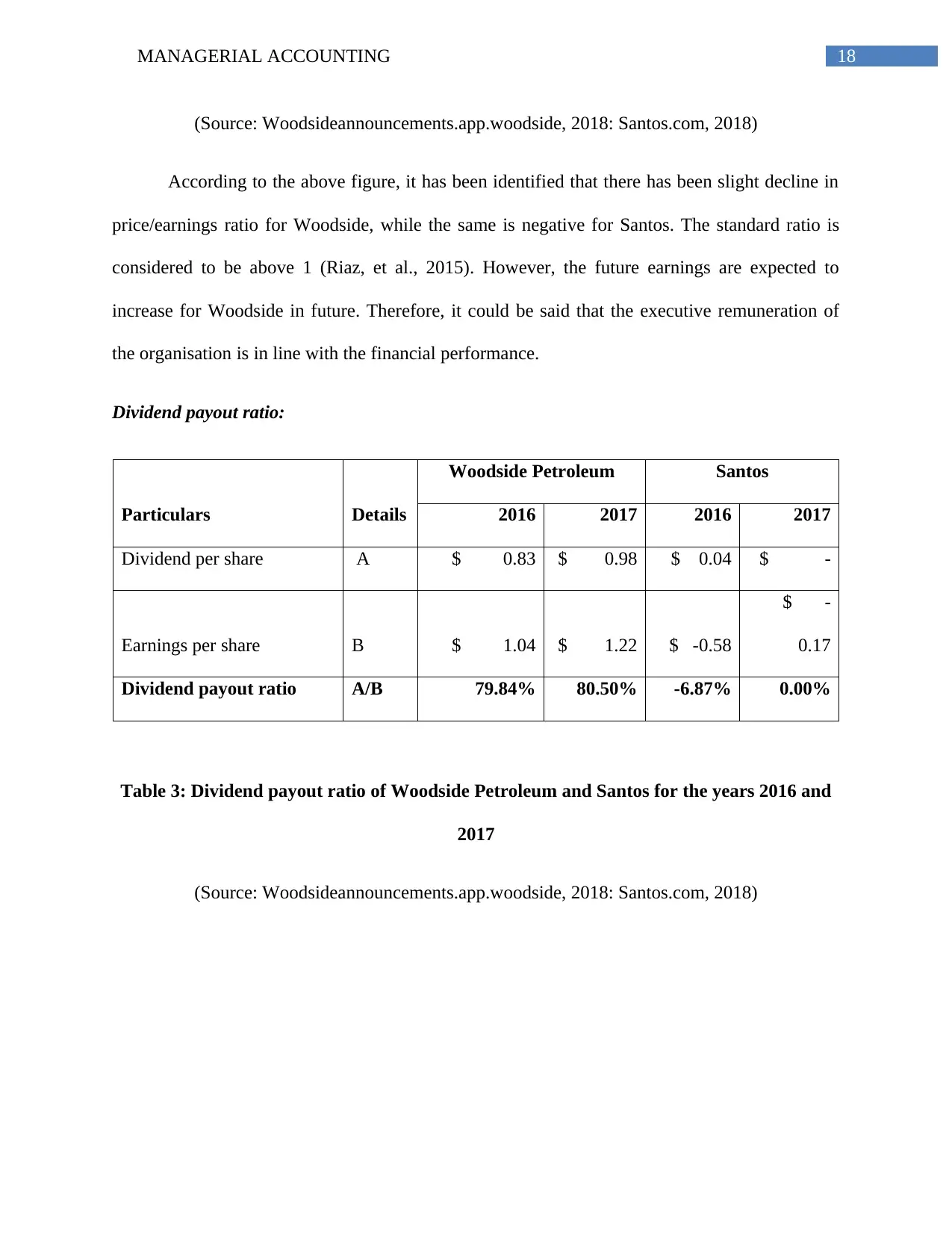

Dividend payout ratio:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Dividend per share A $ 0.83 $ 0.98 $ 0.04 $ -

Earnings per share B $ 1.04 $ 1.22 $ -0.58

$ -

0.17

Dividend payout ratio A/B 79.84% 80.50% -6.87% 0.00%

Table 3: Dividend payout ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

According to the above figure, it has been identified that there has been slight decline in

price/earnings ratio for Woodside, while the same is negative for Santos. The standard ratio is

considered to be above 1 (Riaz, et al., 2015). However, the future earnings are expected to

increase for Woodside in future. Therefore, it could be said that the executive remuneration of

the organisation is in line with the financial performance.

Dividend payout ratio:

Particulars Details

Woodside Petroleum Santos

2016 2017 2016 2017

Dividend per share A $ 0.83 $ 0.98 $ 0.04 $ -

Earnings per share B $ 1.04 $ 1.22 $ -0.58

$ -

0.17

Dividend payout ratio A/B 79.84% 80.50% -6.87% 0.00%

Table 3: Dividend payout ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19MANAGERIAL ACCOUNTING

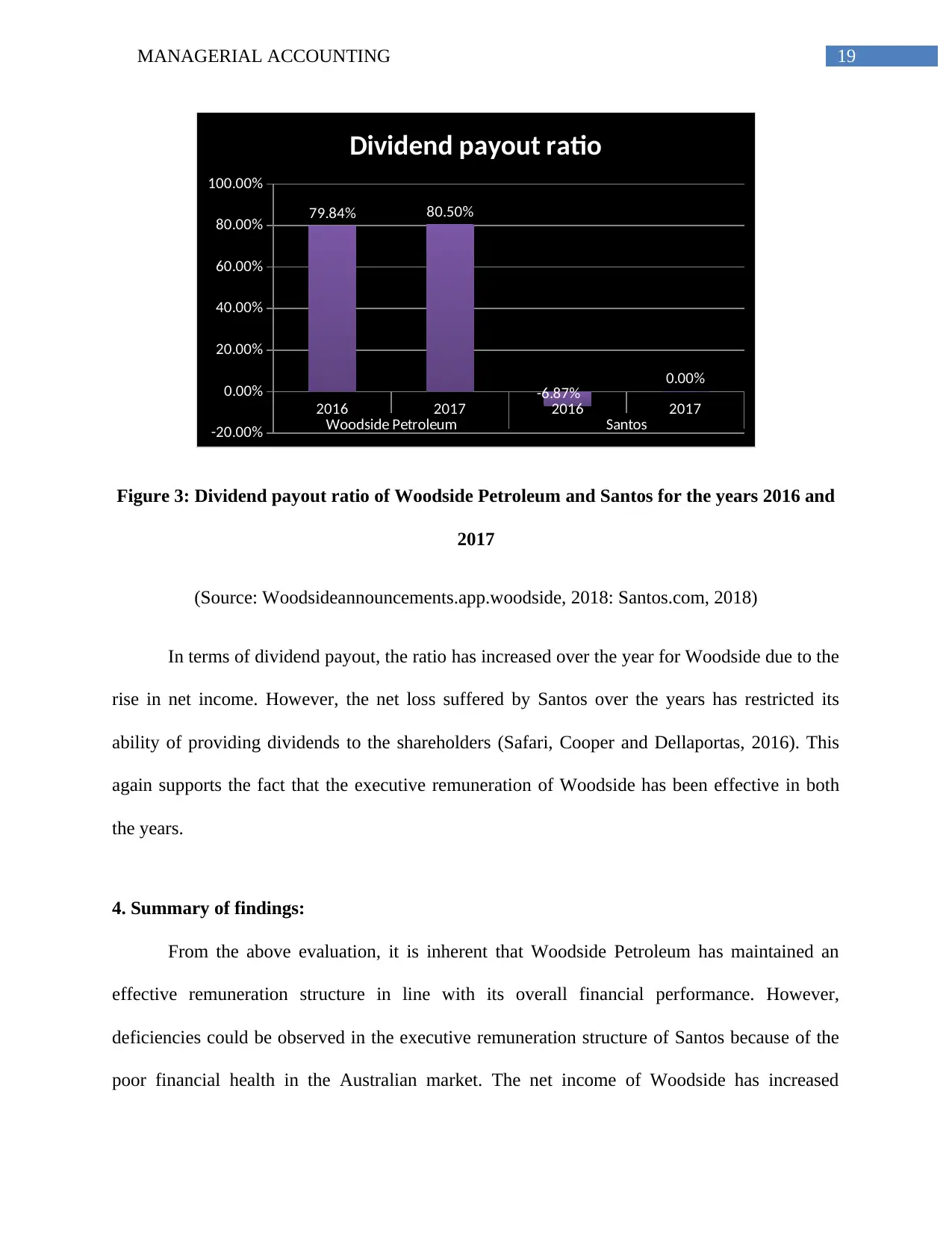

2016 2017 2016 2017

Woodside Petroleum Santos-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

79.84% 80.50%

-6.87% 0.00%

Dividend payout ratio

Figure 3: Dividend payout ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

In terms of dividend payout, the ratio has increased over the year for Woodside due to the

rise in net income. However, the net loss suffered by Santos over the years has restricted its

ability of providing dividends to the shareholders (Safari, Cooper and Dellaportas, 2016). This

again supports the fact that the executive remuneration of Woodside has been effective in both

the years.

4. Summary of findings:

From the above evaluation, it is inherent that Woodside Petroleum has maintained an

effective remuneration structure in line with its overall financial performance. However,

deficiencies could be observed in the executive remuneration structure of Santos because of the

poor financial health in the Australian market. The net income of Woodside has increased

2016 2017 2016 2017

Woodside Petroleum Santos-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

79.84% 80.50%

-6.87% 0.00%

Dividend payout ratio

Figure 3: Dividend payout ratio of Woodside Petroleum and Santos for the years 2016 and

2017

(Source: Woodsideannouncements.app.woodside, 2018: Santos.com, 2018)

In terms of dividend payout, the ratio has increased over the year for Woodside due to the

rise in net income. However, the net loss suffered by Santos over the years has restricted its

ability of providing dividends to the shareholders (Safari, Cooper and Dellaportas, 2016). This

again supports the fact that the executive remuneration of Woodside has been effective in both

the years.

4. Summary of findings:

From the above evaluation, it is inherent that Woodside Petroleum has maintained an

effective remuneration structure in line with its overall financial performance. However,

deficiencies could be observed in the executive remuneration structure of Santos because of the

poor financial health in the Australian market. The net income of Woodside has increased

20MANAGERIAL ACCOUNTING

coupled with fall in outstanding shares for Woodside and the situation is just the opposite for

Santos due to negative net income. Hence, the returns of the shareholders are maximised for

Woodside Petroleum. Woodside has formulated a long-term plan so that sufficient customers

could be ensured for positive financial performance. It has kept aside considerable amount of

funds for research and development to gain additional knowledge about the customers for

meeting their needs in a better manner Moreover, the other financial measures reveal the same

scenario and in terms of non-financial measures, Woodside is placed in a favourable position in

contrast to Santos (Riaz, et al., 2015).

5. Analysis and comparison of remuneration methods used:

5.1 Best result in terms of shareholder returns:

The shareholders return refers to the measurement of performance of the companies by

analysing the stock and shares over a specified time period. In the chosen company of Woodside

petroleum, they have a clear strategy to deliver the shareholders returns in three horizons with

respect to time. The horizon 1 consists of the year from 2017 to 2021; the horizon 2 includes the

year from 2022 to 2026 and the horizon of the years after 2027. The horizons are cash

generation, lower capital intensity development and unlocking the values. Safety integrity and

reliability in the production of hydrocarbon products helps in achieving the superior shareholders

return (Fuzi, Halim and Julizaerma, 2016). In 2017 the EPS was 122 cents for Woodside

petroleum and 51.6 cents for Santos. In comparison with the Santos Annual Report 2017, it can

be identified that share price and dividend yield is taken in consideration to measure the

shareholders return. However, in the annual report, the Board of directors of the company of

Santos there is no declaration of the final dividend. The company is confident that prioritising

coupled with fall in outstanding shares for Woodside and the situation is just the opposite for

Santos due to negative net income. Hence, the returns of the shareholders are maximised for

Woodside Petroleum. Woodside has formulated a long-term plan so that sufficient customers

could be ensured for positive financial performance. It has kept aside considerable amount of

funds for research and development to gain additional knowledge about the customers for

meeting their needs in a better manner Moreover, the other financial measures reveal the same

scenario and in terms of non-financial measures, Woodside is placed in a favourable position in

contrast to Santos (Riaz, et al., 2015).

5. Analysis and comparison of remuneration methods used:

5.1 Best result in terms of shareholder returns:

The shareholders return refers to the measurement of performance of the companies by

analysing the stock and shares over a specified time period. In the chosen company of Woodside

petroleum, they have a clear strategy to deliver the shareholders returns in three horizons with

respect to time. The horizon 1 consists of the year from 2017 to 2021; the horizon 2 includes the

year from 2022 to 2026 and the horizon of the years after 2027. The horizons are cash

generation, lower capital intensity development and unlocking the values. Safety integrity and

reliability in the production of hydrocarbon products helps in achieving the superior shareholders

return (Fuzi, Halim and Julizaerma, 2016). In 2017 the EPS was 122 cents for Woodside

petroleum and 51.6 cents for Santos. In comparison with the Santos Annual Report 2017, it can

be identified that share price and dividend yield is taken in consideration to measure the

shareholders return. However, in the annual report, the Board of directors of the company of

Santos there is no declaration of the final dividend. The company is confident that prioritising

21MANAGERIAL ACCOUNTING

debt repayment is the right course of action to position the company to fund growth opportunities

from a position of strength and obtain shareholder returns that is sustainable (Santos.com, 2018).

5.2 Best result in short-term:

The key short terms results for Woodside Petroleum needs to be inferred with the start up

of Brunelio field in 2017. In addition to this, it is also able to become the First LNG production

team from Train 1. The production of the LNG Train 1 was commenced after the LNG cargo was

delivered to japan in 12 November 2017. The domestic gas plant with a producing capacity of

200TJ every day is also depicted to be most noted perk of the company. The company was also

able to commence the processing options for the third-party petroleum contracts from 2017

which has been seen to take the production of the company to a new level (Kannadhasan, Goyal

and Charan, 2016).

The best short-term results for Santos need to be considered with the reduction of the

carbon emissions and displacing of the coal with natural gas. It has been also seen that various

types of the improvement measures initiatives taken by the company are evident with the

economic development which are combined with the renewable energy solution and combined

gas. The company is also seen to hold a significant position as a national supplier of domestic

gas in Australia (Allen, Carletti and Marquez, 2015). Some of the various types of the other

initiatives of the company need to be also considered as per the increasing LNG sales among the

Asian consumers. In a very short period of time span the company has been able to prove itself

as the market leader for the lowest cost facilitator in Australia. This is also associated to the

positive contribution towards the communities pertaining to provide the jobs for the supply of the

various types of the impediments of the energy supply and local partnerships. Some of the other

debt repayment is the right course of action to position the company to fund growth opportunities

from a position of strength and obtain shareholder returns that is sustainable (Santos.com, 2018).

5.2 Best result in short-term:

The key short terms results for Woodside Petroleum needs to be inferred with the start up

of Brunelio field in 2017. In addition to this, it is also able to become the First LNG production

team from Train 1. The production of the LNG Train 1 was commenced after the LNG cargo was

delivered to japan in 12 November 2017. The domestic gas plant with a producing capacity of

200TJ every day is also depicted to be most noted perk of the company. The company was also

able to commence the processing options for the third-party petroleum contracts from 2017

which has been seen to take the production of the company to a new level (Kannadhasan, Goyal

and Charan, 2016).

The best short-term results for Santos need to be considered with the reduction of the

carbon emissions and displacing of the coal with natural gas. It has been also seen that various

types of the improvement measures initiatives taken by the company are evident with the

economic development which are combined with the renewable energy solution and combined

gas. The company is also seen to hold a significant position as a national supplier of domestic

gas in Australia (Allen, Carletti and Marquez, 2015). Some of the various types of the other

initiatives of the company need to be also considered as per the increasing LNG sales among the

Asian consumers. In a very short period of time span the company has been able to prove itself

as the market leader for the lowest cost facilitator in Australia. This is also associated to the

positive contribution towards the communities pertaining to provide the jobs for the supply of the

various types of the impediments of the energy supply and local partnerships. Some of the other

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22MANAGERIAL ACCOUNTING

developmental opportunities of the company need to be identified with the improvements as per

delivering the cultural responsibilities (Salman and Hassan, 2016).

5.3 Best result in long-term:

The prime aspects for the long-term performance increase of Woodside Petroleum are

depicted with various types of the increased profit after tax has increased by 18%. In terms of the

long term financial highlight the company has generated a cash flow $ 832 million. It needs to be

also understood that the company was able to achieve the long-term goal of the maintaining unit

production of $ 5.2/boe and decreasing overall total recordable injury rate by 21% in 2017. The

delivery of the near-term production of the production growth of the company is depicted is seen

with the depicted with the consideration of the various types of the project which are considered

as the commence of greater Enfield drilling project and commissions of the greater western flank

infrastructure (Petria, Capraru and Ihnatov, 2015).

The long-term project goals of Santos are achieved with the depiction of the strong

performance in terms of the sales volume, production and sales revenue. The cash flow

transformation and the underlying increase in the profit has been considered with the various

types of the increase which are relevant as per the increasing operating cash flow. However, in

compared to free cash flow the company has been depicted with a decreasing performance,

which is seen to be evident with a decrease over the next four years (Pigé, 2017). The company

has been further able to maintain a lower cost pertaining to the unit production cost. This has

been also significant reduction in the capital expenditure. The long-term improvement off the

company is seen to be evident with the decrease in the total debt in the last four years (Shah and

Arora, 2014).

developmental opportunities of the company need to be identified with the improvements as per

delivering the cultural responsibilities (Salman and Hassan, 2016).

5.3 Best result in long-term:

The prime aspects for the long-term performance increase of Woodside Petroleum are

depicted with various types of the increased profit after tax has increased by 18%. In terms of the

long term financial highlight the company has generated a cash flow $ 832 million. It needs to be

also understood that the company was able to achieve the long-term goal of the maintaining unit

production of $ 5.2/boe and decreasing overall total recordable injury rate by 21% in 2017. The

delivery of the near-term production of the production growth of the company is depicted is seen

with the depicted with the consideration of the various types of the project which are considered

as the commence of greater Enfield drilling project and commissions of the greater western flank

infrastructure (Petria, Capraru and Ihnatov, 2015).

The long-term project goals of Santos are achieved with the depiction of the strong

performance in terms of the sales volume, production and sales revenue. The cash flow

transformation and the underlying increase in the profit has been considered with the various

types of the increase which are relevant as per the increasing operating cash flow. However, in

compared to free cash flow the company has been depicted with a decreasing performance,

which is seen to be evident with a decrease over the next four years (Pigé, 2017). The company

has been further able to maintain a lower cost pertaining to the unit production cost. This has

been also significant reduction in the capital expenditure. The long-term improvement off the

company is seen to be evident with the decrease in the total debt in the last four years (Shah and

Arora, 2014).

23MANAGERIAL ACCOUNTING

6. Conclusion:

The overall findings of the report have been able to state that Woodside petroleum is

depicted to be in a better position in terms of the Executive performance and remuneration in

public companies. In addition to this, it needs to be also seen that the Effectiveness of control

systems is seen to be in a better position for the Woodside petroleum. It needs to be also seen

that there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million. Santos on the other hand has been depicted with a decreasing

performance, which is seen to be evident with a decrease over the next four years. It needs to be

also discerned that WoodSide petroleum has been depicted with a better mix of performance

measures used. It needs to be also discerned that in 2017 the EPS was 122 cents for Woodside

petroleum and 51.6 cents for Santos. In comparison with the Santos Annual Report 2017, it can

be identified that share price and dividend yield is taken in consideration to measure the

shareholders return. However; in the annual report, the Board of directors of the company of

Santos there is no declaration of the final dividend.

6. Conclusion:

The overall findings of the report have been able to state that Woodside petroleum is

depicted to be in a better position in terms of the Executive performance and remuneration in

public companies. In addition to this, it needs to be also seen that the Effectiveness of control

systems is seen to be in a better position for the Woodside petroleum. It needs to be also seen

that there has been considerable amount of improvement as per the allocation of executive

remuneration for WoodSide petroleum in compared to Santos. In terms of the long term financial

highlight the company is depicted to be in a better position. This is evident with a cash flow

generation of $ 832 million. Santos on the other hand has been depicted with a decreasing

performance, which is seen to be evident with a decrease over the next four years. It needs to be

also discerned that WoodSide petroleum has been depicted with a better mix of performance

measures used. It needs to be also discerned that in 2017 the EPS was 122 cents for Woodside

petroleum and 51.6 cents for Santos. In comparison with the Santos Annual Report 2017, it can

be identified that share price and dividend yield is taken in consideration to measure the

shareholders return. However; in the annual report, the Board of directors of the company of

Santos there is no declaration of the final dividend.

24MANAGERIAL ACCOUNTING

References:

Allen, F., Carletti, E. and Marquez, R., 2015. Deposits and bank capital structure. Journal of

Financial Economics, 118(3), pp.601-619.

Argyris, C., 2017. Integrating the Individual and the Organisation. Routledge.

Beaumont, S., Clarkson, P. and Tutticci, I., 2018. Identifying lobbying strategies: An analysis of

public responses to the Productivity Commission Inquiry into executive remuneration in

Australia. Journal of Contemporary Accounting & Economics, 14(3), pp.288-306.

Faghani, M., Monem, R. and Ng, C., 2015. Say on pay regulation and chief executive officer

pay: Evidence from Australia. Corporate Ownership and Control, 12(3), pp.28-39.

Fuzi, S.F.S., Halim, S.A.A. and Julizaerma, M.K., 2016. Board independence and firm

performance. Procedia Economics and Finance, 37, pp.460-465.

Goh, L. and Gupta, A., 2016. Remuneration of non-executive directors: Evidence from the

UK. The British Accounting Review, 48(3), pp.379-399.

Hooghiemstra, R., Kuang, Y.F. and Qin, B., 2017. Does obfuscating excessive CEO pay work?

The influence of remuneration report readability on say-on-pay votes. Accounting and Business

Research, 47(6), pp.695-729.

Kanapathippillai, S., Mihret, D. and Johl, S., 2017. Remuneration Committees and Attribution

Disclosures on Remuneration Decisions: Australian Evidence. Journal of Business Ethics, pp.1-

20.

References:

Allen, F., Carletti, E. and Marquez, R., 2015. Deposits and bank capital structure. Journal of

Financial Economics, 118(3), pp.601-619.

Argyris, C., 2017. Integrating the Individual and the Organisation. Routledge.

Beaumont, S., Clarkson, P. and Tutticci, I., 2018. Identifying lobbying strategies: An analysis of

public responses to the Productivity Commission Inquiry into executive remuneration in

Australia. Journal of Contemporary Accounting & Economics, 14(3), pp.288-306.

Faghani, M., Monem, R. and Ng, C., 2015. Say on pay regulation and chief executive officer

pay: Evidence from Australia. Corporate Ownership and Control, 12(3), pp.28-39.

Fuzi, S.F.S., Halim, S.A.A. and Julizaerma, M.K., 2016. Board independence and firm

performance. Procedia Economics and Finance, 37, pp.460-465.

Goh, L. and Gupta, A., 2016. Remuneration of non-executive directors: Evidence from the

UK. The British Accounting Review, 48(3), pp.379-399.

Hooghiemstra, R., Kuang, Y.F. and Qin, B., 2017. Does obfuscating excessive CEO pay work?

The influence of remuneration report readability on say-on-pay votes. Accounting and Business

Research, 47(6), pp.695-729.

Kanapathippillai, S., Mihret, D. and Johl, S., 2017. Remuneration Committees and Attribution

Disclosures on Remuneration Decisions: Australian Evidence. Journal of Business Ethics, pp.1-

20.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

25MANAGERIAL ACCOUNTING

Kannadhasan, M., Goyal, V. and Charan, P., 2016. The Role of Financial Performance as a

Moderator on the Relationship Between Financial Leverage and Shareholders Return. Journal of

Modern Accounting and Auditing, 12(7), pp.379-387.

Kent, P., Kercher, K. and Routledge, J., 2018. Remuneration committees, shareholder dissent on

CEO pay and the CEO pay–performance link. Accounting & Finance, 58(2), pp.445-475.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

Méndez, C.F., Pathan, S. and García, R.A., 2015. Monitoring capabilities of busy and overlap

directors: Evidence from Australia. Pacific-Basin Finance Journal, 35, pp.444-469.

Moriarty, R., 2018. Asic highlights the importance of annual general meetings and recent trends

in corporate governance. Governance Directions, 70(2), pp.77-81.

Peetz, D., 2015. An institutional analysis of the growth of executive remuneration. Journal of

Industrial Relations, 57(5), pp.707-725.

Petria, N., Capraru, B. and Ihnatov, I., 2015. Determinants of banks’ profitability: evidence from

EU 27 banking systems. Procedia Economics and Finance, 20, pp.518-524.

Pigé, B., 2017. Stakeholder theory and corporate governance: the nature of the board

information. Management: journal of contemporary management issues, 7(1), pp.1-17.

Price, J., 2018. The regulatory perspective-ASIC's observations on 2017 annual general

meetings. Governance Directions, 70(2), pp.62-78.

Kannadhasan, M., Goyal, V. and Charan, P., 2016. The Role of Financial Performance as a

Moderator on the Relationship Between Financial Leverage and Shareholders Return. Journal of

Modern Accounting and Auditing, 12(7), pp.379-387.

Kent, P., Kercher, K. and Routledge, J., 2018. Remuneration committees, shareholder dissent on

CEO pay and the CEO pay–performance link. Accounting & Finance, 58(2), pp.445-475.

Kerzner, H. and Kerzner, H.R., 2017. Project management: a systems approach to planning,

scheduling, and controlling. John Wiley & Sons.

Méndez, C.F., Pathan, S. and García, R.A., 2015. Monitoring capabilities of busy and overlap

directors: Evidence from Australia. Pacific-Basin Finance Journal, 35, pp.444-469.

Moriarty, R., 2018. Asic highlights the importance of annual general meetings and recent trends

in corporate governance. Governance Directions, 70(2), pp.77-81.

Peetz, D., 2015. An institutional analysis of the growth of executive remuneration. Journal of

Industrial Relations, 57(5), pp.707-725.

Petria, N., Capraru, B. and Ihnatov, I., 2015. Determinants of banks’ profitability: evidence from

EU 27 banking systems. Procedia Economics and Finance, 20, pp.518-524.

Pigé, B., 2017. Stakeholder theory and corporate governance: the nature of the board

information. Management: journal of contemporary management issues, 7(1), pp.1-17.

Price, J., 2018. The regulatory perspective-ASIC's observations on 2017 annual general

meetings. Governance Directions, 70(2), pp.62-78.

26MANAGERIAL ACCOUNTING

Qu, X., Percy, M., Stewart, J. and Hu, F., 2018. Executive stock option vesting conditions,

corporate governance and CEO attributes: evidence from Australia. Accounting &

Finance, 58(2), pp.503-533.

Riaz, Z. and Kirkbride, J., 2017. Governance of director and executive remuneration in leading

firms of Australia. Economics and Business Review, 3(4), pp.66-86.

Riaz, Z., Ray, S. and Ray, P., 2015. The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Riaz, Z., Ray, S. and Ray, P., 2015. The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Riaz, Z., Ray, S. and Ray, P.K., 2015. Collibration as an alternative regulatory mechanism to

govern the disclosure of director and executive remuneration in Australia. International Journal

of Corporate Governance, 6(2-4), pp.241-274.

Riaz, Z., Ray, S., Ray, P.K. and Kumar, V., 2015. Disclosure practices of foreign and domestic

firms in Australia. Journal of World Business, 50(4), pp.781-792.

Riaz, Z., Ray, S., Ray, P.K. and Kumar, V., 2015. Disclosure practices of foreign and domestic

firms in Australia. Journal of World Business, 50(4), pp.781-792.

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures on

financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

Qu, X., Percy, M., Stewart, J. and Hu, F., 2018. Executive stock option vesting conditions,

corporate governance and CEO attributes: evidence from Australia. Accounting &

Finance, 58(2), pp.503-533.

Riaz, Z. and Kirkbride, J., 2017. Governance of director and executive remuneration in leading

firms of Australia. Economics and Business Review, 3(4), pp.66-86.

Riaz, Z., Ray, S. and Ray, P., 2015. The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Riaz, Z., Ray, S. and Ray, P., 2015. The Synergistic Effect of State Regulation and Self-

Regulation on Disclosure Level of Director and Executive Remuneration in

Australia. Administration & Society, 47(6), pp.623-655.

Riaz, Z., Ray, S. and Ray, P.K., 2015. Collibration as an alternative regulatory mechanism to

govern the disclosure of director and executive remuneration in Australia. International Journal

of Corporate Governance, 6(2-4), pp.241-274.

Riaz, Z., Ray, S., Ray, P.K. and Kumar, V., 2015. Disclosure practices of foreign and domestic

firms in Australia. Journal of World Business, 50(4), pp.781-792.

Riaz, Z., Ray, S., Ray, P.K. and Kumar, V., 2015. Disclosure practices of foreign and domestic

firms in Australia. Journal of World Business, 50(4), pp.781-792.

Safari, M., Cooper, B.J. and Dellaportas, S., 2016. The influence of remuneration structures on

financial reporting quality: evidence from Australia. Australian Accounting Review, 26(1),

pp.66-75.

27MANAGERIAL ACCOUNTING

Salman, R.T. and Hassan, Y., 2016. Effects of Financial Leverage on Shareholders' Return of

Deposit Money Banks in Nigeria.

Santos.com., 2018. [online] Available at: https://www.santos.com/media/4319/2017-annual-

report.pdf [Accessed 4 Sep. 2018].

Sayles, L.R., 2017. Managing large systems: Organisations for the future. Routledge.

Scott, W.R., 2015. Organisations and organizing: Rational, natural and open systems

perspectives. Routledge.

Shah, P. and Arora, P., 2014. M&A announcements and their effect on return to shareholders:

An event study. Accounting and Finance Research, 3(2), p.170.

Woodsideannouncements.app.woodside., 2018. [online] Available at:

https://woodsideannouncements.app.woodside/14.02.2018+Annual+Report+2017.pdf [Accessed

4 Sep. 2018].

Salman, R.T. and Hassan, Y., 2016. Effects of Financial Leverage on Shareholders' Return of

Deposit Money Banks in Nigeria.

Santos.com., 2018. [online] Available at: https://www.santos.com/media/4319/2017-annual-

report.pdf [Accessed 4 Sep. 2018].

Sayles, L.R., 2017. Managing large systems: Organisations for the future. Routledge.

Scott, W.R., 2015. Organisations and organizing: Rational, natural and open systems

perspectives. Routledge.

Shah, P. and Arora, P., 2014. M&A announcements and their effect on return to shareholders:

An event study. Accounting and Finance Research, 3(2), p.170.

Woodsideannouncements.app.woodside., 2018. [online] Available at:

https://woodsideannouncements.app.woodside/14.02.2018+Annual+Report+2017.pdf [Accessed

4 Sep. 2018].

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.