Accounting for Managers: Financial Ratios, Ethics, and Cash Flow

VerifiedAdded on 2020/04/07

|10

|3351

|210

Homework Assignment

AI Summary

This assignment solution for Accounting for Managers provides a comprehensive analysis of financial statements, including the income statement, balance sheet, and cash flow statement, emphasizing the importance of financial ratios like liquidity, solvency, profitability, and efficiency ratios. It includes calculations and interpretations of these ratios over a three-year period, highlighting trends and potential areas of concern. The assignment also delves into ethical considerations, examining a case where an accountant faces moral dilemmas related to financial reporting and provides recommendations for resolving the ethical issues. Furthermore, the solution addresses cash flow management challenges, specifically discussing the benefits of implementing a Just-In-Time (JIT) inventory system and computerized accounting software to improve inventory control and customer credit management. Overall, the assignment offers a practical application of accounting principles and their implications for managerial decision-making.

ACCOUNTING FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

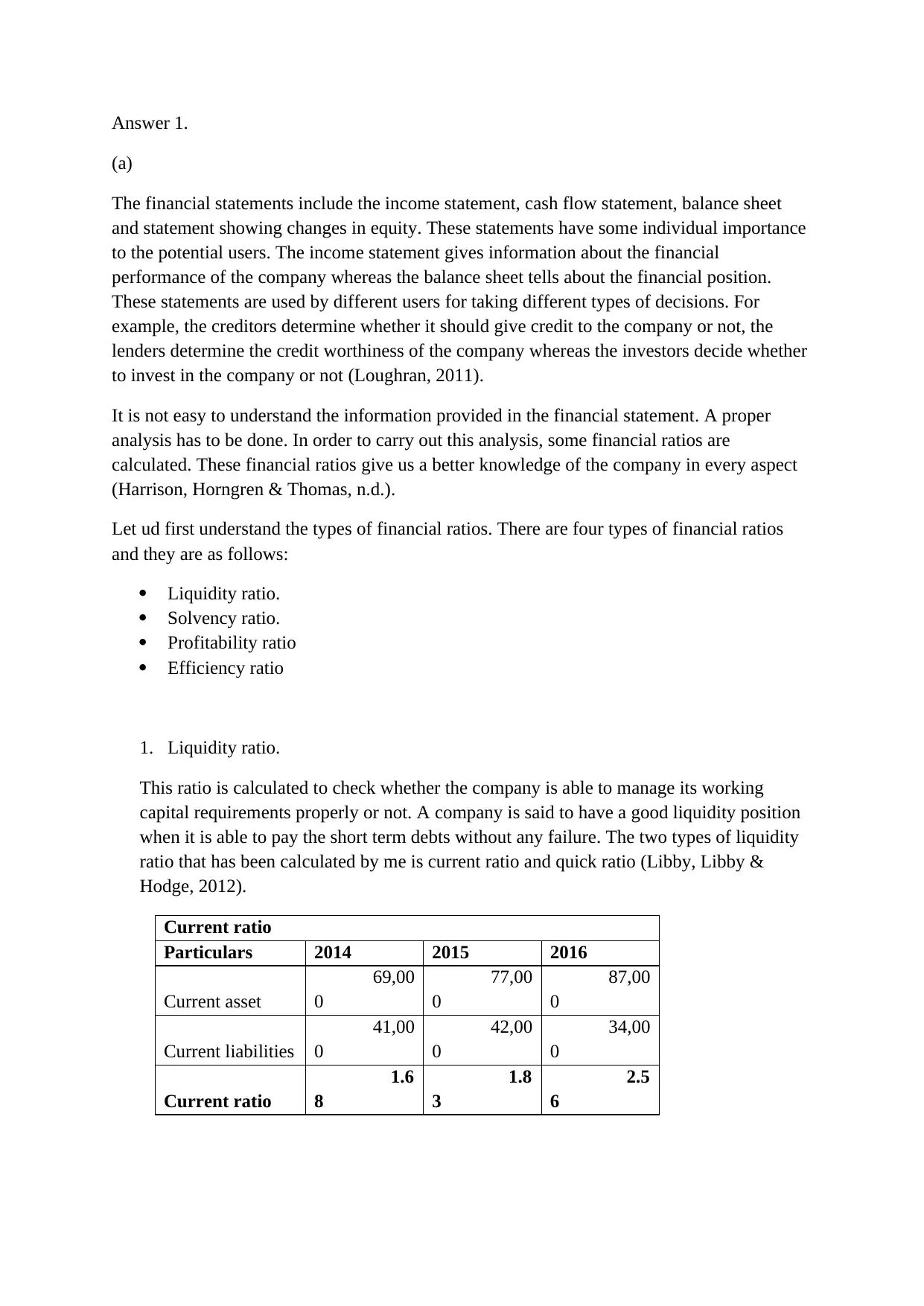

Answer 1.

(a)

The financial statements include the income statement, cash flow statement, balance sheet

and statement showing changes in equity. These statements have some individual importance

to the potential users. The income statement gives information about the financial

performance of the company whereas the balance sheet tells about the financial position.

These statements are used by different users for taking different types of decisions. For

example, the creditors determine whether it should give credit to the company or not, the

lenders determine the credit worthiness of the company whereas the investors decide whether

to invest in the company or not (Loughran, 2011).

It is not easy to understand the information provided in the financial statement. A proper

analysis has to be done. In order to carry out this analysis, some financial ratios are

calculated. These financial ratios give us a better knowledge of the company in every aspect

(Harrison, Horngren & Thomas, n.d.).

Let ud first understand the types of financial ratios. There are four types of financial ratios

and they are as follows:

Liquidity ratio.

Solvency ratio.

Profitability ratio

Efficiency ratio

1. Liquidity ratio.

This ratio is calculated to check whether the company is able to manage its working

capital requirements properly or not. A company is said to have a good liquidity position

when it is able to pay the short term debts without any failure. The two types of liquidity

ratio that has been calculated by me is current ratio and quick ratio (Libby, Libby &

Hodge, 2012).

Current ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Current ratio

1.6

8

1.8

3

2.5

6

(a)

The financial statements include the income statement, cash flow statement, balance sheet

and statement showing changes in equity. These statements have some individual importance

to the potential users. The income statement gives information about the financial

performance of the company whereas the balance sheet tells about the financial position.

These statements are used by different users for taking different types of decisions. For

example, the creditors determine whether it should give credit to the company or not, the

lenders determine the credit worthiness of the company whereas the investors decide whether

to invest in the company or not (Loughran, 2011).

It is not easy to understand the information provided in the financial statement. A proper

analysis has to be done. In order to carry out this analysis, some financial ratios are

calculated. These financial ratios give us a better knowledge of the company in every aspect

(Harrison, Horngren & Thomas, n.d.).

Let ud first understand the types of financial ratios. There are four types of financial ratios

and they are as follows:

Liquidity ratio.

Solvency ratio.

Profitability ratio

Efficiency ratio

1. Liquidity ratio.

This ratio is calculated to check whether the company is able to manage its working

capital requirements properly or not. A company is said to have a good liquidity position

when it is able to pay the short term debts without any failure. The two types of liquidity

ratio that has been calculated by me is current ratio and quick ratio (Libby, Libby &

Hodge, 2012).

Current ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Current ratio

1.6

8

1.8

3

2.5

6

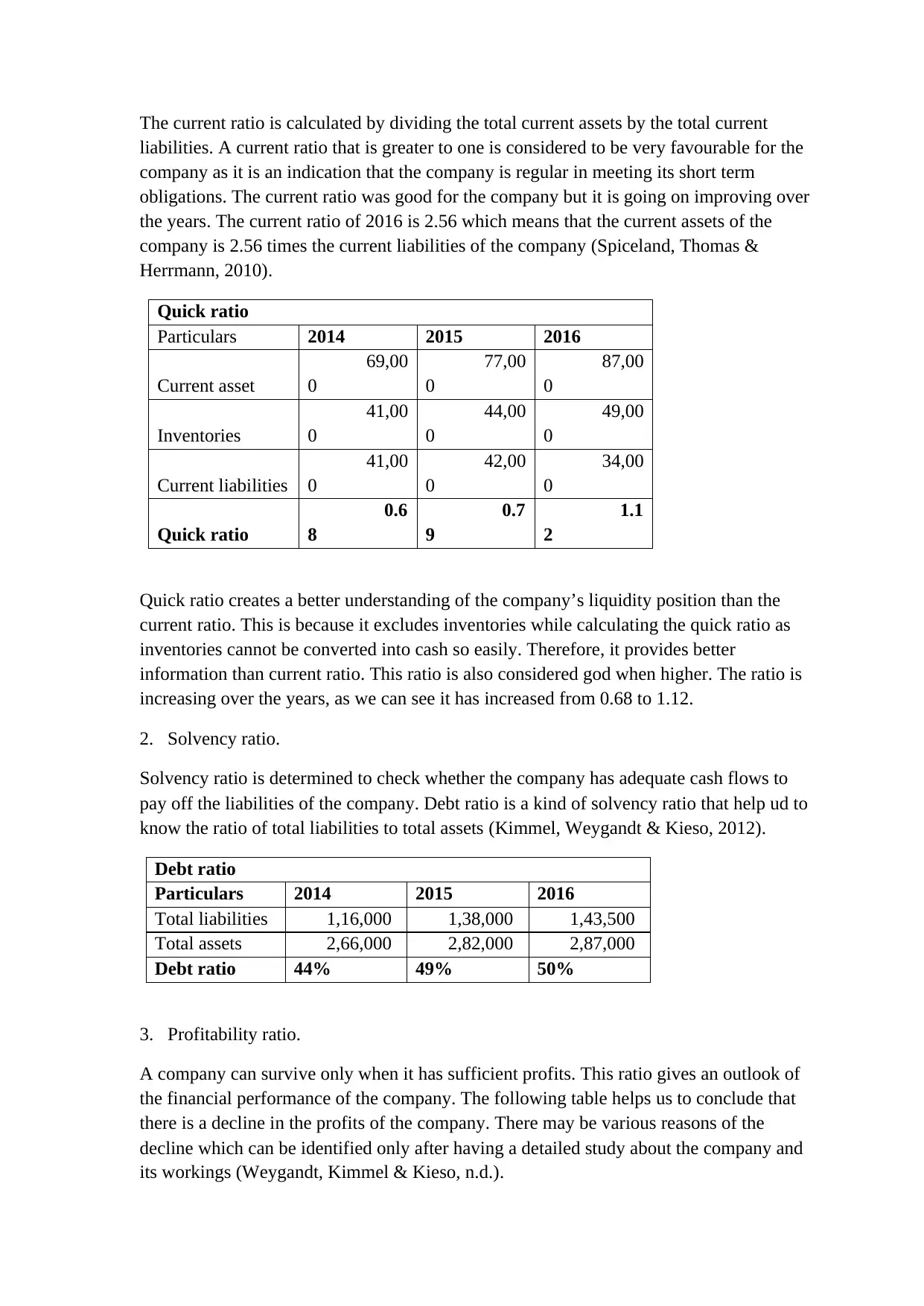

The current ratio is calculated by dividing the total current assets by the total current

liabilities. A current ratio that is greater to one is considered to be very favourable for the

company as it is an indication that the company is regular in meeting its short term

obligations. The current ratio was good for the company but it is going on improving over

the years. The current ratio of 2016 is 2.56 which means that the current assets of the

company is 2.56 times the current liabilities of the company (Spiceland, Thomas &

Herrmann, 2010).

Quick ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Inventories

41,00

0

44,00

0

49,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Quick ratio

0.6

8

0.7

9

1.1

2

Quick ratio creates a better understanding of the company’s liquidity position than the

current ratio. This is because it excludes inventories while calculating the quick ratio as

inventories cannot be converted into cash so easily. Therefore, it provides better

information than current ratio. This ratio is also considered god when higher. The ratio is

increasing over the years, as we can see it has increased from 0.68 to 1.12.

2. Solvency ratio.

Solvency ratio is determined to check whether the company has adequate cash flows to

pay off the liabilities of the company. Debt ratio is a kind of solvency ratio that help ud to

know the ratio of total liabilities to total assets (Kimmel, Weygandt & Kieso, 2012).

Debt ratio

Particulars 2014 2015 2016

Total liabilities 1,16,000 1,38,000 1,43,500

Total assets 2,66,000 2,82,000 2,87,000

Debt ratio 44% 49% 50%

3. Profitability ratio.

A company can survive only when it has sufficient profits. This ratio gives an outlook of

the financial performance of the company. The following table helps us to conclude that

there is a decline in the profits of the company. There may be various reasons of the

decline which can be identified only after having a detailed study about the company and

its workings (Weygandt, Kimmel & Kieso, n.d.).

liabilities. A current ratio that is greater to one is considered to be very favourable for the

company as it is an indication that the company is regular in meeting its short term

obligations. The current ratio was good for the company but it is going on improving over

the years. The current ratio of 2016 is 2.56 which means that the current assets of the

company is 2.56 times the current liabilities of the company (Spiceland, Thomas &

Herrmann, 2010).

Quick ratio

Particulars 2014 2015 2016

Current asset

69,00

0

77,00

0

87,00

0

Inventories

41,00

0

44,00

0

49,00

0

Current liabilities

41,00

0

42,00

0

34,00

0

Quick ratio

0.6

8

0.7

9

1.1

2

Quick ratio creates a better understanding of the company’s liquidity position than the

current ratio. This is because it excludes inventories while calculating the quick ratio as

inventories cannot be converted into cash so easily. Therefore, it provides better

information than current ratio. This ratio is also considered god when higher. The ratio is

increasing over the years, as we can see it has increased from 0.68 to 1.12.

2. Solvency ratio.

Solvency ratio is determined to check whether the company has adequate cash flows to

pay off the liabilities of the company. Debt ratio is a kind of solvency ratio that help ud to

know the ratio of total liabilities to total assets (Kimmel, Weygandt & Kieso, 2012).

Debt ratio

Particulars 2014 2015 2016

Total liabilities 1,16,000 1,38,000 1,43,500

Total assets 2,66,000 2,82,000 2,87,000

Debt ratio 44% 49% 50%

3. Profitability ratio.

A company can survive only when it has sufficient profits. This ratio gives an outlook of

the financial performance of the company. The following table helps us to conclude that

there is a decline in the profits of the company. There may be various reasons of the

decline which can be identified only after having a detailed study about the company and

its workings (Weygandt, Kimmel & Kieso, n.d.).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

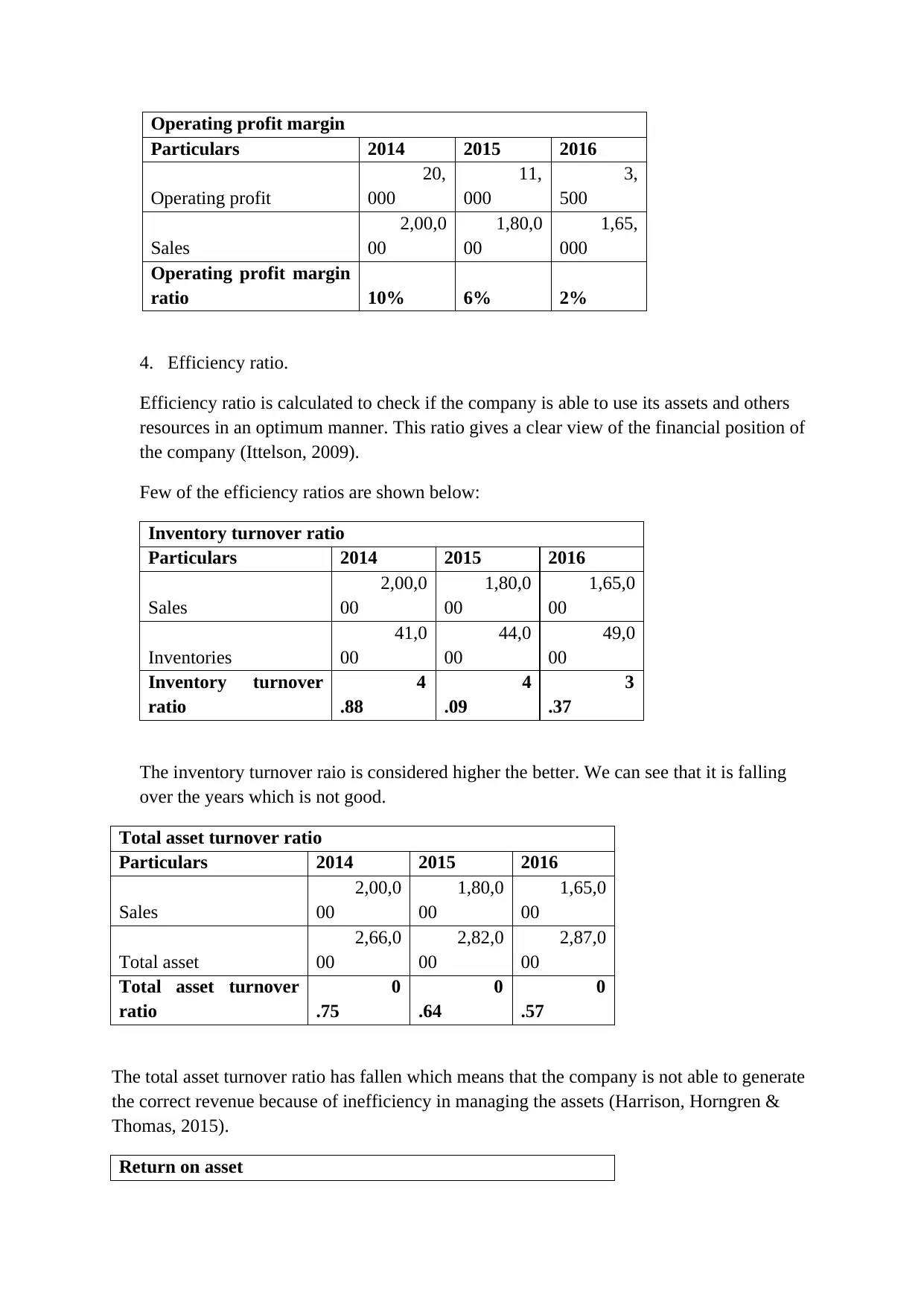

Operating profit margin

Particulars 2014 2015 2016

Operating profit

20,

000

11,

000

3,

500

Sales

2,00,0

00

1,80,0

00

1,65,

000

Operating profit margin

ratio 10% 6% 2%

4. Efficiency ratio.

Efficiency ratio is calculated to check if the company is able to use its assets and others

resources in an optimum manner. This ratio gives a clear view of the financial position of

the company (Ittelson, 2009).

Few of the efficiency ratios are shown below:

Inventory turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Inventories

41,0

00

44,0

00

49,0

00

Inventory turnover

ratio

4

.88

4

.09

3

.37

The inventory turnover raio is considered higher the better. We can see that it is falling

over the years which is not good.

Total asset turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Total asset

2,66,0

00

2,82,0

00

2,87,0

00

Total asset turnover

ratio

0

.75

0

.64

0

.57

The total asset turnover ratio has fallen which means that the company is not able to generate

the correct revenue because of inefficiency in managing the assets (Harrison, Horngren &

Thomas, 2015).

Return on asset

Particulars 2014 2015 2016

Operating profit

20,

000

11,

000

3,

500

Sales

2,00,0

00

1,80,0

00

1,65,

000

Operating profit margin

ratio 10% 6% 2%

4. Efficiency ratio.

Efficiency ratio is calculated to check if the company is able to use its assets and others

resources in an optimum manner. This ratio gives a clear view of the financial position of

the company (Ittelson, 2009).

Few of the efficiency ratios are shown below:

Inventory turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Inventories

41,0

00

44,0

00

49,0

00

Inventory turnover

ratio

4

.88

4

.09

3

.37

The inventory turnover raio is considered higher the better. We can see that it is falling

over the years which is not good.

Total asset turnover ratio

Particulars 2014 2015 2016

Sales

2,00,0

00

1,80,0

00

1,65,0

00

Total asset

2,66,0

00

2,82,0

00

2,87,0

00

Total asset turnover

ratio

0

.75

0

.64

0

.57

The total asset turnover ratio has fallen which means that the company is not able to generate

the correct revenue because of inefficiency in managing the assets (Harrison, Horngren &

Thomas, 2015).

Return on asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

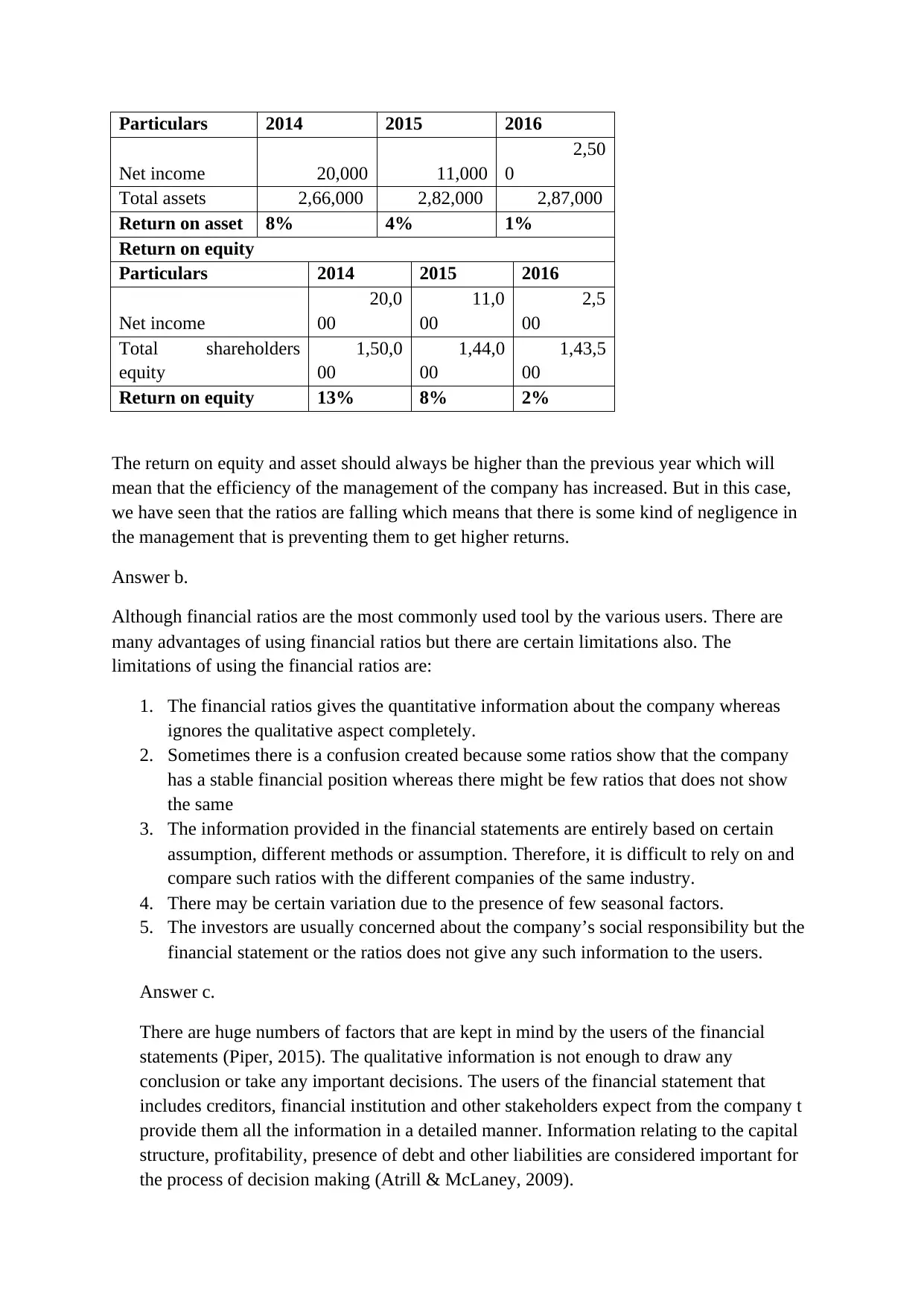

Particulars 2014 2015 2016

Net income 20,000 11,000

2,50

0

Total assets 2,66,000 2,82,000 2,87,000

Return on asset 8% 4% 1%

Return on equity

Particulars 2014 2015 2016

Net income

20,0

00

11,0

00

2,5

00

Total shareholders

equity

1,50,0

00

1,44,0

00

1,43,5

00

Return on equity 13% 8% 2%

The return on equity and asset should always be higher than the previous year which will

mean that the efficiency of the management of the company has increased. But in this case,

we have seen that the ratios are falling which means that there is some kind of negligence in

the management that is preventing them to get higher returns.

Answer b.

Although financial ratios are the most commonly used tool by the various users. There are

many advantages of using financial ratios but there are certain limitations also. The

limitations of using the financial ratios are:

1. The financial ratios gives the quantitative information about the company whereas

ignores the qualitative aspect completely.

2. Sometimes there is a confusion created because some ratios show that the company

has a stable financial position whereas there might be few ratios that does not show

the same

3. The information provided in the financial statements are entirely based on certain

assumption, different methods or assumption. Therefore, it is difficult to rely on and

compare such ratios with the different companies of the same industry.

4. There may be certain variation due to the presence of few seasonal factors.

5. The investors are usually concerned about the company’s social responsibility but the

financial statement or the ratios does not give any such information to the users.

Answer c.

There are huge numbers of factors that are kept in mind by the users of the financial

statements (Piper, 2015). The qualitative information is not enough to draw any

conclusion or take any important decisions. The users of the financial statement that

includes creditors, financial institution and other stakeholders expect from the company t

provide them all the information in a detailed manner. Information relating to the capital

structure, profitability, presence of debt and other liabilities are considered important for

the process of decision making (Atrill & McLaney, 2009).

Net income 20,000 11,000

2,50

0

Total assets 2,66,000 2,82,000 2,87,000

Return on asset 8% 4% 1%

Return on equity

Particulars 2014 2015 2016

Net income

20,0

00

11,0

00

2,5

00

Total shareholders

equity

1,50,0

00

1,44,0

00

1,43,5

00

Return on equity 13% 8% 2%

The return on equity and asset should always be higher than the previous year which will

mean that the efficiency of the management of the company has increased. But in this case,

we have seen that the ratios are falling which means that there is some kind of negligence in

the management that is preventing them to get higher returns.

Answer b.

Although financial ratios are the most commonly used tool by the various users. There are

many advantages of using financial ratios but there are certain limitations also. The

limitations of using the financial ratios are:

1. The financial ratios gives the quantitative information about the company whereas

ignores the qualitative aspect completely.

2. Sometimes there is a confusion created because some ratios show that the company

has a stable financial position whereas there might be few ratios that does not show

the same

3. The information provided in the financial statements are entirely based on certain

assumption, different methods or assumption. Therefore, it is difficult to rely on and

compare such ratios with the different companies of the same industry.

4. There may be certain variation due to the presence of few seasonal factors.

5. The investors are usually concerned about the company’s social responsibility but the

financial statement or the ratios does not give any such information to the users.

Answer c.

There are huge numbers of factors that are kept in mind by the users of the financial

statements (Piper, 2015). The qualitative information is not enough to draw any

conclusion or take any important decisions. The users of the financial statement that

includes creditors, financial institution and other stakeholders expect from the company t

provide them all the information in a detailed manner. Information relating to the capital

structure, profitability, presence of debt and other liabilities are considered important for

the process of decision making (Atrill & McLaney, 2009).

Answer 2.

Ethics are values based on those morals or principles that affect an individual’s work or

behaviour. The way of working in which an individual can match the societies behavior and

thinking is considered to be the best value. The main objective of a firm for having a

successful business is to behave in a proper manner and also keep the following principles in

mind which are Impartiality, honesty, pluralism, dignity, equality and individual rights.

In the following case, the accountant of Allandale ltd, Tom Lyons is facing a huge moral

problem. The company took a mortgage loan of $20 million which was given on the basis of

two demands which were: the value of current ratio should be 2:1 and also after the payment

of tax the returns on asset should have a minimum value of 10%. Howsoever, the balance

sheet shows that the firm owns a boat valued at $500000 on the asset side which may have a

net realizable value stated at $350000. There was also a customer who owed an amount of

$20 million to the firm but was able to pay only the half amount because of a severe financial

crisis. Thus the provisions amounting to $150000 and $200000 respectively meet all the three

conditions which state that the amounts should be considered as provisions in the account.

After all these calculations the current ratio will be 1.6:1 and the return on assets will be

amounting to 2% whereas previously the current ratio was stated to be 2.1:1 and the value of

return on assets will be amounting to 11 %. Because of such values, the creditors will ask for

the immediate repayment of the mortgage loan as there will be high values of provision

which shows that the company may have a financial crisis (Hart, Wilson & Fergus, 2012).

Thus, a new problem was raised to recognize an expenditure which has not taken place

actually and also by doing this the firm may be risking its reputation and the issues of

bankruptcy and unemployment may arise leading to the firm’s failure.

1. Tom Lyons, the charted accountant of the firm, should follow certain steps to deal

with the ethical problem he and the firm have been facing:

There are three conditions which are stated in the accounting standards for the

recognition of a provision which are: there must have been some activities in

the past which may increase the current liability; if there are chances less than

50% of facing a loss then we may make a provision; also all the reliable

documents should be checked before creating a provision as it may harm the

business in future. If all these conditions are applied then there shall be no

problem in the creation of the provision (Berry & Jarvis, 2007).

There are certain principles like the “prudence” concept which should be kept

in mind before presenting or making the financial statements. This concept

states that there should be certain measures which should be adopted so that

the income and assets are not overvalued and the liabilities and expenditures

are not undervalued. It also means that the asset shouldn’t be valued at a

higher price than what it needs to be recovered in the future and the liabilities

shouldn’t be valued at a lower price than what it needs to be paid in the future.

Ethics are values based on those morals or principles that affect an individual’s work or

behaviour. The way of working in which an individual can match the societies behavior and

thinking is considered to be the best value. The main objective of a firm for having a

successful business is to behave in a proper manner and also keep the following principles in

mind which are Impartiality, honesty, pluralism, dignity, equality and individual rights.

In the following case, the accountant of Allandale ltd, Tom Lyons is facing a huge moral

problem. The company took a mortgage loan of $20 million which was given on the basis of

two demands which were: the value of current ratio should be 2:1 and also after the payment

of tax the returns on asset should have a minimum value of 10%. Howsoever, the balance

sheet shows that the firm owns a boat valued at $500000 on the asset side which may have a

net realizable value stated at $350000. There was also a customer who owed an amount of

$20 million to the firm but was able to pay only the half amount because of a severe financial

crisis. Thus the provisions amounting to $150000 and $200000 respectively meet all the three

conditions which state that the amounts should be considered as provisions in the account.

After all these calculations the current ratio will be 1.6:1 and the return on assets will be

amounting to 2% whereas previously the current ratio was stated to be 2.1:1 and the value of

return on assets will be amounting to 11 %. Because of such values, the creditors will ask for

the immediate repayment of the mortgage loan as there will be high values of provision

which shows that the company may have a financial crisis (Hart, Wilson & Fergus, 2012).

Thus, a new problem was raised to recognize an expenditure which has not taken place

actually and also by doing this the firm may be risking its reputation and the issues of

bankruptcy and unemployment may arise leading to the firm’s failure.

1. Tom Lyons, the charted accountant of the firm, should follow certain steps to deal

with the ethical problem he and the firm have been facing:

There are three conditions which are stated in the accounting standards for the

recognition of a provision which are: there must have been some activities in

the past which may increase the current liability; if there are chances less than

50% of facing a loss then we may make a provision; also all the reliable

documents should be checked before creating a provision as it may harm the

business in future. If all these conditions are applied then there shall be no

problem in the creation of the provision (Berry & Jarvis, 2007).

There are certain principles like the “prudence” concept which should be kept

in mind before presenting or making the financial statements. This concept

states that there should be certain measures which should be adopted so that

the income and assets are not overvalued and the liabilities and expenditures

are not undervalued. It also means that the asset shouldn’t be valued at a

higher price than what it needs to be recovered in the future and the liabilities

shouldn’t be valued at a lower price than what it needs to be paid in the future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The company should try and take some time to return the loan to the lender

instead of paying the loan immediately which may help it to recover from the

disturbing circumstances and make their present ratios presentable also

helping it to avoid bankruptcy in near future (Shim, Siegel & Shim, 2013).

instead of paying the loan immediately which may help it to recover from the

disturbing circumstances and make their present ratios presentable also

helping it to avoid bankruptcy in near future (Shim, Siegel & Shim, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 3.

1. According to the given case, the Giggling Bothers are facing many difficulties in the

management of the continuous negative cash flows. It will be better if the company

replaces its old manual accounting system with a new automatic Just-In-Time system

as the major problems caused are because of the mismanagement of the stock which is

caused because of excessive or less purchase of the inventories made by the firm

inadequately. Just-In-Time system may be helpful to improve the management of

inventories as it makes strategies which may be helpful in the increment of the

efficiency and also it may decrease the waste leading to the proper functioning of the

purchasing department. This strategy is taken into consideration so that the company

can provide its customers whenever they need the product and also be safe from

facing the problem of storing unused inventories and thus leading to the reduction of

the inventory costs (Lalli, 2012).

The JIT strategy assists the firm to track the demand of the environment correctly,

thus leading to help the firm in deciding the amount of materials which may be

needed for the production of goods. Thus the new software will help the purchasing

department in the proper functioning of the firm. The accounting software should be

computerized in a manner which will help to notify the firm whenever there is a low

credit balance of a customer so that the firm may stop further sales and ask the debtor

to clear his accounts before any further business is being done.

2. The adoption of the new computerized JIT system will help the firm in many ways.

Some of the advantages are stated below (Loganathan, 1997):

The new system will help the company to know the demands of its customers

accurately and thus order the materials accordingly with no waste left. This will help

the firm to maintain a good relationship with its customers because of the high-quality

goods at low costs and timely delivery.

The computerized software uses a technology which helps the firm to determine and

reduce the overhead expenses, transportation costs, storage costs, etc. It also helps the

firm to detect information about any malfunctioning present in the production of

goods which may be helpful in the future to make a correction and reduce the

production cost (Izhar & Hontoir, 2001).

It also helps to reduce the amount of fund which is invested in the stock. The saved

money may be used anywhere else to improve the business. It will also be clearing the

space of warehouse by removing the excessive inventories. The extra space may be

used for expanding the business in any other manner.

The adoption of such system requires regular synchronizing between the several

departments as if any of the departments fail to coordinate the whole organization will

suffer. Thus the introduction of any such new software requires teamwork of the

departments which may help the firm to improve its business indirectly

(Bhattacharyya, 2011).

The new system of JIT will help the firm in better management of the firms account

as it will help the department to recognize the major weaknesses of the firm by

observing the unwanted expenses or to check whether there is any accrued income

1. According to the given case, the Giggling Bothers are facing many difficulties in the

management of the continuous negative cash flows. It will be better if the company

replaces its old manual accounting system with a new automatic Just-In-Time system

as the major problems caused are because of the mismanagement of the stock which is

caused because of excessive or less purchase of the inventories made by the firm

inadequately. Just-In-Time system may be helpful to improve the management of

inventories as it makes strategies which may be helpful in the increment of the

efficiency and also it may decrease the waste leading to the proper functioning of the

purchasing department. This strategy is taken into consideration so that the company

can provide its customers whenever they need the product and also be safe from

facing the problem of storing unused inventories and thus leading to the reduction of

the inventory costs (Lalli, 2012).

The JIT strategy assists the firm to track the demand of the environment correctly,

thus leading to help the firm in deciding the amount of materials which may be

needed for the production of goods. Thus the new software will help the purchasing

department in the proper functioning of the firm. The accounting software should be

computerized in a manner which will help to notify the firm whenever there is a low

credit balance of a customer so that the firm may stop further sales and ask the debtor

to clear his accounts before any further business is being done.

2. The adoption of the new computerized JIT system will help the firm in many ways.

Some of the advantages are stated below (Loganathan, 1997):

The new system will help the company to know the demands of its customers

accurately and thus order the materials accordingly with no waste left. This will help

the firm to maintain a good relationship with its customers because of the high-quality

goods at low costs and timely delivery.

The computerized software uses a technology which helps the firm to determine and

reduce the overhead expenses, transportation costs, storage costs, etc. It also helps the

firm to detect information about any malfunctioning present in the production of

goods which may be helpful in the future to make a correction and reduce the

production cost (Izhar & Hontoir, 2001).

It also helps to reduce the amount of fund which is invested in the stock. The saved

money may be used anywhere else to improve the business. It will also be clearing the

space of warehouse by removing the excessive inventories. The extra space may be

used for expanding the business in any other manner.

The adoption of such system requires regular synchronizing between the several

departments as if any of the departments fail to coordinate the whole organization will

suffer. Thus the introduction of any such new software requires teamwork of the

departments which may help the firm to improve its business indirectly

(Bhattacharyya, 2011).

The new system of JIT will help the firm in better management of the firms account

as it will help the department to recognize the major weaknesses of the firm by

observing the unwanted expenses or to check whether there is any accrued income

which is not received by the firm. These are the problems which may have been raised

in the previous manual system but is now repaired by the new automatic system.

The new system will be less time consuming and thus the saved time may be used by

the accountants for better planning and organizing of the future strategies of the firm

(Epstein & Lee, 2012).

3. The new system may not be very cheap at cost, so the company should evaluate all

other costs before implementation of the system. The Giggling Brothers are adopting

the software so as to ascertain that there are less overhead expenses and normal

inventory costs. The excess profit may be used to provide loans and earn interests also

the free warehouse space may be rented for earning extra revenue. The company may

also reduce the workforce for the accounting department as there will be less work

which can be finished by two or three employees who are expert at their job thus,

leading to an overall decrease in the company’s expenses.

4. Before setting the software and using it, the company should look at the following

facts:

The system should be organized in a manner in which it shows the monthly

cash flows because previously the company was suffering a loss in every six

months. If such action continues then the company should take immediate

steps to cure the problem.

It should also show a quarterly report which may be used to analyze the

purchase made, sales made or accrued income so that the management could

take steps to treat loss appropriately.

The firm should check whether there are any unusual sales taking place in the

company as the maximum treachery takes place because of poor management

of accounts. Thus to be on the safe side, the firm should either train its

employees or replace them with the experts of the particular field.

The company should also take into account that it is investing the funds in the

appropriate activities and it should also check that it is covering all the costs

and incurring profits.

5. The company was incurring good profit before but is suffering loss recently. It is also

late for the adoption of the new system as the competitors of the firm may have

already adopted it a long time back in the past. They may have also faced the

problems but after analyzing the new system they may have found the solutions for

problems. Thus the company should try and get educated by the experience of the

competitors. Thus it will be helpful for the company if they examine the whole system

before implementing it.

in the previous manual system but is now repaired by the new automatic system.

The new system will be less time consuming and thus the saved time may be used by

the accountants for better planning and organizing of the future strategies of the firm

(Epstein & Lee, 2012).

3. The new system may not be very cheap at cost, so the company should evaluate all

other costs before implementation of the system. The Giggling Brothers are adopting

the software so as to ascertain that there are less overhead expenses and normal

inventory costs. The excess profit may be used to provide loans and earn interests also

the free warehouse space may be rented for earning extra revenue. The company may

also reduce the workforce for the accounting department as there will be less work

which can be finished by two or three employees who are expert at their job thus,

leading to an overall decrease in the company’s expenses.

4. Before setting the software and using it, the company should look at the following

facts:

The system should be organized in a manner in which it shows the monthly

cash flows because previously the company was suffering a loss in every six

months. If such action continues then the company should take immediate

steps to cure the problem.

It should also show a quarterly report which may be used to analyze the

purchase made, sales made or accrued income so that the management could

take steps to treat loss appropriately.

The firm should check whether there are any unusual sales taking place in the

company as the maximum treachery takes place because of poor management

of accounts. Thus to be on the safe side, the firm should either train its

employees or replace them with the experts of the particular field.

The company should also take into account that it is investing the funds in the

appropriate activities and it should also check that it is covering all the costs

and incurring profits.

5. The company was incurring good profit before but is suffering loss recently. It is also

late for the adoption of the new system as the competitors of the firm may have

already adopted it a long time back in the past. They may have also faced the

problems but after analyzing the new system they may have found the solutions for

problems. Thus the company should try and get educated by the experience of the

competitors. Thus it will be helpful for the company if they examine the whole system

before implementing it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References:

Atrill, P., & McLaney, E. (2009). Management accounting for decision makers. Harlow,

England: Financial Times/Prentice Hall.

Berry, A., & Jarvis, R. (2007). Accounting in a business context. London: Thomson Learning.

Bhattacharyya, D. (2011). Management accounting. Noida, India: Pearson.

Epstein, M., & Lee, J. (2012). Advances in management accounting. Bingley: Emerald.

Harrison, W., Horngren, C., & Thomas, C. (2015). Financial accounting. Upper Saddle

River: Prentice Hall.

Harrison, W., Horngren, C., & Thomas, C. Financial accounting.

Hart, J., Wilson, C., & Fergus, C. (2012). Management accounting. Frenchs Forest, N.S.W.:

Pearson Australia.

Ittelson, T. (2009). Financial statements. Franklin Lakes, N.J.: Career Press.

Izhar, R., & Hontoir, J. (2001). Accounting, costing and management. Oxford: Oxford

University Press.

Kimmel, P., Weygandt, J., & Kieso, D. (2012). Financial Accounting.

Lalli, W. (2012). Handbook of budgeting. Hoboken, N.J: Wiley.

Libby, R., Libby, P., & Hodge, F. (2012). Financial accounting.

Loganathan, N. (1997). Foundations of budgeting. Sydney: UNSW Press.

Loughran, M. (2011). Financial accounting for dummies. Hoboken (NJ): Wiley.

Piper, M. (2015). Accounting made simple. [United States]: [CreateSpace Pub.].

Shim, A., Siegel, J., & Shim, J. (2013). Budgeting basics and beyond. Hoboken, N.J.: Wiley.

Spiceland, J., Thomas, W., & Herrmann, D. (2010). Financial accounting.

Weygandt, J., Kimmel, P., & Kieso, D. Financial accounting.

Atrill, P., & McLaney, E. (2009). Management accounting for decision makers. Harlow,

England: Financial Times/Prentice Hall.

Berry, A., & Jarvis, R. (2007). Accounting in a business context. London: Thomson Learning.

Bhattacharyya, D. (2011). Management accounting. Noida, India: Pearson.

Epstein, M., & Lee, J. (2012). Advances in management accounting. Bingley: Emerald.

Harrison, W., Horngren, C., & Thomas, C. (2015). Financial accounting. Upper Saddle

River: Prentice Hall.

Harrison, W., Horngren, C., & Thomas, C. Financial accounting.

Hart, J., Wilson, C., & Fergus, C. (2012). Management accounting. Frenchs Forest, N.S.W.:

Pearson Australia.

Ittelson, T. (2009). Financial statements. Franklin Lakes, N.J.: Career Press.

Izhar, R., & Hontoir, J. (2001). Accounting, costing and management. Oxford: Oxford

University Press.

Kimmel, P., Weygandt, J., & Kieso, D. (2012). Financial Accounting.

Lalli, W. (2012). Handbook of budgeting. Hoboken, N.J: Wiley.

Libby, R., Libby, P., & Hodge, F. (2012). Financial accounting.

Loganathan, N. (1997). Foundations of budgeting. Sydney: UNSW Press.

Loughran, M. (2011). Financial accounting for dummies. Hoboken (NJ): Wiley.

Piper, M. (2015). Accounting made simple. [United States]: [CreateSpace Pub.].

Shim, A., Siegel, J., & Shim, J. (2013). Budgeting basics and beyond. Hoboken, N.J.: Wiley.

Spiceland, J., Thomas, W., & Herrmann, D. (2010). Financial accounting.

Weygandt, J., Kimmel, P., & Kieso, D. Financial accounting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.