University Finance Report: Oil Search Limited Analysis

VerifiedAdded on 2020/05/28

|16

|3257

|80

Report

AI Summary

This report provides a comprehensive financial analysis of Oil Search Limited, a major oil and gas exploration company. It begins with a description of the company and its operational structure, followed by an examination of its ownership and governance. Key financial ratios, including Return on Assets (ROA), Return on Equity (ROE), and the debt ratio, are calculated and analyzed for the years 2013-2016, highlighting the relationship between ROE and ROA and the implications of the debt ratio. The report also analyzes stock price movements over a two-year period using data from the ASX, along with recent company announcements. Furthermore, it calculates the company's beta and assesses its suitability as a conservative investment. The Weighted Average Cost of Capital (WACC) is computed, along with an exploration of its implications for management evaluation. The report concludes with an analysis of the optimal capital structure and provides recommendations based on the financial data.

Running head: FINANCE FOR BUSINESS - MASTERS

Finance for business – Masters

Name of the student

Name of the university

Author note

Finance for business – Masters

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS - MASTERS

Table of Contents

1. Description of company......................................................................................................2

2. Structure of ownership governance....................................................................................2

3. Key ratios............................................................................................................................3

4. Information derived from the website of ASX...................................................................5

5. Recent announcements.......................................................................................................8

6. Stock field...........................................................................................................................9

7. Weighted average cost of capital........................................................................................9

8. Debt ratio..........................................................................................................................11

9. Dividend policy.................................................................................................................12

10. Recommendation...........................................................................................................12

Reference..................................................................................................................................14

Table of Contents

1. Description of company......................................................................................................2

2. Structure of ownership governance....................................................................................2

3. Key ratios............................................................................................................................3

4. Information derived from the website of ASX...................................................................5

5. Recent announcements.......................................................................................................8

6. Stock field...........................................................................................................................9

7. Weighted average cost of capital........................................................................................9

8. Debt ratio..........................................................................................................................11

9. Dividend policy.................................................................................................................12

10. Recommendation...........................................................................................................12

Reference..................................................................................................................................14

2FINANCE FOR BUSINESS - MASTERS

1. Description of company

Oil Search Limited, the biggest gas and oil exploration companies was incorporated in

the Papua New Guinea and operates under the oilfields of Papua New Guinea (PNG). The

company was established in the year 1929. Under PNG, the company holds more than 98%

of assets and it holds extensive exploration and appraisal portfolio. The company has clear

strategy for driving the future growth. Further, the company is pursuing the opportunities for

developing the additional LNG for providing trainings in PNG (Oilsearch 2017). The

company is involved for liquefying the natural gas production and the developments of it

through the interest in LNG PNG projects that is operated by PNG Limited. The company has

three main products; these are – gas, oil and liquefied natural gas (LNG). The company

operates 3 units for the business that involves PNG gas and oil, LNG PNG products and

Middle East and North America (MENA)

2. Structure of ownership governance

i. Substantial ownership

More than 20% shareholding – no shareholders are there in the company who is

holding more than 20% of shares.

More than 5% shareholding – International Petroleum Invt. Co. PJSC (Investment

Management) is holding 12.9% shares in the company and Npcp Investment Ltd is

holding 9.80% shares in Oil Search Limited.

ii. Name of key personnel

Chairman - Mr RJ Lee

Board members

Mr PR Botten – Managing director

Mr G Aopi – Executive director

1. Description of company

Oil Search Limited, the biggest gas and oil exploration companies was incorporated in

the Papua New Guinea and operates under the oilfields of Papua New Guinea (PNG). The

company was established in the year 1929. Under PNG, the company holds more than 98%

of assets and it holds extensive exploration and appraisal portfolio. The company has clear

strategy for driving the future growth. Further, the company is pursuing the opportunities for

developing the additional LNG for providing trainings in PNG (Oilsearch 2017). The

company is involved for liquefying the natural gas production and the developments of it

through the interest in LNG PNG projects that is operated by PNG Limited. The company has

three main products; these are – gas, oil and liquefied natural gas (LNG). The company

operates 3 units for the business that involves PNG gas and oil, LNG PNG products and

Middle East and North America (MENA)

2. Structure of ownership governance

i. Substantial ownership

More than 20% shareholding – no shareholders are there in the company who is

holding more than 20% of shares.

More than 5% shareholding – International Petroleum Invt. Co. PJSC (Investment

Management) is holding 12.9% shares in the company and Npcp Investment Ltd is

holding 9.80% shares in Oil Search Limited.

ii. Name of key personnel

Chairman - Mr RJ Lee

Board members

Mr PR Botten – Managing director

Mr G Aopi – Executive director

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS - MASTERS

Sir KG Constantinou – Non-Executive director

Dr EJ Doyle – Non-Executive director

Ms FE Harris – Non –executive Director

Dr AJ Kantsler – Non-Executive director

Mr B Philemon – Non-Executive Director

Mr KW Spence – Non-Executive Director

Dr ZE Switkowski – Non-Executive Director

Mr MP Togolo – Non-Executive Ditector

CEO – Mr PR Botten

More than 20% shareholding – as none of the above mentioned key personnel are

holding more than 5% or more than 20% shares in the company they do not fall under

the category of substantial shareholders.

3. Key ratios

i. Return on assets (ROA) = (NPAT / Total Assets)

Return on Equity (ROE) = (Net profit after tax / Ordinary equity)

Ratio Formula 2016 2015 2014 2013

Return on assets NAPT / Total asset 0.009 -0.004 0.033 0.024

Return on equity NPAT / Ordinary equity 0.019 -0.008 0.070 0.060

Debt ratio = Total liabilities / Total assets

Debt ratio Total liabilities / Total assets 0.533 0.545 0.533 0.594

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

Sir KG Constantinou – Non-Executive director

Dr EJ Doyle – Non-Executive director

Ms FE Harris – Non –executive Director

Dr AJ Kantsler – Non-Executive director

Mr B Philemon – Non-Executive Director

Mr KW Spence – Non-Executive Director

Dr ZE Switkowski – Non-Executive Director

Mr MP Togolo – Non-Executive Ditector

CEO – Mr PR Botten

More than 20% shareholding – as none of the above mentioned key personnel are

holding more than 5% or more than 20% shares in the company they do not fall under

the category of substantial shareholders.

3. Key ratios

i. Return on assets (ROA) = (NPAT / Total Assets)

Return on Equity (ROE) = (Net profit after tax / Ordinary equity)

Ratio Formula 2016 2015 2014 2013

Return on assets NAPT / Total asset 0.009 -0.004 0.033 0.024

Return on equity NPAT / Ordinary equity 0.019 -0.008 0.070 0.060

Debt ratio = Total liabilities / Total assets

Debt ratio Total liabilities / Total assets 0.533 0.545 0.533 0.594

EBIT/TA * NPAT/EBIT * TA/OE = NPAT/OE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS - MASTERS

EBIT/TA * NPAT/EBIT * TA/OE = 381,031/10,126,129 * 89,795/381,031 *

10,126,129/47,25,316 = 0.019

NPAT/OE = 89,795/4725316 = 0.019

From the above calculation it can be proved that EBIT/TA * NPAT/EBIT * TA/OE =

NPAT/OE

ii. Phenomenon of TA/OE

The phenomenon of TA/OE represents the total assets of the company as compared to

it’s to its owner’s equity or ordinary equity. It stats the exposure of the company towards the

risk of insolvency and measures the shareholder’s risk exposures as compared to the

company’s total assets. If the company’s total assets reduce, it will increase the return on

assets whereas if the total assets of the company go up, it will reduce the return on assets of

the company (Naser et al. 2013). The value and importance of the total asset to equity ratio

depends on the industry, present economic status, company’s sales and assets and various

other factors. Though there is no ideal value for the ratio and it is used for comparing the

business with its peers. However, high ratio indicates that the company is highly leveraged.

Further, the reason behind the high asset equity ratio may be that the borrowed capital is

more as compared to the capital cost (Akeem et al. 2014). Further. Very high ratio may lead

the company to the unsustainable level as additional debt increases the cost of interest which

in turn may deteriorate the financial status of the company. On the other hand, low asset-

equity ratio indicates that firm’s position is strong and requires no further debt or the

company is over conservative and missing the business opportunities.

iii. Reasons why ROE is greater than ROA

EBIT/TA * NPAT/EBIT * TA/OE = 381,031/10,126,129 * 89,795/381,031 *

10,126,129/47,25,316 = 0.019

NPAT/OE = 89,795/4725316 = 0.019

From the above calculation it can be proved that EBIT/TA * NPAT/EBIT * TA/OE =

NPAT/OE

ii. Phenomenon of TA/OE

The phenomenon of TA/OE represents the total assets of the company as compared to

it’s to its owner’s equity or ordinary equity. It stats the exposure of the company towards the

risk of insolvency and measures the shareholder’s risk exposures as compared to the

company’s total assets. If the company’s total assets reduce, it will increase the return on

assets whereas if the total assets of the company go up, it will reduce the return on assets of

the company (Naser et al. 2013). The value and importance of the total asset to equity ratio

depends on the industry, present economic status, company’s sales and assets and various

other factors. Though there is no ideal value for the ratio and it is used for comparing the

business with its peers. However, high ratio indicates that the company is highly leveraged.

Further, the reason behind the high asset equity ratio may be that the borrowed capital is

more as compared to the capital cost (Akeem et al. 2014). Further. Very high ratio may lead

the company to the unsustainable level as additional debt increases the cost of interest which

in turn may deteriorate the financial status of the company. On the other hand, low asset-

equity ratio indicates that firm’s position is strong and requires no further debt or the

company is over conservative and missing the business opportunities.

iii. Reasons why ROE is greater than ROA

5FINANCE FOR BUSINESS - MASTERS

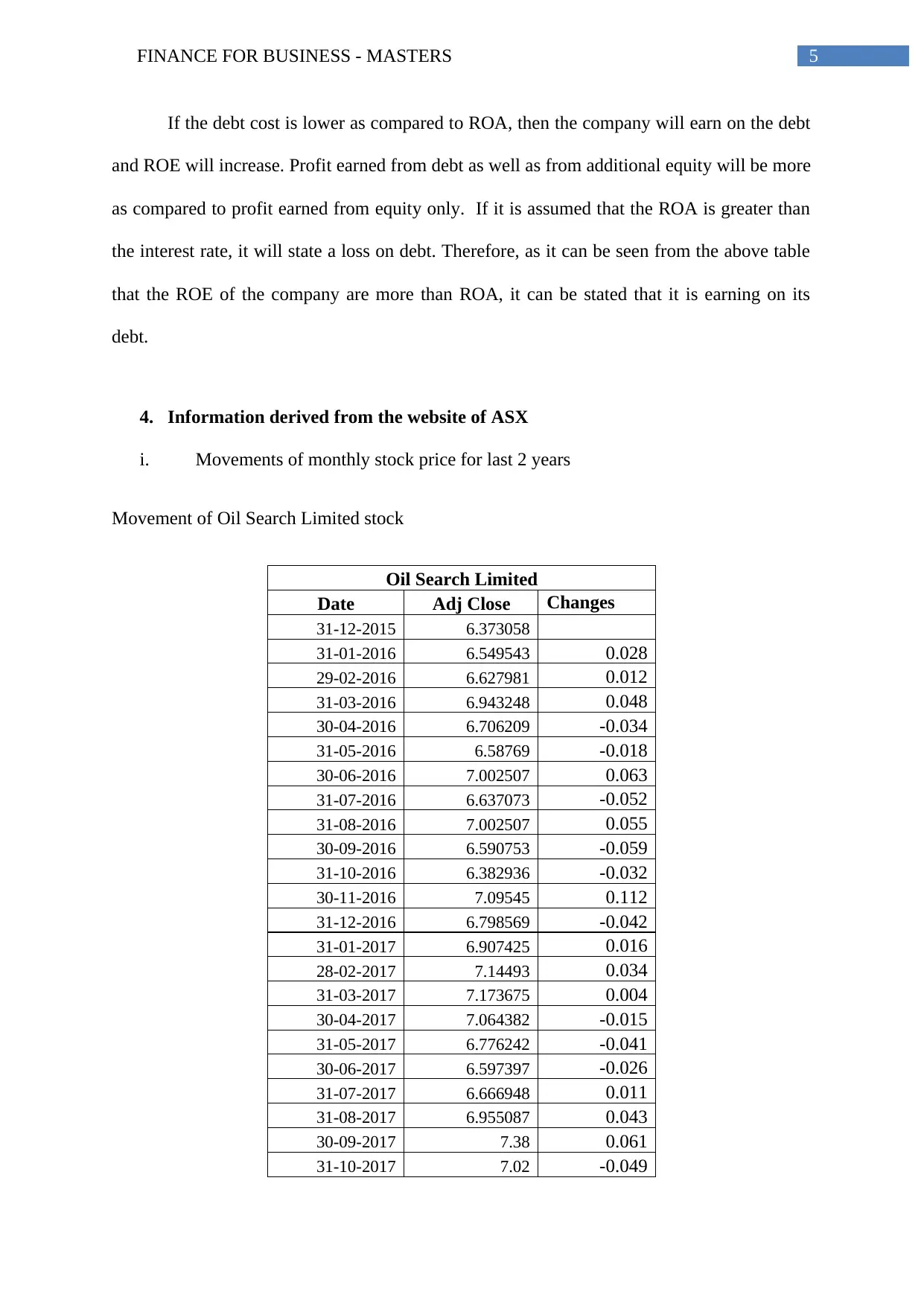

If the debt cost is lower as compared to ROA, then the company will earn on the debt

and ROE will increase. Profit earned from debt as well as from additional equity will be more

as compared to profit earned from equity only. If it is assumed that the ROA is greater than

the interest rate, it will state a loss on debt. Therefore, as it can be seen from the above table

that the ROE of the company are more than ROA, it can be stated that it is earning on its

debt.

4. Information derived from the website of ASX

i. Movements of monthly stock price for last 2 years

Movement of Oil Search Limited stock

Oil Search Limited

Date Adj Close Changes

31-12-2015 6.373058

31-01-2016 6.549543 0.028

29-02-2016 6.627981 0.012

31-03-2016 6.943248 0.048

30-04-2016 6.706209 -0.034

31-05-2016 6.58769 -0.018

30-06-2016 7.002507 0.063

31-07-2016 6.637073 -0.052

31-08-2016 7.002507 0.055

30-09-2016 6.590753 -0.059

31-10-2016 6.382936 -0.032

30-11-2016 7.09545 0.112

31-12-2016 6.798569 -0.042

31-01-2017 6.907425 0.016

28-02-2017 7.14493 0.034

31-03-2017 7.173675 0.004

30-04-2017 7.064382 -0.015

31-05-2017 6.776242 -0.041

30-06-2017 6.597397 -0.026

31-07-2017 6.666948 0.011

31-08-2017 6.955087 0.043

30-09-2017 7.38 0.061

31-10-2017 7.02 -0.049

If the debt cost is lower as compared to ROA, then the company will earn on the debt

and ROE will increase. Profit earned from debt as well as from additional equity will be more

as compared to profit earned from equity only. If it is assumed that the ROA is greater than

the interest rate, it will state a loss on debt. Therefore, as it can be seen from the above table

that the ROE of the company are more than ROA, it can be stated that it is earning on its

debt.

4. Information derived from the website of ASX

i. Movements of monthly stock price for last 2 years

Movement of Oil Search Limited stock

Oil Search Limited

Date Adj Close Changes

31-12-2015 6.373058

31-01-2016 6.549543 0.028

29-02-2016 6.627981 0.012

31-03-2016 6.943248 0.048

30-04-2016 6.706209 -0.034

31-05-2016 6.58769 -0.018

30-06-2016 7.002507 0.063

31-07-2016 6.637073 -0.052

31-08-2016 7.002507 0.055

30-09-2016 6.590753 -0.059

31-10-2016 6.382936 -0.032

30-11-2016 7.09545 0.112

31-12-2016 6.798569 -0.042

31-01-2017 6.907425 0.016

28-02-2017 7.14493 0.034

31-03-2017 7.173675 0.004

30-04-2017 7.064382 -0.015

31-05-2017 6.776242 -0.041

30-06-2017 6.597397 -0.026

31-07-2017 6.666948 0.011

31-08-2017 6.955087 0.043

30-09-2017 7.38 0.061

31-10-2017 7.02 -0.049

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS - MASTERS

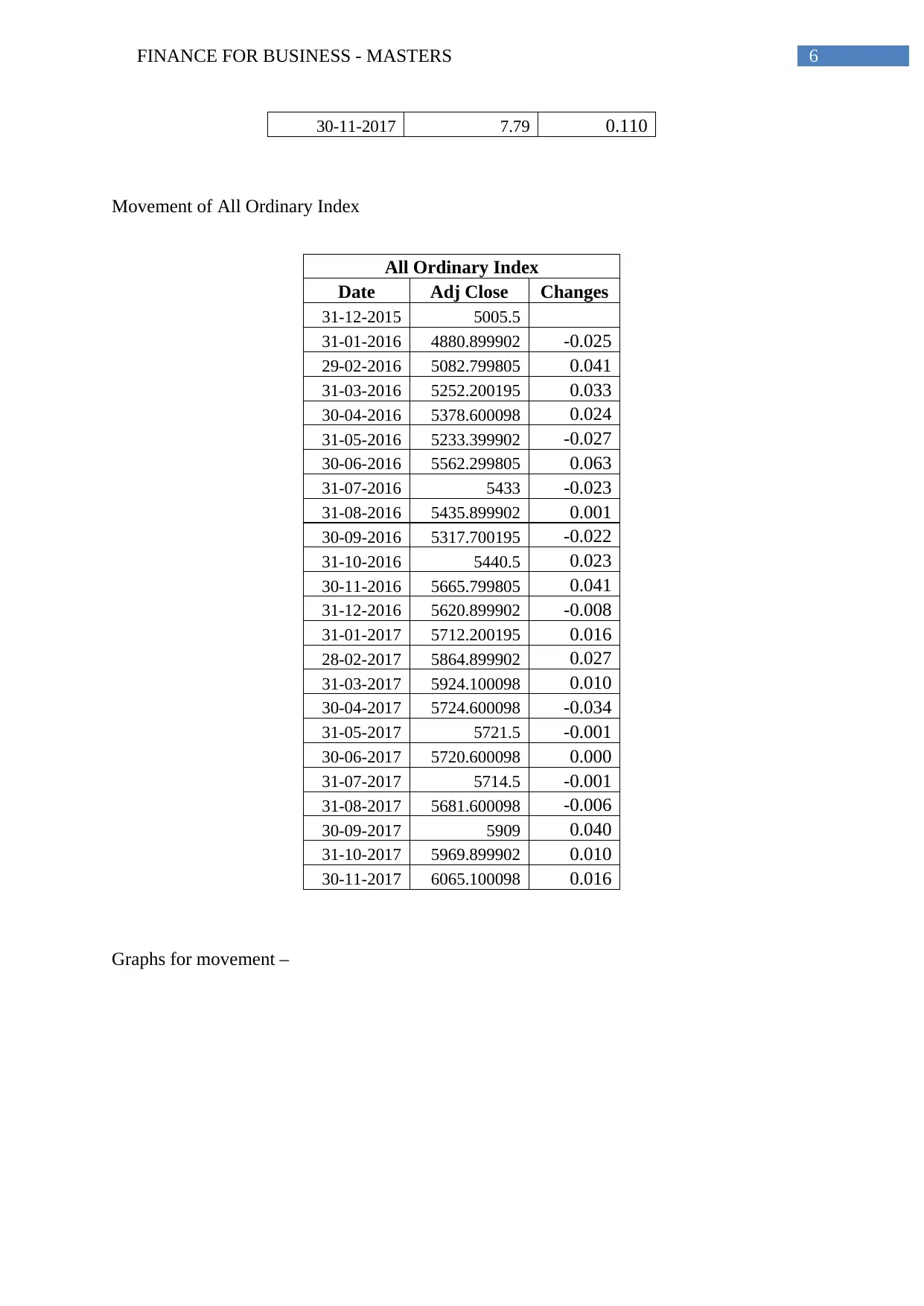

30-11-2017 7.79 0.110

Movement of All Ordinary Index

All Ordinary Index

Date Adj Close Changes

31-12-2015 5005.5

31-01-2016 4880.899902 -0.025

29-02-2016 5082.799805 0.041

31-03-2016 5252.200195 0.033

30-04-2016 5378.600098 0.024

31-05-2016 5233.399902 -0.027

30-06-2016 5562.299805 0.063

31-07-2016 5433 -0.023

31-08-2016 5435.899902 0.001

30-09-2016 5317.700195 -0.022

31-10-2016 5440.5 0.023

30-11-2016 5665.799805 0.041

31-12-2016 5620.899902 -0.008

31-01-2017 5712.200195 0.016

28-02-2017 5864.899902 0.027

31-03-2017 5924.100098 0.010

30-04-2017 5724.600098 -0.034

31-05-2017 5721.5 -0.001

30-06-2017 5720.600098 0.000

31-07-2017 5714.5 -0.001

31-08-2017 5681.600098 -0.006

30-09-2017 5909 0.040

31-10-2017 5969.899902 0.010

30-11-2017 6065.100098 0.016

Graphs for movement –

30-11-2017 7.79 0.110

Movement of All Ordinary Index

All Ordinary Index

Date Adj Close Changes

31-12-2015 5005.5

31-01-2016 4880.899902 -0.025

29-02-2016 5082.799805 0.041

31-03-2016 5252.200195 0.033

30-04-2016 5378.600098 0.024

31-05-2016 5233.399902 -0.027

30-06-2016 5562.299805 0.063

31-07-2016 5433 -0.023

31-08-2016 5435.899902 0.001

30-09-2016 5317.700195 -0.022

31-10-2016 5440.5 0.023

30-11-2016 5665.799805 0.041

31-12-2016 5620.899902 -0.008

31-01-2017 5712.200195 0.016

28-02-2017 5864.899902 0.027

31-03-2017 5924.100098 0.010

30-04-2017 5724.600098 -0.034

31-05-2017 5721.5 -0.001

30-06-2017 5720.600098 0.000

31-07-2017 5714.5 -0.001

31-08-2017 5681.600098 -0.006

30-09-2017 5909 0.040

31-10-2017 5969.899902 0.010

30-11-2017 6065.100098 0.016

Graphs for movement –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS - MASTERS

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1

2

3

4

5

6

7

8

9

Oil Search Limited

Adj Close

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1000

2000

3000

4000

5000

6000

7000

All Ordinary Index

Adj Close

ii. Report on movement of the stock

It can be recognized from the above table and graphs that both the stocks are upward

moving. However, if closely looked, it can be seen that the stock of Oil Search Limited is

more fluctuating as compared to the All Ordinary Stock. Therefore, it can be stated that the

stock of Oil Search Limited is more volatile. Further, the correlations between 2 funds are

computed as 0.732. Therefore, the stocks are positively correlated.

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1

2

3

4

5

6

7

8

9

Oil Search Limited

Adj Close

01/12/2015

01/02/2016

01/04/2016

01/06/2016

01/08/2016

01/10/2016

01/12/2016

01/02/2017

01/04/2017

01/06/2017

01/08/2017

01/10/2017

0

1000

2000

3000

4000

5000

6000

7000

All Ordinary Index

Adj Close

ii. Report on movement of the stock

It can be recognized from the above table and graphs that both the stocks are upward

moving. However, if closely looked, it can be seen that the stock of Oil Search Limited is

more fluctuating as compared to the All Ordinary Stock. Therefore, it can be stated that the

stock of Oil Search Limited is more volatile. Further, the correlations between 2 funds are

computed as 0.732. Therefore, the stocks are positively correlated.

8FINANCE FOR BUSINESS - MASTERS

5. Recent announcements

On 1st November 2017, the company announced that it has acquired the interest in

world-class Tier 1 oil assets under Alaskan North Slope with material potential of

growth. The acquisition was 8 months of the comprehensive due diligence and it was

very important comprehensive due diligence for the company.

On 24th August 2017 the company served notice regarding change in the substantial

interest with regard to shareholding, under section 671B. For the purpose of notice the

outstanding share balance of 15,23,631,192, shares were used for calculating the

holding percentage.

On 14th June 2017 the company successfully tested the production of Muruk 1ST3 to

south west of Muruk 1 gas recovery. The drilling programme of Muruk successfully

discovered the potential significant new gas field. The data generated from Muruk

well and the 3 sidetracks will be analysed for assessing the potential resources for gas.

On 3rd January 2017, the director of Oil Search Limited Mr Peter Botten changed his

shareholding on account of the ordinary restricted shares. The consideration paid for

each share was A$ 7.17. Prior to change, the number of shareholdings were 23,68,039

ordinary shares. After changing the holding, the number of securities held by the

director was 15,94,082 ordinary shares.

On 21st November 2016 the company successfully help the TB patients to complete

their treatment along with Kikori Hospital. The oil search foundation is continuing

their support to the hospital with the ongoing food supplementation and is also

working with the local group of women for providing food at lower cost for the

patients.

5. Recent announcements

On 1st November 2017, the company announced that it has acquired the interest in

world-class Tier 1 oil assets under Alaskan North Slope with material potential of

growth. The acquisition was 8 months of the comprehensive due diligence and it was

very important comprehensive due diligence for the company.

On 24th August 2017 the company served notice regarding change in the substantial

interest with regard to shareholding, under section 671B. For the purpose of notice the

outstanding share balance of 15,23,631,192, shares were used for calculating the

holding percentage.

On 14th June 2017 the company successfully tested the production of Muruk 1ST3 to

south west of Muruk 1 gas recovery. The drilling programme of Muruk successfully

discovered the potential significant new gas field. The data generated from Muruk

well and the 3 sidetracks will be analysed for assessing the potential resources for gas.

On 3rd January 2017, the director of Oil Search Limited Mr Peter Botten changed his

shareholding on account of the ordinary restricted shares. The consideration paid for

each share was A$ 7.17. Prior to change, the number of shareholdings were 23,68,039

ordinary shares. After changing the holding, the number of securities held by the

director was 15,94,082 ordinary shares.

On 21st November 2016 the company successfully help the TB patients to complete

their treatment along with Kikori Hospital. The oil search foundation is continuing

their support to the hospital with the ongoing food supplementation and is also

working with the local group of women for providing food at lower cost for the

patients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR BUSINESS - MASTERS

6. Stock field

i. Calculated beta for the company is 0.69

ii. Risk free rate = Rf = 4%, market risk premium = Rm = 6%

Therefore, required rate of return for the company’s share =

R = Rf + β ( Rm – Rf )

R = 4% + 0.69* (6% – 4%) = 5.38% (Zabarankin, Pavlikov and Uryasev 2014)

iii. Conservative investment

Conservative investment is the investment strategy that preserves the value of

investment portfolio through investing at securities associated with lower risks. Lower risks

here mean the investment with fixed money market securities and fixed income (Halili, Saleh

and Zeitun 2015). The fund with lower beta, higher return and regular dividend paying may be

considered as conservative investment. From the above analysis it can be found that the beta

of the company is 0.69 which can be considered as low and the ROE of the company is more

than its ROA (Renneboog and Szilagyi 2015). Further, it can be found from the annual report

of the company that the company is regular in paying dividend to the shareholders and it paid

3.5 US cents dividend per share during the year 2016. Therefore, the company Oil Search

Limited is considered as a conservative investment.

7. Weighted average cost of capital

i. Calculation of WACC

For computation of WACC the company’s capital cost under each category of the

capital is weighted proportionately. All the sources of capital that includes the preferred

stock, common stock, bonds and other non-current debts are taken into consideration for

6. Stock field

i. Calculated beta for the company is 0.69

ii. Risk free rate = Rf = 4%, market risk premium = Rm = 6%

Therefore, required rate of return for the company’s share =

R = Rf + β ( Rm – Rf )

R = 4% + 0.69* (6% – 4%) = 5.38% (Zabarankin, Pavlikov and Uryasev 2014)

iii. Conservative investment

Conservative investment is the investment strategy that preserves the value of

investment portfolio through investing at securities associated with lower risks. Lower risks

here mean the investment with fixed money market securities and fixed income (Halili, Saleh

and Zeitun 2015). The fund with lower beta, higher return and regular dividend paying may be

considered as conservative investment. From the above analysis it can be found that the beta

of the company is 0.69 which can be considered as low and the ROE of the company is more

than its ROA (Renneboog and Szilagyi 2015). Further, it can be found from the annual report

of the company that the company is regular in paying dividend to the shareholders and it paid

3.5 US cents dividend per share during the year 2016. Therefore, the company Oil Search

Limited is considered as a conservative investment.

7. Weighted average cost of capital

i. Calculation of WACC

For computation of WACC the company’s capital cost under each category of the

capital is weighted proportionately. All the sources of capital that includes the preferred

stock, common stock, bonds and other non-current debts are taken into consideration for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS - MASTERS

calculation of WACC. With the increase of rate of return on the equity and beta the WACC

of the company goes up (Ajanthan 2013). However, the increase in WACC denotes the

reduction in valuation and increase in the risk. The WACC is calculates as follows –

WACC = E/V * Re +D/V * Rd * (1-Tc), Where,

E/V = Percentage of equity in capital structure

D/V = Percentage of debt in capital structure

Re = Cost of equity = 5.38%

Rd = Rate of debt = 4.85%

Tc = corporate tax rate

As per the given information in the annual report –

Amount in $'000

Amount of Debt 4012278.00

Amount of Equity 3147340.00

Total 7159618.00

Percentage of debt 56%

Percentage of equity 44%

Therefore, WACC = 56*5.38% + 44*4.85% (1-0.515)

= 3.018 + 1.03499

= 3.16899% or 3.17%.

ii. Implication of Higher WACC on management’s evaluation

The (WACC) weighted average cost of the capital is the rate which the company

expects for paying on average to all the security holders for financing the assets. It is the

calculation of WACC. With the increase of rate of return on the equity and beta the WACC

of the company goes up (Ajanthan 2013). However, the increase in WACC denotes the

reduction in valuation and increase in the risk. The WACC is calculates as follows –

WACC = E/V * Re +D/V * Rd * (1-Tc), Where,

E/V = Percentage of equity in capital structure

D/V = Percentage of debt in capital structure

Re = Cost of equity = 5.38%

Rd = Rate of debt = 4.85%

Tc = corporate tax rate

As per the given information in the annual report –

Amount in $'000

Amount of Debt 4012278.00

Amount of Equity 3147340.00

Total 7159618.00

Percentage of debt 56%

Percentage of equity 44%

Therefore, WACC = 56*5.38% + 44*4.85% (1-0.515)

= 3.018 + 1.03499

= 3.16899% or 3.17%.

ii. Implication of Higher WACC on management’s evaluation

The (WACC) weighted average cost of the capital is the rate which the company

expects for paying on average to all the security holders for financing the assets. It is the

11FINANCE FOR BUSINESS - MASTERS

company’s cost of capital (Zabarankin, Pavlikov and Uryasev 2014). Further, the WACC of

the company is influenced by the external market and not by the management. It shows the

cost of firm for using the money to the projects that are intended for generating growth.

Whether the money is arranged through debt or through equity it comes in exchange of cost.

Higher WACC denotes that the company is associated with more risk. Therefore, if the

company has higher WACC, the management will try to arrange the fund through cheaper

sources (Baños-Caballero, García-Teruel and Martínez-Solano 2014). In such cases, it is the

indication that the company is losing its value and possibilities are there that more efficient

projects are there for investing.

8. Debt ratio

i. Optimal capital structure

Debt ratio Total liabilities / Total assets Year 2016 - 0.533 Year 2015 - 0.545

The optimal capital structure is the optimum debt to equity ratio that can maximise the

value of a company. For any company it is the one that provides the balance among the range

of debt to equity and can minimizes the company’s capital cost (Albul, Jaffee and Tchistyi

2015). Theoretically, the debt finance is regarded as having low cost capital as compared to

equity as the debts are tax deductible. However, with the increase of debt the risk of the

company also increases. Generally, the debt ratio of 50% is considered as optimal capital

structure as the company has a balance among its liabilities and assets (He and

Krishnamurthy 2013). It can be seen from the above table that for both 2015 as well as 2016

the debt ratio of the company is more or less same and it is moving around 50%.

ii. Gearing ratio

company’s cost of capital (Zabarankin, Pavlikov and Uryasev 2014). Further, the WACC of

the company is influenced by the external market and not by the management. It shows the

cost of firm for using the money to the projects that are intended for generating growth.

Whether the money is arranged through debt or through equity it comes in exchange of cost.

Higher WACC denotes that the company is associated with more risk. Therefore, if the

company has higher WACC, the management will try to arrange the fund through cheaper

sources (Baños-Caballero, García-Teruel and Martínez-Solano 2014). In such cases, it is the

indication that the company is losing its value and possibilities are there that more efficient

projects are there for investing.

8. Debt ratio

i. Optimal capital structure

Debt ratio Total liabilities / Total assets Year 2016 - 0.533 Year 2015 - 0.545

The optimal capital structure is the optimum debt to equity ratio that can maximise the

value of a company. For any company it is the one that provides the balance among the range

of debt to equity and can minimizes the company’s capital cost (Albul, Jaffee and Tchistyi

2015). Theoretically, the debt finance is regarded as having low cost capital as compared to

equity as the debts are tax deductible. However, with the increase of debt the risk of the

company also increases. Generally, the debt ratio of 50% is considered as optimal capital

structure as the company has a balance among its liabilities and assets (He and

Krishnamurthy 2013). It can be seen from the above table that for both 2015 as well as 2016

the debt ratio of the company is more or less same and it is moving around 50%.

ii. Gearing ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.