Sweet Menu Restaurant: Finance Sources and Implications Analysis

VerifiedAdded on 2020/02/14

|16

|5543

|379

Report

AI Summary

This report analyzes the financial strategies for the expansion of Sweet Menu Restaurant, focusing on the identification and evaluation of various funding sources. It begins by outlining potential sources of finance, including share capital, debentures, retained earnings, loans, venture funding, hire purchase, and leasing, and explores the implications of each, considering legal and financial aspects. The report then evaluates the most appropriate sources for the restaurant, recommending a combination of retained earnings, bank loans, and hire purchase. It analyzes the costs associated with these choices, including interest rates on loans and potential risks related to retained earnings and hire purchase agreements. The report also delves into financial planning, assessing information needs for decision-makers and the impact of selected finance sources. Furthermore, it includes a budget analysis, unit cost calculations, and investment appraisal techniques to assess the project's feasibility, culminating in a discussion of financial statements and ratio analysis to provide a comprehensive financial overview.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Sources of finances available.....................................................................................................3

1.2 Implication of the sources..........................................................................................................4

1.3 Evaluation of most appropriate sources. ...................................................................................6

TASK 2.................................................................................................................................................6

2.1 Analysing cost of different sources............................................................................................6

2.2 Importance of financial planning...............................................................................................7

2.3 Assessment of information needs of decision makers. .............................................................7

2.4 Impact of identified source of finance.......................................................................................8

TASK 3.................................................................................................................................................8

3.1 Analysis of the budget and proposed recommendations............................................................8

3.2 Calculations of Unit cost and pricing decisions.........................................................................9

3.3 Assessment of the projects through investment appraisal techniques.......................................9

TASK 4...............................................................................................................................................11

4.1 Discussion on the financial statements....................................................................................11

4.2 Comparison of different financial formats...............................................................................12

4.3 Ratio analysis...........................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Sources of finances available.....................................................................................................3

1.2 Implication of the sources..........................................................................................................4

1.3 Evaluation of most appropriate sources. ...................................................................................6

TASK 2.................................................................................................................................................6

2.1 Analysing cost of different sources............................................................................................6

2.2 Importance of financial planning...............................................................................................7

2.3 Assessment of information needs of decision makers. .............................................................7

2.4 Impact of identified source of finance.......................................................................................8

TASK 3.................................................................................................................................................8

3.1 Analysis of the budget and proposed recommendations............................................................8

3.2 Calculations of Unit cost and pricing decisions.........................................................................9

3.3 Assessment of the projects through investment appraisal techniques.......................................9

TASK 4...............................................................................................................................................11

4.1 Discussion on the financial statements....................................................................................11

4.2 Comparison of different financial formats...............................................................................12

4.3 Ratio analysis...........................................................................................................................12

CONCLUSION..................................................................................................................................13

REFERENCES...................................................................................................................................14

INTRODUCTION

Financial resource plays a vital role for the development and smooth operations of a

business. They are the core pillars for establishing any business and making it a success. It is very

important for the business to manage financial resources available to the enterprise in effective

manner. A business requires financial assistance at various steps (Keller, 2013). Decision making is

one among the different steps. The financial manager requires finances while planning or

implementing the decision into the firms. Financial funds available to the business must be used

very appropriately and the manager must examine the return on investment being generated.

The current report is on identifying available sources of finance available to Sweet Menu

Restaurant. As the restaurant is doing well in terms of profitability, the owners are planning for

expansion to two new locations; one being in Central London and the other in Croydon. The finance

manager has acquired few choices to raise funds for the business. For this, an in-depth assessment

has been done by the manager to ascertain the feasibility of choices of finances (Kil, 2013). The

other part of the report discusses about raising budget for Blue Island Restaurant. Directors

understand the relevance of budget and cost as they have less knowledge about financial planning.

Thus, to evaluate the sources and choices available to both the businesses, various techniques have

been used which are discussed in the report.

TASK 1

1.1 Sources of finances available

Sweet Menu restaurant is planning to expand its business to two new locations, the business

requires identifying available sources of finances. They are as follows-

Long term sources of finance Share Capital- Share capital signifies sharing of ownership rights to a business or company.

They are considered as a cheaper mode as compared to shares. The share holders ave a equal

right in the decision making of the company. Debentures- The company can also raise capital with the help of debentures (External

Source of Finance / Capital, 2016). The company does not have to share its control with the

debenture holders and in return only have to provide them with timely dividends. Retained Earnings- A portion of income is reserved by the organisation which is known as

retained earnings. Instead of distributing dividends among the investors, the organisation

Financial resource plays a vital role for the development and smooth operations of a

business. They are the core pillars for establishing any business and making it a success. It is very

important for the business to manage financial resources available to the enterprise in effective

manner. A business requires financial assistance at various steps (Keller, 2013). Decision making is

one among the different steps. The financial manager requires finances while planning or

implementing the decision into the firms. Financial funds available to the business must be used

very appropriately and the manager must examine the return on investment being generated.

The current report is on identifying available sources of finance available to Sweet Menu

Restaurant. As the restaurant is doing well in terms of profitability, the owners are planning for

expansion to two new locations; one being in Central London and the other in Croydon. The finance

manager has acquired few choices to raise funds for the business. For this, an in-depth assessment

has been done by the manager to ascertain the feasibility of choices of finances (Kil, 2013). The

other part of the report discusses about raising budget for Blue Island Restaurant. Directors

understand the relevance of budget and cost as they have less knowledge about financial planning.

Thus, to evaluate the sources and choices available to both the businesses, various techniques have

been used which are discussed in the report.

TASK 1

1.1 Sources of finances available

Sweet Menu restaurant is planning to expand its business to two new locations, the business

requires identifying available sources of finances. They are as follows-

Long term sources of finance Share Capital- Share capital signifies sharing of ownership rights to a business or company.

They are considered as a cheaper mode as compared to shares. The share holders ave a equal

right in the decision making of the company. Debentures- The company can also raise capital with the help of debentures (External

Source of Finance / Capital, 2016). The company does not have to share its control with the

debenture holders and in return only have to provide them with timely dividends. Retained Earnings- A portion of income is reserved by the organisation which is known as

retained earnings. Instead of distributing dividends among the investors, the organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

may decide to hold the income in order to retain the earning for future use. It is easier for the

business to reinvest retained earnings to his/her company. Loan- A loan may be lended by a bank or a financial institution or by a friend and relative

(Sources of finance, 2012). Loan seekers require paying for a security in terms of getting the

loan approved. The security is kept in hold with the loan giver. Seeker of the loan will have

to pay the principal amount along with the interest amount. Loan can be used for purchasing

assets or inventory for the company.

Venture funding- The venture capitalist are investors who invest in a business by examining

its feasibility. They tend to acquire stocks or ownership in the business. They are generally

those people who have a set of money but they do not know as to where to invest it

(Financial ratio and Analysis, 2013). Thus, they tend to find potential start-ups or business

that has high potential for generating profitability.

Short term sources of finance

Hire Purchase/ Leasing- Hire purchase is a short term loan, as the business would have to

return principal amount in the form of instalments. Purchaser purchases certain goods or

machinery in the form of hires purchase but can repay the amount on instalment basis

(Managing financial resources, 2014). In leasing, business rents a property or equipment

from the lessor under contractual agreements. For example, the restaurant can lease

computer or microwave oven for a set period of time by paying amount in instalment.

1.2 Implication of the sources

Sources Share Capital/

Debentures

Retained

Earnings

Loan Venture

Capital

Hire

Purchase/Leas

ing

Legal

Implications

The company

have to clearly

state the fact

related to

shares and

dentures under

a legal

statement

(Ryan, 2009).

This is to avoid

any legal

The

shareholders

may not agree

to retain

earning of the

company as it

may restrict

their right to

receive

dividends.

The company

have to make

sure to

understand all

the terms and

condition

provided by

the bank or

financial

institution.

They also have

The

organization

will have to

make sure to

duly

understand the

demands of the

venture

capitalist

before making

any contracts

The lessor or

the owner may

take legal

actions against

the company

(Brealey,

2012). If the

business is not

able to pay for

the instalment

amount on the

business to reinvest retained earnings to his/her company. Loan- A loan may be lended by a bank or a financial institution or by a friend and relative

(Sources of finance, 2012). Loan seekers require paying for a security in terms of getting the

loan approved. The security is kept in hold with the loan giver. Seeker of the loan will have

to pay the principal amount along with the interest amount. Loan can be used for purchasing

assets or inventory for the company.

Venture funding- The venture capitalist are investors who invest in a business by examining

its feasibility. They tend to acquire stocks or ownership in the business. They are generally

those people who have a set of money but they do not know as to where to invest it

(Financial ratio and Analysis, 2013). Thus, they tend to find potential start-ups or business

that has high potential for generating profitability.

Short term sources of finance

Hire Purchase/ Leasing- Hire purchase is a short term loan, as the business would have to

return principal amount in the form of instalments. Purchaser purchases certain goods or

machinery in the form of hires purchase but can repay the amount on instalment basis

(Managing financial resources, 2014). In leasing, business rents a property or equipment

from the lessor under contractual agreements. For example, the restaurant can lease

computer or microwave oven for a set period of time by paying amount in instalment.

1.2 Implication of the sources

Sources Share Capital/

Debentures

Retained

Earnings

Loan Venture

Capital

Hire

Purchase/Leas

ing

Legal

Implications

The company

have to clearly

state the fact

related to

shares and

dentures under

a legal

statement

(Ryan, 2009).

This is to avoid

any legal

The

shareholders

may not agree

to retain

earning of the

company as it

may restrict

their right to

receive

dividends.

The company

have to make

sure to

understand all

the terms and

condition

provided by

the bank or

financial

institution.

They also have

The

organization

will have to

make sure to

duly

understand the

demands of the

venture

capitalist

before making

any contracts

The lessor or

the owner may

take legal

actions against

the company

(Brealey,

2012). If the

business is not

able to pay for

the instalment

amount on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

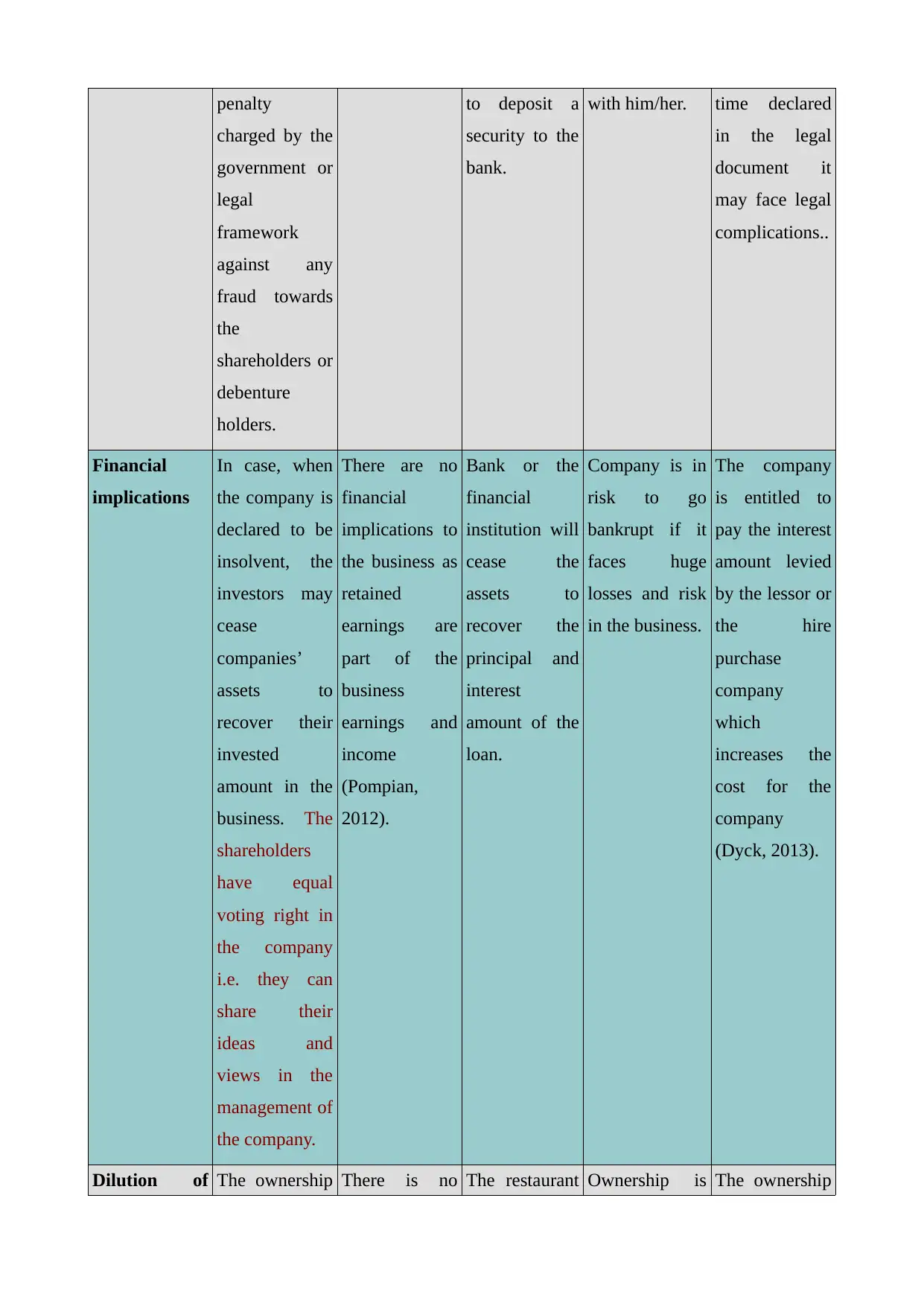

penalty

charged by the

government or

legal

framework

against any

fraud towards

the

shareholders or

debenture

holders.

to deposit a

security to the

bank.

with him/her. time declared

in the legal

document it

may face legal

complications..

Financial

implications

In case, when

the company is

declared to be

insolvent, the

investors may

cease

companies’

assets to

recover their

invested

amount in the

business. The

shareholders

have equal

voting right in

the company

i.e. they can

share their

ideas and

views in the

management of

the company.

There are no

financial

implications to

the business as

retained

earnings are

part of the

business

earnings and

income

(Pompian,

2012).

Bank or the

financial

institution will

cease the

assets to

recover the

principal and

interest

amount of the

loan.

Company is in

risk to go

bankrupt if it

faces huge

losses and risk

in the business.

The company

is entitled to

pay the interest

amount levied

by the lessor or

the hire

purchase

company

which

increases the

cost for the

company

(Dyck, 2013).

Dilution of The ownership There is no The restaurant Ownership is The ownership

charged by the

government or

legal

framework

against any

fraud towards

the

shareholders or

debenture

holders.

to deposit a

security to the

bank.

with him/her. time declared

in the legal

document it

may face legal

complications..

Financial

implications

In case, when

the company is

declared to be

insolvent, the

investors may

cease

companies’

assets to

recover their

invested

amount in the

business. The

shareholders

have equal

voting right in

the company

i.e. they can

share their

ideas and

views in the

management of

the company.

There are no

financial

implications to

the business as

retained

earnings are

part of the

business

earnings and

income

(Pompian,

2012).

Bank or the

financial

institution will

cease the

assets to

recover the

principal and

interest

amount of the

loan.

Company is in

risk to go

bankrupt if it

faces huge

losses and risk

in the business.

The company

is entitled to

pay the interest

amount levied

by the lessor or

the hire

purchase

company

which

increases the

cost for the

company

(Dyck, 2013).

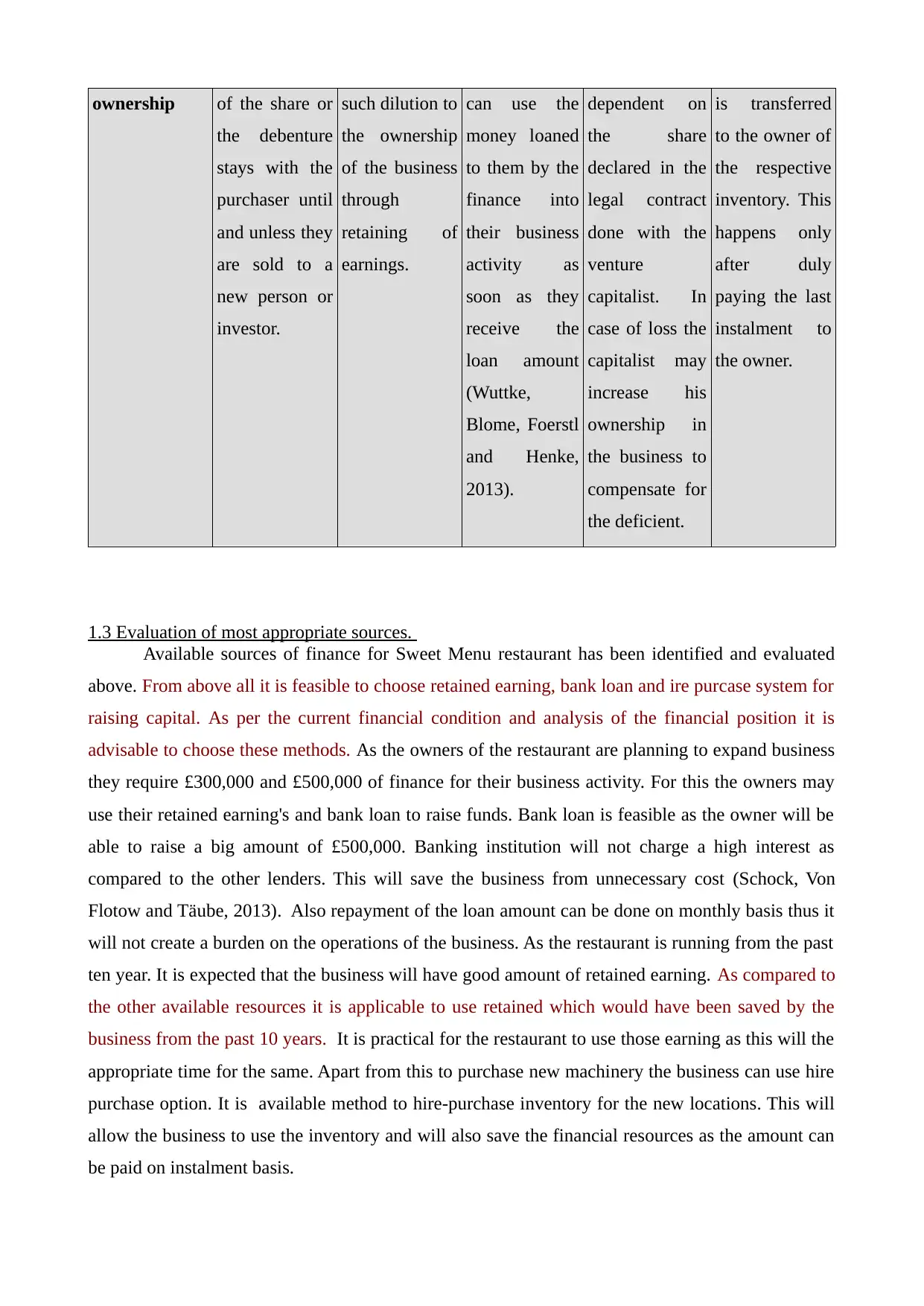

Dilution of The ownership There is no The restaurant Ownership is The ownership

ownership of the share or

the debenture

stays with the

purchaser until

and unless they

are sold to a

new person or

investor.

such dilution to

the ownership

of the business

through

retaining of

earnings.

can use the

money loaned

to them by the

finance into

their business

activity as

soon as they

receive the

loan amount

(Wuttke,

Blome, Foerstl

and Henke,

2013).

dependent on

the share

declared in the

legal contract

done with the

venture

capitalist. In

case of loss the

capitalist may

increase his

ownership in

the business to

compensate for

the deficient.

is transferred

to the owner of

the respective

inventory. This

happens only

after duly

paying the last

instalment to

the owner.

1.3 Evaluation of most appropriate sources.

Available sources of finance for Sweet Menu restaurant has been identified and evaluated

above. From above all it is feasible to choose retained earning, bank loan and ire purcase system for

raising capital. As per the current financial condition and analysis of the financial position it is

advisable to choose these methods. As the owners of the restaurant are planning to expand business

they require £300,000 and £500,000 of finance for their business activity. For this the owners may

use their retained earning's and bank loan to raise funds. Bank loan is feasible as the owner will be

able to raise a big amount of £500,000. Banking institution will not charge a high interest as

compared to the other lenders. This will save the business from unnecessary cost (Schock, Von

Flotow and Täube, 2013). Also repayment of the loan amount can be done on monthly basis thus it

will not create a burden on the operations of the business. As the restaurant is running from the past

ten year. It is expected that the business will have good amount of retained earning. As compared to

the other available resources it is applicable to use retained which would have been saved by the

business from the past 10 years. It is practical for the restaurant to use those earning as this will the

appropriate time for the same. Apart from this to purchase new machinery the business can use hire

purchase option. It is available method to hire-purchase inventory for the new locations. This will

allow the business to use the inventory and will also save the financial resources as the amount can

be paid on instalment basis.

the debenture

stays with the

purchaser until

and unless they

are sold to a

new person or

investor.

such dilution to

the ownership

of the business

through

retaining of

earnings.

can use the

money loaned

to them by the

finance into

their business

activity as

soon as they

receive the

loan amount

(Wuttke,

Blome, Foerstl

and Henke,

2013).

dependent on

the share

declared in the

legal contract

done with the

venture

capitalist. In

case of loss the

capitalist may

increase his

ownership in

the business to

compensate for

the deficient.

is transferred

to the owner of

the respective

inventory. This

happens only

after duly

paying the last

instalment to

the owner.

1.3 Evaluation of most appropriate sources.

Available sources of finance for Sweet Menu restaurant has been identified and evaluated

above. From above all it is feasible to choose retained earning, bank loan and ire purcase system for

raising capital. As per the current financial condition and analysis of the financial position it is

advisable to choose these methods. As the owners of the restaurant are planning to expand business

they require £300,000 and £500,000 of finance for their business activity. For this the owners may

use their retained earning's and bank loan to raise funds. Bank loan is feasible as the owner will be

able to raise a big amount of £500,000. Banking institution will not charge a high interest as

compared to the other lenders. This will save the business from unnecessary cost (Schock, Von

Flotow and Täube, 2013). Also repayment of the loan amount can be done on monthly basis thus it

will not create a burden on the operations of the business. As the restaurant is running from the past

ten year. It is expected that the business will have good amount of retained earning. As compared to

the other available resources it is applicable to use retained which would have been saved by the

business from the past 10 years. It is practical for the restaurant to use those earning as this will the

appropriate time for the same. Apart from this to purchase new machinery the business can use hire

purchase option. It is available method to hire-purchase inventory for the new locations. This will

allow the business to use the inventory and will also save the financial resources as the amount can

be paid on instalment basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

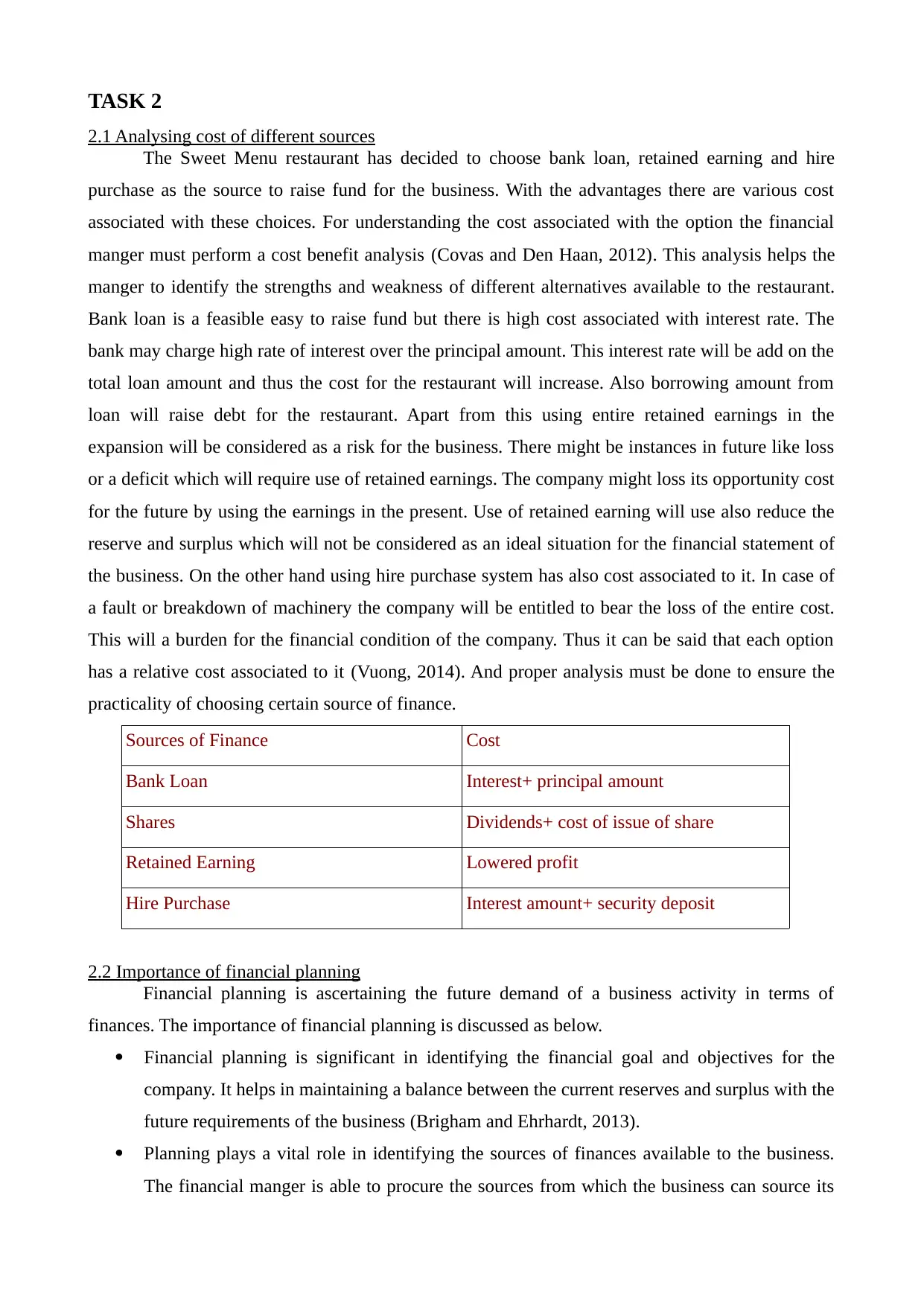

TASK 2

2.1 Analysing cost of different sources

The Sweet Menu restaurant has decided to choose bank loan, retained earning and hire

purchase as the source to raise fund for the business. With the advantages there are various cost

associated with these choices. For understanding the cost associated with the option the financial

manger must perform a cost benefit analysis (Covas and Den Haan, 2012). This analysis helps the

manger to identify the strengths and weakness of different alternatives available to the restaurant.

Bank loan is a feasible easy to raise fund but there is high cost associated with interest rate. The

bank may charge high rate of interest over the principal amount. This interest rate will be add on the

total loan amount and thus the cost for the restaurant will increase. Also borrowing amount from

loan will raise debt for the restaurant. Apart from this using entire retained earnings in the

expansion will be considered as a risk for the business. There might be instances in future like loss

or a deficit which will require use of retained earnings. The company might loss its opportunity cost

for the future by using the earnings in the present. Use of retained earning will use also reduce the

reserve and surplus which will not be considered as an ideal situation for the financial statement of

the business. On the other hand using hire purchase system has also cost associated to it. In case of

a fault or breakdown of machinery the company will be entitled to bear the loss of the entire cost.

This will a burden for the financial condition of the company. Thus it can be said that each option

has a relative cost associated to it (Vuong, 2014). And proper analysis must be done to ensure the

practicality of choosing certain source of finance.

Sources of Finance Cost

Bank Loan Interest+ principal amount

Shares Dividends+ cost of issue of share

Retained Earning Lowered profit

Hire Purchase Interest amount+ security deposit

2.2 Importance of financial planning

Financial planning is ascertaining the future demand of a business activity in terms of

finances. The importance of financial planning is discussed as below.

Financial planning is significant in identifying the financial goal and objectives for the

company. It helps in maintaining a balance between the current reserves and surplus with the

future requirements of the business (Brigham and Ehrhardt, 2013).

Planning plays a vital role in identifying the sources of finances available to the business.

The financial manger is able to procure the sources from which the business can source its

2.1 Analysing cost of different sources

The Sweet Menu restaurant has decided to choose bank loan, retained earning and hire

purchase as the source to raise fund for the business. With the advantages there are various cost

associated with these choices. For understanding the cost associated with the option the financial

manger must perform a cost benefit analysis (Covas and Den Haan, 2012). This analysis helps the

manger to identify the strengths and weakness of different alternatives available to the restaurant.

Bank loan is a feasible easy to raise fund but there is high cost associated with interest rate. The

bank may charge high rate of interest over the principal amount. This interest rate will be add on the

total loan amount and thus the cost for the restaurant will increase. Also borrowing amount from

loan will raise debt for the restaurant. Apart from this using entire retained earnings in the

expansion will be considered as a risk for the business. There might be instances in future like loss

or a deficit which will require use of retained earnings. The company might loss its opportunity cost

for the future by using the earnings in the present. Use of retained earning will use also reduce the

reserve and surplus which will not be considered as an ideal situation for the financial statement of

the business. On the other hand using hire purchase system has also cost associated to it. In case of

a fault or breakdown of machinery the company will be entitled to bear the loss of the entire cost.

This will a burden for the financial condition of the company. Thus it can be said that each option

has a relative cost associated to it (Vuong, 2014). And proper analysis must be done to ensure the

practicality of choosing certain source of finance.

Sources of Finance Cost

Bank Loan Interest+ principal amount

Shares Dividends+ cost of issue of share

Retained Earning Lowered profit

Hire Purchase Interest amount+ security deposit

2.2 Importance of financial planning

Financial planning is ascertaining the future demand of a business activity in terms of

finances. The importance of financial planning is discussed as below.

Financial planning is significant in identifying the financial goal and objectives for the

company. It helps in maintaining a balance between the current reserves and surplus with the

future requirements of the business (Brigham and Ehrhardt, 2013).

Planning plays a vital role in identifying the sources of finances available to the business.

The financial manger is able to procure the sources from which the business can source its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

funds.

It is also viable to determine and formulate policies or strategies for a business activity of

the business. The manger is able to find out different methods to properly utilise the sources

of finance by making new strategies and policies (McKinney, 2015).

Financial planning guides the manger in understanding whether the procured resources are

being utilised to their full potential or not. It is important to maintain the feasibility and

regular monitoring is facilitated by planning.

Management of the cash flow is easily done with the help of financial planning. The manger

can closely monitor the areas where unnecessary money is flowing out of the business

(Moyer, McGuigan and Rao, 2014). The manager is able to identify the shortage as well as

the surplus of cash flow in the organisation.

2.3 Assessment of information needs of decision makers.

Stakeholders are the people who have an interest in the profitably of the business. There are

different types of stakeholders and the business must ensure to provide them with every information

they require form the business.

1. Supplier- They are very important to the business as they provide or supply raw materials to

the the business (Ogiela, 2015). In a restaurant, raw materials are the key ingredients that

help make the business stand out among its competitors. The business must make sure that

the suppliers are paid on time. They play a important role in customer satisfaction thus

cordial relationship must be maintained with them to enhance their loyalty with the

restaurant.

2. Customers- The customers must be provided with excellent service and quality of the food

must be very good. In case of change in menu or tariff the customers must be informed by

the waiter or the manger (Brigham and Daves, 2012). The service of the restaurant must be

outstanding to fulfil the demand and needs of the customer.

3. Lenders- They monitor the profitability of the business to ensure their return on investment.

The business must provide them with financial information like balance sheet and profit &

loss statement. Their dues must be paid ion time to avoid any charges or penalties.

4. Employees- They are the staff and the management of the restaurant business. Being part of

the hospitality industry employees are the key person who are responsible for the services

provided to the employees (Banerjee, 2015). Financial information like working capital,

debt or cash flow must be informed to the management. They must be motivated and must

be paid with appraisal to enhance their work quality.

2.4 Impact of identified source of finance

Sweet Menu restaurant have suggested to use retained earning, bank loan and hire purchase

system to raise fund for the business. Retained earning will reduce the opportunity of the business

It is also viable to determine and formulate policies or strategies for a business activity of

the business. The manger is able to find out different methods to properly utilise the sources

of finance by making new strategies and policies (McKinney, 2015).

Financial planning guides the manger in understanding whether the procured resources are

being utilised to their full potential or not. It is important to maintain the feasibility and

regular monitoring is facilitated by planning.

Management of the cash flow is easily done with the help of financial planning. The manger

can closely monitor the areas where unnecessary money is flowing out of the business

(Moyer, McGuigan and Rao, 2014). The manager is able to identify the shortage as well as

the surplus of cash flow in the organisation.

2.3 Assessment of information needs of decision makers.

Stakeholders are the people who have an interest in the profitably of the business. There are

different types of stakeholders and the business must ensure to provide them with every information

they require form the business.

1. Supplier- They are very important to the business as they provide or supply raw materials to

the the business (Ogiela, 2015). In a restaurant, raw materials are the key ingredients that

help make the business stand out among its competitors. The business must make sure that

the suppliers are paid on time. They play a important role in customer satisfaction thus

cordial relationship must be maintained with them to enhance their loyalty with the

restaurant.

2. Customers- The customers must be provided with excellent service and quality of the food

must be very good. In case of change in menu or tariff the customers must be informed by

the waiter or the manger (Brigham and Daves, 2012). The service of the restaurant must be

outstanding to fulfil the demand and needs of the customer.

3. Lenders- They monitor the profitability of the business to ensure their return on investment.

The business must provide them with financial information like balance sheet and profit &

loss statement. Their dues must be paid ion time to avoid any charges or penalties.

4. Employees- They are the staff and the management of the restaurant business. Being part of

the hospitality industry employees are the key person who are responsible for the services

provided to the employees (Banerjee, 2015). Financial information like working capital,

debt or cash flow must be informed to the management. They must be motivated and must

be paid with appraisal to enhance their work quality.

2.4 Impact of identified source of finance

Sweet Menu restaurant have suggested to use retained earning, bank loan and hire purchase

system to raise fund for the business. Retained earning will reduce the opportunity of the business

due use the amount for future purposes. As the retained earning are shown in the liability side of the

profit and loss statement the profit will reduce in absence of retained earning. A lowered profit will

not be ideal situation for the business. Bank loan will raise the liability of the business (Cheng and

Dong, 2015). Whereas hire purchasing inventory will increase the cash outflow of the business. In

the profit and loss statement the tax calculation will rise due to te higher interest paid in the above

chosen financial resources. In this case the business is entitled to pay back the amount for the

inventory on instalment basis. The net profit will decrease due to high rate of cash outflow. As the

restaurant is entitled to pay back the principal as well as the loan amount in the given period of

time. Altogether raising sources of finance will impact the profit and loss statement of the business.

The profit is directly affected by bank loan, retained earning and hire purchase of inventory. It is

important for the financial manager to carefully monitor the impact to avoid any loss of profit.

TASK 3

3.1 Analysis of the budget and proposed recommendations.

Budget analysis is the tool used to manage budgeting process of the business. It includes

formulation, estimation and report making of the budget required by a business activity of the

restaurant. As presented in the case study, the budget of Blue island restaurant is been presented to

analyse the budget. It is very crucial for the Blue Island restaurant to analyse its budget in order to

ascertain it practicality towards the business activity (Wu and Olson, 2015). By looking at the

budget it is clearly understood that the cash sales are reasonably good which is consider as a better

condition for the restaurant. Although the restaurant is earning good, the expense for running the

restaurant is relatively higher then the sales. The restaurant is not able to manage the balance so as

to increase the net profit. It is also clear that as sales rises the expenses are also rising

simultaneously. In the month of December specifically the money outflow is more then the inflow

of the money. Thus it can analysed that the sale of services is linked with the expenses of the

business. As there is consecutive negative net balance, the restaurant must emphasize on reducing

its expense and to increase the sale.

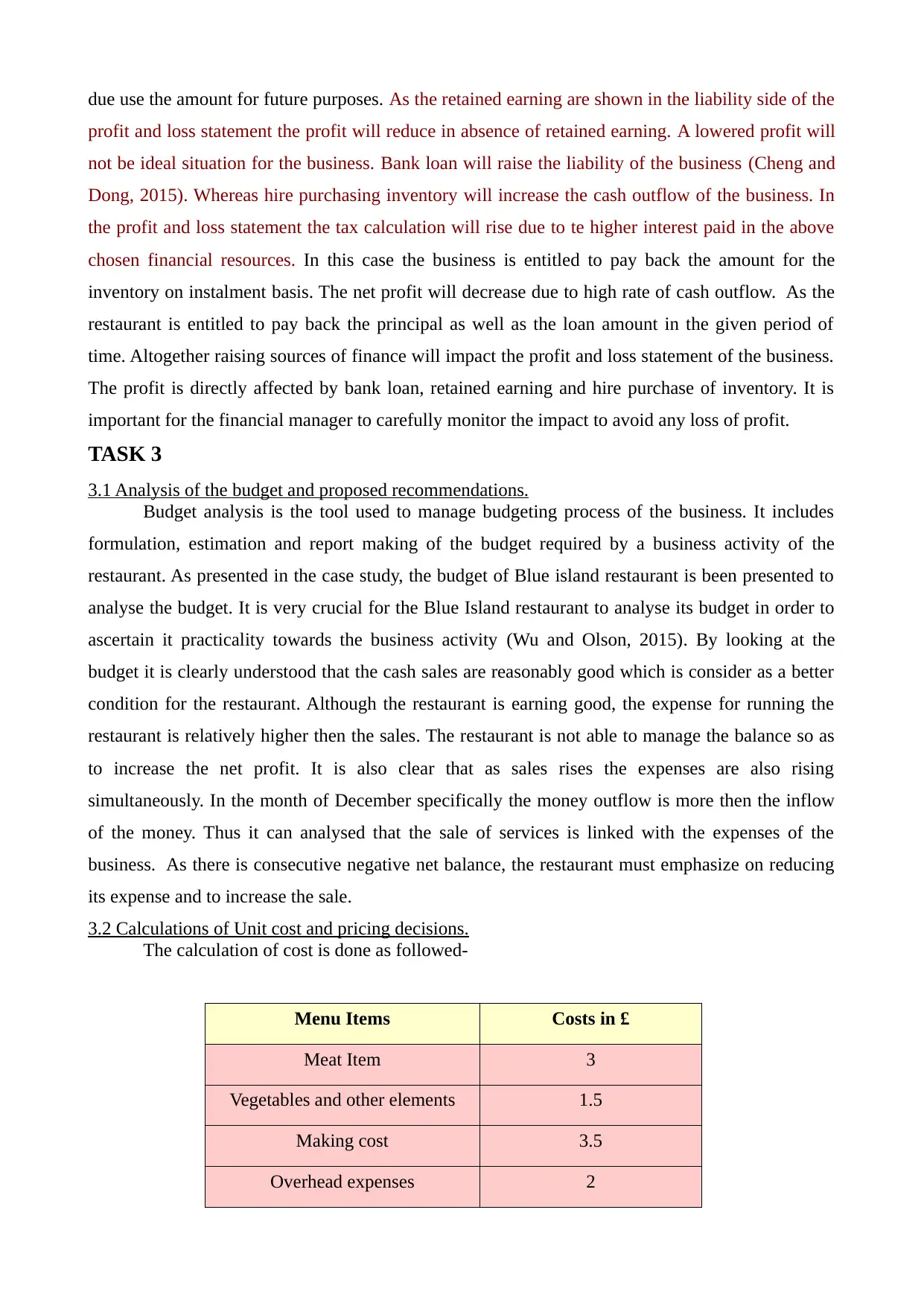

3.2 Calculations of Unit cost and pricing decisions.

The calculation of cost is done as followed-

Menu Items Costs in £

Meat Item 3

Vegetables and other elements 1.5

Making cost 3.5

Overhead expenses 2

profit and loss statement the profit will reduce in absence of retained earning. A lowered profit will

not be ideal situation for the business. Bank loan will raise the liability of the business (Cheng and

Dong, 2015). Whereas hire purchasing inventory will increase the cash outflow of the business. In

the profit and loss statement the tax calculation will rise due to te higher interest paid in the above

chosen financial resources. In this case the business is entitled to pay back the amount for the

inventory on instalment basis. The net profit will decrease due to high rate of cash outflow. As the

restaurant is entitled to pay back the principal as well as the loan amount in the given period of

time. Altogether raising sources of finance will impact the profit and loss statement of the business.

The profit is directly affected by bank loan, retained earning and hire purchase of inventory. It is

important for the financial manager to carefully monitor the impact to avoid any loss of profit.

TASK 3

3.1 Analysis of the budget and proposed recommendations.

Budget analysis is the tool used to manage budgeting process of the business. It includes

formulation, estimation and report making of the budget required by a business activity of the

restaurant. As presented in the case study, the budget of Blue island restaurant is been presented to

analyse the budget. It is very crucial for the Blue Island restaurant to analyse its budget in order to

ascertain it practicality towards the business activity (Wu and Olson, 2015). By looking at the

budget it is clearly understood that the cash sales are reasonably good which is consider as a better

condition for the restaurant. Although the restaurant is earning good, the expense for running the

restaurant is relatively higher then the sales. The restaurant is not able to manage the balance so as

to increase the net profit. It is also clear that as sales rises the expenses are also rising

simultaneously. In the month of December specifically the money outflow is more then the inflow

of the money. Thus it can analysed that the sale of services is linked with the expenses of the

business. As there is consecutive negative net balance, the restaurant must emphasize on reducing

its expense and to increase the sale.

3.2 Calculations of Unit cost and pricing decisions.

The calculation of cost is done as followed-

Menu Items Costs in £

Meat Item 3

Vegetables and other elements 1.5

Making cost 3.5

Overhead expenses 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Cost 10

Mark Up @ 40% 4

Value Added Tax 2

Total Selling Price 16

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

Percentage of Food Cost = 10/16*100

Total Percentage = 62.50%

Blue Island Restaurant is expecting 40% profit in the cost and will levy 20% VAT charges as

defined by the legal framework. As per the calculation, the total selling price of the meal is £16 and

the total food cost in percentage is 62.50%. Food costing enables the restaurant to identify the

pricing decisions (Stulz, 2015). It is helpful in identify the total sale price which allows the business

to estimate the cost that it can apply to ensure that it receives marginal profit from its sales. If the

business knows what it requires to spend, it can accordingly plan for the cost of service provided by

it. Overhead and labour cost are included as they are part of expense of the business. The restaurant

can plan for the pricing decision based on the cost that its service will incur.

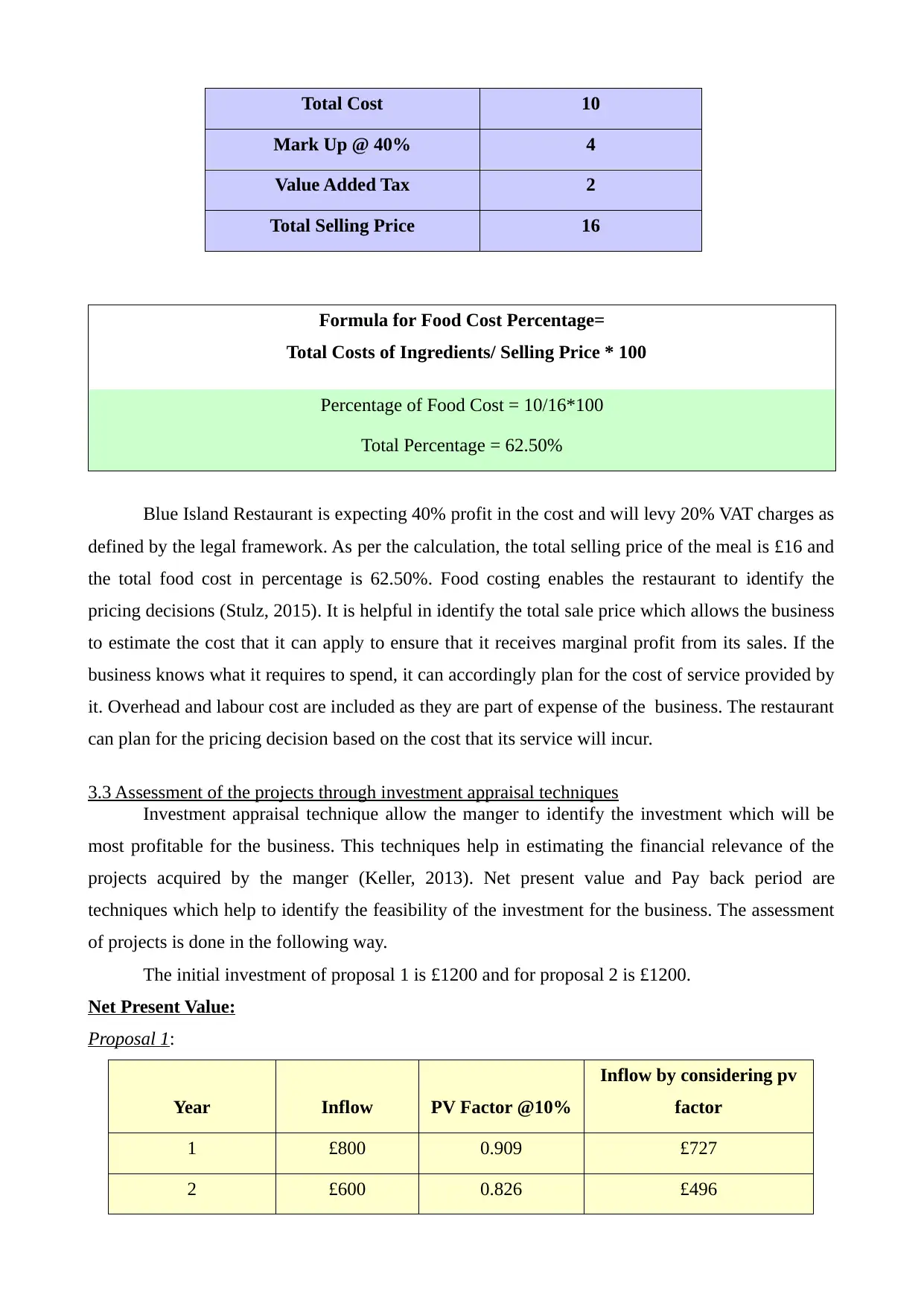

3.3 Assessment of the projects through investment appraisal techniques

Investment appraisal technique allow the manger to identify the investment which will be

most profitable for the business. This techniques help in estimating the financial relevance of the

projects acquired by the manger (Keller, 2013). Net present value and Pay back period are

techniques which help to identify the feasibility of the investment for the business. The assessment

of projects is done in the following way.

The initial investment of proposal 1 is £1200 and for proposal 2 is £1200.

Net Present Value:

Proposal 1:

Year Inflow PV Factor @10%

Inflow by considering pv

factor

1 £800 0.909 £727

2 £600 0.826 £496

Mark Up @ 40% 4

Value Added Tax 2

Total Selling Price 16

Formula for Food Cost Percentage=

Total Costs of Ingredients/ Selling Price * 100

Percentage of Food Cost = 10/16*100

Total Percentage = 62.50%

Blue Island Restaurant is expecting 40% profit in the cost and will levy 20% VAT charges as

defined by the legal framework. As per the calculation, the total selling price of the meal is £16 and

the total food cost in percentage is 62.50%. Food costing enables the restaurant to identify the

pricing decisions (Stulz, 2015). It is helpful in identify the total sale price which allows the business

to estimate the cost that it can apply to ensure that it receives marginal profit from its sales. If the

business knows what it requires to spend, it can accordingly plan for the cost of service provided by

it. Overhead and labour cost are included as they are part of expense of the business. The restaurant

can plan for the pricing decision based on the cost that its service will incur.

3.3 Assessment of the projects through investment appraisal techniques

Investment appraisal technique allow the manger to identify the investment which will be

most profitable for the business. This techniques help in estimating the financial relevance of the

projects acquired by the manger (Keller, 2013). Net present value and Pay back period are

techniques which help to identify the feasibility of the investment for the business. The assessment

of projects is done in the following way.

The initial investment of proposal 1 is £1200 and for proposal 2 is £1200.

Net Present Value:

Proposal 1:

Year Inflow PV Factor @10%

Inflow by considering pv

factor

1 £800 0.909 £727

2 £600 0.826 £496

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

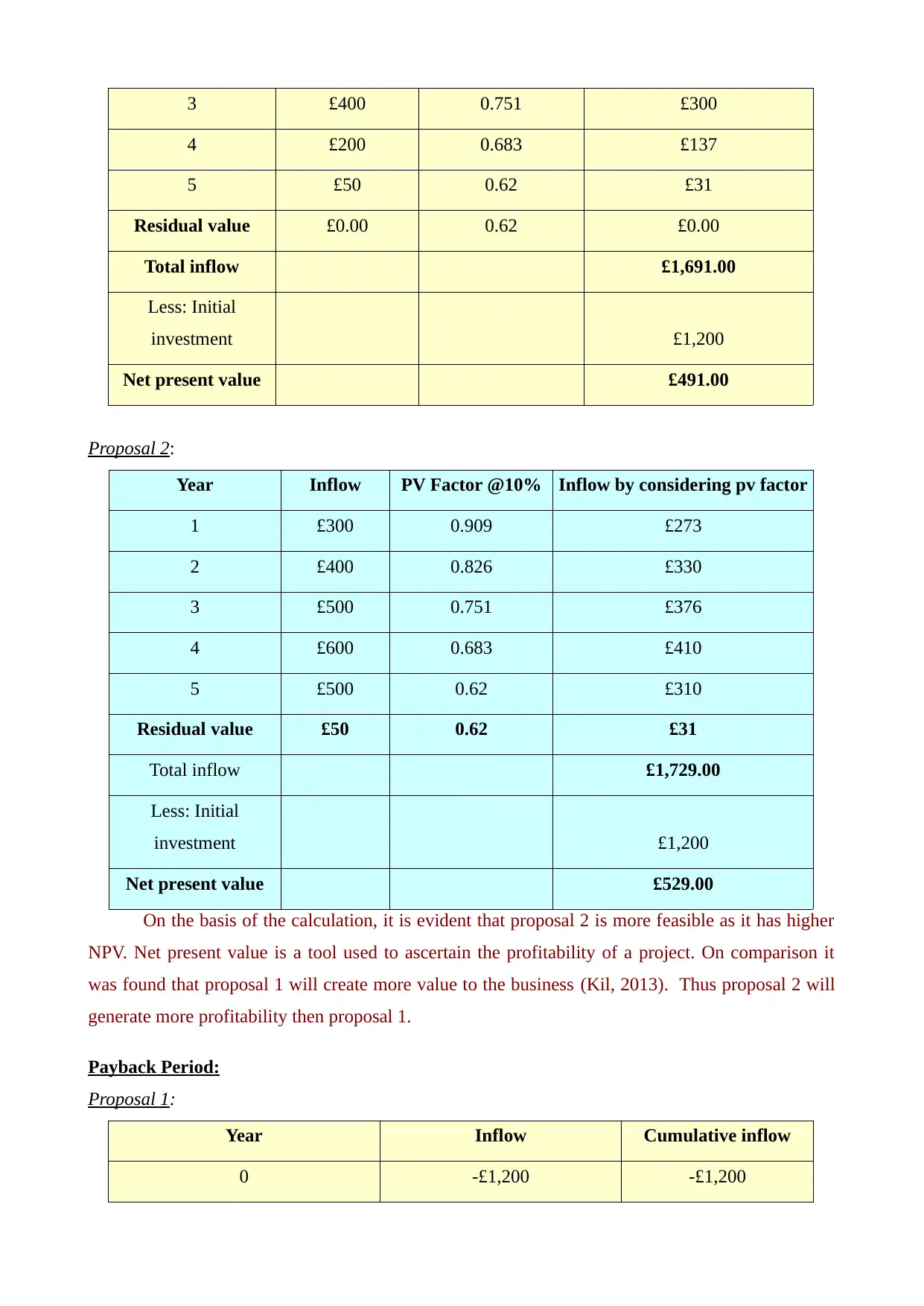

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

On the basis of the calculation, it is evident that proposal 2 is more feasible as it has higher

NPV. Net present value is a tool used to ascertain the profitability of a project. On comparison it

was found that proposal 1 will create more value to the business (Kil, 2013). Thus proposal 2 will

generate more profitability then proposal 1.

Payback Period:

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total inflow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow PV Factor @10% Inflow by considering pv factor

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

4 £600 0.683 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1,729.00

Less: Initial

investment £1,200

Net present value £529.00

On the basis of the calculation, it is evident that proposal 2 is more feasible as it has higher

NPV. Net present value is a tool used to ascertain the profitability of a project. On comparison it

was found that proposal 1 will create more value to the business (Kil, 2013). Thus proposal 2 will

generate more profitability then proposal 1.

Payback Period:

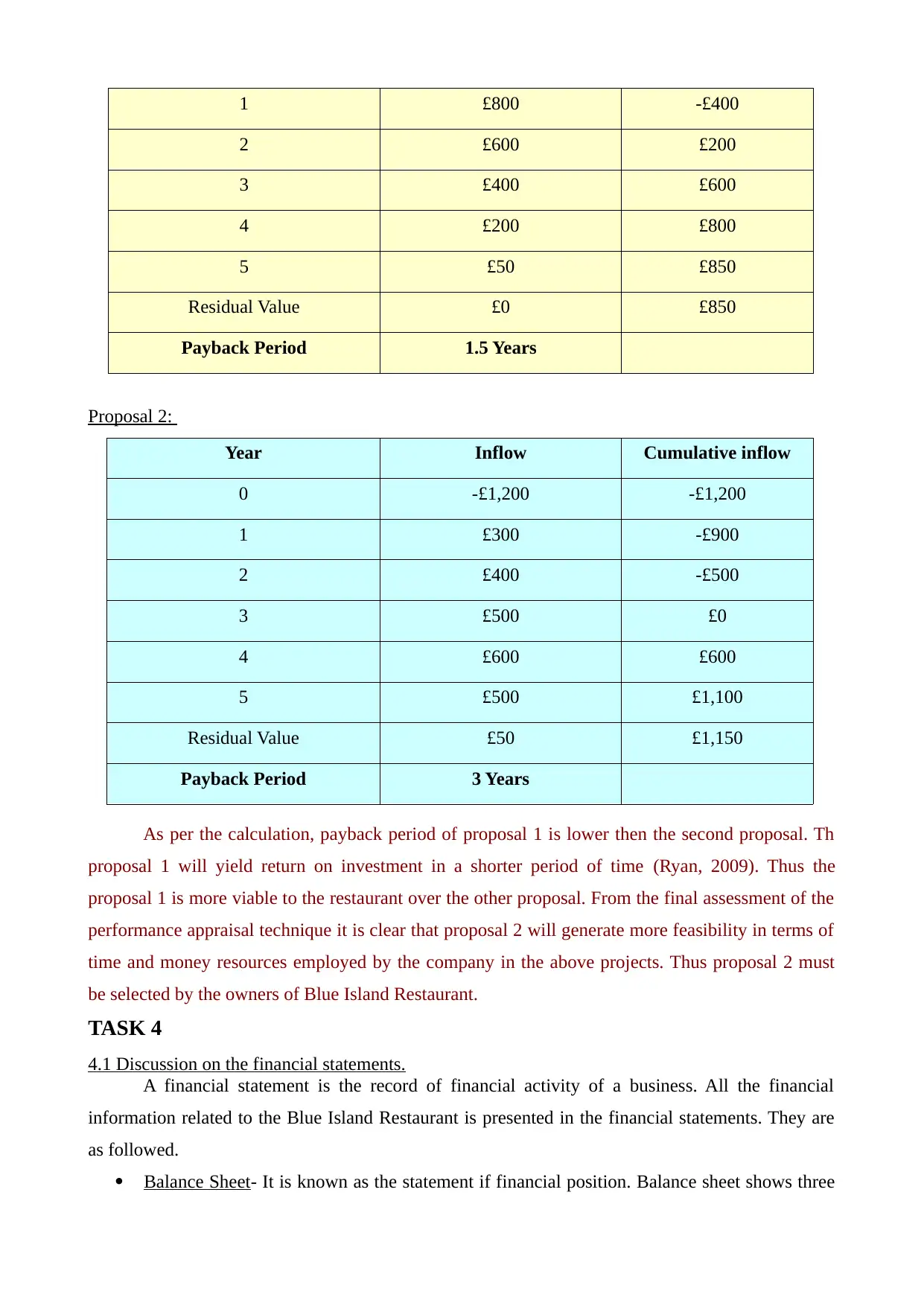

Proposal 1:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

As per the calculation, payback period of proposal 1 is lower then the second proposal. Th

proposal 1 will yield return on investment in a shorter period of time (Ryan, 2009). Thus the

proposal 1 is more viable to the restaurant over the other proposal. From the final assessment of the

performance appraisal technique it is clear that proposal 2 will generate more feasibility in terms of

time and money resources employed by the company in the above projects. Thus proposal 2 must

be selected by the owners of Blue Island Restaurant.

TASK 4

4.1 Discussion on the financial statements.

A financial statement is the record of financial activity of a business. All the financial

information related to the Blue Island Restaurant is presented in the financial statements. They are

as followed.

Balance Sheet- It is known as the statement if financial position. Balance sheet shows three

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

As per the calculation, payback period of proposal 1 is lower then the second proposal. Th

proposal 1 will yield return on investment in a shorter period of time (Ryan, 2009). Thus the

proposal 1 is more viable to the restaurant over the other proposal. From the final assessment of the

performance appraisal technique it is clear that proposal 2 will generate more feasibility in terms of

time and money resources employed by the company in the above projects. Thus proposal 2 must

be selected by the owners of Blue Island Restaurant.

TASK 4

4.1 Discussion on the financial statements.

A financial statement is the record of financial activity of a business. All the financial

information related to the Blue Island Restaurant is presented in the financial statements. They are

as followed.

Balance Sheet- It is known as the statement if financial position. Balance sheet shows three

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.