Business Performance Analysis and Improvement for ZZA Accountancy

VerifiedAdded on 2020/02/14

|30

|6474

|496

Report

AI Summary

This report provides a comprehensive analysis of ZZA Accountancy, a small-sized business facing challenges in profitability and operational efficiency. The report identifies three key issues: the absence of an online presence, long customer waiting times, and outdated software operations. It then delves into investment appraisal techniques, including payback period, net present value (NPV), performance metrics, and SAFE criteria, to evaluate potential solutions. The analysis includes detailed calculations of payback periods and NPV for three proposed projects: developing an online website, hiring two employees, and upgrading software. Performance metrics and SAFE criteria are used to further assess the viability of each option. The report concludes by recommending a draft plan for improvement, addressing project risks, and suggesting modifications to optimize ZZA Accountancy's business performance. The report highlights the need for continuous improvement and strategic changes to enhance the company's competitiveness.

Improving Business Performance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Now a days, each organization places emphasis on framing the operational strategy with the

aim to get the desired outcome or success. By framing the operational strategy business unit is able

to make effective use of the resources to the significant level. For this report ZZA Accountancy is

selected who provides tax refund, self assessment, translation and bankruptcy services to the

customers. ZZA Accountancy is facing 3 problems such as lack of online service, customer waiting

time and software program which may cause of declining the productivity and profitability aspects.

On the basis of investment appraisal techniques it can be summarized that business unit needs to

develop online website which is financially more liable for the project. Further, business unit needs

to undertake continuous improvement and radical change strategy which will help business

enterprise in achieving success in the dynamic business arena.

2

Now a days, each organization places emphasis on framing the operational strategy with the

aim to get the desired outcome or success. By framing the operational strategy business unit is able

to make effective use of the resources to the significant level. For this report ZZA Accountancy is

selected who provides tax refund, self assessment, translation and bankruptcy services to the

customers. ZZA Accountancy is facing 3 problems such as lack of online service, customer waiting

time and software program which may cause of declining the productivity and profitability aspects.

On the basis of investment appraisal techniques it can be summarized that business unit needs to

develop online website which is financially more liable for the project. Further, business unit needs

to undertake continuous improvement and radical change strategy which will help business

enterprise in achieving success in the dynamic business arena.

2

Contents

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

Introduction of the organization.......................................................................................................4

TASK 2.................................................................................................................................................4

Stating the three changes to the operational problem......................................................................4

TASK 3.................................................................................................................................................5

Literature review on the investment appraisal techniques...............................................................5

TASK 4.................................................................................................................................................6

Calculating and evaluating the 3 options ........................................................................................6

TASK 5 ..............................................................................................................................................10

Literature on Radical change (RC) and Continuous improvement (CI)........................................10

TASK 6...............................................................................................................................................11

Evaluating change and using CI or RC approach .........................................................................11

TASK 7...............................................................................................................................................11

Constructing draft plan .................................................................................................................11

TASK 8...............................................................................................................................................12

Literature on project risk and identifying the risk factors ............................................................12

TASK 9...............................................................................................................................................12

Evaluating the draft project............................................................................................................12

TASK 10.............................................................................................................................................12

Modified draft plan .......................................................................................................................12

............................................................................................................................................................18

............................................................................................................................................................19

appendix ............................................................................................................................................19

References..........................................................................................................................................20

3

INTRODUCTION ...............................................................................................................................4

TASK 1.................................................................................................................................................4

Introduction of the organization.......................................................................................................4

TASK 2.................................................................................................................................................4

Stating the three changes to the operational problem......................................................................4

TASK 3.................................................................................................................................................5

Literature review on the investment appraisal techniques...............................................................5

TASK 4.................................................................................................................................................6

Calculating and evaluating the 3 options ........................................................................................6

TASK 5 ..............................................................................................................................................10

Literature on Radical change (RC) and Continuous improvement (CI)........................................10

TASK 6...............................................................................................................................................11

Evaluating change and using CI or RC approach .........................................................................11

TASK 7...............................................................................................................................................11

Constructing draft plan .................................................................................................................11

TASK 8...............................................................................................................................................12

Literature on project risk and identifying the risk factors ............................................................12

TASK 9...............................................................................................................................................12

Evaluating the draft project............................................................................................................12

TASK 10.............................................................................................................................................12

Modified draft plan .......................................................................................................................12

............................................................................................................................................................18

............................................................................................................................................................19

appendix ............................................................................................................................................19

References..........................................................................................................................................20

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Business organization makes use of operational strategy which helps them in getting the

desired outcome or success. Operational strategy defines the ways in which company will employ

and make use of the resources for producing the product or services (Understanding operations

management, 2016). In the present era, business enterprise frames operational strategy which helps

them in making optimum use of resources, personnel and work process. Thus, by preparing suitable

operational strategy which supports the corporate aspects business unit is able to make

improvement in their business performance to the large extent. Moreover, this strategy provides

deeper insight about the areas which company need to improve. Thus, by identifying this aspect

corporation is able to achieve success in the strategic business arena. For this project report report,

ZZA Accountancy is selected as an organization.

TASK 1

Introduction of the organization

ZZA Accountancy is the small sized business organization which established in 2009. It is

self employed firm who serve approximately 200 customers. This accountancy firm offers wide

range of services to the customers who include self assessment, tax refund, divorces, benefits,

translation and bankruptcy etc. The profitability aspect of the company is constant because gross

margin of the accountancy firm is not increasing with the very high pace. Besides this, the process

which is followed by ZZA Accountancy is highly stable.

TASK 2

Stating the three changes to the operational problem

ZZA Accountancy offers variety of services to their customers but still profitability aspect of

the business unit is not very high. It indicates that company needs to make changes in its operation

strategies and other aspects. Thus, by conducting investigation Accountancy firm has identified

there are mainly three problems which might cause of sloe growth in profitability aspect are

enumerated below:

Online website: From investigation it has been identifying that ZZA Accountancy needs to

develop its online website. Moreover, due to the absence online services customers cannot

contact with the business unit through the means of internet. Besides this, customers are not

able to get information or service through online. This aspect closely affects the convenience

of the customers to the large extent. Now, each person has smart and they make use of

internet. Hence, customers prefer to make use of the services of firm who offers high level

4

Business organization makes use of operational strategy which helps them in getting the

desired outcome or success. Operational strategy defines the ways in which company will employ

and make use of the resources for producing the product or services (Understanding operations

management, 2016). In the present era, business enterprise frames operational strategy which helps

them in making optimum use of resources, personnel and work process. Thus, by preparing suitable

operational strategy which supports the corporate aspects business unit is able to make

improvement in their business performance to the large extent. Moreover, this strategy provides

deeper insight about the areas which company need to improve. Thus, by identifying this aspect

corporation is able to achieve success in the strategic business arena. For this project report report,

ZZA Accountancy is selected as an organization.

TASK 1

Introduction of the organization

ZZA Accountancy is the small sized business organization which established in 2009. It is

self employed firm who serve approximately 200 customers. This accountancy firm offers wide

range of services to the customers who include self assessment, tax refund, divorces, benefits,

translation and bankruptcy etc. The profitability aspect of the company is constant because gross

margin of the accountancy firm is not increasing with the very high pace. Besides this, the process

which is followed by ZZA Accountancy is highly stable.

TASK 2

Stating the three changes to the operational problem

ZZA Accountancy offers variety of services to their customers but still profitability aspect of

the business unit is not very high. It indicates that company needs to make changes in its operation

strategies and other aspects. Thus, by conducting investigation Accountancy firm has identified

there are mainly three problems which might cause of sloe growth in profitability aspect are

enumerated below:

Online website: From investigation it has been identifying that ZZA Accountancy needs to

develop its online website. Moreover, due to the absence online services customers cannot

contact with the business unit through the means of internet. Besides this, customers are not

able to get information or service through online. This aspect closely affects the convenience

of the customers to the large extent. Now, each person has smart and they make use of

internet. Hence, customers prefer to make use of the services of firm who offers high level

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of convenience to them (Ramani, 2016). In order to overcome this problem company needs

to develop effective and attractive website. Through this, Accountancy firm is able to make

interaction with the large number of customers. It also offers opportunity to the business unit

to serve the large number of customers. Thus, this strategy will provide assistance to the

firm in enhancing their productivity and profitability.

Company is required to hire 2 employees: The problem which is facing by the accountancy

firm is the more waiting time of the staff. In the present time, customers do not want to wait

for the long time. High waiting time is one the main factors which closely affect his

satisfaction level of customers and hereby negatively hamper the gross margin of the firm.

ZZA accountancy is facing this problem because they have very short staff as only one

people who offers the services to the customers. Hence, business unit needs to employ two

employees which enable them to quick or faster services to the customers. It also enables

firm to serve more customers at one time. Hence, by offering the faster services small sized

business unit is able evolve satisfaction among the customers which may turn into loyalty in

the near future. Further, when company serves more customers then it may also result into

high profitability.

Software operations: ZZA Accountancy also needs to employ latest software which helps

them in resolving the problems or issue within the suitable time frame. Moreover, when

business unit takes longer time to resolve the issues then it closely influence the satisfaction

of the customers. Word of mouth publicity of the firm is also affected when company makes

fails to offer suitable solution within the suitable timer frame. Thus, by offering the solution

more quickly Accountancy firm is able to attract the large number of customers. It enables

firm to maximize their sales and profitability aspects.

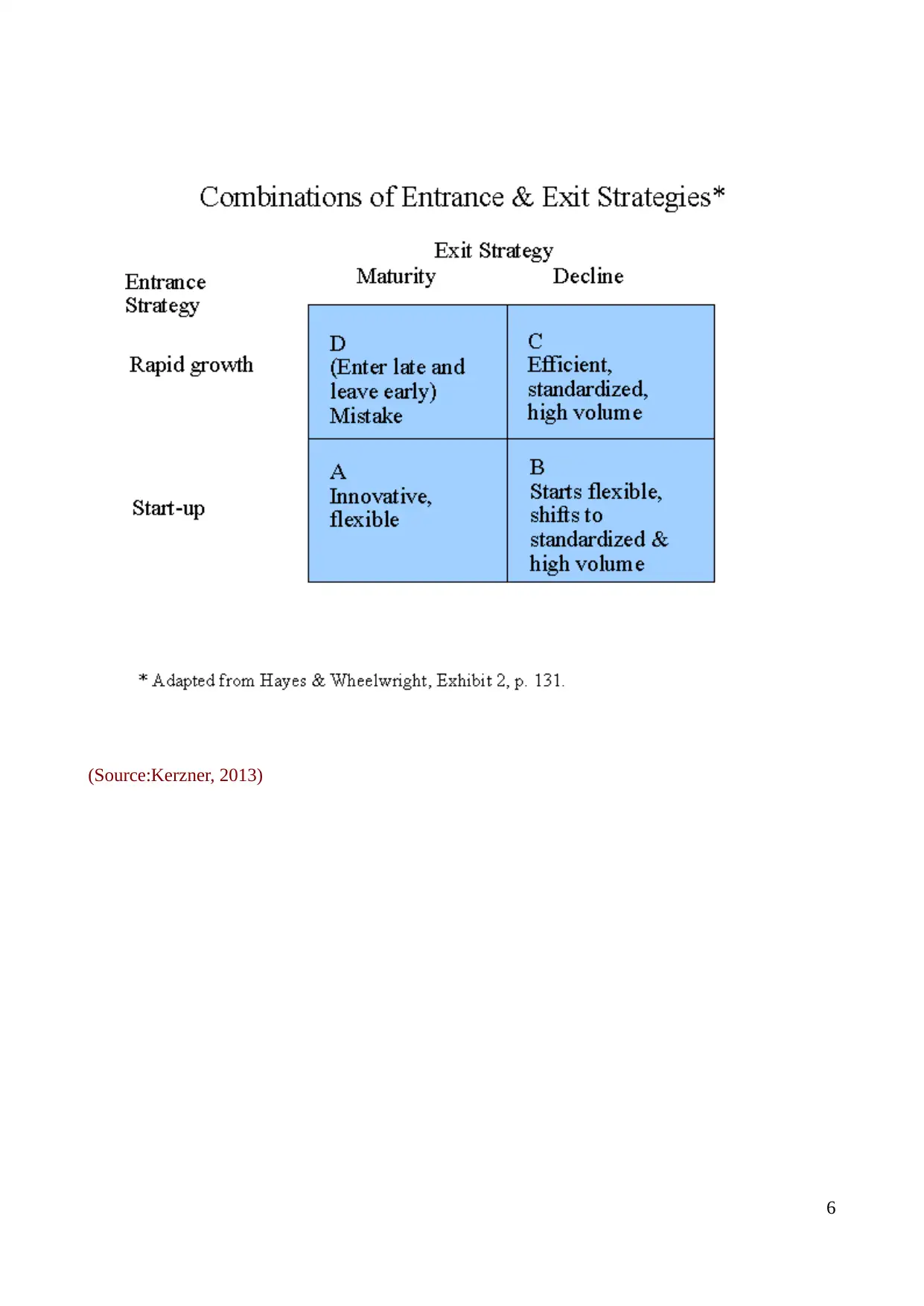

According to the Hayes & Wheelwright model ZZA accountancy lies in the maturity phase.

Moreover, in this company needs to make changes in their operational strategy which helps them in

attaining competitive edge over others. Through this, business unit is able to convert maturity phase

into the rapid growth.

5

to develop effective and attractive website. Through this, Accountancy firm is able to make

interaction with the large number of customers. It also offers opportunity to the business unit

to serve the large number of customers. Thus, this strategy will provide assistance to the

firm in enhancing their productivity and profitability.

Company is required to hire 2 employees: The problem which is facing by the accountancy

firm is the more waiting time of the staff. In the present time, customers do not want to wait

for the long time. High waiting time is one the main factors which closely affect his

satisfaction level of customers and hereby negatively hamper the gross margin of the firm.

ZZA accountancy is facing this problem because they have very short staff as only one

people who offers the services to the customers. Hence, business unit needs to employ two

employees which enable them to quick or faster services to the customers. It also enables

firm to serve more customers at one time. Hence, by offering the faster services small sized

business unit is able evolve satisfaction among the customers which may turn into loyalty in

the near future. Further, when company serves more customers then it may also result into

high profitability.

Software operations: ZZA Accountancy also needs to employ latest software which helps

them in resolving the problems or issue within the suitable time frame. Moreover, when

business unit takes longer time to resolve the issues then it closely influence the satisfaction

of the customers. Word of mouth publicity of the firm is also affected when company makes

fails to offer suitable solution within the suitable timer frame. Thus, by offering the solution

more quickly Accountancy firm is able to attract the large number of customers. It enables

firm to maximize their sales and profitability aspects.

According to the Hayes & Wheelwright model ZZA accountancy lies in the maturity phase.

Moreover, in this company needs to make changes in their operational strategy which helps them in

attaining competitive edge over others. Through this, business unit is able to convert maturity phase

into the rapid growth.

5

(Source:Kerzner, 2013)

6

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

Literature review on the investment appraisal techniques

Business organization can evaluate the viability or suitability of change by employing

different investment appraisal methods are as under:

Investment appraisal methods

Pay back period: According to the view points of Hoerl and Snee (2012) payback period

method of capital budgeting provides deeper insight about the time frame within which

business unit is get back the initial investment. Easy to calculate is one the main attributes of

this method which encourage manager to make use of this method. Besides this, it helps

company in identifying the time after which they are able to make profit. However, it is to

be critically evaluated by Molnau (2014) that it only entails the time period within which

company is able get initial investment. Nevertheless, it does not provide information about

the cash flow which is generated by the firm during the suitable time frame. Besides this, it

does not undertake time value of money concept which also limits the significance of this

method.

Net present value: Ramani (2016) said that net present value method offers highly realistic

outcome because it considers time value of money concept. This method of investment

appraisal serves information about the return which business unit will get after the

predetermined time frame. However, Baum and Crosby (2014) argued that it is highly

difficult for the investment manager to undertake suitable discounting factor for the

computation. If manager fails to employ suitable factor then this method will offer highly

biased results.

Performance matrix: As per the view points of Upton, J. and et.al., performance matrix helps

organization in evaluating the performance and activities of project. This metrics helps in

supporting the needs of the wide range of stakeholders from customers, investors or

shareholders to employees. Safety, time, cost, resources, scope, actions and quality are the

seven parameters which assists in evaluating the project to the significant level. This

statement has been contradicted by Stevanović and Pucar (2012) that these parameters

which are undertaken by the experts have less value or importance as compared to the

mathematical tools or techniques.

SAFE criteria: In accordance with the view points of Dyson and Berry (2014) Safe criteria is

7

Literature review on the investment appraisal techniques

Business organization can evaluate the viability or suitability of change by employing

different investment appraisal methods are as under:

Investment appraisal methods

Pay back period: According to the view points of Hoerl and Snee (2012) payback period

method of capital budgeting provides deeper insight about the time frame within which

business unit is get back the initial investment. Easy to calculate is one the main attributes of

this method which encourage manager to make use of this method. Besides this, it helps

company in identifying the time after which they are able to make profit. However, it is to

be critically evaluated by Molnau (2014) that it only entails the time period within which

company is able get initial investment. Nevertheless, it does not provide information about

the cash flow which is generated by the firm during the suitable time frame. Besides this, it

does not undertake time value of money concept which also limits the significance of this

method.

Net present value: Ramani (2016) said that net present value method offers highly realistic

outcome because it considers time value of money concept. This method of investment

appraisal serves information about the return which business unit will get after the

predetermined time frame. However, Baum and Crosby (2014) argued that it is highly

difficult for the investment manager to undertake suitable discounting factor for the

computation. If manager fails to employ suitable factor then this method will offer highly

biased results.

Performance matrix: As per the view points of Upton, J. and et.al., performance matrix helps

organization in evaluating the performance and activities of project. This metrics helps in

supporting the needs of the wide range of stakeholders from customers, investors or

shareholders to employees. Safety, time, cost, resources, scope, actions and quality are the

seven parameters which assists in evaluating the project to the significant level. This

statement has been contradicted by Stevanović and Pucar (2012) that these parameters

which are undertaken by the experts have less value or importance as compared to the

mathematical tools or techniques.

SAFE criteria: In accordance with the view points of Dyson and Berry (2014) Safe criteria is

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

usually employed by the firm with the aim to evaluate the feasibility, suitability and

acceptability of the project. By taking into account this criteria business unit is able to

assess the risks which are associated with the particular project. Besides this, it also provides

information about the performance of particular project or option.

TASK 4

Calculating and evaluating the 3 options

Investment appraisal techniques are adopted by the business unit for assessing the viability

or profitability of project. Payback, net present value as well as ARR is the most effectual tool

which helps manager in making most suitable and effective decision making. Net present value

undertakes time value of money concept. Thus, if assists ZZA accountant in making most viable

decision.

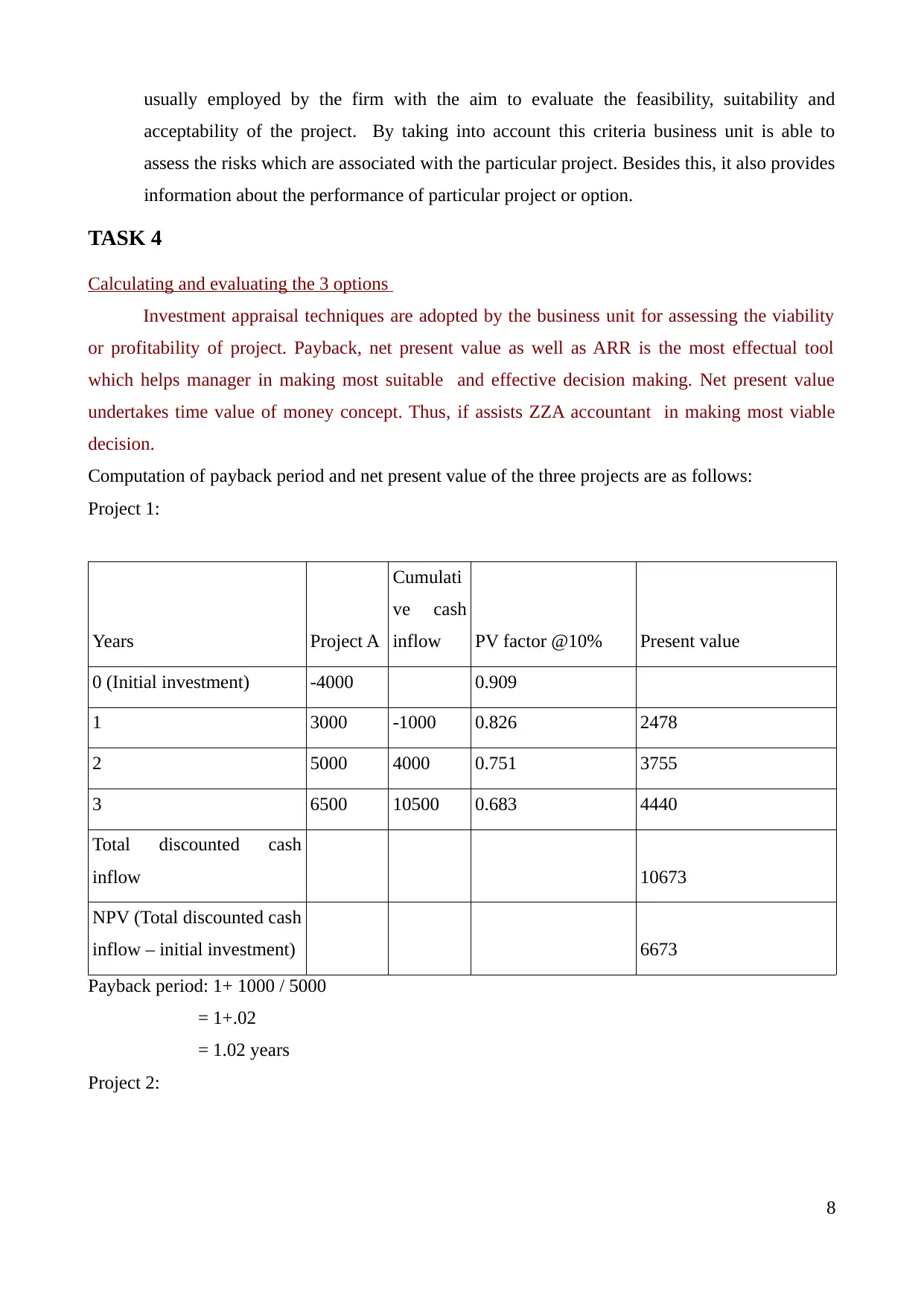

Computation of payback period and net present value of the three projects are as follows:

Project 1:

Years Project A

Cumulati

ve cash

inflow PV factor @10% Present value

0 (Initial investment) -4000 0.909

1 3000 -1000 0.826 2478

2 5000 4000 0.751 3755

3 6500 10500 0.683 4440

Total discounted cash

inflow 10673

NPV (Total discounted cash

inflow – initial investment) 6673

Payback period: 1+ 1000 / 5000

= 1+.02

= 1.02 years

Project 2:

8

acceptability of the project. By taking into account this criteria business unit is able to

assess the risks which are associated with the particular project. Besides this, it also provides

information about the performance of particular project or option.

TASK 4

Calculating and evaluating the 3 options

Investment appraisal techniques are adopted by the business unit for assessing the viability

or profitability of project. Payback, net present value as well as ARR is the most effectual tool

which helps manager in making most suitable and effective decision making. Net present value

undertakes time value of money concept. Thus, if assists ZZA accountant in making most viable

decision.

Computation of payback period and net present value of the three projects are as follows:

Project 1:

Years Project A

Cumulati

ve cash

inflow PV factor @10% Present value

0 (Initial investment) -4000 0.909

1 3000 -1000 0.826 2478

2 5000 4000 0.751 3755

3 6500 10500 0.683 4440

Total discounted cash

inflow 10673

NPV (Total discounted cash

inflow – initial investment) 6673

Payback period: 1+ 1000 / 5000

= 1+.02

= 1.02 years

Project 2:

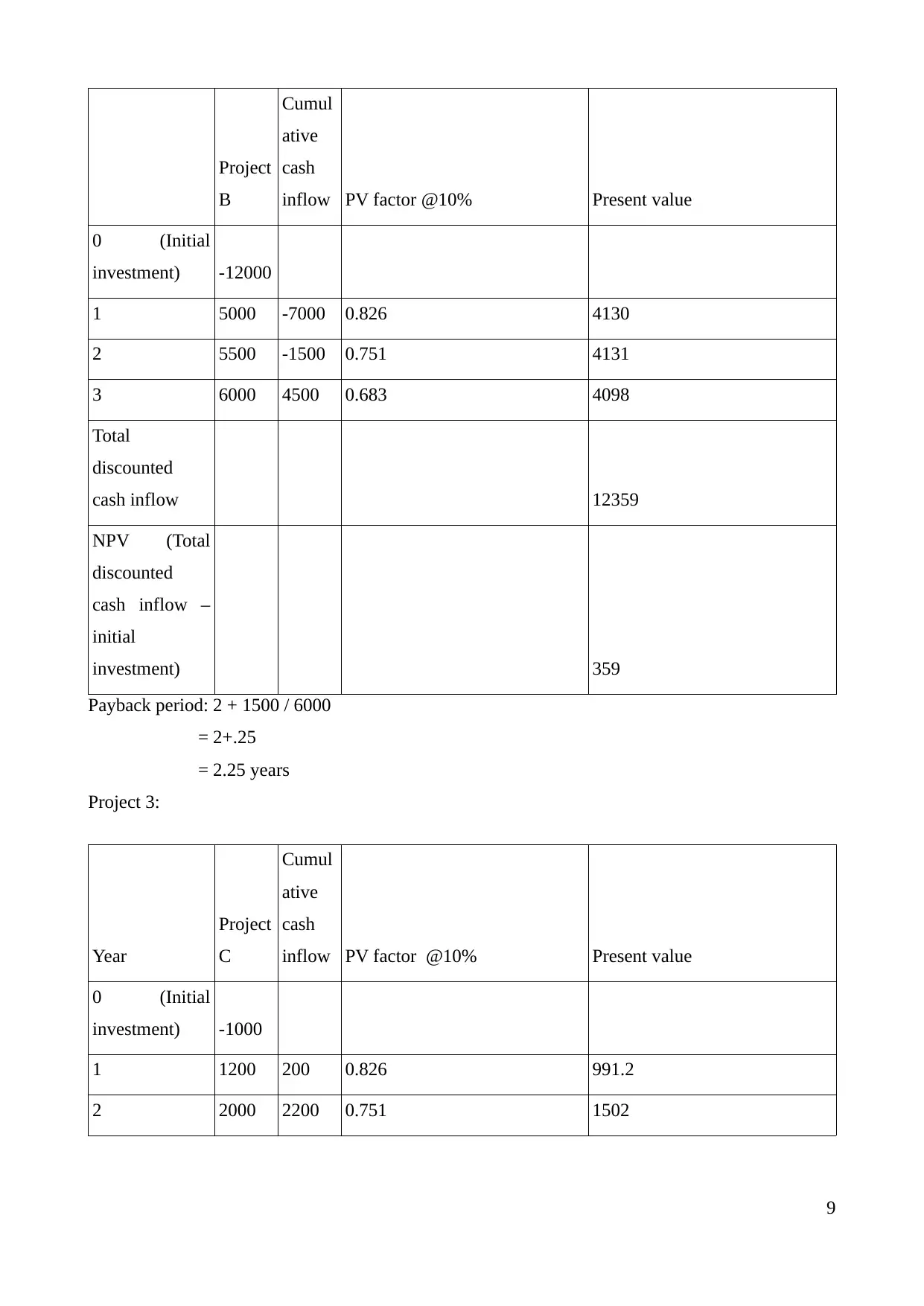

8

Project

B

Cumul

ative

cash

inflow PV factor @10% Present value

0 (Initial

investment) -12000

1 5000 -7000 0.826 4130

2 5500 -1500 0.751 4131

3 6000 4500 0.683 4098

Total

discounted

cash inflow 12359

NPV (Total

discounted

cash inflow –

initial

investment) 359

Payback period: 2 + 1500 / 6000

= 2+.25

= 2.25 years

Project 3:

Year

Project

C

Cumul

ative

cash

inflow PV factor @10% Present value

0 (Initial

investment) -1000

1 1200 200 0.826 991.2

2 2000 2200 0.751 1502

9

B

Cumul

ative

cash

inflow PV factor @10% Present value

0 (Initial

investment) -12000

1 5000 -7000 0.826 4130

2 5500 -1500 0.751 4131

3 6000 4500 0.683 4098

Total

discounted

cash inflow 12359

NPV (Total

discounted

cash inflow –

initial

investment) 359

Payback period: 2 + 1500 / 6000

= 2+.25

= 2.25 years

Project 3:

Year

Project

C

Cumul

ative

cash

inflow PV factor @10% Present value

0 (Initial

investment) -1000

1 1200 200 0.826 991.2

2 2000 2200 0.751 1502

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

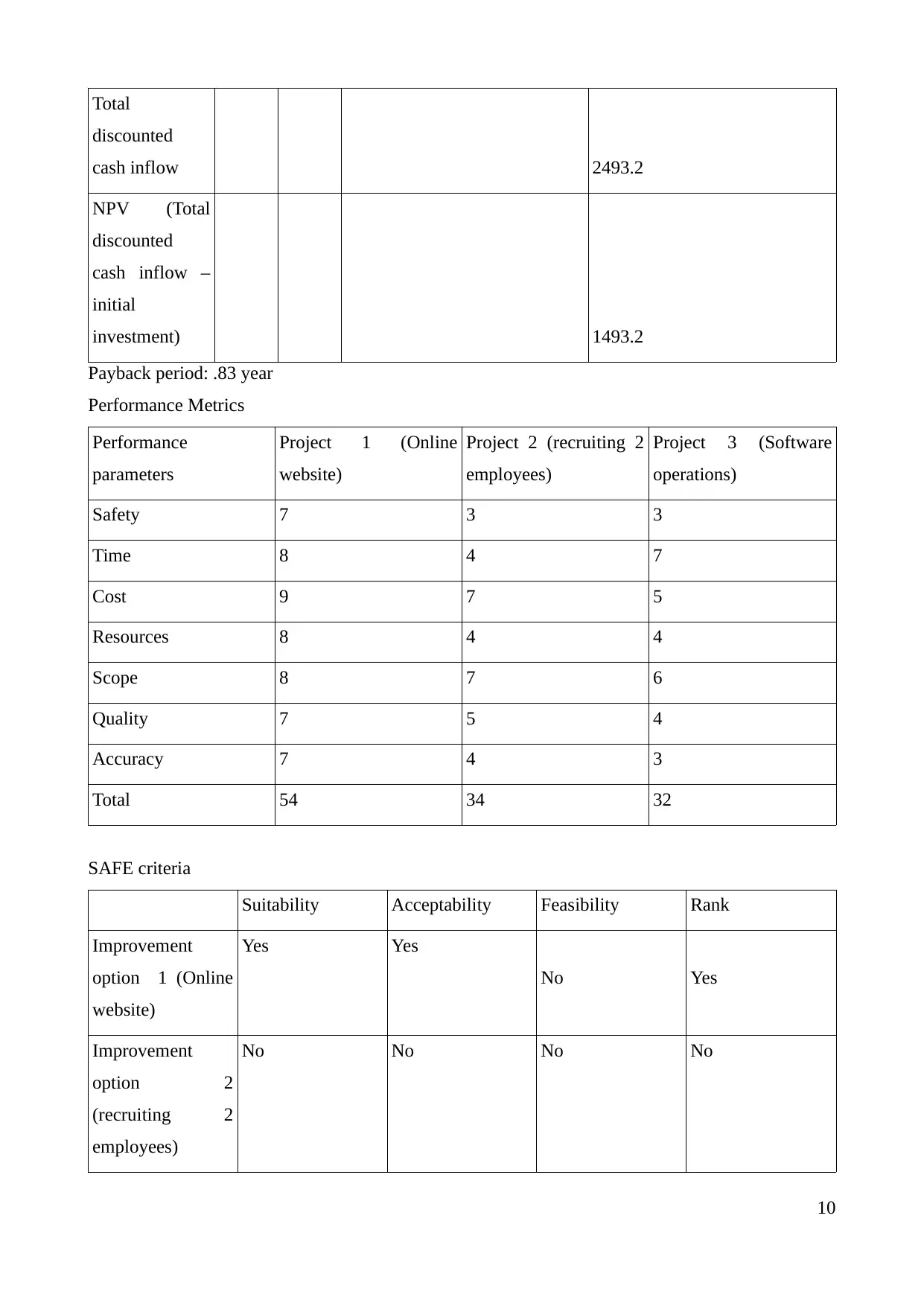

Total

discounted

cash inflow 2493.2

NPV (Total

discounted

cash inflow –

initial

investment) 1493.2

Payback period: .83 year

Performance Metrics

Performance

parameters

Project 1 (Online

website)

Project 2 (recruiting 2

employees)

Project 3 (Software

operations)

Safety 7 3 3

Time 8 4 7

Cost 9 7 5

Resources 8 4 4

Scope 8 7 6

Quality 7 5 4

Accuracy 7 4 3

Total 54 34 32

SAFE criteria

Suitability Acceptability Feasibility Rank

Improvement

option 1 (Online

website)

Yes Yes

No Yes

Improvement

option 2

(recruiting 2

employees)

No No No No

10

discounted

cash inflow 2493.2

NPV (Total

discounted

cash inflow –

initial

investment) 1493.2

Payback period: .83 year

Performance Metrics

Performance

parameters

Project 1 (Online

website)

Project 2 (recruiting 2

employees)

Project 3 (Software

operations)

Safety 7 3 3

Time 8 4 7

Cost 9 7 5

Resources 8 4 4

Scope 8 7 6

Quality 7 5 4

Accuracy 7 4 3

Total 54 34 32

SAFE criteria

Suitability Acceptability Feasibility Rank

Improvement

option 1 (Online

website)

Yes Yes

No Yes

Improvement

option 2

(recruiting 2

employees)

No No No No

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

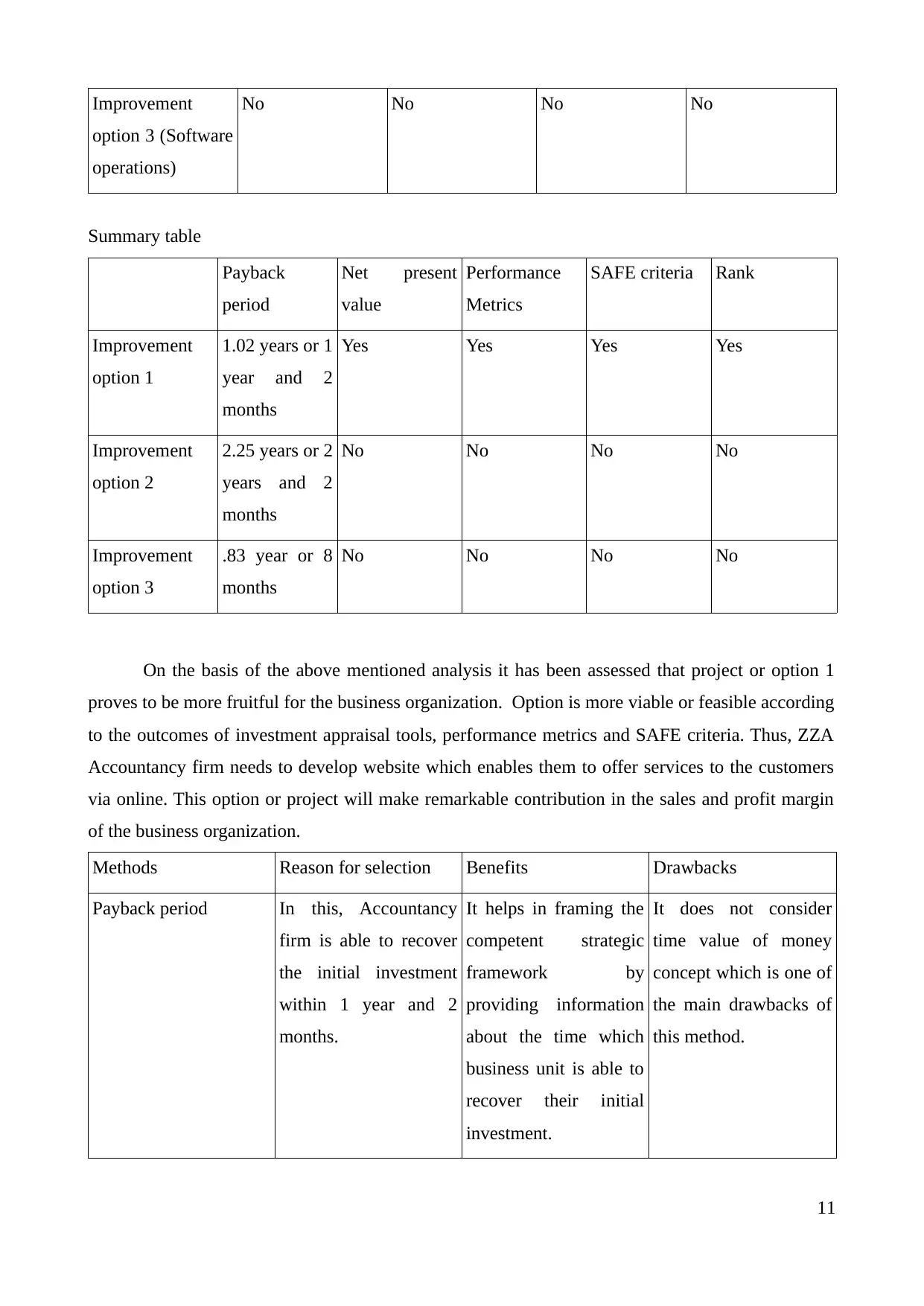

Improvement

option 3 (Software

operations)

No No No No

Summary table

Payback

period

Net present

value

Performance

Metrics

SAFE criteria Rank

Improvement

option 1

1.02 years or 1

year and 2

months

Yes Yes Yes Yes

Improvement

option 2

2.25 years or 2

years and 2

months

No No No No

Improvement

option 3

.83 year or 8

months

No No No No

On the basis of the above mentioned analysis it has been assessed that project or option 1

proves to be more fruitful for the business organization. Option is more viable or feasible according

to the outcomes of investment appraisal tools, performance metrics and SAFE criteria. Thus, ZZA

Accountancy firm needs to develop website which enables them to offer services to the customers

via online. This option or project will make remarkable contribution in the sales and profit margin

of the business organization.

Methods Reason for selection Benefits Drawbacks

Payback period In this, Accountancy

firm is able to recover

the initial investment

within 1 year and 2

months.

It helps in framing the

competent strategic

framework by

providing information

about the time which

business unit is able to

recover their initial

investment.

It does not consider

time value of money

concept which is one of

the main drawbacks of

this method.

11

option 3 (Software

operations)

No No No No

Summary table

Payback

period

Net present

value

Performance

Metrics

SAFE criteria Rank

Improvement

option 1

1.02 years or 1

year and 2

months

Yes Yes Yes Yes

Improvement

option 2

2.25 years or 2

years and 2

months

No No No No

Improvement

option 3

.83 year or 8

months

No No No No

On the basis of the above mentioned analysis it has been assessed that project or option 1

proves to be more fruitful for the business organization. Option is more viable or feasible according

to the outcomes of investment appraisal tools, performance metrics and SAFE criteria. Thus, ZZA

Accountancy firm needs to develop website which enables them to offer services to the customers

via online. This option or project will make remarkable contribution in the sales and profit margin

of the business organization.

Methods Reason for selection Benefits Drawbacks

Payback period In this, Accountancy

firm is able to recover

the initial investment

within 1 year and 2

months.

It helps in framing the

competent strategic

framework by

providing information

about the time which

business unit is able to

recover their initial

investment.

It does not consider

time value of money

concept which is one of

the main drawbacks of

this method.

11

Net present value

(NPV)

NEPV of option A is

higher as compared to

the rest of options

available.

This methods offer

highly suitable results

by taking into account

the time value of

money concept.

This method does not

make any

differentiation between

the proposals which are

available to the

business unit.

Performance Metrics Project will offer high

level of support to the

business enterprises.

It offers different

framework which helps

in evaluating the

project in an effectual

manner.

This metrics only place

emphasis on

performance rather than

other aspects.

SAFE criteria This project is safe

because it has lower

level of risk.

This criteria helps in

assessing the

suitability, acceptability

and feasibility of the

project in an effective

manner.

It makes analysis of

particular option which

limits the significance

of this method.

TASK 5

Literature on Radical change (RC) and Continuous improvement (CI)

Continuous improvement: According to the view point of Kerzner (2013) continuous improvement

is the ongoing process in which business unit continuously makes effort to improve the product or

services which are offered by them. Usually, business organization continuously examines their

process and activities with the aim to identify and eliminate the problems. Through this, company

can easily identify and grab the opportunities which are available at marketplace. In addition to

this, it also helps business enterprise in framing the cost effectual strategies and policies which

make contribution in the attainment of organizational goals and objectives. However, it is to be

critically evaluated by Burke (2013) that for making continuous improvement company has to incur

huge expenses which impose high level of cost in front of it. Thus, it is not an going process,

business organization undertakes it on a periodical basis.

Radical change: As per the view points of Walker (2015) in radical change employees of the

business organization react in different manner towards the changing methods or approaches. In

12

(NPV)

NEPV of option A is

higher as compared to

the rest of options

available.

This methods offer

highly suitable results

by taking into account

the time value of

money concept.

This method does not

make any

differentiation between

the proposals which are

available to the

business unit.

Performance Metrics Project will offer high

level of support to the

business enterprises.

It offers different

framework which helps

in evaluating the

project in an effectual

manner.

This metrics only place

emphasis on

performance rather than

other aspects.

SAFE criteria This project is safe

because it has lower

level of risk.

This criteria helps in

assessing the

suitability, acceptability

and feasibility of the

project in an effective

manner.

It makes analysis of

particular option which

limits the significance

of this method.

TASK 5

Literature on Radical change (RC) and Continuous improvement (CI)

Continuous improvement: According to the view point of Kerzner (2013) continuous improvement

is the ongoing process in which business unit continuously makes effort to improve the product or

services which are offered by them. Usually, business organization continuously examines their

process and activities with the aim to identify and eliminate the problems. Through this, company

can easily identify and grab the opportunities which are available at marketplace. In addition to

this, it also helps business enterprise in framing the cost effectual strategies and policies which

make contribution in the attainment of organizational goals and objectives. However, it is to be

critically evaluated by Burke (2013) that for making continuous improvement company has to incur

huge expenses which impose high level of cost in front of it. Thus, it is not an going process,

business organization undertakes it on a periodical basis.

Radical change: As per the view points of Walker (2015) in radical change employees of the

business organization react in different manner towards the changing methods or approaches. In

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.