BUL Financial Statements: Revaluation Model Analysis & AASB 110 Memo

VerifiedAdded on 2023/06/10

|10

|1617

|103

Report

AI Summary

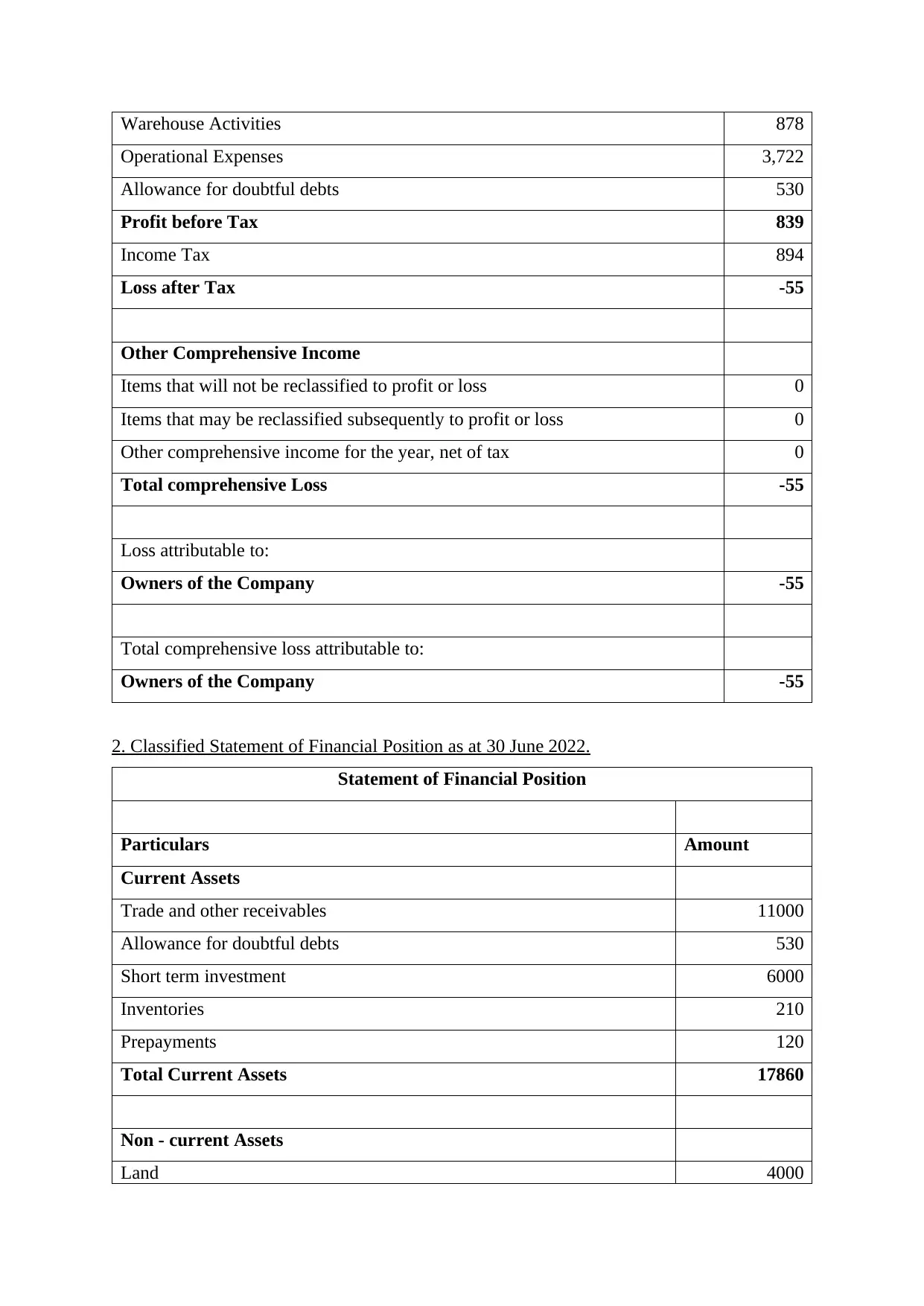

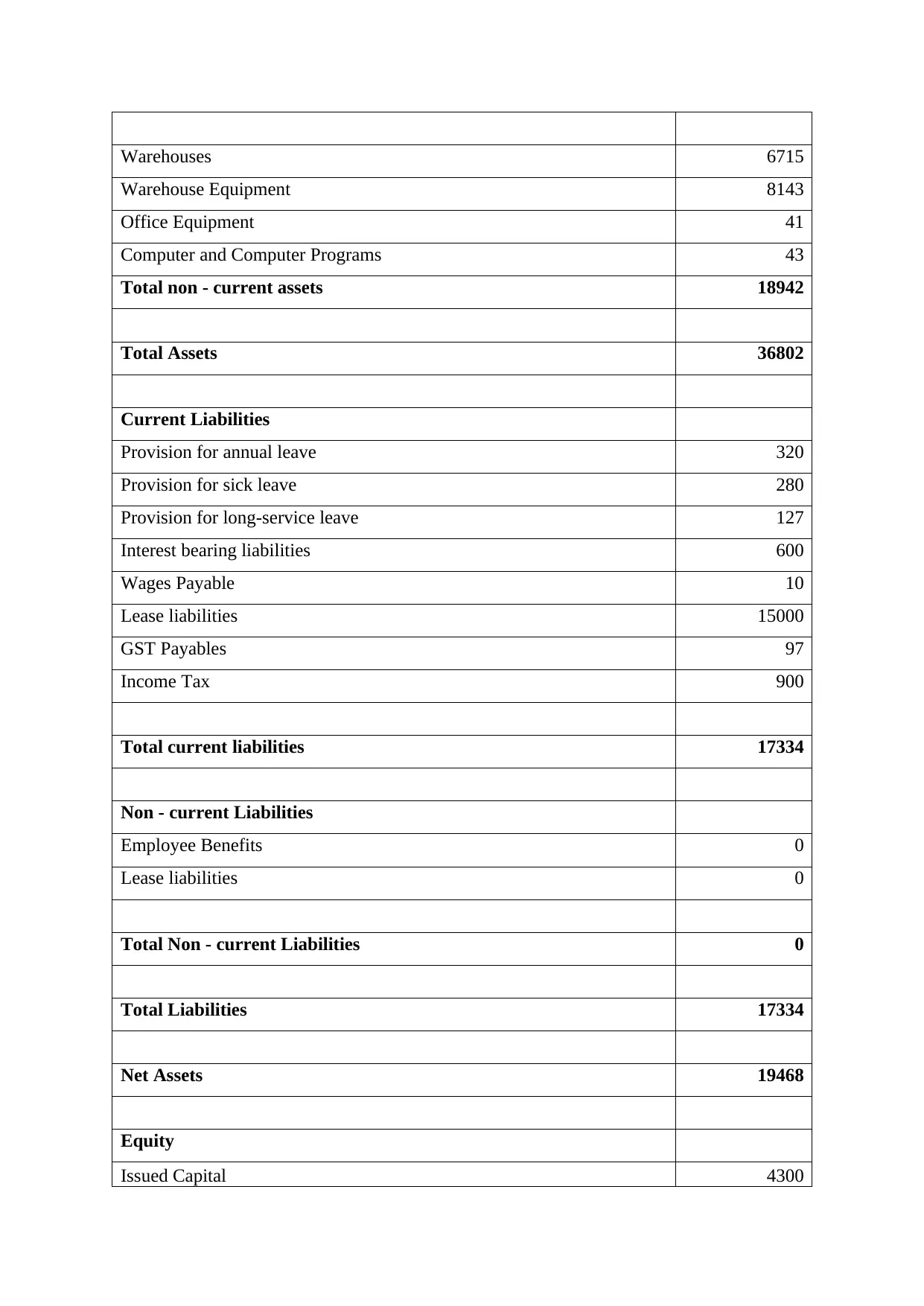

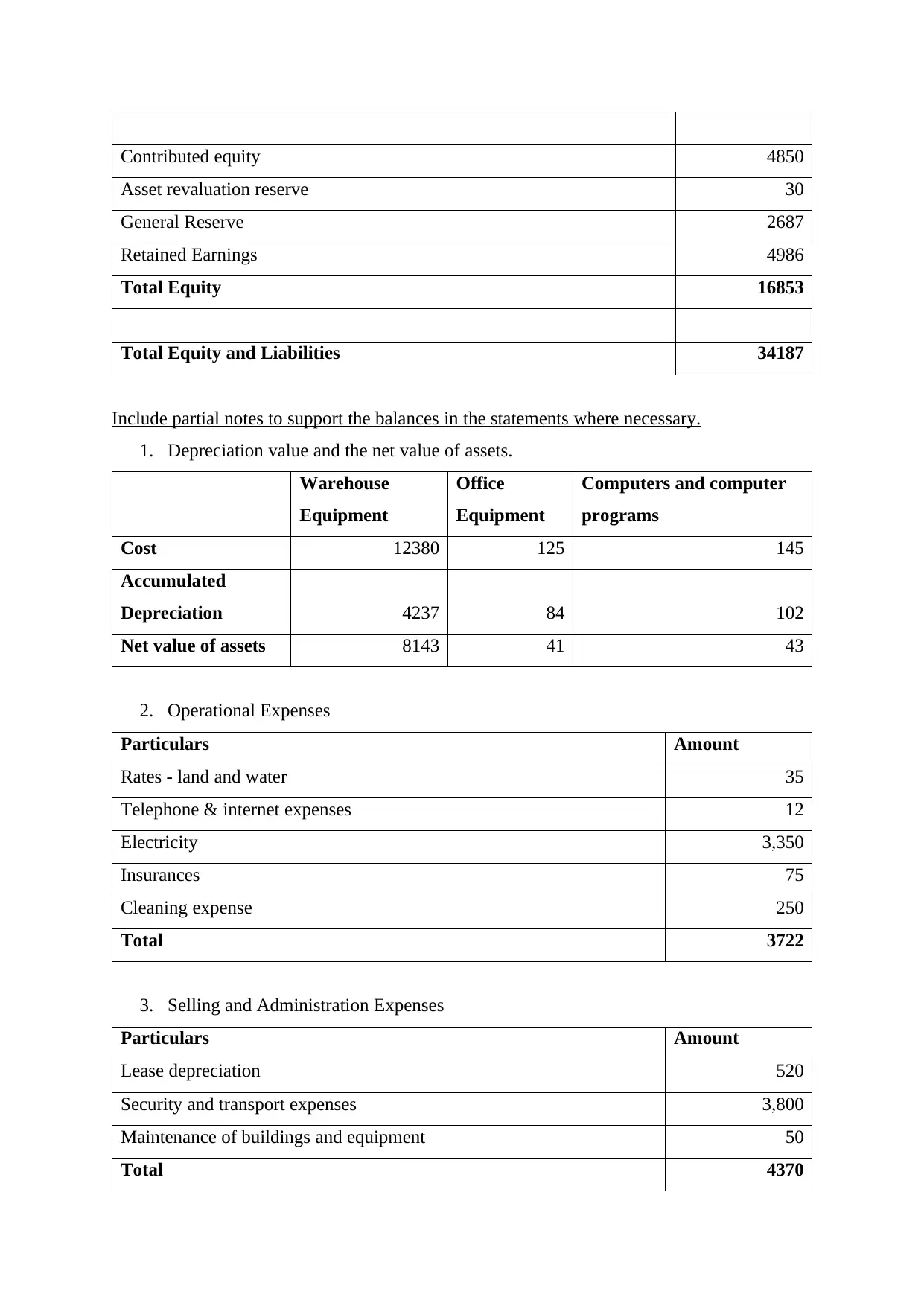

This report provides a comprehensive analysis of financial statements, focusing on the revaluation model and compliance with AASB standards. It includes an internal memo addressing the Chairperson on relevant aspects of the revaluation model, along with prepared financial statements for Business as Usual Limited (BUL), including the Statement of Profit or Loss and Other Comprehensive Income and the Statement of Financial Position. Partial notes support the balances in the statements. Additionally, an internal memo for the CEO and board of directors discusses adjusting and non-adjusting events as per AASB 110. The report concludes by emphasizing the importance of adhering to accounting standards and making appropriate adjustments after the reporting period.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.