Financial Analysis of Wesfarmers (Coles): WACC and Capital Structure

VerifiedAdded on 2023/04/23

|10

|2235

|72

Report

AI Summary

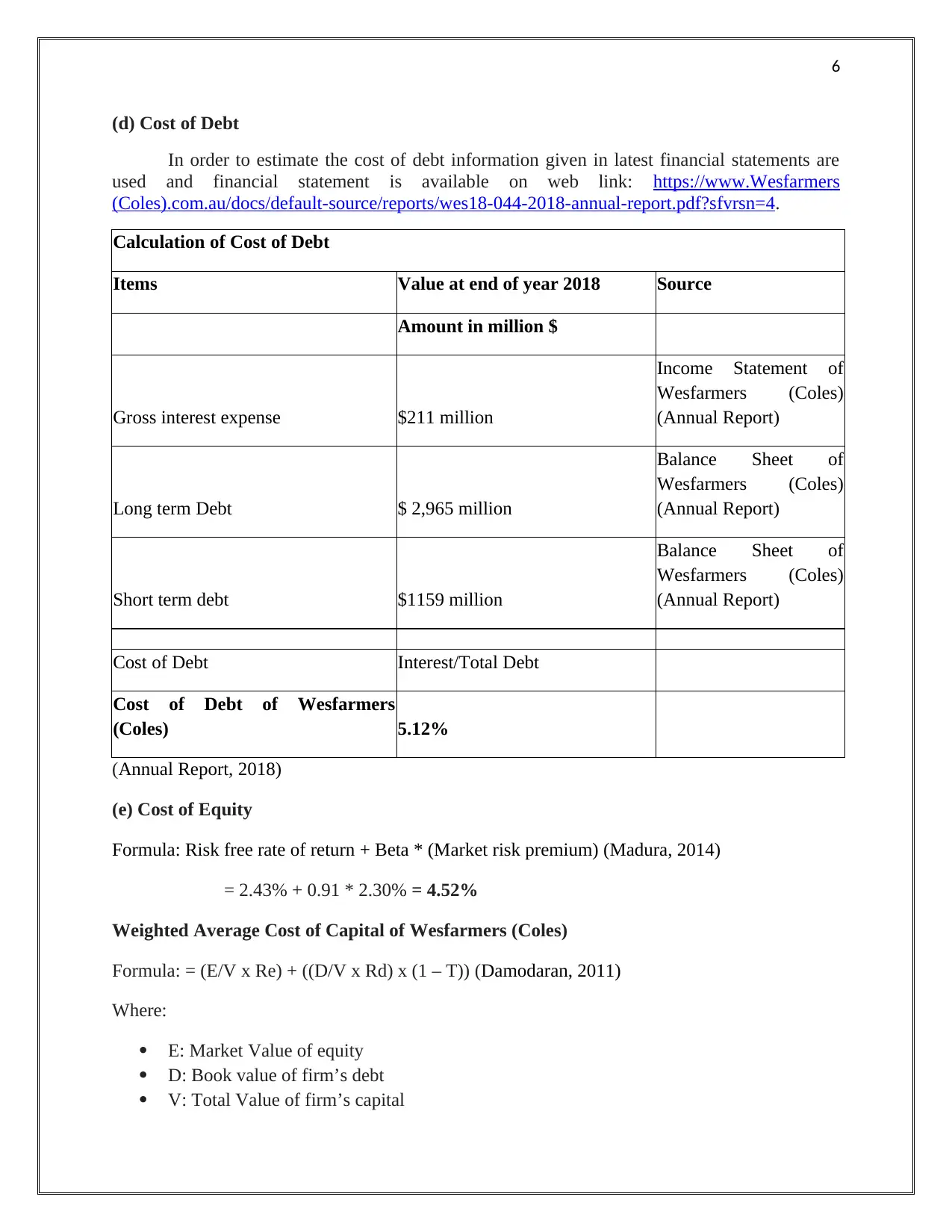

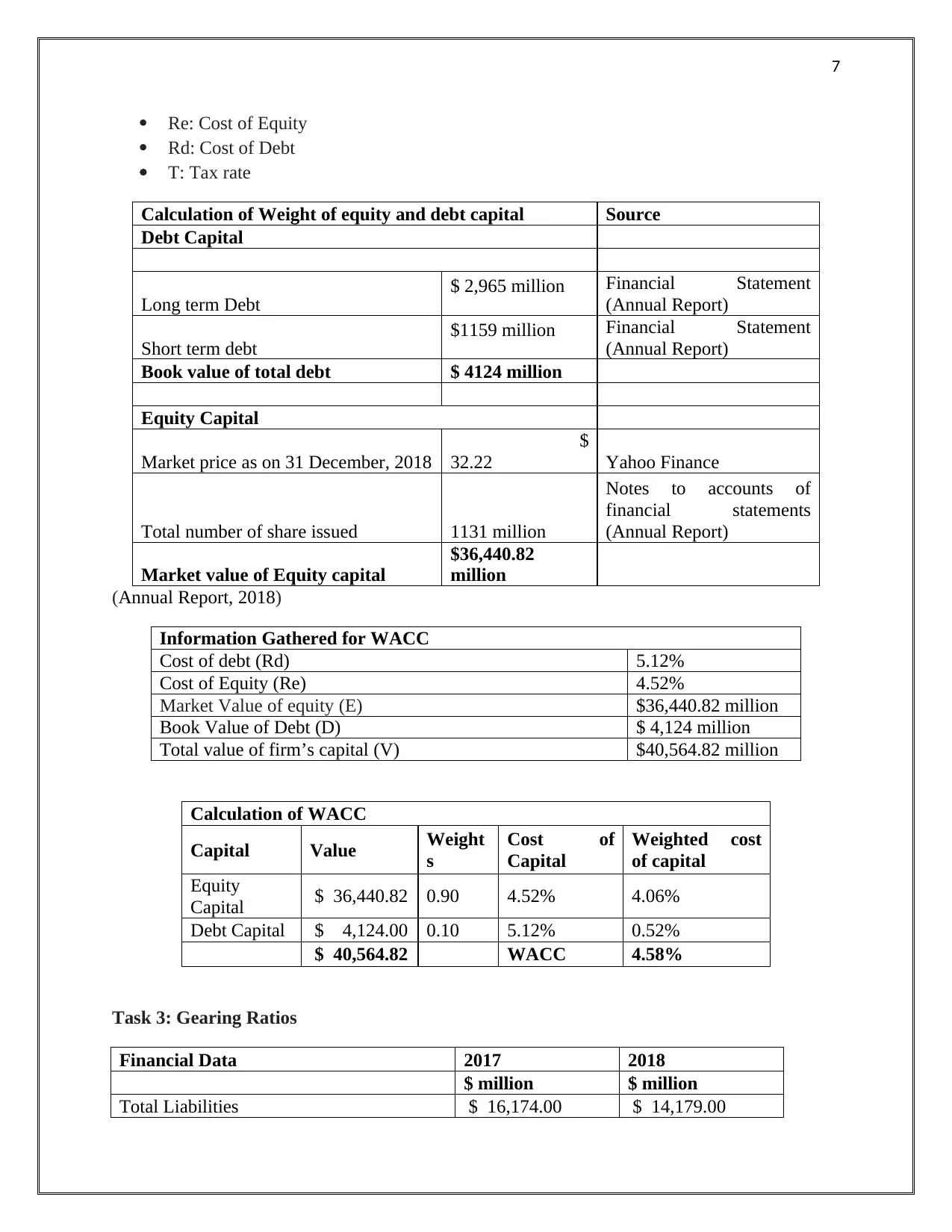

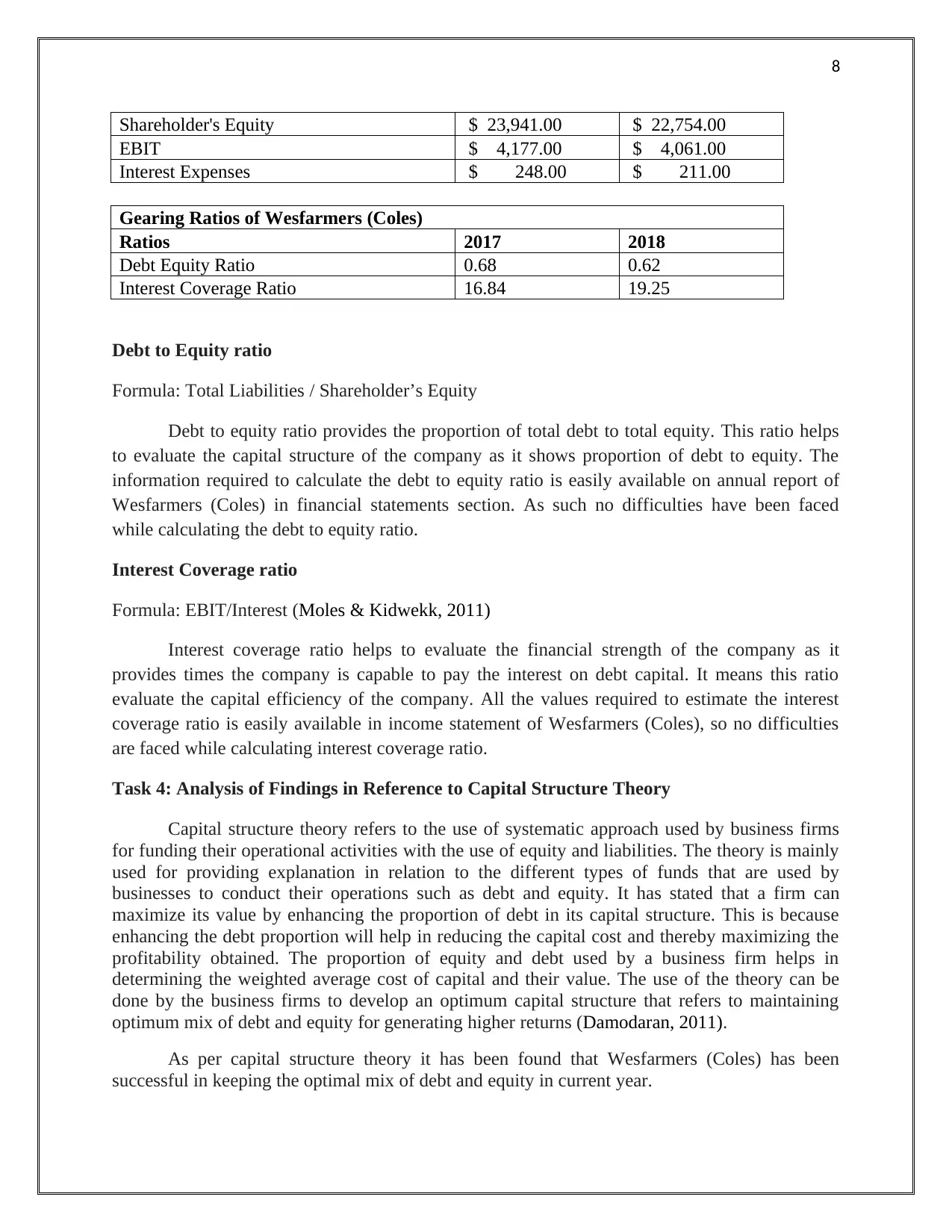

This report provides a detailed financial analysis of Wesfarmers (Coles), focusing on the calculation and interpretation of its Weighted Average Cost of Capital (WACC) and capital structure. The analysis begins with determining the risk-free rate of return, market equity premium, and beta to calculate the cost of equity. The cost of debt is calculated using information from the company's financial statements. Subsequently, the WACC is calculated using the cost of equity and debt, along with their respective weights. The report also includes the calculation of gearing ratios, such as the debt-to-equity ratio and the interest coverage ratio, to assess the company's financial leverage and solvency. The findings are then analyzed in the context of capital structure theory, discussing the optimal mix of debt and equity. Finally, the report provides recommendations to the Board regarding the company's capital structure, suggesting potential adjustments to reduce the cost of capital and maximize firm value. The report concludes with a reflection on the challenges encountered during the analysis, such as estimating the weights of equity and debt capital and the selection of appropriate data sources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.