Financial Analysis and Investment Appraisal of RP Plc

VerifiedAdded on 2023/06/07

|9

|1465

|353

AI Summary

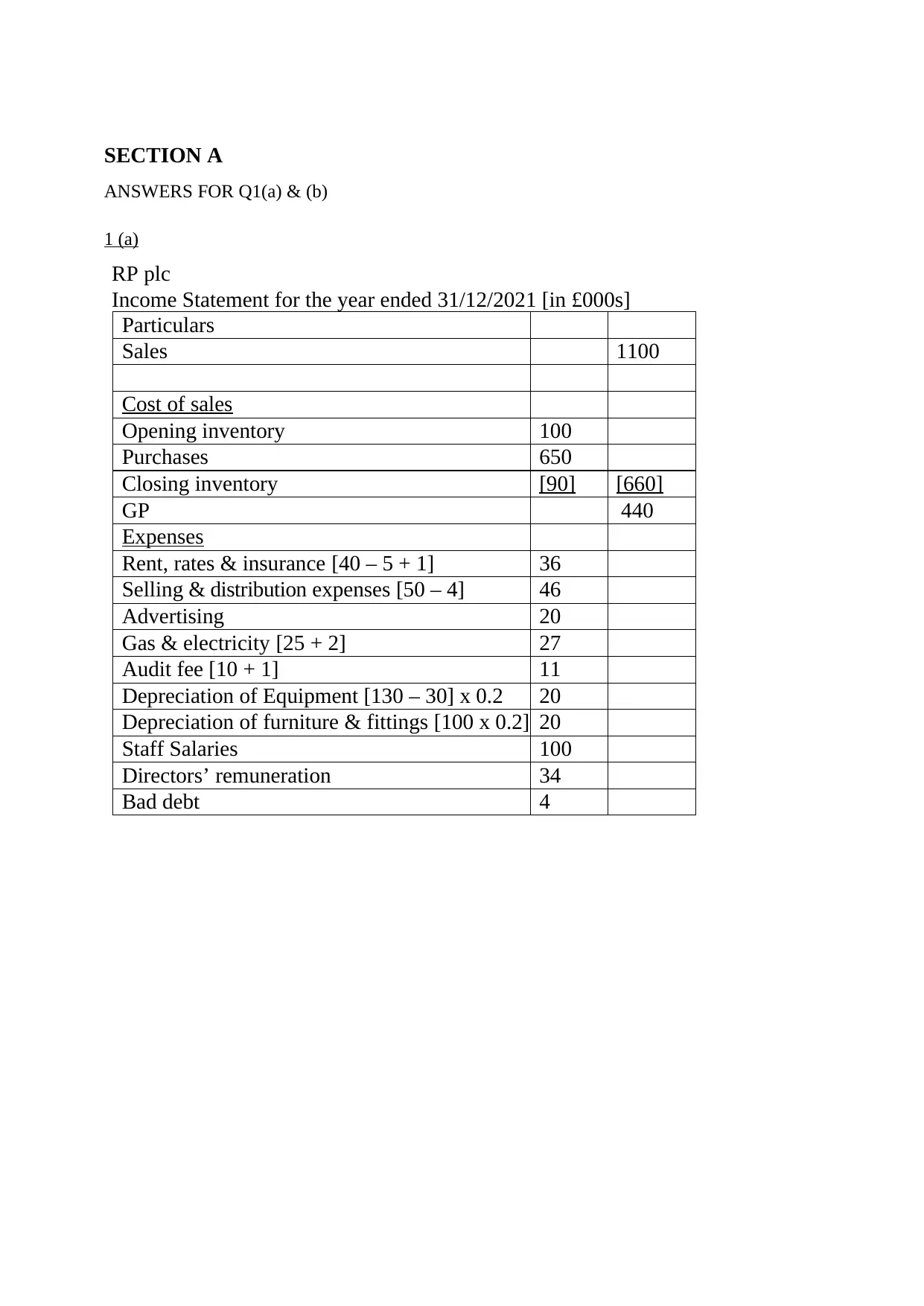

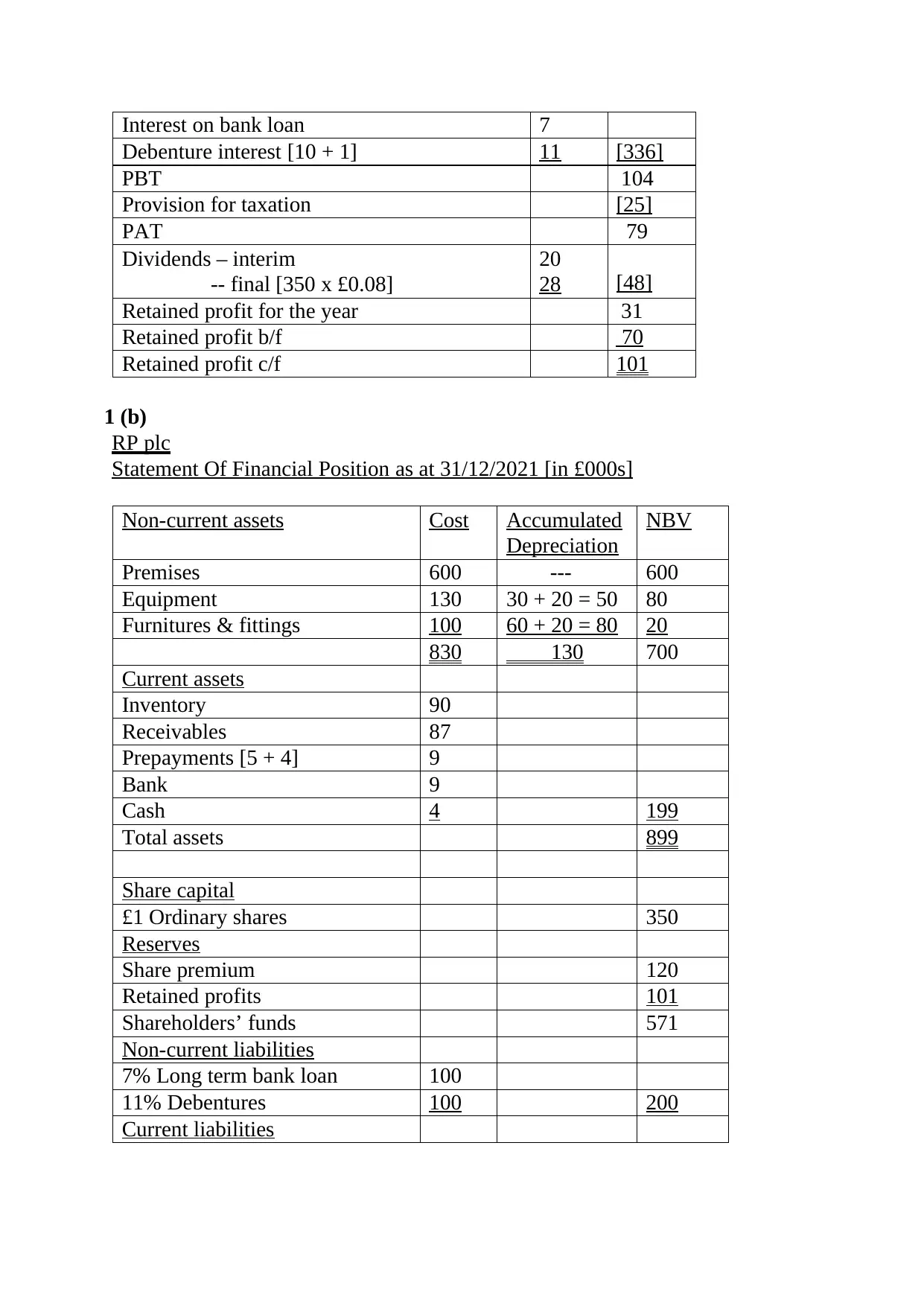

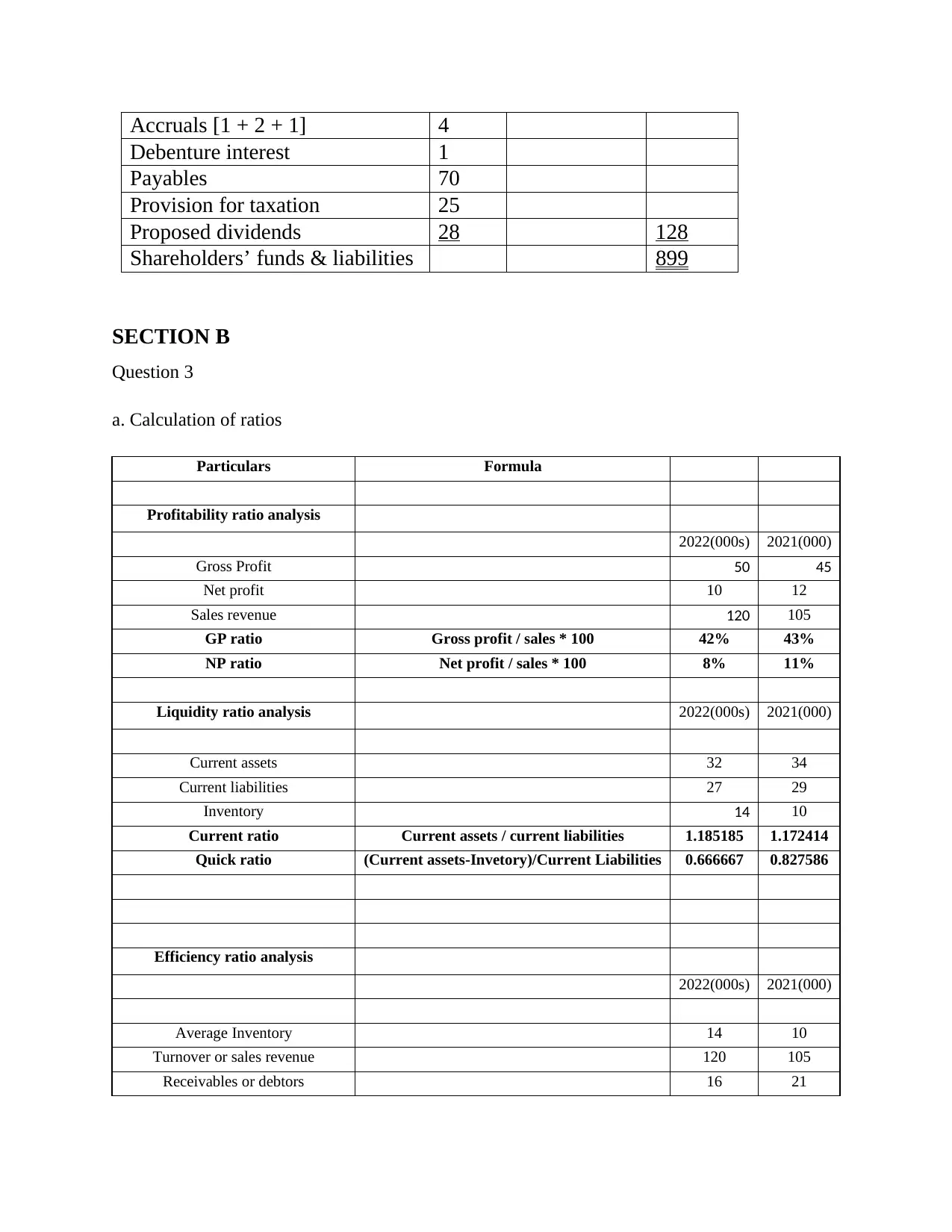

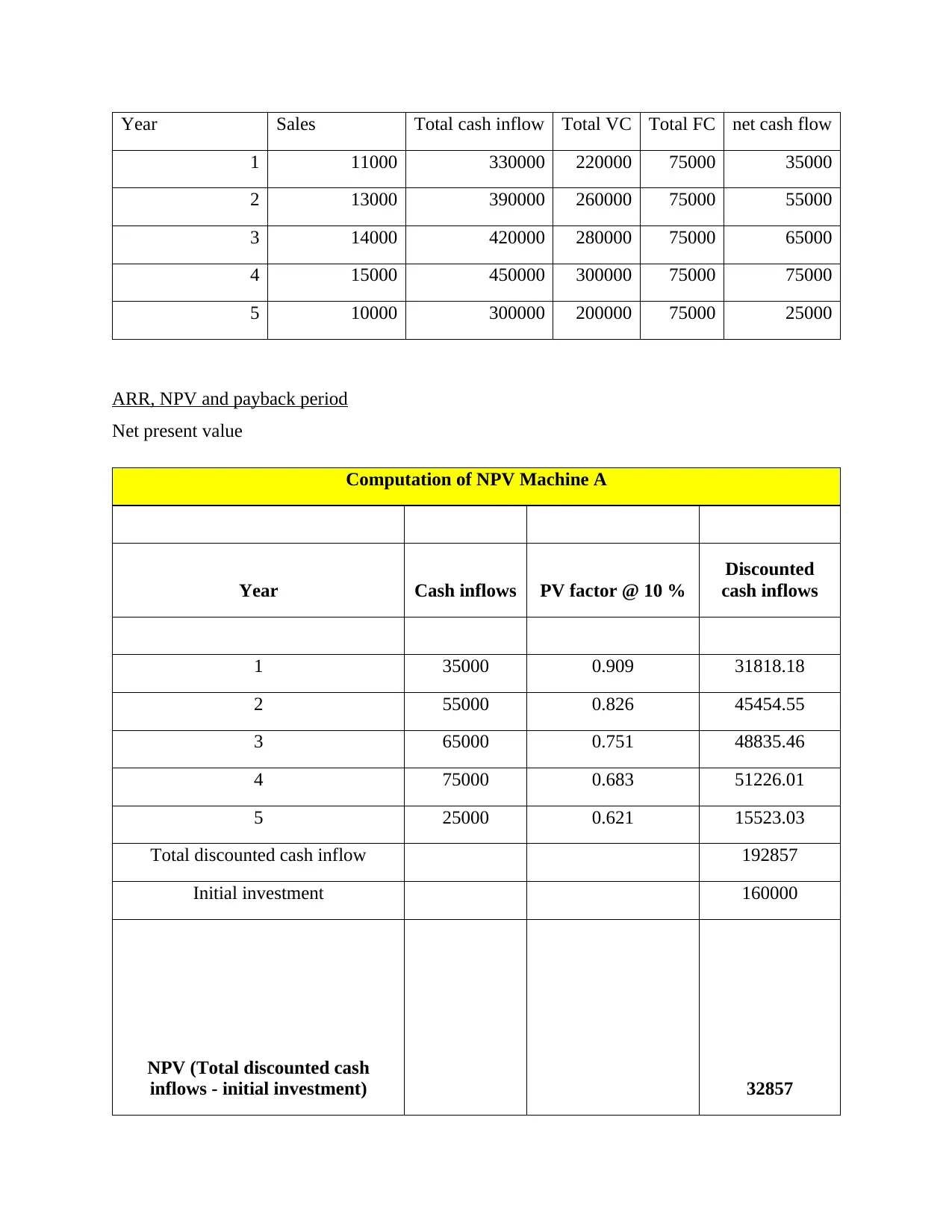

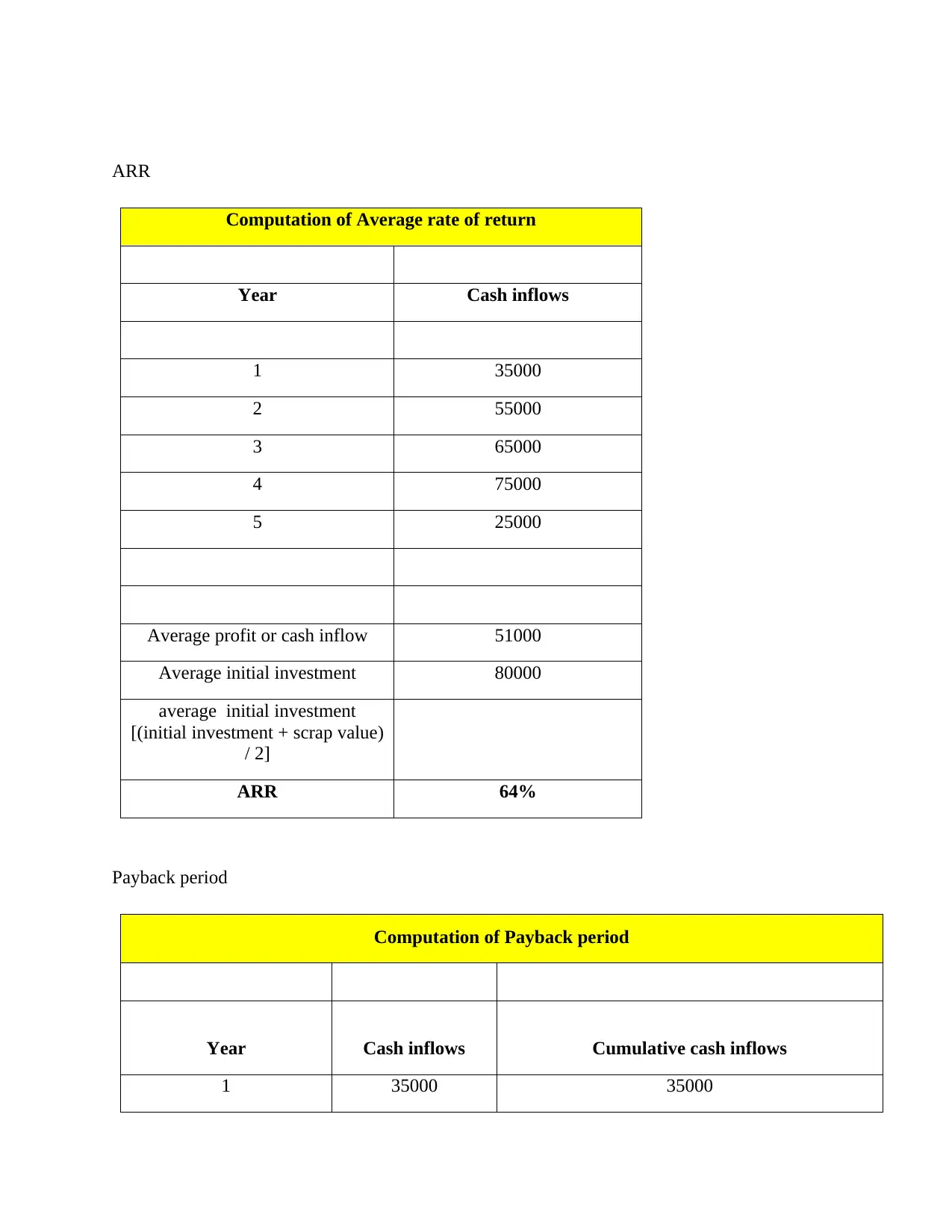

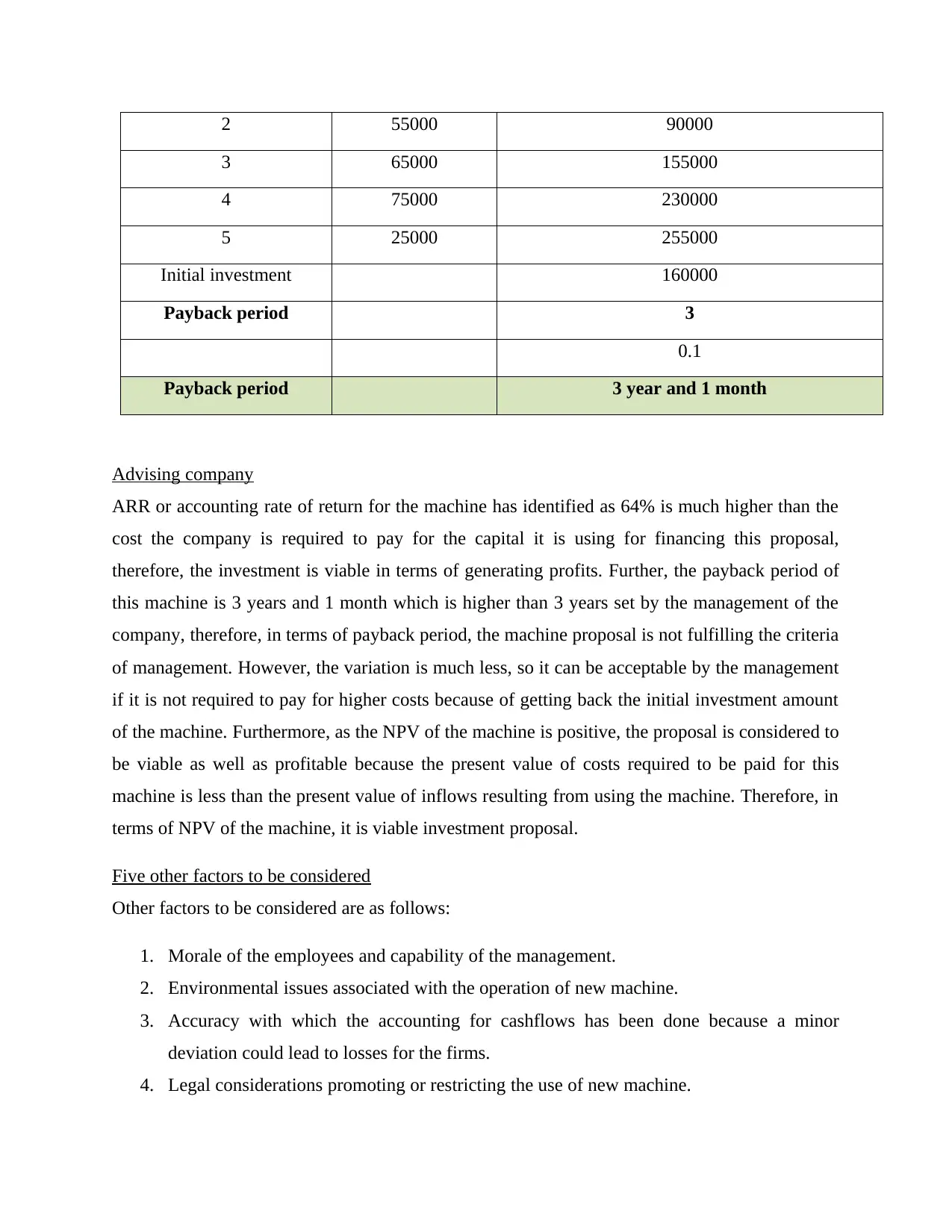

This article provides a comprehensive financial analysis and investment appraisal of RP Plc, including its profitability, liquidity, and efficiency ratios. It also includes a detailed calculation of ARR, NPV, and payback period, along with the advantages of IRR. The article also suggests five other factors that need to be considered before making an investment decision.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.