ACCT1059 Auditing 1: Sheridan AV Case Study Individual Assignment

VerifiedAdded on 2022/11/01

|14

|3570

|212

Case Study

AI Summary

This case study analyzes the Sheridan AV audit for the financial year ending March 31, 2021. The assignment involves identifying significant inherent risks at the industry and entity levels, assessing control risks for various assertions related to sales, accounts receivables, and cash. It includes identifying poor and strong internal controls and proposing recommendations for improvement. The solution provides detailed assessments of inherent risks and control risks, along with recommendations for implementing electronic inventory tracking and enhancing warehouse security. The analysis also includes a discussion of strong internal controls like inventory counting processes, and suggests control tests for each control. The document also includes working papers for risk assessment and control risk assessment.

Sheridan Av Case Study 1

SHERIDAN AV CASE STUDY

By (Student’s Name)

Professor’s Name

College

Course

Date

SHERIDAN AV CASE STUDY

By (Student’s Name)

Professor’s Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sheridan Av Case Study 2

Questions:

Sheridan AV is a new client of your firm and you were appointed as Audit Senior for Sheridan AV’s

audit for the financial year ended 31 March 2021. Perform the following tasks:

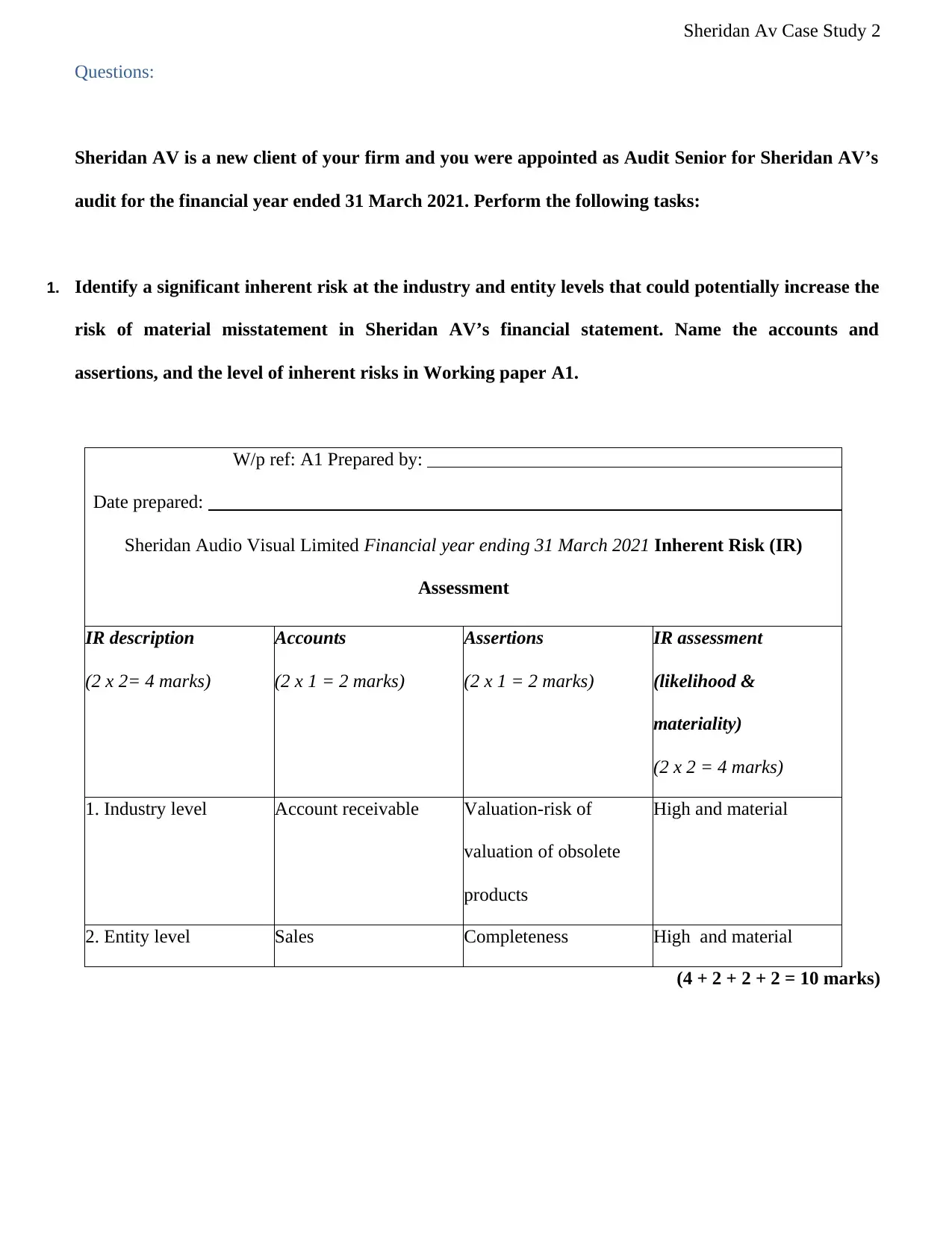

1. Identify a significant inherent risk at the industry and entity levels that could potentially increase the

risk of material misstatement in Sheridan AV’s financial statement. Name the accounts and

assertions, and the level of inherent risks in Working paper A1.

W/p ref: A1 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Inherent Risk (IR)

Assessment

IR description

(2 x 2= 4 marks)

Accounts

(2 x 1 = 2 marks)

Assertions

(2 x 1 = 2 marks)

IR assessment

(likelihood &

materiality)

(2 x 2 = 4 marks)

1. Industry level Account receivable Valuation-risk of

valuation of obsolete

products

High and material

2. Entity level Sales Completeness High and material

(4 + 2 + 2 + 2 = 10 marks)

Questions:

Sheridan AV is a new client of your firm and you were appointed as Audit Senior for Sheridan AV’s

audit for the financial year ended 31 March 2021. Perform the following tasks:

1. Identify a significant inherent risk at the industry and entity levels that could potentially increase the

risk of material misstatement in Sheridan AV’s financial statement. Name the accounts and

assertions, and the level of inherent risks in Working paper A1.

W/p ref: A1 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Inherent Risk (IR)

Assessment

IR description

(2 x 2= 4 marks)

Accounts

(2 x 1 = 2 marks)

Assertions

(2 x 1 = 2 marks)

IR assessment

(likelihood &

materiality)

(2 x 2 = 4 marks)

1. Industry level Account receivable Valuation-risk of

valuation of obsolete

products

High and material

2. Entity level Sales Completeness High and material

(4 + 2 + 2 + 2 = 10 marks)

Sheridan Av Case Study 3

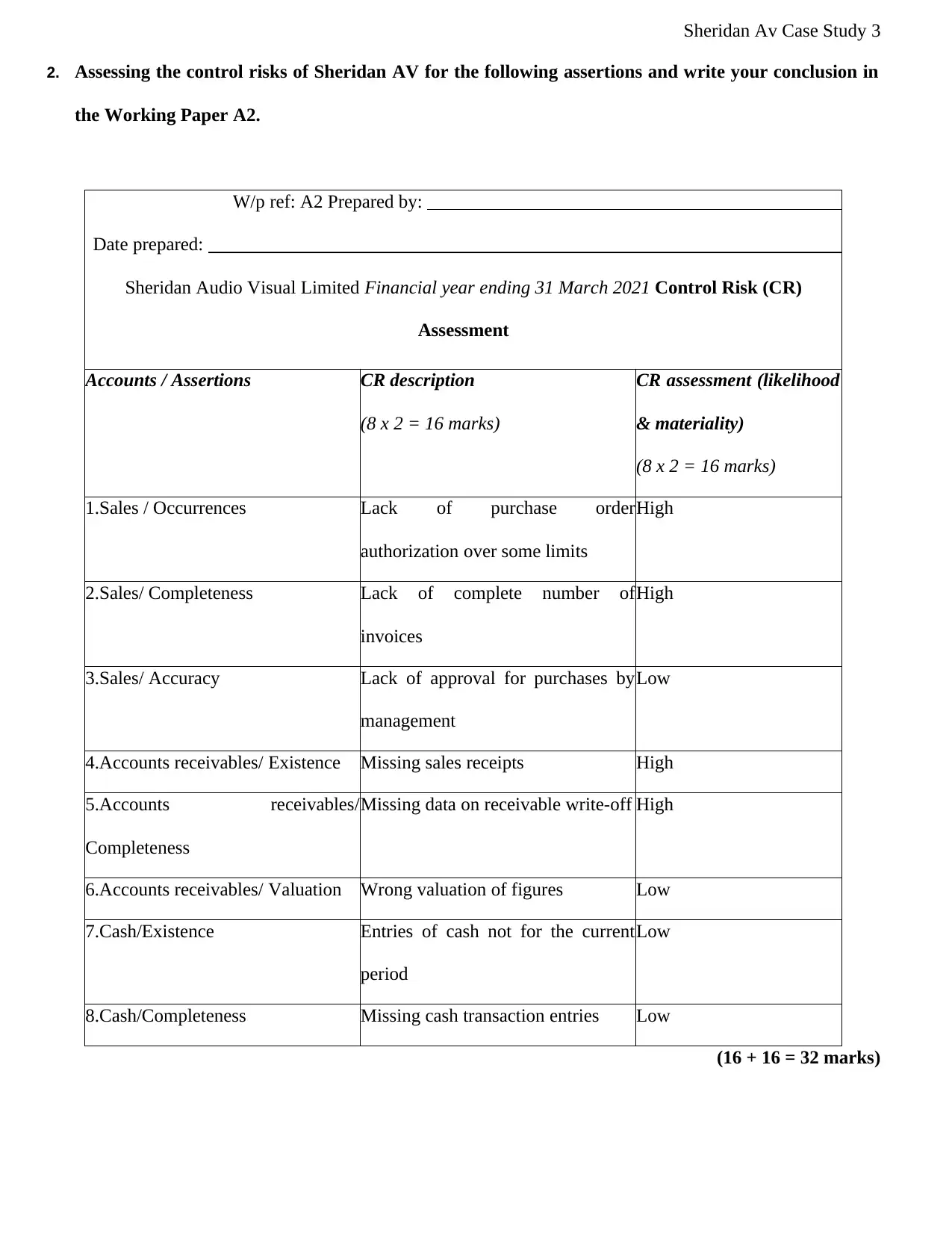

2. Assessing the control risks of Sheridan AV for the following assertions and write your conclusion in

the Working Paper A2.

W/p ref: A2 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Control Risk (CR)

Assessment

Accounts / Assertions CR description

(8 x 2 = 16 marks)

CR assessment (likelihood

& materiality)

(8 x 2 = 16 marks)

1.Sales / Occurrences Lack of purchase order

authorization over some limits

High

2.Sales/ Completeness Lack of complete number of

invoices

High

3.Sales/ Accuracy Lack of approval for purchases by

management

Low

4.Accounts receivables/ Existence Missing sales receipts High

5.Accounts receivables/

Completeness

Missing data on receivable write-off High

6.Accounts receivables/ Valuation Wrong valuation of figures Low

7.Cash/Existence Entries of cash not for the current

period

Low

8.Cash/Completeness Missing cash transaction entries Low

(16 + 16 = 32 marks)

2. Assessing the control risks of Sheridan AV for the following assertions and write your conclusion in

the Working Paper A2.

W/p ref: A2 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Control Risk (CR)

Assessment

Accounts / Assertions CR description

(8 x 2 = 16 marks)

CR assessment (likelihood

& materiality)

(8 x 2 = 16 marks)

1.Sales / Occurrences Lack of purchase order

authorization over some limits

High

2.Sales/ Completeness Lack of complete number of

invoices

High

3.Sales/ Accuracy Lack of approval for purchases by

management

Low

4.Accounts receivables/ Existence Missing sales receipts High

5.Accounts receivables/

Completeness

Missing data on receivable write-off High

6.Accounts receivables/ Valuation Wrong valuation of figures Low

7.Cash/Existence Entries of cash not for the current

period

Low

8.Cash/Completeness Missing cash transaction entries Low

(16 + 16 = 32 marks)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sheridan Av Case Study 4

3. Identify TWO poor internal controls and propose TWO recommendations you would raise in the

management letter to David Sheridan. (16 marks)

1. There is no effective tracking system of maintaining a catalog of exactly what Sheridan AV

has and where it is because the business is still using the traditional methods of tracking without using

electronic inventories through either bad codes or RFID.

Recommendation: The organization should embrace electronic inventory tracking system using

RFID tags to keep close of all items. This will help ensure that every inventory location is numbered

correctly and inventory item is identified with such numbers. RFID will enhance inventory visibility by

giving real-time updates as well as faster inventory scanning (Ertugrul 2017). Having RFID readers in

place at every portal or even doorway will ensure that the Company exactly knows when the inventories

comes into or exit a location, unlike barcodes which can still help workers to potentially move items

without scanning hence eroding the accuracy of data (Glickman et al. 2015). Such an improved visibility

will further improve the returns or recalled items tracking by giving real-time updates as items re-enter the

warehouse and storerooms in Sheridan AV.

The RFID will significantly improve the stock tracking in the organization (Alwadi et al. 2017). This

is because it will not only lead to proper inventory control, it increases inventory security as well as quality

management. This is because it will allow Sheridan AV to identity all its individual products as well as

components, and subsequently track them effectively throughout the supply chain to point of sale from

production. The RFID tag is only a tiny microchip, with a small aerial, that will significantly help this

organization to contain a massive array of digital information regarding the specific item. Such tags are

effectively encapsulated in paper, plastic or even identical materials and fixed to product or the packaging,

to a container or pallet, or delivery van or truck (Payson et al. 2015.). This tag will be interrogated

effectively by the RFID reader thus transmitting and receiving the radio signals both to and from the tag.

Thus, Sheridan AV will have readers that can vary in sizes from a hand-held device to the portal via which

3. Identify TWO poor internal controls and propose TWO recommendations you would raise in the

management letter to David Sheridan. (16 marks)

1. There is no effective tracking system of maintaining a catalog of exactly what Sheridan AV

has and where it is because the business is still using the traditional methods of tracking without using

electronic inventories through either bad codes or RFID.

Recommendation: The organization should embrace electronic inventory tracking system using

RFID tags to keep close of all items. This will help ensure that every inventory location is numbered

correctly and inventory item is identified with such numbers. RFID will enhance inventory visibility by

giving real-time updates as well as faster inventory scanning (Ertugrul 2017). Having RFID readers in

place at every portal or even doorway will ensure that the Company exactly knows when the inventories

comes into or exit a location, unlike barcodes which can still help workers to potentially move items

without scanning hence eroding the accuracy of data (Glickman et al. 2015). Such an improved visibility

will further improve the returns or recalled items tracking by giving real-time updates as items re-enter the

warehouse and storerooms in Sheridan AV.

The RFID will significantly improve the stock tracking in the organization (Alwadi et al. 2017). This

is because it will not only lead to proper inventory control, it increases inventory security as well as quality

management. This is because it will allow Sheridan AV to identity all its individual products as well as

components, and subsequently track them effectively throughout the supply chain to point of sale from

production. The RFID tag is only a tiny microchip, with a small aerial, that will significantly help this

organization to contain a massive array of digital information regarding the specific item. Such tags are

effectively encapsulated in paper, plastic or even identical materials and fixed to product or the packaging,

to a container or pallet, or delivery van or truck (Payson et al. 2015.). This tag will be interrogated

effectively by the RFID reader thus transmitting and receiving the radio signals both to and from the tag.

Thus, Sheridan AV will have readers that can vary in sizes from a hand-held device to the portal via which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sheridan Av Case Study 5

various tagged devices might get passed at once, for example, on the pallet.

The info which is collected by the readers becomes collated and then processed utilizing special

computer software. Thus, the readers might be put at different positions within the warehouse to showcase

when goods are shipped or moved and hence giving continuous control for inventory in the organization.

The Sheridan AV will greatly benefit from utilizing the RFID tagging for control of inventory as compared

to other methods like barcodes. For example, the tags will be read remotely, usually at the distance of many

meters away and also the various tags might be read at a go, allowing the complete pallet-load of good to

be effectively checked. Another advantage is that the tags might be provided unique identification codes

thus individual products will be tracked. Some kinds of tags might get overwritten, allowing info regarding

items to be effectively updated, for example, when they are shipped or moved from a given part of factory

to another.

The organization will also use the RFID tagging to deter over- or under stocking a component or

product. It will also be utilized in stock security by positioning the reader of the tag at different high-risk

points like exits and hence triggering alarms. Also, it will be used in quality control, specifically if they

stock or make items with a limited life in the shelf. The RFID installation and implementation costs have

dropped over recent past, and they continue to decrease, thus bring the practice within reach of many

business. The benefits of increasingly efficient stock control as well as enhanced security make it

specifically appealing to retailers like Sheridan AV who are also distributors stocking a broad array of

items.

2. There is no system in place advanced security of the inventory. Whereas the organization

has ensured some level of security in terms of keeping its inventories in a central location that is

warehouse and storeroom, which permits it to keep inventory secure, only locks are used. The firms

must keep its stock secure and this relies on knowing what the organization, where it is situated and

how worth-thus good records remain necessary. The stock which is portable, or does not feature the

logo of the business or is easy selling on, remains at specific risk. The stock must be protected by

identifying and marking expensive portable equipment like TVs. If where feasible, the organization

various tagged devices might get passed at once, for example, on the pallet.

The info which is collected by the readers becomes collated and then processed utilizing special

computer software. Thus, the readers might be put at different positions within the warehouse to showcase

when goods are shipped or moved and hence giving continuous control for inventory in the organization.

The Sheridan AV will greatly benefit from utilizing the RFID tagging for control of inventory as compared

to other methods like barcodes. For example, the tags will be read remotely, usually at the distance of many

meters away and also the various tags might be read at a go, allowing the complete pallet-load of good to

be effectively checked. Another advantage is that the tags might be provided unique identification codes

thus individual products will be tracked. Some kinds of tags might get overwritten, allowing info regarding

items to be effectively updated, for example, when they are shipped or moved from a given part of factory

to another.

The organization will also use the RFID tagging to deter over- or under stocking a component or

product. It will also be utilized in stock security by positioning the reader of the tag at different high-risk

points like exits and hence triggering alarms. Also, it will be used in quality control, specifically if they

stock or make items with a limited life in the shelf. The RFID installation and implementation costs have

dropped over recent past, and they continue to decrease, thus bring the practice within reach of many

business. The benefits of increasingly efficient stock control as well as enhanced security make it

specifically appealing to retailers like Sheridan AV who are also distributors stocking a broad array of

items.

2. There is no system in place advanced security of the inventory. Whereas the organization

has ensured some level of security in terms of keeping its inventories in a central location that is

warehouse and storeroom, which permits it to keep inventory secure, only locks are used. The firms

must keep its stock secure and this relies on knowing what the organization, where it is situated and

how worth-thus good records remain necessary. The stock which is portable, or does not feature the

logo of the business or is easy selling on, remains at specific risk. The stock must be protected by

identifying and marking expensive portable equipment like TVs. If where feasible, the organization

Sheridan Av Case Study 6

need to fit valuable inventory with security tags-like RFID tags that shall sound the desired alarm

where they get moved.

The organization does not need to leave any equipment hanging around following delivery.

This should be placed away in a secure and safe place, recording it and clearing up packaging. It is

also a desirable idea to dispose of all the packaging safely and securely because leaving the boxes in

the view might attract or invite the thieves. The security should also be enhanced by taking regular

inventories as well as putting CCTV in the organization’s parking lots alongside key locations. The

security of the stock should also be improved to avoid any theft by the staff. This is because theft by

workers can be a great problem which might be avoided. The organization must train the staff

regarding the organization stock security systems and the disciplinary procedures and policies

(Ozguven and Ozbay 2015). This training regarding the cost of stealing stock shall assist since several

individual are not aware of implications for organization turnover as well as job security. The

organization must also set up the desired procedures to deter theft because staff with financial

responsibilities need not to be in charge of inventory control. The organization must further limit the

access to its warehouse, as well as storerooms and change the staff regularly to evade bad practice or

collusion.

Recommendation The organization enhance security of its warehouse by having security

codes which can make sure that only trusted individuals have access to its inventory. There is also a

need to ensure that all deliveries from suppliers are counted for prior to getting into inventory to

ensure that discrepancies between deliveries as well as purchase orders are instantly remedied. The

secure code system will enable the process which permit Sheridan to control as well as administer

secure warehouse operations from time materials and goods enter the warehouse till when goods move

the warehouse to be delivered to customers. The warehouse operations encompasses the management

of inventory, auditing, and picking process (Axsäter 2015). WMS will provide the desired visibility

into the Sheridan organization inventory all the times as well as in all locations irrespective of whether

the goods are in transit or in the facility. It will help effectively made the supply chain operations from

need to fit valuable inventory with security tags-like RFID tags that shall sound the desired alarm

where they get moved.

The organization does not need to leave any equipment hanging around following delivery.

This should be placed away in a secure and safe place, recording it and clearing up packaging. It is

also a desirable idea to dispose of all the packaging safely and securely because leaving the boxes in

the view might attract or invite the thieves. The security should also be enhanced by taking regular

inventories as well as putting CCTV in the organization’s parking lots alongside key locations. The

security of the stock should also be improved to avoid any theft by the staff. This is because theft by

workers can be a great problem which might be avoided. The organization must train the staff

regarding the organization stock security systems and the disciplinary procedures and policies

(Ozguven and Ozbay 2015). This training regarding the cost of stealing stock shall assist since several

individual are not aware of implications for organization turnover as well as job security. The

organization must also set up the desired procedures to deter theft because staff with financial

responsibilities need not to be in charge of inventory control. The organization must further limit the

access to its warehouse, as well as storerooms and change the staff regularly to evade bad practice or

collusion.

Recommendation The organization enhance security of its warehouse by having security

codes which can make sure that only trusted individuals have access to its inventory. There is also a

need to ensure that all deliveries from suppliers are counted for prior to getting into inventory to

ensure that discrepancies between deliveries as well as purchase orders are instantly remedied. The

secure code system will enable the process which permit Sheridan to control as well as administer

secure warehouse operations from time materials and goods enter the warehouse till when goods move

the warehouse to be delivered to customers. The warehouse operations encompasses the management

of inventory, auditing, and picking process (Axsäter 2015). WMS will provide the desired visibility

into the Sheridan organization inventory all the times as well as in all locations irrespective of whether

the goods are in transit or in the facility. It will help effectively made the supply chain operations from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sheridan Av Case Study 7

the wholesaler or manufacturer, to distribution center or retailer. WMS will be used together with or

integrated with the TMS or transportation management system or even IS (inventory management)

(Fan et al. 2015).

4. Identify TWO strong internal controls and propose a control test for each control. (16 marks)

1. There is proper culture of inventory counting process which ensures there is proper tracking

of inventory: The stock is effectively prepared for counting and the shop remain closed on 31 March 31.

Moreover, the there is a designated person, Peter Fillion-who is the warehouse and distribution manager

who takes charge of the counting process. The stock is neatly stacked read for counting and the system is in

place to count both stock and raw materials which are stored in warehouse and storeroom (Baptiste et al.

2016). The different zones in the store room makes counting easy as the stock is identified by different type

per zone as speaker systems (zone 1- both finished products made in the company and those purchased

from other manufacturers); TVs and projectors in zone 2 and Blu Ray players, amplifiers and the likes in

zone 4 and finished cabinets made in the firm in zone 4 which ensures that each item is considered and

counted per the zones (Phillips et al. 2017).

The inventory counting process is strong because there is no room for stocks to go in or out of the

Sheridan premises during the day of counting as the doors to the warehouse remains closed and no

deliveries in or out is allowed. Moreover, manufacturing is closed during the day of accounting as Jane

Darrow, production manager closed down all production and production remains stopped from 3 pm the

previous day to counting as well as the workshop being closed the whole day for counting. This ensures

that no room unnecessary counting errors (Goyal et al. 2016). The counting procedure is also effective

because the Sheridan Av has three people responsible for counting the inventory.

Rob Cole (Peter’s warehouse assistant) and Dan Sheppard always do the most of the counting and

Peter, end up also doing a bit of counting in store room and his warehouse assistant does the most of

counting in warehouse. Dan who is the retail shop assistant is responsible for counting in the shop and

demo rooms and hence such designation or roles separation ensures effective counting (Goyal et al. 2016).

the wholesaler or manufacturer, to distribution center or retailer. WMS will be used together with or

integrated with the TMS or transportation management system or even IS (inventory management)

(Fan et al. 2015).

4. Identify TWO strong internal controls and propose a control test for each control. (16 marks)

1. There is proper culture of inventory counting process which ensures there is proper tracking

of inventory: The stock is effectively prepared for counting and the shop remain closed on 31 March 31.

Moreover, the there is a designated person, Peter Fillion-who is the warehouse and distribution manager

who takes charge of the counting process. The stock is neatly stacked read for counting and the system is in

place to count both stock and raw materials which are stored in warehouse and storeroom (Baptiste et al.

2016). The different zones in the store room makes counting easy as the stock is identified by different type

per zone as speaker systems (zone 1- both finished products made in the company and those purchased

from other manufacturers); TVs and projectors in zone 2 and Blu Ray players, amplifiers and the likes in

zone 4 and finished cabinets made in the firm in zone 4 which ensures that each item is considered and

counted per the zones (Phillips et al. 2017).

The inventory counting process is strong because there is no room for stocks to go in or out of the

Sheridan premises during the day of counting as the doors to the warehouse remains closed and no

deliveries in or out is allowed. Moreover, manufacturing is closed during the day of accounting as Jane

Darrow, production manager closed down all production and production remains stopped from 3 pm the

previous day to counting as well as the workshop being closed the whole day for counting. This ensures

that no room unnecessary counting errors (Goyal et al. 2016). The counting procedure is also effective

because the Sheridan Av has three people responsible for counting the inventory.

Rob Cole (Peter’s warehouse assistant) and Dan Sheppard always do the most of the counting and

Peter, end up also doing a bit of counting in store room and his warehouse assistant does the most of

counting in warehouse. Dan who is the retail shop assistant is responsible for counting in the shop and

demo rooms and hence such designation or roles separation ensures effective counting (Goyal et al. 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sheridan Av Case Study 8

The warehouse counting is effective since the firm has a set of counting sheets to work from and the sheets

are on pre-printed sheets with stock number and item description printed already and this allows Rob to fill

in the blank fields at top of a form and work through the various zones in warehouse as he writes done zone

and quantity of each item and make notes of all the damaged or slow-moving stock (Phillip et al. 2019).

The counting in sheets for demo and shop are blank and this allows Dan Sheppard to count goods in

shop and demo rooms and write all details in by hand while store room counting also uses blank sheets as

Peter himself does the counting (Clements, Tyco Fire and Security GmbH 2015). There is also Test in

place as Sheridan Av has a system in place for inventory counting test. Specifically, Peter does the test

counts on a sample of work from Dan and Rob. Further, Peter gives additional instruction for counting by

asking both Dan and Rob who do the most of the counting to attach a small sticker to every item they count

to avoid any chance for double counting as there are thousands of items in stock (Goyal et al. 2016).

Moreover, Peter additionally instructs Rob and Dan to make notes on sheets of any stock that is

damaged, old, or moving slow as this help determine the risk of damages and even the valuation risks due

to obsolesce (Glickman et al. 2015). The proposed test is for Peter to always to take a sample check of the

already counted items by both Rob and Dan by choosing count sheets at random and checking the items on

count sheets against items on warehouse shelf to check if there is a match and also do the reverse to see if

the items on shelves match those sample count sheets to ensure correct recording (Bynum and Ramey

2016).

2. There is correct numbering of invoice which improves sales internal control. The invoicing

is important as aspect of internal control as it ensures that payment is tracked effectively. The proposed

control test for invoice number is for auditor to ensure that all numbers in a given section remain accounted

for and that none is missing (Alyahya, Wang and Bennett 2016).

5. Based on your results of question 1 and 2, complete Working paper A5 to determine the overall risk

assessment and acceptable detection risk (DR). Provide your assessment if each item is “high”, “low”

The warehouse counting is effective since the firm has a set of counting sheets to work from and the sheets

are on pre-printed sheets with stock number and item description printed already and this allows Rob to fill

in the blank fields at top of a form and work through the various zones in warehouse as he writes done zone

and quantity of each item and make notes of all the damaged or slow-moving stock (Phillip et al. 2019).

The counting in sheets for demo and shop are blank and this allows Dan Sheppard to count goods in

shop and demo rooms and write all details in by hand while store room counting also uses blank sheets as

Peter himself does the counting (Clements, Tyco Fire and Security GmbH 2015). There is also Test in

place as Sheridan Av has a system in place for inventory counting test. Specifically, Peter does the test

counts on a sample of work from Dan and Rob. Further, Peter gives additional instruction for counting by

asking both Dan and Rob who do the most of the counting to attach a small sticker to every item they count

to avoid any chance for double counting as there are thousands of items in stock (Goyal et al. 2016).

Moreover, Peter additionally instructs Rob and Dan to make notes on sheets of any stock that is

damaged, old, or moving slow as this help determine the risk of damages and even the valuation risks due

to obsolesce (Glickman et al. 2015). The proposed test is for Peter to always to take a sample check of the

already counted items by both Rob and Dan by choosing count sheets at random and checking the items on

count sheets against items on warehouse shelf to check if there is a match and also do the reverse to see if

the items on shelves match those sample count sheets to ensure correct recording (Bynum and Ramey

2016).

2. There is correct numbering of invoice which improves sales internal control. The invoicing

is important as aspect of internal control as it ensures that payment is tracked effectively. The proposed

control test for invoice number is for auditor to ensure that all numbers in a given section remain accounted

for and that none is missing (Alyahya, Wang and Bennett 2016).

5. Based on your results of question 1 and 2, complete Working paper A5 to determine the overall risk

assessment and acceptable detection risk (DR). Provide your assessment if each item is “high”, “low”

Sheridan Av Case Study 9

or “medium”.

or “medium”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sheridan Av Case Study 10

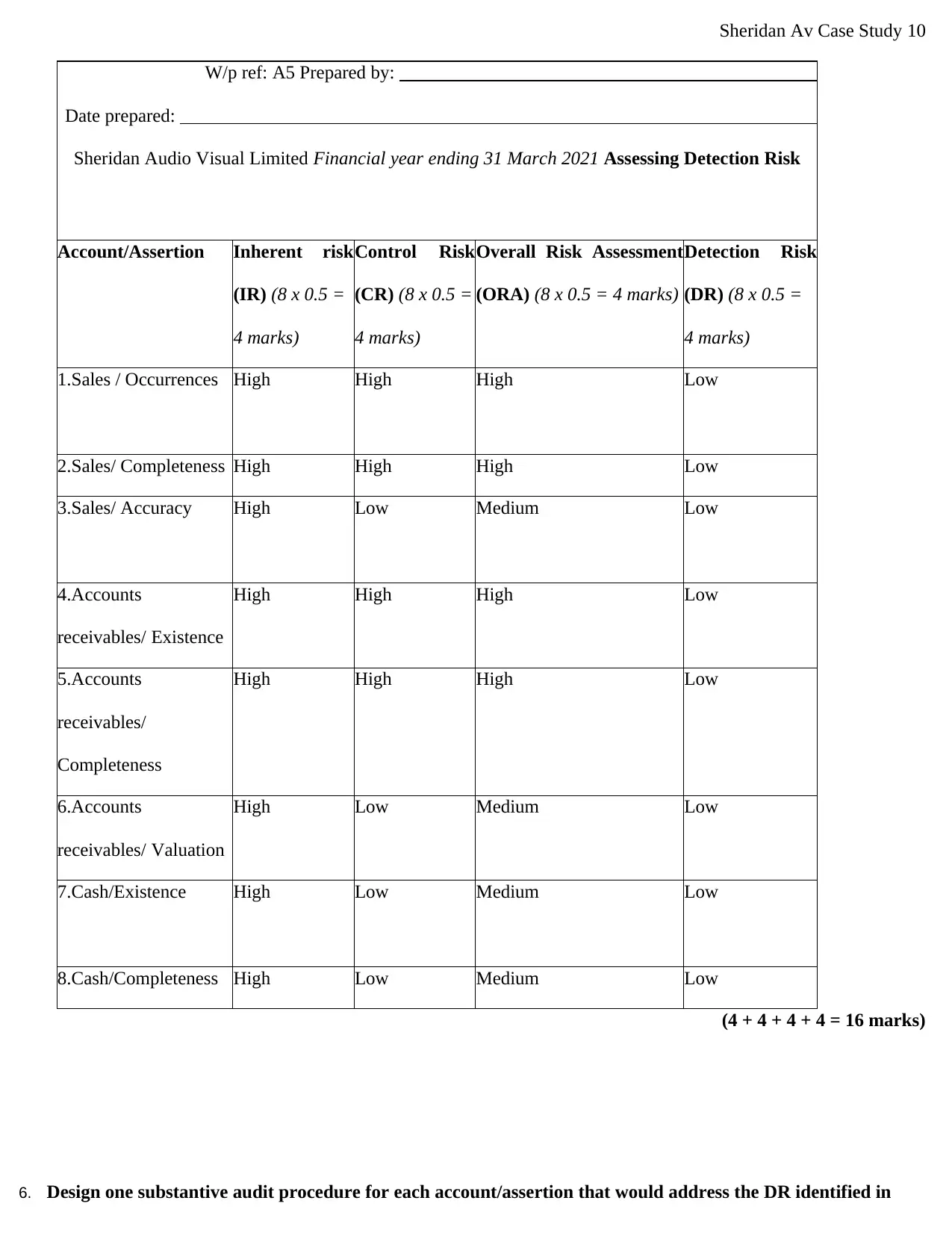

W/p ref: A5 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Assessing Detection Risk

Account/Assertion Inherent risk

(IR) (8 x 0.5 =

4 marks)

Control Risk

(CR) (8 x 0.5 =

4 marks)

Overall Risk Assessment

(ORA) (8 x 0.5 = 4 marks)

Detection Risk

(DR) (8 x 0.5 =

4 marks)

1.Sales / Occurrences High High High Low

2.Sales/ Completeness High High High Low

3.Sales/ Accuracy High Low Medium Low

4.Accounts

receivables/ Existence

High High High Low

5.Accounts

receivables/

Completeness

High High High Low

6.Accounts

receivables/ Valuation

High Low Medium Low

7.Cash/Existence High Low Medium Low

8.Cash/Completeness High Low Medium Low

(4 + 4 + 4 + 4 = 16 marks)

6. Design one substantive audit procedure for each account/assertion that would address the DR identified in

W/p ref: A5 Prepared by:

Date prepared:

Sheridan Audio Visual Limited Financial year ending 31 March 2021 Assessing Detection Risk

Account/Assertion Inherent risk

(IR) (8 x 0.5 =

4 marks)

Control Risk

(CR) (8 x 0.5 =

4 marks)

Overall Risk Assessment

(ORA) (8 x 0.5 = 4 marks)

Detection Risk

(DR) (8 x 0.5 =

4 marks)

1.Sales / Occurrences High High High Low

2.Sales/ Completeness High High High Low

3.Sales/ Accuracy High Low Medium Low

4.Accounts

receivables/ Existence

High High High Low

5.Accounts

receivables/

Completeness

High High High Low

6.Accounts

receivables/ Valuation

High Low Medium Low

7.Cash/Existence High Low Medium Low

8.Cash/Completeness High Low Medium Low

(4 + 4 + 4 + 4 = 16 marks)

6. Design one substantive audit procedure for each account/assertion that would address the DR identified in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sheridan Av Case Study 11

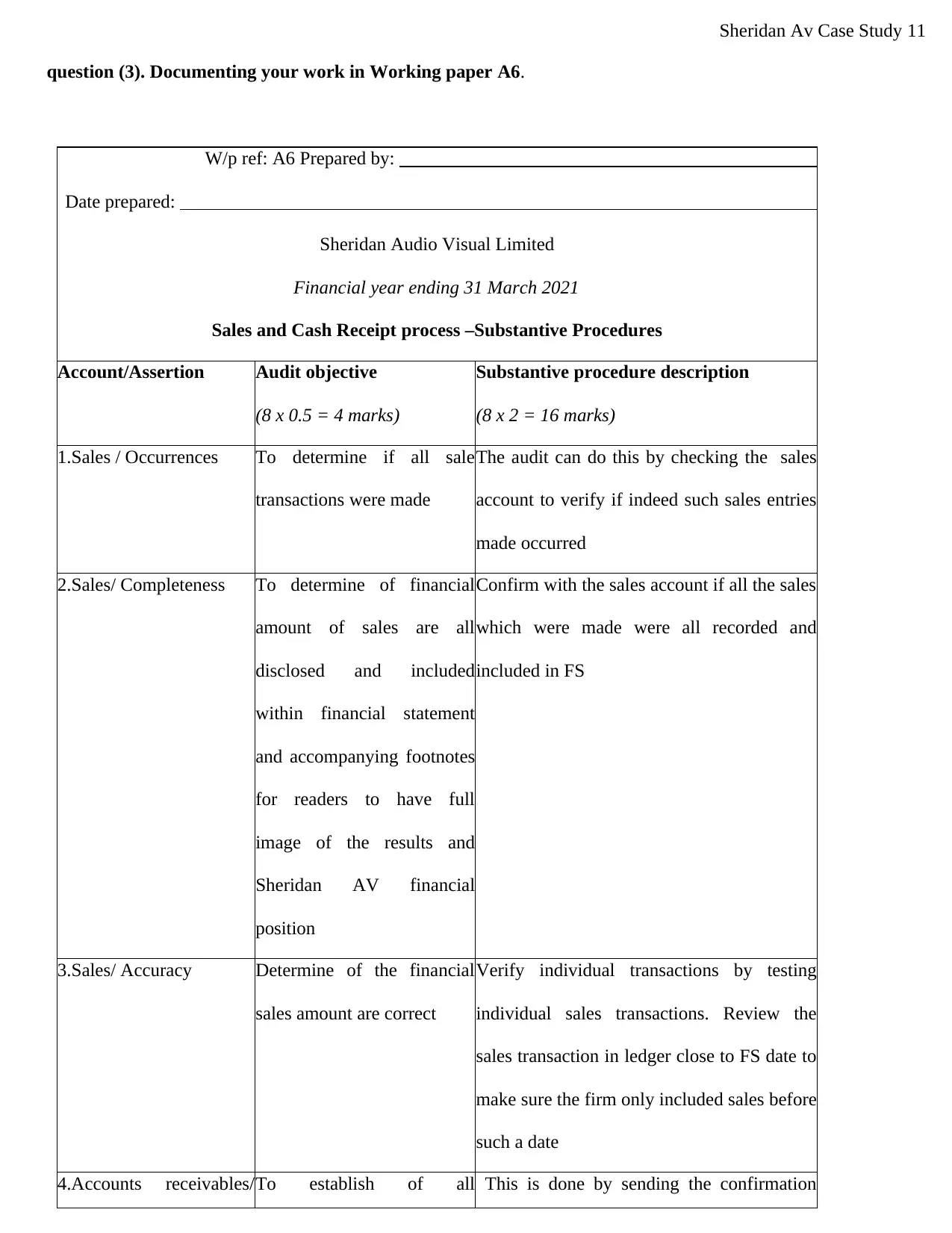

question (3). Documenting your work in Working paper A6.

W/p ref: A6 Prepared by:

Date prepared:

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Sales and Cash Receipt process –Substantive Procedures

Account/Assertion Audit objective

(8 x 0.5 = 4 marks)

Substantive procedure description

(8 x 2 = 16 marks)

1.Sales / Occurrences To determine if all sale

transactions were made

The audit can do this by checking the sales

account to verify if indeed such sales entries

made occurred

2.Sales/ Completeness To determine of financial

amount of sales are all

disclosed and included

within financial statement

and accompanying footnotes

for readers to have full

image of the results and

Sheridan AV financial

position

Confirm with the sales account if all the sales

which were made were all recorded and

included in FS

3.Sales/ Accuracy Determine of the financial

sales amount are correct

Verify individual transactions by testing

individual sales transactions. Review the

sales transaction in ledger close to FS date to

make sure the firm only included sales before

such a date

4.Accounts receivables/To establish of all This is done by sending the confirmation

question (3). Documenting your work in Working paper A6.

W/p ref: A6 Prepared by:

Date prepared:

Sheridan Audio Visual Limited

Financial year ending 31 March 2021

Sales and Cash Receipt process –Substantive Procedures

Account/Assertion Audit objective

(8 x 0.5 = 4 marks)

Substantive procedure description

(8 x 2 = 16 marks)

1.Sales / Occurrences To determine if all sale

transactions were made

The audit can do this by checking the sales

account to verify if indeed such sales entries

made occurred

2.Sales/ Completeness To determine of financial

amount of sales are all

disclosed and included

within financial statement

and accompanying footnotes

for readers to have full

image of the results and

Sheridan AV financial

position

Confirm with the sales account if all the sales

which were made were all recorded and

included in FS

3.Sales/ Accuracy Determine of the financial

sales amount are correct

Verify individual transactions by testing

individual sales transactions. Review the

sales transaction in ledger close to FS date to

make sure the firm only included sales before

such a date

4.Accounts receivables/To establish of all This is done by sending the confirmation

Sheridan Av Case Study 12

Existence transactions under the

account receivable occurred

in the said period

letters to the customers to obtain objective

assurance of the correctness of the balance

5.Accounts receivables/

Completeness

To establish of the account

receivable transactions

disclosed and included all

the information in FS

Check the account receivable entries and

confirm if all transactions were made

6.Accounts receivables/

Valuation

To determine if account

receivable transactions

summarized in FS were

valued properly especially

those that need to be either

first or consequently

recorded at market price

Check the valuation of each transactions if

were either initially or subsequently done as

required

7.Cash/Existence

To confirm if the cash

recorded occurred in the said

period

Check the cash account and ensure only

those cash transactions that took place in that

period are recorded

8.Cash/Completeness

To establish of the cash

information were fully

disclosed and included in FS

Verify the cash account and see if all cash

entries were made

(4 + 16 = 20 marks)

References

Existence transactions under the

account receivable occurred

in the said period

letters to the customers to obtain objective

assurance of the correctness of the balance

5.Accounts receivables/

Completeness

To establish of the account

receivable transactions

disclosed and included all

the information in FS

Check the account receivable entries and

confirm if all transactions were made

6.Accounts receivables/

Valuation

To determine if account

receivable transactions

summarized in FS were

valued properly especially

those that need to be either

first or consequently

recorded at market price

Check the valuation of each transactions if

were either initially or subsequently done as

required

7.Cash/Existence

To confirm if the cash

recorded occurred in the said

period

Check the cash account and ensure only

those cash transactions that took place in that

period are recorded

8.Cash/Completeness

To establish of the cash

information were fully

disclosed and included in FS

Verify the cash account and see if all cash

entries were made

(4 + 16 = 20 marks)

References

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.