Comprehensive Management Accounting Report for Jeffrey & Son's

VerifiedAdded on 2020/01/15

|19

|5698

|198

Report

AI Summary

This management accounting report focuses on Jeffrey & Son's, a manufacturing organization producing Exquisite products. It explores various managerial tools to enhance the company's performance, including cost classification based on elements, functions, nature, and behavior. The report calculates total and unit costs using job costing methods, determines overhead absorption rates, and prepares cost reports with variance analysis. It also examines performance indicators to identify improvement areas and suggests cost reduction, value enhancement, and quality improvement strategies. Furthermore, the report covers budgeting processes, including production, material purchase, and cash budgets, along with variance detection, root cause analysis, and corrective actions. Finally, the report presents findings to responsibility centers, providing a comprehensive overview of management accounting applications for improved operational and financial performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Cost classification based on element, function, nature and behaviour.................1

AC 1.2 Computation of total and unit cost for Job no. 444 through using job costing

method...............................................................................................................................2

AC 1.3 Determination of cost of Exquisite through using job costing method................3

AC 1.4 Computation of cost through using direct labour hours for overhead absorption5

TASK 2......................................................................................................................................6

AC 2.1 Preparation and analysis of cost report and comment on respective variances....6

AC 2.2 Performance indicators to determine potential improvement areas.....................7

AC 2.3 Suggestive ways to reduce cost, enhance value and quality................................8

TASK 3......................................................................................................................................9

AC 3.1 Purpose and nature of budgeting process to Jeffrey & Son's budget holders......9

AC 3.2 Appropriate budgeting method for Jeffrey & Son's.............................................9

AC 3.3 Preparation of production and material purchase budget.....................................9

AC 3.4 Preparation of Jeffrey & Son's cash budget.........................................................9

TASK 4......................................................................................................................................9

AC 4.1 Detecting variances, its causes and recommend corrective actions.....................9

AC 4.2 Preparation of operating statement through reconciling budgeted and actual results

...........................................................................................................................................9

AC 4.3 Report of findings to responsibility centres.........................................................9

CONCLUSION..........................................................................................................................9

REFERENCES...........................................................................................................................9

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Cost classification based on element, function, nature and behaviour.................1

AC 1.2 Computation of total and unit cost for Job no. 444 through using job costing

method...............................................................................................................................2

AC 1.3 Determination of cost of Exquisite through using job costing method................3

AC 1.4 Computation of cost through using direct labour hours for overhead absorption5

TASK 2......................................................................................................................................6

AC 2.1 Preparation and analysis of cost report and comment on respective variances....6

AC 2.2 Performance indicators to determine potential improvement areas.....................7

AC 2.3 Suggestive ways to reduce cost, enhance value and quality................................8

TASK 3......................................................................................................................................9

AC 3.1 Purpose and nature of budgeting process to Jeffrey & Son's budget holders......9

AC 3.2 Appropriate budgeting method for Jeffrey & Son's.............................................9

AC 3.3 Preparation of production and material purchase budget.....................................9

AC 3.4 Preparation of Jeffrey & Son's cash budget.........................................................9

TASK 4......................................................................................................................................9

AC 4.1 Detecting variances, its causes and recommend corrective actions.....................9

AC 4.2 Preparation of operating statement through reconciling budgeted and actual results

...........................................................................................................................................9

AC 4.3 Report of findings to responsibility centres.........................................................9

CONCLUSION..........................................................................................................................9

REFERENCES...........................................................................................................................9

INTRODUCTION

Managers play a crucial role in the business success as they analyse company's

financial performance and take strategic decisions. Management accounting is the process of

preparing managerial reports from financial information, taking effective decisions, ensure

optimum allocation of resources, and manage firm’s operational and financial risk. Jeffrey &

Son's is a manufacturing organization which produces variety of popular and branded

products, called Exquisite. In present project report, various kinds of managerial tools will be

discussed for improving company's performance. The report will describe the significance of

management accounting for cost computation, effective cost management, preparing cost

report, variance analysis and taking corrective actions to eliminate adverse variances.

Moreover, various budgeting techniques will be explained to manage firms operations.

TASK 1

AC 1.1 Cost classification based on element, function, nature and behaviour

Cost elements: Jeffrey & Son's has three types of cost elements that are material,

labour and overhead. Quantity and amount of raw material which have been used in

production process to convert it into finished goods is known as material cost such as cost of

purchasing raw material. However, wages paid by Jeffrey & Son's to their employees is

called labour cost (Weygandt, Kimmel and Kieso, 2015). All the other expenses are known as

overheads such as telephone, office rent, building depreciation, royalty and cost of scrap.

Cost function: On that basis, cost can be classified into various types such as

administration, factory and selling and distribution overheads. In context to Jeffrey & Son's,

office rent, stationery, printing and photocopier charges are the types of administrative cost.

However, factory rent, lighting and energy will be included in factory cost while all the

expenses which have been incurred for selling Exquisite product into the market is known as

selling and distribution overheads (Gibson and Haynes, 2015). For instance, advertisement,

marketing and cost of distributing free samples.

Cost nature: There are two types of cost nature, direct and indirect. Direct cost can be

specifically charged to a specific cost element and cost centre. On contrary, indirect cost

cannot be charged to a specific cost centre or elements. Direct material can be charged to an

specific cost centre and integral part of Exquisite whilst indirect material cost cannot be

directly charged to an individual cost centres (Ward, 2012). For instance, cost of consumable

stores, oil and lubricants are known as indirect material cost. Direct labour can be directly

charged to an individual cost centre and paid to the employees who are involve in Jeffrey &

1 | P a g e

Managers play a crucial role in the business success as they analyse company's

financial performance and take strategic decisions. Management accounting is the process of

preparing managerial reports from financial information, taking effective decisions, ensure

optimum allocation of resources, and manage firm’s operational and financial risk. Jeffrey &

Son's is a manufacturing organization which produces variety of popular and branded

products, called Exquisite. In present project report, various kinds of managerial tools will be

discussed for improving company's performance. The report will describe the significance of

management accounting for cost computation, effective cost management, preparing cost

report, variance analysis and taking corrective actions to eliminate adverse variances.

Moreover, various budgeting techniques will be explained to manage firms operations.

TASK 1

AC 1.1 Cost classification based on element, function, nature and behaviour

Cost elements: Jeffrey & Son's has three types of cost elements that are material,

labour and overhead. Quantity and amount of raw material which have been used in

production process to convert it into finished goods is known as material cost such as cost of

purchasing raw material. However, wages paid by Jeffrey & Son's to their employees is

called labour cost (Weygandt, Kimmel and Kieso, 2015). All the other expenses are known as

overheads such as telephone, office rent, building depreciation, royalty and cost of scrap.

Cost function: On that basis, cost can be classified into various types such as

administration, factory and selling and distribution overheads. In context to Jeffrey & Son's,

office rent, stationery, printing and photocopier charges are the types of administrative cost.

However, factory rent, lighting and energy will be included in factory cost while all the

expenses which have been incurred for selling Exquisite product into the market is known as

selling and distribution overheads (Gibson and Haynes, 2015). For instance, advertisement,

marketing and cost of distributing free samples.

Cost nature: There are two types of cost nature, direct and indirect. Direct cost can be

specifically charged to a specific cost element and cost centre. On contrary, indirect cost

cannot be charged to a specific cost centre or elements. Direct material can be charged to an

specific cost centre and integral part of Exquisite whilst indirect material cost cannot be

directly charged to an individual cost centres (Ward, 2012). For instance, cost of consumable

stores, oil and lubricants are known as indirect material cost. Direct labour can be directly

charged to an individual cost centre and paid to the employees who are involve in Jeffrey &

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Son's manufacturing process. On contrary, indirect cost cannot be charged to an individual

cost centre and employees are not engaged in production process as they only assist other

workers. For instance, Foreman and storekeeper wages and salary of work manager are the

type of indirect labour cost. In addition, direct overhead for Jeffrey & Son's includes hire

charges and cost of defective works whereas indirect overhead includes telephone, stationery

and insurance expenditures.

Cost behaviour: It determines the changes in cost with changing production level at

Jeffrey & Son's. Fixed cost remains unchanged with changing the production or output level

of Jeffrey & Son's. However, Variable cost gets changes with the same direction of

production changes (Demski, 2013). For instance, depreciation and insurance are fixed cost

while material and labour wages are variable cost. Another, semi variable cost get changes

after a specified production limit. For instance, telephone expenditures and electricity bill are

the types of semi-variable cost.

AC 1.2 Computation of total and unit cost for Job no. 444 through using job costing method

Job costing method: It is a costing method which reports about material, labour and

manufacturing overhead assigned to each job (Mishan, 2015). In context to the given

scenario, job cost technique has been implemented to determine job cost of 200 units.

Particular Total Amount (In £)

Material expenses 40000

Labour expenses 54000

Variable production overhead 36000

Total variable cost 130000

Fixed production overhead 24000

Total cost 154000

Working note: 1. Material cost = Material quantity*material price*total units

Material quantity per unit = 50 Kg

Material price per kg = £4 per kg.

Total number of units = 200 units

Material cost = 50 kg*£4 per kg.*200 units = £40000

2 | P a g e

cost centre and employees are not engaged in production process as they only assist other

workers. For instance, Foreman and storekeeper wages and salary of work manager are the

type of indirect labour cost. In addition, direct overhead for Jeffrey & Son's includes hire

charges and cost of defective works whereas indirect overhead includes telephone, stationery

and insurance expenditures.

Cost behaviour: It determines the changes in cost with changing production level at

Jeffrey & Son's. Fixed cost remains unchanged with changing the production or output level

of Jeffrey & Son's. However, Variable cost gets changes with the same direction of

production changes (Demski, 2013). For instance, depreciation and insurance are fixed cost

while material and labour wages are variable cost. Another, semi variable cost get changes

after a specified production limit. For instance, telephone expenditures and electricity bill are

the types of semi-variable cost.

AC 1.2 Computation of total and unit cost for Job no. 444 through using job costing method

Job costing method: It is a costing method which reports about material, labour and

manufacturing overhead assigned to each job (Mishan, 2015). In context to the given

scenario, job cost technique has been implemented to determine job cost of 200 units.

Particular Total Amount (In £)

Material expenses 40000

Labour expenses 54000

Variable production overhead 36000

Total variable cost 130000

Fixed production overhead 24000

Total cost 154000

Working note: 1. Material cost = Material quantity*material price*total units

Material quantity per unit = 50 Kg

Material price per kg = £4 per kg.

Total number of units = 200 units

Material cost = 50 kg*£4 per kg.*200 units = £40000

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Labour cost = Labour hours*labour rate*total number of units

Labour hours = 30 hours per unit

Labour rate = £9 per hour

Labour cost = 30 hours*£9 per hour*200 units = £54000

3. Variable production overhead = Total direct labour hours*overhead rate per hour

Total direct labour hours = 30 hours per unit*200 units = 6000 hours

Variable overhead rate = £6 per hour

Variable production overhead = 6000 hours*£6 per hour = £36000

4. Fixed production overhead for 200 units

= (Total fixed overheads/total budgeted direct labour hours*direct labour hours for 200 units)

Fixed overheads = (£80000)/ (20000 hours)*6000 hours = £24000

5. Cost per unit = Total cost/number of unit produced

Unit cost = £154000/200 units = £77

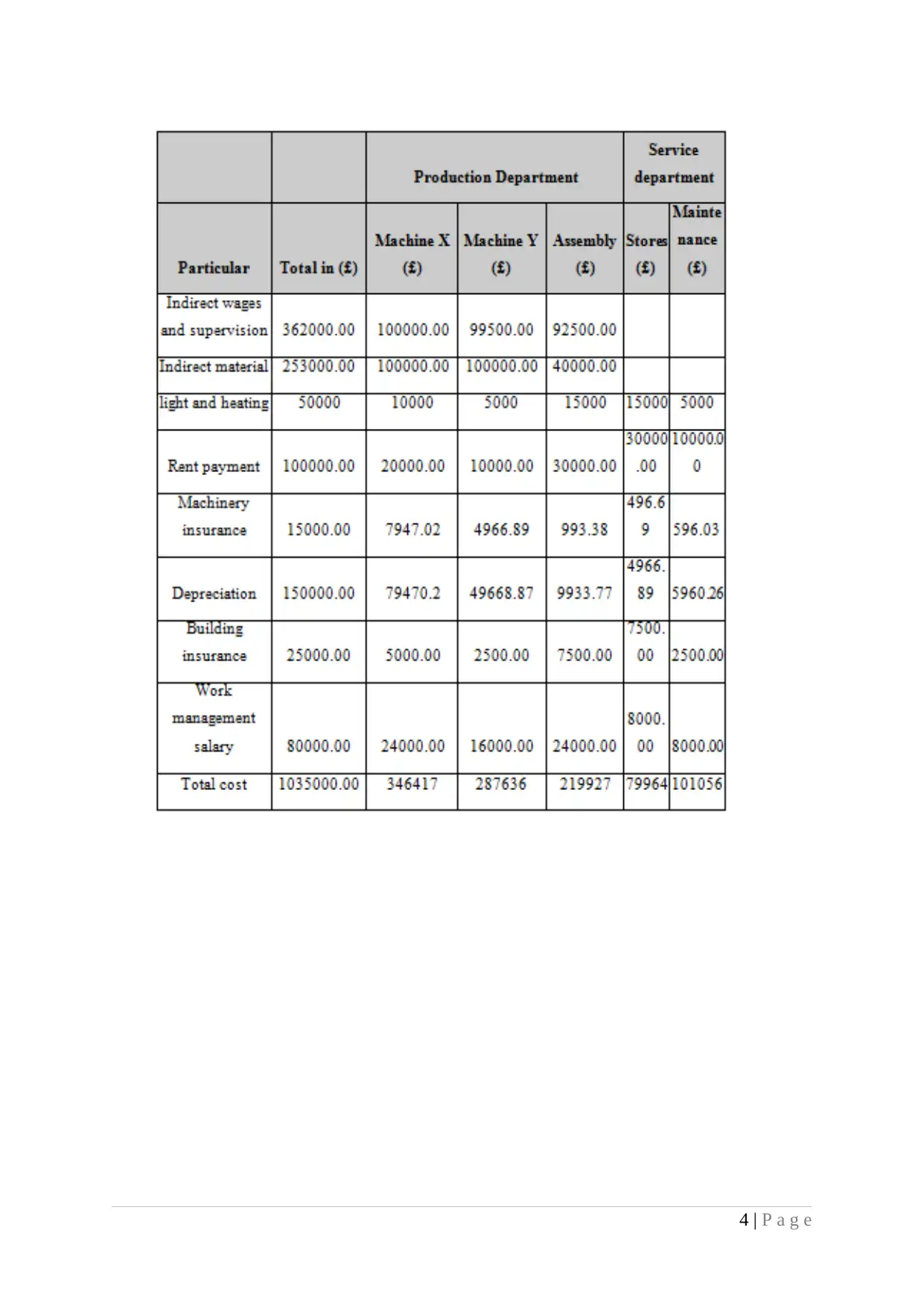

AC 1.3 Determination of cost of Exquisite through using job costing method

a) Allocation and apportionment of overheads to the three production

departments:

3 | P a g e

Labour hours = 30 hours per unit

Labour rate = £9 per hour

Labour cost = 30 hours*£9 per hour*200 units = £54000

3. Variable production overhead = Total direct labour hours*overhead rate per hour

Total direct labour hours = 30 hours per unit*200 units = 6000 hours

Variable overhead rate = £6 per hour

Variable production overhead = 6000 hours*£6 per hour = £36000

4. Fixed production overhead for 200 units

= (Total fixed overheads/total budgeted direct labour hours*direct labour hours for 200 units)

Fixed overheads = (£80000)/ (20000 hours)*6000 hours = £24000

5. Cost per unit = Total cost/number of unit produced

Unit cost = £154000/200 units = £77

AC 1.3 Determination of cost of Exquisite through using job costing method

a) Allocation and apportionment of overheads to the three production

departments:

3 | P a g e

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

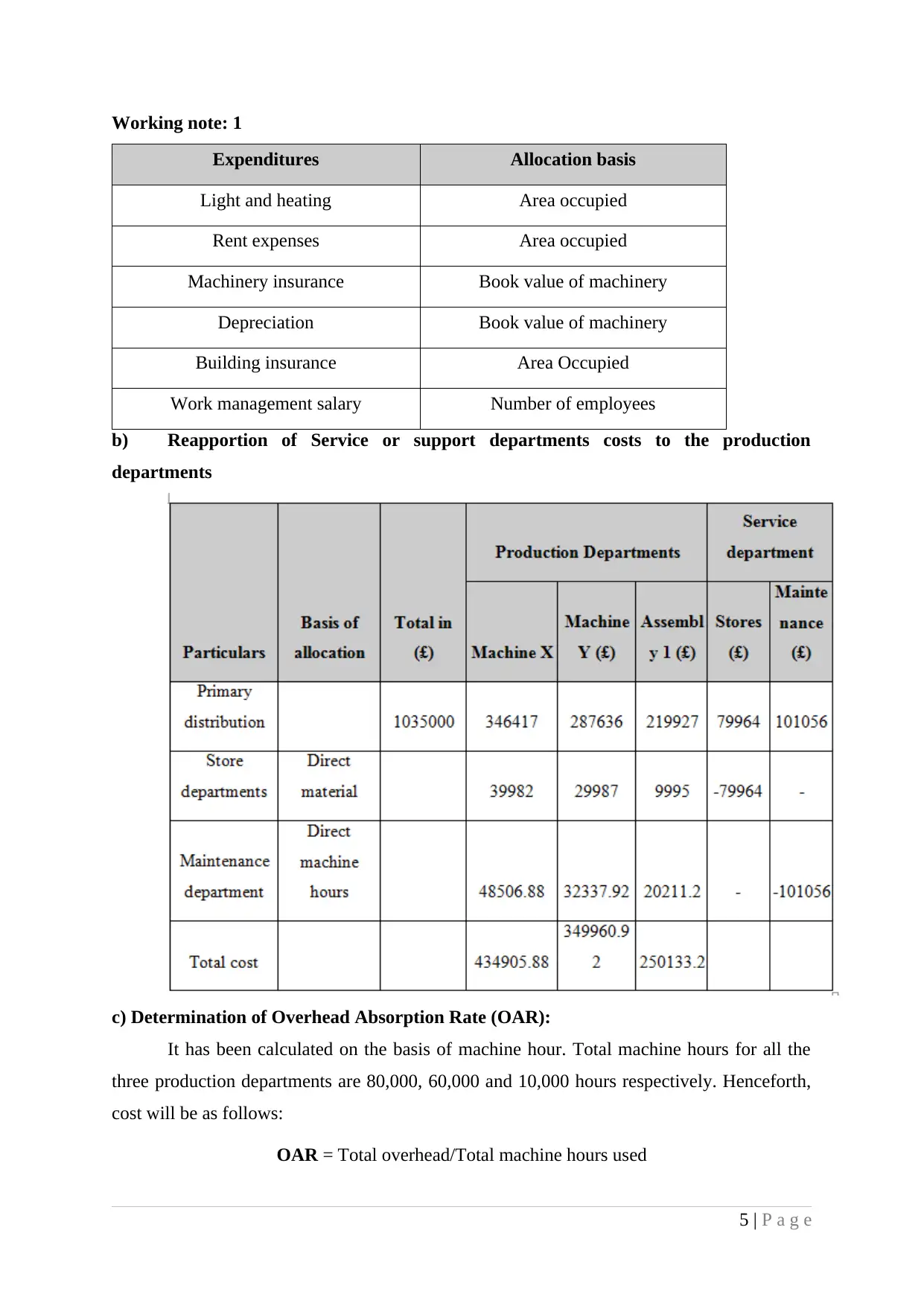

Working note: 1

Expenditures Allocation basis

Light and heating Area occupied

Rent expenses Area occupied

Machinery insurance Book value of machinery

Depreciation Book value of machinery

Building insurance Area Occupied

Work management salary Number of employees

b) Reapportion of Service or support departments costs to the production

departments

c) Determination of Overhead Absorption Rate (OAR):

It has been calculated on the basis of machine hour. Total machine hours for all the

three production departments are 80,000, 60,000 and 10,000 hours respectively. Henceforth,

cost will be as follows:

OAR = Total overhead/Total machine hours used

5 | P a g e

Expenditures Allocation basis

Light and heating Area occupied

Rent expenses Area occupied

Machinery insurance Book value of machinery

Depreciation Book value of machinery

Building insurance Area Occupied

Work management salary Number of employees

b) Reapportion of Service or support departments costs to the production

departments

c) Determination of Overhead Absorption Rate (OAR):

It has been calculated on the basis of machine hour. Total machine hours for all the

three production departments are 80,000, 60,000 and 10,000 hours respectively. Henceforth,

cost will be as follows:

OAR = Total overhead/Total machine hours used

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

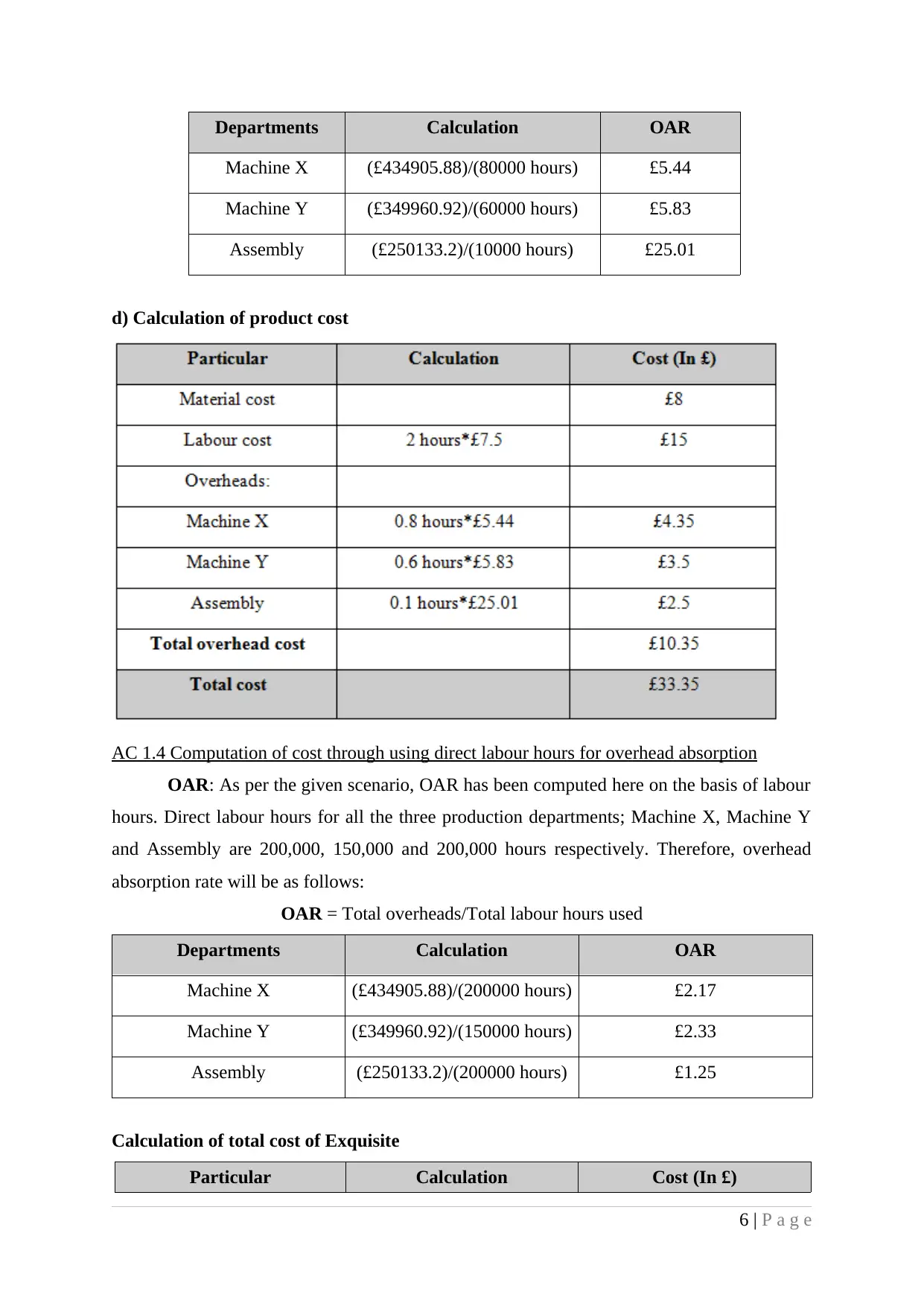

Departments Calculation OAR

Machine X (£434905.88)/(80000 hours) £5.44

Machine Y (£349960.92)/(60000 hours) £5.83

Assembly (£250133.2)/(10000 hours) £25.01

d) Calculation of product cost

AC 1.4 Computation of cost through using direct labour hours for overhead absorption

OAR: As per the given scenario, OAR has been computed here on the basis of labour

hours. Direct labour hours for all the three production departments; Machine X, Machine Y

and Assembly are 200,000, 150,000 and 200,000 hours respectively. Therefore, overhead

absorption rate will be as follows:

OAR = Total overheads/Total labour hours used

Departments Calculation OAR

Machine X (£434905.88)/(200000 hours) £2.17

Machine Y (£349960.92)/(150000 hours) £2.33

Assembly (£250133.2)/(200000 hours) £1.25

Calculation of total cost of Exquisite

Particular Calculation Cost (In £)

6 | P a g e

Machine X (£434905.88)/(80000 hours) £5.44

Machine Y (£349960.92)/(60000 hours) £5.83

Assembly (£250133.2)/(10000 hours) £25.01

d) Calculation of product cost

AC 1.4 Computation of cost through using direct labour hours for overhead absorption

OAR: As per the given scenario, OAR has been computed here on the basis of labour

hours. Direct labour hours for all the three production departments; Machine X, Machine Y

and Assembly are 200,000, 150,000 and 200,000 hours respectively. Therefore, overhead

absorption rate will be as follows:

OAR = Total overheads/Total labour hours used

Departments Calculation OAR

Machine X (£434905.88)/(200000 hours) £2.17

Machine Y (£349960.92)/(150000 hours) £2.33

Assembly (£250133.2)/(200000 hours) £1.25

Calculation of total cost of Exquisite

Particular Calculation Cost (In £)

6 | P a g e

Cost of material £8

Cost of labour 2 hours*£7.5 £15

Overheads:

Machine X 2 hours*£2.17 £4.34

Machine Y 1.5 hours*£2.33 £3.5

Assembly 1 hours*£1.25 £1.25

Total overhead cost £9.09

Total cost £32.09

Interpretation: On the basis of machine hour and labour hour, Machine X and

Machine Y department’s overhead costs are approximately equal to £4.34 and £3.5.

However, Assembly department cost shows a significant difference as it got reduced from

£2.5 to £1.25. In turn, total overhead cost fall by £1.26 to £9.09 and total cost has been

declined from £33.35£ to £32.09. Henceforth, it can be concluded that Jeffrey & Son's has to

use labour hour basis for allocation. The reason behind this is that it is a cost effective method

which reduces Exquisite cost and improves business profits (Shepherd, 2015). Thus, Jeffrey

& Son's can improve their operational performance by using labour hour basis.

TASK 2

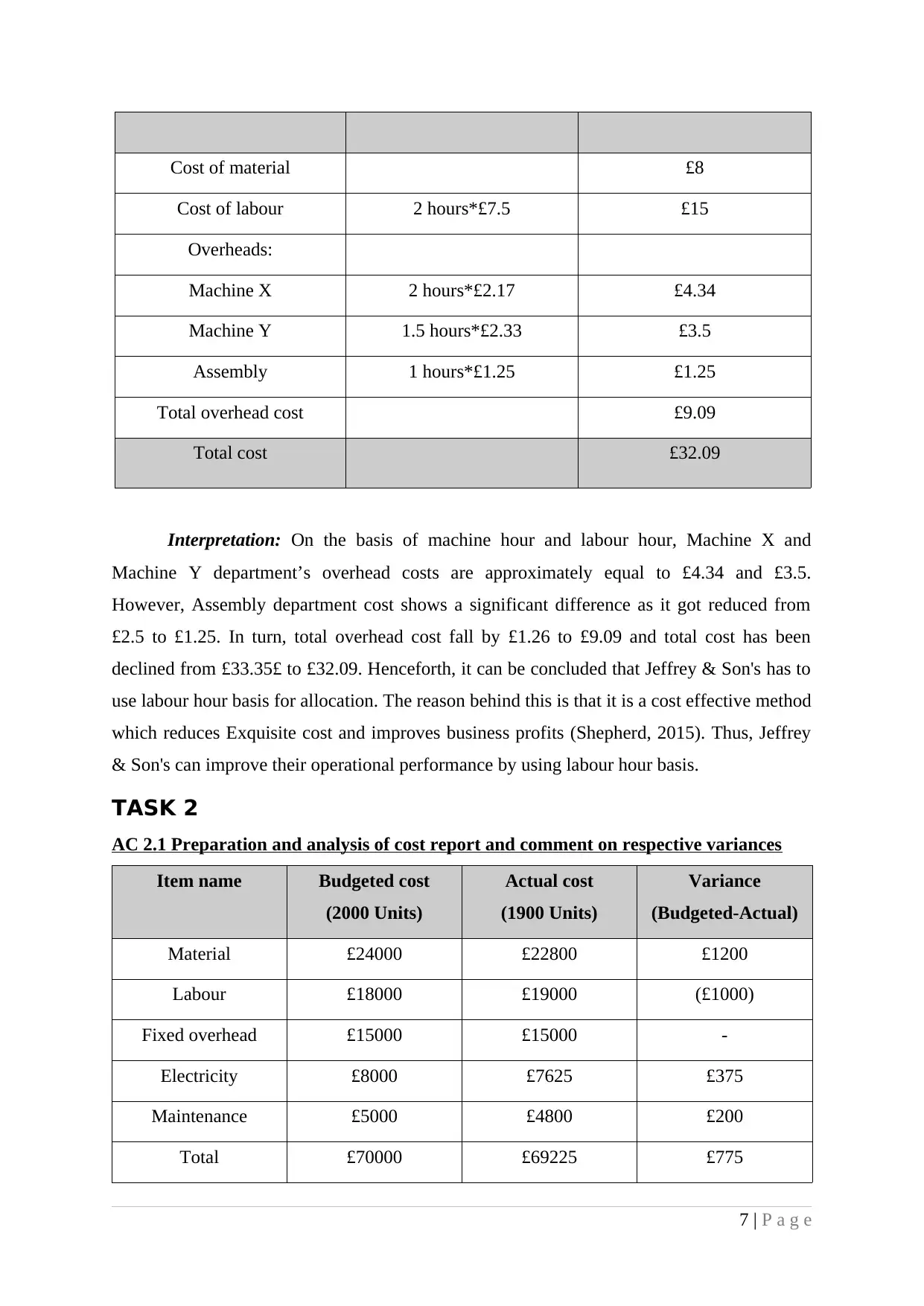

AC 2.1 Preparation and analysis of cost report and comment on respective variances

Item name Budgeted cost

(2000 Units)

Actual cost

(1900 Units)

Variance

(Budgeted-Actual)

Material £24000 £22800 £1200

Labour £18000 £19000 (£1000)

Fixed overhead £15000 £15000 -

Electricity £8000 £7625 £375

Maintenance £5000 £4800 £200

Total £70000 £69225 £775

7 | P a g e

Cost of labour 2 hours*£7.5 £15

Overheads:

Machine X 2 hours*£2.17 £4.34

Machine Y 1.5 hours*£2.33 £3.5

Assembly 1 hours*£1.25 £1.25

Total overhead cost £9.09

Total cost £32.09

Interpretation: On the basis of machine hour and labour hour, Machine X and

Machine Y department’s overhead costs are approximately equal to £4.34 and £3.5.

However, Assembly department cost shows a significant difference as it got reduced from

£2.5 to £1.25. In turn, total overhead cost fall by £1.26 to £9.09 and total cost has been

declined from £33.35£ to £32.09. Henceforth, it can be concluded that Jeffrey & Son's has to

use labour hour basis for allocation. The reason behind this is that it is a cost effective method

which reduces Exquisite cost and improves business profits (Shepherd, 2015). Thus, Jeffrey

& Son's can improve their operational performance by using labour hour basis.

TASK 2

AC 2.1 Preparation and analysis of cost report and comment on respective variances

Item name Budgeted cost

(2000 Units)

Actual cost

(1900 Units)

Variance

(Budgeted-Actual)

Material £24000 £22800 £1200

Labour £18000 £19000 (£1000)

Fixed overhead £15000 £15000 -

Electricity £8000 £7625 £375

Maintenance £5000 £4800 £200

Total £70000 £69225 £775

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working note:

1. Actual cost of material = £12*1900 units = £22800

2. Actual labour cost = £10*1900 units = £19000

3. Actual electricity cost = (£8000*£5000)/ (2000U.-1200U.) = £3.75 per unit'

Fixed = £8000 - (£3.75*2000U.) = £500

Variable = £3.75*1900U. = £7125

Total electricity cost = £7125 + £500 = £7625

4. Maintenance = £5000 - (£1000/500U.*100U.) = £4800

Interpretation: The reason for having favourable material variance is reducing total

production level from 2,000 units to 1,900 units while material price remains fixed to £12.

However, labour cost variance got changed due to increasing piece rate from £9 to £10. This

will impose higher labour cost by £1000. As discussed earlier, fixed cost has no relation with

the production changes hence; it remains fixed to £15000. Moreover, electricity is a semi-

variable cost because it remains fixed up to £500 and after that it got changed with the

production changes. Thus, lower output to 1,900 units is the only reason for declined

electricity cost. However, maintenance is a stepped cost and increase by £1000 for every

additional production of 500 units. In present case, total production got reduced by 100 units

therefore; maintenance cost has been declined by £200. Thus, it can be said that Jeffrey &

Son's management has to enhance its total production. Furthermore, it should employ

workers at lower piece rate which helps to decline total wages payments. It assists managers

to manage company’s operations effectively and achieve its set budgeted targets.

AC 2.2 Performance indicators to determine potential improvement areas

Key Performance Indicators (KPIs) are the best way to measure the areas for making

potential improvement in Jeffrey & Son's. These have been described here as under:

Revenues: Jeffrey & Son’s produces variety of products to generate revenues through

selling them in the market. Therefore, managers have to analyse the changes in revenues over

the period. If Jeffrey & Son's have higher sales, then this will indicate good operational

performance while declined trend in revenues need improvement.

Cost of goods sold: Along with sales, Jeffrey & Son's managers also have to analyse

their product cost. Reasonable increase in cost is quiet good because it is may be due to

higher production and increase in material prices. However, high increase in cost indicates

that management has to make effective control over the cost (Drury, 2013). For instance, high

8 | P a g e

1. Actual cost of material = £12*1900 units = £22800

2. Actual labour cost = £10*1900 units = £19000

3. Actual electricity cost = (£8000*£5000)/ (2000U.-1200U.) = £3.75 per unit'

Fixed = £8000 - (£3.75*2000U.) = £500

Variable = £3.75*1900U. = £7125

Total electricity cost = £7125 + £500 = £7625

4. Maintenance = £5000 - (£1000/500U.*100U.) = £4800

Interpretation: The reason for having favourable material variance is reducing total

production level from 2,000 units to 1,900 units while material price remains fixed to £12.

However, labour cost variance got changed due to increasing piece rate from £9 to £10. This

will impose higher labour cost by £1000. As discussed earlier, fixed cost has no relation with

the production changes hence; it remains fixed to £15000. Moreover, electricity is a semi-

variable cost because it remains fixed up to £500 and after that it got changed with the

production changes. Thus, lower output to 1,900 units is the only reason for declined

electricity cost. However, maintenance is a stepped cost and increase by £1000 for every

additional production of 500 units. In present case, total production got reduced by 100 units

therefore; maintenance cost has been declined by £200. Thus, it can be said that Jeffrey &

Son's management has to enhance its total production. Furthermore, it should employ

workers at lower piece rate which helps to decline total wages payments. It assists managers

to manage company’s operations effectively and achieve its set budgeted targets.

AC 2.2 Performance indicators to determine potential improvement areas

Key Performance Indicators (KPIs) are the best way to measure the areas for making

potential improvement in Jeffrey & Son's. These have been described here as under:

Revenues: Jeffrey & Son’s produces variety of products to generate revenues through

selling them in the market. Therefore, managers have to analyse the changes in revenues over

the period. If Jeffrey & Son's have higher sales, then this will indicate good operational

performance while declined trend in revenues need improvement.

Cost of goods sold: Along with sales, Jeffrey & Son's managers also have to analyse

their product cost. Reasonable increase in cost is quiet good because it is may be due to

higher production and increase in material prices. However, high increase in cost indicates

that management has to make effective control over the cost (Drury, 2013). For instance, high

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

material prices can be reduced through findings new suppliers who supply at cheaper rates.

Profitability: Jeffrey & Son's is a profit earning organization henceforth: it has the

objectives to earn more and more profits. High profitability is a good sign of company's

operational performance while decreased profit margin indicates poor performance. Thus,

mangers have to improve earnings and reduce spending to enhance its overall profit margin.

Product quality: Jeffrey & Son's is a manufacturing firm henceforth; quality is the

most important factor that affects its revenues. It has to provide better quality of products

through quality management techniques otherwise it may lead to fall in revenues (Al-Shuaibi,

Zain and Kassim, 2016).

Customer satisfaction and retention: High customer satisfaction, increase number of

customers and higher retention ratio indicate good performance (Fernández and et.al, 2016).

However, in case of declining consumer satisfaction, Jeffrey & Son's need to focus on it.

They have to determine its causes and eliminate it to enjoy high customer satisfaction.

Qualitative products, affordable prices, price stability make Jeffrey & Son's able to retain

exited consumers and attract new customers.

AC 2.3 Suggestive ways to reduce cost, enhance value and quality

Being a manufacturing company, Jeffrey & Son's incurred variety of expenses which

impose cost to the company. Therefore, it became necessary for Jeffrey & Son's to control

their production cost and attain higher profitability. Variety of material has been available in

the market thus, Jeffrey & Son's has to determine customer demand and select best among

them for production purpose. Moreover, suppliers provide material at different rates so that

Jeffrey & Son's has to find best suppliers whose rate is comparatively cheaper than others

(Crosson, 2013). Another, scrap reduction and waste management also assist in material cost

reduction. On contrary, hiring labour that provides their services at lower rates will help to

reduce labour cost. Moreover, using efficient technology makes Jeffrey & Son's able to

decline their product cost. Along with it, curtailment of unnecessary expenses, effective

control and elimination of undesired product features will provide assistance to control

Exquisite cost. This in turn, company can enhance their profit margin and enjoy success.

Improved business value and quality improvement are the two most essential

elements for successful business. Different strategies can be employed for enhancing Jeffrey

& Son's performance.

9 | P a g e

Profitability: Jeffrey & Son's is a profit earning organization henceforth: it has the

objectives to earn more and more profits. High profitability is a good sign of company's

operational performance while decreased profit margin indicates poor performance. Thus,

mangers have to improve earnings and reduce spending to enhance its overall profit margin.

Product quality: Jeffrey & Son's is a manufacturing firm henceforth; quality is the

most important factor that affects its revenues. It has to provide better quality of products

through quality management techniques otherwise it may lead to fall in revenues (Al-Shuaibi,

Zain and Kassim, 2016).

Customer satisfaction and retention: High customer satisfaction, increase number of

customers and higher retention ratio indicate good performance (Fernández and et.al, 2016).

However, in case of declining consumer satisfaction, Jeffrey & Son's need to focus on it.

They have to determine its causes and eliminate it to enjoy high customer satisfaction.

Qualitative products, affordable prices, price stability make Jeffrey & Son's able to retain

exited consumers and attract new customers.

AC 2.3 Suggestive ways to reduce cost, enhance value and quality

Being a manufacturing company, Jeffrey & Son's incurred variety of expenses which

impose cost to the company. Therefore, it became necessary for Jeffrey & Son's to control

their production cost and attain higher profitability. Variety of material has been available in

the market thus, Jeffrey & Son's has to determine customer demand and select best among

them for production purpose. Moreover, suppliers provide material at different rates so that

Jeffrey & Son's has to find best suppliers whose rate is comparatively cheaper than others

(Crosson, 2013). Another, scrap reduction and waste management also assist in material cost

reduction. On contrary, hiring labour that provides their services at lower rates will help to

reduce labour cost. Moreover, using efficient technology makes Jeffrey & Son's able to

decline their product cost. Along with it, curtailment of unnecessary expenses, effective

control and elimination of undesired product features will provide assistance to control

Exquisite cost. This in turn, company can enhance their profit margin and enjoy success.

Improved business value and quality improvement are the two most essential

elements for successful business. Different strategies can be employed for enhancing Jeffrey

& Son's performance.

9 | P a g e

Sell value not the prices: Jeffrey & Son's has to provide value added products to their

customers so that company can charge premium prices and generate high revenues and

profits.

Diversify customer base: Through diversifying company's customer base, Jeffrey &

Son's can offer its product and services to a large customer base (Wild and Shaw, 2013). This

will contribute to increase its revenues, occupy larger market share and leading position.

Improve strategic capabilities: Skilled and experienced employees, adequate funds,

stabilize prices and sufficient availability of resources help to improve competitive position

and value of Jeffrey & Son's.

Brand loyalty: Through serving qualitative products at reasonable prices and

eliminating customers problems helps to build consumer loyalty. They will prefer only

Exquisite product without comparing it with the others firms offerings and increase business

value.

Increase shareholders wealth: Increasing profitability, shareholders earnings and

providing regular return in way of dividend is another way to enhance Jeffrey & Son's value

to a great extent.

Quality improvement: It can be done through using better quality of material, innovated

technological production process, ensure quality management tools, investment in training,

establishing goals and improving workers performance.

TASK 3

AC 3.1 Purpose and nature of budgeting process to Jeffrey & Son's budget holders

Nature: Budget is a financial monetary tool and a summarized statement of forecasted

future revenues and expenditures. Jeffrey and Sons manager estimate their potential incomes

and payments in future context. Estimation of revenues includes sales forecasting while

expenditures include purchase, wages, fixed and variable overhead forecasting. Thereafter,

net cash flow will be determined through identifying the difference between revenues and

payments (Ibrahim, 2015). Surplus indicates that revenues are higher whereas deficit will be

arising in case of higher payments. Thereafter, closing cash balance will be determined

through adding opening cash balance to the net cash flow.

Purpose: Jeffrey & Son's prepare budget to control its payments and maximize their

revenues. Another purpose is to have adequate surplus cash available to support its daily

functions. These monetary tools provide assistance to establish effective financial control. It

10 | P a g e

customers so that company can charge premium prices and generate high revenues and

profits.

Diversify customer base: Through diversifying company's customer base, Jeffrey &

Son's can offer its product and services to a large customer base (Wild and Shaw, 2013). This

will contribute to increase its revenues, occupy larger market share and leading position.

Improve strategic capabilities: Skilled and experienced employees, adequate funds,

stabilize prices and sufficient availability of resources help to improve competitive position

and value of Jeffrey & Son's.

Brand loyalty: Through serving qualitative products at reasonable prices and

eliminating customers problems helps to build consumer loyalty. They will prefer only

Exquisite product without comparing it with the others firms offerings and increase business

value.

Increase shareholders wealth: Increasing profitability, shareholders earnings and

providing regular return in way of dividend is another way to enhance Jeffrey & Son's value

to a great extent.

Quality improvement: It can be done through using better quality of material, innovated

technological production process, ensure quality management tools, investment in training,

establishing goals and improving workers performance.

TASK 3

AC 3.1 Purpose and nature of budgeting process to Jeffrey & Son's budget holders

Nature: Budget is a financial monetary tool and a summarized statement of forecasted

future revenues and expenditures. Jeffrey and Sons manager estimate their potential incomes

and payments in future context. Estimation of revenues includes sales forecasting while

expenditures include purchase, wages, fixed and variable overhead forecasting. Thereafter,

net cash flow will be determined through identifying the difference between revenues and

payments (Ibrahim, 2015). Surplus indicates that revenues are higher whereas deficit will be

arising in case of higher payments. Thereafter, closing cash balance will be determined

through adding opening cash balance to the net cash flow.

Purpose: Jeffrey & Son's prepare budget to control its payments and maximize their

revenues. Another purpose is to have adequate surplus cash available to support its daily

functions. These monetary tools provide assistance to establish effective financial control. It

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.