Statistics Report

VerifiedAdded on 2019/10/30

|23

|2647

|186

Report

AI Summary

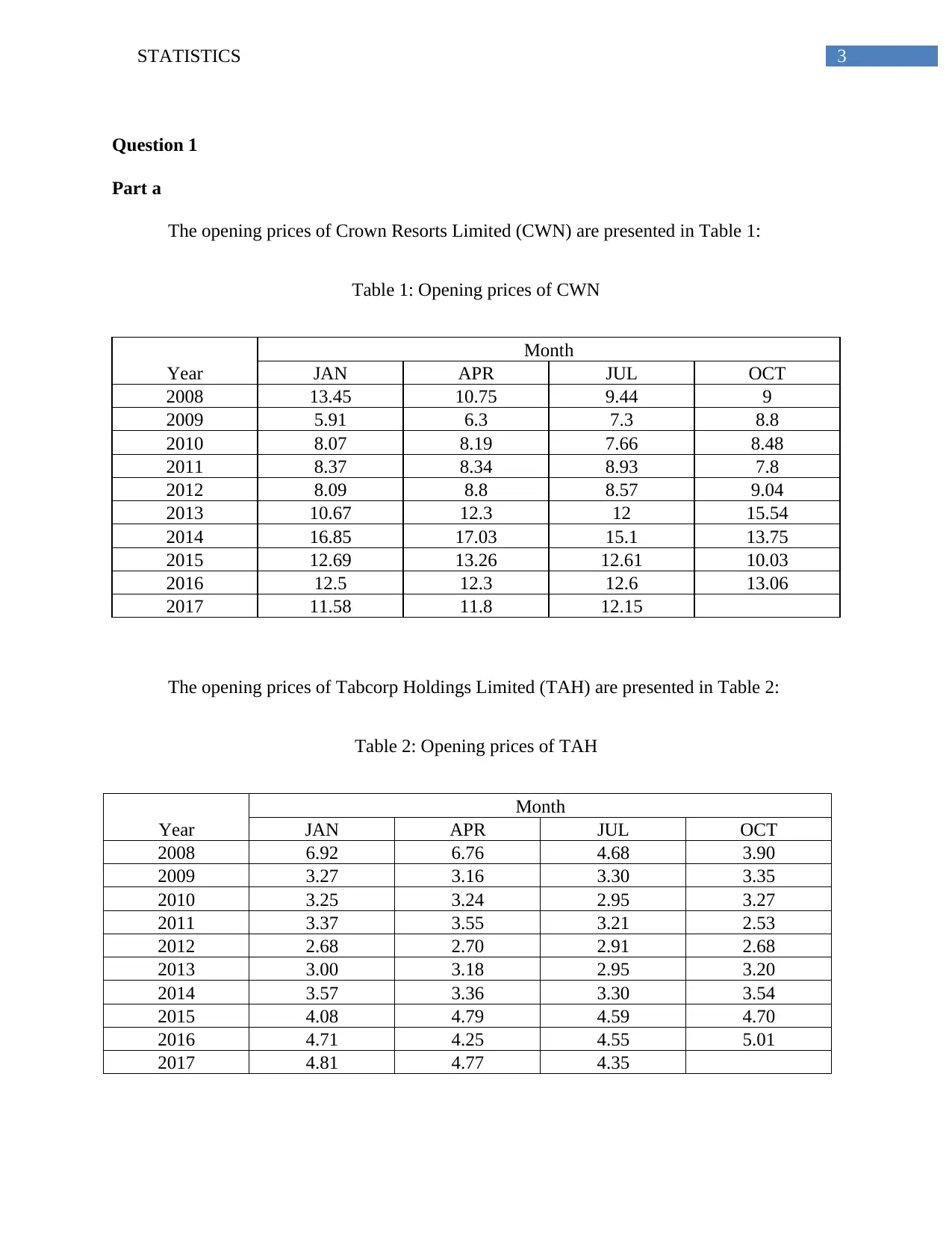

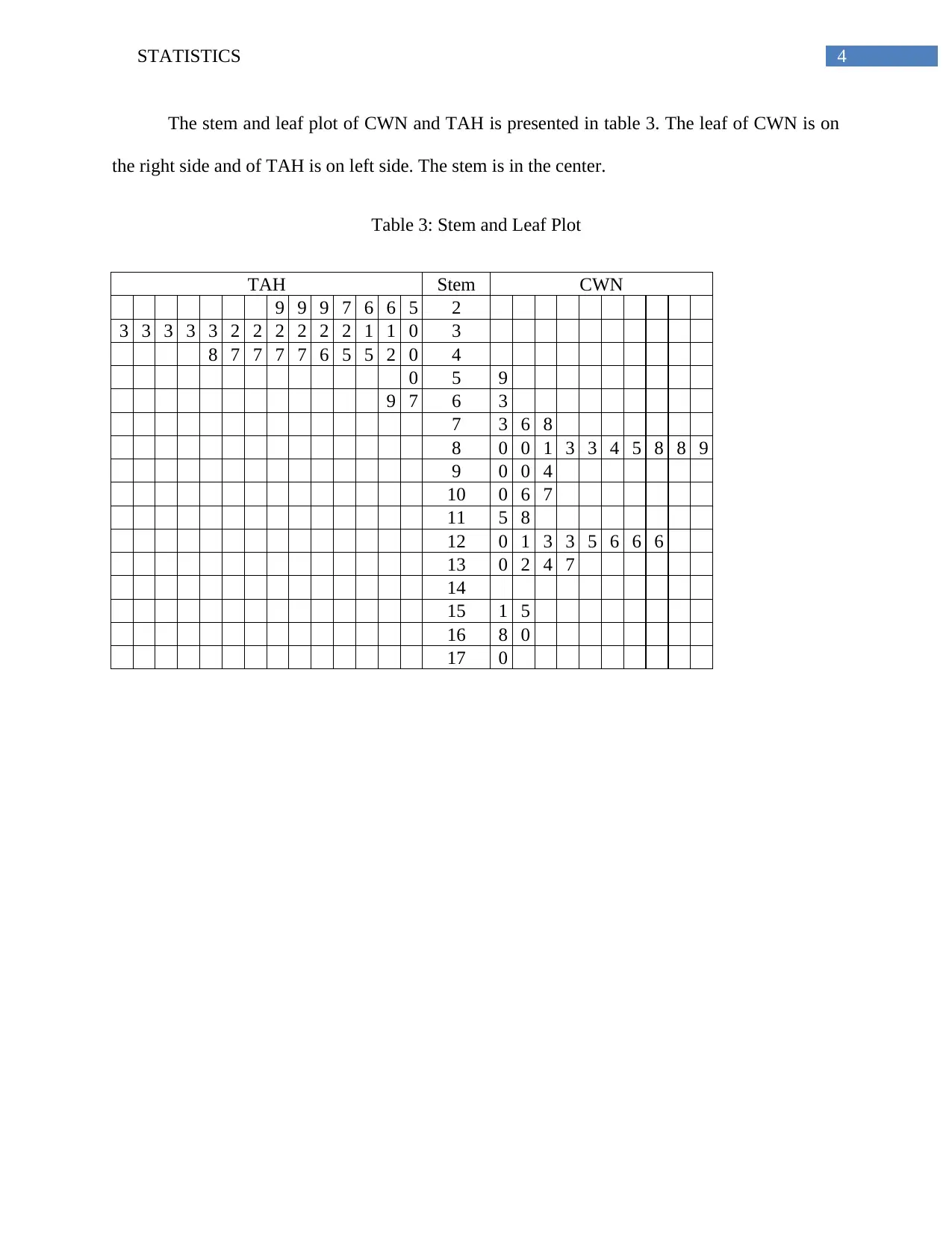

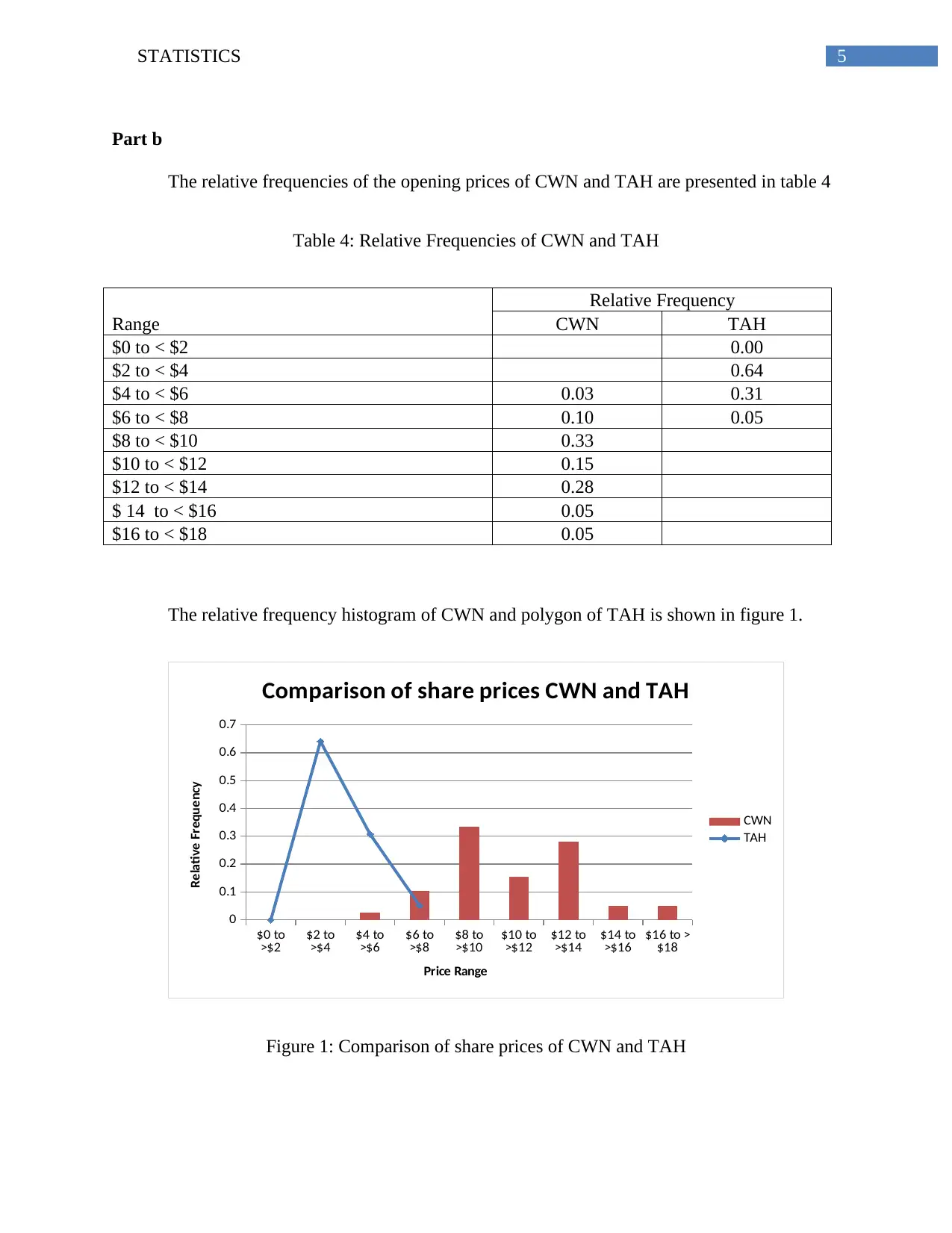

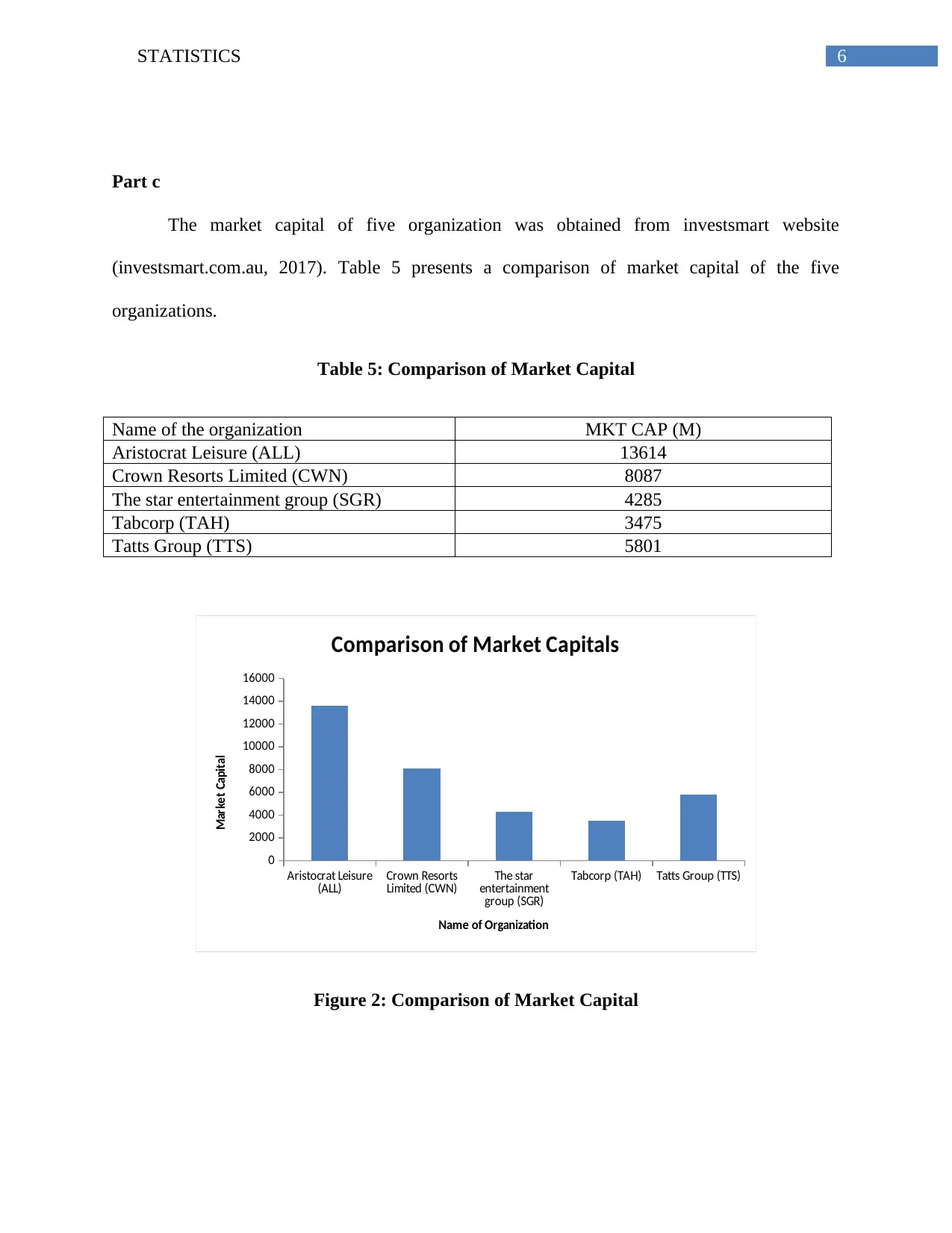

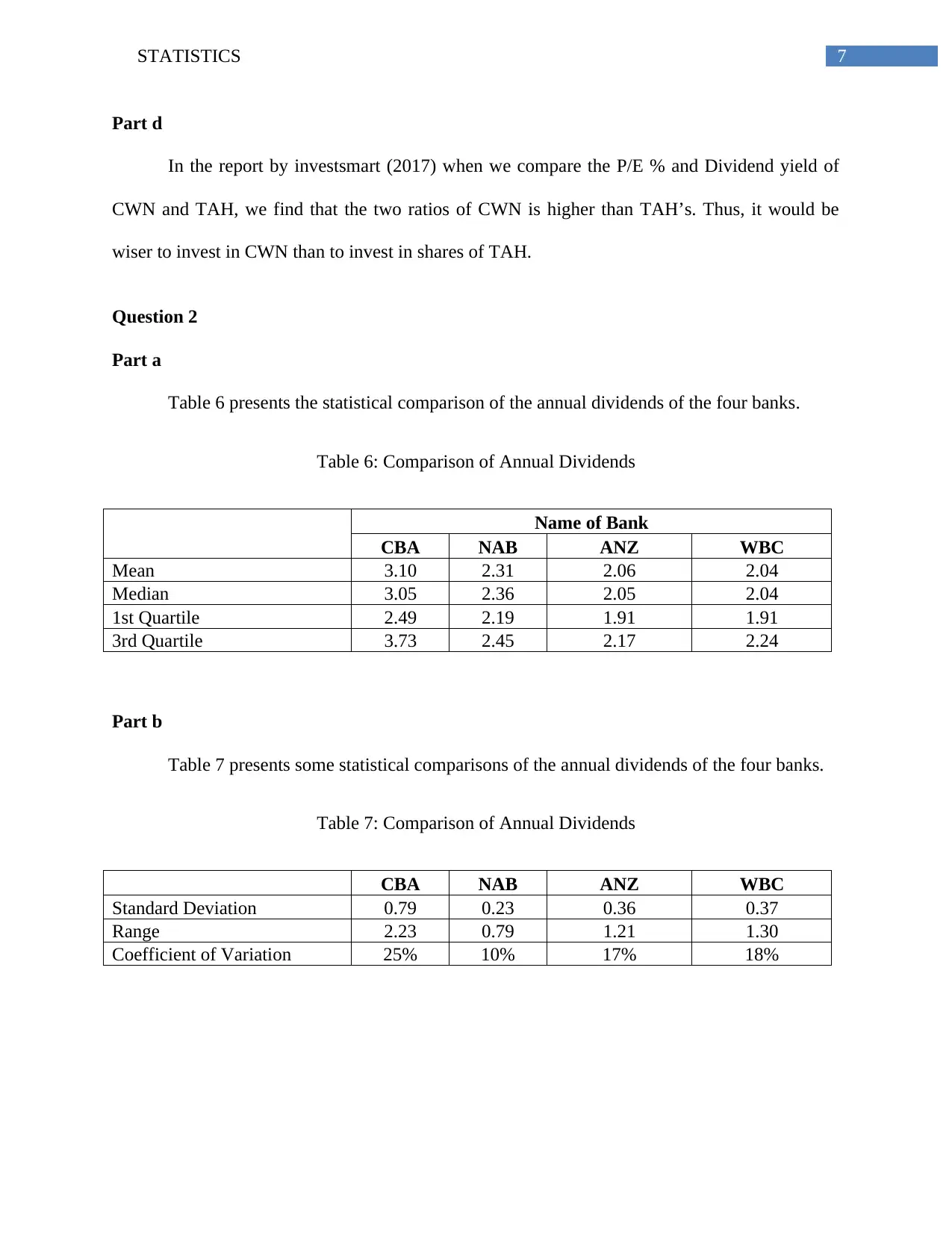

This statistics report presents a comprehensive analysis of financial data, encompassing various statistical techniques. The report begins by examining the opening prices of Crown Resorts Limited (CWN) and Tabcorp Holdings Limited (TAH), utilizing stem-and-leaf plots and relative frequency histograms to compare their share prices. Further analysis involves comparing the market capital of five organizations and evaluating investment strategies based on P/E ratios and dividend yields. The report then shifts focus to a statistical comparison of annual dividends from four Australian banks, employing descriptive statistics and visualizations to highlight key differences. A detailed analysis of ATAR scores for Australian students across different fields of study is also included, along with probability calculations based on rainfall data from Adelaide Airport. Finally, the report investigates bankruptcy prediction using multiple regression analysis, examining the normality of predictors, constructing confidence intervals, and performing hypothesis tests to determine statistically significant differences between bankrupt and non-bankrupt firms. The report concludes by identifying key factors that can predict bankruptcy.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.