Cost Management and Sustainability Analysis

VerifiedAdded on 2020/07/22

|22

|5695

|31

AI Summary

This assignment involves a detailed analysis of cost management strategies for QPT Ltd. The report explores the concept of target costing, its importance in making pricing decisions, and its application in reducing costs. Additionally, it examines life cycle budgeting, which is essential for making optimum use of financial resources. The report also discusses the significance of efficiency and pro-activity phases of sustainability in reducing costs and building a strong image among stakeholders. Furthermore, it evaluates alternatives for QPT Ltd, including the replacement of halogen with LED bulbs to save energy and expenses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Strategic Applications of Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

CASE STUDY 1..............................................................................................................................1

1. Assessing the pricing strategy that HWL need to adopt from 2019 to 2021...........................1

2. Calculating target cost per unit of RayHot on the basis of required profit margin on sales

@20%..........................................................................................................................................2

3. Computing total cost per unit..................................................................................................2

4. Comparing target cost per unit with total cost PU...................................................................3

a....................................................................................................................................................3

b...................................................................................................................................................4

c....................................................................................................................................................4

5. Preparing life cycle budget for RayHot from 2018 to 2022....................................................4

A. On the basis of data given in table 1, 2 and 3.........................................................................4

b. As per data given in table 1 and target requirements of 4(a)...................................................5

c. Performing NPV analysis considering the table 4...................................................................5

CASE STUDY 2..............................................................................................................................5

1. Evaluating trial cost saving rewards system in the context of ATL........................................5

2. Identifying the extent to which team based cost saving measures help in evaluating

performance and awarding bonus................................................................................................6

3. Assessing cost saving performance measures and other forms of incentive scheme..............7

4...................................................................................................................................................7

a....................................................................................................................................................7

B...................................................................................................................................................7

5...................................................................................................................................................8

a....................................................................................................................................................8

INTRODUCTION...........................................................................................................................1

CASE STUDY 1..............................................................................................................................1

1. Assessing the pricing strategy that HWL need to adopt from 2019 to 2021...........................1

2. Calculating target cost per unit of RayHot on the basis of required profit margin on sales

@20%..........................................................................................................................................2

3. Computing total cost per unit..................................................................................................2

4. Comparing target cost per unit with total cost PU...................................................................3

a....................................................................................................................................................3

b...................................................................................................................................................4

c....................................................................................................................................................4

5. Preparing life cycle budget for RayHot from 2018 to 2022....................................................4

A. On the basis of data given in table 1, 2 and 3.........................................................................4

b. As per data given in table 1 and target requirements of 4(a)...................................................5

c. Performing NPV analysis considering the table 4...................................................................5

CASE STUDY 2..............................................................................................................................5

1. Evaluating trial cost saving rewards system in the context of ATL........................................5

2. Identifying the extent to which team based cost saving measures help in evaluating

performance and awarding bonus................................................................................................6

3. Assessing cost saving performance measures and other forms of incentive scheme..............7

4...................................................................................................................................................7

a....................................................................................................................................................7

B...................................................................................................................................................7

5...................................................................................................................................................8

a....................................................................................................................................................8

b...................................................................................................................................................9

c....................................................................................................................................................9

CASE STUDY 3..............................................................................................................................9

1. Determining annual electricity cost for QPT Ltd that is associated with the heating of water

at 70 degree temperature..............................................................................................................9

2. Calculating saving amount in dollar if lower temperature is used such as 60 degree...........10

3. Computing electricity cost at both 70 and 60 degree when water flow decreased from 12 to

6 minutes....................................................................................................................................12

4. Computation of energy cost saving.......................................................................................14

5. Calculating annual lighting cost for the QPT........................................................................14

6. Assessing saving amount if QPT will replace 80Watt Halogen bulbs with 20 Watt LED’s.15

7. Providing recommendations to the managing director of QPT Ltd......................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

c....................................................................................................................................................9

CASE STUDY 3..............................................................................................................................9

1. Determining annual electricity cost for QPT Ltd that is associated with the heating of water

at 70 degree temperature..............................................................................................................9

2. Calculating saving amount in dollar if lower temperature is used such as 60 degree...........10

3. Computing electricity cost at both 70 and 60 degree when water flow decreased from 12 to

6 minutes....................................................................................................................................12

4. Computation of energy cost saving.......................................................................................14

5. Calculating annual lighting cost for the QPT........................................................................14

6. Assessing saving amount if QPT will replace 80Watt Halogen bulbs with 20 Watt LED’s.15

7. Providing recommendations to the managing director of QPT Ltd......................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

In the recent times, business units lay high level of emphasis on undertaking the tools and

techniques of management accounting for the purpose of decision making. Moreover, by

applying the tools of management accounting manager of the firm can make proper forecast of

sales, cost and price etc. This in turn provides high level of assistance to the management team of

firm in setting suitable budgeting framework for the future or specific time frame. Hence, by

using such budgeting framework manager can compare actual performance and thereby would

become able to find out the deviations. In this way, techniques of management accounting gives

indication for the areas that need improvement and meanwhile aid in the success of firm.

The present report is based on different case situations which will develop understanding

about the aspect of target costing. Besides this, it will shed light on the manner through which

unit cost of per unit can be assessed. It also depicts how techniques of investment appraisal help

in making selection of suitable proposal over others. Further, it will also describe various types

of performance measures that can be used within the organization.

CASE STUDY 1

1. Assessing the pricing strategy that HWL need to adopt from 2019 to 2021

There are different types of pricing strategies that can be employed by HWL such as

penetration, competitive and cost plus pricing etc. Thus, out of such pricing strategies firm

should lay greater emphasis on undertaking competitive pricing strategy. The rationale behind

this, usually customers make comparison of price with quality aspect. In this regard, by setting

competitive prices HWL would become able to attract more customers. On the other side,

business unit can also employ cost plus pricing strategy which in enables it to attain desired

margin. On the basis of cited case situation, HWL wishes to earn 20% profit margin by selling

In the recent times, business units lay high level of emphasis on undertaking the tools and

techniques of management accounting for the purpose of decision making. Moreover, by

applying the tools of management accounting manager of the firm can make proper forecast of

sales, cost and price etc. This in turn provides high level of assistance to the management team of

firm in setting suitable budgeting framework for the future or specific time frame. Hence, by

using such budgeting framework manager can compare actual performance and thereby would

become able to find out the deviations. In this way, techniques of management accounting gives

indication for the areas that need improvement and meanwhile aid in the success of firm.

The present report is based on different case situations which will develop understanding

about the aspect of target costing. Besides this, it will shed light on the manner through which

unit cost of per unit can be assessed. It also depicts how techniques of investment appraisal help

in making selection of suitable proposal over others. Further, it will also describe various types

of performance measures that can be used within the organization.

CASE STUDY 1

1. Assessing the pricing strategy that HWL need to adopt from 2019 to 2021

There are different types of pricing strategies that can be employed by HWL such as

penetration, competitive and cost plus pricing etc. Thus, out of such pricing strategies firm

should lay greater emphasis on undertaking competitive pricing strategy. The rationale behind

this, usually customers make comparison of price with quality aspect. In this regard, by setting

competitive prices HWL would become able to attract more customers. On the other side,

business unit can also employ cost plus pricing strategy which in enables it to attain desired

margin. On the basis of cited case situation, HWL wishes to earn 20% profit margin by selling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

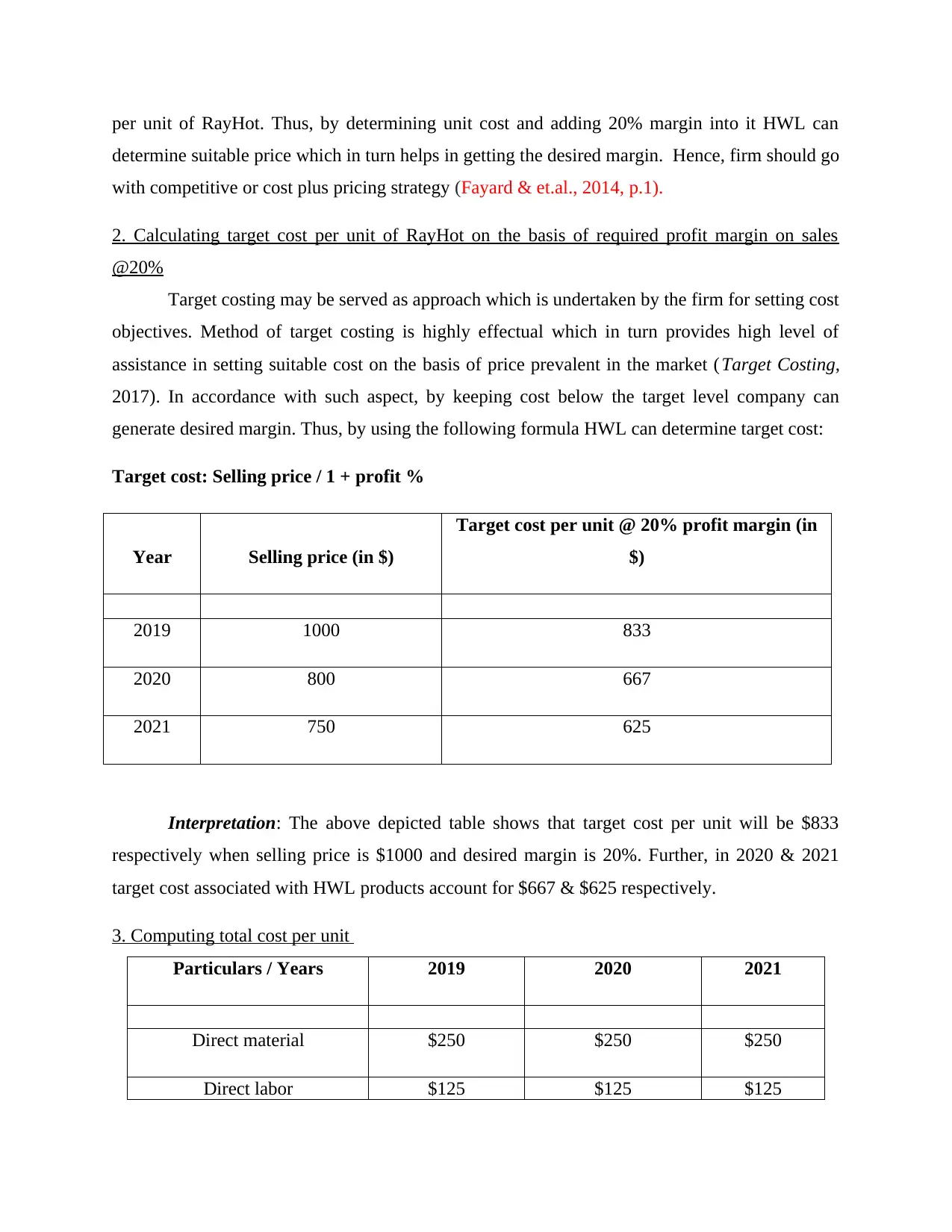

per unit of RayHot. Thus, by determining unit cost and adding 20% margin into it HWL can

determine suitable price which in turn helps in getting the desired margin. Hence, firm should go

with competitive or cost plus pricing strategy (Fayard & et.al., 2014, p.1).

2. Calculating target cost per unit of RayHot on the basis of required profit margin on sales

@20%

Target costing may be served as approach which is undertaken by the firm for setting cost

objectives. Method of target costing is highly effectual which in turn provides high level of

assistance in setting suitable cost on the basis of price prevalent in the market (Target Costing,

2017). In accordance with such aspect, by keeping cost below the target level company can

generate desired margin. Thus, by using the following formula HWL can determine target cost:

Target cost: Selling price / 1 + profit %

Year Selling price (in $)

Target cost per unit @ 20% profit margin (in

$)

2019 1000 833

2020 800 667

2021 750 625

Interpretation: The above depicted table shows that target cost per unit will be $833

respectively when selling price is $1000 and desired margin is 20%. Further, in 2020 & 2021

target cost associated with HWL products account for $667 & $625 respectively.

3. Computing total cost per unit

Particulars / Years 2019 2020 2021

Direct material $250 $250 $250

Direct labor $125 $125 $125

determine suitable price which in turn helps in getting the desired margin. Hence, firm should go

with competitive or cost plus pricing strategy (Fayard & et.al., 2014, p.1).

2. Calculating target cost per unit of RayHot on the basis of required profit margin on sales

@20%

Target costing may be served as approach which is undertaken by the firm for setting cost

objectives. Method of target costing is highly effectual which in turn provides high level of

assistance in setting suitable cost on the basis of price prevalent in the market (Target Costing,

2017). In accordance with such aspect, by keeping cost below the target level company can

generate desired margin. Thus, by using the following formula HWL can determine target cost:

Target cost: Selling price / 1 + profit %

Year Selling price (in $)

Target cost per unit @ 20% profit margin (in

$)

2019 1000 833

2020 800 667

2021 750 625

Interpretation: The above depicted table shows that target cost per unit will be $833

respectively when selling price is $1000 and desired margin is 20%. Further, in 2020 & 2021

target cost associated with HWL products account for $667 & $625 respectively.

3. Computing total cost per unit

Particulars / Years 2019 2020 2021

Direct material $250 $250 $250

Direct labor $125 $125 $125

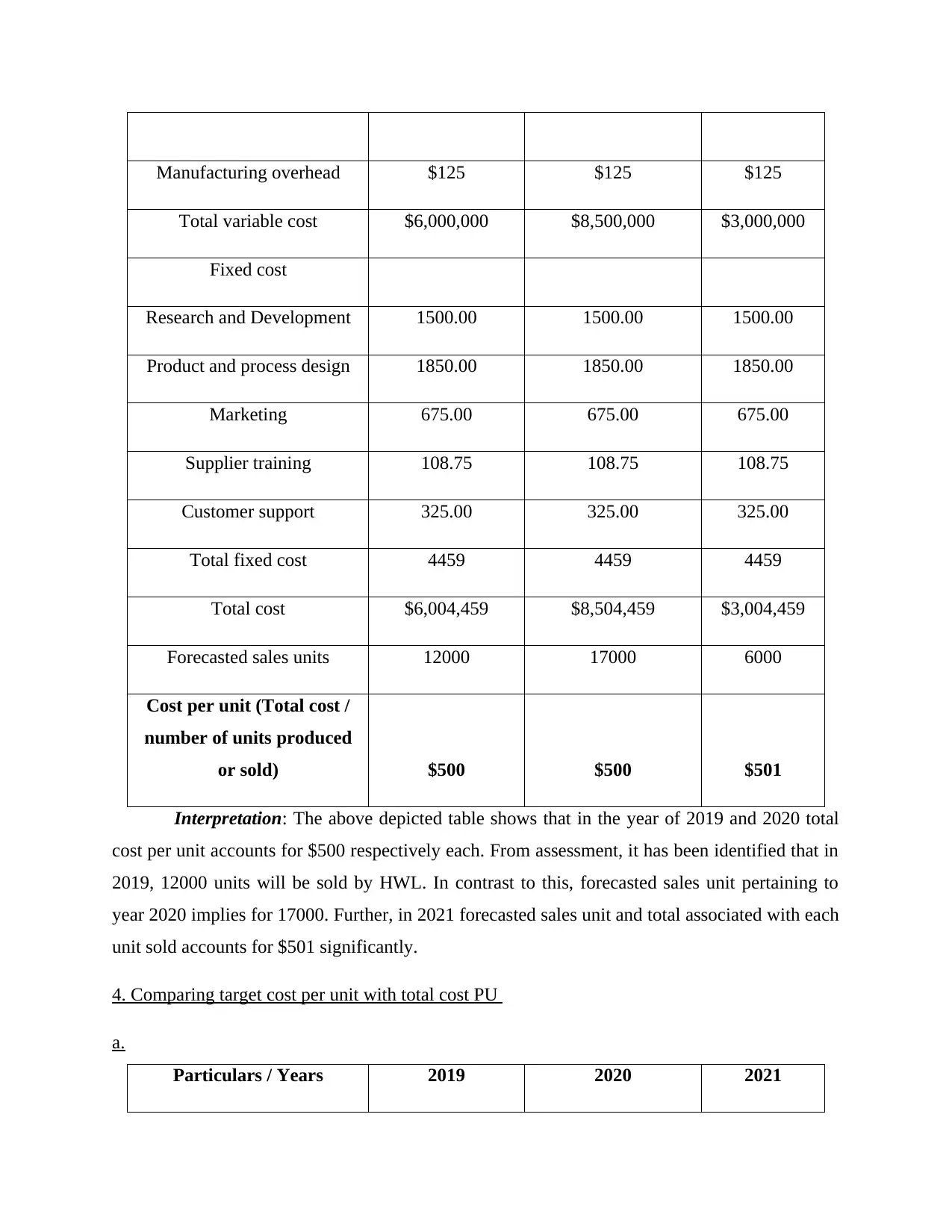

Manufacturing overhead $125 $125 $125

Total variable cost $6,000,000 $8,500,000 $3,000,000

Fixed cost

Research and Development 1500.00 1500.00 1500.00

Product and process design 1850.00 1850.00 1850.00

Marketing 675.00 675.00 675.00

Supplier training 108.75 108.75 108.75

Customer support 325.00 325.00 325.00

Total fixed cost 4459 4459 4459

Total cost $6,004,459 $8,504,459 $3,004,459

Forecasted sales units 12000 17000 6000

Cost per unit (Total cost /

number of units produced

or sold) $500 $500 $501

Interpretation: The above depicted table shows that in the year of 2019 and 2020 total

cost per unit accounts for $500 respectively each. From assessment, it has been identified that in

2019, 12000 units will be sold by HWL. In contrast to this, forecasted sales unit pertaining to

year 2020 implies for 17000. Further, in 2021 forecasted sales unit and total associated with each

unit sold accounts for $501 significantly.

4. Comparing target cost per unit with total cost PU

a.

Particulars / Years 2019 2020 2021

Total variable cost $6,000,000 $8,500,000 $3,000,000

Fixed cost

Research and Development 1500.00 1500.00 1500.00

Product and process design 1850.00 1850.00 1850.00

Marketing 675.00 675.00 675.00

Supplier training 108.75 108.75 108.75

Customer support 325.00 325.00 325.00

Total fixed cost 4459 4459 4459

Total cost $6,004,459 $8,504,459 $3,004,459

Forecasted sales units 12000 17000 6000

Cost per unit (Total cost /

number of units produced

or sold) $500 $500 $501

Interpretation: The above depicted table shows that in the year of 2019 and 2020 total

cost per unit accounts for $500 respectively each. From assessment, it has been identified that in

2019, 12000 units will be sold by HWL. In contrast to this, forecasted sales unit pertaining to

year 2020 implies for 17000. Further, in 2021 forecasted sales unit and total associated with each

unit sold accounts for $501 significantly.

4. Comparing target cost per unit with total cost PU

a.

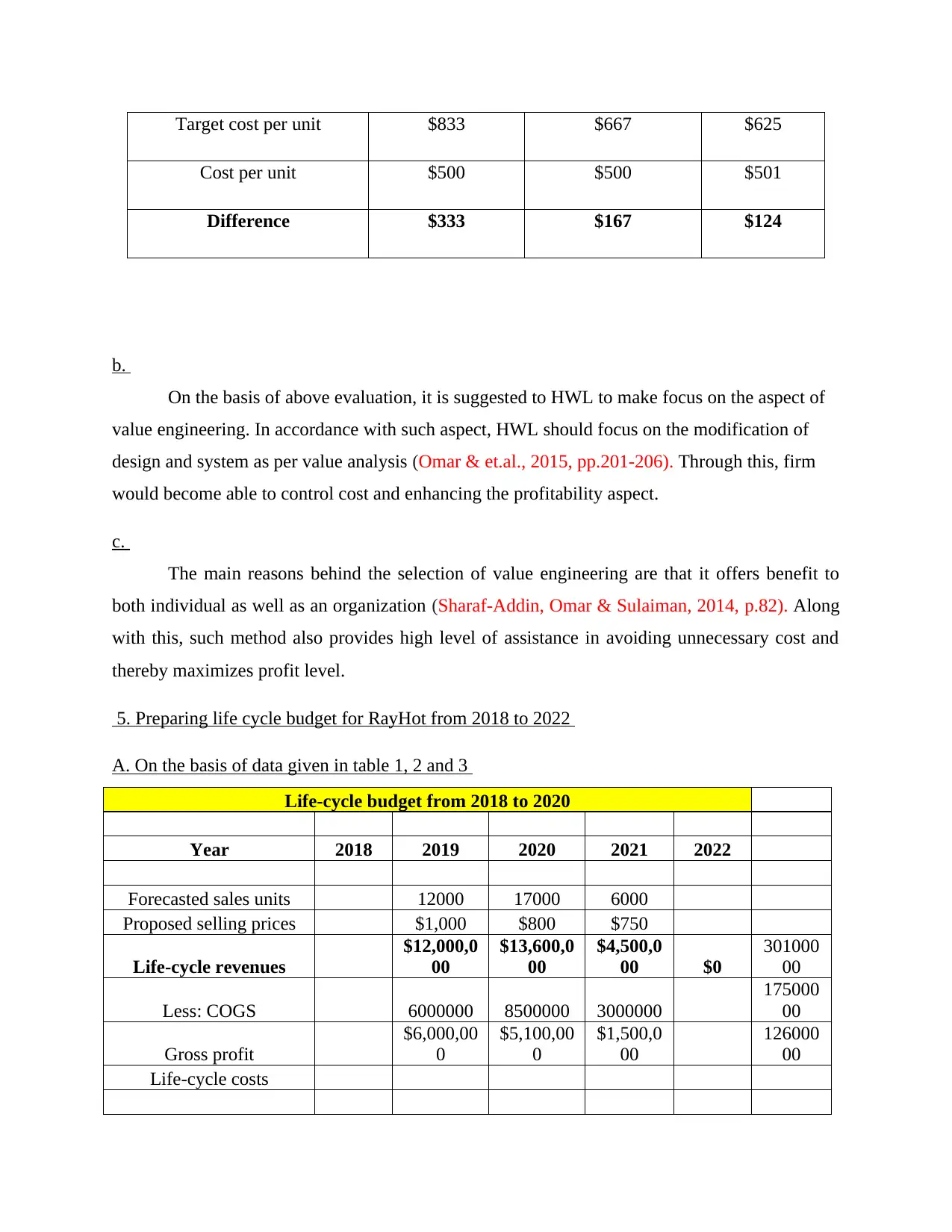

Particulars / Years 2019 2020 2021

Target cost per unit $833 $667 $625

Cost per unit $500 $500 $501

Difference $333 $167 $124

b.

On the basis of above evaluation, it is suggested to HWL to make focus on the aspect of

value engineering. In accordance with such aspect, HWL should focus on the modification of

design and system as per value analysis (Omar & et.al., 2015, pp.201-206). Through this, firm

would become able to control cost and enhancing the profitability aspect.

c.

The main reasons behind the selection of value engineering are that it offers benefit to

both individual as well as an organization (Sharaf-Addin, Omar & Sulaiman, 2014, p.82). Along

with this, such method also provides high level of assistance in avoiding unnecessary cost and

thereby maximizes profit level.

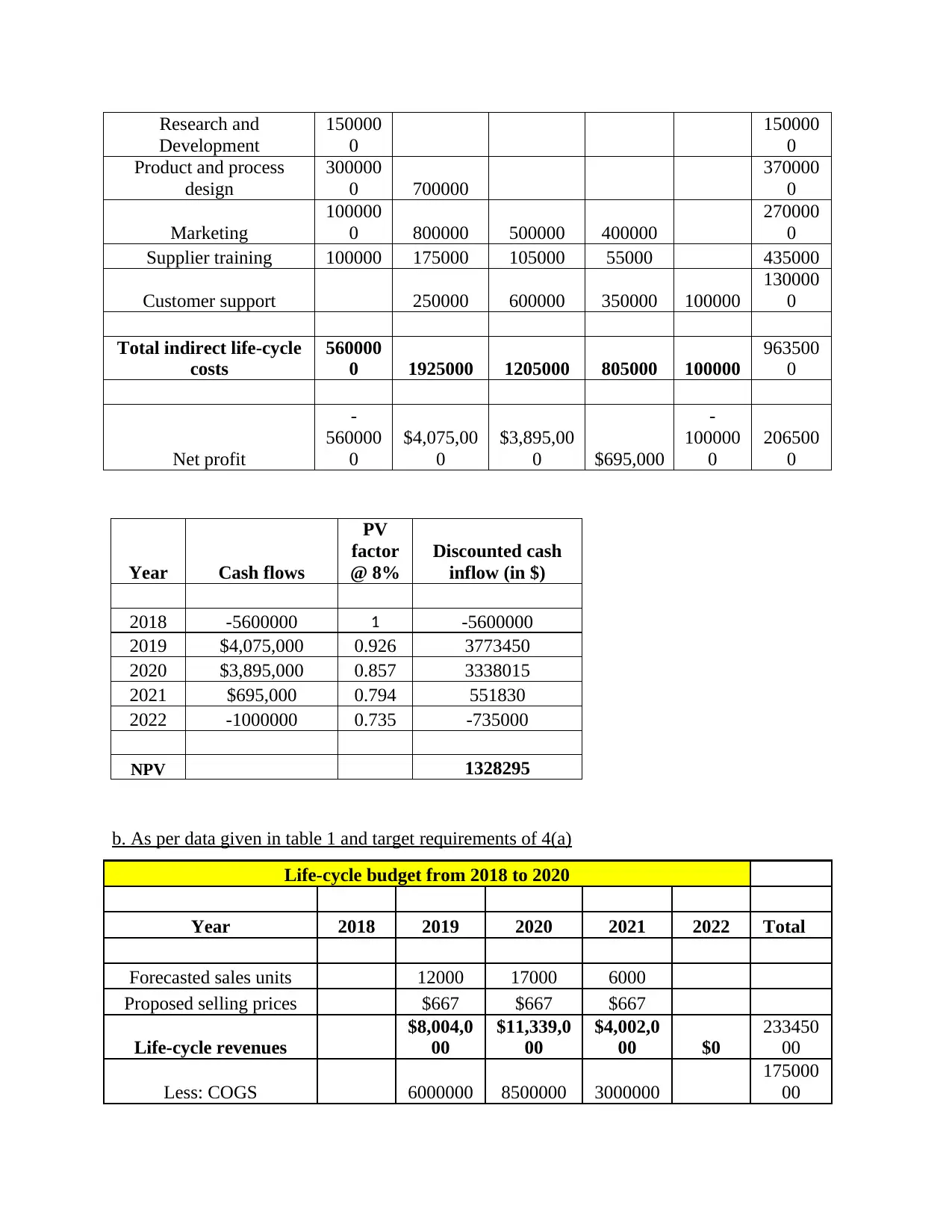

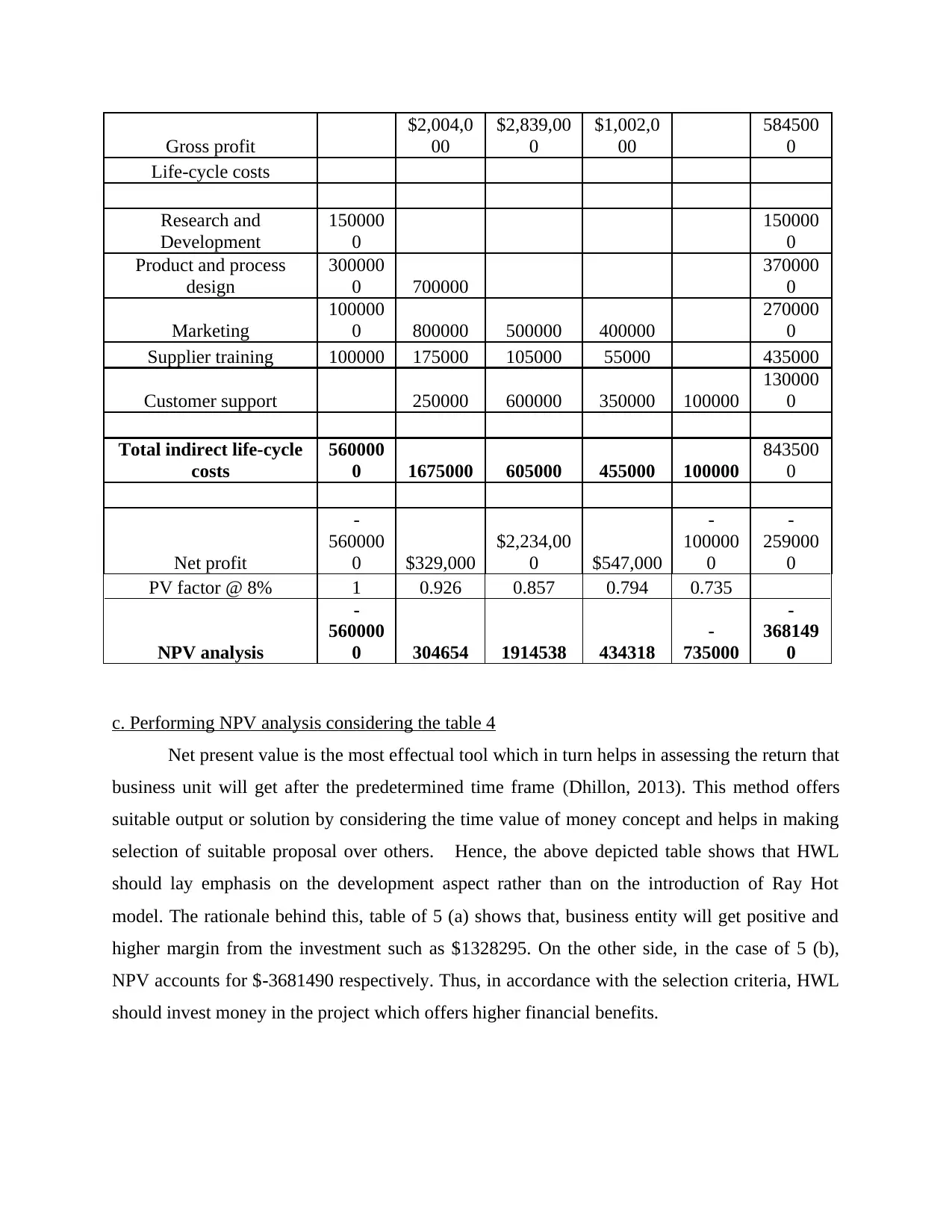

5. Preparing life cycle budget for RayHot from 2018 to 2022

A. On the basis of data given in table 1, 2 and 3

Life-cycle budget from 2018 to 2020

Year 2018 2019 2020 2021 2022

Forecasted sales units 12000 17000 6000

Proposed selling prices $1,000 $800 $750

Life-cycle revenues

$12,000,0

00

$13,600,0

00

$4,500,0

00 $0

301000

00

Less: COGS 6000000 8500000 3000000

175000

00

Gross profit

$6,000,00

0

$5,100,00

0

$1,500,0

00

126000

00

Life-cycle costs

Cost per unit $500 $500 $501

Difference $333 $167 $124

b.

On the basis of above evaluation, it is suggested to HWL to make focus on the aspect of

value engineering. In accordance with such aspect, HWL should focus on the modification of

design and system as per value analysis (Omar & et.al., 2015, pp.201-206). Through this, firm

would become able to control cost and enhancing the profitability aspect.

c.

The main reasons behind the selection of value engineering are that it offers benefit to

both individual as well as an organization (Sharaf-Addin, Omar & Sulaiman, 2014, p.82). Along

with this, such method also provides high level of assistance in avoiding unnecessary cost and

thereby maximizes profit level.

5. Preparing life cycle budget for RayHot from 2018 to 2022

A. On the basis of data given in table 1, 2 and 3

Life-cycle budget from 2018 to 2020

Year 2018 2019 2020 2021 2022

Forecasted sales units 12000 17000 6000

Proposed selling prices $1,000 $800 $750

Life-cycle revenues

$12,000,0

00

$13,600,0

00

$4,500,0

00 $0

301000

00

Less: COGS 6000000 8500000 3000000

175000

00

Gross profit

$6,000,00

0

$5,100,00

0

$1,500,0

00

126000

00

Life-cycle costs

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Research and

Development

150000

0

150000

0

Product and process

design

300000

0 700000

370000

0

Marketing

100000

0 800000 500000 400000

270000

0

Supplier training 100000 175000 105000 55000 435000

Customer support 250000 600000 350000 100000

130000

0

Total indirect life-cycle

costs

560000

0 1925000 1205000 805000 100000

963500

0

Net profit

-

560000

0

$4,075,00

0

$3,895,00

0 $695,000

-

100000

0

206500

0

Year Cash flows

PV

factor

@ 8%

Discounted cash

inflow (in $)

2018 -5600000 1 -5600000

2019 $4,075,000 0.926 3773450

2020 $3,895,000 0.857 3338015

2021 $695,000 0.794 551830

2022 -1000000 0.735 -735000

NPV 1328295

b. As per data given in table 1 and target requirements of 4(a)

Life-cycle budget from 2018 to 2020

Year 2018 2019 2020 2021 2022 Total

Forecasted sales units 12000 17000 6000

Proposed selling prices $667 $667 $667

Life-cycle revenues

$8,004,0

00

$11,339,0

00

$4,002,0

00 $0

233450

00

Less: COGS 6000000 8500000 3000000

175000

00

Development

150000

0

150000

0

Product and process

design

300000

0 700000

370000

0

Marketing

100000

0 800000 500000 400000

270000

0

Supplier training 100000 175000 105000 55000 435000

Customer support 250000 600000 350000 100000

130000

0

Total indirect life-cycle

costs

560000

0 1925000 1205000 805000 100000

963500

0

Net profit

-

560000

0

$4,075,00

0

$3,895,00

0 $695,000

-

100000

0

206500

0

Year Cash flows

PV

factor

@ 8%

Discounted cash

inflow (in $)

2018 -5600000 1 -5600000

2019 $4,075,000 0.926 3773450

2020 $3,895,000 0.857 3338015

2021 $695,000 0.794 551830

2022 -1000000 0.735 -735000

NPV 1328295

b. As per data given in table 1 and target requirements of 4(a)

Life-cycle budget from 2018 to 2020

Year 2018 2019 2020 2021 2022 Total

Forecasted sales units 12000 17000 6000

Proposed selling prices $667 $667 $667

Life-cycle revenues

$8,004,0

00

$11,339,0

00

$4,002,0

00 $0

233450

00

Less: COGS 6000000 8500000 3000000

175000

00

Gross profit

$2,004,0

00

$2,839,00

0

$1,002,0

00

584500

0

Life-cycle costs

Research and

Development

150000

0

150000

0

Product and process

design

300000

0 700000

370000

0

Marketing

100000

0 800000 500000 400000

270000

0

Supplier training 100000 175000 105000 55000 435000

Customer support 250000 600000 350000 100000

130000

0

Total indirect life-cycle

costs

560000

0 1675000 605000 455000 100000

843500

0

Net profit

-

560000

0 $329,000

$2,234,00

0 $547,000

-

100000

0

-

259000

0

PV factor @ 8% 1 0.926 0.857 0.794 0.735

NPV analysis

-

560000

0 304654 1914538 434318

-

735000

-

368149

0

c. Performing NPV analysis considering the table 4

Net present value is the most effectual tool which in turn helps in assessing the return that

business unit will get after the predetermined time frame (Dhillon, 2013). This method offers

suitable output or solution by considering the time value of money concept and helps in making

selection of suitable proposal over others. Hence, the above depicted table shows that HWL

should lay emphasis on the development aspect rather than on the introduction of Ray Hot

model. The rationale behind this, table of 5 (a) shows that, business entity will get positive and

higher margin from the investment such as $1328295. On the other side, in the case of 5 (b),

NPV accounts for $-3681490 respectively. Thus, in accordance with the selection criteria, HWL

should invest money in the project which offers higher financial benefits.

$2,004,0

00

$2,839,00

0

$1,002,0

00

584500

0

Life-cycle costs

Research and

Development

150000

0

150000

0

Product and process

design

300000

0 700000

370000

0

Marketing

100000

0 800000 500000 400000

270000

0

Supplier training 100000 175000 105000 55000 435000

Customer support 250000 600000 350000 100000

130000

0

Total indirect life-cycle

costs

560000

0 1675000 605000 455000 100000

843500

0

Net profit

-

560000

0 $329,000

$2,234,00

0 $547,000

-

100000

0

-

259000

0

PV factor @ 8% 1 0.926 0.857 0.794 0.735

NPV analysis

-

560000

0 304654 1914538 434318

-

735000

-

368149

0

c. Performing NPV analysis considering the table 4

Net present value is the most effectual tool which in turn helps in assessing the return that

business unit will get after the predetermined time frame (Dhillon, 2013). This method offers

suitable output or solution by considering the time value of money concept and helps in making

selection of suitable proposal over others. Hence, the above depicted table shows that HWL

should lay emphasis on the development aspect rather than on the introduction of Ray Hot

model. The rationale behind this, table of 5 (a) shows that, business entity will get positive and

higher margin from the investment such as $1328295. On the other side, in the case of 5 (b),

NPV accounts for $-3681490 respectively. Thus, in accordance with the selection criteria, HWL

should invest money in the project which offers higher financial benefits.

CASE STUDY 2

1. Evaluating trial cost saving rewards system in the context of ATL

Cited case situation presents that Alum Tubes Ltd (ATL) has introduced cost saving

performance related pay system for the period of 2017. Hence, company has announced that

from January to December 2017 team who will meet or exceed the performance target entitled to

get a bonus pool of $30000. With the aim to motivate all the personnel and to get the desired

level of outcome targets for the quarter are shared equally among the members. On the initial

level, such scheme has placed positive impact on employee motivation because it will assist

them in attaining financial gain.

However, at the time and during the implementation of such system several issues were

faced by the team who participated in such process such as Scuba finishing. Moreover, at the

time of evaluation related to trial cost saving program member of team Scuba finishing entails

that due to some issues they were failed to meet the target. During discussion, member of Scuba

finishing said that team Scuba assembly supplied faulty product to them for further processing.

Due to this, team Scuba finishing has taken long time for the completion of manufacturing

process. Besides this, team Scuba finishing claimed that purchasing department placed order for

the material too late. Thus, all such are the main issues due to which ATL failed to get desired

level of success from trial cost saving rewards system.

Along with this, team fire finishing stated that they were not the part of bonus scheme.

Hence, for ATL there is a requirement to make some modifications in the existing framework

which in turn contribute in the attainment of organizational goals. In accordance with the

outcome of evaluation ATL tends to make focus on undertaking activity based budgeting

technique. This in turn facilitates optimum allocation of cost on the basis of concerned driver and

thereby helps in making effectual use of financial resources (Martinez-Sanchez, Kromann &

Astrup, 2015, pp.343-355).

2. Identifying the extent to which team based cost saving measures help in evaluating

performance and awarding bonus

From assessment, it has been identified that team based cost saving measures are

appropriate when one is not based on another. In the current situation, team members of Scuba

1. Evaluating trial cost saving rewards system in the context of ATL

Cited case situation presents that Alum Tubes Ltd (ATL) has introduced cost saving

performance related pay system for the period of 2017. Hence, company has announced that

from January to December 2017 team who will meet or exceed the performance target entitled to

get a bonus pool of $30000. With the aim to motivate all the personnel and to get the desired

level of outcome targets for the quarter are shared equally among the members. On the initial

level, such scheme has placed positive impact on employee motivation because it will assist

them in attaining financial gain.

However, at the time and during the implementation of such system several issues were

faced by the team who participated in such process such as Scuba finishing. Moreover, at the

time of evaluation related to trial cost saving program member of team Scuba finishing entails

that due to some issues they were failed to meet the target. During discussion, member of Scuba

finishing said that team Scuba assembly supplied faulty product to them for further processing.

Due to this, team Scuba finishing has taken long time for the completion of manufacturing

process. Besides this, team Scuba finishing claimed that purchasing department placed order for

the material too late. Thus, all such are the main issues due to which ATL failed to get desired

level of success from trial cost saving rewards system.

Along with this, team fire finishing stated that they were not the part of bonus scheme.

Hence, for ATL there is a requirement to make some modifications in the existing framework

which in turn contribute in the attainment of organizational goals. In accordance with the

outcome of evaluation ATL tends to make focus on undertaking activity based budgeting

technique. This in turn facilitates optimum allocation of cost on the basis of concerned driver and

thereby helps in making effectual use of financial resources (Martinez-Sanchez, Kromann &

Astrup, 2015, pp.343-355).

2. Identifying the extent to which team based cost saving measures help in evaluating

performance and awarding bonus

From assessment, it has been identified that team based cost saving measures are

appropriate when one is not based on another. In the current situation, team members of Scuba

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

finishing are highly dependent on assembly. On the basis of such aspect, if one team fails to

perform in right direction then it closely impacts another. In this situation, it is not possible for

ATL to determine the efficiency level of team in an appropriate manner and award them with

bonuses. As per the given case situation, Team Scuba finishing performance is based on

assembly, whereas others are considered as independent. In this, irrespective of having high

efficiency level Scuba finishing failed to perform activities in a prominent way.

3. Assessing cost saving performance measures and other forms of incentive scheme

By doing assessment of the current strategic framework it has found that ATL’s trial cost

saving performance related pay system is not highly effectual. Thus, for the achievement of goals

and objectives it is highly required for the business unit to make focus on undertaking effective

measures (Tsai & et.al., 2014, pp.607-619). Thus, prominent or competent measures on which

firm should focus on includes contribution to total spend ratio, purchase price variance, contract

pricing, supplier management and performance. Hence, by employing all such measure ATL

would become able to assess the extent to which specific team has made contribution in cost

control.

Along with this, ALT should focus on developing budget by employing ABB techniques.

Moreover, such technique lays high level of emphasis on the cost of overhead which is large

proportion of operating cost. Further, in this, budgeting is highly based on activity framework as

well as cost driver and variance feedback processes. Thus, it can be stated that budget which is

based on ABB presents clear view of financials and thereby helps in setting suitable standards

for incentive schemes. On the basis of such aspect by making comparison of actual performance

in against to set standards ATL can assess deviations and thereby would become able to evaluate

the efficiency of team.

4.

a.

Strategies at various levels

Strategies at various levels

perform in right direction then it closely impacts another. In this situation, it is not possible for

ATL to determine the efficiency level of team in an appropriate manner and award them with

bonuses. As per the given case situation, Team Scuba finishing performance is based on

assembly, whereas others are considered as independent. In this, irrespective of having high

efficiency level Scuba finishing failed to perform activities in a prominent way.

3. Assessing cost saving performance measures and other forms of incentive scheme

By doing assessment of the current strategic framework it has found that ATL’s trial cost

saving performance related pay system is not highly effectual. Thus, for the achievement of goals

and objectives it is highly required for the business unit to make focus on undertaking effective

measures (Tsai & et.al., 2014, pp.607-619). Thus, prominent or competent measures on which

firm should focus on includes contribution to total spend ratio, purchase price variance, contract

pricing, supplier management and performance. Hence, by employing all such measure ATL

would become able to assess the extent to which specific team has made contribution in cost

control.

Along with this, ALT should focus on developing budget by employing ABB techniques.

Moreover, such technique lays high level of emphasis on the cost of overhead which is large

proportion of operating cost. Further, in this, budgeting is highly based on activity framework as

well as cost driver and variance feedback processes. Thus, it can be stated that budget which is

based on ABB presents clear view of financials and thereby helps in setting suitable standards

for incentive schemes. On the basis of such aspect by making comparison of actual performance

in against to set standards ATL can assess deviations and thereby would become able to evaluate

the efficiency of team.

4.

a.

Strategies at various levels

Strategies at various levels

Corporate: In the corporate context, firm needs to evaluate the sustainability practices

which are undertaken by competitors.

Business or enterprise: In this, business unit should employ competent strategic

framework and technology which in turn contributes in the sustainability aspects.

Functional: On functional level business unit requires to conduct training and

development session for personnel.

B.

In the business organization, it is highly required for ATL to create effectual culture by sharing

vision with personnel. Hence, manager of the firm should communicate to the personnel about

the significance of sustainability practices. Thus, firm should organize workshops, meetings and

send mail to the individuals or personnel regarding the role of sustainability practices in cost

reduction and enhancement of operational efficiency. Thus, by communicating both short and

long term benefits to personnel which are associated with sustainability practices firm can gain

competitive edge over others. Along with this, by making investment in training and

development activity ATL would become able to persuade personnel specifically Team fire

finishing about how to deal with the technological aspect firm can attain sustainability related

objectives (Mohamad & et.al., 2014, pp.78-89). Hence, by organizing training activity firm can

enhance the proficiency level of personnel and would become able to indulge the culture of

teamwork as well as innovation within ATL.

5.

Societal values account for the ways through which scare resources can be allocated and

used more efficiently. Hence, it focuses on looking beyond the price and considers all the factors

that a public authority or body chooses to award a contract. Thus, the main motives of the firm

behind all such aspects are to contribute in the collective benefit of community.

a.

From evaluation, it has been identified that some modifications are required in the new

performance evaluation system. It is cited in the case situation that CEO of ATL has taken

decision in relation to not involving the team Fire Finishing trial cost efficiency performance-

which are undertaken by competitors.

Business or enterprise: In this, business unit should employ competent strategic

framework and technology which in turn contributes in the sustainability aspects.

Functional: On functional level business unit requires to conduct training and

development session for personnel.

B.

In the business organization, it is highly required for ATL to create effectual culture by sharing

vision with personnel. Hence, manager of the firm should communicate to the personnel about

the significance of sustainability practices. Thus, firm should organize workshops, meetings and

send mail to the individuals or personnel regarding the role of sustainability practices in cost

reduction and enhancement of operational efficiency. Thus, by communicating both short and

long term benefits to personnel which are associated with sustainability practices firm can gain

competitive edge over others. Along with this, by making investment in training and

development activity ATL would become able to persuade personnel specifically Team fire

finishing about how to deal with the technological aspect firm can attain sustainability related

objectives (Mohamad & et.al., 2014, pp.78-89). Hence, by organizing training activity firm can

enhance the proficiency level of personnel and would become able to indulge the culture of

teamwork as well as innovation within ATL.

5.

Societal values account for the ways through which scare resources can be allocated and

used more efficiently. Hence, it focuses on looking beyond the price and considers all the factors

that a public authority or body chooses to award a contract. Thus, the main motives of the firm

behind all such aspects are to contribute in the collective benefit of community.

a.

From evaluation, it has been identified that some modifications are required in the new

performance evaluation system. It is cited in the case situation that CEO of ATL has taken

decision in relation to not involving the team Fire Finishing trial cost efficiency performance-

related pay scheme. Moreover, CEO believes that team fire finishing has lack of knowledge and

experience. Thus, according to efficiency phase management team of ATL should conduct

training for personnel. By this, firm would become able to provide information to the personnel

about which they need to carry out activities in a sustainable way (Seuring & Gold, 2013, pp.1-

6). Thus, it is one of the most effectual strategies which in turn contribute in the aspect of

environment sustainability and helps in enhancing the performance of employees at operational

level.

For evaluating the performance of suppliers and determining the incentive or reward

scheme firm should focus on undertaking purchasing price variance technique. Thus, by

undertaking such technique firm can assess the differences which take place between actual price

of the item and amount paid for the same. Hence, by evaluating such figure and assessing the

deviations for same ATL would become able to take appropriate action for improvement.

Further, by using contribution to spend ratio firm can assess the extent to training activity has

positively contributed in the performance and innovative practices of personnel (Corporate

sustainability, 2017). Hence, by making focus on the aspect of efficiency phase of sustainability

and moving to strategic pro-activity firm would become able to create suitable vision and involve

the culture of innovation.

b.

Efficiency phase of sustainability focuses on the implementation of human resources as

well as environmental policies and practices. This in turn helps in eliminating wastage,

contributes in cost saving as well as innovation aspect to a great extent. Along with this, strategic

pro-activity phase focuses on becoming a market leader in sustainability practices. On the basis

of such aspect, by conducting training session ATL would become able to enhance the skills and

abilities of individual to the significant level. Along with this, such modification is needed for

encouraging teamwork and innovation. Moreover, team includes people who having expertise

and knowledge in relation to different areas (Starik & Kanashiro, 2013, pp.7-30). The reason

behind this, when people of different backgrounds work together, then it may result into

innovative practices. Along with this, when personnel work in a sustainable manner then there is

less wastage of resources and cost reduction. Thus, all the above depicted aspects have

encouraged ATL to undertake training activity.

experience. Thus, according to efficiency phase management team of ATL should conduct

training for personnel. By this, firm would become able to provide information to the personnel

about which they need to carry out activities in a sustainable way (Seuring & Gold, 2013, pp.1-

6). Thus, it is one of the most effectual strategies which in turn contribute in the aspect of

environment sustainability and helps in enhancing the performance of employees at operational

level.

For evaluating the performance of suppliers and determining the incentive or reward

scheme firm should focus on undertaking purchasing price variance technique. Thus, by

undertaking such technique firm can assess the differences which take place between actual price

of the item and amount paid for the same. Hence, by evaluating such figure and assessing the

deviations for same ATL would become able to take appropriate action for improvement.

Further, by using contribution to spend ratio firm can assess the extent to training activity has

positively contributed in the performance and innovative practices of personnel (Corporate

sustainability, 2017). Hence, by making focus on the aspect of efficiency phase of sustainability

and moving to strategic pro-activity firm would become able to create suitable vision and involve

the culture of innovation.

b.

Efficiency phase of sustainability focuses on the implementation of human resources as

well as environmental policies and practices. This in turn helps in eliminating wastage,

contributes in cost saving as well as innovation aspect to a great extent. Along with this, strategic

pro-activity phase focuses on becoming a market leader in sustainability practices. On the basis

of such aspect, by conducting training session ATL would become able to enhance the skills and

abilities of individual to the significant level. Along with this, such modification is needed for

encouraging teamwork and innovation. Moreover, team includes people who having expertise

and knowledge in relation to different areas (Starik & Kanashiro, 2013, pp.7-30). The reason

behind this, when people of different backgrounds work together, then it may result into

innovative practices. Along with this, when personnel work in a sustainable manner then there is

less wastage of resources and cost reduction. Thus, all the above depicted aspects have

encouraged ATL to undertake training activity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

c.

For the creation of sustainability culture it is highly required for ATL Malaysia to

strongly make focus on the development of employees, training, safe etc. By doing this, firm can

enhance the capabilities of employees and thereby would become able to overcome the

differences assessed.

CASE STUDY 3

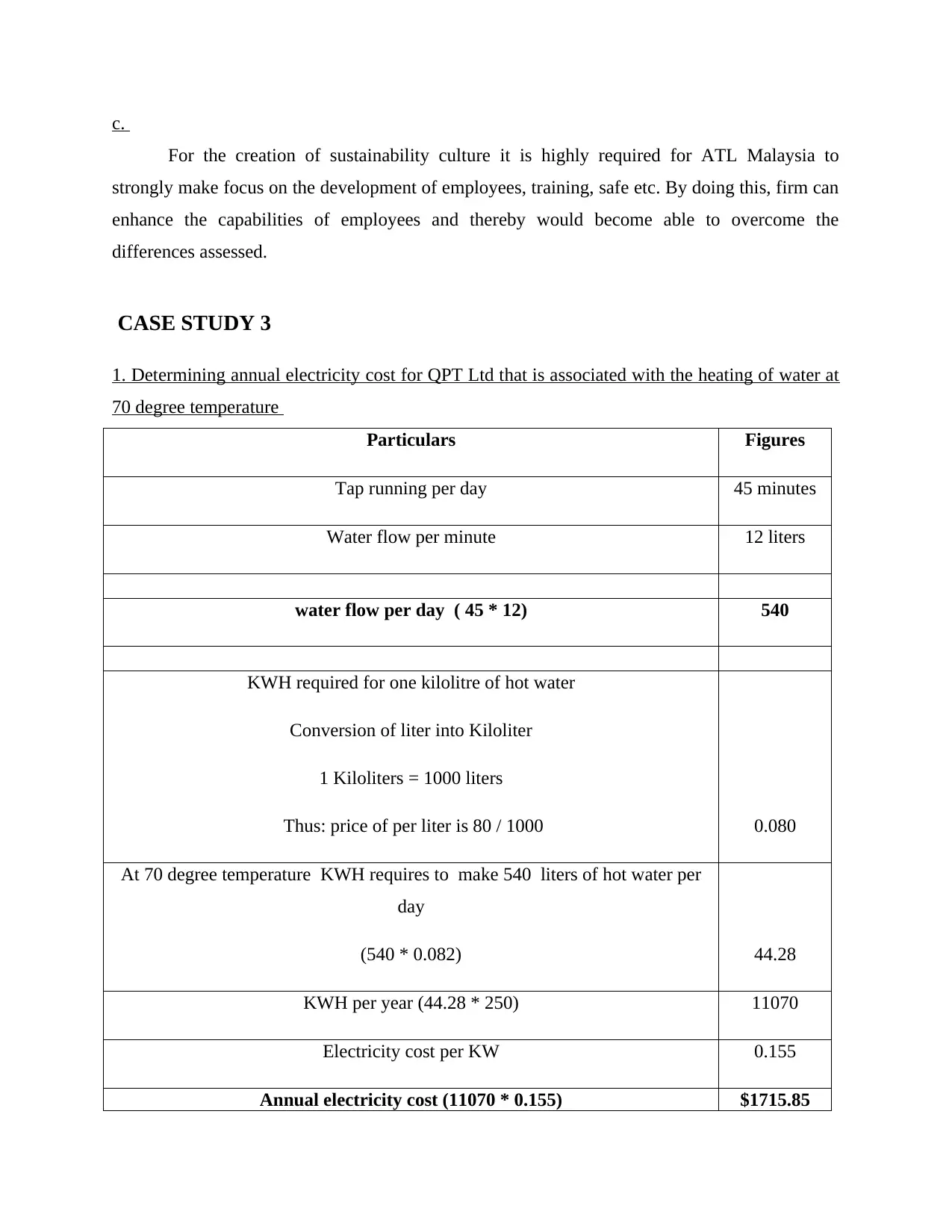

1. Determining annual electricity cost for QPT Ltd that is associated with the heating of water at

70 degree temperature

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 12 liters

water flow per day ( 45 * 12) 540

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 80 / 1000 0.080

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.082) 44.28

KWH per year (44.28 * 250) 11070

Electricity cost per KW 0.155

Annual electricity cost (11070 * 0.155) $1715.85

For the creation of sustainability culture it is highly required for ATL Malaysia to

strongly make focus on the development of employees, training, safe etc. By doing this, firm can

enhance the capabilities of employees and thereby would become able to overcome the

differences assessed.

CASE STUDY 3

1. Determining annual electricity cost for QPT Ltd that is associated with the heating of water at

70 degree temperature

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 12 liters

water flow per day ( 45 * 12) 540

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 80 / 1000 0.080

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.082) 44.28

KWH per year (44.28 * 250) 11070

Electricity cost per KW 0.155

Annual electricity cost (11070 * 0.155) $1715.85

Interpretation: From evaluation, it has been identified that annual electricity cost which

is associated with 70 degree temperature accounts for $1716 respectively. Tabular presentation

clearly shows that water flow per day is 540 liters. Hence, KWH required to make hot water

implies for 44.28 hours. Further, it is clearly mentioned in the case scenario that activity in

relation to making hot water is performed by QPT ltd for 250 days in a year. On the basis of such

aspect, KWH per year associated with making hot water is 11070. Thus, in accordance with

electricity cost per KW such as $0.155, EC of the company is $1716 per annum.

2. Calculating saving amount in dollar if lower temperature is used such as 60 degree

With the motive to assess the annual electricity cost and determines the savings amount

manager of finance department has done evaluation on 60 degree hot water temperature. This in

turn helps in assessing the extent to which electricity cost will reduce when Hot water

temperature shifted from 70 to 60 degree. Hence, for getting suitable information for decision

making electricity cost is assessed on 60 degree temperature in the following manner:

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 12 liters

water flow per day ( 45 * 12) 540

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 64 / 1000 0.064

is associated with 70 degree temperature accounts for $1716 respectively. Tabular presentation

clearly shows that water flow per day is 540 liters. Hence, KWH required to make hot water

implies for 44.28 hours. Further, it is clearly mentioned in the case scenario that activity in

relation to making hot water is performed by QPT ltd for 250 days in a year. On the basis of such

aspect, KWH per year associated with making hot water is 11070. Thus, in accordance with

electricity cost per KW such as $0.155, EC of the company is $1716 per annum.

2. Calculating saving amount in dollar if lower temperature is used such as 60 degree

With the motive to assess the annual electricity cost and determines the savings amount

manager of finance department has done evaluation on 60 degree hot water temperature. This in

turn helps in assessing the extent to which electricity cost will reduce when Hot water

temperature shifted from 70 to 60 degree. Hence, for getting suitable information for decision

making electricity cost is assessed on 60 degree temperature in the following manner:

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 12 liters

water flow per day ( 45 * 12) 540

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 64 / 1000 0.064

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.064) 34.56

KWH per year (34.56 * 250) 8640

Electricity cost per kilolitre 0.155

Annual electricity cost (8640 * 0.155) $1339.2

Savings (1715.85 – 1339.2) 377

Interpretation: By doing assessment, it has discovered that EC is $1716 when hot water

temperature is 70 degree. On the other side, in the case of 60 degree hot water temperature

electricity cost is $1339 significantly. Thus, outcome of evaluation presents that if QPT Ltd will

consider 60 degree temperature as compared to 70 then savings accounts for $377. The rationale

behind this, at the level 60 degree temperature KWH per day decreased from 44.28 to 34.56.

Thus, by taking into account the results of evaluation it can be said that QPT Ltd will get

financial benefits when temperature level is 60.

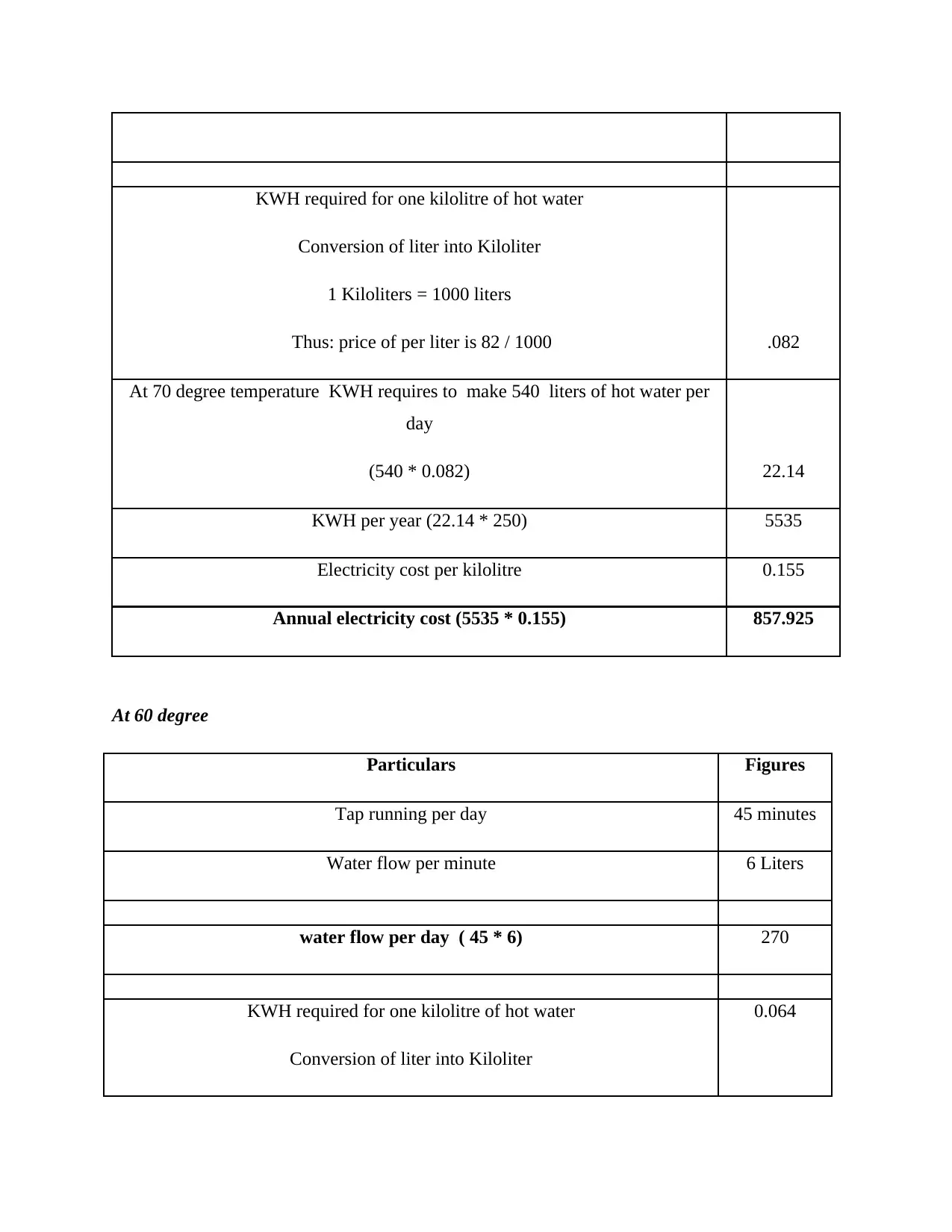

3. Computing electricity cost at both 70 and 60 degree when water flow decreased from 12 to 6

minutes

On the basis of given case situation, if water flow restrictor will reduce the level from 12

to 6 lire then electricity cost at 70 and 60 degree temperature will be:

At 70 degree

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 6Liters

water flow per day ( 45 * 6) 270

day

(540 * 0.064) 34.56

KWH per year (34.56 * 250) 8640

Electricity cost per kilolitre 0.155

Annual electricity cost (8640 * 0.155) $1339.2

Savings (1715.85 – 1339.2) 377

Interpretation: By doing assessment, it has discovered that EC is $1716 when hot water

temperature is 70 degree. On the other side, in the case of 60 degree hot water temperature

electricity cost is $1339 significantly. Thus, outcome of evaluation presents that if QPT Ltd will

consider 60 degree temperature as compared to 70 then savings accounts for $377. The rationale

behind this, at the level 60 degree temperature KWH per day decreased from 44.28 to 34.56.

Thus, by taking into account the results of evaluation it can be said that QPT Ltd will get

financial benefits when temperature level is 60.

3. Computing electricity cost at both 70 and 60 degree when water flow decreased from 12 to 6

minutes

On the basis of given case situation, if water flow restrictor will reduce the level from 12

to 6 lire then electricity cost at 70 and 60 degree temperature will be:

At 70 degree

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 6Liters

water flow per day ( 45 * 6) 270

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 82 / 1000 .082

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.082) 22.14

KWH per year (22.14 * 250) 5535

Electricity cost per kilolitre 0.155

Annual electricity cost (5535 * 0.155) 857.925

At 60 degree

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 6 Liters

water flow per day ( 45 * 6) 270

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

0.064

Conversion of liter into Kiloliter

1 Kiloliters = 1000 liters

Thus: price of per liter is 82 / 1000 .082

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.082) 22.14

KWH per year (22.14 * 250) 5535

Electricity cost per kilolitre 0.155

Annual electricity cost (5535 * 0.155) 857.925

At 60 degree

Particulars Figures

Tap running per day 45 minutes

Water flow per minute 6 Liters

water flow per day ( 45 * 6) 270

KWH required for one kilolitre of hot water

Conversion of liter into Kiloliter

0.064

1 Kiloliters = 1000 liters

Thus: price of per liter is 64 / 1000

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.064) 17.28

KWH per year (17.28 * 250) 4320

Electricity cost per kilolitre 0.155

Annual electricity cost (4320 * 0.155) 669.6

Interpretation: Tabular presentation shows that if in 1 minute level of water flow will be 6 liters

in 1 minute then per day running accounts for 270 lt. Hence, in this, KWH per day at 70 and 60

degree hot water temperature is 22.14 & 17.28 respectively. Result of evaluation exhibits that

when water flow in per minute will be 6 liters then annual electricity cost on 70 and 60 degree

implies for $858 & 670.

4. Computation of energy cost saving

Particulars Figures

What water flow is 12 liters in per minute and

temperature is 70 degree (assuming tap is

running 45 minutes in a day and year includes

250 days)

$1716

What water flow is 12 liters in per minute and

temperature is 60 degree

$1339

Cost saving $1716 - $1339 = $377

Thus: price of per liter is 64 / 1000

At 70 degree temperature KWH requires to make 540 liters of hot water per

day

(540 * 0.064) 17.28

KWH per year (17.28 * 250) 4320

Electricity cost per kilolitre 0.155

Annual electricity cost (4320 * 0.155) 669.6

Interpretation: Tabular presentation shows that if in 1 minute level of water flow will be 6 liters

in 1 minute then per day running accounts for 270 lt. Hence, in this, KWH per day at 70 and 60

degree hot water temperature is 22.14 & 17.28 respectively. Result of evaluation exhibits that

when water flow in per minute will be 6 liters then annual electricity cost on 70 and 60 degree

implies for $858 & 670.

4. Computation of energy cost saving

Particulars Figures

What water flow is 12 liters in per minute and

temperature is 70 degree (assuming tap is

running 45 minutes in a day and year includes

250 days)

$1716

What water flow is 12 liters in per minute and

temperature is 60 degree

$1339

Cost saving $1716 - $1339 = $377

On the basis of cited case situation following aspects have been considered in Q.3 to

determine energy cost are enumerated below:

Water flow: 6 liters in 1 minute (Tap is running 45 minutes in a day)

Days in a year: 250

70 degree 60 degree

Electricity cost $858 $670

Savings 858 – 670 = $188

Interpretation: Tabular presentation shows that energy saving amount is higher when

water flow level is 12 liters in a 1 minute such as $377. On the other side, in the case of water

flow reduction from 12 liters to 6 then saving figure is $188 respectively. In accordance with

such aspect, it can be stated that high savings are associated with the level of water flow 12 liters

in 1 minute. However, cost will be lower to a great extent if QPT Ltd will reduce flow from 12 to

6 liters.

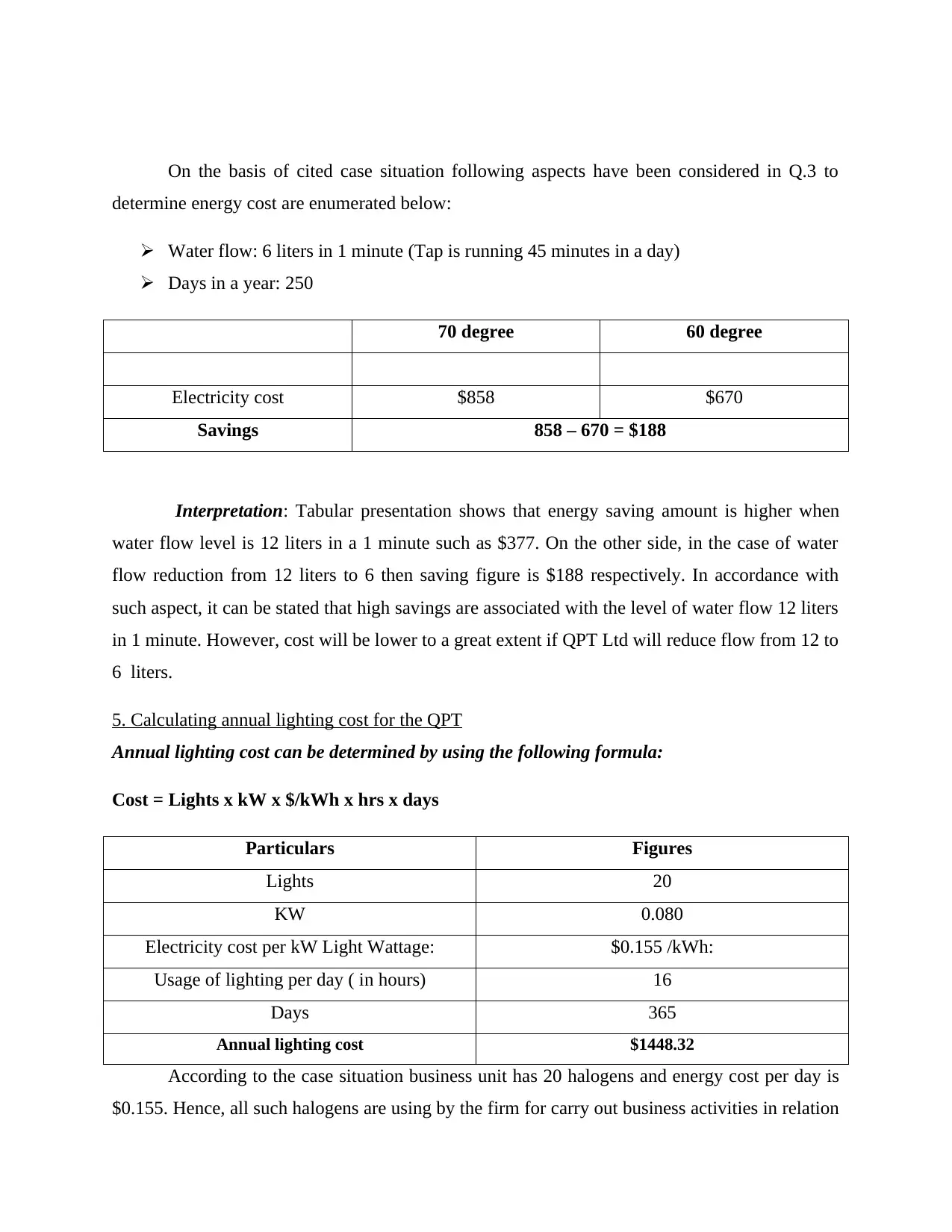

5. Calculating annual lighting cost for the QPT

Annual lighting cost can be determined by using the following formula:

Cost = Lights x kW x $/kWh x hrs x days

Particulars Figures

Lights 20

KW 0.080

Electricity cost per kW Light Wattage: $0.155 /kWh:

Usage of lighting per day ( in hours) 16

Days 365

Annual lighting cost $1448.32

According to the case situation business unit has 20 halogens and energy cost per day is

$0.155. Hence, all such halogens are using by the firm for carry out business activities in relation

determine energy cost are enumerated below:

Water flow: 6 liters in 1 minute (Tap is running 45 minutes in a day)

Days in a year: 250

70 degree 60 degree

Electricity cost $858 $670

Savings 858 – 670 = $188

Interpretation: Tabular presentation shows that energy saving amount is higher when

water flow level is 12 liters in a 1 minute such as $377. On the other side, in the case of water

flow reduction from 12 liters to 6 then saving figure is $188 respectively. In accordance with

such aspect, it can be stated that high savings are associated with the level of water flow 12 liters

in 1 minute. However, cost will be lower to a great extent if QPT Ltd will reduce flow from 12 to

6 liters.

5. Calculating annual lighting cost for the QPT

Annual lighting cost can be determined by using the following formula:

Cost = Lights x kW x $/kWh x hrs x days

Particulars Figures

Lights 20

KW 0.080

Electricity cost per kW Light Wattage: $0.155 /kWh:

Usage of lighting per day ( in hours) 16

Days 365

Annual lighting cost $1448.32

According to the case situation business unit has 20 halogens and energy cost per day is

$0.155. Hence, all such halogens are using by the firm for carry out business activities in relation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

to 16 hours. By applying the above depicted formula, it has been identified that annual lighting

cost which is associated with the business operations of QPT ltd implies for $1448.

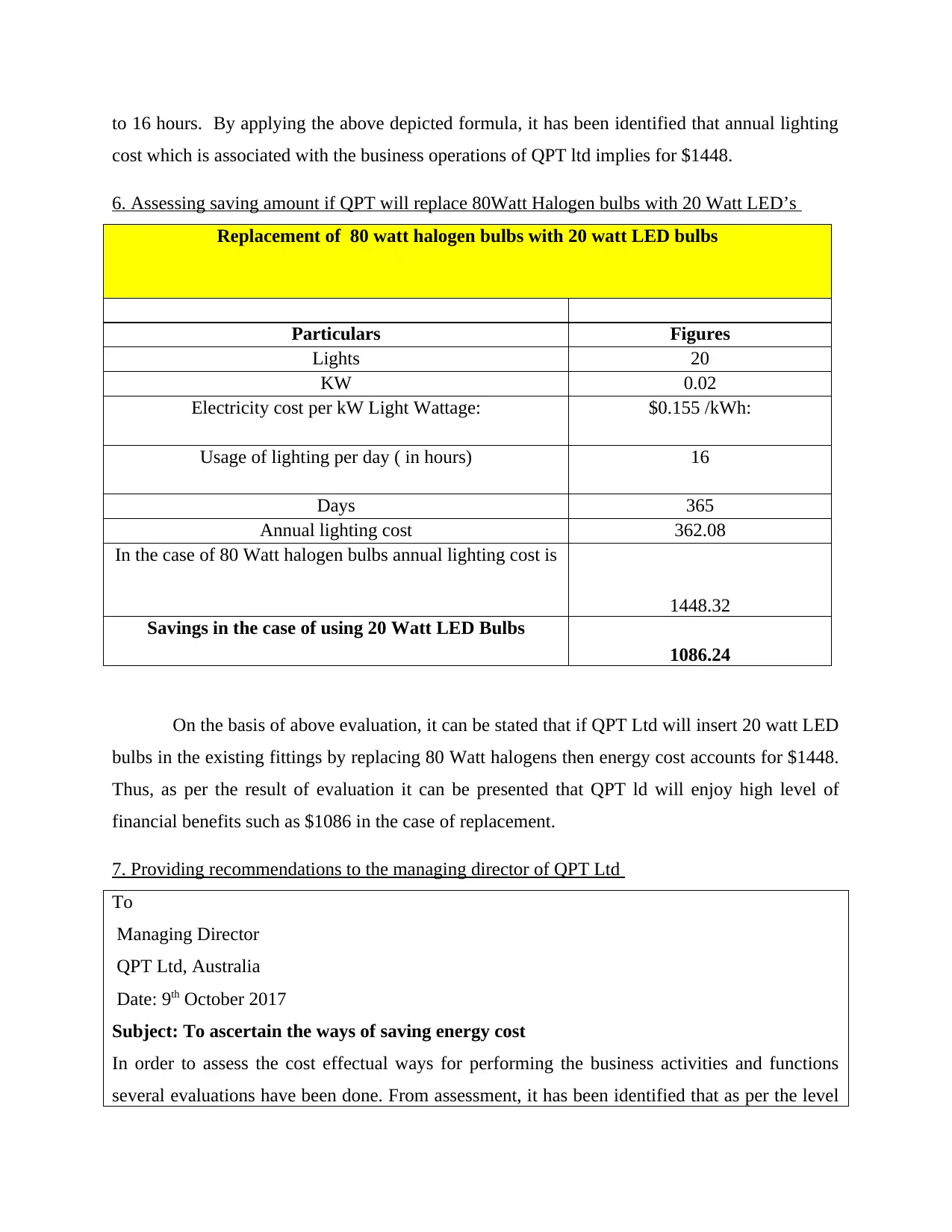

6. Assessing saving amount if QPT will replace 80Watt Halogen bulbs with 20 Watt LED’s

Replacement of 80 watt halogen bulbs with 20 watt LED bulbs

Particulars Figures

Lights 20

KW 0.02

Electricity cost per kW Light Wattage: $0.155 /kWh:

Usage of lighting per day ( in hours) 16

Days 365

Annual lighting cost 362.08

In the case of 80 Watt halogen bulbs annual lighting cost is

1448.32

Savings in the case of using 20 Watt LED Bulbs

1086.24

On the basis of above evaluation, it can be stated that if QPT Ltd will insert 20 watt LED

bulbs in the existing fittings by replacing 80 Watt halogens then energy cost accounts for $1448.

Thus, as per the result of evaluation it can be presented that QPT ld will enjoy high level of

financial benefits such as $1086 in the case of replacement.

7. Providing recommendations to the managing director of QPT Ltd

To

Managing Director

QPT Ltd, Australia

Date: 9th October 2017

Subject: To ascertain the ways of saving energy cost

In order to assess the cost effectual ways for performing the business activities and functions

several evaluations have been done. From assessment, it has been identified that as per the level

cost which is associated with the business operations of QPT ltd implies for $1448.

6. Assessing saving amount if QPT will replace 80Watt Halogen bulbs with 20 Watt LED’s

Replacement of 80 watt halogen bulbs with 20 watt LED bulbs

Particulars Figures

Lights 20

KW 0.02

Electricity cost per kW Light Wattage: $0.155 /kWh:

Usage of lighting per day ( in hours) 16

Days 365

Annual lighting cost 362.08

In the case of 80 Watt halogen bulbs annual lighting cost is

1448.32

Savings in the case of using 20 Watt LED Bulbs

1086.24

On the basis of above evaluation, it can be stated that if QPT Ltd will insert 20 watt LED

bulbs in the existing fittings by replacing 80 Watt halogens then energy cost accounts for $1448.

Thus, as per the result of evaluation it can be presented that QPT ld will enjoy high level of

financial benefits such as $1086 in the case of replacement.

7. Providing recommendations to the managing director of QPT Ltd

To

Managing Director

QPT Ltd, Australia

Date: 9th October 2017

Subject: To ascertain the ways of saving energy cost

In order to assess the cost effectual ways for performing the business activities and functions

several evaluations have been done. From assessment, it has been identified that as per the level

of water flow within 1 minute energy cost varies significantly. Along with this, as per

temperature level cost of electricity also differs. It has been identified from evaluation that

energy cost at 70 degree hot water temperature is $1716. In contrast to this, when hot water

temperature is 60 degree then cost pertaining to energy implies for $1339. Hence, it is suggested

to the manager of company to set 60 degree hot water temperature which in turn assists

corporation in getting the benefits of $377. On the basis of evaluation results it is recommended

to QPT ltd to lay emphasis on replacing 80 Watt halogens with 20 Watt LED. Moreover, such

strategy will offer high level of benefit to the firm in monetary terms. Moreover, in the case of 80

watt halogen bulbs energy cost is F $858. Whereas, if firm will use LED bulbs then cost of

energy accounts for $1086.24 which in turn helps in getting benefits of $188. Thus, firm should

focus on fitting LED bulbs within the organization which in turn helps it in saving energy cost to

the significant level. Hence, by considering all such aspects firm can develop suitable strategic

framework and thereby would become able to control or reduce the cost level as well as

maximize the profitability aspect.

Sincerely

Analyst

CONCLUSION

From the above report, it has been concluded that target and life cycle budget is highly

significant which in turn helps in making optimum use of financial resources and thereby helps

in getting benefits in monetary terms. It can be seen in the report that determination of unit cots

is highly required for making pricing decision. In addition to this, it can be depicted that ATL

should focus on efficiency and pro-activity phase of sustainability which in turn helps in

reducing the cost level and building effective image in the mind of stakeholders. Besides this, it

can be inferred that manager of the firm should lay emphasis on evaluating all the alternatives

which are available to them. It can be summarized from the evaluation that QPT needs to

consider 60 degree temperature for making the water hot. By doing this, firm can make control

over cost and would become able to get high margin. In addition to this, it can be stated that QPT

Ltd should focus on the replacement of halogen with LED bulbs. This is turn provides high level

temperature level cost of electricity also differs. It has been identified from evaluation that

energy cost at 70 degree hot water temperature is $1716. In contrast to this, when hot water

temperature is 60 degree then cost pertaining to energy implies for $1339. Hence, it is suggested

to the manager of company to set 60 degree hot water temperature which in turn assists

corporation in getting the benefits of $377. On the basis of evaluation results it is recommended

to QPT ltd to lay emphasis on replacing 80 Watt halogens with 20 Watt LED. Moreover, such

strategy will offer high level of benefit to the firm in monetary terms. Moreover, in the case of 80

watt halogen bulbs energy cost is F $858. Whereas, if firm will use LED bulbs then cost of

energy accounts for $1086.24 which in turn helps in getting benefits of $188. Thus, firm should

focus on fitting LED bulbs within the organization which in turn helps it in saving energy cost to

the significant level. Hence, by considering all such aspects firm can develop suitable strategic

framework and thereby would become able to control or reduce the cost level as well as

maximize the profitability aspect.

Sincerely

Analyst

CONCLUSION

From the above report, it has been concluded that target and life cycle budget is highly

significant which in turn helps in making optimum use of financial resources and thereby helps

in getting benefits in monetary terms. It can be seen in the report that determination of unit cots

is highly required for making pricing decision. In addition to this, it can be depicted that ATL

should focus on efficiency and pro-activity phase of sustainability which in turn helps in

reducing the cost level and building effective image in the mind of stakeholders. Besides this, it

can be inferred that manager of the firm should lay emphasis on evaluating all the alternatives

which are available to them. It can be summarized from the evaluation that QPT needs to

consider 60 degree temperature for making the water hot. By doing this, firm can make control

over cost and would become able to get high margin. In addition to this, it can be stated that QPT

Ltd should focus on the replacement of halogen with LED bulbs. This is turn provides high level

of assistance to QPT Ltd in saving both energy and associated expenses. It has been articulated

that cost is one of the main factors that have significant impact on the profitability.

that cost is one of the main factors that have significant impact on the profitability.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.