Management Accounting Report: Budgeting and Cost Analysis for KBC Ltd

VerifiedAdded on 2019/12/28

|22

|6816

|204

Report

AI Summary

This management accounting report, prepared for KBC Ltd, delves into the significance of budgeting, outlining administrative procedures and the stages involved in the budgeting process. It classifies costs, calculates fixed and variable costs using the high-low method, and compares absorption and marginal costing methods, illustrating their impact on inventory valuation and profit determination. The report further examines break-even analysis, including contribution to sales ratio, break-even point calculation, and the determination of required sales to achieve a target profit. It also explores cash budgeting, flexed budgeting, and variance analysis. Finally, it discusses various budgeting methods, including cash budgets, and provides recommendations for KBC Ltd based on the analysis.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

A) Importance of budgeting for the businesses...........................................................................4

B) Administrative procedures used in Budgeting process...........................................................5

C) Stages of budgeting process....................................................................................................5

Task 2...............................................................................................................................................6

A) Classification of costs.............................................................................................................6

B) Calculate fixed and variable costs...........................................................................................7

Task 3...............................................................................................................................................8

A) Effect of absorption and marginal costing on inventory valuation and profit determination.8

B) Differentiate between various costing methods......................................................................8

c) Preparation of profit and loss statement on the basis of Absorption costing ..........................9

d) Preparation of profit and loss statement for South Area on the basis of Marginal costing . .10

TASK 4..........................................................................................................................................10

a) Advice to KBC Ltd................................................................................................................10

b) Calculation of BEP, contribution to sales and required units to earn target profit................11

b) (1) Contribution to sales ratio, based on sales mix of the four products...............................11

(2) Break-even point in £000.....................................................................................................12

(3) Required sales to earn profit of £90000...............................................................................12

c) Calculation of profits at £10 labour rate with restricted 66000 labour hours........................12

d) Calculation of profits for further 6000 hours.........................................................................12

TASK 5..........................................................................................................................................12

a) Types of budgeting methods..................................................................................................12

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

A) Importance of budgeting for the businesses...........................................................................4

B) Administrative procedures used in Budgeting process...........................................................5

C) Stages of budgeting process....................................................................................................5

Task 2...............................................................................................................................................6

A) Classification of costs.............................................................................................................6

B) Calculate fixed and variable costs...........................................................................................7

Task 3...............................................................................................................................................8

A) Effect of absorption and marginal costing on inventory valuation and profit determination.8

B) Differentiate between various costing methods......................................................................8

c) Preparation of profit and loss statement on the basis of Absorption costing ..........................9

d) Preparation of profit and loss statement for South Area on the basis of Marginal costing . .10

TASK 4..........................................................................................................................................10

a) Advice to KBC Ltd................................................................................................................10

b) Calculation of BEP, contribution to sales and required units to earn target profit................11

b) (1) Contribution to sales ratio, based on sales mix of the four products...............................11

(2) Break-even point in £000.....................................................................................................12

(3) Required sales to earn profit of £90000...............................................................................12

c) Calculation of profits at £10 labour rate with restricted 66000 labour hours........................12

d) Calculation of profits for further 6000 hours.........................................................................12

TASK 5..........................................................................................................................................12

a) Types of budgeting methods..................................................................................................12

b) Cash budget...........................................................................................................................14

1) Calculation of amounts of direct material purchases.............................................................14

2) Preparation of cash budgets for July, August and September................................................14

3) Advantages of cash budget....................................................................................................15

4) Advise the Board for the cash flow variances.......................................................................15

Task 6.............................................................................................................................................15

(i) Prepare Flexed Budget and compute variance......................................................................15

(ii) Variance Analysis.................................................................................................................16

(iii) Report findings....................................................................................................................17

TASK 7..........................................................................................................................................17

a) Calculation of BEP and Margin of Safety.............................................................................17

b) Calculation of profit/Loss at 26500 pair of shoes..................................................................18

c) Calculation of number of units to earn desired profit of £240100 at £2 per unit sales

commission................................................................................................................................19

e) Calculation of BEP units to reach at fixed advertisement cost of £20000 and increase........19

selling price by 15%...................................................................................................................19

e) Recommendation with justification.......................................................................................19

Conclusion.....................................................................................................................................20

References......................................................................................................................................21

1) Calculation of amounts of direct material purchases.............................................................14

2) Preparation of cash budgets for July, August and September................................................14

3) Advantages of cash budget....................................................................................................15

4) Advise the Board for the cash flow variances.......................................................................15

Task 6.............................................................................................................................................15

(i) Prepare Flexed Budget and compute variance......................................................................15

(ii) Variance Analysis.................................................................................................................16

(iii) Report findings....................................................................................................................17

TASK 7..........................................................................................................................................17

a) Calculation of BEP and Margin of Safety.............................................................................17

b) Calculation of profit/Loss at 26500 pair of shoes..................................................................18

c) Calculation of number of units to earn desired profit of £240100 at £2 per unit sales

commission................................................................................................................................19

e) Calculation of BEP units to reach at fixed advertisement cost of £20000 and increase........19

selling price by 15%...................................................................................................................19

e) Recommendation with justification.......................................................................................19

Conclusion.....................................................................................................................................20

References......................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is fundamental in strategic planning. When a business is looking

to make a strategic decision, for example, whether to develop a new product line, acquire another

business or expand into other countries, the CIMA trained management accountant can provide

advice. They can use a number of tools to assist decision-making. Management accountants look

ahead - they focus on forecasting and decision-making (Islam and Dellaportas, 2011). They use

information to advice on how the business can move forward, for example, should a company

buy another, should it invest in new equipment. Management accounting involves using the

internal financial information available to managers, as well as that information which

companies must publish by law (Lindholm and Suomala, 2007). This contributes to forward

planning, reviewing and analyzing the performance of the business. In the present report,

Management Accountant has been appointed for KBC Ltd to evaluate importance of budgeting

and budgetary control mechanism. Along with this, provide the clear understanding of the cost

implications in order to help management of KBC Ltd in classifying the costs. Further,

accountant will assist in computing BEP for making short term management decisions. Lastly,

concepts and significance of different types of budgeting has been focused on to enhance the

understanding of management of KBC Ltd.

TASK 1

A) Importance of budgeting for the businesses

Budgeting is considered as the critical part of the business planning process. However, it

is the responsibility of business owners and managers to predict whether business will make

profit of not. The main purpose of behind budgeting is that it assist the managers of organisation

to forecast the financial functioning of business (Maelah and et. al, 2012). According to the

present given scenario, management of KBC Ltd is facing various issues in managing costs thus,

accounting is focusing on providing information regarding the importance of budgeting in

mitigating the same problem.

However, budgeting is considered as the decision making tool by providing financial

framework to managerial level people. Through the means of this, managers can easily control or

maintain the level of expenditure or outflow on the basis of inflow. In addition to it, KBC Ltd

can make use of different types of budgeting techniques to monitor the performance of business

(Gupta, Sharma and Ahuja, 2012). However, it’s one of the major advantages is that budgeting

4

Management accounting is fundamental in strategic planning. When a business is looking

to make a strategic decision, for example, whether to develop a new product line, acquire another

business or expand into other countries, the CIMA trained management accountant can provide

advice. They can use a number of tools to assist decision-making. Management accountants look

ahead - they focus on forecasting and decision-making (Islam and Dellaportas, 2011). They use

information to advice on how the business can move forward, for example, should a company

buy another, should it invest in new equipment. Management accounting involves using the

internal financial information available to managers, as well as that information which

companies must publish by law (Lindholm and Suomala, 2007). This contributes to forward

planning, reviewing and analyzing the performance of the business. In the present report,

Management Accountant has been appointed for KBC Ltd to evaluate importance of budgeting

and budgetary control mechanism. Along with this, provide the clear understanding of the cost

implications in order to help management of KBC Ltd in classifying the costs. Further,

accountant will assist in computing BEP for making short term management decisions. Lastly,

concepts and significance of different types of budgeting has been focused on to enhance the

understanding of management of KBC Ltd.

TASK 1

A) Importance of budgeting for the businesses

Budgeting is considered as the critical part of the business planning process. However, it

is the responsibility of business owners and managers to predict whether business will make

profit of not. The main purpose of behind budgeting is that it assist the managers of organisation

to forecast the financial functioning of business (Maelah and et. al, 2012). According to the

present given scenario, management of KBC Ltd is facing various issues in managing costs thus,

accounting is focusing on providing information regarding the importance of budgeting in

mitigating the same problem.

However, budgeting is considered as the decision making tool by providing financial

framework to managerial level people. Through the means of this, managers can easily control or

maintain the level of expenditure or outflow on the basis of inflow. In addition to it, KBC Ltd

can make use of different types of budgeting techniques to monitor the performance of business

(Gupta, Sharma and Ahuja, 2012). However, it’s one of the major advantages is that budgeting

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assist in enabling the measuring of actual business performance against the estimated business

performance so that potential measures can be employed to minimize the variances.

B) Administrative procedures used in Budgeting process

In general administrative procedures can be defined as the method or approaches

determined by the government to prepare the budgets in accurate and appropriate manner. These

procedures are system of rules that govern the process of managing the activities of the business

enterprise. The main purpose of administrative procedures is that it assist in establishing

efficiency, consistency responsibility and accountability (Harrison and Lock, 2004). There are

various budget management standards that top level management of KBC Ltd has to undertake in

order to carry out the budgeting process as per the guidelines or procedures of administrative.

The total estimated amounts proposed for each expenditure during the reporting

year should be in terms maximum expended value for that fiscal year and it must

authorized by the board of trustees or members (Administrative Procedure, 2014).

On the basis of budget and accounting manual, the term major classification

should refers to the major code of classification.

Funds should be transferred only form the available reserves to any unwanted

expenditure or uncertainties in terms of written resolution and must be approved by 2/3

vote of the Board of Members of KBC Ltd.

Further, the additional transfer of money in the same major classification of accounts

does not require prior board approval.

C) Stages of budgeting process

In accounting terms, budget is prepared with the aim of determining the expectations for

revenues and expenses in the near future. Thus, to prepare a budget it is important for finance

manager of KBC Ltd to abide and follow all the regulations so that completed budget is ready to

use for fiscal year. Following are the various stages involved in budgeting process that

management of KBC Ltd should consider while preparing the budget: Determining the details of budget policy and guideline to the committee members: Under

this stage top level management of cited organisation should provide detailed information

and guidelines document to the people who are responsible for preparing the budget.

However, by abiding these guidelines and regulations committee members can prepare

effective and reliable budget (Hill, 2003).

5

performance so that potential measures can be employed to minimize the variances.

B) Administrative procedures used in Budgeting process

In general administrative procedures can be defined as the method or approaches

determined by the government to prepare the budgets in accurate and appropriate manner. These

procedures are system of rules that govern the process of managing the activities of the business

enterprise. The main purpose of administrative procedures is that it assist in establishing

efficiency, consistency responsibility and accountability (Harrison and Lock, 2004). There are

various budget management standards that top level management of KBC Ltd has to undertake in

order to carry out the budgeting process as per the guidelines or procedures of administrative.

The total estimated amounts proposed for each expenditure during the reporting

year should be in terms maximum expended value for that fiscal year and it must

authorized by the board of trustees or members (Administrative Procedure, 2014).

On the basis of budget and accounting manual, the term major classification

should refers to the major code of classification.

Funds should be transferred only form the available reserves to any unwanted

expenditure or uncertainties in terms of written resolution and must be approved by 2/3

vote of the Board of Members of KBC Ltd.

Further, the additional transfer of money in the same major classification of accounts

does not require prior board approval.

C) Stages of budgeting process

In accounting terms, budget is prepared with the aim of determining the expectations for

revenues and expenses in the near future. Thus, to prepare a budget it is important for finance

manager of KBC Ltd to abide and follow all the regulations so that completed budget is ready to

use for fiscal year. Following are the various stages involved in budgeting process that

management of KBC Ltd should consider while preparing the budget: Determining the details of budget policy and guideline to the committee members: Under

this stage top level management of cited organisation should provide detailed information

and guidelines document to the people who are responsible for preparing the budget.

However, by abiding these guidelines and regulations committee members can prepare

effective and reliable budget (Hill, 2003).

5

Determining the factors that restricts output and taking corrective actions to solve the

problems: During this stage, people responsible for preparing the budgets will make

efforts to identify and evaluate all the factors that are affecting the course of sales and

manufacturing process of the company so that desired projections can be made and

realistic estimations can be proposed. Preparation of sales budget: Once the factors are identified and keeping those in mind

managers can prepare sales budget and communicated to the sales department so that

they can execute their functioning accordingly. Initial preparation of various budgets: Once the Board of Directors of KBC Ltd approves

the projections of budget value so that further it can be divided into different budges so

that allocation of funds can be done on effective basis (Davis and Davis, 2012). Negotiation of budgets with superiors: After preparing all the budgets for different

departments, committee members consults with superiors of each department and if

required changes are made. Coordination and review of budgets: In this section, defined changes will take place and

reviewed once again for the final approval.

Final acceptance of budgets: This is the last stage of budgeting process in which budgets

for different departments are accepted by the top level managers and accordingly flow of

money is managed and controlled (Ezeoha, 2011).

TASK 2

A) Classification of costs

Costs in general can be defined as the amount of money spent by the firm to produce a

single unit of product or service. Further, costs can be classified on several basis which are as

follows: Function: Costs related to production (factory lighting and rent, unproductive wages),

administrative (stationery, postage etc.), selling and distribution departments

(advertisement, marketing and free samples) are considered as the function based costs

classification (Galloway and Deakins, 2012). Looking the functioning of KBC Ltd, it is

important for the managers to maintain costs related to all the defined department so that

better financial position can be achieved.

6

problems: During this stage, people responsible for preparing the budgets will make

efforts to identify and evaluate all the factors that are affecting the course of sales and

manufacturing process of the company so that desired projections can be made and

realistic estimations can be proposed. Preparation of sales budget: Once the factors are identified and keeping those in mind

managers can prepare sales budget and communicated to the sales department so that

they can execute their functioning accordingly. Initial preparation of various budgets: Once the Board of Directors of KBC Ltd approves

the projections of budget value so that further it can be divided into different budges so

that allocation of funds can be done on effective basis (Davis and Davis, 2012). Negotiation of budgets with superiors: After preparing all the budgets for different

departments, committee members consults with superiors of each department and if

required changes are made. Coordination and review of budgets: In this section, defined changes will take place and

reviewed once again for the final approval.

Final acceptance of budgets: This is the last stage of budgeting process in which budgets

for different departments are accepted by the top level managers and accordingly flow of

money is managed and controlled (Ezeoha, 2011).

TASK 2

A) Classification of costs

Costs in general can be defined as the amount of money spent by the firm to produce a

single unit of product or service. Further, costs can be classified on several basis which are as

follows: Function: Costs related to production (factory lighting and rent, unproductive wages),

administrative (stationery, postage etc.), selling and distribution departments

(advertisement, marketing and free samples) are considered as the function based costs

classification (Galloway and Deakins, 2012). Looking the functioning of KBC Ltd, it is

important for the managers to maintain costs related to all the defined department so that

better financial position can be achieved.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Behaviour: On the basis of behaviour costs can be classified as fixed, variable and

stepped fixed or semi-variable costs. However, fixed costs are those which does not

change despite of alter in level of production such as depreciation and insurance.

Whereas, variable costs are those which changes as per the level of output such as

material purchase. While on the other hand, stepped fixed costs is the costs which does

not changes on the basis of increase or decrease in level of activity but alter when activity

is shifted substantially for instance, management of KBC wants to by new machinery so

that they can enhance the level of production (Graff, 2003). However, semi-variable costs

can be defined as the expenditure which remains fixed up to certain level and the changes

with the level such as electricity and telephone charges.

Nature: On the basis of nature there are two types of costs direct and indirect. However,

direct costs are those which are involved in the manufacturing process of the product

such as costs of material, labour. While indirect costs are those which are not directly

charged to a product such as rent, deprecation etc.

B) Calculate fixed and variable costs

High-low method:

This method focuses on splitting a mixed costs into its fixed and variable components.

However, it is easy to understand but it is relatively unreliable because it only considers to

extreme activity level i.e. labor hours and machine hours etc (Lindholm and Suomala, 2007).

Formula:

Variable cost per unit:

Highest costs 56000

lowest costs 20000

highest unit 6100

lowest unit 2100

Variable costs per unit: Highest costs – lowest costs/ highest unit – lowest unit

Variable costs per unit: 56000-20000/6100-2100

Variable costs per unit: 36000/4000

Variable costs per unit: 9

Total fixed costs:

7

stepped fixed or semi-variable costs. However, fixed costs are those which does not

change despite of alter in level of production such as depreciation and insurance.

Whereas, variable costs are those which changes as per the level of output such as

material purchase. While on the other hand, stepped fixed costs is the costs which does

not changes on the basis of increase or decrease in level of activity but alter when activity

is shifted substantially for instance, management of KBC wants to by new machinery so

that they can enhance the level of production (Graff, 2003). However, semi-variable costs

can be defined as the expenditure which remains fixed up to certain level and the changes

with the level such as electricity and telephone charges.

Nature: On the basis of nature there are two types of costs direct and indirect. However,

direct costs are those which are involved in the manufacturing process of the product

such as costs of material, labour. While indirect costs are those which are not directly

charged to a product such as rent, deprecation etc.

B) Calculate fixed and variable costs

High-low method:

This method focuses on splitting a mixed costs into its fixed and variable components.

However, it is easy to understand but it is relatively unreliable because it only considers to

extreme activity level i.e. labor hours and machine hours etc (Lindholm and Suomala, 2007).

Formula:

Variable cost per unit:

Highest costs 56000

lowest costs 20000

highest unit 6100

lowest unit 2100

Variable costs per unit: Highest costs – lowest costs/ highest unit – lowest unit

Variable costs per unit: 56000-20000/6100-2100

Variable costs per unit: 36000/4000

Variable costs per unit: 9

Total fixed costs:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Highest costs – (Variable costs per unit*highest unit) = lowest costs – (Variable costs per

unit*lowest unit)

Total fixed costs: 56000-(9*6100) = 20000-(9*2100)

Total fixed costs: 1100 = 1100

The main purpose behind using high-low method is that it assist in obtaining cost volume

formula i.e. y = a + bx = y = 1100 + 9x

TASK 3

A) Effect of absorption and marginal costing on inventory valuation and profit determination

In terms of inventory valuation, marginal costing values inventory of the company at the

total variable production cost of a unit of product (Cooper and Kaplan, 2008). While on the other

hand, absorption costing values inventory at the full production costs of unit of product.

Furthermore, in both method inventory values will differ at the initial and end of the period. In

case, if inventory values differs than this will have direct impact on the net profit in the income

statement. However, determining of profit will differ from marginal costing principles to

absorption costing principles.

If inventory level increase absorption costing generates high profits.

If inventory level decrease marginal costing generates high profits.

If inventory level remain constant than both method provide same profit (DRURY, 2013).

B) Differentiate between various costing methods Job costing: This costing method defined as the approach which gathers all the variables

and fixed costs that are assigned to specific tasks. It is considered as the one of the best

costing method in identifying the cost of individual job (Method of costing. 2014). Batch costing: It is the identification and assignment of costs that is related to

manufacturing of certain amount of products in a batch. However, this costs of both fixed

and variable in producing the batch (Armstrong, 2014). Process costing: It refers to the accumulation of costs for the long-lasting manufacturing

run that consist of products that are vague from one another.

Service costing: It is the part of operation costing which is used in all the companies that

are services oriented (Burns, Hopper and Yazdifar, 2004).

8

unit*lowest unit)

Total fixed costs: 56000-(9*6100) = 20000-(9*2100)

Total fixed costs: 1100 = 1100

The main purpose behind using high-low method is that it assist in obtaining cost volume

formula i.e. y = a + bx = y = 1100 + 9x

TASK 3

A) Effect of absorption and marginal costing on inventory valuation and profit determination

In terms of inventory valuation, marginal costing values inventory of the company at the

total variable production cost of a unit of product (Cooper and Kaplan, 2008). While on the other

hand, absorption costing values inventory at the full production costs of unit of product.

Furthermore, in both method inventory values will differ at the initial and end of the period. In

case, if inventory values differs than this will have direct impact on the net profit in the income

statement. However, determining of profit will differ from marginal costing principles to

absorption costing principles.

If inventory level increase absorption costing generates high profits.

If inventory level decrease marginal costing generates high profits.

If inventory level remain constant than both method provide same profit (DRURY, 2013).

B) Differentiate between various costing methods Job costing: This costing method defined as the approach which gathers all the variables

and fixed costs that are assigned to specific tasks. It is considered as the one of the best

costing method in identifying the cost of individual job (Method of costing. 2014). Batch costing: It is the identification and assignment of costs that is related to

manufacturing of certain amount of products in a batch. However, this costs of both fixed

and variable in producing the batch (Armstrong, 2014). Process costing: It refers to the accumulation of costs for the long-lasting manufacturing

run that consist of products that are vague from one another.

Service costing: It is the part of operation costing which is used in all the companies that

are services oriented (Burns, Hopper and Yazdifar, 2004).

8

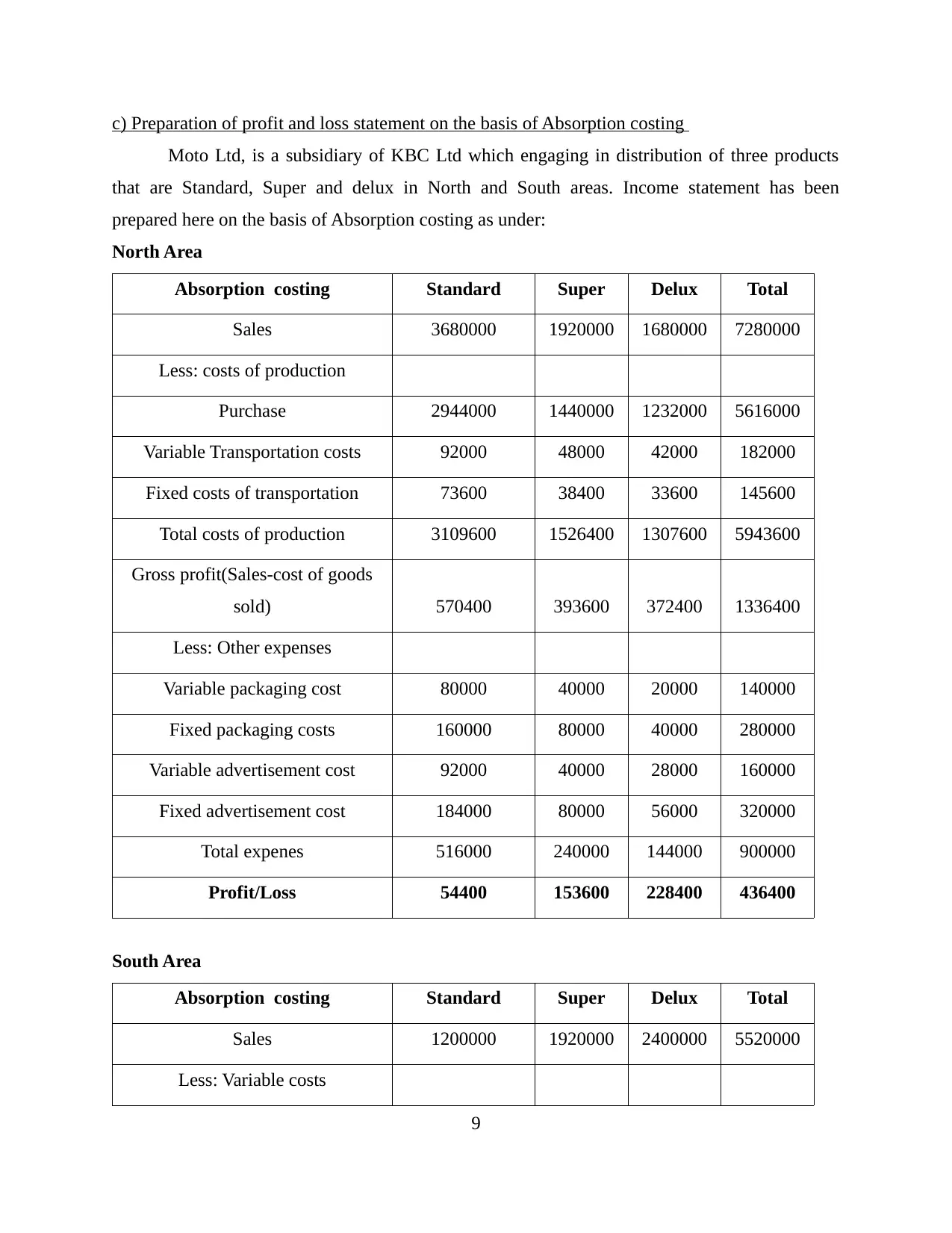

c) Preparation of profit and loss statement on the basis of Absorption costing

Moto Ltd, is a subsidiary of KBC Ltd which engaging in distribution of three products

that are Standard, Super and delux in North and South areas. Income statement has been

prepared here on the basis of Absorption costing as under:

North Area

Absorption costing Standard Super Delux Total

Sales 3680000 1920000 1680000 7280000

Less: costs of production

Purchase 2944000 1440000 1232000 5616000

Variable Transportation costs 92000 48000 42000 182000

Fixed costs of transportation 73600 38400 33600 145600

Total costs of production 3109600 1526400 1307600 5943600

Gross profit(Sales-cost of goods

sold) 570400 393600 372400 1336400

Less: Other expenses

Variable packaging cost 80000 40000 20000 140000

Fixed packaging costs 160000 80000 40000 280000

Variable advertisement cost 92000 40000 28000 160000

Fixed advertisement cost 184000 80000 56000 320000

Total expenes 516000 240000 144000 900000

Profit/Loss 54400 153600 228400 436400

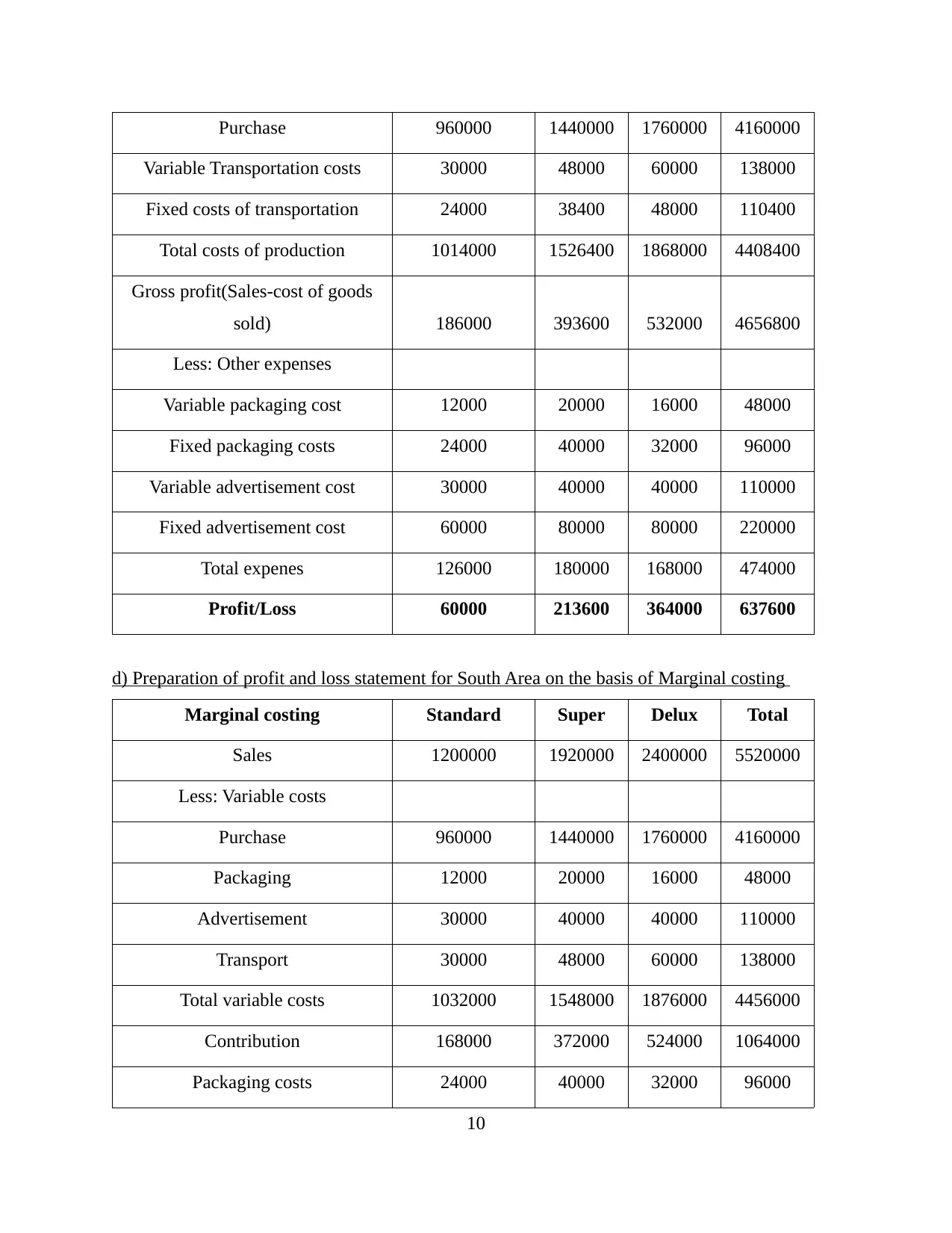

South Area

Absorption costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

9

Moto Ltd, is a subsidiary of KBC Ltd which engaging in distribution of three products

that are Standard, Super and delux in North and South areas. Income statement has been

prepared here on the basis of Absorption costing as under:

North Area

Absorption costing Standard Super Delux Total

Sales 3680000 1920000 1680000 7280000

Less: costs of production

Purchase 2944000 1440000 1232000 5616000

Variable Transportation costs 92000 48000 42000 182000

Fixed costs of transportation 73600 38400 33600 145600

Total costs of production 3109600 1526400 1307600 5943600

Gross profit(Sales-cost of goods

sold) 570400 393600 372400 1336400

Less: Other expenses

Variable packaging cost 80000 40000 20000 140000

Fixed packaging costs 160000 80000 40000 280000

Variable advertisement cost 92000 40000 28000 160000

Fixed advertisement cost 184000 80000 56000 320000

Total expenes 516000 240000 144000 900000

Profit/Loss 54400 153600 228400 436400

South Area

Absorption costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Purchase 960000 1440000 1760000 4160000

Variable Transportation costs 30000 48000 60000 138000

Fixed costs of transportation 24000 38400 48000 110400

Total costs of production 1014000 1526400 1868000 4408400

Gross profit(Sales-cost of goods

sold) 186000 393600 532000 4656800

Less: Other expenses

Variable packaging cost 12000 20000 16000 48000

Fixed packaging costs 24000 40000 32000 96000

Variable advertisement cost 30000 40000 40000 110000

Fixed advertisement cost 60000 80000 80000 220000

Total expenes 126000 180000 168000 474000

Profit/Loss 60000 213600 364000 637600

d) Preparation of profit and loss statement for South Area on the basis of Marginal costing

Marginal costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

Purchase 960000 1440000 1760000 4160000

Packaging 12000 20000 16000 48000

Advertisement 30000 40000 40000 110000

Transport 30000 48000 60000 138000

Total variable costs 1032000 1548000 1876000 4456000

Contribution 168000 372000 524000 1064000

Packaging costs 24000 40000 32000 96000

10

Variable Transportation costs 30000 48000 60000 138000

Fixed costs of transportation 24000 38400 48000 110400

Total costs of production 1014000 1526400 1868000 4408400

Gross profit(Sales-cost of goods

sold) 186000 393600 532000 4656800

Less: Other expenses

Variable packaging cost 12000 20000 16000 48000

Fixed packaging costs 24000 40000 32000 96000

Variable advertisement cost 30000 40000 40000 110000

Fixed advertisement cost 60000 80000 80000 220000

Total expenes 126000 180000 168000 474000

Profit/Loss 60000 213600 364000 637600

d) Preparation of profit and loss statement for South Area on the basis of Marginal costing

Marginal costing Standard Super Delux Total

Sales 1200000 1920000 2400000 5520000

Less: Variable costs

Purchase 960000 1440000 1760000 4160000

Packaging 12000 20000 16000 48000

Advertisement 30000 40000 40000 110000

Transport 30000 48000 60000 138000

Total variable costs 1032000 1548000 1876000 4456000

Contribution 168000 372000 524000 1064000

Packaging costs 24000 40000 32000 96000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advertisement 60000 80000 80000 220000

Transport 24000 38400 48000 110400

Total fixed costs 108000 158400 160000 426400

Profit/Loss 60000 213600 364000 637600

TASK 4

KBC Ltd, is producing 4 products A, B, D and E in its product mix. Sccenario stated that

product A and D are incurring loss worth £5000 and £3000 while, product B and E are having

loss. Therefore, Board intends to discontinue this loss contributing products so as to improve

potential profitability.

a) Advice to KBC Ltd

It can be advised that KBC Ltd, should not produce A and E product. It is because if KBC

does not manufacture this products than it can enhance its contribution to sales ratio to 23.81%.

Moreover, BEP can achieve at sales of only £2099958 which is comparatively lower than

previous BEP at £3650000. In addition, if KBC Ltd, intends to earn desired profit at £90000 than

it will require to sale amounted to £2477950.44 which is comparatively lower than overall sales

requirement worth £2902115.101. Thus by considering all the aspects, it can be advised that

KBC Ltd should discontinue its loss contributing products A and D.

b) Calculation of BEP, contribution to sales and required units to earn target profit

Particulars A B D E Total

Sales 750000 1000000 800000 1100000 3650000

Less: Variable costs

Material 180000 260000 268000 270000 978000

Labour 260000 260000 200000 280000 1000000

Variable overheads 190000 230000 210000 300000 930000

Total variable

expenses 630000 750000 678000 850000 2908000

11

Transport 24000 38400 48000 110400

Total fixed costs 108000 158400 160000 426400

Profit/Loss 60000 213600 364000 637600

TASK 4

KBC Ltd, is producing 4 products A, B, D and E in its product mix. Sccenario stated that

product A and D are incurring loss worth £5000 and £3000 while, product B and E are having

loss. Therefore, Board intends to discontinue this loss contributing products so as to improve

potential profitability.

a) Advice to KBC Ltd

It can be advised that KBC Ltd, should not produce A and E product. It is because if KBC

does not manufacture this products than it can enhance its contribution to sales ratio to 23.81%.

Moreover, BEP can achieve at sales of only £2099958 which is comparatively lower than

previous BEP at £3650000. In addition, if KBC Ltd, intends to earn desired profit at £90000 than

it will require to sale amounted to £2477950.44 which is comparatively lower than overall sales

requirement worth £2902115.101. Thus by considering all the aspects, it can be advised that

KBC Ltd should discontinue its loss contributing products A and D.

b) Calculation of BEP, contribution to sales and required units to earn target profit

Particulars A B D E Total

Sales 750000 1000000 800000 1100000 3650000

Less: Variable costs

Material 180000 260000 268000 270000 978000

Labour 260000 260000 200000 280000 1000000

Variable overheads 190000 230000 210000 300000 930000

Total variable

expenses 630000 750000 678000 850000 2908000

11

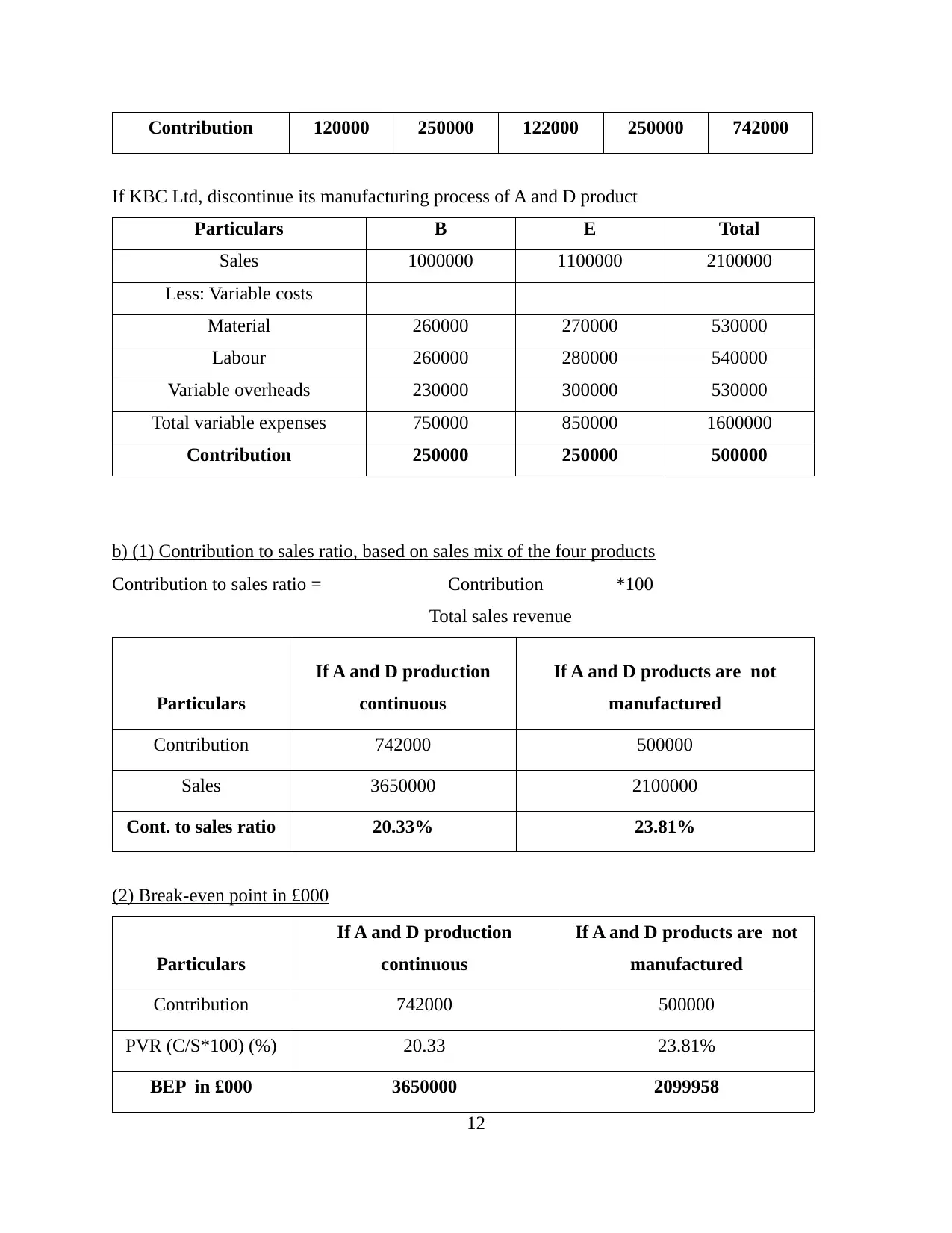

Contribution 120000 250000 122000 250000 742000

If KBC Ltd, discontinue its manufacturing process of A and D product

Particulars B E Total

Sales 1000000 1100000 2100000

Less: Variable costs

Material 260000 270000 530000

Labour 260000 280000 540000

Variable overheads 230000 300000 530000

Total variable expenses 750000 850000 1600000

Contribution 250000 250000 500000

b) (1) Contribution to sales ratio, based on sales mix of the four products

Contribution to sales ratio = Contribution *100

Total sales revenue

Particulars

If A and D production

continuous

If A and D products are not

manufactured

Contribution 742000 500000

Sales 3650000 2100000

Cont. to sales ratio 20.33% 23.81%

(2) Break-even point in £000

Particulars

If A and D production

continuous

If A and D products are not

manufactured

Contribution 742000 500000

PVR (C/S*100) (%) 20.33 23.81%

BEP in £000 3650000 2099958

12

If KBC Ltd, discontinue its manufacturing process of A and D product

Particulars B E Total

Sales 1000000 1100000 2100000

Less: Variable costs

Material 260000 270000 530000

Labour 260000 280000 540000

Variable overheads 230000 300000 530000

Total variable expenses 750000 850000 1600000

Contribution 250000 250000 500000

b) (1) Contribution to sales ratio, based on sales mix of the four products

Contribution to sales ratio = Contribution *100

Total sales revenue

Particulars

If A and D production

continuous

If A and D products are not

manufactured

Contribution 742000 500000

Sales 3650000 2100000

Cont. to sales ratio 20.33% 23.81%

(2) Break-even point in £000

Particulars

If A and D production

continuous

If A and D products are not

manufactured

Contribution 742000 500000

PVR (C/S*100) (%) 20.33 23.81%

BEP in £000 3650000 2099958

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.