Strategic Management Accounting Report: Comparing Costing Systems

VerifiedAdded on 2023/01/18

|7

|779

|58

Report

AI Summary

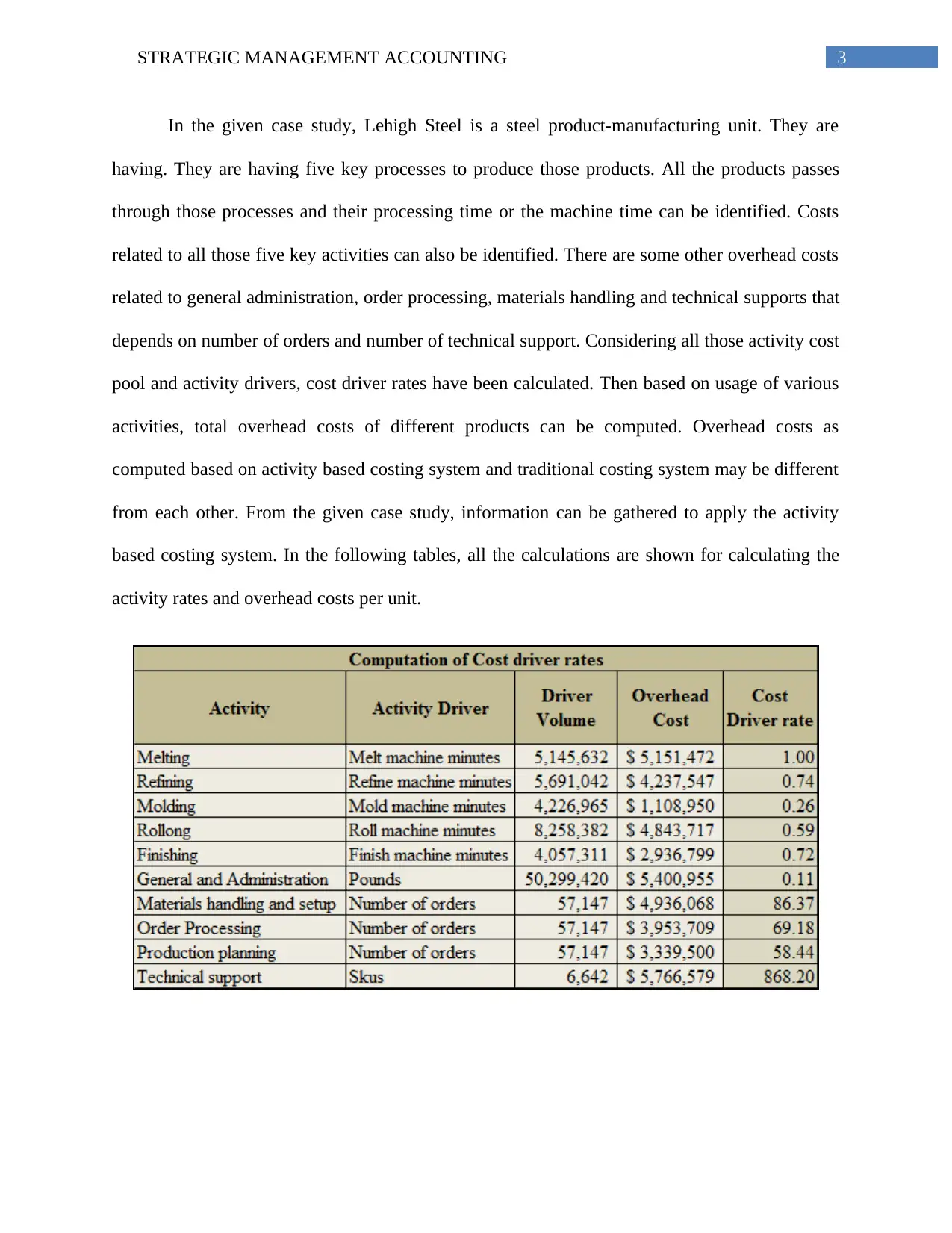

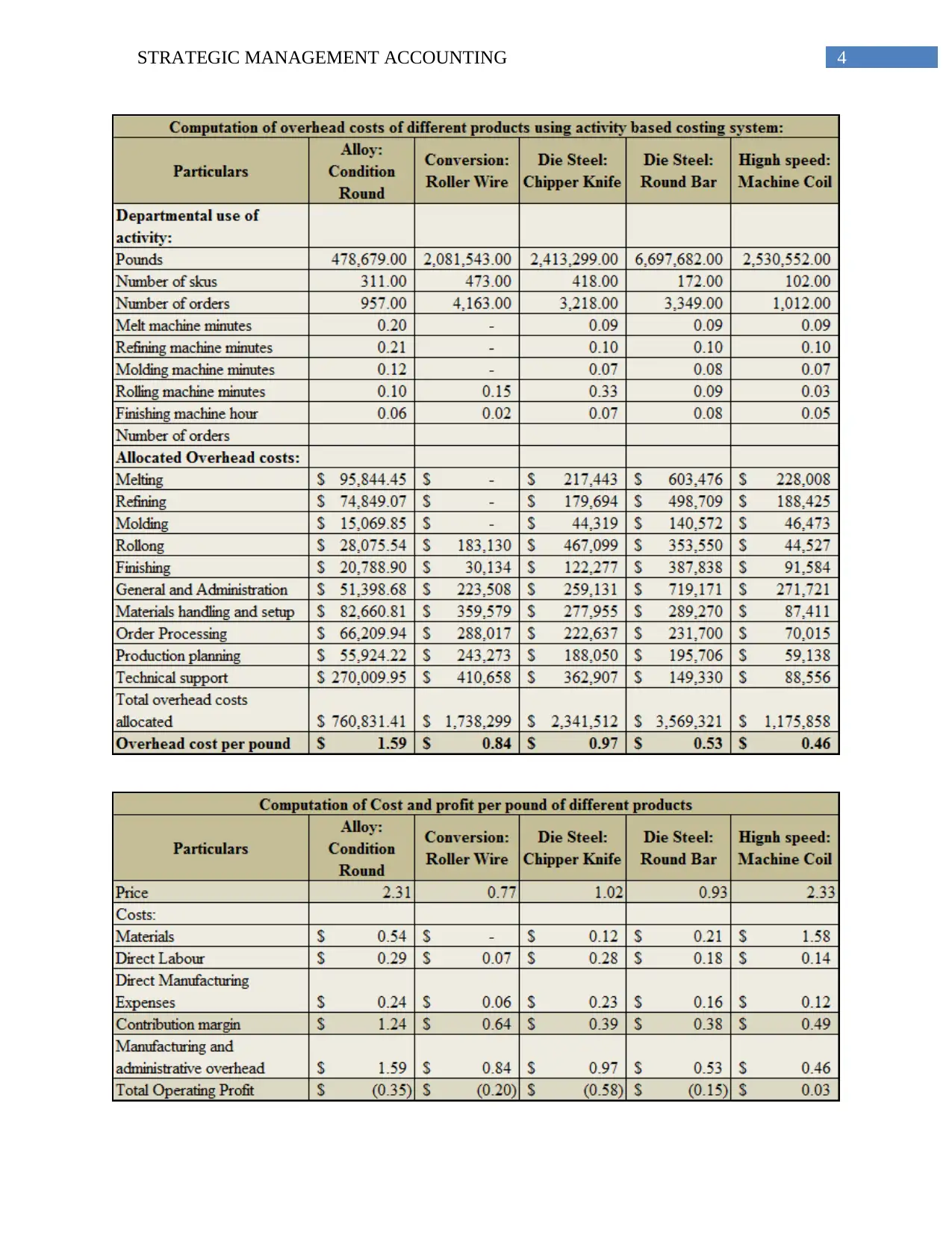

This report focuses on strategic management accounting, specifically analyzing overhead allocation methods. It begins by defining overhead costs and differentiating between traditional, volume-based, and activity-based costing systems. The report highlights the limitations of traditional methods and emphasizes the rationality and accuracy of activity-based costing (ABC). A case study of Lehigh Steel is presented, illustrating the application of ABC. The analysis includes calculations of activity rates and overhead costs per unit, demonstrating the superiority of ABC in capturing the impact of various activities on total overhead costs. The report concludes that ABC is a more appropriate and advanced method compared to traditional volume-based costing. References and bibliography are also included.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.