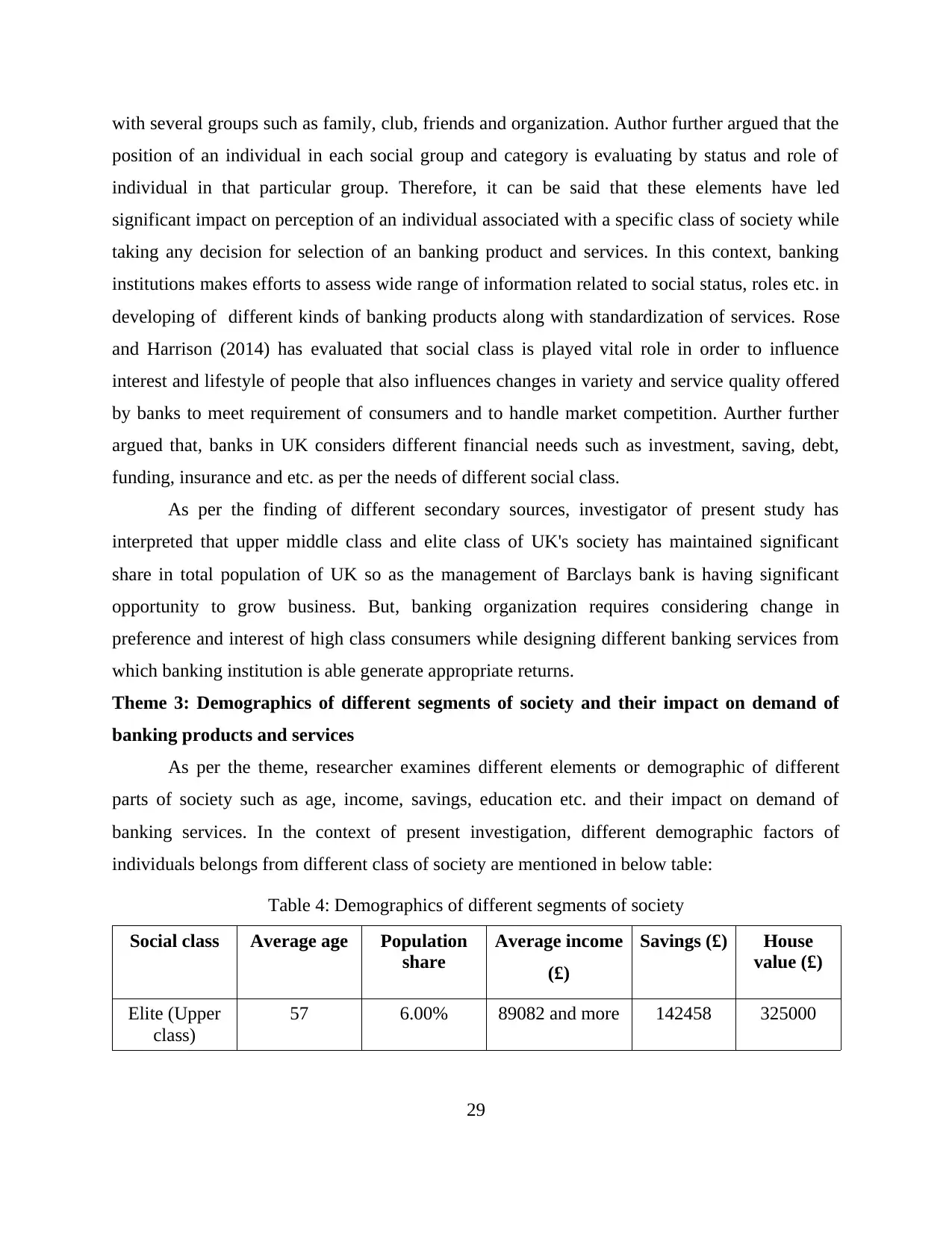

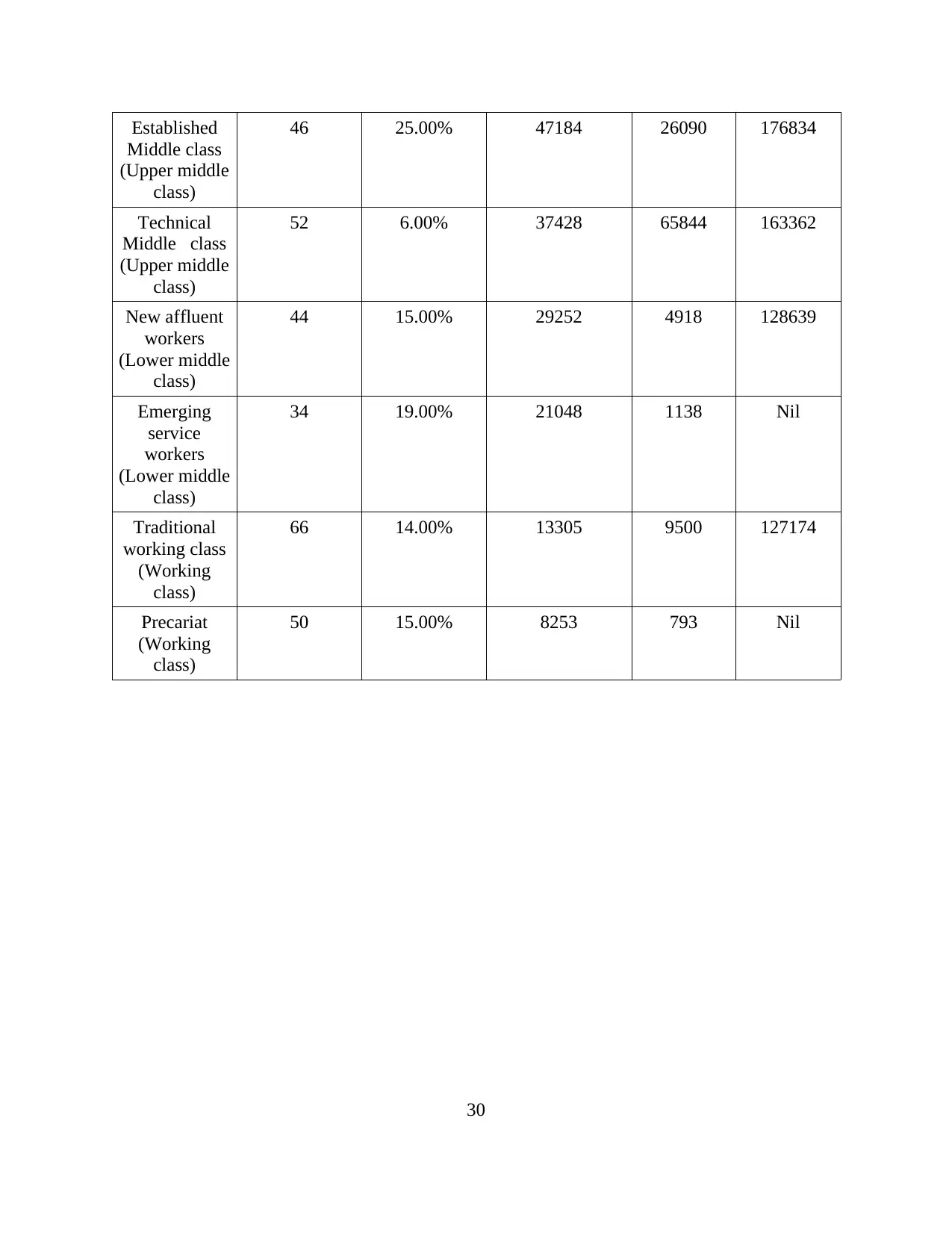

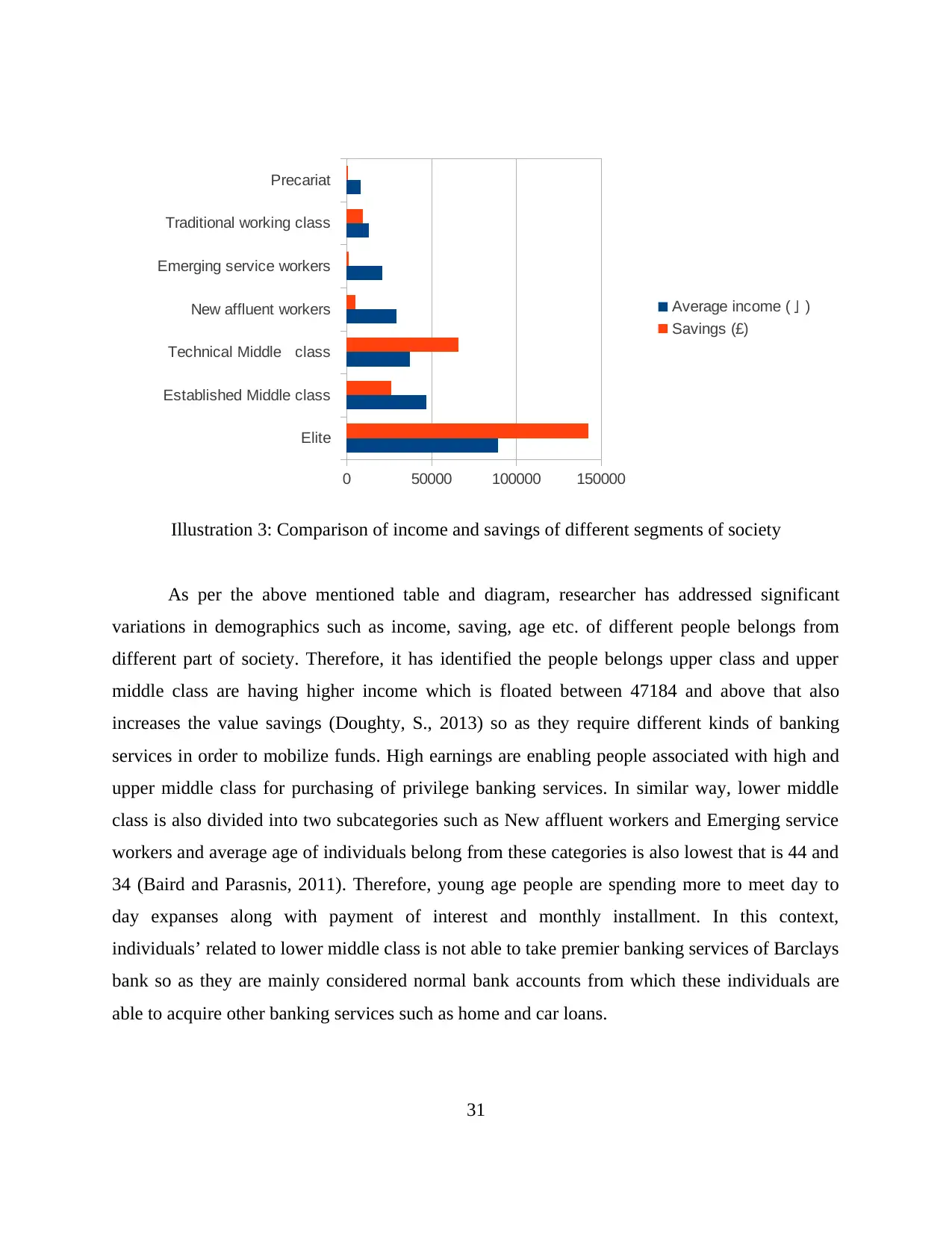

The provided content discusses the concept of social change with a global perspective, exploring the intersection of social class and financial inclusion in the context of retail banking. The texts examined include research papers on ethics in qualitative research, financial inclusion policy, and consumer financial literacy, as well as articles from online sources such as Barclays, Daily Mail, and BBC News. The content highlights the diversity of social classes in the UK, with seven distinct groups identified, and explores how these social classes influence customer demand for financial services offered by commercial banks. The summary also touches on the importance of research methodology and tools in understanding social change.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)