Tax Treatment of Various Items - Income Tax Assessment Act 1997

VerifiedAdded on 2023/06/12

|13

|2843

|176

AI Summary

This article provides a clear understanding of the tax treatment of various items under the Income Tax Assessment Act 1997. It covers service fees, interest accrued, stock in transit, bad debt, preliminary expenses, replacement, borrowing, shares, carry forward of losses, depreciation, entertainment expenses, and restrictive covenants. It also analyzes the issue of tax compliance and tax avoidance in the accounting profession.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAX

Table of Contents

Part A...............................................................................................................................................2

a)..................................................................................................................................................2

b)..................................................................................................................................................6

Part B...............................................................................................................................................7

Issues:..........................................................................................................................................7

Analyse:.......................................................................................................................................8

Critique:.......................................................................................................................................8

Conclusion:..................................................................................................................................9

Referencing....................................................................................................................................10

Table of Contents

Part A...............................................................................................................................................2

a)..................................................................................................................................................2

b)..................................................................................................................................................6

Part B...............................................................................................................................................7

Issues:..........................................................................................................................................7

Analyse:.......................................................................................................................................8

Critique:.......................................................................................................................................8

Conclusion:..................................................................................................................................9

Referencing....................................................................................................................................10

2TAX

Part A

a)

MEMORANDUM

To’

The Chief Financial Officer

Subject: Income Tax treatment of various items

The main aim of this Memo is to provide a clear understanding regarding the tax

treatment of various items discussed. The treatment is provided by refereeing to the sections,

case laws and legislations. The purpose of this memo is to discuss clearly the treatment of tax of

various items.

Item 1: Service fees

The section 4-1 of the Income tax Assessment Act 1997 provides that every individual,

company and some other entities are required to pay tax on their taxable income. The section 4-

15 of the Income Tax Assessment Act 1997 provides that income on which tax is applied is

calculated by deducting allowable deduction from the Assessable income (Gitman et al. 2015).

The income is classified into ordinary income provided under section 6-5 of the ITAA 1997 and

the statutory income provided under section 6-10 of the ITAA 1997. The income according to

the ordinary concept is referred to as the ordinary income as per section 6-5(1) of the Income

Tax Assessment Act 1997. The income that are not assessable income are statutory income as

per section 6-10 of the ITAA 1997. The income received in the form of service fees is an

ordinary income as per the section 6-5 of the act. The Taxation Ruling 98/1 deals with the

determination of income whether it is receipt based or earning. The Para 16 of the Taxation

Part A

a)

MEMORANDUM

To’

The Chief Financial Officer

Subject: Income Tax treatment of various items

The main aim of this Memo is to provide a clear understanding regarding the tax

treatment of various items discussed. The treatment is provided by refereeing to the sections,

case laws and legislations. The purpose of this memo is to discuss clearly the treatment of tax of

various items.

Item 1: Service fees

The section 4-1 of the Income tax Assessment Act 1997 provides that every individual,

company and some other entities are required to pay tax on their taxable income. The section 4-

15 of the Income Tax Assessment Act 1997 provides that income on which tax is applied is

calculated by deducting allowable deduction from the Assessable income (Gitman et al. 2015).

The income is classified into ordinary income provided under section 6-5 of the ITAA 1997 and

the statutory income provided under section 6-10 of the ITAA 1997. The income according to

the ordinary concept is referred to as the ordinary income as per section 6-5(1) of the Income

Tax Assessment Act 1997. The income that are not assessable income are statutory income as

per section 6-10 of the ITAA 1997. The income received in the form of service fees is an

ordinary income as per the section 6-5 of the act. The Taxation Ruling 98/1 deals with the

determination of income whether it is receipt based or earning. The Para 16 of the Taxation

3TAX

Ruling states that the two method of tax accounting is the receipt method and the accrual method

(Saad 2014). The Taxation Ruling 98/ 1 in Para 8 discusses receipt method or cash basis of

deriving assessable income. In the Receipt method the income is derived when the amount is

actually received. The Para 9 of the Taxation Ruling 98/1 deals with the earning method or

accrual method of determining the taxable income. In this method the income is derived when it

is earned. The Para 18 of the Taxation Ruling 98/1 states that the accounting method of receipt

basis is appropriate in the cases of income derived by employee, non-business income and

business income when the income is derived from providing knowledge. The Para 20 of the

Taxation Ruling 98/1 clearly states that the earning method is the most appropriate method of

determining business income. In the current case the service fees received should be accounted

based on earning method. Therefore, it can be said that as the service has not been provided so

income has not been earned so according to the earning method the amount received should not

be included in the assessable income (Cardew 2017).

Item 2: Interest Accrued

The Para 13 of the Taxation Ruling 98/11 provides that income from investment can

come from different sources that includes interest income. It is provided in Para 19 of the

Taxation Ruling 98/1 that it is the general rule that the income derived from investment should

be recorded in the receipt method. In the current case the interest income has not been received

so it is not taxable as per the earning method as stated in the taxation Ruling (Braithwaite 2017).

Item 3: Stock in Transit

The section 70-10 of the ITAA 1997 states that trading stock includes anything that is

held for the purpose of manufacturing, exchange or sales. The bill of lading is the detailed bill

Ruling states that the two method of tax accounting is the receipt method and the accrual method

(Saad 2014). The Taxation Ruling 98/ 1 in Para 8 discusses receipt method or cash basis of

deriving assessable income. In the Receipt method the income is derived when the amount is

actually received. The Para 9 of the Taxation Ruling 98/1 deals with the earning method or

accrual method of determining the taxable income. In this method the income is derived when it

is earned. The Para 18 of the Taxation Ruling 98/1 states that the accounting method of receipt

basis is appropriate in the cases of income derived by employee, non-business income and

business income when the income is derived from providing knowledge. The Para 20 of the

Taxation Ruling 98/1 clearly states that the earning method is the most appropriate method of

determining business income. In the current case the service fees received should be accounted

based on earning method. Therefore, it can be said that as the service has not been provided so

income has not been earned so according to the earning method the amount received should not

be included in the assessable income (Cardew 2017).

Item 2: Interest Accrued

The Para 13 of the Taxation Ruling 98/11 provides that income from investment can

come from different sources that includes interest income. It is provided in Para 19 of the

Taxation Ruling 98/1 that it is the general rule that the income derived from investment should

be recorded in the receipt method. In the current case the interest income has not been received

so it is not taxable as per the earning method as stated in the taxation Ruling (Braithwaite 2017).

Item 3: Stock in Transit

The section 70-10 of the ITAA 1997 states that trading stock includes anything that is

held for the purpose of manufacturing, exchange or sales. The bill of lading is the detailed bill

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAX

that is given for the cargo of the ship. In this case the bill of lading has not been received but has

claimed an expenses of $50000 for the trading stock. The Taxation Determination TD 93/138

deals with the expenses that are incurred for purchasing the imported stock that are in transit and

the bill of lading has not been received. The section 51 (1) of ITAA 1997 provides that it is

precondition for deductibility that the legal liability or obligation is not payable but it should be

due. The Para 6 of the Taxation Ruling IT 2625 states that whether a liability exists in any

particular situation is determined as the matter of fact or that particular case. There is no

particular rule for determining the liability that exists in purchase for stock in transit. The Para 2

of the TD 93/138 provides that it is held that liability does not exist if there is no bill of lading.

Therefore in this case as the bill of lading has not been received so expenses cannot be claimed

(Symes 2016).

Item 4: Bad debt

The Taxation Ruling 92/ 18 deals with the issue of bad debt in the income tax law. The

ruling clearly specifies the circumstances under which the assesse can claim deduction in respect

of bad debts. Section 63 deals with the deduction that is receivable by the assesse in respect of

the bad debt. As specified in the para 31 a debt can be considered to have gone bad in the

following cases:

a) The debtor has died and left behind inadequate assets for the recovery of the entire

amount.

b) It has not been possible to trace the debtor and the creditor has no access to such assets

against which actions could be taken (Katic and Leigh 2016).

that is given for the cargo of the ship. In this case the bill of lading has not been received but has

claimed an expenses of $50000 for the trading stock. The Taxation Determination TD 93/138

deals with the expenses that are incurred for purchasing the imported stock that are in transit and

the bill of lading has not been received. The section 51 (1) of ITAA 1997 provides that it is

precondition for deductibility that the legal liability or obligation is not payable but it should be

due. The Para 6 of the Taxation Ruling IT 2625 states that whether a liability exists in any

particular situation is determined as the matter of fact or that particular case. There is no

particular rule for determining the liability that exists in purchase for stock in transit. The Para 2

of the TD 93/138 provides that it is held that liability does not exist if there is no bill of lading.

Therefore in this case as the bill of lading has not been received so expenses cannot be claimed

(Symes 2016).

Item 4: Bad debt

The Taxation Ruling 92/ 18 deals with the issue of bad debt in the income tax law. The

ruling clearly specifies the circumstances under which the assesse can claim deduction in respect

of bad debts. Section 63 deals with the deduction that is receivable by the assesse in respect of

the bad debt. As specified in the para 31 a debt can be considered to have gone bad in the

following cases:

a) The debtor has died and left behind inadequate assets for the recovery of the entire

amount.

b) It has not been possible to trace the debtor and the creditor has no access to such assets

against which actions could be taken (Katic and Leigh 2016).

5TAX

c) The debt has been made statute barred and it is expected that the debtor is going to rely

on this fact as his defense for non-payment.

d) If the amount is due from a company and the company is in liquidation or receivership

and there is insufficient assets available to pay the whole of debt or a part of it.

e) After considering all the facts and probabilities there is not chance that the debt or a part

of it is going to be recovered.

Therefore in this case the director should evaluate the particular situation as stated above and

then determine the bad debt expenses. It is provided that in order to claim deduction for bad debt

it is necessary to write off the bad debt.

Item 5: Preliminary expenses

The issue of the deduction of preliminary expense is dealt with by the statute under s40-880.

For the purpose of availing the deduction the expenditure must:

a) Be related to the business that is being proposed to carry on and

b) Is either

i) Incurred for the purpose of obtaining advice or services in relation to the

proposed structure or in respect of the proposed operations for the business to be

carried out.

ii) Or is a type of payment that is being given to Australian government agency as a

fee, tax or charge which is incurred in respect of setting up of a business and to

establish the structure of its operations.

c) The debt has been made statute barred and it is expected that the debtor is going to rely

on this fact as his defense for non-payment.

d) If the amount is due from a company and the company is in liquidation or receivership

and there is insufficient assets available to pay the whole of debt or a part of it.

e) After considering all the facts and probabilities there is not chance that the debt or a part

of it is going to be recovered.

Therefore in this case the director should evaluate the particular situation as stated above and

then determine the bad debt expenses. It is provided that in order to claim deduction for bad debt

it is necessary to write off the bad debt.

Item 5: Preliminary expenses

The issue of the deduction of preliminary expense is dealt with by the statute under s40-880.

For the purpose of availing the deduction the expenditure must:

a) Be related to the business that is being proposed to carry on and

b) Is either

i) Incurred for the purpose of obtaining advice or services in relation to the

proposed structure or in respect of the proposed operations for the business to be

carried out.

ii) Or is a type of payment that is being given to Australian government agency as a

fee, tax or charge which is incurred in respect of setting up of a business and to

establish the structure of its operations.

6TAX

The Taxation Ruling 2011/6 provides that taxable purpose test applies to expenditure

under the above section. The Para 26 of the TR 2011/6 provides that only expenditures that are

incurred for current business, former business or proposed business is allowed as deduction. In

this case company has incurred the expenses for obtaining service or advice for the purpose of

business so it is an allowable expense.

Item 6: Replacement

The section 25-10 of the Income Tax Assessment Act 1997 states that expenses that are

incurred for repairing the premises or depreciable assets that are used for producing the

assessable income can be claimed as deduction. The Para 32 of the Taxation Ruling 97/23

states that expenses incurred for replacement or renewal of a part is regarded as capital expenses

and not repair. In this case the expense that have been incurred for replacement of the celling is a

capital expenditure and should not be allowed as deduction (Coxon 2016).

Item 7: Borrowing

The section 25-25 of the Income Tax Assessment Act 1997 states that expenditure

incurred for borrowing money in order to use that for producing the assessable income is an

allowed deduction. In the current case the borrowing expenses has not produced any assessable

income so it cannot be allowed as deduction. However the deduction for interest is allowed in

calculating the capital gain for sale of factory building (McCluskey and Franzsen 2017).

Item 8: Shares

The section 102-5(1) of the Income Tax Assessment Act 1997 provides that the net

capital gain should be included in the assessable income. In this case the capital gain of $130000

made from the sale of shares should be included in the assessable income.

The Taxation Ruling 2011/6 provides that taxable purpose test applies to expenditure

under the above section. The Para 26 of the TR 2011/6 provides that only expenditures that are

incurred for current business, former business or proposed business is allowed as deduction. In

this case company has incurred the expenses for obtaining service or advice for the purpose of

business so it is an allowable expense.

Item 6: Replacement

The section 25-10 of the Income Tax Assessment Act 1997 states that expenses that are

incurred for repairing the premises or depreciable assets that are used for producing the

assessable income can be claimed as deduction. The Para 32 of the Taxation Ruling 97/23

states that expenses incurred for replacement or renewal of a part is regarded as capital expenses

and not repair. In this case the expense that have been incurred for replacement of the celling is a

capital expenditure and should not be allowed as deduction (Coxon 2016).

Item 7: Borrowing

The section 25-25 of the Income Tax Assessment Act 1997 states that expenditure

incurred for borrowing money in order to use that for producing the assessable income is an

allowed deduction. In the current case the borrowing expenses has not produced any assessable

income so it cannot be allowed as deduction. However the deduction for interest is allowed in

calculating the capital gain for sale of factory building (McCluskey and Franzsen 2017).

Item 8: Shares

The section 102-5(1) of the Income Tax Assessment Act 1997 provides that the net

capital gain should be included in the assessable income. In this case the capital gain of $130000

made from the sale of shares should be included in the assessable income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

Item 9: Carry forward of losses

The section 960-20(3) of the Income Tax Assessment Act 1997 provides that the net

capital loses is utilized for reducing the capital gain. In the current case the capital losses of

$35000 of the previous year should be set off against the capital gain (McIntosh et al. 2015).

Item 10: Depreciation

The depreciation for the income tax purpose is $112000 and it is allowed as deduction.

The depreciation expenses of $120000 claimed should be added back and the expenses of

$112000 should be claimed.

Item 11: Entertainment Expenses

The Taxation Ruling 97/17 deals with the entertainment expenses incurred. The section

32-5 of the Income Tax Assessment Act 1997 states that the expenses incurred for providing

entertainment is not an allowed expenditure. However section 32-20 of the Income Tax

Assessment Act 1997 states that entertainment expenses on which fringe benefit tax is paid is

allowed as deduction. Therefore the entertainment expenses is allowed as deduction.

Item 12: Restrictive Covenants

The Taxation Ruling 94/D33 deals with the restrictive covenants and trade ties. The

expenses that is paid for restricting competition is an allowable expenses. However, the expenses

should be claimed over the 5 year period (Okello 2014).

b)

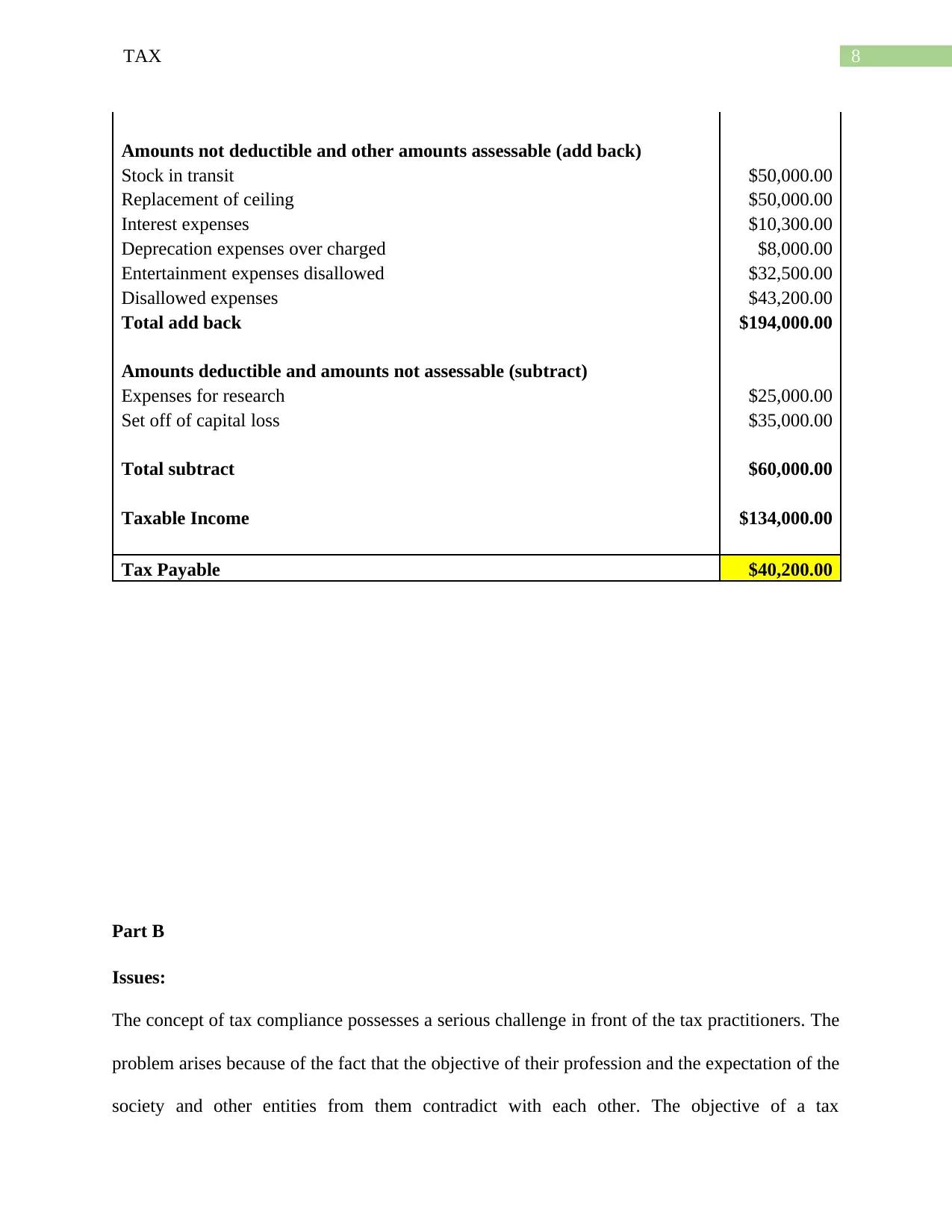

Calculation of Tax Payable

Particulars Amount

Net Accounting Profit $620,500.00

Item 9: Carry forward of losses

The section 960-20(3) of the Income Tax Assessment Act 1997 provides that the net

capital loses is utilized for reducing the capital gain. In the current case the capital losses of

$35000 of the previous year should be set off against the capital gain (McIntosh et al. 2015).

Item 10: Depreciation

The depreciation for the income tax purpose is $112000 and it is allowed as deduction.

The depreciation expenses of $120000 claimed should be added back and the expenses of

$112000 should be claimed.

Item 11: Entertainment Expenses

The Taxation Ruling 97/17 deals with the entertainment expenses incurred. The section

32-5 of the Income Tax Assessment Act 1997 states that the expenses incurred for providing

entertainment is not an allowed expenditure. However section 32-20 of the Income Tax

Assessment Act 1997 states that entertainment expenses on which fringe benefit tax is paid is

allowed as deduction. Therefore the entertainment expenses is allowed as deduction.

Item 12: Restrictive Covenants

The Taxation Ruling 94/D33 deals with the restrictive covenants and trade ties. The

expenses that is paid for restricting competition is an allowable expenses. However, the expenses

should be claimed over the 5 year period (Okello 2014).

b)

Calculation of Tax Payable

Particulars Amount

Net Accounting Profit $620,500.00

8TAX

Amounts not deductible and other amounts assessable (add back)

Stock in transit $50,000.00

Replacement of ceiling $50,000.00

Interest expenses $10,300.00

Deprecation expenses over charged $8,000.00

Entertainment expenses disallowed $32,500.00

Disallowed expenses $43,200.00

Total add back $194,000.00

Amounts deductible and amounts not assessable (subtract)

Expenses for research $25,000.00

Set off of capital loss $35,000.00

Total subtract $60,000.00

Taxable Income $134,000.00

Tax Payable $40,200.00

Part B

Issues:

The concept of tax compliance possesses a serious challenge in front of the tax practitioners. The

problem arises because of the fact that the objective of their profession and the expectation of the

society and other entities from them contradict with each other. The objective of a tax

Amounts not deductible and other amounts assessable (add back)

Stock in transit $50,000.00

Replacement of ceiling $50,000.00

Interest expenses $10,300.00

Deprecation expenses over charged $8,000.00

Entertainment expenses disallowed $32,500.00

Disallowed expenses $43,200.00

Total add back $194,000.00

Amounts deductible and amounts not assessable (subtract)

Expenses for research $25,000.00

Set off of capital loss $35,000.00

Total subtract $60,000.00

Taxable Income $134,000.00

Tax Payable $40,200.00

Part B

Issues:

The concept of tax compliance possesses a serious challenge in front of the tax practitioners. The

problem arises because of the fact that the objective of their profession and the expectation of the

society and other entities from them contradict with each other. The objective of a tax

9TAX

practitioner is to ensure that his client is giving only the requisite amount of tax. The payment of

which will not attract any tax obligation on the part of the client. But, in order to do that the tax

practitioner have to ensure that he is able to utilise any sort of loophole present in the law to the

benefit of the client. On the other hand, due to these sorts of practices adopted by the accountant

the state is derived from substantial amount of funds that could have been used for the purpose of

welfare of the society.

Analyse:

In today’s world, the concept of tax avoidance has become the most debated topic for the entire

genre of public that is dependent on the expenditure incurred by the government for the purpose

of development of the country. At a time when the government is trying to bridge the gap

between the economic disparities among the population of the county, systematic tax avoidance

is posing a serious threat to the society (Duong and Evans 2016). The reason being that the

government becomes helpless in this kind of situation. The tax is levied on the amount of profit

earned by the company at the end of the year. Now the amount of the profit can be adjusted by

many non-cash and non-real expenditures. The accountants make use of these loopholes and thus

enable the client company to prevent taxes. The accountant must also look or factor in the ethical

aspect of their profession, which prohibits them from adapting to practices that might harm the

interest of the community at large. The accountants must make sure that the tax advantage

accruing towards the company are real in terms of validity and authenticity (Chang et al. 2016).

Critique:

The allegation that the companies and the big corporate houses make use of the loopholes

present in the law to avoid tax systematically is true but at the same time inconclusive. In other

words, it is not the fault of the company that there are severe loopholes in the provisions made by

practitioner is to ensure that his client is giving only the requisite amount of tax. The payment of

which will not attract any tax obligation on the part of the client. But, in order to do that the tax

practitioner have to ensure that he is able to utilise any sort of loophole present in the law to the

benefit of the client. On the other hand, due to these sorts of practices adopted by the accountant

the state is derived from substantial amount of funds that could have been used for the purpose of

welfare of the society.

Analyse:

In today’s world, the concept of tax avoidance has become the most debated topic for the entire

genre of public that is dependent on the expenditure incurred by the government for the purpose

of development of the country. At a time when the government is trying to bridge the gap

between the economic disparities among the population of the county, systematic tax avoidance

is posing a serious threat to the society (Duong and Evans 2016). The reason being that the

government becomes helpless in this kind of situation. The tax is levied on the amount of profit

earned by the company at the end of the year. Now the amount of the profit can be adjusted by

many non-cash and non-real expenditures. The accountants make use of these loopholes and thus

enable the client company to prevent taxes. The accountant must also look or factor in the ethical

aspect of their profession, which prohibits them from adapting to practices that might harm the

interest of the community at large. The accountants must make sure that the tax advantage

accruing towards the company are real in terms of validity and authenticity (Chang et al. 2016).

Critique:

The allegation that the companies and the big corporate houses make use of the loopholes

present in the law to avoid tax systematically is true but at the same time inconclusive. In other

words, it is not the fault of the company that there are severe loopholes in the provisions made by

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAX

the state. The company’s main objective is to maximise the returns for its shareholders. If the

company is able to reduce its tax burden without incurring any legal penalties or actions the

companies will continue to operate in the same manner. Having said that the company must

remember that the society gave it the power and right to use its resources and hence it should

give something back to it. Otherwise, the society will take away the powers granted by it to the

company.

Conclusion:

In order to address the issue the government, the accountants and the companies will have to

collectively perform their part. The government must make sure that there is no big loophole in

the tax provision, which could be misused. The accountant must adhere to ethical practices while

–performing his duty and the company must refrain from taking undue advantage of the

resources that has been granted to it by the stakeholders for the purpose of creating value for

them and the society at large.

the state. The company’s main objective is to maximise the returns for its shareholders. If the

company is able to reduce its tax burden without incurring any legal penalties or actions the

companies will continue to operate in the same manner. Having said that the company must

remember that the society gave it the power and right to use its resources and hence it should

give something back to it. Otherwise, the society will take away the powers granted by it to the

company.

Conclusion:

In order to address the issue the government, the accountants and the companies will have to

collectively perform their part. The government must make sure that there is no big loophole in

the tax provision, which could be misused. The accountant must adhere to ethical practices while

–performing his duty and the company must refrain from taking undue advantage of the

resources that has been granted to it by the stakeholders for the purpose of creating value for

them and the society at large.

11TAX

Referencing

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cardew, R., 2017. Privatisation of infrastructure in Sydney, Australia. In Infrastructure

Provision and the Negotiating Process (pp. 129-146). Routledge.

Chang, Y., Fang, Z. and Li, Y., 2016. Renewable energy policies in promoting financing and

investment among the East Asia Summit countries: Quantitative assessment and policy

implications. Energy Policy, 95, pp.427-436.

Coxon, H., 2016. Australian Official Publications: Guides to Official Publications. Elsevier.

Duong, L. and Evans, J., 2016. Gender differences in compensation and earnings management:

Evidence from Australian CFOs. Pacific-Basin Finance Journal, 40, pp.17-35.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Katic, P. and Leigh, A., 2016. Top wealth shares in Australia 1915–2012. Review of Income and

Wealth, 62(2), pp.209-222.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

McIntosh, J., Trubka, R. and Newman, P., 2015. Tax Increment Financing framework for

integrated transit and urban renewal projects in car-dependent cities. Urban Policy and

Research, 33(1), pp.37-60.

Referencing

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cardew, R., 2017. Privatisation of infrastructure in Sydney, Australia. In Infrastructure

Provision and the Negotiating Process (pp. 129-146). Routledge.

Chang, Y., Fang, Z. and Li, Y., 2016. Renewable energy policies in promoting financing and

investment among the East Asia Summit countries: Quantitative assessment and policy

implications. Energy Policy, 95, pp.427-436.

Coxon, H., 2016. Australian Official Publications: Guides to Official Publications. Elsevier.

Duong, L. and Evans, J., 2016. Gender differences in compensation and earnings management:

Evidence from Australian CFOs. Pacific-Basin Finance Journal, 40, pp.17-35.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Katic, P. and Leigh, A., 2016. Top wealth shares in Australia 1915–2012. Review of Income and

Wealth, 62(2), pp.209-222.

McCluskey, W.J. and Franzsen, R.C., 2017. Land value taxation: An applied analysis.

Routledge.

McIntosh, J., Trubka, R. and Newman, P., 2015. Tax Increment Financing framework for

integrated transit and urban renewal projects in car-dependent cities. Urban Policy and

Research, 33(1), pp.37-60.

12TAX

Okello, A., 2014. Managing Income Tax Compliance through Self-Assessment (No. 14-41).

International Monetary Fund.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Symes, C.F., 2016. Statutory priorities in corporate insolvency law: an analysis of preferred

creditor status. Routledge.

Okello, A., 2014. Managing Income Tax Compliance through Self-Assessment (No. 14-41).

International Monetary Fund.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Symes, C.F., 2016. Statutory priorities in corporate insolvency law: an analysis of preferred

creditor status. Routledge.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.