Taxation and Business Transactions

VerifiedAdded on 2020/04/01

|7

|2220

|35

AI Summary

This assignment delves into the complexities of taxation within various business contexts. It examines scenarios involving income reduction strategies, logging firm agreements, and emphasizes the importance of ethical practices when navigating tax regulations. The focus is on understanding how legal frameworks impact financial decisions and the potential consequences of unethical tax avoidance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation

<Student ID>

<Student Name>

<University Name>

<Student ID>

<Student Name>

<University Name>

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1. Eric’s net capital gain or loss for the year

Issue:

In the past 12 months, Eric has acquired various assets such as an antique vase, an antique

chair, a painting, a home sound system, and shares in a listed company. Last week he has sold

the same for different values. This shows that the assets were in his possession for less than a

year1. Thus his net capital gain or loss this year would be short-term in nature. The taxability

aspect of capital gains can be realized only when the sale proceeds from the assets are greater

than the cost base at which they have been purchased. A significant observation is that Eric

would not be able to take advantage of the indexation model since the assets were held by

him for less than 12 months2.

Rule:

When an individual buys assets in order to meet his personal needs or recreation purposes,

the same can be termed as “assets for personal use”. Collectibles are the assets that are of

lower quantity but of higher value. Eric’s assets like the home sound system and the shares of

the listed firm belong to “assets for personal use” category whereas the antique vase, antique

chair, and painting can be categorized under collectibles3.

When assets with the procurement cost of less than USD 10,000 are sold, the capital profits

from such sale are not subject to taxation. In the given situation, assets for Eric’s personal are

the home sound system worth USD 12,000 and the shares in a listed organization worth USD

5,000.

Application

The other assets that were sold be Eric were collectibles. As per the taxation rules, the capital

gains that an individual acquires from such sale, whose procurement cost is at par with or less

than USD 500 cannot be subject to tax4. Eric’s collectibles included antique vase worth USD

2,000, antique chair worth USD 3,000, and the painting worth USD 9,000. The provided

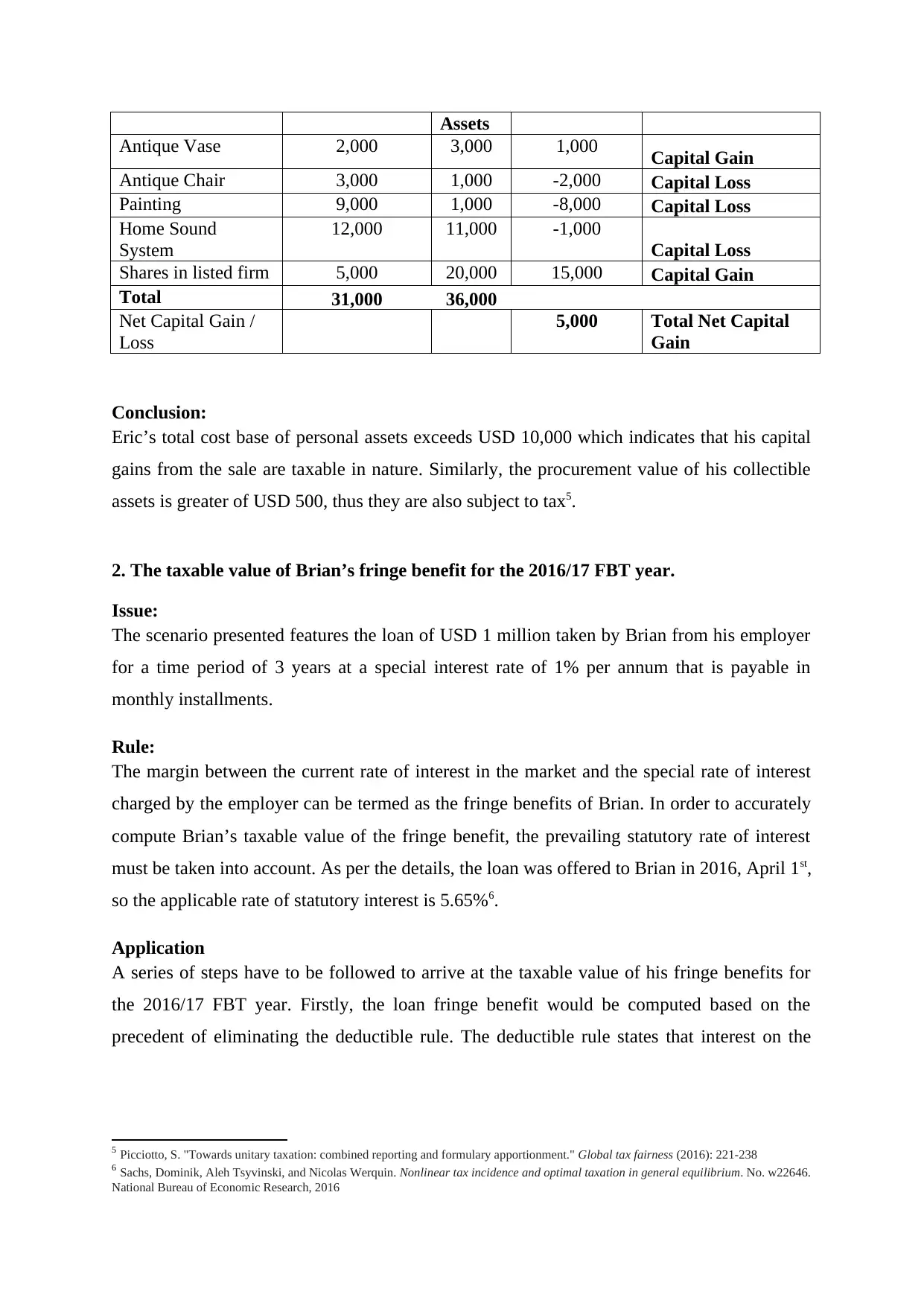

information has been used to determine Eric’s capital performance:

Assets Cost base of

Assets

Capital

Procee

ds of

Difference

value

Net Capital Gain/

(Net Capital Loss)

1 Serrato, Juan Carlos Suárez, and Owen M. Zidar. The Structure of State Corporate Taxation and its Impact on State Tax Revenues and

Economic Activity. No. w23653. National Bureau of Economic Research, 2017

2 Sierra, Gretchen, Rosanne Altshuler, Ray Beeman, and Ronald Dickel. "Cross-Border Taxation: Exploring Options." Taxes 92 (2014): 95

3 Spilker, Brian, B. C. Ayers, J. Robinson, E. Outslay, R. G. Worsham, J. A. Barrick, and C. Weaver. "Taxation of Business Entities."

(2014)

4 Foucault, Martial, Katsunori Seki, and Guy D. Whitten. "Good times, bad times: Taxation and electoral accountability." Electoral

Studies 45 (2017): 191-200.

Issue:

In the past 12 months, Eric has acquired various assets such as an antique vase, an antique

chair, a painting, a home sound system, and shares in a listed company. Last week he has sold

the same for different values. This shows that the assets were in his possession for less than a

year1. Thus his net capital gain or loss this year would be short-term in nature. The taxability

aspect of capital gains can be realized only when the sale proceeds from the assets are greater

than the cost base at which they have been purchased. A significant observation is that Eric

would not be able to take advantage of the indexation model since the assets were held by

him for less than 12 months2.

Rule:

When an individual buys assets in order to meet his personal needs or recreation purposes,

the same can be termed as “assets for personal use”. Collectibles are the assets that are of

lower quantity but of higher value. Eric’s assets like the home sound system and the shares of

the listed firm belong to “assets for personal use” category whereas the antique vase, antique

chair, and painting can be categorized under collectibles3.

When assets with the procurement cost of less than USD 10,000 are sold, the capital profits

from such sale are not subject to taxation. In the given situation, assets for Eric’s personal are

the home sound system worth USD 12,000 and the shares in a listed organization worth USD

5,000.

Application

The other assets that were sold be Eric were collectibles. As per the taxation rules, the capital

gains that an individual acquires from such sale, whose procurement cost is at par with or less

than USD 500 cannot be subject to tax4. Eric’s collectibles included antique vase worth USD

2,000, antique chair worth USD 3,000, and the painting worth USD 9,000. The provided

information has been used to determine Eric’s capital performance:

Assets Cost base of

Assets

Capital

Procee

ds of

Difference

value

Net Capital Gain/

(Net Capital Loss)

1 Serrato, Juan Carlos Suárez, and Owen M. Zidar. The Structure of State Corporate Taxation and its Impact on State Tax Revenues and

Economic Activity. No. w23653. National Bureau of Economic Research, 2017

2 Sierra, Gretchen, Rosanne Altshuler, Ray Beeman, and Ronald Dickel. "Cross-Border Taxation: Exploring Options." Taxes 92 (2014): 95

3 Spilker, Brian, B. C. Ayers, J. Robinson, E. Outslay, R. G. Worsham, J. A. Barrick, and C. Weaver. "Taxation of Business Entities."

(2014)

4 Foucault, Martial, Katsunori Seki, and Guy D. Whitten. "Good times, bad times: Taxation and electoral accountability." Electoral

Studies 45 (2017): 191-200.

Assets

Antique Vase 2,000 3,000 1,000 Capital Gain

Antique Chair 3,000 1,000 -2,000 Capital Loss

Painting 9,000 1,000 -8,000 Capital Loss

Home Sound

System

12,000 11,000 -1,000

Capital Loss

Shares in listed firm 5,000 20,000 15,000 Capital Gain

Total 31,000 36,000

Net Capital Gain /

Loss

5,000 Total Net Capital

Gain

Conclusion:

Eric’s total cost base of personal assets exceeds USD 10,000 which indicates that his capital

gains from the sale are taxable in nature. Similarly, the procurement value of his collectible

assets is greater of USD 500, thus they are also subject to tax5.

2. The taxable value of Brian’s fringe benefit for the 2016/17 FBT year.

Issue:

The scenario presented features the loan of USD 1 million taken by Brian from his employer

for a time period of 3 years at a special interest rate of 1% per annum that is payable in

monthly installments.

Rule:

The margin between the current rate of interest in the market and the special rate of interest

charged by the employer can be termed as the fringe benefits of Brian. In order to accurately

compute Brian’s taxable value of the fringe benefit, the prevailing statutory rate of interest

must be taken into account. As per the details, the loan was offered to Brian in 2016, April 1st,

so the applicable rate of statutory interest is 5.65%6.

Application

A series of steps have to be followed to arrive at the taxable value of his fringe benefits for

the 2016/17 FBT year. Firstly, the loan fringe benefit would be computed based on the

precedent of eliminating the deductible rule. The deductible rule states that interest on the

5 Picciotto, S. "Towards unitary taxation: combined reporting and formulary apportionment." Global tax fairness (2016): 221-238

6 Sachs, Dominik, Aleh Tsyvinski, and Nicolas Werquin. Nonlinear tax incidence and optimal taxation in general equilibrium. No. w22646.

National Bureau of Economic Research, 2016

Antique Vase 2,000 3,000 1,000 Capital Gain

Antique Chair 3,000 1,000 -2,000 Capital Loss

Painting 9,000 1,000 -8,000 Capital Loss

Home Sound

System

12,000 11,000 -1,000

Capital Loss

Shares in listed firm 5,000 20,000 15,000 Capital Gain

Total 31,000 36,000

Net Capital Gain /

Loss

5,000 Total Net Capital

Gain

Conclusion:

Eric’s total cost base of personal assets exceeds USD 10,000 which indicates that his capital

gains from the sale are taxable in nature. Similarly, the procurement value of his collectible

assets is greater of USD 500, thus they are also subject to tax5.

2. The taxable value of Brian’s fringe benefit for the 2016/17 FBT year.

Issue:

The scenario presented features the loan of USD 1 million taken by Brian from his employer

for a time period of 3 years at a special interest rate of 1% per annum that is payable in

monthly installments.

Rule:

The margin between the current rate of interest in the market and the special rate of interest

charged by the employer can be termed as the fringe benefits of Brian. In order to accurately

compute Brian’s taxable value of the fringe benefit, the prevailing statutory rate of interest

must be taken into account. As per the details, the loan was offered to Brian in 2016, April 1st,

so the applicable rate of statutory interest is 5.65%6.

Application

A series of steps have to be followed to arrive at the taxable value of his fringe benefits for

the 2016/17 FBT year. Firstly, the loan fringe benefit would be computed based on the

precedent of eliminating the deductible rule. The deductible rule states that interest on the

5 Picciotto, S. "Towards unitary taxation: combined reporting and formulary apportionment." Global tax fairness (2016): 221-238

6 Sachs, Dominik, Aleh Tsyvinski, and Nicolas Werquin. Nonlinear tax incidence and optimal taxation in general equilibrium. No. w22646.

National Bureau of Economic Research, 2016

loan as per actual interest rate must be subtracted from the interest on the loan based on the

statutory interest rate7.

(1)Thus Interest value based on statutory interest rate of 5.65% = USD 10,00,000 * 5.65% =

USD 56,500 and interest value based on actual interest rate of 1.00%) = USD 10,00,000 *

1.00% = USD 10,000. So derived loan fringe benefits = USD 56,500- USD 10,000 = USD

46,500.

(2)The interest value based on the statutory interest rate is USD 56,500 (USD 10,00,000 *

5.65%). The particular assumption made at this stage is that this value is the real amount

payable.

(3)As per provided details, Brian has used 40% of the financial loan for income-producing

purposes and other financial obligations. So his tax-deductible interest expense is USD

56,500 * 40% = USD 22,600. This is a hypothetical figure.

(4)His real tax-deductible interest expense must be calculated, which is USD 10,000 * 40% =

USD 4,000.

(5)The real tax-deductible interest expense has to be deducted from the hypothetical value:

USD 22,600 - USD 4,000 = USD 18,600.

(6)Brian’s ultimate taxable amount that he has to pay can be arrived by deducting 5th step

value from the 1st step i.e. USD 46,500 - USD 18,600 = USD 27,900.

Conclusion

In case the interest is paid at the end of the loan period, the deemed time is estimated from the

time when the interest becomes payable. But if Brian’s loan interest is paid in monthly

installments, the particular period is assumed from the time when the interest payment starts.

Another consideration that needs to be made if Brian does not have to repay the loan interest

is that the same steps would be followed but the rate of interest would be taken at 0 percent.

3. Accounting of capital gain or capital loss

Issue:

The presented scenario involves a couple, Jack, and Jill, who are tied up in a written

agreement relating to the renting of property.

7 Møller, Niels Framroze. "Energy demand, substitution and environmental taxation: An econometric analysis of eight subsectors of the

Danish economy." Energy Economics 61 (2017): 97-109.

statutory interest rate7.

(1)Thus Interest value based on statutory interest rate of 5.65% = USD 10,00,000 * 5.65% =

USD 56,500 and interest value based on actual interest rate of 1.00%) = USD 10,00,000 *

1.00% = USD 10,000. So derived loan fringe benefits = USD 56,500- USD 10,000 = USD

46,500.

(2)The interest value based on the statutory interest rate is USD 56,500 (USD 10,00,000 *

5.65%). The particular assumption made at this stage is that this value is the real amount

payable.

(3)As per provided details, Brian has used 40% of the financial loan for income-producing

purposes and other financial obligations. So his tax-deductible interest expense is USD

56,500 * 40% = USD 22,600. This is a hypothetical figure.

(4)His real tax-deductible interest expense must be calculated, which is USD 10,000 * 40% =

USD 4,000.

(5)The real tax-deductible interest expense has to be deducted from the hypothetical value:

USD 22,600 - USD 4,000 = USD 18,600.

(6)Brian’s ultimate taxable amount that he has to pay can be arrived by deducting 5th step

value from the 1st step i.e. USD 46,500 - USD 18,600 = USD 27,900.

Conclusion

In case the interest is paid at the end of the loan period, the deemed time is estimated from the

time when the interest becomes payable. But if Brian’s loan interest is paid in monthly

installments, the particular period is assumed from the time when the interest payment starts.

Another consideration that needs to be made if Brian does not have to repay the loan interest

is that the same steps would be followed but the rate of interest would be taken at 0 percent.

3. Accounting of capital gain or capital loss

Issue:

The presented scenario involves a couple, Jack, and Jill, who are tied up in a written

agreement relating to the renting of property.

7 Møller, Niels Framroze. "Energy demand, substitution and environmental taxation: An econometric analysis of eight subsectors of the

Danish economy." Energy Economics 61 (2017): 97-109.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Rule:

According to the agreement, Jack is eligible to get only 10% of earned profits from the

property while Jill is supposed to receive 90% of its earned profits. In case of loss, Jack has to

suffer the total loss.

Application

Last year Jack and Jill have incurred a loss of USD 10,000. As per the agreement, dealing

with the loss from the property is the sole responsibility of Jack and Kill has no role to play in

this situation. As per set rules Jack must bear the entire loss that has been incurred o the

property.

Jack basically has two choices with him at the moment to deal with the loss that has arisen.

The first option is that he can offset this particular loss with his other source of income

earned during the financial year. The second option is that he could carry forward the loss to

subsequent year until the sale of the property8. When profits are generated from the property,

the same must be distributed between Jack and Jill on the basis of the agreed proportion i.e.

1:9. The interesting observation from the presented scenario is that Jack has the right to offset

the loss against the gains that could arise after the sale of the particular property.

Conclusion:

Thus in the presented plot, it can be stated that Jill will not be having any responsibility with

respect to the taxation implications relating to the rental property. Jack will have the financial

responsibility for the losses relating to the property and he will have to record it in his books

of accounts9.

4. Principle established in IRC v Duke of Westminster [1936] AC 1

Issue:

The case IRC v Duke of Westminster [1936] is a popular legal scenario that has gained

significant attention due to its relation to taxation rule. It basically highlights the fact that an

individual is righteously entitled to use the legal measures and methods to reduce his tax

figure by depreciating his net income. The key principles from the case have been

highlighted.

8 Le Bodo, Yann, Marie-Claude Paquette, and Philippe De Wals. "Feasibility of Sugar-Sweetened Beverage TaxationFeasibility, of SSB

Taxation in Canada in CanadaSSB Taxation in Canada Feasibility of." In Taxing Soda for Public Health, pp. 163-192. Springer

International Publishing, 2016

9 Mattauch, Linus, Jan Siegmeier, Ottmar Edenhofer, and Felix Creutzig. "Financing public capital through land rent taxation: A

macroeconomic henry george theorem." (2013)

According to the agreement, Jack is eligible to get only 10% of earned profits from the

property while Jill is supposed to receive 90% of its earned profits. In case of loss, Jack has to

suffer the total loss.

Application

Last year Jack and Jill have incurred a loss of USD 10,000. As per the agreement, dealing

with the loss from the property is the sole responsibility of Jack and Kill has no role to play in

this situation. As per set rules Jack must bear the entire loss that has been incurred o the

property.

Jack basically has two choices with him at the moment to deal with the loss that has arisen.

The first option is that he can offset this particular loss with his other source of income

earned during the financial year. The second option is that he could carry forward the loss to

subsequent year until the sale of the property8. When profits are generated from the property,

the same must be distributed between Jack and Jill on the basis of the agreed proportion i.e.

1:9. The interesting observation from the presented scenario is that Jack has the right to offset

the loss against the gains that could arise after the sale of the particular property.

Conclusion:

Thus in the presented plot, it can be stated that Jill will not be having any responsibility with

respect to the taxation implications relating to the rental property. Jack will have the financial

responsibility for the losses relating to the property and he will have to record it in his books

of accounts9.

4. Principle established in IRC v Duke of Westminster [1936] AC 1

Issue:

The case IRC v Duke of Westminster [1936] is a popular legal scenario that has gained

significant attention due to its relation to taxation rule. It basically highlights the fact that an

individual is righteously entitled to use the legal measures and methods to reduce his tax

figure by depreciating his net income. The key principles from the case have been

highlighted.

8 Le Bodo, Yann, Marie-Claude Paquette, and Philippe De Wals. "Feasibility of Sugar-Sweetened Beverage TaxationFeasibility, of SSB

Taxation in Canada in CanadaSSB Taxation in Canada Feasibility of." In Taxing Soda for Public Health, pp. 163-192. Springer

International Publishing, 2016

9 Mattauch, Linus, Jan Siegmeier, Ottmar Edenhofer, and Felix Creutzig. "Financing public capital through land rent taxation: A

macroeconomic henry george theorem." (2013)

Rule:

Every individual has the fundamental right to apply strategic change model to accounting

management in order to reduce his total income that he has earned during a period. The

crucial necessity is that ethical methods must have been used by him to exempt himself from

making the payment of excess tax amount. The ethical and fair application of legal tools and

strategies for the purpose of minimizing the total earnings on which tax is applicable puts the

individual in a safe position10. The authoritative figures like Commissioner of Inland Revenue

cannot compel him to pay additional tax if he is backed by law.

Application

In the current times, the application of this rule might be questioned based on the inferences

from latest case laws. As per the new case laws, a firm that incurs loss could alter the

financial details in its financial statements like balance sheet and income statement and it

could also write off its fixed assets at any value as per its desire.

But at the same time, it allows individuals to adopt fair means to reduce the tax amount that

has to be paid by them. Individuals and concerns need to adopt ethical practices and use the

tax law to minimize the payable tax value. Due to the increase in the use of unethical methods

by organizations and individuals, this rule is being questioned. But the fair implementation of

the rule is necessary so that tax burden can be fairly reduced.

Conclusion:

It is necessary for an organization to adopt fair and ethical means while performing its

financial transactions so that in future it will not have to face any kind of penalty. This case

that has been presented empowers individuals to reduce their tax burden by applying fair and

legal means. Thus individuals and firm must use ethical practices and not try to betray the

law11.

5. Logging firm case

Issue:

Bill owns a large parcel of land with many tall pine trees. He wishes to use it for grazing

sheep and thus wants to clear the trees. A logging firm seems interested to pay him USD

10 Hansen, Benjamin, Keaton Miller, and Caroline Weber. The taxation of recreational marijuana: Evidence from Washington state. No.

w23632. National Bureau of Economic Research, 2017.

11 Juranek, Steffen, Dirk Schindler, and Guttorm Schjelderup. "Transfer pricing regulation and taxation of royalty payments." Journal of

Public Economic Theory (2017)

Every individual has the fundamental right to apply strategic change model to accounting

management in order to reduce his total income that he has earned during a period. The

crucial necessity is that ethical methods must have been used by him to exempt himself from

making the payment of excess tax amount. The ethical and fair application of legal tools and

strategies for the purpose of minimizing the total earnings on which tax is applicable puts the

individual in a safe position10. The authoritative figures like Commissioner of Inland Revenue

cannot compel him to pay additional tax if he is backed by law.

Application

In the current times, the application of this rule might be questioned based on the inferences

from latest case laws. As per the new case laws, a firm that incurs loss could alter the

financial details in its financial statements like balance sheet and income statement and it

could also write off its fixed assets at any value as per its desire.

But at the same time, it allows individuals to adopt fair means to reduce the tax amount that

has to be paid by them. Individuals and concerns need to adopt ethical practices and use the

tax law to minimize the payable tax value. Due to the increase in the use of unethical methods

by organizations and individuals, this rule is being questioned. But the fair implementation of

the rule is necessary so that tax burden can be fairly reduced.

Conclusion:

It is necessary for an organization to adopt fair and ethical means while performing its

financial transactions so that in future it will not have to face any kind of penalty. This case

that has been presented empowers individuals to reduce their tax burden by applying fair and

legal means. Thus individuals and firm must use ethical practices and not try to betray the

law11.

5. Logging firm case

Issue:

Bill owns a large parcel of land with many tall pine trees. He wishes to use it for grazing

sheep and thus wants to clear the trees. A logging firm seems interested to pay him USD

10 Hansen, Benjamin, Keaton Miller, and Caroline Weber. The taxation of recreational marijuana: Evidence from Washington state. No.

w23632. National Bureau of Economic Research, 2017.

11 Juranek, Steffen, Dirk Schindler, and Guttorm Schjelderup. "Transfer pricing regulation and taxation of royalty payments." Journal of

Public Economic Theory (2017)

1,000 for every 100 meters of timber that they take from the land. The presented case needs

to be reviewed to understand the taxation aspects.

Rule:

The receipt of Bill from the logging concern reveals two different scenarios. The first

scenario states that Bill would be receiving a lump sum amount of USD 50,000 from the

company for clearing the trees from his yard12. The other scenario states that Bill would be

receiving recurring amounts from the concern of USD 1,000 for every 100 meters of timber

that they would clear from his land. Both the scenarios are different in nature since the first

one is a onetime transaction while the latter one is a repeated transaction.

Application

If Bill would be receiving USD 50,000 from the logging company for granting them the right

to remove as much timber as required from the land, it would be assumed to be his capital

receipt. It would also imply that the firm would have entire right to cut off the trees in the

pineyard. A vital aspect that needs to be taken into consideration in this scenario relates to the

tax relating to such capital gains. Taxes would be charged on Billy for the bulk receipt for the

simple reason that the receipt is of a large value and it is not recurring in nature.

Conclusion:

The nature of the financial transaction between the two parties i.e. Bill and the logging

company is crucial since it has a vital impact on the applicability of the taxation rules. As per

the prevailing tax laws, the receipt of a bulk value is considered to be a capital receipt and

relevant tax rates are applicable in the situation.

If Bill would be receiving recurring amounts of small amount, the rules relating to capital

gains would not apply in the situation13. The income earned by him would be recurring in

nature and thus the tax that would be charged on such income would be as per the normal

interest rates. So the nature of receipts has a strong correlation with the tax rule that is applied

in any given circumstances.

12 Foucault, Martial, Katsunori Seki, and Guy D. Whitten. "Good times, bad times: Taxation and electoral accountability." Electoral

Studies 45 (2017): 191-200

13 Andrikopoulos, Andreas, and Konstantinos Kostaris. "Journal of International Accounting, Auditing and Taxation." Journal of

International Accounting, Auditing and Taxation 28 (2017): 1-9.

to be reviewed to understand the taxation aspects.

Rule:

The receipt of Bill from the logging concern reveals two different scenarios. The first

scenario states that Bill would be receiving a lump sum amount of USD 50,000 from the

company for clearing the trees from his yard12. The other scenario states that Bill would be

receiving recurring amounts from the concern of USD 1,000 for every 100 meters of timber

that they would clear from his land. Both the scenarios are different in nature since the first

one is a onetime transaction while the latter one is a repeated transaction.

Application

If Bill would be receiving USD 50,000 from the logging company for granting them the right

to remove as much timber as required from the land, it would be assumed to be his capital

receipt. It would also imply that the firm would have entire right to cut off the trees in the

pineyard. A vital aspect that needs to be taken into consideration in this scenario relates to the

tax relating to such capital gains. Taxes would be charged on Billy for the bulk receipt for the

simple reason that the receipt is of a large value and it is not recurring in nature.

Conclusion:

The nature of the financial transaction between the two parties i.e. Bill and the logging

company is crucial since it has a vital impact on the applicability of the taxation rules. As per

the prevailing tax laws, the receipt of a bulk value is considered to be a capital receipt and

relevant tax rates are applicable in the situation.

If Bill would be receiving recurring amounts of small amount, the rules relating to capital

gains would not apply in the situation13. The income earned by him would be recurring in

nature and thus the tax that would be charged on such income would be as per the normal

interest rates. So the nature of receipts has a strong correlation with the tax rule that is applied

in any given circumstances.

12 Foucault, Martial, Katsunori Seki, and Guy D. Whitten. "Good times, bad times: Taxation and electoral accountability." Electoral

Studies 45 (2017): 191-200

13 Andrikopoulos, Andreas, and Konstantinos Kostaris. "Journal of International Accounting, Auditing and Taxation." Journal of

International Accounting, Auditing and Taxation 28 (2017): 1-9.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.