Holmes Institute Taxation Law Assignment: CGT, Depreciation, and Tax

VerifiedAdded on 2022/11/18

|13

|2848

|237

Homework Assignment

AI Summary

This taxation law assignment analyzes two key scenarios. The first scenario examines Jasmine's tax liabilities, including capital gains tax (CGT) implications on her family home (pre-CGT asset), a car (private use asset), the sale of her cleaning business (small business concessions), furniture, and paintings (collectibles). The assignment applies relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997), such as those related to CGT exemptions, private use asset rules, and small business concessions like the 15-year exemption and 50% reduction. The second scenario focuses on John and his claim for tax deductions related to the depreciation of a CNC machine, imported from Germany. It considers the cost base of the asset and the timing of depreciation, referencing the relevant provisions of the ITAA 1997, including those related to depreciating assets and the start time for depreciation calculation. The assignment addresses the application of the law, including the Broken Hill Pty Co Ltd v. FCT case, to determine the allowable deductions.

Running Head: TAXATION LAW

TAXATION LAW

Name of the Student

Name of the University

Author Note

TAXATION LAW

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Issues:.....................................................................................................................................7

Law:........................................................................................................................................7

Application:............................................................................................................................8

Conclusion:............................................................................................................................9

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

A: The capital gain on family home:

The tax paid on the assets which are purchased or deemed to purchase on or following

20/9/1985 is commonly referred as capital gains tax (Smith 2014). As a consequence, Pre-

CGT and Post-CGT are the expressions usually applied on those assets which are purchased

or events taking place prior to or following the particular date.

A taxpayer is allowed a basic exemption for capital gain or for capital loss, provided

the CGT originates from such an event where the asset of CGT is a house. In “sec-118-110

(1), ITAA 1997” the house of the taxpayer must be treated as the basic dwelling place

throughout the ownership period (Freebairn 2016).

As apparent the circumstance of Jasmine demonstrates that she paid for a house for

$40,000 in the year 1981 and sold it off eventually for $650,000. The home of Jasmine falls

under the class of Pre-CGT asset as it was procured before CGT regime was applied.

Moreover, “sec-118-110 (1)” can be applied in Jasmine’s case as she was living in the house

ever since it was purchased (Jones 2018). Thus, the capital gains will be omitted from CGT

which was made afterwards the sale of house.

B: Capital gain or loss made from the car:

An event of CGT A1 takes place when the taxpayer is selling off the CGT asset under

“section 104-10 (1)”. As per the “section 108-20 (2)” an asset can be referred to as private

use asset which are generally used by the tax payer for personal use and enjoyment purposes

other than the collectables except for land and building (Pinto and Evans 2018). The

examples of private use assets normally includes,

TV at home

Answer to question 1:

A: The capital gain on family home:

The tax paid on the assets which are purchased or deemed to purchase on or following

20/9/1985 is commonly referred as capital gains tax (Smith 2014). As a consequence, Pre-

CGT and Post-CGT are the expressions usually applied on those assets which are purchased

or events taking place prior to or following the particular date.

A taxpayer is allowed a basic exemption for capital gain or for capital loss, provided

the CGT originates from such an event where the asset of CGT is a house. In “sec-118-110

(1), ITAA 1997” the house of the taxpayer must be treated as the basic dwelling place

throughout the ownership period (Freebairn 2016).

As apparent the circumstance of Jasmine demonstrates that she paid for a house for

$40,000 in the year 1981 and sold it off eventually for $650,000. The home of Jasmine falls

under the class of Pre-CGT asset as it was procured before CGT regime was applied.

Moreover, “sec-118-110 (1)” can be applied in Jasmine’s case as she was living in the house

ever since it was purchased (Jones 2018). Thus, the capital gains will be omitted from CGT

which was made afterwards the sale of house.

B: Capital gain or loss made from the car:

An event of CGT A1 takes place when the taxpayer is selling off the CGT asset under

“section 104-10 (1)”. As per the “section 108-20 (2)” an asset can be referred to as private

use asset which are generally used by the tax payer for personal use and enjoyment purposes

other than the collectables except for land and building (Pinto and Evans 2018). The

examples of private use assets normally includes,

TV at home

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

A car or bicycle

A yacht for personal usage

Mobile phone for private usage

Few firm special rules which are applicable on private use assets. The capital gains from

personal use assets are to be omitted by the taxpayer if it was procured for $10,000 or less

under “sec 118-10 (3)” (Nassios et al. 2019). At the same time the capital loss occurred after

selling a private use asset is usually omitted as per “section 108-20 (1)”.

The instance reading of Jasmine shows that she has paid for a car for $31,000 in the year

2011 and was sold ultimately for $10k. A capital loss was suffered after disposing the car. On

the other hand, the car has been treated as a private use asset, therefore under “section 108-

20 (1)” the capital loss is supposed to be disregarded by Jasmine as it has been incurred from

trading a private usage asset (Chow 2018).

C: The capital gain on sale of business:

There are concessions available for helping the small businesses under “division

152”. The primary conditions include-

a) The entity is supposed to be a small business entity with a total of yearly turnover of

less than $2 million for the current year or the previous year or the assets having a net

worth of $6 million or less (Ross, Walker and Walker 2017).

b) CGT asset is necessarily be an active asset.

Four types of concessions are mainly found for small business. These include the following-

1) 15-year exemption- The taxpayer can hold a CGT asset for a minimum period of 15

years.

A car or bicycle

A yacht for personal usage

Mobile phone for private usage

Few firm special rules which are applicable on private use assets. The capital gains from

personal use assets are to be omitted by the taxpayer if it was procured for $10,000 or less

under “sec 118-10 (3)” (Nassios et al. 2019). At the same time the capital loss occurred after

selling a private use asset is usually omitted as per “section 108-20 (1)”.

The instance reading of Jasmine shows that she has paid for a car for $31,000 in the year

2011 and was sold ultimately for $10k. A capital loss was suffered after disposing the car. On

the other hand, the car has been treated as a private use asset, therefore under “section 108-

20 (1)” the capital loss is supposed to be disregarded by Jasmine as it has been incurred from

trading a private usage asset (Chow 2018).

C: The capital gain on sale of business:

There are concessions available for helping the small businesses under “division

152”. The primary conditions include-

a) The entity is supposed to be a small business entity with a total of yearly turnover of

less than $2 million for the current year or the previous year or the assets having a net

worth of $6 million or less (Ross, Walker and Walker 2017).

b) CGT asset is necessarily be an active asset.

Four types of concessions are mainly found for small business. These include the following-

1) 15-year exemption- The taxpayer can hold a CGT asset for a minimum period of 15

years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

2) 50% reduction- The capital gain can be reduced by 50% by the qualifying tax payer

under this scheme.

3) Retirement concession- The capital gain is ignored on selling of a CGT asset of

small business provided the revenue of sales is used for retirement purpose (Toth and

Burns 2016).

4) Roll-over relief- When a replacement asset is purchased by a taxpayer its capital

gains are to be deferred.

As shown by the circumstances of Jasmine it is obvious that she is coming back to US

after retiring from her cleaning business. She is selling off her business to a buyer who is

willing to take over a cleaning business. The sales value of the cleaning business is $125,000,

where the business has been sold for $65,000 and the goodwill for $60,000. Jasmine is

eligible to avail the concessions for small business under “division 152” as the net worth of

her business assets is not exceeding $6 million. Moreover, the sold assets have been used by

Jasmine throughout during the business (Campbell 2018). The business equipment are held

by Jasmine for a minimum of 15 years therefore she can acquire a 15-year exemption.

In consideration of her goodwill, an event of CGT C1 has been occurred as her

business is getting ceased permanently. According to “TR 1999/16”, when the processes of a

business gets ceased either voluntarily or involuntarily, the business goodwill is lost or

destroyed (Edmonds, Holle and Hartanti 2015). Correspondingly, in terms of Jasmine’s Case

the operations of the business is to be ceased permanently with the selling of her business

goodwill. Therefore, a 50% reduction under the “subdivision 152-C” can be obtained by

Jasmine.

D: The capital gain from selling the furniture:

2) 50% reduction- The capital gain can be reduced by 50% by the qualifying tax payer

under this scheme.

3) Retirement concession- The capital gain is ignored on selling of a CGT asset of

small business provided the revenue of sales is used for retirement purpose (Toth and

Burns 2016).

4) Roll-over relief- When a replacement asset is purchased by a taxpayer its capital

gains are to be deferred.

As shown by the circumstances of Jasmine it is obvious that she is coming back to US

after retiring from her cleaning business. She is selling off her business to a buyer who is

willing to take over a cleaning business. The sales value of the cleaning business is $125,000,

where the business has been sold for $65,000 and the goodwill for $60,000. Jasmine is

eligible to avail the concessions for small business under “division 152” as the net worth of

her business assets is not exceeding $6 million. Moreover, the sold assets have been used by

Jasmine throughout during the business (Campbell 2018). The business equipment are held

by Jasmine for a minimum of 15 years therefore she can acquire a 15-year exemption.

In consideration of her goodwill, an event of CGT C1 has been occurred as her

business is getting ceased permanently. According to “TR 1999/16”, when the processes of a

business gets ceased either voluntarily or involuntarily, the business goodwill is lost or

destroyed (Edmonds, Holle and Hartanti 2015). Correspondingly, in terms of Jasmine’s Case

the operations of the business is to be ceased permanently with the selling of her business

goodwill. Therefore, a 50% reduction under the “subdivision 152-C” can be obtained by

Jasmine.

D: The capital gain from selling the furniture:

5TAXATION LAW

Other instances found in the case shows that the furniture was also sold by Jasmine.

They were sold for $5,000 whereas the furniture has a purchase price of $2,000. The capital

gains here is overlooked according to the “section 118-10 (3)” since the purchase price of the

private use asset was less than $10,000 (McGillivray 2018). Similarly, Jasmine bought the

furniture with an amount less than $2,000 and therefore under “section 118-10 (3)” the

capital gain will be disregarded that took place after the selling of the furniture by Jasmine.

E: The capital gain from selling the paintings:

The characterisation of collectibles implies as an asset which is used for personal

pleasure purpose of the taxpayer as per the “sec 108-10, ITAA 1997” (Mangioni 2015).

According to the “Section 108-10 (2)”, a list of collectibles includes the following-

Art works such as (paintings and sculptures)

Antiques and jewelry

Rare stamps, coins

There are certain exceptional rules applicable in terms of collectibles. According to

the “sec108-10 (1), ITAA 1997” the capital loss incurred from the selling of collectibles is

kept aside and is allowed only for outweighing the capital gains of some other collectibles

(Landsberg and Young 2018). The capital gain is subject to disregard if the purchase price of

the collectible is less than $500 as per “section 118-10 (1)”.

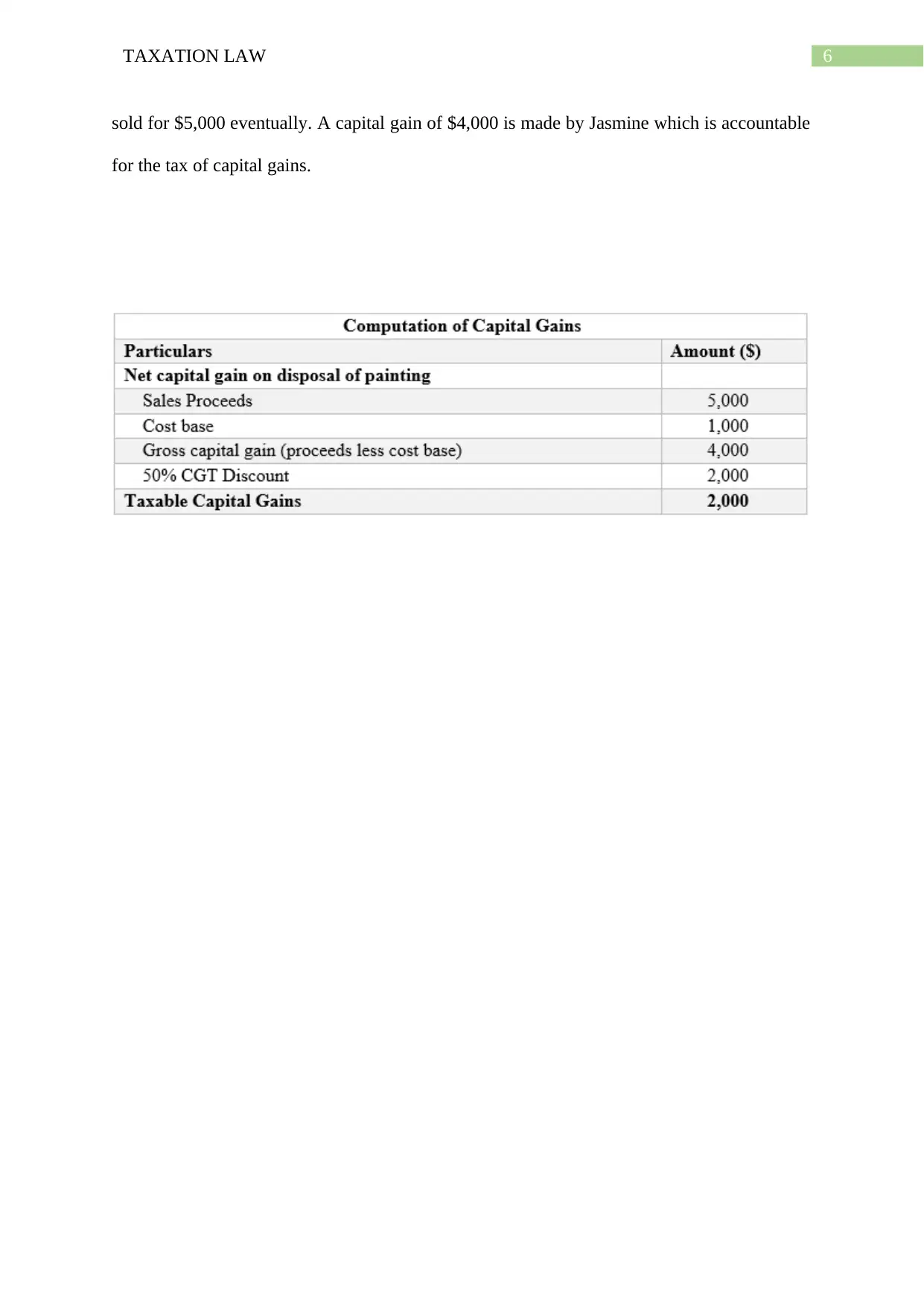

In Jasmine’s case, several paintings were bought by Jasmine with a cost not more than

$500 for each. Jasmine sold off all the paintings for $35,000. Referring the special rules

coming under “section 108-10 (1)”, the capital gains will be disregarded as it has derived

from the disposal of the paintings and the cost of each painting is $500 and not more than that

(Ferraro 2016). Nevertheless, the cost of one of her purchased painting was $1,000 and it was

Other instances found in the case shows that the furniture was also sold by Jasmine.

They were sold for $5,000 whereas the furniture has a purchase price of $2,000. The capital

gains here is overlooked according to the “section 118-10 (3)” since the purchase price of the

private use asset was less than $10,000 (McGillivray 2018). Similarly, Jasmine bought the

furniture with an amount less than $2,000 and therefore under “section 118-10 (3)” the

capital gain will be disregarded that took place after the selling of the furniture by Jasmine.

E: The capital gain from selling the paintings:

The characterisation of collectibles implies as an asset which is used for personal

pleasure purpose of the taxpayer as per the “sec 108-10, ITAA 1997” (Mangioni 2015).

According to the “Section 108-10 (2)”, a list of collectibles includes the following-

Art works such as (paintings and sculptures)

Antiques and jewelry

Rare stamps, coins

There are certain exceptional rules applicable in terms of collectibles. According to

the “sec108-10 (1), ITAA 1997” the capital loss incurred from the selling of collectibles is

kept aside and is allowed only for outweighing the capital gains of some other collectibles

(Landsberg and Young 2018). The capital gain is subject to disregard if the purchase price of

the collectible is less than $500 as per “section 118-10 (1)”.

In Jasmine’s case, several paintings were bought by Jasmine with a cost not more than

$500 for each. Jasmine sold off all the paintings for $35,000. Referring the special rules

coming under “section 108-10 (1)”, the capital gains will be disregarded as it has derived

from the disposal of the paintings and the cost of each painting is $500 and not more than that

(Ferraro 2016). Nevertheless, the cost of one of her purchased painting was $1,000 and it was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

sold for $5,000 eventually. A capital gain of $4,000 is made by Jasmine which is accountable

for the tax of capital gains.

sold for $5,000 eventually. A capital gain of $4,000 is made by Jasmine which is accountable

for the tax of capital gains.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

Is it permissible to claim tax deduction by the taxpayer under the operative provision

of “section 40-25 (1), ITAA 1997” which is equivalent to the declining value of the asset

depreciation which readily installed for taxable reason by the taxpayer?

Law:

Conferring to the “div 40, ITAA 1997”, it is permissible for a taxpayer to avail

deduction whose amount is equivalent to the “decline in value” of the asset held by a

taxpayer which is depreciated on the basis of its affectivity. According to “sec 40-25 (1)”, a

principal operative operation, taxpayers are allowed deductions which is equivalent to the

depreciating assets’ decline in value held by taxpayers during an entire year and is used for

making earnings which are chargeable or installed for instant use (Williams 2018).

An asset starts to depreciate or starts losing its worth held by taxpayers when the start

time takes place as per “sect 40-60 (1)”. When a taxpayer uses an asset for the first time or is

installed for instant use represents the start time of a depreciating asset. Thus, it can be

implied that an asset’s decline in value starts when the asset is used for the first time by a

taxpayer even if it is used for personal purpose. It must be donated by the taxpayer that there

is no deduction allowed to the taxpayers under “sec 40-25 (2), ITAA 1997” until when the

asset has been used for taxable purpose (Chow 2018). There will be 100% reduction in

deduction in the asset when it is only used for private consumption by the taxpayer for that

time but no deduction will be considered for such private purpose. An asset having a limited

actual life is termed as depreciating asset according to “sect 40-30 (1)” and the fall in value is

anticipated rationally till

the time it is used.

Answer to question 2:

Issues:

Is it permissible to claim tax deduction by the taxpayer under the operative provision

of “section 40-25 (1), ITAA 1997” which is equivalent to the declining value of the asset

depreciation which readily installed for taxable reason by the taxpayer?

Law:

Conferring to the “div 40, ITAA 1997”, it is permissible for a taxpayer to avail

deduction whose amount is equivalent to the “decline in value” of the asset held by a

taxpayer which is depreciated on the basis of its affectivity. According to “sec 40-25 (1)”, a

principal operative operation, taxpayers are allowed deductions which is equivalent to the

depreciating assets’ decline in value held by taxpayers during an entire year and is used for

making earnings which are chargeable or installed for instant use (Williams 2018).

An asset starts to depreciate or starts losing its worth held by taxpayers when the start

time takes place as per “sect 40-60 (1)”. When a taxpayer uses an asset for the first time or is

installed for instant use represents the start time of a depreciating asset. Thus, it can be

implied that an asset’s decline in value starts when the asset is used for the first time by a

taxpayer even if it is used for personal purpose. It must be donated by the taxpayer that there

is no deduction allowed to the taxpayers under “sec 40-25 (2), ITAA 1997” until when the

asset has been used for taxable purpose (Chow 2018). There will be 100% reduction in

deduction in the asset when it is only used for private consumption by the taxpayer for that

time but no deduction will be considered for such private purpose. An asset having a limited

actual life is termed as depreciating asset according to “sect 40-30 (1)” and the fall in value is

anticipated rationally till

the time it is used.

8TAXATION LAW

Depreciation is calculated based on the price of the asset under the “sub-division 40-

C”. The court of law in “Broken Hill Pty Co Ltd v. FCT” (1969-70) has a general rule which

states that the purchase price will not be included in the cost but other costs like cost of

installation and delivery will be included (Landsberg and Young 2018). Furthermore, petty

expenses like expenses incurred for removing or rearranging a plant for the accommodation

of a new plant gets included in the cost.

There are five elements which comprises the cost base of assets according to “section

110-25, ITAA 1997” (Ferraro 2016). The first element includes the money which is paid for

purchasing the asset and the market value of the asset. The following are the cost base

elements-

1) For assets purchased following 20 August 1991, the cost of title is to be included

2) Amount paid or necessarily needed to be paid in relation to the purchase of asset

3) Related charges occurred in buying or selling the asset

4) Capital expenses occurred for preserving the title rights of assets.

5) Capital expenses incurred to increase asset’s value or associated to installing or

moving asset

The second element is associated with the sale or acquisition comprising costs as per

“section 110-35”. The costs include transfer cost, professional fees like stamp duty, surveyor

cost, cost of advertisement and valuation cost or cost of borrowing.

Application:

The circumstances of John evidently shows that a CNC machine is imported by him

on 1st November 2014 from Germany. Referencing “section 40-30 (1)”, the CNC machine

falls under the category of depreciating assets and has a limited functional lifespan. It has

Depreciation is calculated based on the price of the asset under the “sub-division 40-

C”. The court of law in “Broken Hill Pty Co Ltd v. FCT” (1969-70) has a general rule which

states that the purchase price will not be included in the cost but other costs like cost of

installation and delivery will be included (Landsberg and Young 2018). Furthermore, petty

expenses like expenses incurred for removing or rearranging a plant for the accommodation

of a new plant gets included in the cost.

There are five elements which comprises the cost base of assets according to “section

110-25, ITAA 1997” (Ferraro 2016). The first element includes the money which is paid for

purchasing the asset and the market value of the asset. The following are the cost base

elements-

1) For assets purchased following 20 August 1991, the cost of title is to be included

2) Amount paid or necessarily needed to be paid in relation to the purchase of asset

3) Related charges occurred in buying or selling the asset

4) Capital expenses occurred for preserving the title rights of assets.

5) Capital expenses incurred to increase asset’s value or associated to installing or

moving asset

The second element is associated with the sale or acquisition comprising costs as per

“section 110-35”. The costs include transfer cost, professional fees like stamp duty, surveyor

cost, cost of advertisement and valuation cost or cost of borrowing.

Application:

The circumstances of John evidently shows that a CNC machine is imported by him

on 1st November 2014 from Germany. Referencing “section 40-30 (1)”, the CNC machine

falls under the category of depreciating assets and has a limited functional lifespan. It has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

been anticipated reasonably that decline in value is calculated from the time it is being used

for taxable purpose by John.

According to “section 40-60 (1)”, the start time of CNC machine is calculated from

15th January, as this time is represented as the time of the completion of installation and the

asset was first used by John. Besides, there are other expenses which is incurred by John after

the machine was installed. This cost includes the cost of a guiding rod costing $5,000 which

was installed on 1st February. As the guiding rod was added to the CNC machine later, the

cost base will be containing second element of expenses as referred to “Broken Hill Pty Co

Ltd v. FCT” (1969-70).

As per the primary operative provision of “section 40-25 (1)”, it is permissible for

John to access deduction of income tax, the value of which is equivalent to the CNC

machine’s decline value. The cost base of the asset which falls in the first element of the

“section 110-25, ITAA 1997” which includes the payment related to the CNC machine

(Landsberg and Young 2018). The cost made by John for the inspection of the CNC machine

falls under the second element related to acquisition which is incurred as related costs as it

took place during the purchase of the asset.

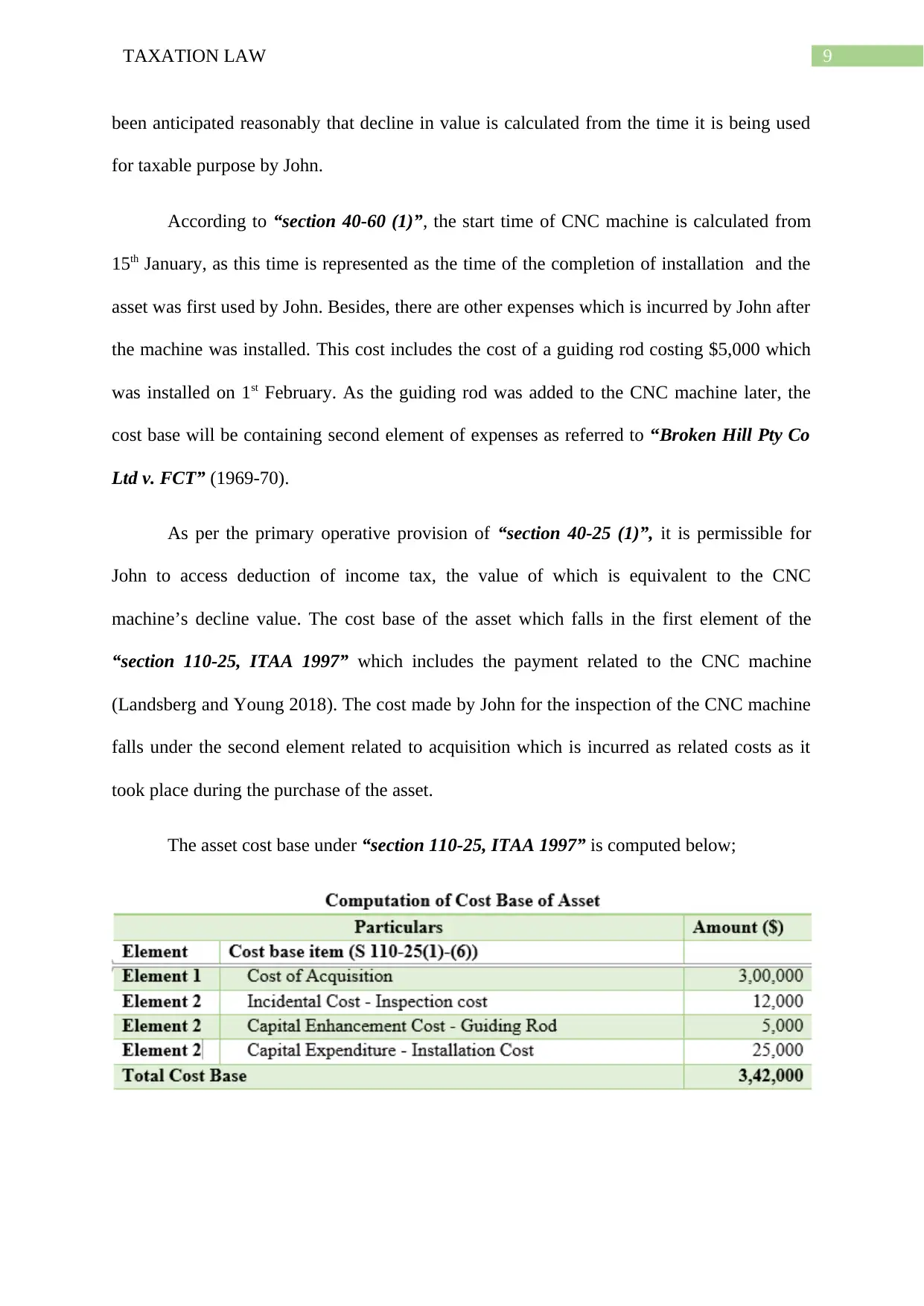

The asset cost base under “section 110-25, ITAA 1997” is computed below;

been anticipated reasonably that decline in value is calculated from the time it is being used

for taxable purpose by John.

According to “section 40-60 (1)”, the start time of CNC machine is calculated from

15th January, as this time is represented as the time of the completion of installation and the

asset was first used by John. Besides, there are other expenses which is incurred by John after

the machine was installed. This cost includes the cost of a guiding rod costing $5,000 which

was installed on 1st February. As the guiding rod was added to the CNC machine later, the

cost base will be containing second element of expenses as referred to “Broken Hill Pty Co

Ltd v. FCT” (1969-70).

As per the primary operative provision of “section 40-25 (1)”, it is permissible for

John to access deduction of income tax, the value of which is equivalent to the CNC

machine’s decline value. The cost base of the asset which falls in the first element of the

“section 110-25, ITAA 1997” which includes the payment related to the CNC machine

(Landsberg and Young 2018). The cost made by John for the inspection of the CNC machine

falls under the second element related to acquisition which is incurred as related costs as it

took place during the purchase of the asset.

The asset cost base under “section 110-25, ITAA 1997” is computed below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Conclusion:

The conclusion can be made that under the “section 40-25 (1), ITAA 1997” deduction

can be claimed by John which is equivalent to the CNC machine’s decline in value from the

date 15th January as it was used then for taxable purpose for the first time. It is allowable for

John for claiming depreciation based on total cost base of the assets under sub-division 40-C.

Conclusion:

The conclusion can be made that under the “section 40-25 (1), ITAA 1997” deduction

can be claimed by John which is equivalent to the CNC machine’s decline in value from the

date 15th January as it was used then for taxable purpose for the first time. It is allowable for

John for claiming depreciation based on total cost base of the assets under sub-division 40-C.

11TAXATION LAW

References:

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), p.263.

Chow, S., 2018. The wait is over. A new investment vehicle is coming!. Taxation in

Australia, 52(10), p.560.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super funds-tax

impediments to going global. Taxation in Australia, 49(7), p.413.

Ferraro, R., 2016. Tax education: First graduands to receive GDATL. Taxation in

Australia, 50(10), p.594.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in Australia, 53(6),

p.296.

Landsberg, S. and Young, A., 2018. Stapled structures and foreign investor

measures. Taxation in Australia, 53(6), p.329.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McGillivray, A., 2018. VAT: The perfect solution to the taxation of consumption?. Taxation

in Australia, 52(10), p.555.

Nassios, J., Giesecke, J.A., Dixon, P.B. and Rimmer, M.T., 2019. Modelling the allocative

efficiency of landowner taxation. Economic Modelling.

Pinto, D. and Evans, M., 2018. Returning income taxation revenue to the states: back to the

future.

References:

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 1. Taxation in

Australia, 53(5), p.263.

Chow, S., 2018. The wait is over. A new investment vehicle is coming!. Taxation in

Australia, 52(10), p.560.

Edmonds, M., Holle, C. and Hartanti, W., 2015. Alternative assets insights: Super funds-tax

impediments to going global. Taxation in Australia, 49(7), p.413.

Ferraro, R., 2016. Tax education: First graduands to receive GDATL. Taxation in

Australia, 50(10), p.594.

Freebairn, J., 2016. Taxation of housing. Australian Economic Review, 49(3), pp.307-316.

Jones, D., 2018. Complexity of tax residency attracts review. Taxation in Australia, 53(6),

p.296.

Landsberg, S. and Young, A., 2018. Stapled structures and foreign investor

measures. Taxation in Australia, 53(6), p.329.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

McGillivray, A., 2018. VAT: The perfect solution to the taxation of consumption?. Taxation

in Australia, 52(10), p.555.

Nassios, J., Giesecke, J.A., Dixon, P.B. and Rimmer, M.T., 2019. Modelling the allocative

efficiency of landowner taxation. Economic Modelling.

Pinto, D. and Evans, M., 2018. Returning income taxation revenue to the states: back to the

future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.