Taxation Assignment: Calculation of Net Capital Gain or Loss and FBT Consequences

VerifiedAdded on 2023/06/04

|14

|3244

|411

AI Summary

This report aims at calculation of net capital gain or loss for a client that is given in the assignment scenario. It includes different transactions given in the scenario, which will be considered while determining the value of net capital gain or loss for the client. The report also includes the critical analysis of FBT or fringe benefits taxation laws of Australia. This analysis will be done in context of the scenario that is given in section of assignment file. It will also focus on analysing that how a particular transaction can affect the FBT consequences for a company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Assignment 1

Taxation Theory Assignment

Taxation Theory Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Assignment 2

Table of Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................4

Question 2..................................................................................................................................9

(a) FBT Consequences for Rapid Heat Company................................................................10

(b) FBT Consequences if Remaining $50,000 is also used by Jasmine...............................11

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Question 1..................................................................................................................................4

Question 2..................................................................................................................................9

(a) FBT Consequences for Rapid Heat Company................................................................10

(b) FBT Consequences if Remaining $50,000 is also used by Jasmine...............................11

Conclusion................................................................................................................................12

References................................................................................................................................13

Taxation Assignment 3

Introduction

This report is quite helpful in developing practical knowledge about different concepts related

to financial accounting. The report aims at calculation of net capital gain or loss for a client

that is given in the assignment scenario. There are different transactions given in the scenario,

which will be considered while determining the value of net capital gain or loss for the client.

Example of these transactions includes sale of a vacant land, antique bed, sale of painting, the

investment in shares of different companies and the sale of violin. This way, the report is

helpful in understanding treatment of different types of transactions in business for the

valuation of net capital gain or loss. Apart from this, the report will also include the critical

analysis of FBT or fringe benefits taxation laws of Australia. This analysis will be done in

context of the scenario that is given in section of assignment file. It will also focus on

analysing that how a particular transaction can affect the FBT consequences for a company.

Introduction

This report is quite helpful in developing practical knowledge about different concepts related

to financial accounting. The report aims at calculation of net capital gain or loss for a client

that is given in the assignment scenario. There are different transactions given in the scenario,

which will be considered while determining the value of net capital gain or loss for the client.

Example of these transactions includes sale of a vacant land, antique bed, sale of painting, the

investment in shares of different companies and the sale of violin. This way, the report is

helpful in understanding treatment of different types of transactions in business for the

valuation of net capital gain or loss. Apart from this, the report will also include the critical

analysis of FBT or fringe benefits taxation laws of Australia. This analysis will be done in

context of the scenario that is given in section of assignment file. It will also focus on

analysing that how a particular transaction can affect the FBT consequences for a company.

Taxation Assignment 4

Question 1

In general, the net capital gain refers to total contribution that is made by a transaction of

organization towards the capital position of company. The contribution from a business

transaction or capital transaction towards net capital of the company is calculated by finding

out difference of selling price from the different expenses and purchase cost incurred with

that asset or equipment.The value of capital gain can be obtained either positive or negative.

If it is negative, then it is often called as the capital loss (Becker et al., 2015). If there are two

or more than two transactions given, then capital gain contribution from each transaction is

determined and finally the gains from all transactions are added to obtain value of net capital

gain. Following formula is used for the valuation of capital gain for different transactions:

Capital Gain/ Loss = Selling Price of the Product – Purchase Price – Other Expenditures

Incurred

The valuation of capital gain or loss from different transactions given in the scenario is as

below:

(i) Selling of the Vacant Land

Following are the details related to purchasing price, selling price and the cost associated

with sewerage rates, land taxes, water and the fee of local council that have been faced by the

client:

Selling Price = $320,000

Purchasing Price = $100,000

Cost of Local Council, Water and sewerage = $20,000

So, by applying the formula of capital gain or loss:

Capital Gain/ Loss = $320,000 - $100,000 - $20,000

= $200,000

Question 1

In general, the net capital gain refers to total contribution that is made by a transaction of

organization towards the capital position of company. The contribution from a business

transaction or capital transaction towards net capital of the company is calculated by finding

out difference of selling price from the different expenses and purchase cost incurred with

that asset or equipment.The value of capital gain can be obtained either positive or negative.

If it is negative, then it is often called as the capital loss (Becker et al., 2015). If there are two

or more than two transactions given, then capital gain contribution from each transaction is

determined and finally the gains from all transactions are added to obtain value of net capital

gain. Following formula is used for the valuation of capital gain for different transactions:

Capital Gain/ Loss = Selling Price of the Product – Purchase Price – Other Expenditures

Incurred

The valuation of capital gain or loss from different transactions given in the scenario is as

below:

(i) Selling of the Vacant Land

Following are the details related to purchasing price, selling price and the cost associated

with sewerage rates, land taxes, water and the fee of local council that have been faced by the

client:

Selling Price = $320,000

Purchasing Price = $100,000

Cost of Local Council, Water and sewerage = $20,000

So, by applying the formula of capital gain or loss:

Capital Gain/ Loss = $320,000 - $100,000 - $20,000

= $200,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Assignment 5

Note: There is a situation that is given in this transaction. According to this situation, the

client has received the amount of $20,000, when she signs the sales contract. The rest of

transaction amount will be given by purchaser in upcoming year. In this context, the

contribution of this transaction towards net capital gain for this year will be only

$20,000(Stiglitz and Rosengard, 2015). The rest of transaction amount will be considered as

capital gain in next year, when it will be received from purchaser.

(ii) Sale of Antique Bed

In this transaction, there is no specific amount of selling price given in context of Antique

Bes. In this transaction, the client has faced theft of antique four-poster Louis XIV bed from

the house. The amount shown as selling price is the price that will be received by her from

the insurance company. So, different data in context of Antique Bes are as below:

Selling Price (amount received by client from insurance company) = $11,000

Purchase Price = $3,500

Cost of Alterations = $1,500

So, by applying the formula of capital gain or loss on this transaction:

Capital gain/ loss = $11,000 - $3,500 - $1,500

= $6,000

(iii) The Sale of Painting

Following are the data related to purchasing and selling price of painting made by a well

known Australian artist:

Selling Price = $125,000

Purchase Price = $2,000

Application of formula of capital gain/ loss on the transaction of selling painting:

Capital Gain/ Loss = $125,000 - $2,000

= $123,000

Note: There is a situation that is given in this transaction. According to this situation, the

client has received the amount of $20,000, when she signs the sales contract. The rest of

transaction amount will be given by purchaser in upcoming year. In this context, the

contribution of this transaction towards net capital gain for this year will be only

$20,000(Stiglitz and Rosengard, 2015). The rest of transaction amount will be considered as

capital gain in next year, when it will be received from purchaser.

(ii) Sale of Antique Bed

In this transaction, there is no specific amount of selling price given in context of Antique

Bes. In this transaction, the client has faced theft of antique four-poster Louis XIV bed from

the house. The amount shown as selling price is the price that will be received by her from

the insurance company. So, different data in context of Antique Bes are as below:

Selling Price (amount received by client from insurance company) = $11,000

Purchase Price = $3,500

Cost of Alterations = $1,500

So, by applying the formula of capital gain or loss on this transaction:

Capital gain/ loss = $11,000 - $3,500 - $1,500

= $6,000

(iii) The Sale of Painting

Following are the data related to purchasing and selling price of painting made by a well

known Australian artist:

Selling Price = $125,000

Purchase Price = $2,000

Application of formula of capital gain/ loss on the transaction of selling painting:

Capital Gain/ Loss = $125,000 - $2,000

= $123,000

Taxation Assignment 6

(iv) Transactions Related to Purchase and Sale of Shares

In context of the purchase and selling of securities of shares of different companies, the

investors also face the brokerage fee, which is also expenditure for the investor. In this

context, the brokerage expense also needs to be reduced from income in order to determine

total capital gain from sell of securities of a company (Dunn, 2011). Similar to this, stamp

duty faced with purchase of securities of a company is also reduced from income for getting

net value of capital gain from a transaction related to purchase and sale of securities in capital

market (Simpson et al., 2013). Following formula can be taken into account for the valuation

of capital gain for the transactions related to investment in securities of different companies:

Capital gain on sale of stocks = Sales price of securities – Purchase price – stamp duty –

brokerage payment

(a) Securities of Common Bank Ltd

Total Sales Price Received from Sale of Securities of a Company can be determined through

use of following formula:

Sales Price = Selling Price of Each Security * Total Number of Shares

= $47 * 1000 = $47,000

Total Purchase Price paid for purchase of Securities of a Company can be determined through

use of following formula:

Total Purchase Cost = Purchase Price of Each Security * Total Number of Securities

= $15 * 1000 = $15,000

Cost of Brokerage Charges = $550

So, by putting the above values in the formula of capital gain:

Capital gain on Shares of Common Bank Ltd = 47,000 – 15000 – 550

= $30,700

(b) Capital gain or loss on sale of securities of PHB Iron Ore Ltd

(iv) Transactions Related to Purchase and Sale of Shares

In context of the purchase and selling of securities of shares of different companies, the

investors also face the brokerage fee, which is also expenditure for the investor. In this

context, the brokerage expense also needs to be reduced from income in order to determine

total capital gain from sell of securities of a company (Dunn, 2011). Similar to this, stamp

duty faced with purchase of securities of a company is also reduced from income for getting

net value of capital gain from a transaction related to purchase and sale of securities in capital

market (Simpson et al., 2013). Following formula can be taken into account for the valuation

of capital gain for the transactions related to investment in securities of different companies:

Capital gain on sale of stocks = Sales price of securities – Purchase price – stamp duty –

brokerage payment

(a) Securities of Common Bank Ltd

Total Sales Price Received from Sale of Securities of a Company can be determined through

use of following formula:

Sales Price = Selling Price of Each Security * Total Number of Shares

= $47 * 1000 = $47,000

Total Purchase Price paid for purchase of Securities of a Company can be determined through

use of following formula:

Total Purchase Cost = Purchase Price of Each Security * Total Number of Securities

= $15 * 1000 = $15,000

Cost of Brokerage Charges = $550

So, by putting the above values in the formula of capital gain:

Capital gain on Shares of Common Bank Ltd = 47,000 – 15000 – 550

= $30,700

(b) Capital gain or loss on sale of securities of PHB Iron Ore Ltd

Taxation Assignment 7

Total Purchase Price paid for purchase of Securities of a Company can be determined through

use of following formula:

Purchase Price of Shares = Purchase Price of Each Stock * Total Number of Stocks

= $12 * 2500 = $30,000

Total Sales Price Received from Sale of Securities of a Company can be determined through

use of following formula:

Value of Sales of Shares = Per Security Selling Price * Number of stocks/ securities

= $25 * 2500 = $62,500

Cost of Brokerage Charges = $1,000

Stamp Duty Paid on the Stocks of PHB Iron Ore Ltd = $1,500

So, value of capital gain on the sale of shares of PHB Iron Ore Ltd can be ascertained through

use of following formula:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 62,500 – 30,000 – 1,000 – 1,500

= $30,000

(c) Capital Gain or Loss on the Sales of Shares of Young Kids Learning Ltd

Total Purchase Price = Per Share Purchase Price * Total Shares Purchased

= $5 * 1200

= $6,000

Total Sales Price of Young Kids Learning Ltd Shares = Per Share Selling Price * Total

Shares

= $0.50 * 1200 = $600

Cost of Stamp Duty Paid = $500

Cost of Brokerage = $100

Total Purchase Price paid for purchase of Securities of a Company can be determined through

use of following formula:

Purchase Price of Shares = Purchase Price of Each Stock * Total Number of Stocks

= $12 * 2500 = $30,000

Total Sales Price Received from Sale of Securities of a Company can be determined through

use of following formula:

Value of Sales of Shares = Per Security Selling Price * Number of stocks/ securities

= $25 * 2500 = $62,500

Cost of Brokerage Charges = $1,000

Stamp Duty Paid on the Stocks of PHB Iron Ore Ltd = $1,500

So, value of capital gain on the sale of shares of PHB Iron Ore Ltd can be ascertained through

use of following formula:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 62,500 – 30,000 – 1,000 – 1,500

= $30,000

(c) Capital Gain or Loss on the Sales of Shares of Young Kids Learning Ltd

Total Purchase Price = Per Share Purchase Price * Total Shares Purchased

= $5 * 1200

= $6,000

Total Sales Price of Young Kids Learning Ltd Shares = Per Share Selling Price * Total

Shares

= $0.50 * 1200 = $600

Cost of Stamp Duty Paid = $500

Cost of Brokerage = $100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation Assignment 8

So, by putting the above values in formula of capital gain:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 600 – 6000 – 100 – 500

= -$6000

(d) Capital Gain or Loss on Sale of Shares of Share Build Ltd

Total Purchase Price = Purchase Price for Each Share * Total Shares Purchased

= $1 * 10,000 = $10,000

Total Sales Price = Selling Price of Each Share * Total Shares Sold

= $2.50 * 10,000 = $25,000

Expense of Stamp Duty faced on the Shares = $1,100

Cost of Brokerage Charges Faced on the Shares = $900

So, by putting the above values in the formula of capital gain:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 25,000 – 10,000 – 900 – 1,100

= $13,000

(v) Valuation of Capital Gain or Loss on the Sale of Violin

Purchasing Price of the Violin = $5,500

Selling Price of Violin = $12,000

So, by putting the above values in the formula of capital gain and loss:

Capital Gain or Loss = Selling Price of Violin – Purchase Price of Violin

= 12,000 - 5,500

= $6,500

So, by putting the above values in formula of capital gain:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 600 – 6000 – 100 – 500

= -$6000

(d) Capital Gain or Loss on Sale of Shares of Share Build Ltd

Total Purchase Price = Purchase Price for Each Share * Total Shares Purchased

= $1 * 10,000 = $10,000

Total Sales Price = Selling Price of Each Share * Total Shares Sold

= $2.50 * 10,000 = $25,000

Expense of Stamp Duty faced on the Shares = $1,100

Cost of Brokerage Charges Faced on the Shares = $900

So, by putting the above values in the formula of capital gain:

Capital Gain = Total Sales Price – Total Purchase Price – Brokerage Cost – Cost of Stamp

Duty

= 25,000 – 10,000 – 900 – 1,100

= $13,000

(v) Valuation of Capital Gain or Loss on the Sale of Violin

Purchasing Price of the Violin = $5,500

Selling Price of Violin = $12,000

So, by putting the above values in the formula of capital gain and loss:

Capital Gain or Loss = Selling Price of Violin – Purchase Price of Violin

= 12,000 - 5,500

= $6,500

Taxation Assignment 9

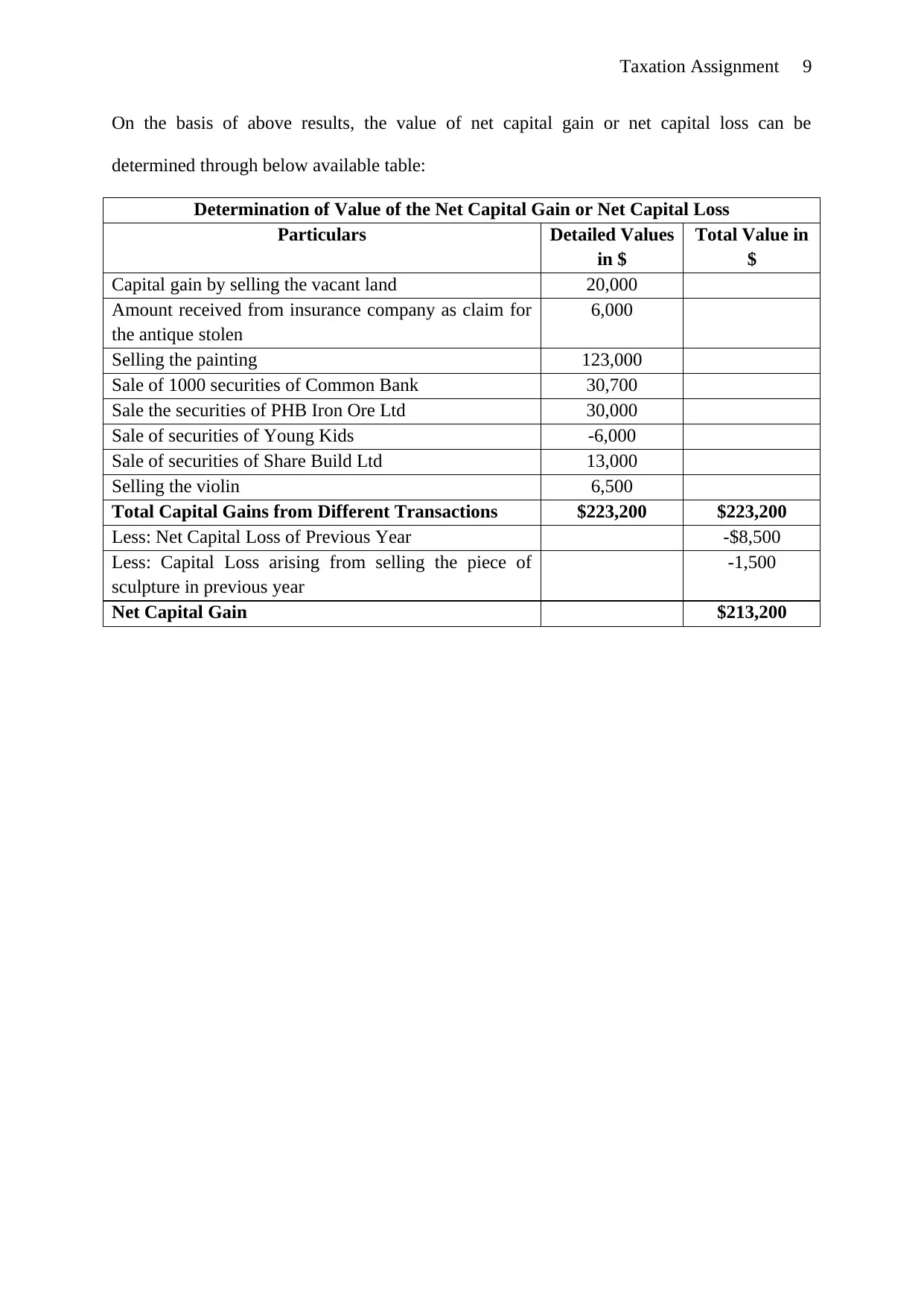

On the basis of above results, the value of net capital gain or net capital loss can be

determined through below available table:

Determination of Value of the Net Capital Gain or Net Capital Loss

Particulars Detailed Values

in $

Total Value in

$

Capital gain by selling the vacant land 20,000

Amount received from insurance company as claim for

the antique stolen

6,000

Selling the painting 123,000

Sale of 1000 securities of Common Bank 30,700

Sale the securities of PHB Iron Ore Ltd 30,000

Sale of securities of Young Kids -6,000

Sale of securities of Share Build Ltd 13,000

Selling the violin 6,500

Total Capital Gains from Different Transactions $223,200 $223,200

Less: Net Capital Loss of Previous Year -$8,500

Less: Capital Loss arising from selling the piece of

sculpture in previous year

-1,500

Net Capital Gain $213,200

On the basis of above results, the value of net capital gain or net capital loss can be

determined through below available table:

Determination of Value of the Net Capital Gain or Net Capital Loss

Particulars Detailed Values

in $

Total Value in

$

Capital gain by selling the vacant land 20,000

Amount received from insurance company as claim for

the antique stolen

6,000

Selling the painting 123,000

Sale of 1000 securities of Common Bank 30,700

Sale the securities of PHB Iron Ore Ltd 30,000

Sale of securities of Young Kids -6,000

Sale of securities of Share Build Ltd 13,000

Selling the violin 6,500

Total Capital Gains from Different Transactions $223,200 $223,200

Less: Net Capital Loss of Previous Year -$8,500

Less: Capital Loss arising from selling the piece of

sculpture in previous year

-1,500

Net Capital Gain $213,200

Taxation Assignment 10

Question 2

FBT Consequences:

In general, the FBT stands for fringe benefit taxation. The FBT is the legislation related to

fringe benefits that applies across the entire Australia. All the employers or companies that

provide fringe benefits to their employees are bound by this law. At the same time, the fringe

benefits can be explained as the monetary or non-monetary benefits that are offered by

different companies to their employees other than their basic salary (Gov Australia, 2017;

Saad, 2014). Different fringe benefits that are given by different companies in different

countries are well refurbished living rooms, flats, personal cars, special membership cards for

restaurants or spa, tickets of foreign tours for spouse or for family, etc. In this context, the

taxes that are levied by regulatory bodies of a country over these fringe benefits are termed as

FBT or Fringe benefit tax (Marsden, 2010). But at the same time, there are some examples of

benefits additional to basic salary of employees that cannot be considered as fringe benefits

by employers or government bodies. These benefits are payment received by employees as

termination pay, company shares given/ allotted to employees under employee share

acquisition programs, and the benefits that are gained by employees from some well known

or international welfare organization or religious firms.

The FBT taxation law is mandatory for compliance for all the employers or companies that

are operating in Australia and offers fringe benefits to their staff. The fringe benefit tax will

also be chargeable on fringe benefits received by the Australian resident workers that are

working doing job abroad. In contrast to this, if a business firm is a foreign company and

offers fringe benefits to workers/ staff in Australia. This type of business entities is also

bound by the FBT taxation law of Australia (McLaren, 2017). In this aspect, Australian

Question 2

FBT Consequences:

In general, the FBT stands for fringe benefit taxation. The FBT is the legislation related to

fringe benefits that applies across the entire Australia. All the employers or companies that

provide fringe benefits to their employees are bound by this law. At the same time, the fringe

benefits can be explained as the monetary or non-monetary benefits that are offered by

different companies to their employees other than their basic salary (Gov Australia, 2017;

Saad, 2014). Different fringe benefits that are given by different companies in different

countries are well refurbished living rooms, flats, personal cars, special membership cards for

restaurants or spa, tickets of foreign tours for spouse or for family, etc. In this context, the

taxes that are levied by regulatory bodies of a country over these fringe benefits are termed as

FBT or Fringe benefit tax (Marsden, 2010). But at the same time, there are some examples of

benefits additional to basic salary of employees that cannot be considered as fringe benefits

by employers or government bodies. These benefits are payment received by employees as

termination pay, company shares given/ allotted to employees under employee share

acquisition programs, and the benefits that are gained by employees from some well known

or international welfare organization or religious firms.

The FBT taxation law is mandatory for compliance for all the employers or companies that

are operating in Australia and offers fringe benefits to their staff. The fringe benefit tax will

also be chargeable on fringe benefits received by the Australian resident workers that are

working doing job abroad. In contrast to this, if a business firm is a foreign company and

offers fringe benefits to workers/ staff in Australia. This type of business entities is also

bound by the FBT taxation law of Australia (McLaren, 2017). In this aspect, Australian

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Assignment 11

government has implemented the double tax agreements with different countries like UK and

the New Zealand. Apart from these, the FBT tax laws are imposed on all the types of

organizations such as sole trader, partnership business firms, private sector and public sector

business firms, as well as the non-profit organizations, if they are paying any fringe benefits

to their employees or members (Nethercott, 2010). It is also stated by the FBT taxation

legislation of Australia that FBT will be applicable on all companies even if they are not

entitled for payment of income tax or personal income tax.

(a) FBT Consequences for Rapid Heat Company

FBT Consequence for Rapid Heat due to Personal Car Offered t its Employee Jasmine:

Rapid Heat Pty ltd has offered a personal car to Jasmine, which is its employee. This benefit

is other than basic salary, so it will be considered as a fringe benefit by the employer. For this

reason, the FAB tax will be applicable on this transaction or benefit. From the analysis of

different tax slabs, it is observed that the chargeable tax rate for this transaction will be 47%

for the company (Gov Australia, 2017; Wilmot, 2012). Following formula is helpful to

determine the tax liability of Rapid Head for this transaction:

Taxable Value for Determination of FBT Consequence (in $) = Type 1 x 2.0802 + Non-

exempt Amount

The valuation of total fringe benefits offered by Rapid Heat Pty ltd is as below:

= total purchase price of car + other expenses incurred on car like repair and maintenance +

total amount of loan received by jasmine from company and used for personal benefit +

indirect fringe received from purchase of electric heater

= 33,000 + 550 + 450,000 + 1,300

= $484,850

In this way, valuation of taxable value will be as below:

Taxable Value = 484,850 x 2.0802

government has implemented the double tax agreements with different countries like UK and

the New Zealand. Apart from these, the FBT tax laws are imposed on all the types of

organizations such as sole trader, partnership business firms, private sector and public sector

business firms, as well as the non-profit organizations, if they are paying any fringe benefits

to their employees or members (Nethercott, 2010). It is also stated by the FBT taxation

legislation of Australia that FBT will be applicable on all companies even if they are not

entitled for payment of income tax or personal income tax.

(a) FBT Consequences for Rapid Heat Company

FBT Consequence for Rapid Heat due to Personal Car Offered t its Employee Jasmine:

Rapid Heat Pty ltd has offered a personal car to Jasmine, which is its employee. This benefit

is other than basic salary, so it will be considered as a fringe benefit by the employer. For this

reason, the FAB tax will be applicable on this transaction or benefit. From the analysis of

different tax slabs, it is observed that the chargeable tax rate for this transaction will be 47%

for the company (Gov Australia, 2017; Wilmot, 2012). Following formula is helpful to

determine the tax liability of Rapid Head for this transaction:

Taxable Value for Determination of FBT Consequence (in $) = Type 1 x 2.0802 + Non-

exempt Amount

The valuation of total fringe benefits offered by Rapid Heat Pty ltd is as below:

= total purchase price of car + other expenses incurred on car like repair and maintenance +

total amount of loan received by jasmine from company and used for personal benefit +

indirect fringe received from purchase of electric heater

= 33,000 + 550 + 450,000 + 1,300

= $484,850

In this way, valuation of taxable value will be as below:

Taxable Value = 484,850 x 2.0802

Taxation Assignment 12

= $1008584.97

In this context, the FBT consequence for Rapid Heat can be ascertained in following way:

FBT Consequence = Total Taxable Amount x FBT Tax Rate

= 1008584.97 x 47%

= $474,034.94

(b) FBT Consequences if Remaining $50,000 is also used by Jasmine

Valuation of FBT Tax, if the Remaining Loan of $50,000 is used by Jasmine for Investment

in Securities not by Her Husband:

If this amount is not used by her husband and it is used by Jasmine for investment in the

securities of same company (stocks of Telstra Company), then this amount will also be added

while determining total taxable amount (Blue and Blue, 2016). Following formula can be

taken into account for valuation of total fringe benefit’s value:

Total Amount of Fringe Benefits by Rapid Heat = total purchase price of car + other

expenses incurred on car like repair and maintenance + total amount of loan received by

jasmine from company and used for personal benefit + Amount used for investment in

securities of Telstra + indirect fringe received from purchase of electric heater

= 33,000 + 550 + 450,000 + 50,000 + 1,300

= $534,850

Formula of Total Taxable Amount = Type 1 x 2.0802

= 534,850 x 2.0802

= $1,112,594.9

In this way, the FBT tax chargeable from Rapid Heat can be determined through below

available formula:

FBT Tax = Total Taxable Amount x FBT Tax Rate

= $1,112,594.9 x 47%

= $1008584.97

In this context, the FBT consequence for Rapid Heat can be ascertained in following way:

FBT Consequence = Total Taxable Amount x FBT Tax Rate

= 1008584.97 x 47%

= $474,034.94

(b) FBT Consequences if Remaining $50,000 is also used by Jasmine

Valuation of FBT Tax, if the Remaining Loan of $50,000 is used by Jasmine for Investment

in Securities not by Her Husband:

If this amount is not used by her husband and it is used by Jasmine for investment in the

securities of same company (stocks of Telstra Company), then this amount will also be added

while determining total taxable amount (Blue and Blue, 2016). Following formula can be

taken into account for valuation of total fringe benefit’s value:

Total Amount of Fringe Benefits by Rapid Heat = total purchase price of car + other

expenses incurred on car like repair and maintenance + total amount of loan received by

jasmine from company and used for personal benefit + Amount used for investment in

securities of Telstra + indirect fringe received from purchase of electric heater

= 33,000 + 550 + 450,000 + 50,000 + 1,300

= $534,850

Formula of Total Taxable Amount = Type 1 x 2.0802

= 534,850 x 2.0802

= $1,112,594.9

In this way, the FBT tax chargeable from Rapid Heat can be determined through below

available formula:

FBT Tax = Total Taxable Amount x FBT Tax Rate

= $1,112,594.9 x 47%

Taxation Assignment 13

= $522,919.603

Conclusion

As per the findings from accomplishment of this report, it is observed that FBT stands for the

fringe benefit tax that is applicable across Australia. All the companies that are providing

fringe benefits to their employees have to face this tax. From calculation of capital gains, it is

analysed that gains resulting from different transactions are added in the net capital gain of

company only in the year, in which such benefits are received by the company. From

completion of this report, it is also found out that fringe benefit tax rate that is imposed by

Australian government over the employers is 47% for year ending March 2018 and March

2019. There are certain benefits, which are exempt from FBT consequences such as the

benefits that are offered by some international welfare organization or religious entity,

dividend benefits received from companies, termination payment and the benefits received in

the form of allotment of shares under employee share acquisition program.

= $522,919.603

Conclusion

As per the findings from accomplishment of this report, it is observed that FBT stands for the

fringe benefit tax that is applicable across Australia. All the companies that are providing

fringe benefits to their employees have to face this tax. From calculation of capital gains, it is

analysed that gains resulting from different transactions are added in the net capital gain of

company only in the year, in which such benefits are received by the company. From

completion of this report, it is also found out that fringe benefit tax rate that is imposed by

Australian government over the employers is 47% for year ending March 2018 and March

2019. There are certain benefits, which are exempt from FBT consequences such as the

benefits that are offered by some international welfare organization or religious entity,

dividend benefits received from companies, termination payment and the benefits received in

the form of allotment of shares under employee share acquisition program.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation Assignment 14

References

Becker, J., Reimer, E. and Rust, A. (2015) Klaus Vogel on Double Taxation Conventions.

Netherlands: Kluwer Law International.

Blue, R. and Blue, M. (2016) Master Your Money: A Step-by-Step Plan for Experiencing

Financial Contentment. USA: Moody Publishers.

Dunn, J. (2011) Share Investing For Dummies. USA: John Wiley & Sons.

Gov Australia (2017) Fringe benefits tax - a guide for employers. [Online]. Available at:

https://www.ato.gov.au/law/view/document?DocID=SAV%2FFBTGEMP%2F00002

(Accessed: 21 September 2018).

Marsden, S.J. (2010) Australian Master Bookkeepers Guide [2009/10]. Australia: CCH

Australia Limited.

McLaren, J. (2017) The Economic Development of Northern Australia: A Critical Review of

the Taxation Benefits and Incentives Both Past and Present and the Potential Taxation

Options for the Future. J. Australasian Tax Tchrs. Ass'n, 12, pp. 01-10.

Nethercott, L. (2010) Australian Taxation Study Manual: Questions and Suggested Solutions.

Australia: CCH Australia Limited.

Saad, N. (2014) Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp. 1069-1075.

Simpson, M., Johnson, A., Ford, P., McGhee, H., Morley, P., Nicholson, S. and Vaines, P.

(2013) Tax Aspects of the Purchase and Sale of a Private Company's Shares. UK: A&C

Black.

Stiglitz, J.E. and Rosengard, J.K. (2015) Economics of the public sector: Fourth international

student edition. New York: WW Norton & Company.

Wilmot, C. (2012) FBT Compliance Guide 2012. Australia: CCH Australia Limited.

References

Becker, J., Reimer, E. and Rust, A. (2015) Klaus Vogel on Double Taxation Conventions.

Netherlands: Kluwer Law International.

Blue, R. and Blue, M. (2016) Master Your Money: A Step-by-Step Plan for Experiencing

Financial Contentment. USA: Moody Publishers.

Dunn, J. (2011) Share Investing For Dummies. USA: John Wiley & Sons.

Gov Australia (2017) Fringe benefits tax - a guide for employers. [Online]. Available at:

https://www.ato.gov.au/law/view/document?DocID=SAV%2FFBTGEMP%2F00002

(Accessed: 21 September 2018).

Marsden, S.J. (2010) Australian Master Bookkeepers Guide [2009/10]. Australia: CCH

Australia Limited.

McLaren, J. (2017) The Economic Development of Northern Australia: A Critical Review of

the Taxation Benefits and Incentives Both Past and Present and the Potential Taxation

Options for the Future. J. Australasian Tax Tchrs. Ass'n, 12, pp. 01-10.

Nethercott, L. (2010) Australian Taxation Study Manual: Questions and Suggested Solutions.

Australia: CCH Australia Limited.

Saad, N. (2014) Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp. 1069-1075.

Simpson, M., Johnson, A., Ford, P., McGhee, H., Morley, P., Nicholson, S. and Vaines, P.

(2013) Tax Aspects of the Purchase and Sale of a Private Company's Shares. UK: A&C

Black.

Stiglitz, J.E. and Rosengard, J.K. (2015) Economics of the public sector: Fourth international

student edition. New York: WW Norton & Company.

Wilmot, C. (2012) FBT Compliance Guide 2012. Australia: CCH Australia Limited.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.