Taxation Law: Accounting Transactions and Tax Treatment

VerifiedAdded on 2023/06/04

|11

|2071

|176

AI Summary

This report discusses the appropriate tax treatment for accounting transactions under ITAA 1997 and ITAA 1936. It covers topics such as trading stock, service revenue, depreciation, repairs and maintenance, employee entertainment cost, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Tax treatment for Accounting Transactions...............................................................................2

Conclusion:................................................................................................................................7

References:.................................................................................................................................8

Table of Contents

Introduction:...............................................................................................................................2

Tax treatment for Accounting Transactions...............................................................................2

Conclusion:................................................................................................................................7

References:.................................................................................................................................8

2TAXATION LAW

Introduction:

Under the accrual process of accounting expenses arising from the liabilities must be

measured by considering the expected cash flow. Similarly, the tax expenses must replicate

sum of taxes to be paid in the current or future accounting period. The report would be

addressing the CFO of Technical Computer Pty Ltd for appropriate accounting treatment of

transactions to reflect the correct tax amount. The report would consider appropriate

provision of “ITAA 1997” and “ITAA 1936” in providing an explanation of treatment of

each items.

Tax treatment for Accounting Transactions

The tax treatment for each items is given below;

1). Valuation of Trading Stock in Hand: As per “taxation ruling of IT 2670” goods are

considered as trading stock in hand inside the “section 28 of the ITAA 1936” regardless

whether the goods are to be delivered physically or to the premises of taxpayer. The law court

in “All States Frozen Foods Pty Ltd v FC of T (1990)” stated that goods that are in the

transportation stage will be treated as trading stock in hand (Barkoczy 2014). For Technology

Pty Ltd the trading stock which is in transit from Singapore should be treated as stock in

hand. The amount will be included under the heads of assessable income.

2). Service revenue $50,000: As per the “taxation ruling of TR 2014/1” any amount

attributable in respect of contractual obligations under “contingency of repayment” the sum

will be treated as derived for assessment purpose under “section 6-5 of the ITAA 1997”

when the requirements are performed exclusively (James 2016). Similarly in “Arthur

Murray (NSW) Pty Ltd v FC of T (1965)” when it is noticed that the requirements of the

goods is performed and repayment contingency has lapsed the sum turns from “unearned

Introduction:

Under the accrual process of accounting expenses arising from the liabilities must be

measured by considering the expected cash flow. Similarly, the tax expenses must replicate

sum of taxes to be paid in the current or future accounting period. The report would be

addressing the CFO of Technical Computer Pty Ltd for appropriate accounting treatment of

transactions to reflect the correct tax amount. The report would consider appropriate

provision of “ITAA 1997” and “ITAA 1936” in providing an explanation of treatment of

each items.

Tax treatment for Accounting Transactions

The tax treatment for each items is given below;

1). Valuation of Trading Stock in Hand: As per “taxation ruling of IT 2670” goods are

considered as trading stock in hand inside the “section 28 of the ITAA 1936” regardless

whether the goods are to be delivered physically or to the premises of taxpayer. The law court

in “All States Frozen Foods Pty Ltd v FC of T (1990)” stated that goods that are in the

transportation stage will be treated as trading stock in hand (Barkoczy 2014). For Technology

Pty Ltd the trading stock which is in transit from Singapore should be treated as stock in

hand. The amount will be included under the heads of assessable income.

2). Service revenue $50,000: As per the “taxation ruling of TR 2014/1” any amount

attributable in respect of contractual obligations under “contingency of repayment” the sum

will be treated as derived for assessment purpose under “section 6-5 of the ITAA 1997”

when the requirements are performed exclusively (James 2016). Similarly in “Arthur

Murray (NSW) Pty Ltd v FC of T (1965)” when it is noticed that the requirements of the

goods is performed and repayment contingency has lapsed the sum turns from “unearned

3TAXATION LAW

income” to “earned income” (Brokelind 2015). The amount of $50,000 shall be included for

taxable purpose under “section 6-5 of the ITAA 1997” based on ordinary concepts.

3). Depreciation charged on Plant: The deprecation expenses that is charged on the plant

stands $300,000. The sum will be treated for assessment as “amounts not deductible” in

ascertaining the net sum of accounting profit (Grange, Jover-Ledesma and Maydew 2014).

The reason for this is that depreciation method undertaken for accounting purpose reflects

differences from the process of depreciation undertaken for taxation purpose.

4). Accounting profit made from the sale of machine: For Technology Pty Ltd the disposal

of machinery has given rise to gains for accounting purpose. The gains shall be treated as the

taxable profit obtained from machine on the basis of original cost (Jover-Ledesma 2015). The

accounting profit that is obtained from the disposal of machine is included for taxation

purpose based on actual machinery cost. The sum of $100,000 has been included for

assessment purpose under the heads of “assessable amount”.

5). Repairs and Maintenance Expenditure: Below stated are the tax treatment for the

repairs and maintenance for Technology Pty Ltd.

a) Cost of replacing the entire roof: An explanation relating to repairs has been provided

under “taxation ruling of TR 93/23” where repairs carried on the premises of capital nature

are not treated as allowable deductions under the “section 25-10 of the ITAA 1997” (Kenny,

Blissenden and Villios 2018). The court in “Sun Newspaper Ltd v FC of T (1938)” gave its

judgement by stating that cost of replacing the business structure is treated as capital

expenditure. In the current situation it is noticed that cost has been incurred by the company

in replacing the entire roof of the factory that is damaged in hailstorm. The cost incurred

represents in entirety of the premises which is deductible under “section 25-10 of the ITAA

1997”.

income” to “earned income” (Brokelind 2015). The amount of $50,000 shall be included for

taxable purpose under “section 6-5 of the ITAA 1997” based on ordinary concepts.

3). Depreciation charged on Plant: The deprecation expenses that is charged on the plant

stands $300,000. The sum will be treated for assessment as “amounts not deductible” in

ascertaining the net sum of accounting profit (Grange, Jover-Ledesma and Maydew 2014).

The reason for this is that depreciation method undertaken for accounting purpose reflects

differences from the process of depreciation undertaken for taxation purpose.

4). Accounting profit made from the sale of machine: For Technology Pty Ltd the disposal

of machinery has given rise to gains for accounting purpose. The gains shall be treated as the

taxable profit obtained from machine on the basis of original cost (Jover-Ledesma 2015). The

accounting profit that is obtained from the disposal of machine is included for taxation

purpose based on actual machinery cost. The sum of $100,000 has been included for

assessment purpose under the heads of “assessable amount”.

5). Repairs and Maintenance Expenditure: Below stated are the tax treatment for the

repairs and maintenance for Technology Pty Ltd.

a) Cost of replacing the entire roof: An explanation relating to repairs has been provided

under “taxation ruling of TR 93/23” where repairs carried on the premises of capital nature

are not treated as allowable deductions under the “section 25-10 of the ITAA 1997” (Kenny,

Blissenden and Villios 2018). The court in “Sun Newspaper Ltd v FC of T (1938)” gave its

judgement by stating that cost of replacing the business structure is treated as capital

expenditure. In the current situation it is noticed that cost has been incurred by the company

in replacing the entire roof of the factory that is damaged in hailstorm. The cost incurred

represents in entirety of the premises which is deductible under “section 25-10 of the ITAA

1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

b). Cost of demolishing redundant building: Technology Pty Ltd incurred expenses on

demolition of the redundant building. The expenses incurred were in nature of reconstruction

of the entirety. The court in “Lindsay v FC of T (1960)” explained entirety as the separately

identifiable item of capital equipment (McCouat 2018). It stated that expenses occurred in

replacing or establishing the profit making structure are treated as capital expenses within the

meaning of “section 25-10 of the ITAA 1997”. Similarly for Technological Pty Ltd the cost

of $5,400 will be added to the profits under the heads of “items not allowed as deductions”.

c). Cost of converting the old storeroom into factory space: The court in “Sun Newspaper

Ltd v FC of T (1938)” provided a differentiation regarding the capital and revenue expenses

(Kenny 2014). The court decision stated that outgoings incurred in enlarging the revenue

yielding structures are not permitted for deductions. The expense of $14,800 reported by

Technology Pty Ltd for turning the old storeroom into factory is a capital expenses of

reconstruction of entirety. The sum of $14,800 is recorded under the “items not allowed as

deductions”.

6). Written off borrowing expenses: As per “section 8-1, ITAA 1997” taxpayers are

permitted to claim deductions for expenses occurred in derivation of assessable income. The

court in “FC of T v Lunney & Anor (1958)” held that the character of the outgoings must be

judged whether they are occurred in derivation of assessable income (Sadiq et al. 2018). The

borrowing expenses reported by Technology Pty Ltd is associated to derivation of assessable

income. Hence, the borrowing cost is recorded under “deductible and non-assessable” for

subtraction purpose.

7). Surplus on sale of land: Under “section 104-10 (1) of the ITAA 1997” a CGT event A1

happens when a commercial property is sold and result in capital gains or loss (Morgan,

Mortimer and Pinto 2017). As understood Technology Pty Ltd makes a capital gains in the

b). Cost of demolishing redundant building: Technology Pty Ltd incurred expenses on

demolition of the redundant building. The expenses incurred were in nature of reconstruction

of the entirety. The court in “Lindsay v FC of T (1960)” explained entirety as the separately

identifiable item of capital equipment (McCouat 2018). It stated that expenses occurred in

replacing or establishing the profit making structure are treated as capital expenses within the

meaning of “section 25-10 of the ITAA 1997”. Similarly for Technological Pty Ltd the cost

of $5,400 will be added to the profits under the heads of “items not allowed as deductions”.

c). Cost of converting the old storeroom into factory space: The court in “Sun Newspaper

Ltd v FC of T (1938)” provided a differentiation regarding the capital and revenue expenses

(Kenny 2014). The court decision stated that outgoings incurred in enlarging the revenue

yielding structures are not permitted for deductions. The expense of $14,800 reported by

Technology Pty Ltd for turning the old storeroom into factory is a capital expenses of

reconstruction of entirety. The sum of $14,800 is recorded under the “items not allowed as

deductions”.

6). Written off borrowing expenses: As per “section 8-1, ITAA 1997” taxpayers are

permitted to claim deductions for expenses occurred in derivation of assessable income. The

court in “FC of T v Lunney & Anor (1958)” held that the character of the outgoings must be

judged whether they are occurred in derivation of assessable income (Sadiq et al. 2018). The

borrowing expenses reported by Technology Pty Ltd is associated to derivation of assessable

income. Hence, the borrowing cost is recorded under “deductible and non-assessable” for

subtraction purpose.

7). Surplus on sale of land: Under “section 104-10 (1) of the ITAA 1997” a CGT event A1

happens when a commercial property is sold and result in capital gains or loss (Morgan,

Mortimer and Pinto 2017). As understood Technology Pty Ltd makes a capital gains in the

5TAXATION LAW

form of accounting profit upon the disposal of surplus land. The gains under “section 104-10

(1) of the ITAA 1997” has given rise to CGT event A1. The profit is recorded as taxable

amount under heads of assessable income.

8). Employee entertainment cost: As evident the company has reported an expenditure

towards employee entertainment. The employee entertainment expenses has been identified

in the expenditure and it is treated as deductible expenditure.

9). Provision for long service leave and holiday: Provision for long holiday and long

service leave in the form of accrued expenses constitute liability for the company based on

the accounting standards. In determining tax, a deduction is disregarded for accrued leave or

provision for holiday. Deductions are only allowed when the expenses are actually incurred.

Under “section 705-80” the expenses must be adjusted and such provision are included as

liability for the joining entity (Woellner et al. 2018). As evident in Technology Pty Ltd a

provision was increased by the directors relating to holiday and long service leave that

amounted to $60,000. The provision expense constitute liability for the company here and

sum will be added back under “amounts non-deductible”.

10). Research expenses on feasibility of opening new factory: Losses or outgoings that are

preliminary in the start of business activities are not treated as incurred during the course of

business. Therefore, the pre-commencement expenses are non-deductible under provision of

“section 8-1, ITAA 1997”. In “Softwood Pulp and Paper v FC of T (1976)” the taxpayer

was denied deductions for feasibility expenses since the expenses were incurred as

preliminary in start of business (Taylor et al. 2018). For Technology Pty Ltd feasibility

expenses on opening new factory is preliminary in start of business and non-allowable

deductions. The sum is recorded under “amounts not deductible.

form of accounting profit upon the disposal of surplus land. The gains under “section 104-10

(1) of the ITAA 1997” has given rise to CGT event A1. The profit is recorded as taxable

amount under heads of assessable income.

8). Employee entertainment cost: As evident the company has reported an expenditure

towards employee entertainment. The employee entertainment expenses has been identified

in the expenditure and it is treated as deductible expenditure.

9). Provision for long service leave and holiday: Provision for long holiday and long

service leave in the form of accrued expenses constitute liability for the company based on

the accounting standards. In determining tax, a deduction is disregarded for accrued leave or

provision for holiday. Deductions are only allowed when the expenses are actually incurred.

Under “section 705-80” the expenses must be adjusted and such provision are included as

liability for the joining entity (Woellner et al. 2018). As evident in Technology Pty Ltd a

provision was increased by the directors relating to holiday and long service leave that

amounted to $60,000. The provision expense constitute liability for the company here and

sum will be added back under “amounts non-deductible”.

10). Research expenses on feasibility of opening new factory: Losses or outgoings that are

preliminary in the start of business activities are not treated as incurred during the course of

business. Therefore, the pre-commencement expenses are non-deductible under provision of

“section 8-1, ITAA 1997”. In “Softwood Pulp and Paper v FC of T (1976)” the taxpayer

was denied deductions for feasibility expenses since the expenses were incurred as

preliminary in start of business (Taylor et al. 2018). For Technology Pty Ltd feasibility

expenses on opening new factory is preliminary in start of business and non-allowable

deductions. The sum is recorded under “amounts not deductible.

6TAXATION LAW

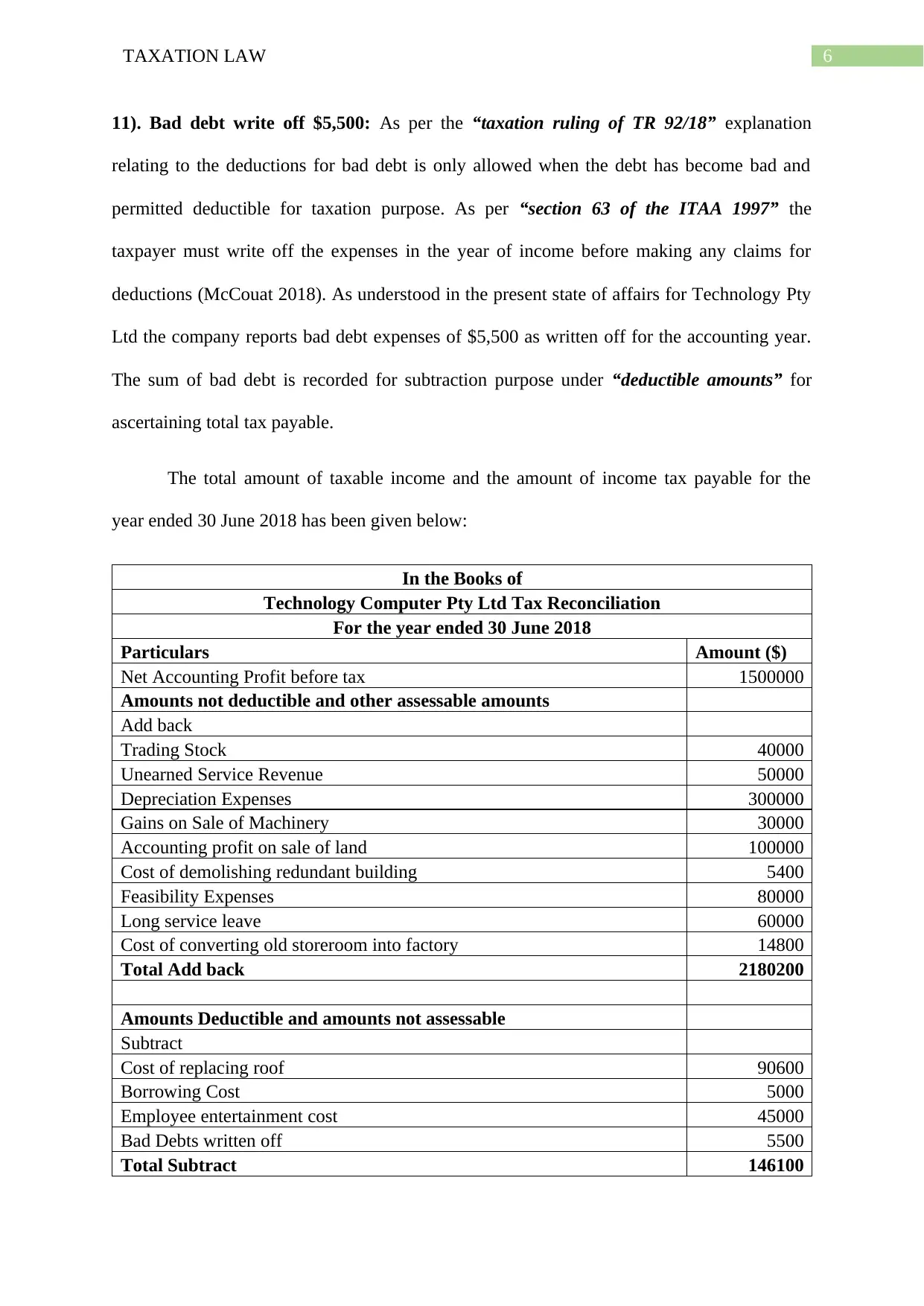

11). Bad debt write off $5,500: As per the “taxation ruling of TR 92/18” explanation

relating to the deductions for bad debt is only allowed when the debt has become bad and

permitted deductible for taxation purpose. As per “section 63 of the ITAA 1997” the

taxpayer must write off the expenses in the year of income before making any claims for

deductions (McCouat 2018). As understood in the present state of affairs for Technology Pty

Ltd the company reports bad debt expenses of $5,500 as written off for the accounting year.

The sum of bad debt is recorded for subtraction purpose under “deductible amounts” for

ascertaining total tax payable.

The total amount of taxable income and the amount of income tax payable for the

year ended 30 June 2018 has been given below:

In the Books of

Technology Computer Pty Ltd Tax Reconciliation

For the year ended 30 June 2018

Particulars Amount ($)

Net Accounting Profit before tax 1500000

Amounts not deductible and other assessable amounts

Add back

Trading Stock 40000

Unearned Service Revenue 50000

Depreciation Expenses 300000

Gains on Sale of Machinery 30000

Accounting profit on sale of land 100000

Cost of demolishing redundant building 5400

Feasibility Expenses 80000

Long service leave 60000

Cost of converting old storeroom into factory 14800

Total Add back 2180200

Amounts Deductible and amounts not assessable

Subtract

Cost of replacing roof 90600

Borrowing Cost 5000

Employee entertainment cost 45000

Bad Debts written off 5500

Total Subtract 146100

11). Bad debt write off $5,500: As per the “taxation ruling of TR 92/18” explanation

relating to the deductions for bad debt is only allowed when the debt has become bad and

permitted deductible for taxation purpose. As per “section 63 of the ITAA 1997” the

taxpayer must write off the expenses in the year of income before making any claims for

deductions (McCouat 2018). As understood in the present state of affairs for Technology Pty

Ltd the company reports bad debt expenses of $5,500 as written off for the accounting year.

The sum of bad debt is recorded for subtraction purpose under “deductible amounts” for

ascertaining total tax payable.

The total amount of taxable income and the amount of income tax payable for the

year ended 30 June 2018 has been given below:

In the Books of

Technology Computer Pty Ltd Tax Reconciliation

For the year ended 30 June 2018

Particulars Amount ($)

Net Accounting Profit before tax 1500000

Amounts not deductible and other assessable amounts

Add back

Trading Stock 40000

Unearned Service Revenue 50000

Depreciation Expenses 300000

Gains on Sale of Machinery 30000

Accounting profit on sale of land 100000

Cost of demolishing redundant building 5400

Feasibility Expenses 80000

Long service leave 60000

Cost of converting old storeroom into factory 14800

Total Add back 2180200

Amounts Deductible and amounts not assessable

Subtract

Cost of replacing roof 90600

Borrowing Cost 5000

Employee entertainment cost 45000

Bad Debts written off 5500

Total Subtract 146100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

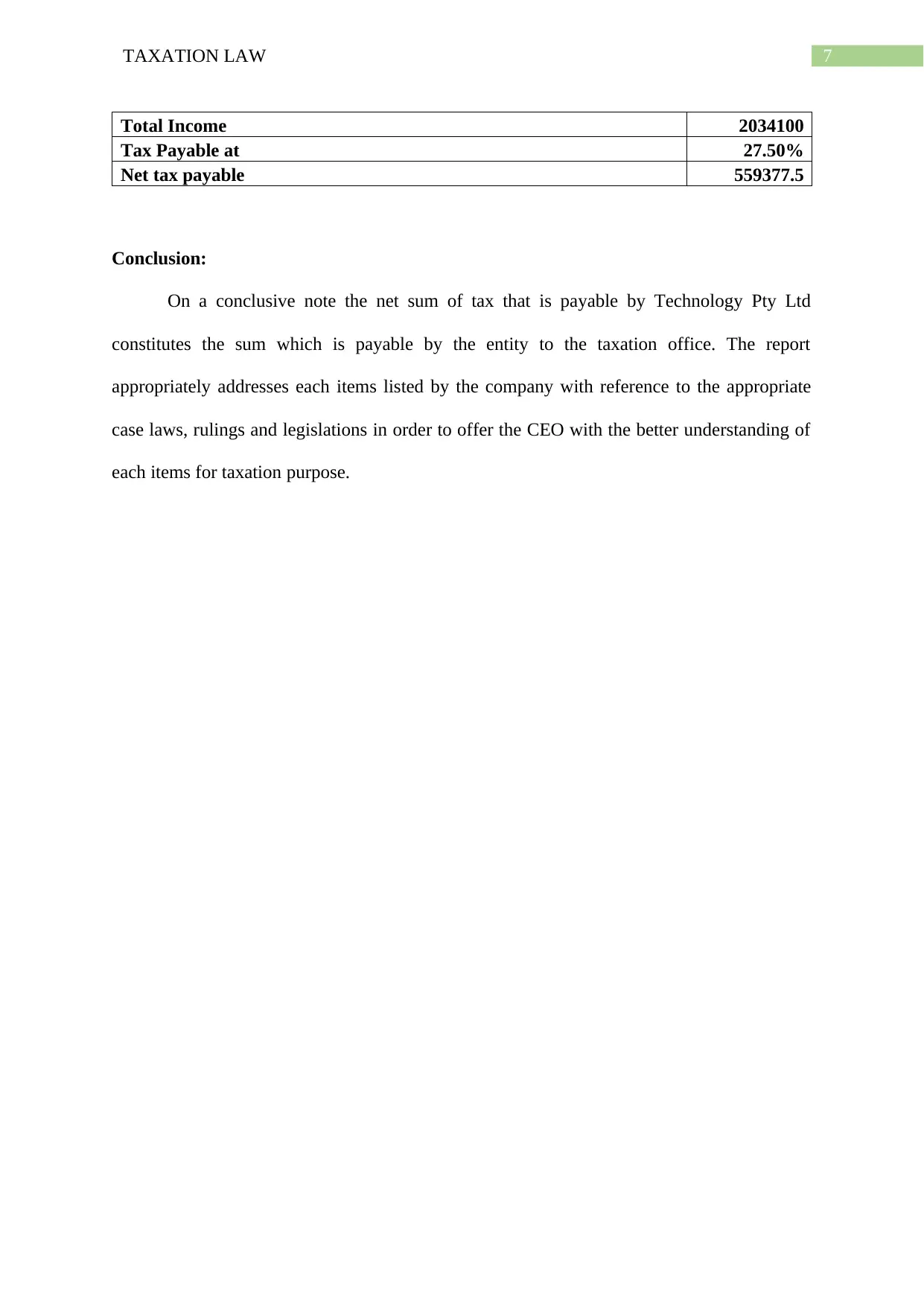

Total Income 2034100

Tax Payable at 27.50%

Net tax payable 559377.5

Conclusion:

On a conclusive note the net sum of tax that is payable by Technology Pty Ltd

constitutes the sum which is payable by the entity to the taxation office. The report

appropriately addresses each items listed by the company with reference to the appropriate

case laws, rulings and legislations in order to offer the CEO with the better understanding of

each items for taxation purpose.

Total Income 2034100

Tax Payable at 27.50%

Net tax payable 559377.5

Conclusion:

On a conclusive note the net sum of tax that is payable by Technology Pty Ltd

constitutes the sum which is payable by the entity to the taxation office. The report

appropriately addresses each items listed by the company with reference to the appropriate

case laws, rulings and legislations in order to offer the CEO with the better understanding of

each items for taxation purpose.

8TAXATION LAW

References:

Barkoczy, S. 2014. Foundations of taxation law.

Brokelind, C. 2015. Principles of law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014.Principles of business taxation.

James, S. 2016. The economics of taxation.

Jover-Ledesma, G. 2015. Principles of business taxation: Cch Incorporated.

Kenny, P. 2014. Australian tax.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. 2018. Australian master GST guide.

Morgan, A., Mortimer, C. and Pinto, D. 2017. A practical introduction to Australian taxation

law.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Taylor, C., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2018. Understanding taxation

law 2018.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2018. Australian taxation

law.

References:

Barkoczy, S. 2014. Foundations of taxation law.

Brokelind, C. 2015. Principles of law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014.Principles of business taxation.

James, S. 2016. The economics of taxation.

Jover-Ledesma, G. 2015. Principles of business taxation: Cch Incorporated.

Kenny, P. 2014. Australian tax.

Kenny, P., Blissenden, M. and Villios, S. 2018. Australian Tax.

McCouat, P. 2018. Australian master GST guide.

Morgan, A., Mortimer, C. and Pinto, D. 2017. A practical introduction to Australian taxation

law.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., Teoh, J. and Ting,

A. 2018. Principles of taxation law.

Taylor, C., Walpole, M., Burton, M., Ciro, T. and Murray, I. 2018. Understanding taxation

law 2018.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2018. Australian taxation

law.

9TAXATION LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.