Assessing Taxpayer Response to Fringe Benefit Rule Changes

VerifiedAdded on 2020/07/22

|15

|4093

|73

AI Summary

This assignment, titled 'Assessing Taxpayer Response to Fringe Benefit Rule Changes', requires an analysis of how taxpayers responded to legislative alterations in the area of in-house fringe benefits. The case study focuses on a specific rule change and its impact on taxpayers' behavior. The goal is to understand how these changes influenced tax management practices, compliance costs, and potential avoidance strategies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW AND PRACTICE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

PART A.........................................................................................................................................................3

Primary sources of commonwealth parliament.......................................................................................3

Tax law primary source............................................................................................................................3

Taxation ruling TR 98/17..........................................................................................................................3

Measurements of Medicare levy.............................................................................................................4

Commonwealth and legislations..............................................................................................................4

Specific deductions by ITAA 97 25-45......................................................................................................4

Case law and the significance of high court.............................................................................................5

Stock on hand and their valuation...........................................................................................................5

Tax to be paid for $45000 earning...........................................................................................................6

PAYG collections......................................................................................................................................6

PART B.........................................................................................................................................................6

PART C.........................................................................................................................................................8

PART D.......................................................................................................................................................11

REFERENCES..............................................................................................................................................14

PART A.........................................................................................................................................................3

Primary sources of commonwealth parliament.......................................................................................3

Tax law primary source............................................................................................................................3

Taxation ruling TR 98/17..........................................................................................................................3

Measurements of Medicare levy.............................................................................................................4

Commonwealth and legislations..............................................................................................................4

Specific deductions by ITAA 97 25-45......................................................................................................4

Case law and the significance of high court.............................................................................................5

Stock on hand and their valuation...........................................................................................................5

Tax to be paid for $45000 earning...........................................................................................................6

PAYG collections......................................................................................................................................6

PART B.........................................................................................................................................................6

PART C.........................................................................................................................................................8

PART D.......................................................................................................................................................11

REFERENCES..............................................................................................................................................14

PART A

Primary sources of commonwealth parliament

The constitution of the commonwealth taxation is under section 51 of

the parliament ATO. It includes all the power and legislation of these law but

without residual powers of commonwealth. Federation from 1901 the laws

have began to granting the powers to various states of Australia (Porter,

Allen & Thompson, 2014). The power to make laws and rules had been

described in the section 39-51 which facilitates the laws with all the legal

rules and regulations to be followed. The financial power and interest trade

laws are described in various sections of commonwealth law and ATO is in

under ITCP (s51(1)) that provide necessary information regarding trade and

commerce in states and several foreign nations.

Tax law primary source

Public laws, internal revenue and income tax treaties are the various

codes of federal laws which are highly authorised and the primary sources of

taxation. The treasury regulation can be known by the IRS which made

various rules and regulation. This facilitate the support to codes and includes

various taxation or revenue rulings, treasury decisions made by the taxation

authority (Tran-Nam, Evans & Lignier, 2014). The taxation related rule and

decisions are to be made with the help of technical advices, revenue

procedures and private latter.

Internal revenue service: this is the primary source of implicating

the taxes over the revenue retain by an individual. This authority is consists

of all the rules and regulation which are being mentioned as in Tax rulings,

various sections and acts.

Taxation ruling TR 98/17

Taxation rulings helps the ATO in deciding the various laws, rules and

regulations imposed over several acts and they provide rights and authority

to such taxation acts. Rulings fixed by federal legislation can be described

under s6(i) of income tax assessment act 1936 and ITAA 1997. TR98/17 of

3

Primary sources of commonwealth parliament

The constitution of the commonwealth taxation is under section 51 of

the parliament ATO. It includes all the power and legislation of these law but

without residual powers of commonwealth. Federation from 1901 the laws

have began to granting the powers to various states of Australia (Porter,

Allen & Thompson, 2014). The power to make laws and rules had been

described in the section 39-51 which facilitates the laws with all the legal

rules and regulations to be followed. The financial power and interest trade

laws are described in various sections of commonwealth law and ATO is in

under ITCP (s51(1)) that provide necessary information regarding trade and

commerce in states and several foreign nations.

Tax law primary source

Public laws, internal revenue and income tax treaties are the various

codes of federal laws which are highly authorised and the primary sources of

taxation. The treasury regulation can be known by the IRS which made

various rules and regulation. This facilitate the support to codes and includes

various taxation or revenue rulings, treasury decisions made by the taxation

authority (Tran-Nam, Evans & Lignier, 2014). The taxation related rule and

decisions are to be made with the help of technical advices, revenue

procedures and private latter.

Internal revenue service: this is the primary source of implicating

the taxes over the revenue retain by an individual. This authority is consists

of all the rules and regulation which are being mentioned as in Tax rulings,

various sections and acts.

Taxation ruling TR 98/17

Taxation rulings helps the ATO in deciding the various laws, rules and

regulations imposed over several acts and they provide rights and authority

to such taxation acts. Rulings fixed by federal legislation can be described

under s6(i) of income tax assessment act 1936 and ITAA 1997. TR98/17 of

3

the acts provides information about the taxation policies to be followed for

residential in Australia which can be described as several different

individuals who residence in Australia such as Migrants from this nation,

people come from different country for work and employment purpose,

students residents in Australia come from different nation for gaining the

education or enrolled in any college or university (Magnusson, 2014). It also

includes tourists who came in Australia for temporary visit or stay.

Measurements of Medicare levy

Medicare levy is a rebate that has been charged by the Australian

government over assessable income gain by the individuals which in context

with facilitating or providing the benefits health and care security to such

individuals (Apps, Long & Rees, 2014). It can be calculated by adding 2% of

the taxable earning by persons. If an individual has gain the insurance cover

from the medical unit of registered hospital of Australia than he will not be

liable add any surcharge over his income. Medicare levy can be assign to

those who are residents in Australia, non residents are not facilitated with it.

Commonwealth and legislations

As per the Competition and consumer act 2010 of ITAA 1997 has

facilitates many rules and regulation to deal with the case in which a

company is misleading or deducting cost of the fine charged by the

government which can be described under various parts of the section such

as XI Application of ACL as commonwealth law, IV Anti-competitive practice

etc. are the parts which provides the necessary informations regarding this

context.

However, in accordance with the division 26 of ITAA 1997 it describes

that there will be allowances were facilitated over such specific amounts and

some of them will never be deductible (26 (5-100)).

Specific deductions by ITAA 97 25-45

ITAA 97 has many laws and rules that will facilitate the individual in

claiming the exemption or deductions over the income and expenditures

made by him. As per section 25-45 the laws has facilitated the deduction for

4

residential in Australia which can be described as several different

individuals who residence in Australia such as Migrants from this nation,

people come from different country for work and employment purpose,

students residents in Australia come from different nation for gaining the

education or enrolled in any college or university (Magnusson, 2014). It also

includes tourists who came in Australia for temporary visit or stay.

Measurements of Medicare levy

Medicare levy is a rebate that has been charged by the Australian

government over assessable income gain by the individuals which in context

with facilitating or providing the benefits health and care security to such

individuals (Apps, Long & Rees, 2014). It can be calculated by adding 2% of

the taxable earning by persons. If an individual has gain the insurance cover

from the medical unit of registered hospital of Australia than he will not be

liable add any surcharge over his income. Medicare levy can be assign to

those who are residents in Australia, non residents are not facilitated with it.

Commonwealth and legislations

As per the Competition and consumer act 2010 of ITAA 1997 has

facilitates many rules and regulation to deal with the case in which a

company is misleading or deducting cost of the fine charged by the

government which can be described under various parts of the section such

as XI Application of ACL as commonwealth law, IV Anti-competitive practice

etc. are the parts which provides the necessary informations regarding this

context.

However, in accordance with the division 26 of ITAA 1997 it describes

that there will be allowances were facilitated over such specific amounts and

some of them will never be deductible (26 (5-100)).

Specific deductions by ITAA 97 25-45

ITAA 97 has many laws and rules that will facilitate the individual in

claiming the exemption or deductions over the income and expenditures

made by him. As per section 25-45 the laws has facilitated the deduction for

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

losses occurred by theft or robbery to a person or a business (Hattingh, Low

& Forrester, 2013). This helps in exempting the amount that has occurred

the losses in assessment year by theft, deflation, stealing, embezzlement,

larceny and misappropriation etc. these all are the losses which can be

deductible under the these section.

Case law and the significance of high court

Deduction must be allowed as on repair and maintenance of newly

acquired or purchased building was discussed under the case of W Thomas &

Co Pty Ltd V. Federal Commission 1995. these can be go with rulings of

capital nature expenditures over maintenance and repair of the old building,

reconstructing the premises can be the issue as in section 25-10 of Income

tax assessment act 1997, renewal and repairing of the building which was

not in commercial use before acquisition (Mitchell & et. al., 2016).

Stock on hand and their valuation

Valuation of the closing inventory for the tax purpose can be made by

using cost pricing, market selling value or replacement method. Increase in

the value of inventory in hand results in higher assessable income whereas

decrease in the same is considered as an allowable deduction.

Valuation of the stock in hand must be calculated by the tax

practitioner by the three methods that are presented here as under:

Cost pricing method: The method consists of fixing the cots over the

product that will help to measure and bring the product to its recent position.

These consists of the prices or costs of various insurance, freight, delivery

charges , custom duties and the excise duties.

Market sales value method: value can be measured under this

method is that the market value or the selling price of product must meet

the priced planned by the managers and the taxes are to be paid by tax

payer on the gains he had due to selling of products (Hattingh, Low &

Forrester, 2013).

5

& Forrester, 2013). This helps in exempting the amount that has occurred

the losses in assessment year by theft, deflation, stealing, embezzlement,

larceny and misappropriation etc. these all are the losses which can be

deductible under the these section.

Case law and the significance of high court

Deduction must be allowed as on repair and maintenance of newly

acquired or purchased building was discussed under the case of W Thomas &

Co Pty Ltd V. Federal Commission 1995. these can be go with rulings of

capital nature expenditures over maintenance and repair of the old building,

reconstructing the premises can be the issue as in section 25-10 of Income

tax assessment act 1997, renewal and repairing of the building which was

not in commercial use before acquisition (Mitchell & et. al., 2016).

Stock on hand and their valuation

Valuation of the closing inventory for the tax purpose can be made by

using cost pricing, market selling value or replacement method. Increase in

the value of inventory in hand results in higher assessable income whereas

decrease in the same is considered as an allowable deduction.

Valuation of the stock in hand must be calculated by the tax

practitioner by the three methods that are presented here as under:

Cost pricing method: The method consists of fixing the cots over the

product that will help to measure and bring the product to its recent position.

These consists of the prices or costs of various insurance, freight, delivery

charges , custom duties and the excise duties.

Market sales value method: value can be measured under this

method is that the market value or the selling price of product must meet

the priced planned by the managers and the taxes are to be paid by tax

payer on the gains he had due to selling of products (Hattingh, Low &

Forrester, 2013).

5

Replacement value method: The replacement cost can be fixed on

the basis of identified product exist in market which will be on the last day of

income year, as it will help in measuring the cost of replacing the product.

Tax to be paid for $45000 earning

As per the acts of ATO including ITAA 97 and ITAA 36 the legislation

authorities has fixed the taxation slab for the individuals who made earnings

and their applicable percentage of taxation (James, Wallschutzky &

Alley,2013). Here the income is $45000 which comes under the slab of

37000 to 80000 which has the taxation rate of 32.5% and additional 3572 as

per the ruling which describes that any single dollar more than the 37000

than the taxpayer has to made payment for 3572 in addition.

PAYG collections

The taxes must be paid by tax practitioner on the basis of the earnings

he made on the regular basis (Magnusson, 2014). Thus it say pay as you go

which means the earning of the individual cam ne deposited in the accounts

and the government do not need to go for paper work over implying the

taxation on earnings it can easily be done by deducting directly through their

accounts.

PART B

As per the case study, during the given financial year, Ram has paid

his tax agent with a fee of $1,000 to complete his income tax return for tax

filling. Along with this, he also paid $2,000 to his legal solicitor in order to

create an objection draft to an ATO assessment that is received by him

before two years and paid $50,000 as income tax.

Referring the Income Tax Assessment Act, section D10 on “Cost of

managing Tax affairs” includes preparation and lodgement tax return, obtain

tax advice from the adviser, appeal to the Tribunals or courts and obtaining a

valuation. It clearly states all the tax deductions that are being available to

the party with regards to managing his or her tax affairs. Fees paid to the

6

the basis of identified product exist in market which will be on the last day of

income year, as it will help in measuring the cost of replacing the product.

Tax to be paid for $45000 earning

As per the acts of ATO including ITAA 97 and ITAA 36 the legislation

authorities has fixed the taxation slab for the individuals who made earnings

and their applicable percentage of taxation (James, Wallschutzky &

Alley,2013). Here the income is $45000 which comes under the slab of

37000 to 80000 which has the taxation rate of 32.5% and additional 3572 as

per the ruling which describes that any single dollar more than the 37000

than the taxpayer has to made payment for 3572 in addition.

PAYG collections

The taxes must be paid by tax practitioner on the basis of the earnings

he made on the regular basis (Magnusson, 2014). Thus it say pay as you go

which means the earning of the individual cam ne deposited in the accounts

and the government do not need to go for paper work over implying the

taxation on earnings it can easily be done by deducting directly through their

accounts.

PART B

As per the case study, during the given financial year, Ram has paid

his tax agent with a fee of $1,000 to complete his income tax return for tax

filling. Along with this, he also paid $2,000 to his legal solicitor in order to

create an objection draft to an ATO assessment that is received by him

before two years and paid $50,000 as income tax.

Referring the Income Tax Assessment Act, section D10 on “Cost of

managing Tax affairs” includes preparation and lodgement tax return, obtain

tax advice from the adviser, appeal to the Tribunals or courts and obtaining a

valuation. It clearly states all the tax deductions that are being available to

the party with regards to managing his or her tax affairs. Fees paid to the

6

recognized tax adviser is tax deductible in the year, in which, it is actually

incurred. For such deduction, it is the main requirement that tax adviser

must be registered includes solicitor, tax agent and barrister. However, if he

or she is not a recognized adviser, then such amount is not deductible (D10

Cost of managing tax affairs, 2015).

D10 has several sub components includes cost of managing tax affaris,

deductible ATO interest charge and cost of litigation (Deduction item D10 to

be split, 2017). According to the section, an individual can claim for the

deduction on interest payment with regards to late payment of tax &

penalties, amount by which tax liability is increased as a result of several

amendments. However, on the other side, tax shortfall & penalties charged

on the taxpayer due to late payment or falling meeting out tax obligations

timely cannot be claimed.

Referring to the section, it is clearly stated that if an assessee pays

fees to a tax advisor, interest charge and any other expenditures in order to

comply with the legal obligations then, he or she can obtain tax deductions

from his assessable income for the expenses paid (The Top 5 Forgotten Tax

Deductions, 2015). Applying it to the provided case, it seems clear that Ram

can get tax deductions for the fees that he had paid to their tax advisor so as

to file his income taxation return to the ATO. Thus, for the tax purpose, it will

be considered as a deductible expense.

Besides this, as per ITAA, an individual can claim for the tax deductions

for the fees that he or she had paid to the solicitor (Tran-Nam, Evans &

Lignier, 2014). In the available case, Ram had contacted a legal solicitor for

preparing an objection draft, on which, he can claim tax deductions for the

solicitor fees worth $2000 and reduce his taxable income.

Income tax refers to the taxation liabilities levied by the taxation

authority on the amount of taxable income as per the taxation rate. As per

progressive structure of Australian income tax, person who earns higher

level of income is charged at high rate or vice-versa (Porter, Allen &

Thompson, 2014). Moreover, it follows equality principle, as per which,

7

incurred. For such deduction, it is the main requirement that tax adviser

must be registered includes solicitor, tax agent and barrister. However, if he

or she is not a recognized adviser, then such amount is not deductible (D10

Cost of managing tax affairs, 2015).

D10 has several sub components includes cost of managing tax affaris,

deductible ATO interest charge and cost of litigation (Deduction item D10 to

be split, 2017). According to the section, an individual can claim for the

deduction on interest payment with regards to late payment of tax &

penalties, amount by which tax liability is increased as a result of several

amendments. However, on the other side, tax shortfall & penalties charged

on the taxpayer due to late payment or falling meeting out tax obligations

timely cannot be claimed.

Referring to the section, it is clearly stated that if an assessee pays

fees to a tax advisor, interest charge and any other expenditures in order to

comply with the legal obligations then, he or she can obtain tax deductions

from his assessable income for the expenses paid (The Top 5 Forgotten Tax

Deductions, 2015). Applying it to the provided case, it seems clear that Ram

can get tax deductions for the fees that he had paid to their tax advisor so as

to file his income taxation return to the ATO. Thus, for the tax purpose, it will

be considered as a deductible expense.

Besides this, as per ITAA, an individual can claim for the tax deductions

for the fees that he or she had paid to the solicitor (Tran-Nam, Evans &

Lignier, 2014). In the available case, Ram had contacted a legal solicitor for

preparing an objection draft, on which, he can claim tax deductions for the

solicitor fees worth $2000 and reduce his taxable income.

Income tax refers to the taxation liabilities levied by the taxation

authority on the amount of taxable income as per the taxation rate. As per

progressive structure of Australian income tax, person who earns higher

level of income is charged at high rate or vice-versa (Porter, Allen &

Thompson, 2014). Moreover, it follows equality principle, as per which,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

people whose income falls under the same slab is levied at the same rate of

tax. Tax deductions are available from the assessable income and on the

rest, tax is charged as per the applied tax rate. Here, Ram has paid income

tax liability worth $50,000, on which, no deductions is available (Mitchell and

et.al., 2016).

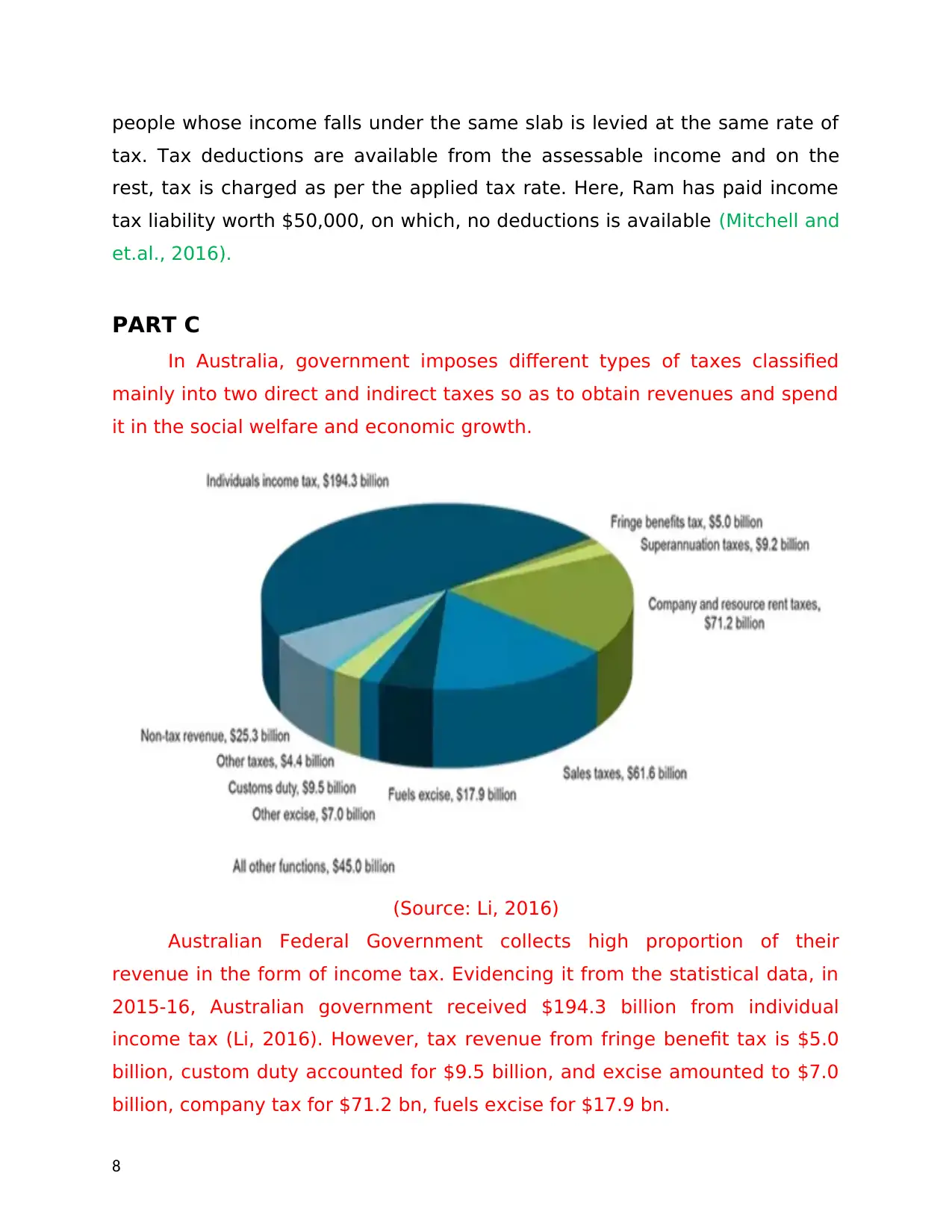

PART C

In Australia, government imposes different types of taxes classified

mainly into two direct and indirect taxes so as to obtain revenues and spend

it in the social welfare and economic growth.

(Source: Li, 2016)

Australian Federal Government collects high proportion of their

revenue in the form of income tax. Evidencing it from the statistical data, in

2015-16, Australian government received $194.3 billion from individual

income tax (Li, 2016). However, tax revenue from fringe benefit tax is $5.0

billion, custom duty accounted for $9.5 billion, and excise amounted to $7.0

billion, company tax for $71.2 bn, fuels excise for $17.9 bn.

8

tax. Tax deductions are available from the assessable income and on the

rest, tax is charged as per the applied tax rate. Here, Ram has paid income

tax liability worth $50,000, on which, no deductions is available (Mitchell and

et.al., 2016).

PART C

In Australia, government imposes different types of taxes classified

mainly into two direct and indirect taxes so as to obtain revenues and spend

it in the social welfare and economic growth.

(Source: Li, 2016)

Australian Federal Government collects high proportion of their

revenue in the form of income tax. Evidencing it from the statistical data, in

2015-16, Australian government received $194.3 billion from individual

income tax (Li, 2016). However, tax revenue from fringe benefit tax is $5.0

billion, custom duty accounted for $9.5 billion, and excise amounted to $7.0

billion, company tax for $71.2 bn, fuels excise for $17.9 bn.

8

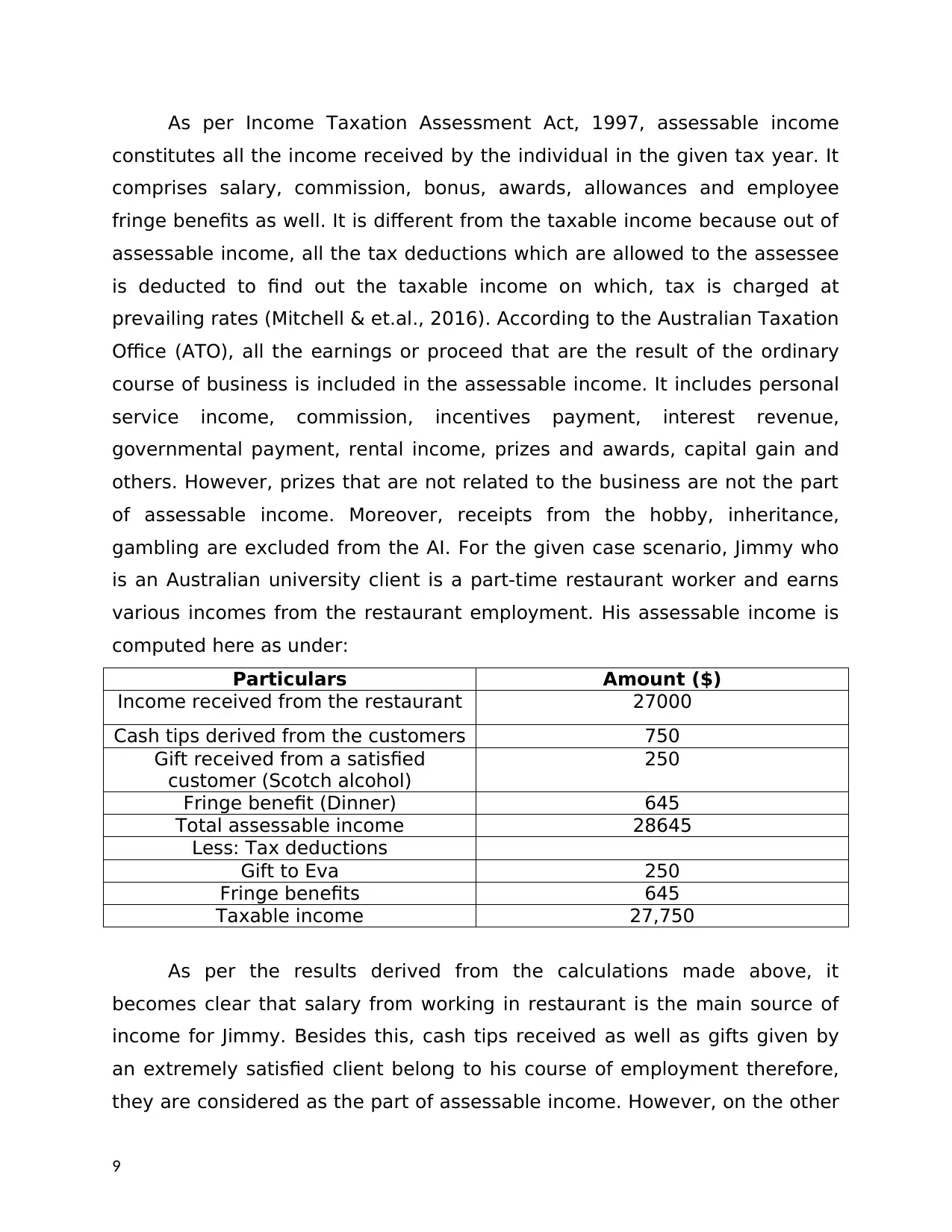

As per Income Taxation Assessment Act, 1997, assessable income

constitutes all the income received by the individual in the given tax year. It

comprises salary, commission, bonus, awards, allowances and employee

fringe benefits as well. It is different from the taxable income because out of

assessable income, all the tax deductions which are allowed to the assessee

is deducted to find out the taxable income on which, tax is charged at

prevailing rates (Mitchell & et.al., 2016). According to the Australian Taxation

Office (ATO), all the earnings or proceed that are the result of the ordinary

course of business is included in the assessable income. It includes personal

service income, commission, incentives payment, interest revenue,

governmental payment, rental income, prizes and awards, capital gain and

others. However, prizes that are not related to the business are not the part

of assessable income. Moreover, receipts from the hobby, inheritance,

gambling are excluded from the AI. For the given case scenario, Jimmy who

is an Australian university client is a part-time restaurant worker and earns

various incomes from the restaurant employment. His assessable income is

computed here as under:

Particulars Amount ($)

Income received from the restaurant 27000

Cash tips derived from the customers 750

Gift received from a satisfied

customer (Scotch alcohol)

250

Fringe benefit (Dinner) 645

Total assessable income 28645

Less: Tax deductions

Gift to Eva 250

Fringe benefits 645

Taxable income 27,750

As per the results derived from the calculations made above, it

becomes clear that salary from working in restaurant is the main source of

income for Jimmy. Besides this, cash tips received as well as gifts given by

an extremely satisfied client belong to his course of employment therefore,

they are considered as the part of assessable income. However, on the other

9

constitutes all the income received by the individual in the given tax year. It

comprises salary, commission, bonus, awards, allowances and employee

fringe benefits as well. It is different from the taxable income because out of

assessable income, all the tax deductions which are allowed to the assessee

is deducted to find out the taxable income on which, tax is charged at

prevailing rates (Mitchell & et.al., 2016). According to the Australian Taxation

Office (ATO), all the earnings or proceed that are the result of the ordinary

course of business is included in the assessable income. It includes personal

service income, commission, incentives payment, interest revenue,

governmental payment, rental income, prizes and awards, capital gain and

others. However, prizes that are not related to the business are not the part

of assessable income. Moreover, receipts from the hobby, inheritance,

gambling are excluded from the AI. For the given case scenario, Jimmy who

is an Australian university client is a part-time restaurant worker and earns

various incomes from the restaurant employment. His assessable income is

computed here as under:

Particulars Amount ($)

Income received from the restaurant 27000

Cash tips derived from the customers 750

Gift received from a satisfied

customer (Scotch alcohol)

250

Fringe benefit (Dinner) 645

Total assessable income 28645

Less: Tax deductions

Gift to Eva 250

Fringe benefits 645

Taxable income 27,750

As per the results derived from the calculations made above, it

becomes clear that salary from working in restaurant is the main source of

income for Jimmy. Besides this, cash tips received as well as gifts given by

an extremely satisfied client belong to his course of employment therefore,

they are considered as the part of assessable income. However, on the other

9

side, consider ITAA, gifts that are not related to the employment is excluded.

Applying the same rule to the givens scenario, gifts worth $15,000 received

from his parents is not added while calculating his assessable income

(Braverman, Marsden and Sadiq, 2015). However, dinner provided by the

employer at his expenditures is included, however, at the same time, on

fringe benefits tax deductions is also allowed, therefore, it is subtracted to

determine taxable income (Min & LV, 2017).

Australian Income Tax Act allows deductions on entertainment that

includes meal, drink, recreation and other expenses. It is exempted from the

fringe benefit tax if its value is below AUD 300. However, according to the

given situation, Jimmy had received an expensive bottle of Scotch alcohol

worth AUD250 from one of the satisfied customer. It is not treated as an

entertainment expense therefore, being a receiver; Jimmy would require

paying tax on the same. Thus, although, its value is below threshold, still, as

it is not an entertainment expense therefore would be taxed (Jims, 2015).

Here, as an alternative option, Jimmy can receive tax-deductible gift like

movie tickets, airline tickets, meal at restaurant and others, on such, no tax

is charged. Referring the same to the scenario, Jimmy gave gift to EVA on

which, tax deductions has been provided to him.

Jimmy’s employer has a policy to take all the workers on a dinner and

Jimmy eats total food worth AUD 645. As said, that AUD 300 is threshold

point for tax exemption which is exceeded therefore, minor benefit

exemption does not apply here and the entire amount will be taxed (FBT and

entertainment. n.d.). As an alternative, Jimmy can receive AUD300 and

AUD300 for associates like spouse because both have separate threshold

limit and save tax from the same. In the case law of Knnew V Commissioner

of Taxation, in which, food restaurant expenses were totalled to AUD679.86

beyond threshold, therefore taxed by the government.

As per the findings, Jimmy’s total assessable and taxable income has

been derived to $28,645 and $27,750 respectively.

10

Applying the same rule to the givens scenario, gifts worth $15,000 received

from his parents is not added while calculating his assessable income

(Braverman, Marsden and Sadiq, 2015). However, dinner provided by the

employer at his expenditures is included, however, at the same time, on

fringe benefits tax deductions is also allowed, therefore, it is subtracted to

determine taxable income (Min & LV, 2017).

Australian Income Tax Act allows deductions on entertainment that

includes meal, drink, recreation and other expenses. It is exempted from the

fringe benefit tax if its value is below AUD 300. However, according to the

given situation, Jimmy had received an expensive bottle of Scotch alcohol

worth AUD250 from one of the satisfied customer. It is not treated as an

entertainment expense therefore, being a receiver; Jimmy would require

paying tax on the same. Thus, although, its value is below threshold, still, as

it is not an entertainment expense therefore would be taxed (Jims, 2015).

Here, as an alternative option, Jimmy can receive tax-deductible gift like

movie tickets, airline tickets, meal at restaurant and others, on such, no tax

is charged. Referring the same to the scenario, Jimmy gave gift to EVA on

which, tax deductions has been provided to him.

Jimmy’s employer has a policy to take all the workers on a dinner and

Jimmy eats total food worth AUD 645. As said, that AUD 300 is threshold

point for tax exemption which is exceeded therefore, minor benefit

exemption does not apply here and the entire amount will be taxed (FBT and

entertainment. n.d.). As an alternative, Jimmy can receive AUD300 and

AUD300 for associates like spouse because both have separate threshold

limit and save tax from the same. In the case law of Knnew V Commissioner

of Taxation, in which, food restaurant expenses were totalled to AUD679.86

beyond threshold, therefore taxed by the government.

As per the findings, Jimmy’s total assessable and taxable income has

been derived to $28,645 and $27,750 respectively.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

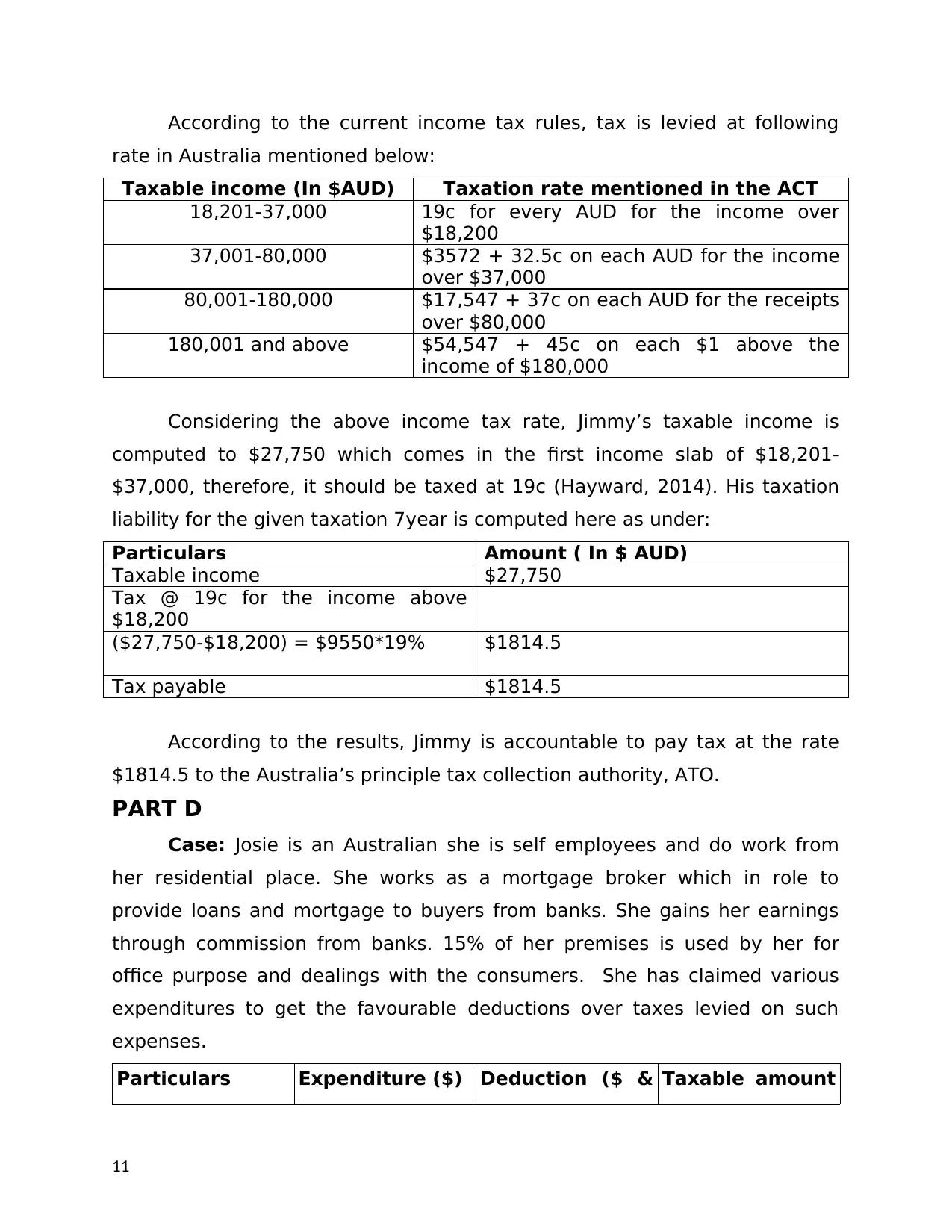

According to the current income tax rules, tax is levied at following

rate in Australia mentioned below:

Taxable income (In $AUD) Taxation rate mentioned in the ACT

18,201-37,000 19c for every AUD for the income over

$18,200

37,001-80,000 $3572 + 32.5c on each AUD for the income

over $37,000

80,001-180,000 $17,547 + 37c on each AUD for the receipts

over $80,000

180,001 and above $54,547 + 45c on each $1 above the

income of $180,000

Considering the above income tax rate, Jimmy’s taxable income is

computed to $27,750 which comes in the first income slab of $18,201-

$37,000, therefore, it should be taxed at 19c (Hayward, 2014). His taxation

liability for the given taxation 7year is computed here as under:

Particulars Amount ( In $ AUD)

Taxable income $27,750

Tax @ 19c for the income above

$18,200

($27,750-$18,200) = $9550*19% $1814.5

Tax payable $1814.5

According to the results, Jimmy is accountable to pay tax at the rate

$1814.5 to the Australia’s principle tax collection authority, ATO.

PART D

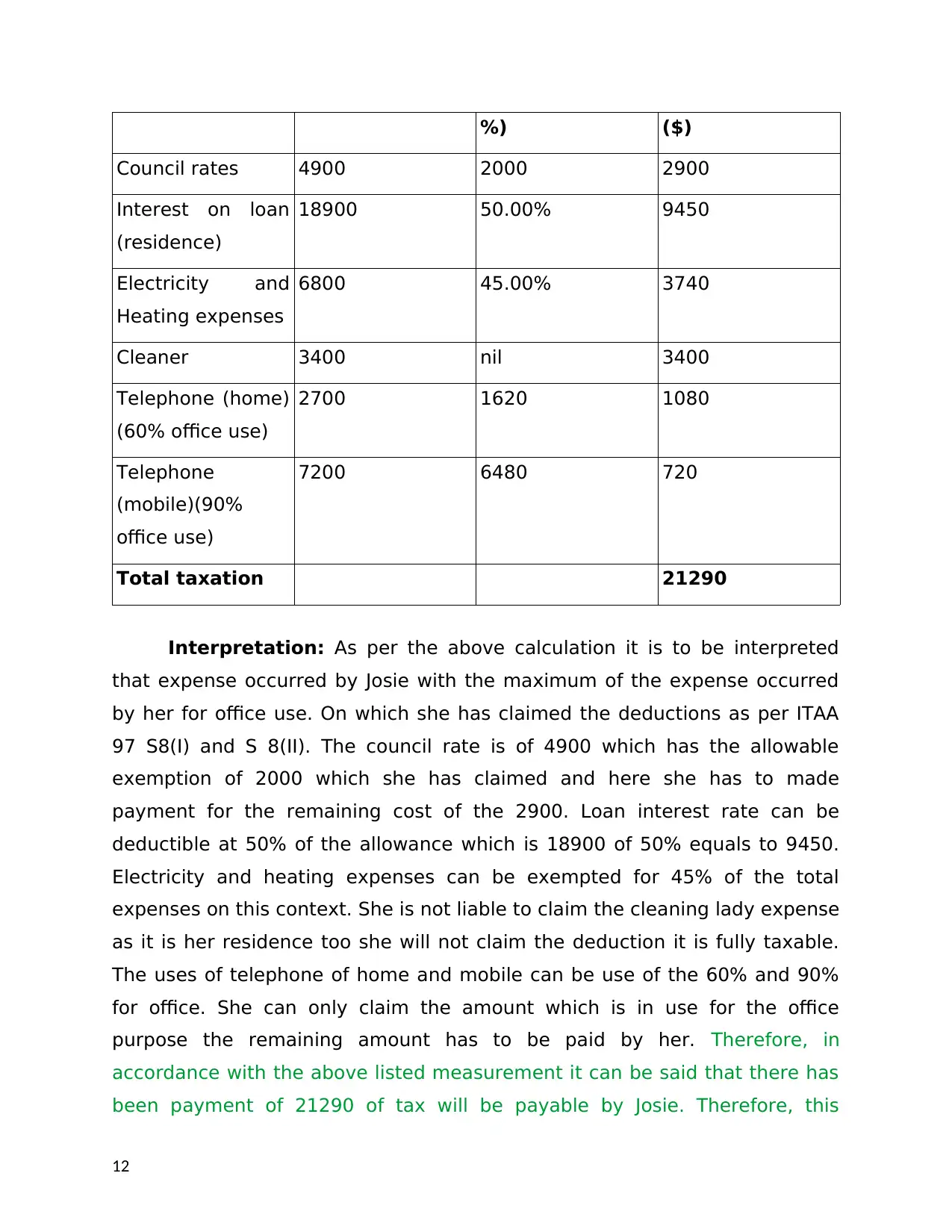

Case: Josie is an Australian she is self employees and do work from

her residential place. She works as a mortgage broker which in role to

provide loans and mortgage to buyers from banks. She gains her earnings

through commission from banks. 15% of her premises is used by her for

office purpose and dealings with the consumers. She has claimed various

expenditures to get the favourable deductions over taxes levied on such

expenses.

Particulars Expenditure ($) Deduction ($ & Taxable amount

11

rate in Australia mentioned below:

Taxable income (In $AUD) Taxation rate mentioned in the ACT

18,201-37,000 19c for every AUD for the income over

$18,200

37,001-80,000 $3572 + 32.5c on each AUD for the income

over $37,000

80,001-180,000 $17,547 + 37c on each AUD for the receipts

over $80,000

180,001 and above $54,547 + 45c on each $1 above the

income of $180,000

Considering the above income tax rate, Jimmy’s taxable income is

computed to $27,750 which comes in the first income slab of $18,201-

$37,000, therefore, it should be taxed at 19c (Hayward, 2014). His taxation

liability for the given taxation 7year is computed here as under:

Particulars Amount ( In $ AUD)

Taxable income $27,750

Tax @ 19c for the income above

$18,200

($27,750-$18,200) = $9550*19% $1814.5

Tax payable $1814.5

According to the results, Jimmy is accountable to pay tax at the rate

$1814.5 to the Australia’s principle tax collection authority, ATO.

PART D

Case: Josie is an Australian she is self employees and do work from

her residential place. She works as a mortgage broker which in role to

provide loans and mortgage to buyers from banks. She gains her earnings

through commission from banks. 15% of her premises is used by her for

office purpose and dealings with the consumers. She has claimed various

expenditures to get the favourable deductions over taxes levied on such

expenses.

Particulars Expenditure ($) Deduction ($ & Taxable amount

11

%) ($)

Council rates 4900 2000 2900

Interest on loan

(residence)

18900 50.00% 9450

Electricity and

Heating expenses

6800 45.00% 3740

Cleaner 3400 nil 3400

Telephone (home)

(60% office use)

2700 1620 1080

Telephone

(mobile)(90%

office use)

7200 6480 720

Total taxation 21290

Interpretation: As per the above calculation it is to be interpreted

that expense occurred by Josie with the maximum of the expense occurred

by her for office use. On which she has claimed the deductions as per ITAA

97 S8(I) and S 8(II). The council rate is of 4900 which has the allowable

exemption of 2000 which she has claimed and here she has to made

payment for the remaining cost of the 2900. Loan interest rate can be

deductible at 50% of the allowance which is 18900 of 50% equals to 9450.

Electricity and heating expenses can be exempted for 45% of the total

expenses on this context. She is not liable to claim the cleaning lady expense

as it is her residence too she will not claim the deduction it is fully taxable.

The uses of telephone of home and mobile can be use of the 60% and 90%

for office. She can only claim the amount which is in use for the office

purpose the remaining amount has to be paid by her. Therefore, in

accordance with the above listed measurement it can be said that there has

been payment of 21290 of tax will be payable by Josie. Therefore, this

12

Council rates 4900 2000 2900

Interest on loan

(residence)

18900 50.00% 9450

Electricity and

Heating expenses

6800 45.00% 3740

Cleaner 3400 nil 3400

Telephone (home)

(60% office use)

2700 1620 1080

Telephone

(mobile)(90%

office use)

7200 6480 720

Total taxation 21290

Interpretation: As per the above calculation it is to be interpreted

that expense occurred by Josie with the maximum of the expense occurred

by her for office use. On which she has claimed the deductions as per ITAA

97 S8(I) and S 8(II). The council rate is of 4900 which has the allowable

exemption of 2000 which she has claimed and here she has to made

payment for the remaining cost of the 2900. Loan interest rate can be

deductible at 50% of the allowance which is 18900 of 50% equals to 9450.

Electricity and heating expenses can be exempted for 45% of the total

expenses on this context. She is not liable to claim the cleaning lady expense

as it is her residence too she will not claim the deduction it is fully taxable.

The uses of telephone of home and mobile can be use of the 60% and 90%

for office. She can only claim the amount which is in use for the office

purpose the remaining amount has to be paid by her. Therefore, in

accordance with the above listed measurement it can be said that there has

been payment of 21290 of tax will be payable by Josie. Therefore, this

12

amount has been analysed as per the revenue gained by her over the

employment and commission. There has been various deductions allowed to

her and she has been profitable with low amount of taxes will be payable

from her.

13

employment and commission. There has been various deductions allowed to

her and she has been profitable with low amount of taxes will be payable

from her.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Apps, P., Long, N., & Rees, R. (2014). Optimal piecewise linear income taxation. Journal of

Public Economic Theory. 16(4). PP.523-545.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer

Response to Legislative Changes: A Case Study of In-House Fringe

Benefits Rules. J. Austl. Tax'n. 17. 1.

Hattingh, L., Low, J. S., & Forrester, K. (2013). Australian pharmacy law and practice. Elsevier

Health Sciences.

Hayward, R. (Ed.). (2014). Valuation: principles into practice. Taylor & Francis.

James, S., Wallschutzky, I., & Alley, C. (2013). The Henry Report and the taxation of work

related expenses: Principles versus practice.

Min, S. H. E. N., & LV, L. Q. (2017). English-Chinese Translation for Tax Vocabularies in

Business English. DEStech Transactions on Social Science, Education and Human

Science, (meit).

Mitchell, R. & et.al., (2016). Law, corporate governance and partnerships at work: a study of

australian regulatory style and business practice. Routledge.

Porter, D., Allen, B., & Thompson, G. (2014). Development in Practice (Routledge Revivals):

Paved with Good Intentions. Routledge.

Tran-Nam, B., Evans, C., & Lignier, P. (2014). Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F.. 29. 137.

Online

D10 Cost of managing tax affairs. (2015). [Online]. Available through: <

https://www.ato.gov.au/Individuals/Tax-return/2015/Tax-return/Deductio

n-questions-D1-D10/D10-Cost-of-managing-tax-affairs/>.

14

Books and Journals

Apps, P., Long, N., & Rees, R. (2014). Optimal piecewise linear income taxation. Journal of

Public Economic Theory. 16(4). PP.523-545.

Braverman, D., Marsden, S., & Sadiq, K. (2015). Assessing Taxpayer

Response to Legislative Changes: A Case Study of In-House Fringe

Benefits Rules. J. Austl. Tax'n. 17. 1.

Hattingh, L., Low, J. S., & Forrester, K. (2013). Australian pharmacy law and practice. Elsevier

Health Sciences.

Hayward, R. (Ed.). (2014). Valuation: principles into practice. Taylor & Francis.

James, S., Wallschutzky, I., & Alley, C. (2013). The Henry Report and the taxation of work

related expenses: Principles versus practice.

Min, S. H. E. N., & LV, L. Q. (2017). English-Chinese Translation for Tax Vocabularies in

Business English. DEStech Transactions on Social Science, Education and Human

Science, (meit).

Mitchell, R. & et.al., (2016). Law, corporate governance and partnerships at work: a study of

australian regulatory style and business practice. Routledge.

Porter, D., Allen, B., & Thompson, G. (2014). Development in Practice (Routledge Revivals):

Paved with Good Intentions. Routledge.

Tran-Nam, B., Evans, C., & Lignier, P. (2014). Personal taxpayer compliance costs: Recent

evidence from Australia. Austl. Tax F.. 29. 137.

Online

D10 Cost of managing tax affairs. (2015). [Online]. Available through: <

https://www.ato.gov.au/Individuals/Tax-return/2015/Tax-return/Deductio

n-questions-D1-D10/D10-Cost-of-managing-tax-affairs/>.

14

Deduction item D10 to be split. (2017). [Online]. Available through: <

http://taxandsupernewsroom.com.au/deduction-item-d10-cost-

managing-tax-affairs-split/>.

FBT and entertainment. (2017) [Online]. Available through: <

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/In-detail/FBT-

and-entertainment-for-small-business/?anchor=H7#H7>.

Jims, (2015). Gifts to employees, Associates and third parties. [Online].

Available through: < http://www.jimsbookkeeping.com.au/gifts-to-

employees-associates/>.

Li, J. (2016). Why are Australia’s taxes high, and what do they cover?

[Online]. Available through: https://www.quora.com/Why-are-

Australias-taxes-high-and-what-do-they-cover. [Accessed on 13th

September 2017].

The Top 5 Forgotten Tax Deductions. (2015). [Online]. Available through: <

https://www.etax.com.au/5-forgotten-tax-deductions/>. [Accessed on

13th September 2017].

15

http://taxandsupernewsroom.com.au/deduction-item-d10-cost-

managing-tax-affairs-split/>.

FBT and entertainment. (2017) [Online]. Available through: <

https://www.ato.gov.au/General/Fringe-benefits-tax-(FBT)/In-detail/FBT-

and-entertainment-for-small-business/?anchor=H7#H7>.

Jims, (2015). Gifts to employees, Associates and third parties. [Online].

Available through: < http://www.jimsbookkeeping.com.au/gifts-to-

employees-associates/>.

Li, J. (2016). Why are Australia’s taxes high, and what do they cover?

[Online]. Available through: https://www.quora.com/Why-are-

Australias-taxes-high-and-what-do-they-cover. [Accessed on 13th

September 2017].

The Top 5 Forgotten Tax Deductions. (2015). [Online]. Available through: <

https://www.etax.com.au/5-forgotten-tax-deductions/>. [Accessed on

13th September 2017].

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.