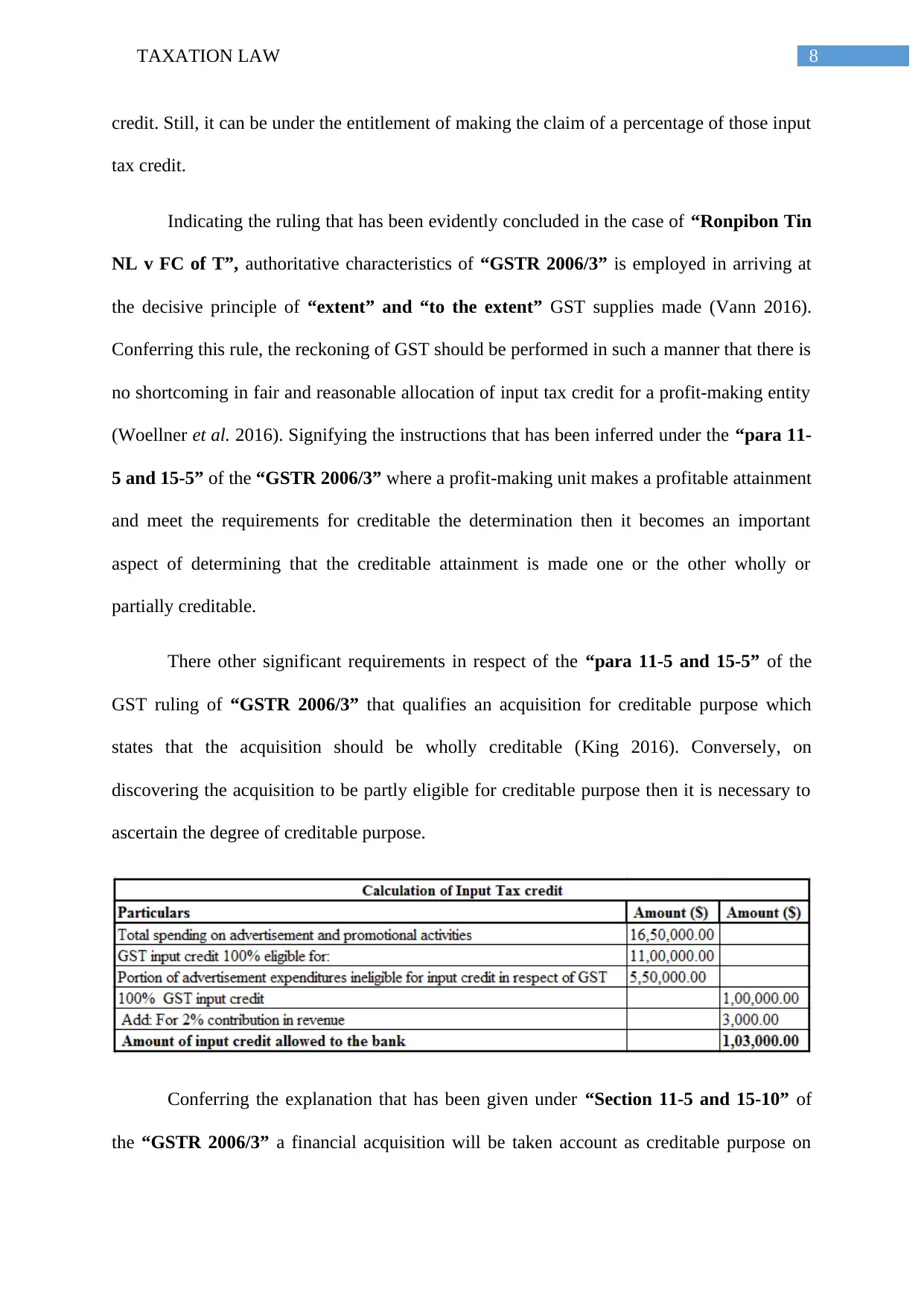

The service spread over more than fifty branches across the country. Big Bank bought forward the programme of insurance and home content in the market besides providing the facilities of loans and deposits to the customers. The ‘Taxation Ruling of GSTR 2006/3’ lays down the rules that are related to the process of calculating the input tax credit in respect of the above-stated ruling. The analysis performed can be bought forward by stating that the business supplies made in the present study accompany the creditable supplies. On performing a thorough analysis of the case study of Big Bank Ltd, the bank has outdone the inception boundary of the fiscal attainment. As a result, it can be bought forward that Big Bank Ltd will be able to claim input tax credit for the summation of GST supplies made.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)