Taxation Law Application - Assignment

VerifiedAdded on 2021/06/14

|10

|1592

|107

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................4

Conclusion:................................................................................................................................6

Reference List:...........................................................................................................................7

Table of Contents

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................4

Conclusion:................................................................................................................................6

Reference List:...........................................................................................................................7

2TAXATION LAW

Headings:

The present issue would be taking into the consideration the computation of the tax

for Kate during the year ended 2017/18.

Issue:

Will the taxpayer be entitled to claim an allowable deductions relating to the

travelling under section “section 8-1 of the ITAA 1997”? Is the taxpayer held assessable for

the income derived during the year under “section 6-5 of the ITAA 1997”?

Rule:

According to “section 6-1 of the ITAA 1997” income from personal exertion refers to

the income derived from the salaries, wages fees or business proceeds. The taxation

commissioner in “Scott v Commissioner of Taxation (1935)” stated that appropriate

principles must be implemented in treating the receipts as ordinary income (Miller and Oats

2016).

As stated under “section 20 of the FBTAA 1986” any expenditure fringe benefit arises

when the employer pays the expenses for employee (Barkoczy 2016). Ordinary awards are

not regarded as income given a satisfactory relation is prevalent between the activities of

taxpayer. Referring to “Kelly v FCT” award received by footballer for being the best player

was regarded taxable since it was related to his employment.

Winning from prizes is held assessable when the prize holds sufficient association

with the income producing actions of an individual taxpayer. The court of law in “FCT v

Stone” held that police women derived assessable income from her salary and also won prize

money from sporting involvement (Bankman et al. 2017). The court held that the police

Headings:

The present issue would be taking into the consideration the computation of the tax

for Kate during the year ended 2017/18.

Issue:

Will the taxpayer be entitled to claim an allowable deductions relating to the

travelling under section “section 8-1 of the ITAA 1997”? Is the taxpayer held assessable for

the income derived during the year under “section 6-5 of the ITAA 1997”?

Rule:

According to “section 6-1 of the ITAA 1997” income from personal exertion refers to

the income derived from the salaries, wages fees or business proceeds. The taxation

commissioner in “Scott v Commissioner of Taxation (1935)” stated that appropriate

principles must be implemented in treating the receipts as ordinary income (Miller and Oats

2016).

As stated under “section 20 of the FBTAA 1986” any expenditure fringe benefit arises

when the employer pays the expenses for employee (Barkoczy 2016). Ordinary awards are

not regarded as income given a satisfactory relation is prevalent between the activities of

taxpayer. Referring to “Kelly v FCT” award received by footballer for being the best player

was regarded taxable since it was related to his employment.

Winning from prizes is held assessable when the prize holds sufficient association

with the income producing actions of an individual taxpayer. The court of law in “FCT v

Stone” held that police women derived assessable income from her salary and also won prize

money from sporting involvement (Bankman et al. 2017). The court held that the police

3TAXATION LAW

women was performing the business activities of professional athlete and the amount derived

would be taxable under “section 6-5 of the ITAA 1997”.

Amount received for public appearance or endorsement is regarded assessable if there

is an appropriate link with the taxpayer earnings activities. Evidently in “Kelly v FCT” the

amount received from public appearance and endorsement was considered as assessable

income.

As defined in “subsection 108-10 (1) of the ITAA 1997” to work out the capital gain

capital losses sustained from collectible should be employed to reduce the capital gains from

collectibles (McDaniel 2017). According to “section 108-15 (1)” collectible are disposed in

set. As stated in “section 108-15 (2) of the ITAA 1997”, collectibles are viewed as single set

of asset and any capital gains from the collectibles that are acquired for less than $500 should

be disregarded by the taxpayer.

The court of law in “Adelaide Fruit and Produce Exchange Co Ltd (1932)” held that

rent represents periodical receipts and should be considered as taxable income. Reward for

services are generally considered as the assessable income (Murphy and Higgins 2016). The

court of law in “Brent v FCT” held that amount received by the wife of train robber for

narrating the story of life is taxable income under ordinary concepts.

Payment received for relinquishing rights is not taxable income but constitutes CGT

event D1. Under “Section 8-1 of the ITAA 1997” a taxpayer is allowed to claim deductions

for legal expenditure when it is related to income producing activity (Schmalbeck, Zelenak

and Lawsky 2015). As held in “FCT v Rowe (1995)” it is vital consider the nature of legal

expenditure for being held as deductible. Expenses that are incidental costs to capital

proceeds are held as allowable deductions.

women was performing the business activities of professional athlete and the amount derived

would be taxable under “section 6-5 of the ITAA 1997”.

Amount received for public appearance or endorsement is regarded assessable if there

is an appropriate link with the taxpayer earnings activities. Evidently in “Kelly v FCT” the

amount received from public appearance and endorsement was considered as assessable

income.

As defined in “subsection 108-10 (1) of the ITAA 1997” to work out the capital gain

capital losses sustained from collectible should be employed to reduce the capital gains from

collectibles (McDaniel 2017). According to “section 108-15 (1)” collectible are disposed in

set. As stated in “section 108-15 (2) of the ITAA 1997”, collectibles are viewed as single set

of asset and any capital gains from the collectibles that are acquired for less than $500 should

be disregarded by the taxpayer.

The court of law in “Adelaide Fruit and Produce Exchange Co Ltd (1932)” held that

rent represents periodical receipts and should be considered as taxable income. Reward for

services are generally considered as the assessable income (Murphy and Higgins 2016). The

court of law in “Brent v FCT” held that amount received by the wife of train robber for

narrating the story of life is taxable income under ordinary concepts.

Payment received for relinquishing rights is not taxable income but constitutes CGT

event D1. Under “Section 8-1 of the ITAA 1997” a taxpayer is allowed to claim deductions

for legal expenditure when it is related to income producing activity (Schmalbeck, Zelenak

and Lawsky 2015). As held in “FCT v Rowe (1995)” it is vital consider the nature of legal

expenditure for being held as deductible. Expenses that are incidental costs to capital

proceeds are held as allowable deductions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

An individual is only allowed to claim deductions for expenses that meet the criteria

stated in positive limbs of “section 8-1 of the ITAA 1997”. In the event of “FCT v

Madealena (1971)” expenses occurred in obtaining a new job is non-allowable deduction

because it is not in the course of gaining assessable income (Burke 2016).

Application:

The receipt of salary by Kate is held as income from personal exertion. Citing the

reference of “Scott v Commissioner of Taxation (1935)” receipts of salary is held as ordinary

income which would be considered for taxation under “section 6-5 of the ITAA 1997” (Hora

2014). While the payment of taxi fares by employer is fringe benefit under “section 20 of the

FBTAA 1986” because it was in respect of her employment.

A cash award of $5,000 was received by kate for being the best account. Referring to

“Kelly v FCT” award received by Kate for being the best account is taxable since it was

related to her employment (Kiprotich 2016). Kate often participated in high-jumping

competition and wins numerous prizes. Referring to “FCT v Stone” the amount derived by

Kate would be taxable under “section 6-5 of the ITAA 1997” because she was carrying the

business of professional athlete and coffee machine that was received would be classified as

gift as it lacked income character.

Referring to “Kelly v FCT” the amount of $40,000 that was received by Kate for

public appearance in sporting event was considered as assessable income. It was noticed that

the bed side lamp was purchased for $700 but sold for loss at $500 and under “section 108-

10 (2)” should disregard the capital loss from the collectibles (Jones and Rhoades-Catanach

2013). Additionally the capital gains made from selling the other lamp should be disregarded

under “section 108-15 (2) of the ITAA 1997” since it was acquired for less than $500. Citing

An individual is only allowed to claim deductions for expenses that meet the criteria

stated in positive limbs of “section 8-1 of the ITAA 1997”. In the event of “FCT v

Madealena (1971)” expenses occurred in obtaining a new job is non-allowable deduction

because it is not in the course of gaining assessable income (Burke 2016).

Application:

The receipt of salary by Kate is held as income from personal exertion. Citing the

reference of “Scott v Commissioner of Taxation (1935)” receipts of salary is held as ordinary

income which would be considered for taxation under “section 6-5 of the ITAA 1997” (Hora

2014). While the payment of taxi fares by employer is fringe benefit under “section 20 of the

FBTAA 1986” because it was in respect of her employment.

A cash award of $5,000 was received by kate for being the best account. Referring to

“Kelly v FCT” award received by Kate for being the best account is taxable since it was

related to her employment (Kiprotich 2016). Kate often participated in high-jumping

competition and wins numerous prizes. Referring to “FCT v Stone” the amount derived by

Kate would be taxable under “section 6-5 of the ITAA 1997” because she was carrying the

business of professional athlete and coffee machine that was received would be classified as

gift as it lacked income character.

Referring to “Kelly v FCT” the amount of $40,000 that was received by Kate for

public appearance in sporting event was considered as assessable income. It was noticed that

the bed side lamp was purchased for $700 but sold for loss at $500 and under “section 108-

10 (2)” should disregard the capital loss from the collectibles (Jones and Rhoades-Catanach

2013). Additionally the capital gains made from selling the other lamp should be disregarded

under “section 108-15 (2) of the ITAA 1997” since it was acquired for less than $500. Citing

5TAXATION LAW

the reference of “Adelaide Fruit and Produce Exchange Co Ltd (1932)” receipt of rent from

property was periodical receipts and be taxable under “section 6-5 of the ITAA 1997”.

Kate received $30,000 for speaking about her life after sports. Referring to “Brent v

FCT” these amounts are regarded as reward for service which is taxable as ordinary income

“section 6-5 of the ITAA 1997”.

An additional payment of $20,000 was received by for relinquishing the right of

appearing in similar TV interview. Therefore these amounts is held as CGT event D1 which

would be included her assessable (Hart et al. 2017). Citing the reference of “FCT v Rowe

(1995)” the legal expenses of $5,000 that incurred by Kate is an incidental costs to capital

proceeds and held as allowable deductions.

Kate regularly looks for new employment and incurs travelling and accommodation to

a new job interview. Referring to “FCT v Madealena (1971)” expenses occurred by Kate in

obtaining a new job is non-allowable deduction because it is not in the course of gaining her

assessable income (Rohatgi 2015).

the reference of “Adelaide Fruit and Produce Exchange Co Ltd (1932)” receipt of rent from

property was periodical receipts and be taxable under “section 6-5 of the ITAA 1997”.

Kate received $30,000 for speaking about her life after sports. Referring to “Brent v

FCT” these amounts are regarded as reward for service which is taxable as ordinary income

“section 6-5 of the ITAA 1997”.

An additional payment of $20,000 was received by for relinquishing the right of

appearing in similar TV interview. Therefore these amounts is held as CGT event D1 which

would be included her assessable (Hart et al. 2017). Citing the reference of “FCT v Rowe

(1995)” the legal expenses of $5,000 that incurred by Kate is an incidental costs to capital

proceeds and held as allowable deductions.

Kate regularly looks for new employment and incurs travelling and accommodation to

a new job interview. Referring to “FCT v Madealena (1971)” expenses occurred by Kate in

obtaining a new job is non-allowable deduction because it is not in the course of gaining her

assessable income (Rohatgi 2015).

6TAXATION LAW

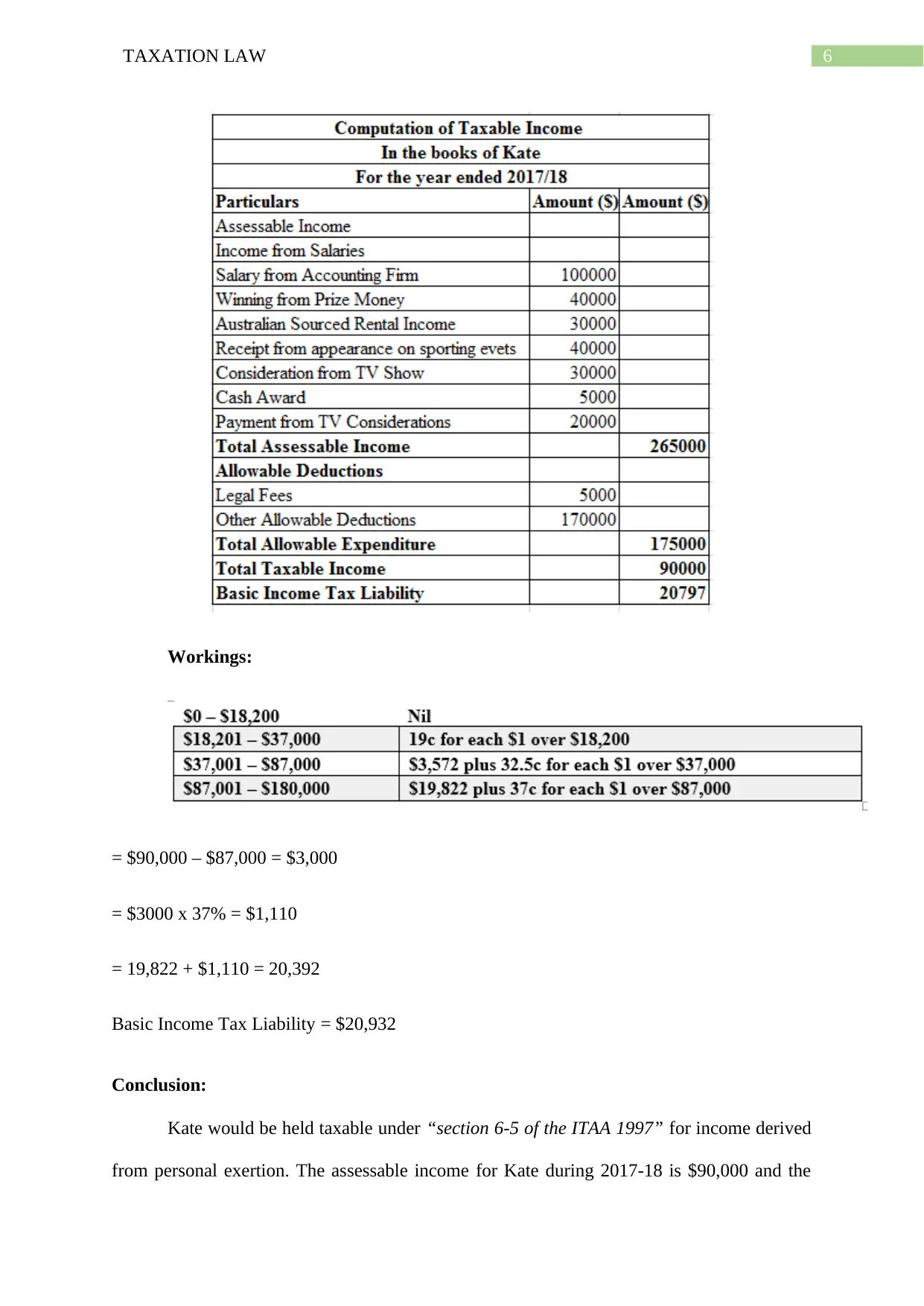

Workings:

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Basic Income Tax Liability = $20,932

Conclusion:

Kate would be held taxable under “section 6-5 of the ITAA 1997” for income derived

from personal exertion. The assessable income for Kate during 2017-18 is $90,000 and the

Workings:

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Basic Income Tax Liability = $20,932

Conclusion:

Kate would be held taxable under “section 6-5 of the ITAA 1997” for income derived

from personal exertion. The assessable income for Kate during 2017-18 is $90,000 and the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

basic tax liability stands $20,797. Kate can allowable deduction for rental property and other

allowable expenses under “section 8-1 of the ITAA 1997”.

basic tax liability stands $20,797. Kate can allowable deduction for rental property and other

allowable expenses under “section 8-1 of the ITAA 1997”.

8TAXATION LAW

Reference List:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Burke, K., 2016. Federal income taxation of partners and partnerships in a nutshell. West

Academic.

Hart, G., Coleman, C., Jogarajan, S., Sadiq, K., McLaren, J. and Krever, R., 2017. Principles

of taxation law.

Hora, B., 2014. Principles of Taxation. Issues in Accounting Education, 19(1), p.150.

Jones, S. and Rhoades-Catanach, S., 2013. Principles of Taxation for Business and

Investment Planning, 2014 edition. McGraw-Hill Higher Education.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

McDaniel, P., 2017. Federal Income Taxation. Foundation Press.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Rohatgi, R., 2015. Basic international taxation. Richmond Law & Tax.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Reference List:

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Burke, K., 2016. Federal income taxation of partners and partnerships in a nutshell. West

Academic.

Hart, G., Coleman, C., Jogarajan, S., Sadiq, K., McLaren, J. and Krever, R., 2017. Principles

of taxation law.

Hora, B., 2014. Principles of Taxation. Issues in Accounting Education, 19(1), p.150.

Jones, S. and Rhoades-Catanach, S., 2013. Principles of Taxation for Business and

Investment Planning, 2014 edition. McGraw-Hill Higher Education.

Kiprotich, B.A., 2016. Principles of Taxation. governance.

McDaniel, P., 2017. Federal Income Taxation. Foundation Press.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Rohatgi, R., 2015. Basic international taxation. Richmond Law & Tax.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

9TAXATION LAW

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.