Taxation Law: Fringe Benefits, Income Tax, and Barter System

VerifiedAdded on 2020/05/28

|10

|1887

|77

Report

AI Summary

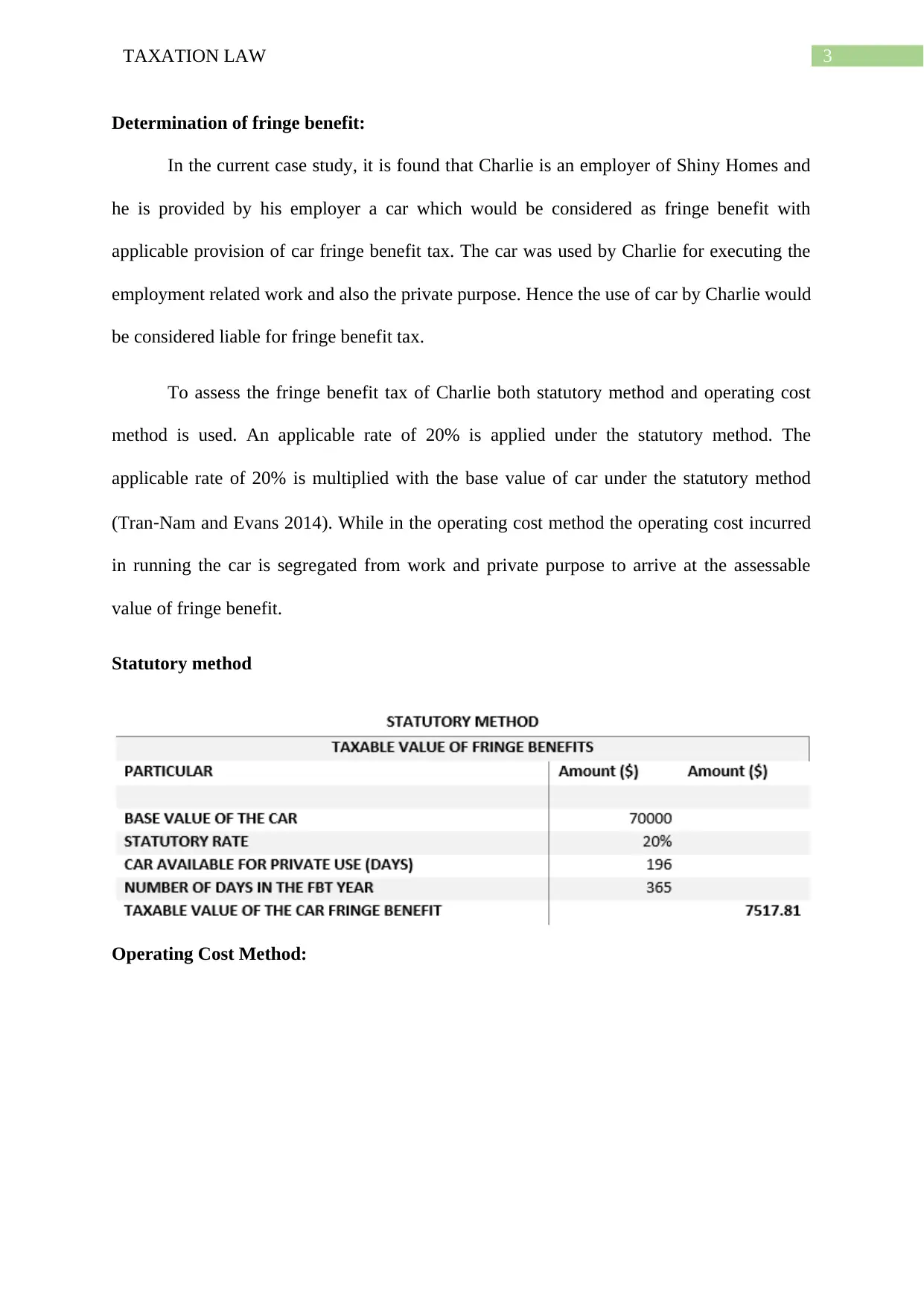

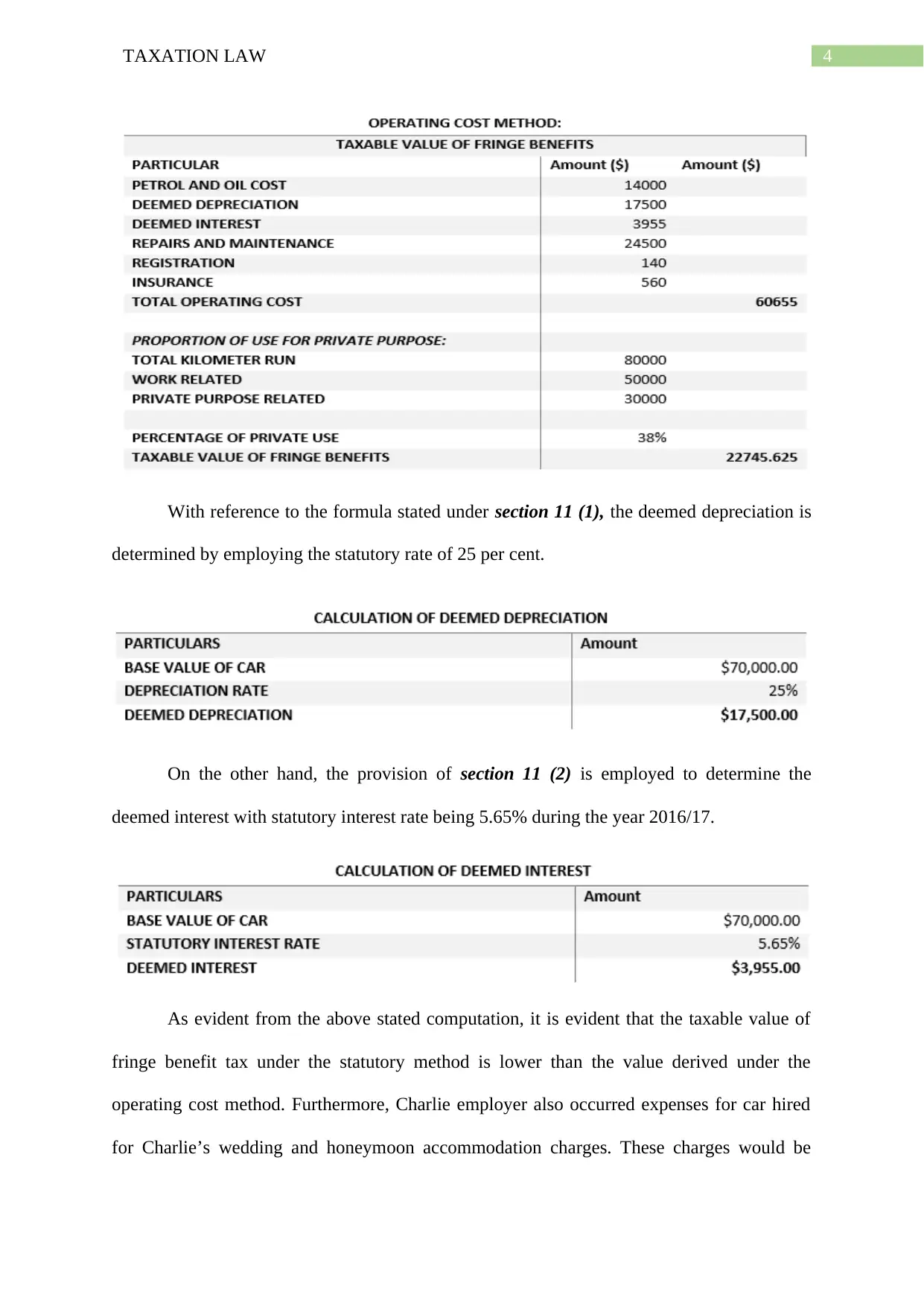

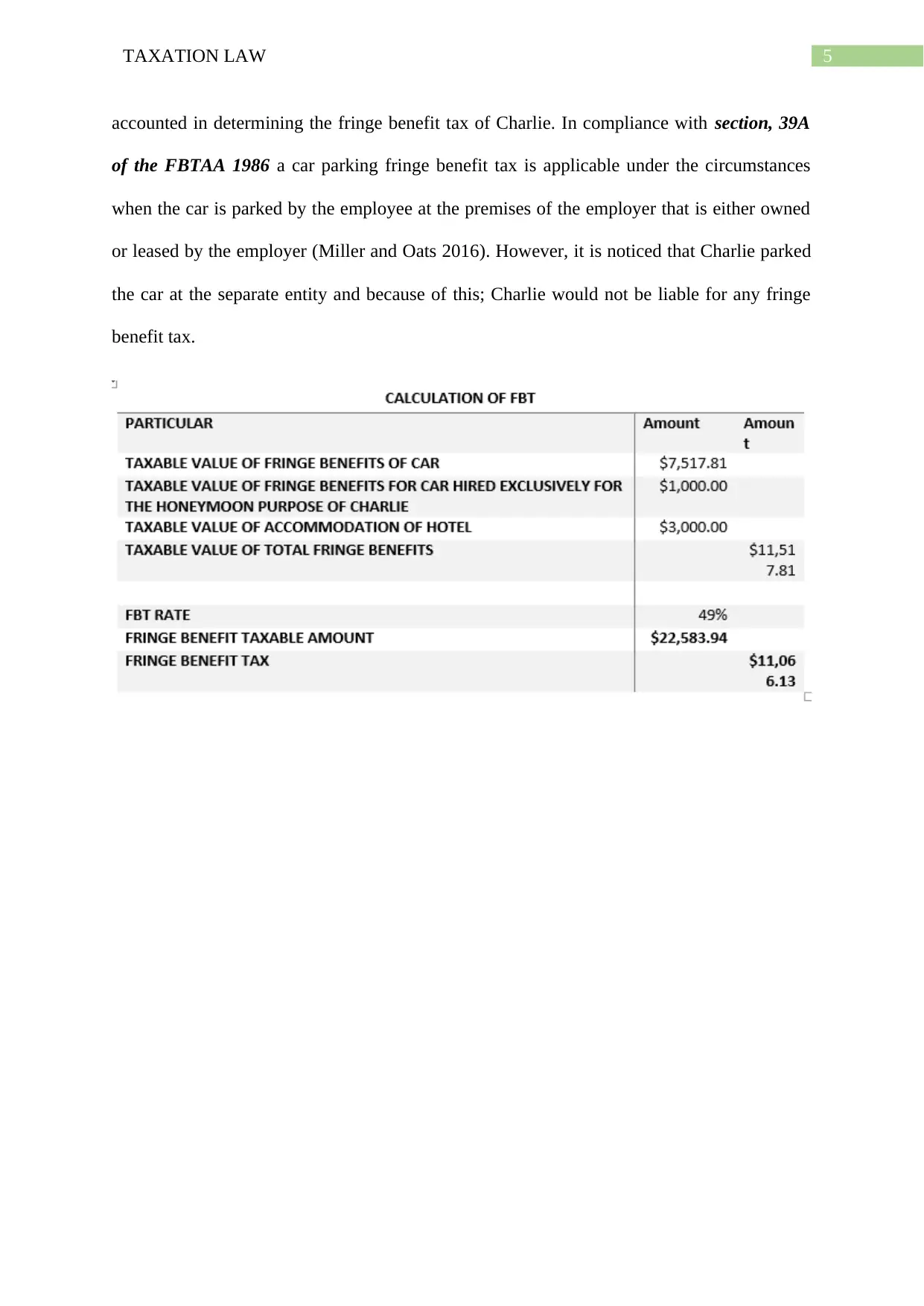

This report comprehensively analyzes various aspects of taxation law, focusing on fringe benefits tax (FBT) and income tax principles within the Australian context. Part A delves into the determination of fringe benefits, specifically car fringe benefits, outlining both the statutory and operating cost methods for calculating taxable amounts. It applies these methods to a case study involving an employee's car usage, considering both work and private purposes, and discusses the implications of car parking fringe benefits. Part B shifts focus to income tax, examining the assessable income of individuals, including income from business and professions, the treatment of gifts, and the application of the 'hobby versus business' distinction. It further explores the tax implications of primary production activities and the tax and GST consequences of barter transactions, referencing relevant legislation and case law, such as the Income Tax Assessment Act 1997 and various taxation rulings and court decisions, to support its arguments and provide practical examples. The report offers a detailed analysis of these complex areas of taxation law, providing students with a clear understanding of the relevant principles and their application in real-world scenarios.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.