Taxation Law .

VerifiedAdded on 2023/05/29

|8

|1820

|500

AI Summary

This text provides answers to questions related to Australian taxation law, including residency status, income tax on gifts and prizes, and deductions for business loans. The text also includes computations for net income and taxable income. References to relevant cases and legislation are provided throughout.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to A:..........................................................................................................................4

Answer to B:..........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to 4.1.........................................................................................................................5

Answer to 4.2:........................................................................................................................6

References:.................................................................................................................................7

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to A:..........................................................................................................................4

Answer to B:..........................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to 4.1.........................................................................................................................5

Answer to 4.2:........................................................................................................................6

References:.................................................................................................................................7

2TAXATION LAW

Answer to question 1:

As per the definition given under “section 995-1 of the ITAA 1997” occupant or

Australian dweller denotes individual that has their home in Australia, except for the tax

officer is satisfied that the individual has their eternal place of house out of Australia

(Woellner et al., 2016). “Section 6(1), ITAA 1936” explains that an individual is said to be

an Australian resident if the person has been present in Australia on continuous basis or

sporadically for more than six months of the income year except the tax officer is content that

he or she has their usual residence out of Australia and hardly has any purpose of taking up

the Australian occupancy.

The case study highlights that Amity left Australia in 2015 to live in Kiribati for a

period of two years and then take up the decision of whether to stay longer given the lifestyle

suits her. The residential status of Amity has been considered in the below listed residency

status.

Resides Test: The resides test denotes dwelling enduringly or for a substantial period. The

court in “FC of T v Miller (1946)” stated that the residency status of an individual is

dependent on the question of “fact and extent” (Pinto, 2013). The intention of the taxpayer or

the purpose of presence along with the household or occupation ties forms necessary in

establishing the domiciliary position of a person.

Domicile Test: As per the “Domicile Act 1982” a person is regarded as the Australian

occupant if he or she has their domicile in Australian except the tax official is satisfied that

the person has their everlasting place of abode out of Australia (Robin, 2017). A person

obtains the domicile of origin by birth or by the operation of law where the taxpayer intends

to take their home indefinitely. As held “FC of T v Applegate (1979)” the high court

considered whether the permanent place of abode is out of Australia. The decision held by the

Answer to question 1:

As per the definition given under “section 995-1 of the ITAA 1997” occupant or

Australian dweller denotes individual that has their home in Australia, except for the tax

officer is satisfied that the individual has their eternal place of house out of Australia

(Woellner et al., 2016). “Section 6(1), ITAA 1936” explains that an individual is said to be

an Australian resident if the person has been present in Australia on continuous basis or

sporadically for more than six months of the income year except the tax officer is content that

he or she has their usual residence out of Australia and hardly has any purpose of taking up

the Australian occupancy.

The case study highlights that Amity left Australia in 2015 to live in Kiribati for a

period of two years and then take up the decision of whether to stay longer given the lifestyle

suits her. The residential status of Amity has been considered in the below listed residency

status.

Resides Test: The resides test denotes dwelling enduringly or for a substantial period. The

court in “FC of T v Miller (1946)” stated that the residency status of an individual is

dependent on the question of “fact and extent” (Pinto, 2013). The intention of the taxpayer or

the purpose of presence along with the household or occupation ties forms necessary in

establishing the domiciliary position of a person.

Domicile Test: As per the “Domicile Act 1982” a person is regarded as the Australian

occupant if he or she has their domicile in Australian except the tax official is satisfied that

the person has their everlasting place of abode out of Australia (Robin, 2017). A person

obtains the domicile of origin by birth or by the operation of law where the taxpayer intends

to take their home indefinitely. As held “FC of T v Applegate (1979)” the high court

considered whether the permanent place of abode is out of Australia. The decision held by the

3TAXATION LAW

court stated that the permanent do not mean eternal and it is judged respectively year. The

taxpayer was having the permanent place of dwelling out of Australia and ultimately returned

when he was ill.

183-day Test: Under the 183 days test a person is the Australian occupant if they had been

present in Australia, uninterruptedly or sporadically for six months or more during the

income year in Australian given the person has the normal dwelling out of Australia with no

intention of residing in Australia.

In the current case, Amity went to Kiribati for two years and also had the choices of

extending the contract for three years. She maintained her social and living arrangements in

Kiribati as her salary was paid into the Asia-Pacific bank. Though she intended to stay long

but returned ultimately after her husband fell ill. Referring to “Applegate v FC of T (1979)”

the actual intent of Amity was to reside outside Australia for two years’ period and also

thought of extending her stay for given the lifestyle suits her. The social and living

arrangements made by Amity reflected her intention of residing out of Australian without

having any certain intent returning Australia.

On a conclusive note, Amity cannot be held as resident of Australian under “section

6(1) of the ITAA 1936” since she did not meet the requirement of Domicile Test and also

failed to meet the requirement of 183 days Test.

Answer to question 2:

Answer to A:

Mere gift is not considered as income. The court in “Hayes v FCT” stated that the

receipts from shares by the company boss was not held as income. Evidently in “Scott v

FCT” the solicitor received 10,000 pounds of gift from the wife of client which was not

treated as income (Blakelock & King, 2017). The employee dentist here received a computer

court stated that the permanent do not mean eternal and it is judged respectively year. The

taxpayer was having the permanent place of dwelling out of Australia and ultimately returned

when he was ill.

183-day Test: Under the 183 days test a person is the Australian occupant if they had been

present in Australia, uninterruptedly or sporadically for six months or more during the

income year in Australian given the person has the normal dwelling out of Australia with no

intention of residing in Australia.

In the current case, Amity went to Kiribati for two years and also had the choices of

extending the contract for three years. She maintained her social and living arrangements in

Kiribati as her salary was paid into the Asia-Pacific bank. Though she intended to stay long

but returned ultimately after her husband fell ill. Referring to “Applegate v FC of T (1979)”

the actual intent of Amity was to reside outside Australia for two years’ period and also

thought of extending her stay for given the lifestyle suits her. The social and living

arrangements made by Amity reflected her intention of residing out of Australian without

having any certain intent returning Australia.

On a conclusive note, Amity cannot be held as resident of Australian under “section

6(1) of the ITAA 1936” since she did not meet the requirement of Domicile Test and also

failed to meet the requirement of 183 days Test.

Answer to question 2:

Answer to A:

Mere gift is not considered as income. The court in “Hayes v FCT” stated that the

receipts from shares by the company boss was not held as income. Evidently in “Scott v

FCT” the solicitor received 10,000 pounds of gift from the wife of client which was not

treated as income (Blakelock & King, 2017). The employee dentist here received a computer

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

game of $600 and hence the receipt did not constitute ordinary income under ordinary

concepts of “section 6-5 of the ITAA 1997”.

Answer to B:

According to ATO a taxpayer winning from any prize or lottery that is run by bank

should be treated as ordinary income that attracts tax liability. This includes cash, interest free

loans and cars. In “Kelly v FCT” the taxpayer was awarded for being the fairest player. The

amount is taxable because it was incidental to his employment (Burton, 2017). Similarly, in

“FCT v Stone” the taxpayer was assessed for receiving prize money for carrying on the

business of professional athlete. Therefore, receiving car as the prize from bank is an ordinary

income under “section 6-5 of the ITAA 1997”.

Answer to question 3:

Answer to A:

“Section 8-1, ITA Act 1997”, allows a person to deduction from their taxable income

for any outgoings till the extent they are occurred in generating assessable income. ATO

states that a person taking loan to use it for personal and business purpose then the taxpayer

can apportion the interest on loan (Miller & Oats, 2016). In such circumstances the interest

on loan must be divided under deductible and non-deductible segments. Betty and Barney can

claim deduction under “section 8-1, ITA Act 1997” for interest on loan up to the amount of

loan that is used for business purpose while the private portion of loan interest is excluded

from deduction.

Answer to B:

“Section 8-1 of ITAA 1997” allows taxpayer to claim deduction for outgoings given

that it is found in business operations which was previously carried on by the taxpayer for

generating taxable earnings (Fleurbaey & Maniquet, 2018). In “FCT v Brown 1999 ATC”

game of $600 and hence the receipt did not constitute ordinary income under ordinary

concepts of “section 6-5 of the ITAA 1997”.

Answer to B:

According to ATO a taxpayer winning from any prize or lottery that is run by bank

should be treated as ordinary income that attracts tax liability. This includes cash, interest free

loans and cars. In “Kelly v FCT” the taxpayer was awarded for being the fairest player. The

amount is taxable because it was incidental to his employment (Burton, 2017). Similarly, in

“FCT v Stone” the taxpayer was assessed for receiving prize money for carrying on the

business of professional athlete. Therefore, receiving car as the prize from bank is an ordinary

income under “section 6-5 of the ITAA 1997”.

Answer to question 3:

Answer to A:

“Section 8-1, ITA Act 1997”, allows a person to deduction from their taxable income

for any outgoings till the extent they are occurred in generating assessable income. ATO

states that a person taking loan to use it for personal and business purpose then the taxpayer

can apportion the interest on loan (Miller & Oats, 2016). In such circumstances the interest

on loan must be divided under deductible and non-deductible segments. Betty and Barney can

claim deduction under “section 8-1, ITA Act 1997” for interest on loan up to the amount of

loan that is used for business purpose while the private portion of loan interest is excluded

from deduction.

Answer to B:

“Section 8-1 of ITAA 1997” allows taxpayer to claim deduction for outgoings given

that it is found in business operations which was previously carried on by the taxpayer for

generating taxable earnings (Fleurbaey & Maniquet, 2018). In “FCT v Brown 1999 ATC”

5TAXATION LAW

the taxation commissioner allowed deduction for interest on loan since the loan was entered

into by the taxpayer to conduct the business activities and for generating income.

i. A deduction under “section 8-1 of the ITAA 1997” will be permitted to Robert for

loan interest when the business was under continuous mode.

ii. Robert would also be permitted to claim deduction under “section 8-1 of the

ITAA 1997” when the business operation was ceased since the loan was entered

into by the taxpayer to conduct the business activities and for generating income.

Answer to question 4:

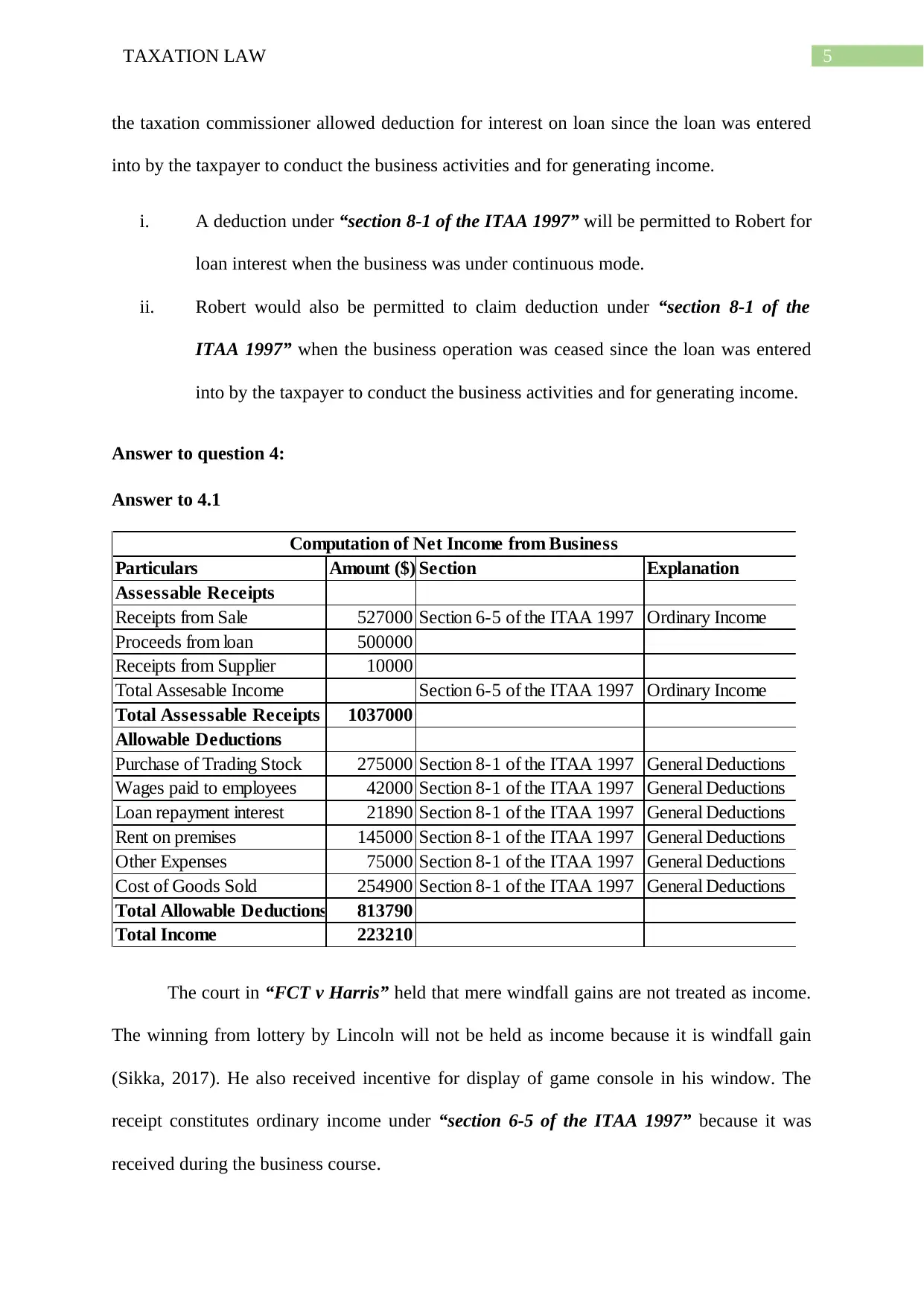

Answer to 4.1

Particulars Amount ($) Section Explanation

Assessable Receipts

Receipts from Sale 527000 Section 6-5 of the ITAA 1997 Ordinary Income

Proceeds from loan 500000

Receipts from Supplier 10000

Total Assesable Income Section 6-5 of the ITAA 1997 Ordinary Income

Total Assessable Receipts 1037000

Allowable Deductions

Purchase of Trading Stock 275000 Section 8-1 of the ITAA 1997 General Deductions

Wages paid to employees 42000 Section 8-1 of the ITAA 1997 General Deductions

Loan repayment interest 21890 Section 8-1 of the ITAA 1997 General Deductions

Rent on premises 145000 Section 8-1 of the ITAA 1997 General Deductions

Other Expenses 75000 Section 8-1 of the ITAA 1997 General Deductions

Cost of Goods Sold 254900 Section 8-1 of the ITAA 1997 General Deductions

Total Allowable Deductions 813790

Total Income 223210

Computation of Net Income from Business

The court in “FCT v Harris” held that mere windfall gains are not treated as income.

The winning from lottery by Lincoln will not be held as income because it is windfall gain

(Sikka, 2017). He also received incentive for display of game console in his window. The

receipt constitutes ordinary income under “section 6-5 of the ITAA 1997” because it was

received during the business course.

the taxation commissioner allowed deduction for interest on loan since the loan was entered

into by the taxpayer to conduct the business activities and for generating income.

i. A deduction under “section 8-1 of the ITAA 1997” will be permitted to Robert for

loan interest when the business was under continuous mode.

ii. Robert would also be permitted to claim deduction under “section 8-1 of the

ITAA 1997” when the business operation was ceased since the loan was entered

into by the taxpayer to conduct the business activities and for generating income.

Answer to question 4:

Answer to 4.1

Particulars Amount ($) Section Explanation

Assessable Receipts

Receipts from Sale 527000 Section 6-5 of the ITAA 1997 Ordinary Income

Proceeds from loan 500000

Receipts from Supplier 10000

Total Assesable Income Section 6-5 of the ITAA 1997 Ordinary Income

Total Assessable Receipts 1037000

Allowable Deductions

Purchase of Trading Stock 275000 Section 8-1 of the ITAA 1997 General Deductions

Wages paid to employees 42000 Section 8-1 of the ITAA 1997 General Deductions

Loan repayment interest 21890 Section 8-1 of the ITAA 1997 General Deductions

Rent on premises 145000 Section 8-1 of the ITAA 1997 General Deductions

Other Expenses 75000 Section 8-1 of the ITAA 1997 General Deductions

Cost of Goods Sold 254900 Section 8-1 of the ITAA 1997 General Deductions

Total Allowable Deductions 813790

Total Income 223210

Computation of Net Income from Business

The court in “FCT v Harris” held that mere windfall gains are not treated as income.

The winning from lottery by Lincoln will not be held as income because it is windfall gain

(Sikka, 2017). He also received incentive for display of game console in his window. The

receipt constitutes ordinary income under “section 6-5 of the ITAA 1997” because it was

received during the business course.

6TAXATION LAW

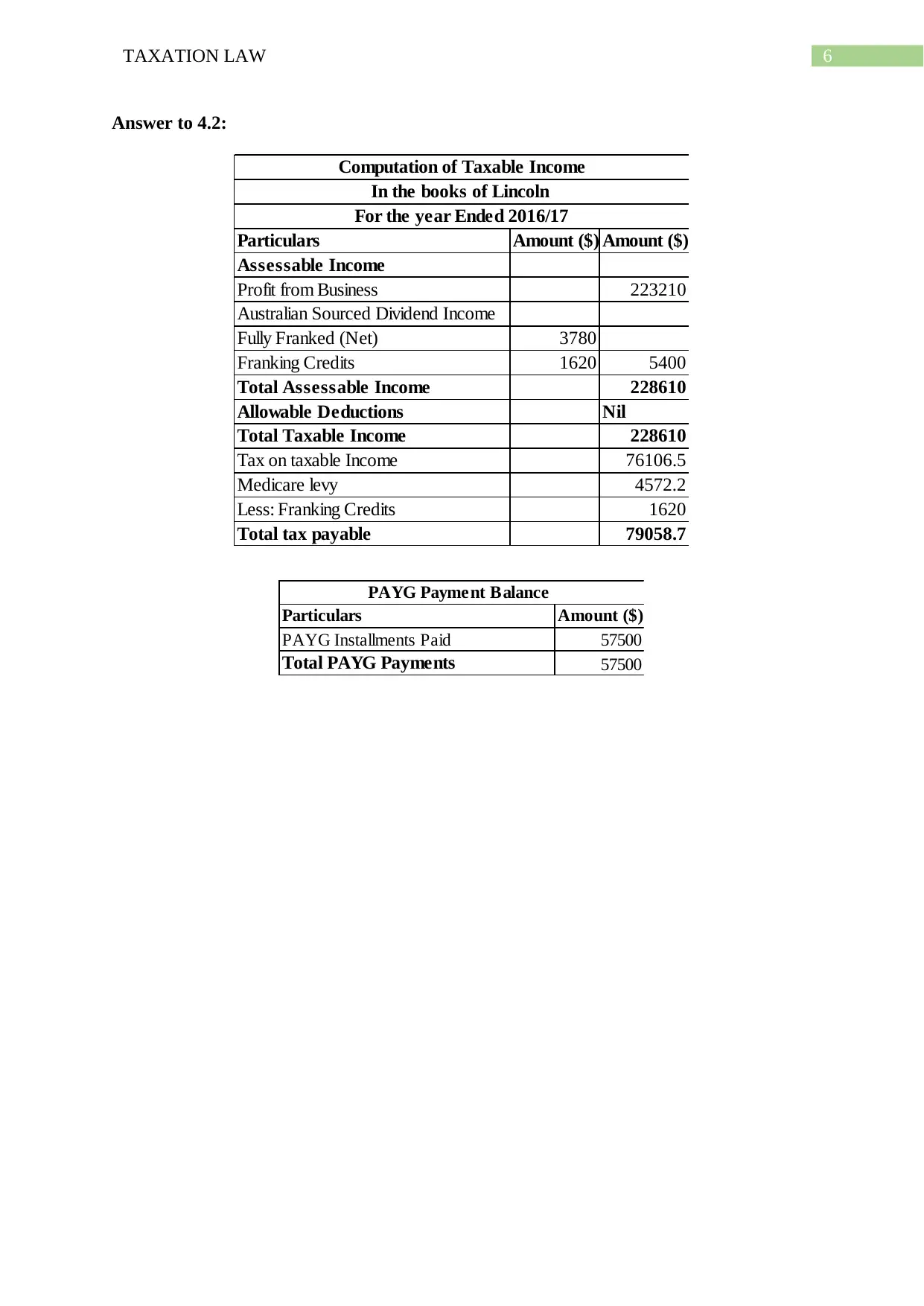

Answer to 4.2:

Particulars Amount ($) Amount ($)

Assessable Income

Profit from Business 223210

Australian Sourced Dividend Income

Fully Franked (Net) 3780

Franking Credits 1620 5400

Total Assessable Income 228610

Allowable Deductions Nil

Total Taxable Income 228610

Tax on taxable Income 76106.5

Medicare levy 4572.2

Less: Franking Credits 1620

Total tax payable 79058.7

Computation of Taxable Income

In the books of Lincoln

For the year Ended 2016/17

Particulars Amount ($)

PAYG Installments Paid 57500

Total PAYG Payments 57500

PAYG Payment Balance

Answer to 4.2:

Particulars Amount ($) Amount ($)

Assessable Income

Profit from Business 223210

Australian Sourced Dividend Income

Fully Franked (Net) 3780

Franking Credits 1620 5400

Total Assessable Income 228610

Allowable Deductions Nil

Total Taxable Income 228610

Tax on taxable Income 76106.5

Medicare levy 4572.2

Less: Franking Credits 1620

Total tax payable 79058.7

Computation of Taxable Income

In the books of Lincoln

For the year Ended 2016/17

Particulars Amount ($)

PAYG Installments Paid 57500

Total PAYG Payments 57500

PAYG Payment Balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

References:

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Pinto, D. (2013). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Robin, H. (2017). Australian taxation law 2017. Oxford University Press.

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

References:

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Pinto, D. (2013). State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Robin, H. (2017). Australian taxation law 2017. Oxford University Press.

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.