HI6028 Taxation Law Assignment: Partnership and Fringe Benefits

VerifiedAdded on 2023/04/25

|12

|2624

|156

Homework Assignment

AI Summary

This assignment solution addresses two key areas of taxation law: partnership taxation and fringe benefits tax. The first part analyzes a case study involving Daniel and Olivia Smith's mixed business, "Brekkie and Lunch and OZ Bottle Shop," determining their net income from the partnership. It applies relevant sections of the ITAA 1936, including sections 6-5, 8-1, 25-10, and 91, to calculate taxable income, allowable deductions (such as car expenses, electricity bills, and repairs), and the impact of various business transactions. The second part examines fringe benefits tax (FBT), focusing on whether payments made by an employer on behalf of an employee constitute a fringe benefit under the FBTAA 1986. It specifically looks at the FBT implications of an employer paying school fees for an employee's child and providing accommodation to an employee, calculating the taxable value of the housing fringe benefit. The solution provides detailed calculations, references to relevant legislation, and conclusions on the tax liabilities of the parties involved.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to question 2:.................................................................................................................7

References:...............................................................................................................................10

2TAXATION LAW

Answer to Question 1:

According to the “division 5 of the ITAA 1936” this case study is determining the net

income from a partnership.

Rule:

According to “section 91, ITAA 1936” a partnership should incur and record the

amount of profit gained by the objectives of partners and this determines the actual taxable

incomes for the partners. Similarly, “section 91, ITAA 1936” this section highlights as per

the rules of general law the partnership need not pay the tax separately (Dong 2018). In terms

of profit the partners needs to calculate their taxable income and they have pay the tax as the

profit earned. Hence the allowable deductions are omitted while calculating the taxable

income.

Under “section 6-5, ITAA 1997” the income gained from the profit of a business is

called as the ordinary income. According to the court under “Scott v CT (1935)” income is

not recognized as the word of art but this is known as proportion of entities used for meeting

the benefits of public along with highest profit throughout the business life cycle (Mares and

Queralt 2015). Hence, according to “section 6-5, ITAA 1997” the incomes and profit gained

from the business objectives are called as the ordinary income. Now the categorization of the

ordinary income must include the receipts forms that are used while gaining the business

objectives or profits.

According to the “section 8-1” the importance of paying tax over gaining profit from

the partnership is that the objective should not only satisfy the basic needs of public but also

this should be following the rules of “section 8-1”. The positive part of the “section 8-1 (1),

ITAA 1997” states that the taxpayer is allowed to get all the deduction if they have made the

expenses for the profit making with respect to their business objective and also this must be

Answer to Question 1:

According to the “division 5 of the ITAA 1936” this case study is determining the net

income from a partnership.

Rule:

According to “section 91, ITAA 1936” a partnership should incur and record the

amount of profit gained by the objectives of partners and this determines the actual taxable

incomes for the partners. Similarly, “section 91, ITAA 1936” this section highlights as per

the rules of general law the partnership need not pay the tax separately (Dong 2018). In terms

of profit the partners needs to calculate their taxable income and they have pay the tax as the

profit earned. Hence the allowable deductions are omitted while calculating the taxable

income.

Under “section 6-5, ITAA 1997” the income gained from the profit of a business is

called as the ordinary income. According to the court under “Scott v CT (1935)” income is

not recognized as the word of art but this is known as proportion of entities used for meeting

the benefits of public along with highest profit throughout the business life cycle (Mares and

Queralt 2015). Hence, according to “section 6-5, ITAA 1997” the incomes and profit gained

from the business objectives are called as the ordinary income. Now the categorization of the

ordinary income must include the receipts forms that are used while gaining the business

objectives or profits.

According to the “section 8-1” the importance of paying tax over gaining profit from

the partnership is that the objective should not only satisfy the basic needs of public but also

this should be following the rules of “section 8-1”. The positive part of the “section 8-1 (1),

ITAA 1997” states that the taxpayer is allowed to get all the deduction if they have made the

expenses for the profit making with respect to their business objective and also this must be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

for gaining the taxable income throughout the business (Berliant and Gouveia 2018).

Consequently if the taxable income is following the negative limbs of the “section 8-1 (1),

ITAA 1997” if the expenses are considered as capital, domestic or private then the taxpayers

are not allowed for the deductions in their taxable incomes.

According to “section 25-10, ITAA 1997” a taxpayer is allowed to claim the

expenditure that happened for the repair in depreciating assets and also for the properties

which may lead to the increment of profit in partnership (Calabrese, Epple and Romano

2018). Under “section 25-10” any kind of maintenance work is known as repairs as painting

of business premises, repair of current business entities that may lead profit increment.

Consequently, the expense involved into this repairs and replacements includes deductions to

the taxable income for the taxpayers as they are incurring these changes for gaining more

taxable income. However, this is very important to be noted that the good or entities those

which are replaced should be same as the worn out entity but this should give more effective

results in terms of production or gaining profit. This aspect is included in order to highlight

the improvement of the business functionalities.

The taxpayer can be allowed instant $20,000 write- off if they have invested this

amount or less than it in their entity repairs and relevant expenses. Hence they will get a

deduction in their taxable income for these kinds of repairs.

Application:

Rendering to the “division 5, ITAA 1936” Daniel and Olivia ha incurred several

business activities those incurred taxable income along with different expenses into their

business (Auerbach and Hassett 2015). According to “section 91, ITAA 1936”, these

expenses along with the taxable income gained by their partnership is elaborated in this

section.

for gaining the taxable income throughout the business (Berliant and Gouveia 2018).

Consequently if the taxable income is following the negative limbs of the “section 8-1 (1),

ITAA 1997” if the expenses are considered as capital, domestic or private then the taxpayers

are not allowed for the deductions in their taxable incomes.

According to “section 25-10, ITAA 1997” a taxpayer is allowed to claim the

expenditure that happened for the repair in depreciating assets and also for the properties

which may lead to the increment of profit in partnership (Calabrese, Epple and Romano

2018). Under “section 25-10” any kind of maintenance work is known as repairs as painting

of business premises, repair of current business entities that may lead profit increment.

Consequently, the expense involved into this repairs and replacements includes deductions to

the taxable income for the taxpayers as they are incurring these changes for gaining more

taxable income. However, this is very important to be noted that the good or entities those

which are replaced should be same as the worn out entity but this should give more effective

results in terms of production or gaining profit. This aspect is included in order to highlight

the improvement of the business functionalities.

The taxpayer can be allowed instant $20,000 write- off if they have invested this

amount or less than it in their entity repairs and relevant expenses. Hence they will get a

deduction in their taxable income for these kinds of repairs.

Application:

Rendering to the “division 5, ITAA 1936” Daniel and Olivia ha incurred several

business activities those incurred taxable income along with different expenses into their

business (Auerbach and Hassett 2015). According to “section 91, ITAA 1936”, these

expenses along with the taxable income gained by their partnership is elaborated in this

section.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Agreeing to “section 6-5, ITAA 1997” the business revenues gained from the direct

debtors payment and business sales are considered as ordinary income in case of Olivia and

Daniel’s partnership. Under “Scott v CT (1935)”, the partnership has gained this profit as the

ordinary income with respect to the ordinary income rules stated under “section 6-5, ITAA

1997” (Saez and Stantcheva 2018).

Apart from the gains and profits, the partnership also incurred car expenses, electricity

bills and insurance amounts are falling under the positive limbs of “section 8-1 (1), ITAA

1997”, hence the partners are allowed for the deductions for their tax payments. These

expenses happened while producing the taxable income hence they are considered as the

positive limbs.

Accordingly the partners have purchased some items for their private purpose. Hence

these expenses will not be allowing them to get deductions as per the negative limbs of

“section 8-1 (2)”. If the expenditures are capital, domestic or private in nature then the

partners are not allowed to get deductions.

Conferring to the “section 25-10, ITAA 1997” the partners are allowed deductions for

the repairs and changes made into their entities such as painting of shop and replacement of

motor for refrigerator (Akcigit et al. 2018). These changes are allowed the educations in

taxable income as these are increasing the business profit as well the replacement of the

motor is reducing the decoration of the production. Hence Daniel and Olivia are allowed for

these expenses.

Apart from this, the purchase of refrigerator is another allowable deduction as they

have less than $20,000 for purchasing it. Hence partners will get deduction from their tax

returns.

Net Income of Partnership:

Agreeing to “section 6-5, ITAA 1997” the business revenues gained from the direct

debtors payment and business sales are considered as ordinary income in case of Olivia and

Daniel’s partnership. Under “Scott v CT (1935)”, the partnership has gained this profit as the

ordinary income with respect to the ordinary income rules stated under “section 6-5, ITAA

1997” (Saez and Stantcheva 2018).

Apart from the gains and profits, the partnership also incurred car expenses, electricity

bills and insurance amounts are falling under the positive limbs of “section 8-1 (1), ITAA

1997”, hence the partners are allowed for the deductions for their tax payments. These

expenses happened while producing the taxable income hence they are considered as the

positive limbs.

Accordingly the partners have purchased some items for their private purpose. Hence

these expenses will not be allowing them to get deductions as per the negative limbs of

“section 8-1 (2)”. If the expenditures are capital, domestic or private in nature then the

partners are not allowed to get deductions.

Conferring to the “section 25-10, ITAA 1997” the partners are allowed deductions for

the repairs and changes made into their entities such as painting of shop and replacement of

motor for refrigerator (Akcigit et al. 2018). These changes are allowed the educations in

taxable income as these are increasing the business profit as well the replacement of the

motor is reducing the decoration of the production. Hence Daniel and Olivia are allowed for

these expenses.

Apart from this, the purchase of refrigerator is another allowable deduction as they

have less than $20,000 for purchasing it. Hence partners will get deduction from their tax

returns.

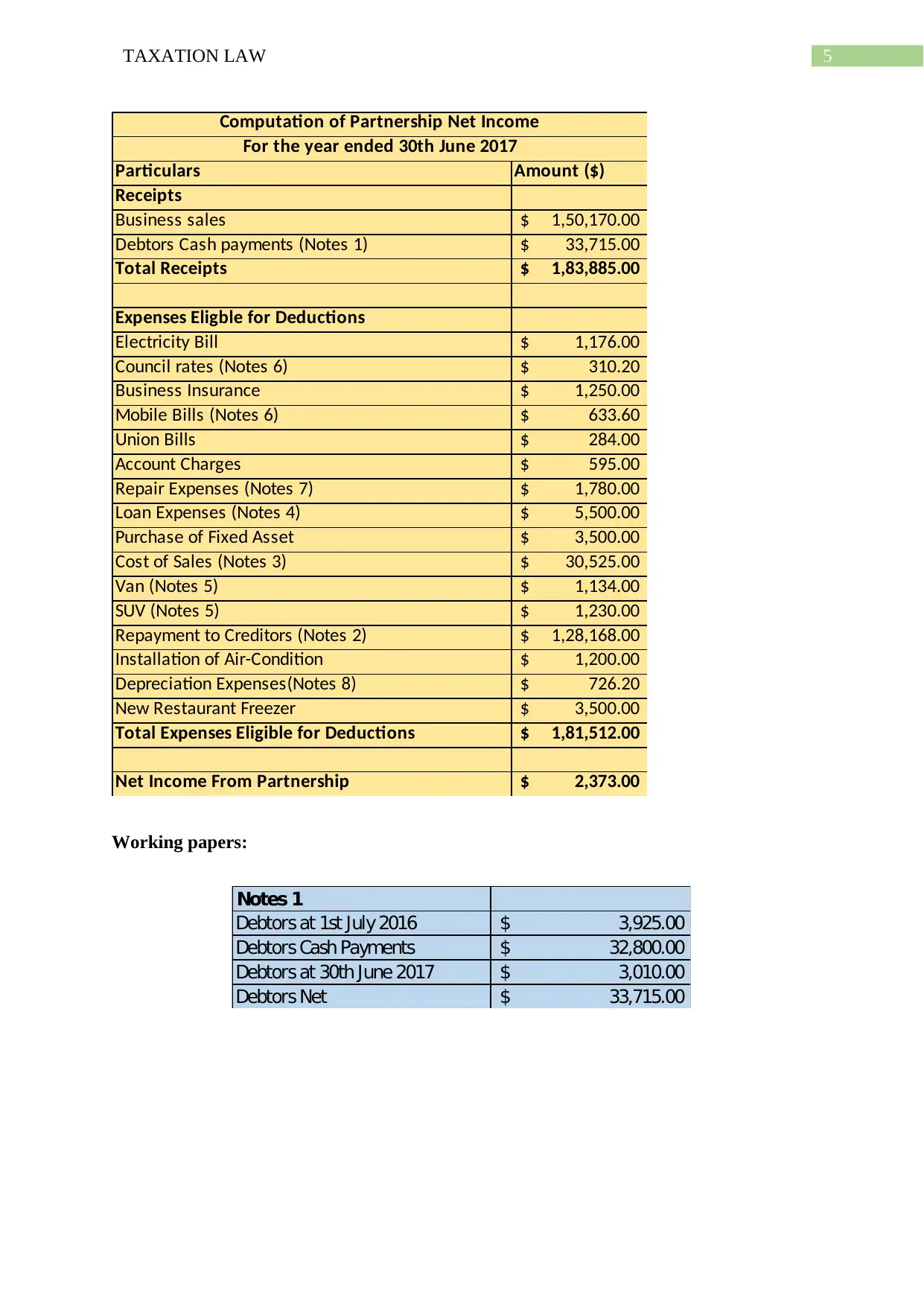

Net Income of Partnership:

5TAXATION LAW

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

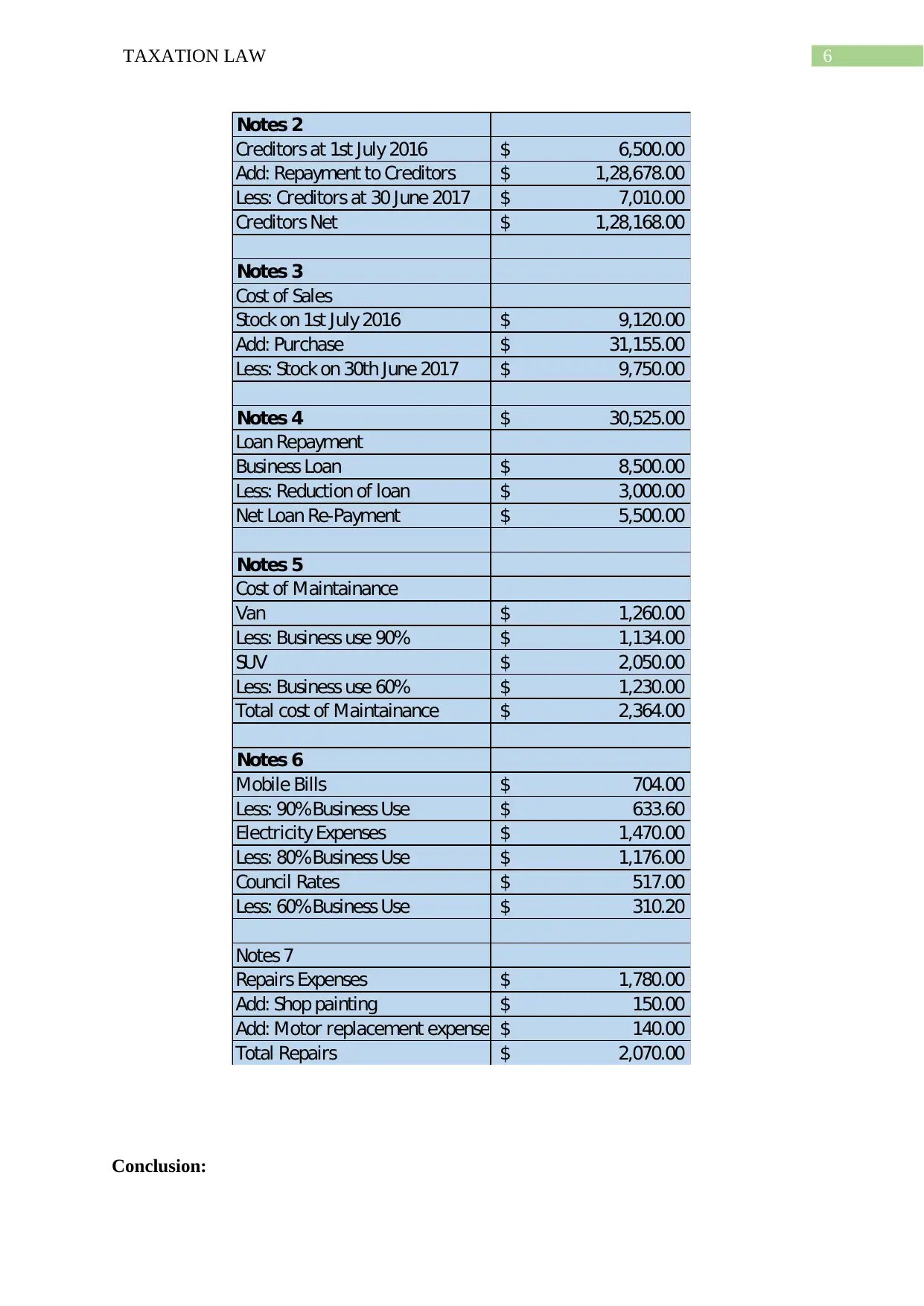

6TAXATION LAW

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Conclusion:

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Olivia and Daniel will be liable in the taxable part of their income and also the

deductions they gained from the tax is also elaborated in this section with examples under

“section 92, ITAA 1936”.

Answer to question 2:

Issues:

Is the payment made by employer in discharge of another person obligations to the

third party amounts to fringe benefit under “section 20, FBTAA 1986”? Is the employer

liable for FBT for granting the housing right to a person in relation to the year of tax under

“section 25, FBTAA 1986”?

Rule:

When the provider makes any kind of payment, in whole or in portions relating to the

obligation of another person or recipient for paying the amount to the third party in relation to

the expenses that is occurred by the recipient shall be taken be fringe benefit under “section

20, FBTAA 1986” (Black 2018). The expense payment fringe benefit only happens based on

the two conditions;

a. When the employer provides any reimbursement of the expenses that is occurred by

the employee. Or;

b. When the employer pay to the third party as the means of satisfying the expenses that

is occurred by the employee.

In both the above stated cases the expenses might be business expenses or the private

expenses. Whereas under “section 23, FBTAA 1986” the taxable value of the expense

Olivia and Daniel will be liable in the taxable part of their income and also the

deductions they gained from the tax is also elaborated in this section with examples under

“section 92, ITAA 1936”.

Answer to question 2:

Issues:

Is the payment made by employer in discharge of another person obligations to the

third party amounts to fringe benefit under “section 20, FBTAA 1986”? Is the employer

liable for FBT for granting the housing right to a person in relation to the year of tax under

“section 25, FBTAA 1986”?

Rule:

When the provider makes any kind of payment, in whole or in portions relating to the

obligation of another person or recipient for paying the amount to the third party in relation to

the expenses that is occurred by the recipient shall be taken be fringe benefit under “section

20, FBTAA 1986” (Black 2018). The expense payment fringe benefit only happens based on

the two conditions;

a. When the employer provides any reimbursement of the expenses that is occurred by

the employee. Or;

b. When the employer pay to the third party as the means of satisfying the expenses that

is occurred by the employee.

In both the above stated cases the expenses might be business expenses or the private

expenses. Whereas under “section 23, FBTAA 1986” the taxable value of the expense

8TAXATION LAW

payment fringe benefit represents the amount the employer pays or reimburses to the

employee (Auerbach 2015).

“Sec 25, FBTAA 1986” describes that a housing fringe benefit takes place on the

condition where the employee is given with the right of using the unit of accommodation or

any lease or licence that grants the right which is existent at the time when the unit of

accommodation forms the normal place of residence for the employee (Mellon 2016). The

unit of accommodation generally comprises of the flat or home or accommodation in the

house. “Section 27, FBTAA 1986” deals with the market value of the housing fringe benefit.

According to “section 27, FBTAA 1986” the employer will be liable for fringe benefit tax

upon the value of housing fringe benefit which is measured by referring to the market value

of the right for occupying the unit of accommodation that is further reduced by the recipient

rent towards the rental property.

Application:

Understandably, it is found that John is working with the printing company under the

post of senior executive. The employer of John pays the school fees of his child at the private

school that costs $15,000. With reference to the “section 20, FBTAA 1986”, payment of

school fees by the employer here gives rise to the expense payment fringe benefit. This is

because the payment made by the employer is in relation to the obligation of the employee

for satisfying the third party expenses (Sheffrin 2018). The payment made by employer in

respect of John’s obligation is private expense. Within the provision of “section 23, FBTAA

1986” a fringe benefit tax will be imposed on the employer for the value of expense payment

fringe benefit provided to John in respect of the child school fees.

During the FBT year it is also noticed that the employer of John provides him with the

accommodation in Sydney apartment. However, the accommodation accompanied a

payment fringe benefit represents the amount the employer pays or reimburses to the

employee (Auerbach 2015).

“Sec 25, FBTAA 1986” describes that a housing fringe benefit takes place on the

condition where the employee is given with the right of using the unit of accommodation or

any lease or licence that grants the right which is existent at the time when the unit of

accommodation forms the normal place of residence for the employee (Mellon 2016). The

unit of accommodation generally comprises of the flat or home or accommodation in the

house. “Section 27, FBTAA 1986” deals with the market value of the housing fringe benefit.

According to “section 27, FBTAA 1986” the employer will be liable for fringe benefit tax

upon the value of housing fringe benefit which is measured by referring to the market value

of the right for occupying the unit of accommodation that is further reduced by the recipient

rent towards the rental property.

Application:

Understandably, it is found that John is working with the printing company under the

post of senior executive. The employer of John pays the school fees of his child at the private

school that costs $15,000. With reference to the “section 20, FBTAA 1986”, payment of

school fees by the employer here gives rise to the expense payment fringe benefit. This is

because the payment made by the employer is in relation to the obligation of the employee

for satisfying the third party expenses (Sheffrin 2018). The payment made by employer in

respect of John’s obligation is private expense. Within the provision of “section 23, FBTAA

1986” a fringe benefit tax will be imposed on the employer for the value of expense payment

fringe benefit provided to John in respect of the child school fees.

During the FBT year it is also noticed that the employer of John provides him with the

accommodation in Sydney apartment. However, the accommodation accompanied a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

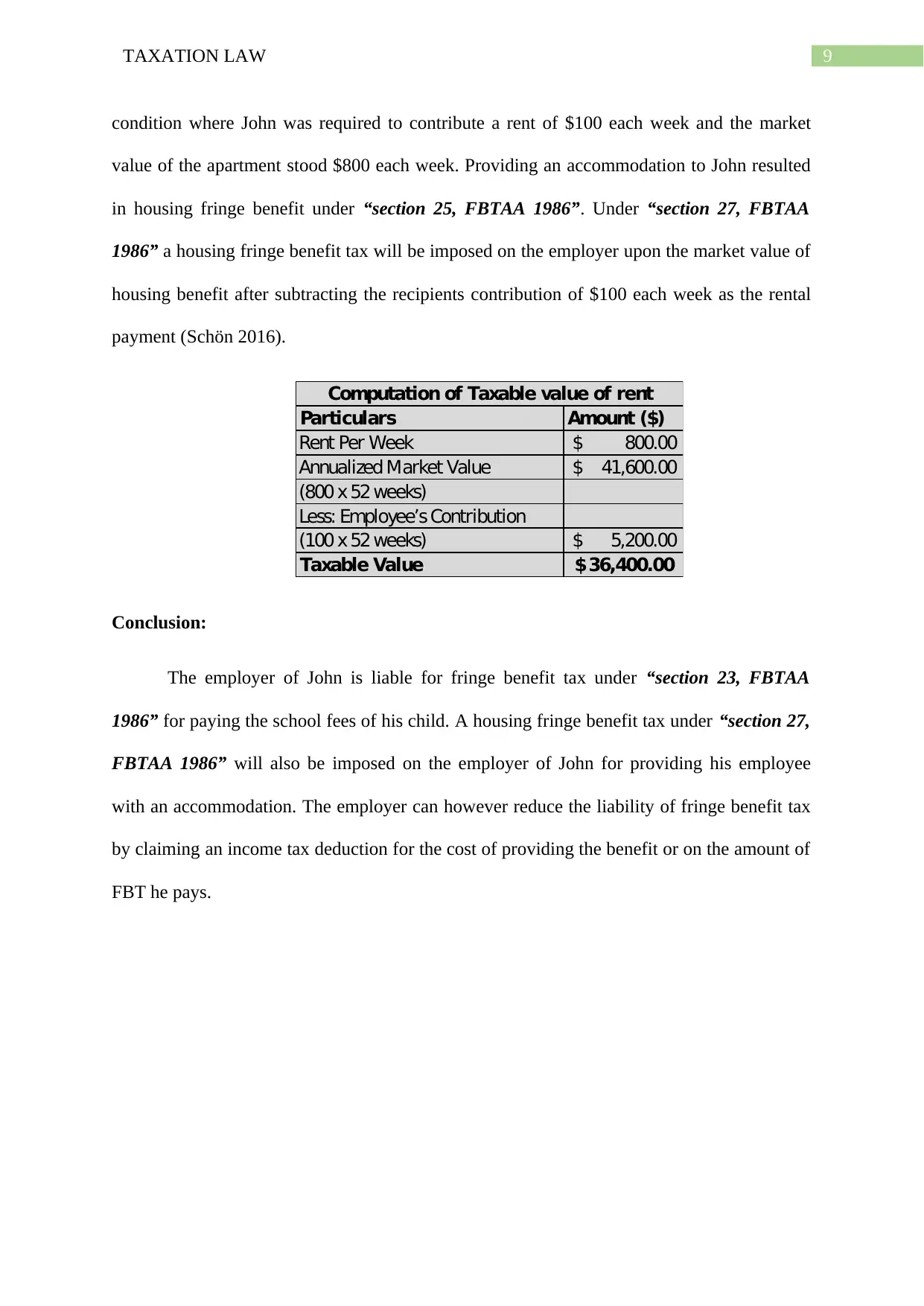

9TAXATION LAW

condition where John was required to contribute a rent of $100 each week and the market

value of the apartment stood $800 each week. Providing an accommodation to John resulted

in housing fringe benefit under “section 25, FBTAA 1986”. Under “section 27, FBTAA

1986” a housing fringe benefit tax will be imposed on the employer upon the market value of

housing benefit after subtracting the recipients contribution of $100 each week as the rental

payment (Schön 2016).

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer of John is liable for fringe benefit tax under “section 23, FBTAA

1986” for paying the school fees of his child. A housing fringe benefit tax under “section 27,

FBTAA 1986” will also be imposed on the employer of John for providing his employee

with an accommodation. The employer can however reduce the liability of fringe benefit tax

by claiming an income tax deduction for the cost of providing the benefit or on the amount of

FBT he pays.

condition where John was required to contribute a rent of $100 each week and the market

value of the apartment stood $800 each week. Providing an accommodation to John resulted

in housing fringe benefit under “section 25, FBTAA 1986”. Under “section 27, FBTAA

1986” a housing fringe benefit tax will be imposed on the employer upon the market value of

housing benefit after subtracting the recipients contribution of $100 each week as the rental

payment (Schön 2016).

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer of John is liable for fringe benefit tax under “section 23, FBTAA

1986” for paying the school fees of his child. A housing fringe benefit tax under “section 27,

FBTAA 1986” will also be imposed on the employer of John for providing his employee

with an accommodation. The employer can however reduce the liability of fringe benefit tax

by claiming an income tax deduction for the cost of providing the benefit or on the amount of

FBT he pays.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Akcigit, U., Grigsby, J., Nicholas, T. and Stantcheva, S., 2018. DP13167 Taxation and

Innovation in the 20th Century.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Auerbach, A.J., 2015, January. Capital Income Taxation: Good Ideas and Other Ideas.

In Proceedings. Annual Conference on Taxation and Minutes of the Annual Meeting of the

National Tax Association (Vol. 108, pp. 1-5). National Tax Association.

Berliant, M. and Gouveia, M., 2018. On the political economy of income taxation.

Black, D., 2018. The incidence of income taxes. Routledge.

Calabrese, S., Epple, D. and Romano, R., 2018. Majority Choice of Taxation and

Redistribution in a Federation (No. w25099). National Bureau of Economic Research.

Dong, J., 2018, October. Research on the Fairness of Income Distribution from the

Perspective of Finance and Taxation Law. In 8th International Conference on Management

and Computer Science (ICMCS 2018). Atlantis Press.

Mares, I. and Queralt, D., 2015. The non-democratic origins of income

taxation. Comparative Political Studies, 48(14), pp.1974-2009.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Schön, W., 2016. Destination-Based Income Taxation and WTO Law: A Note.

References:

Akcigit, U., Grigsby, J., Nicholas, T. and Stantcheva, S., 2018. DP13167 Taxation and

Innovation in the 20th Century.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Auerbach, A.J., 2015, January. Capital Income Taxation: Good Ideas and Other Ideas.

In Proceedings. Annual Conference on Taxation and Minutes of the Annual Meeting of the

National Tax Association (Vol. 108, pp. 1-5). National Tax Association.

Berliant, M. and Gouveia, M., 2018. On the political economy of income taxation.

Black, D., 2018. The incidence of income taxes. Routledge.

Calabrese, S., Epple, D. and Romano, R., 2018. Majority Choice of Taxation and

Redistribution in a Federation (No. w25099). National Bureau of Economic Research.

Dong, J., 2018, October. Research on the Fairness of Income Distribution from the

Perspective of Finance and Taxation Law. In 8th International Conference on Management

and Computer Science (ICMCS 2018). Atlantis Press.

Mares, I. and Queralt, D., 2015. The non-democratic origins of income

taxation. Comparative Political Studies, 48(14), pp.1974-2009.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Saez, E. and Stantcheva, S., 2018. A simpler theory of optimal capital taxation. Journal of

Public Economics, 162, pp.120-142.

Schön, W., 2016. Destination-Based Income Taxation and WTO Law: A Note.

11TAXATION LAW

Sheffrin, S.M., 2018. The Domain of Desert Principles for Taxation. Erasmus Journal for

Philosophy and Economics, 11(2), pp.220-244.

Sheffrin, S.M., 2018. The Domain of Desert Principles for Taxation. Erasmus Journal for

Philosophy and Economics, 11(2), pp.220-244.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.