HI6028 Taxation Law: Partnership Income and Fringe Benefit Analysis

VerifiedAdded on 2023/04/25

|13

|2614

|270

Homework Assignment

AI Summary

This assignment solution addresses two key issues in taxation law. The first question involves determining the net income of a partnership under Division 5 of the ITAA 1936, considering business sales, debtor payments, and various deductible expenses such as electricity bills, council rates, repairs, and depreciation. It applies relevant sections of the ITAA 1936 and case law to compute the partnership's net income. The second question examines the applicability of fringe benefit tax (FBT) under the FBTAA 1986 concerning housing fringe benefits and expense payment benefits provided to an employee. It analyzes whether the employer is accountable for FBT when providing housing and paying for the employee's child's school fees, applying sections of the FBTAA 1986 to determine the taxable value of these benefits and the employer's tax liabilities. The document concludes with computations of taxable amounts and recommendations for minimizing tax liabilities.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................8

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................8

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issues:

The issue is concerned with the determination of the net income of the partnership

under “division 5 of the ITAA 1936”.

Rule:

According to the “section 91, ITAA 1936” the partnership should lodge the income

tax return to reflect the amount of profit to be distributed among the partners. Consequently,

“division 5, ITAA 1936” explains that partnership under the general law is not the separate

legal entity and not required to pay tax (Becker, Reimer and Rust 2015). It is the partners

under “section 92, ITAA 1936” that pay tax in respect of the profits distributed to them. After

the allowable deductions “section 90, ITAA 1936” states that net income of partnership

should be determined.

Usually most of the income that is received by the taxpayer is termed as ordinary

income under “section 6-5, ITAA 1997”. The judicial concept of income in “Scott v CT

(1935)” denotes that income is not the word of art and requires implementation of principles

to determine the proportion of receipts should be held as income based on the ordinary

concepts and use (Tyson and Silverman 2013). Thus, gains originating from the business

activities are treated as income under “section 6-5, ITAA 1997”. To characterise the receipts

as ordinary income from business it is necessary that those receipts forms the part of normal

proceeds of the business.

The potentiality of applying “section 8-1” can be made to any person. Under the

positive limbs of “section 8-1 (1), ITAA 1997” a taxpayer is permitted to obtain deduction

from their taxable earnings for any expense or loss till the extent that it is occurred in

Answer to question 1:

Issues:

The issue is concerned with the determination of the net income of the partnership

under “division 5 of the ITAA 1936”.

Rule:

According to the “section 91, ITAA 1936” the partnership should lodge the income

tax return to reflect the amount of profit to be distributed among the partners. Consequently,

“division 5, ITAA 1936” explains that partnership under the general law is not the separate

legal entity and not required to pay tax (Becker, Reimer and Rust 2015). It is the partners

under “section 92, ITAA 1936” that pay tax in respect of the profits distributed to them. After

the allowable deductions “section 90, ITAA 1936” states that net income of partnership

should be determined.

Usually most of the income that is received by the taxpayer is termed as ordinary

income under “section 6-5, ITAA 1997”. The judicial concept of income in “Scott v CT

(1935)” denotes that income is not the word of art and requires implementation of principles

to determine the proportion of receipts should be held as income based on the ordinary

concepts and use (Tyson and Silverman 2013). Thus, gains originating from the business

activities are treated as income under “section 6-5, ITAA 1997”. To characterise the receipts

as ordinary income from business it is necessary that those receipts forms the part of normal

proceeds of the business.

The potentiality of applying “section 8-1” can be made to any person. Under the

positive limbs of “section 8-1 (1), ITAA 1997” a taxpayer is permitted to obtain deduction

from their taxable earnings for any expense or loss till the extent that it is occurred in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

producing taxable income or incurred in carrying on the business with the intent of gaining

taxable income (Rafool 2014). In “FCT v Amalgamated Zinc Ltd (1935)” gaining or

producing the taxable income should be interpreted as in the course of producing the taxable

income. Conversely, the negative limbs of general deduction rule states that a deduction for

outgoings under the general rule is denied if the expense meets any of the negative limbs

under “section 8-1 (2)”. This includes the expense of capital, domestic or private in nature.

Under “section 25-10, ITAA 1997” a taxpayer is permitted to claim for deduction

relating to expenses occurred on repairs to depreciating assets or properties that is used for

making income (Kaplan and Price 2014). Maintenance work are termed as repairs under

“section 25-10”. For instance, painting of the business property for fixing the current

deterioration and prohibiting any additional deterioration are termed as repair. The cost

incurred on replacing the items that are permanent fixtures installed on the business premises

for generating income is deductible repairs under the section 25-10. It must be noted that

deduction for replacement is only allowed of the worn out unit with the new unit of identical

design which only restores the effective functions and does results in any improvement.

The $20,000 instant write off allows the taxpayer to write-off the cost of assets that is

below the threshold limit of $20,000 up to the business portion in their tax return for the

relevant year of income (Mishra 2014).

Application:

The business activities carried on by Daniel and Olivia constitutes partnership under

“division 5, ITAA 1936”. Based on “section 91, ITAA 1936” the partnership carried on by

Daniel and Olivia should lodge the income tax return to reflect the amount of profit to be

distributed among the partners.

producing taxable income or incurred in carrying on the business with the intent of gaining

taxable income (Rafool 2014). In “FCT v Amalgamated Zinc Ltd (1935)” gaining or

producing the taxable income should be interpreted as in the course of producing the taxable

income. Conversely, the negative limbs of general deduction rule states that a deduction for

outgoings under the general rule is denied if the expense meets any of the negative limbs

under “section 8-1 (2)”. This includes the expense of capital, domestic or private in nature.

Under “section 25-10, ITAA 1997” a taxpayer is permitted to claim for deduction

relating to expenses occurred on repairs to depreciating assets or properties that is used for

making income (Kaplan and Price 2014). Maintenance work are termed as repairs under

“section 25-10”. For instance, painting of the business property for fixing the current

deterioration and prohibiting any additional deterioration are termed as repair. The cost

incurred on replacing the items that are permanent fixtures installed on the business premises

for generating income is deductible repairs under the section 25-10. It must be noted that

deduction for replacement is only allowed of the worn out unit with the new unit of identical

design which only restores the effective functions and does results in any improvement.

The $20,000 instant write off allows the taxpayer to write-off the cost of assets that is

below the threshold limit of $20,000 up to the business portion in their tax return for the

relevant year of income (Mishra 2014).

Application:

The business activities carried on by Daniel and Olivia constitutes partnership under

“division 5, ITAA 1936”. Based on “section 91, ITAA 1936” the partnership carried on by

Daniel and Olivia should lodge the income tax return to reflect the amount of profit to be

distributed among the partners.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The business transactions includes the business sales and debtors cash payments. The

revenue derived from business can be termed as ordinary income under “section 6-5, ITAA

1997”. Citing the event of “Scott v CT (1935)” the gains originating from the business

activities carried on by Daniel and Olivia are treated as income under “section 6-5, ITAA

1997” (Bohanon, Horowitz and McClure 2014). The cash payment and debtor’s payment

should be characterised as ordinary income from business since it forms the part of normal

proceeds of the business.

The partnership of Daniel and Olivia also reported car expenses, electricity bill,

council rates insurance etc. under the positive limbs of “section 8-1 (1), ITAA 1997” the

partners can obtained deduction. Citing “FCT v Amalgamated Zinc Ltd (1935)” the

expenses were occurred by partners in the course of producing the taxable business income.

Daniel and Olivia reported drawings in the form of cash and also drawings of items

for their private use. The partnership will be denied deduction for drawings under the general

rule because the expense meets any of the negative limbs under “section 8-1 (2)” and are

capital or private in nature.

The painting of shop property during partnership business amounts to repairs under

“section 25-10, ITAA 1997” because it involved fixing the current deterioration and

prohibiting any additional deterioration. Whereas the cost incurred on replacing the

refrigerator motor is deductible repairs under the section 25-10 because replacement involved

restoring the effective functions and does results in any improvement.

The purchase of new restaurant freezer is eligible for instant write-off because the

cost of assets is below the threshold limit of $20,000 and can be claimed for deduction from

the tax return.

The business transactions includes the business sales and debtors cash payments. The

revenue derived from business can be termed as ordinary income under “section 6-5, ITAA

1997”. Citing the event of “Scott v CT (1935)” the gains originating from the business

activities carried on by Daniel and Olivia are treated as income under “section 6-5, ITAA

1997” (Bohanon, Horowitz and McClure 2014). The cash payment and debtor’s payment

should be characterised as ordinary income from business since it forms the part of normal

proceeds of the business.

The partnership of Daniel and Olivia also reported car expenses, electricity bill,

council rates insurance etc. under the positive limbs of “section 8-1 (1), ITAA 1997” the

partners can obtained deduction. Citing “FCT v Amalgamated Zinc Ltd (1935)” the

expenses were occurred by partners in the course of producing the taxable business income.

Daniel and Olivia reported drawings in the form of cash and also drawings of items

for their private use. The partnership will be denied deduction for drawings under the general

rule because the expense meets any of the negative limbs under “section 8-1 (2)” and are

capital or private in nature.

The painting of shop property during partnership business amounts to repairs under

“section 25-10, ITAA 1997” because it involved fixing the current deterioration and

prohibiting any additional deterioration. Whereas the cost incurred on replacing the

refrigerator motor is deductible repairs under the section 25-10 because replacement involved

restoring the effective functions and does results in any improvement.

The purchase of new restaurant freezer is eligible for instant write-off because the

cost of assets is below the threshold limit of $20,000 and can be claimed for deduction from

the tax return.

5TAXATION LAW

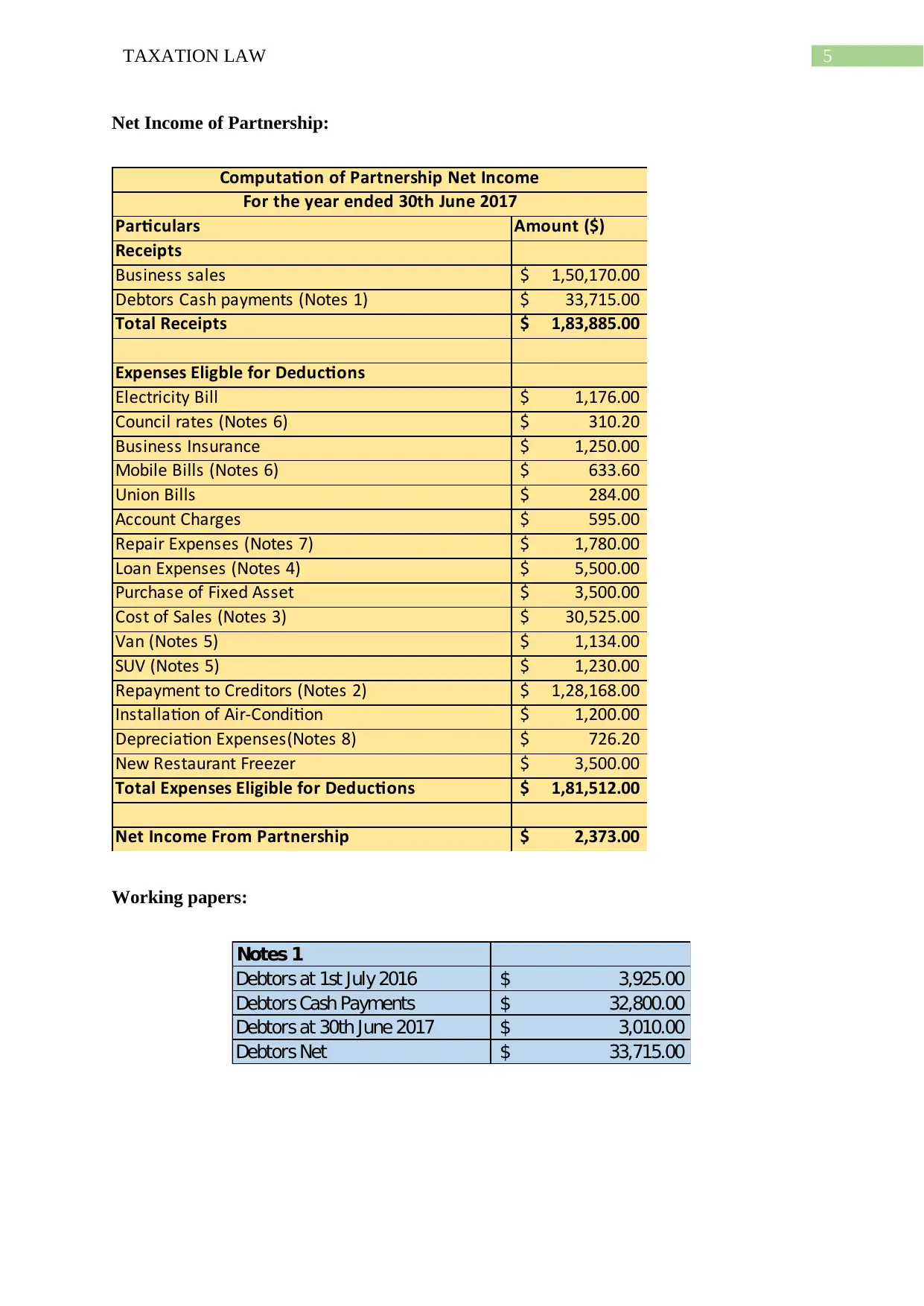

Net Income of Partnership:

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

Net Income of Partnership:

Particulars Amount ($)

Receipts

Business sales 1,50,170.00$

Debtors Cash payments (Notes 1) 33,715.00$

Total Receipts 1,83,885.00$

Expenses Eligble for Deductions

Electricity Bill 1,176.00$

Council rates (Notes 6) 310.20$

Business Insurance 1,250.00$

Mobile Bills (Notes 6) 633.60$

Union Bills 284.00$

Account Charges 595.00$

Repair Expenses (Notes 7) 1,780.00$

Loan Expenses (Notes 4) 5,500.00$

Purchase of Fixed Asset 3,500.00$

Cost of Sales (Notes 3) 30,525.00$

Van (Notes 5) 1,134.00$

SUV (Notes 5) 1,230.00$

Repayment to Creditors (Notes 2) 1,28,168.00$

Installation of Air-Condition 1,200.00$

Depreciation Expenses(Notes 8) 726.20$

New Restaurant Freezer 3,500.00$

Total Expenses Eligible for Deductions 1,81,512.00$

Net Income From Partnership 2,373.00$

Computation of Partnership Net Income

For the year ended 30th June 2017

Working papers:

Notes 1

Debtors at 1st July 2016 3,925.00$

Debtors Cash Payments 32,800.00$

Debtors at 30th June 2017 3,010.00$

Debtors Net 33,715.00$

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

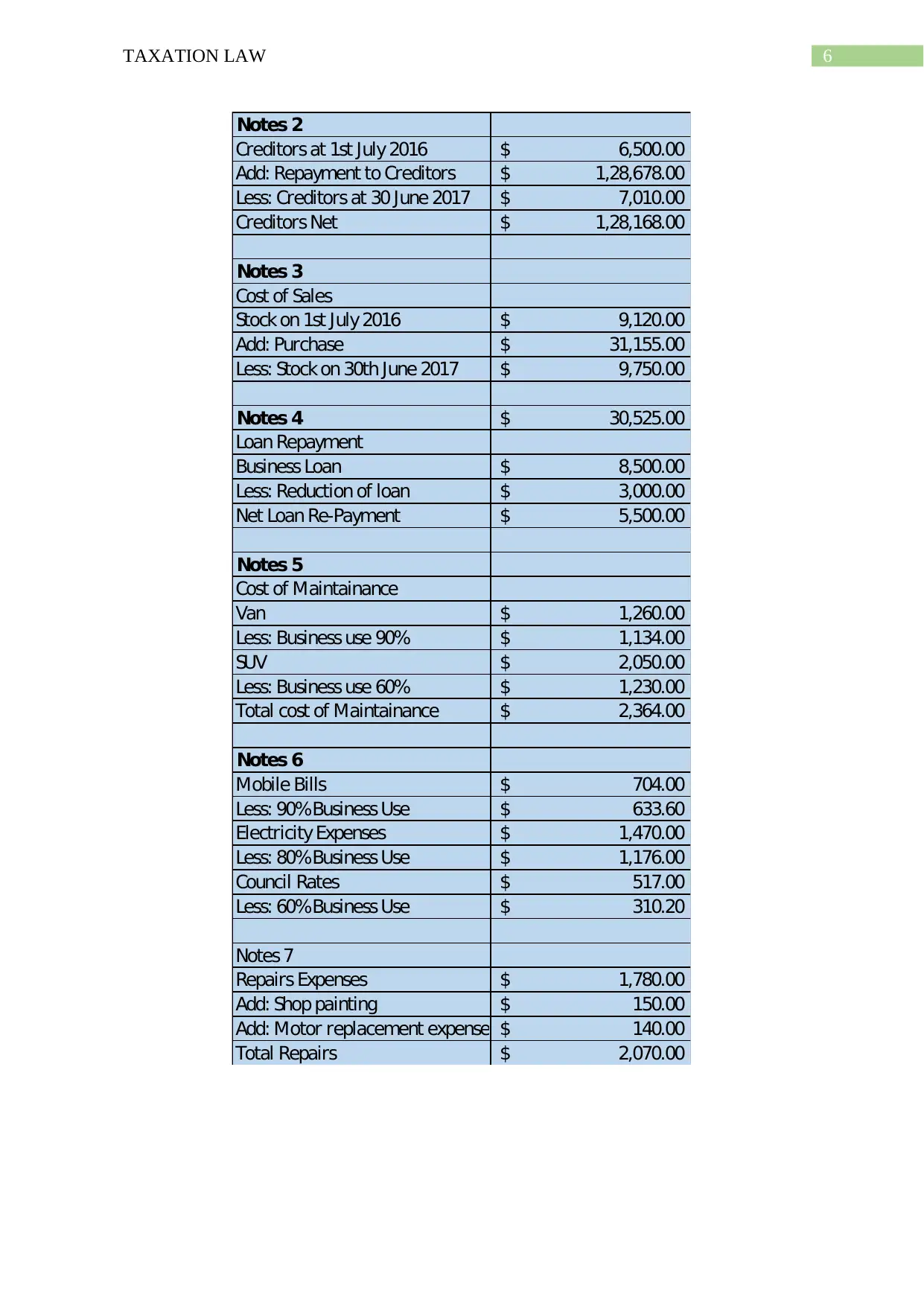

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Notes 2

Creditors at 1st July 2016 6,500.00$

Add: Repayment to Creditors 1,28,678.00$

Less: Creditors at 30 June 2017 7,010.00$

Creditors Net 1,28,168.00$

Notes 3

Cost of Sales

Stock on 1st July 2016 9,120.00$

Add: Purchase 31,155.00$

Less: Stock on 30th June 2017 9,750.00$

Notes 4 30,525.00$

Loan Repayment

Business Loan 8,500.00$

Less: Reduction of loan 3,000.00$

Net Loan Re-Payment 5,500.00$

Notes 5

Cost of Maintainance

Van 1,260.00$

Less: Business use 90% 1,134.00$

SUV 2,050.00$

Less: Business use 60% 1,230.00$

Total cost of Maintainance 2,364.00$

Notes 6

Mobile Bills 704.00$

Less: 90%Business Use 633.60$

Electricity Expenses 1,470.00$

Less: 80%Business Use 1,176.00$

Council Rates 517.00$

Less: 60%Business Use 310.20$

Notes 7

Repairs Expenses 1,780.00$

Add: Shop painting 150.00$

Add: Motor replacement expenses 140.00$

Total Repairs 2,070.00$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

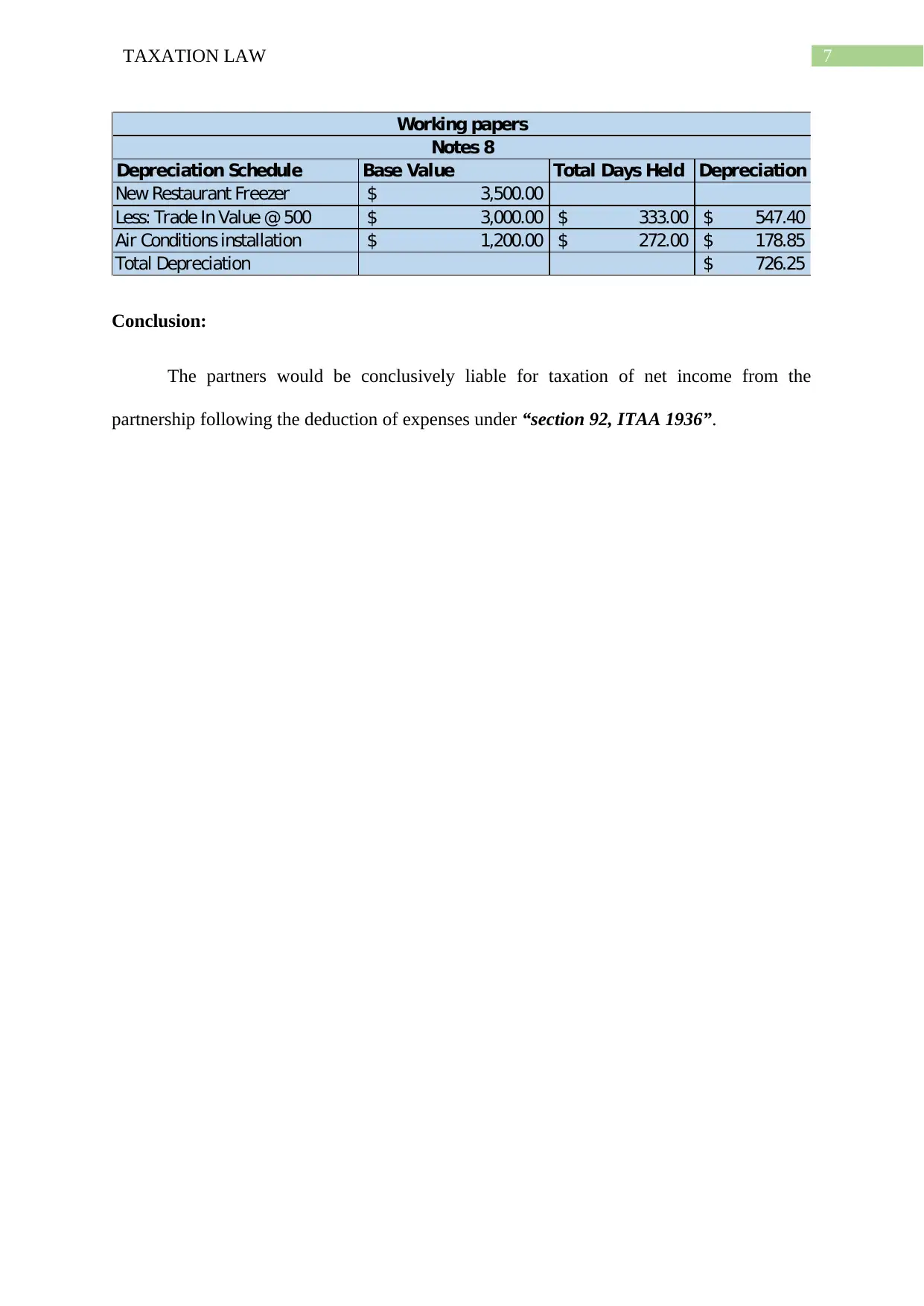

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

The partners would be conclusively liable for taxation of net income from the

partnership following the deduction of expenses under “section 92, ITAA 1936”.

Depreciation Schedule Base Value Total Days Held Depreciation

New Restaurant Freezer 3,500.00$

Less: Trade In Value @ 500 3,000.00$ 333.00$ 547.40$

Air Conditions installation 1,200.00$ 272.00$ 178.85$

Total Depreciation 726.25$

Working papers

Notes 8

Conclusion:

The partners would be conclusively liable for taxation of net income from the

partnership following the deduction of expenses under “section 92, ITAA 1936”.

8TAXATION LAW

Answer to question 2:

Issues:

Whether the employers are held accountable for the fringe benefit tax whey provide

the employee with the right of housing fringe benefit under the provision of “section 27 (a),

FBTAA 1986”? Whether the employer are accountable under the “section 23, FBTAA

1986” for the expense payment benefit provided to the third party on behalf of employee?

Rule:

As per the “section 20, FBTAA 1986” an expense payment benefit for an employer

arises in two ways particularly;

a. When the employer reimburses the employee for any kind of expenditure that is

occurred by them (Braithwaite and Reinhart 2019).

b. When the employer pays the third party for the satisfaction of the expenditure that is

occurred by the employee.

In both of the above stated circumstances the expenditure can be either the private

expense or the business expenditure or may possess the combination of both. As a general

rule, when the expenditure that has been occurred by the employee and the expenditure has

been subsequently reimbursed to the employee or paid directly to the third party then an

expense payment fringe benefit happens (Woellner et al. 2016). The taxable value of the

expense payment fringe benefit under “section 23, FBTAA 1986” represents the amount that

employer pays or reimburses to employee.

Denoting “section 23, FBTAA 1986” a housing fringe benefit happens when the

employee is given by the employer with the right of using a unit of accommodation as the

employee’s usual place of residence (Middleton 2015). “Section 27 (a) of the FBTAA 1986”

Answer to question 2:

Issues:

Whether the employers are held accountable for the fringe benefit tax whey provide

the employee with the right of housing fringe benefit under the provision of “section 27 (a),

FBTAA 1986”? Whether the employer are accountable under the “section 23, FBTAA

1986” for the expense payment benefit provided to the third party on behalf of employee?

Rule:

As per the “section 20, FBTAA 1986” an expense payment benefit for an employer

arises in two ways particularly;

a. When the employer reimburses the employee for any kind of expenditure that is

occurred by them (Braithwaite and Reinhart 2019).

b. When the employer pays the third party for the satisfaction of the expenditure that is

occurred by the employee.

In both of the above stated circumstances the expenditure can be either the private

expense or the business expenditure or may possess the combination of both. As a general

rule, when the expenditure that has been occurred by the employee and the expenditure has

been subsequently reimbursed to the employee or paid directly to the third party then an

expense payment fringe benefit happens (Woellner et al. 2016). The taxable value of the

expense payment fringe benefit under “section 23, FBTAA 1986” represents the amount that

employer pays or reimburses to employee.

Denoting “section 23, FBTAA 1986” a housing fringe benefit happens when the

employee is given by the employer with the right of using a unit of accommodation as the

employee’s usual place of residence (Middleton 2015). “Section 27 (a) of the FBTAA 1986”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

deals with the market value of housing fringe benefit. As per “section 27 (a), FBTAA 1986”

the taxable value of the housing fringe benefit is measured by referring to the market value of

the right for occupying the housing right further reduced by any recipient’s rents effecting the

rental property.

Applications:

Indications from the case study suggest that John was employed with the printing

company and worked as the senior executive. The employer as his salary package provided

John with the school fees of his child that included the cost of $15,000. Denoting the

explanation of “section 20, FBTAA 1986” an expense payment benefit for the employer has

arisen in this case. This is because the employer here has paid the private school fees

occurred by John to the third party for the satisfaction of the expenditure that is occurred by

the employee (Chardon 2014). The expenses incurred here can be termed as private expense.

The employer will be considered taxable under “section 23, FBTAA 1986” for the value of

fringe benefit that is paid to third party for meeting the expense.

In the following part of the case it is noticed that the employer provided John with the

flat in Sydney. As an agreement John has to pay $100 as rent per week for the apartment

while the Sydney apartment had the market value of $800 per week. Denoting “section 23,

FBTAA 1986” a housing fringe benefit has occurred for the employer because John was

provided with the right of using a unit of accommodation as the his usual place of residence.

Under “section 27 (a) of the FBTAA 1986” the employer will be measured for

taxation purpose under the legislation of Fringe Benefit Act for the market value of the right

for occupying the housing right further reduced by John’s contributions of $100 as rent in

effect of the Sydney apartment.

deals with the market value of housing fringe benefit. As per “section 27 (a), FBTAA 1986”

the taxable value of the housing fringe benefit is measured by referring to the market value of

the right for occupying the housing right further reduced by any recipient’s rents effecting the

rental property.

Applications:

Indications from the case study suggest that John was employed with the printing

company and worked as the senior executive. The employer as his salary package provided

John with the school fees of his child that included the cost of $15,000. Denoting the

explanation of “section 20, FBTAA 1986” an expense payment benefit for the employer has

arisen in this case. This is because the employer here has paid the private school fees

occurred by John to the third party for the satisfaction of the expenditure that is occurred by

the employee (Chardon 2014). The expenses incurred here can be termed as private expense.

The employer will be considered taxable under “section 23, FBTAA 1986” for the value of

fringe benefit that is paid to third party for meeting the expense.

In the following part of the case it is noticed that the employer provided John with the

flat in Sydney. As an agreement John has to pay $100 as rent per week for the apartment

while the Sydney apartment had the market value of $800 per week. Denoting “section 23,

FBTAA 1986” a housing fringe benefit has occurred for the employer because John was

provided with the right of using a unit of accommodation as the his usual place of residence.

Under “section 27 (a) of the FBTAA 1986” the employer will be measured for

taxation purpose under the legislation of Fringe Benefit Act for the market value of the right

for occupying the housing right further reduced by John’s contributions of $100 as rent in

effect of the Sydney apartment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

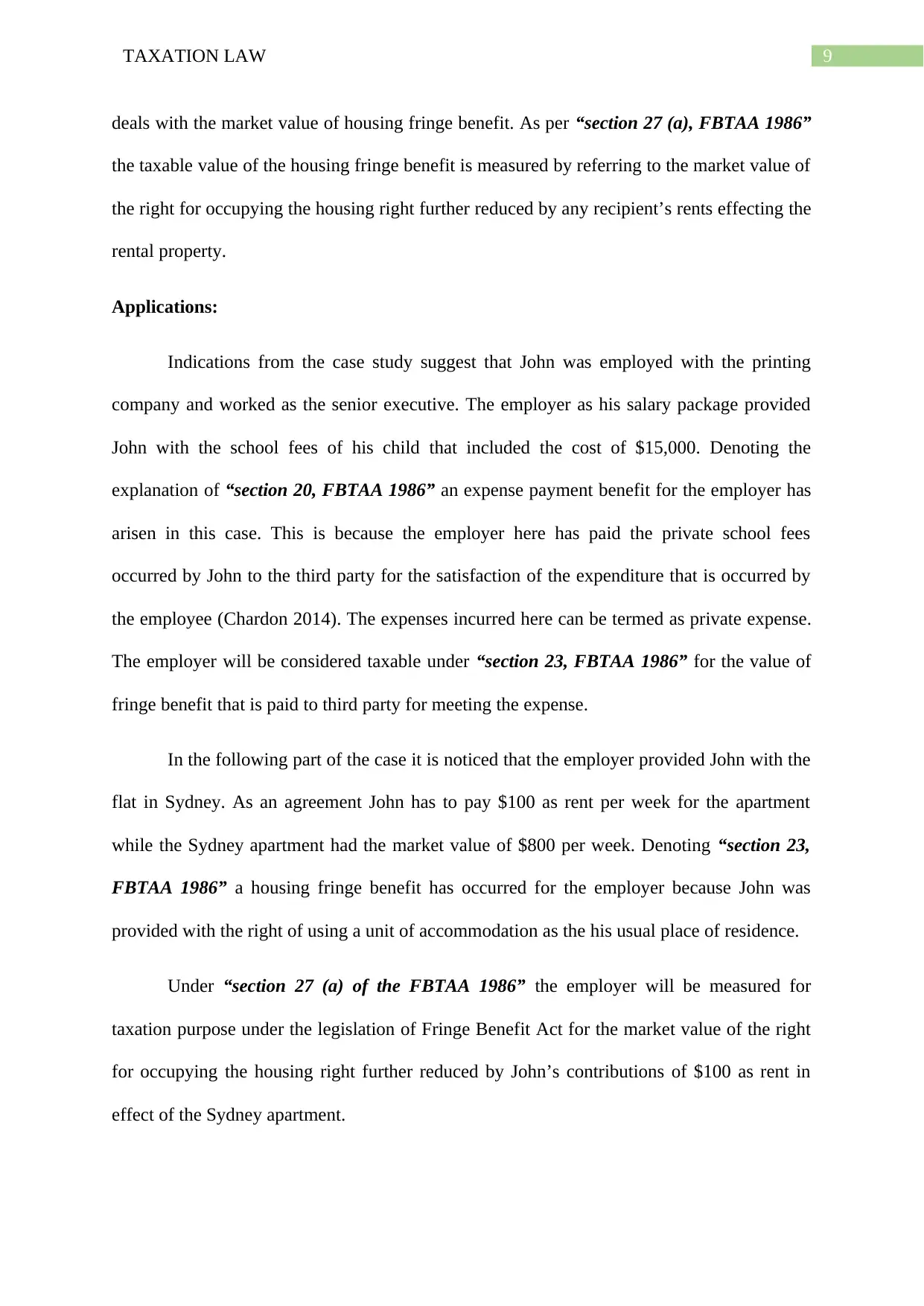

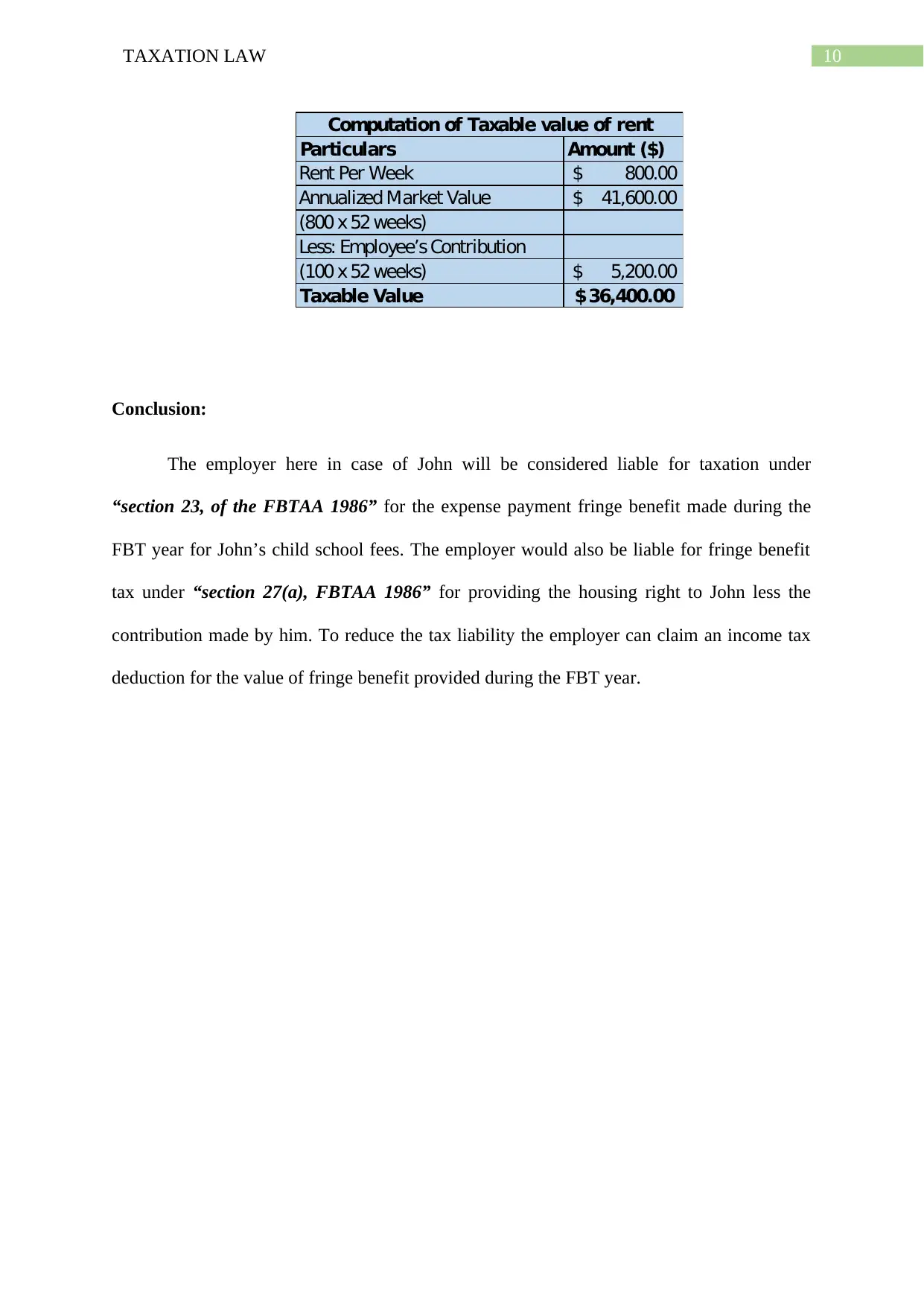

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer here in case of John will be considered liable for taxation under

“section 23, of the FBTAA 1986” for the expense payment fringe benefit made during the

FBT year for John’s child school fees. The employer would also be liable for fringe benefit

tax under “section 27(a), FBTAA 1986” for providing the housing right to John less the

contribution made by him. To reduce the tax liability the employer can claim an income tax

deduction for the value of fringe benefit provided during the FBT year.

Particulars Amount ($)

Rent Per Week 800.00$

Annualized Market Value 41,600.00$

(800 x 52 weeks)

Less: Employee’s Contribution

(100 x 52 weeks) 5,200.00$

Taxable Value 36,400.00$

Computation of Taxable value of rent

Conclusion:

The employer here in case of John will be considered liable for taxation under

“section 23, of the FBTAA 1986” for the expense payment fringe benefit made during the

FBT year for John’s child school fees. The employer would also be liable for fringe benefit

tax under “section 27(a), FBTAA 1986” for providing the housing right to John less the

contribution made by him. To reduce the tax liability the employer can claim an income tax

deduction for the value of fringe benefit provided during the FBT year.

11TAXATION LAW

References:

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bohanon, C.E., Horowitz, J.B. and McClure, J.E., 2014. Saying too little, too late: Public

finance textbooks and the excess burdens of taxation. Econ Journal Watch, 11(3), p.277.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?.

Chardon, T., 2014. Taxation and superannuation literacy in Australia: What do people know

(or think they know)?. JASSA, (1), p.42.

Kaplan, R.L. and Price, D.J., 2014. Change and Continuity in Fringe Benefit Taxation:

Seeking Sense and Sensibility. NYL Sch. L. Rev., 59, p.281.

Middleton, T., 2015. Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, pp.555-580.

Mishra, A.V., 2014. Australia's home bias and cross border taxation. Global Finance

Journal, 25(2), pp.108-123.

Rafool, M., 2014, May. A Guide To Property Taxes: An Overview. Denver: National

Conference of State Legislatures.

Tyson, E. and Silverman, D.J., 2013. Taxes for dummies: 2013 edition. Wiley Publishing,

Incorporated.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References:

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bohanon, C.E., Horowitz, J.B. and McClure, J.E., 2014. Saying too little, too late: Public

finance textbooks and the excess burdens of taxation. Econ Journal Watch, 11(3), p.277.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?.

Chardon, T., 2014. Taxation and superannuation literacy in Australia: What do people know

(or think they know)?. JASSA, (1), p.42.

Kaplan, R.L. and Price, D.J., 2014. Change and Continuity in Fringe Benefit Taxation:

Seeking Sense and Sensibility. NYL Sch. L. Rev., 59, p.281.

Middleton, T., 2015. Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and Securities

Law Journal, 33, pp.555-580.

Mishra, A.V., 2014. Australia's home bias and cross border taxation. Global Finance

Journal, 25(2), pp.108-123.

Rafool, M., 2014, May. A Guide To Property Taxes: An Overview. Denver: National

Conference of State Legislatures.

Tyson, E. and Silverman, D.J., 2013. Taxes for dummies: 2013 edition. Wiley Publishing,

Incorporated.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.