Taxation Law: Examining Capital Gains Tax and Fringe Benefit Issues

VerifiedAdded on 2023/06/06

|16

|3450

|340

Report

AI Summary

This assignment delves into various aspects of taxation law, primarily focusing on capital gains tax (CGT) and fringe benefit tax (FBT). It addresses scenarios involving the sale of vacant land, the loss of an antique bed, the treatment of pre-CGT assets like paintings, and the disposal of shares. The analysis clarifies the applicability of CGT based on asset type and acquisition date, referencing relevant sections of the ITAA 1997. Furthermore, the assignment examines the tax implications of fringe benefits provided to employees, such as car benefits, expense payments, and loans, referencing the Fringe Benefit Tax Assessment Act 1986 (FBTAA). It identifies key issues related to employer-provided benefits and their taxable values, offering a comprehensive overview of the legal framework governing these aspects of taxation.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to B:..............................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Introduction:...............................................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to B:..............................................................................................................................9

References:...............................................................................................................................10

2TAXATION LAW

Introduction:

Capital gains tax functions by the considering the taxable income during the tax year

in which the asset is sold or else disposed to the taxpayer (Engelmann et al. 2017). If the

individual taxpayer is the company, then in such a situation the company should pay 30% on

the net amount of capital gains. If the person is the individual, the tax rate will be similar to

that of the individual tax rate during the year.

Answer to question 1:

Vacant Land:

The treatment of tax for the land and the profits from the sales of those land is in

general reliant on whether it is treated as the capital asset or the matter of business or the

business transactions. Capital gains tax is taken into the account as vacant land is the capital

asset. Still, when the transactions of land are assumed as the element of the business activity,

the sale proceeds of the land may be treated as the ordinary income and might be subjected to

GST (Tanzi 2014). A capital gains tax liability will arise if a vacant land is acquired by the

person. The vacant land sums up as the capital asset. But when an individual purchase the

land to use it in the business or for making revenue then the person is dealing in the activity

of land. The sale proceeds of the land are the ordinary income where the taxpayer will be

compelled to register under the goods and service tax.

Selling the block of empty land at $320,000 amounts to capital gains tax. The cost

base of the vacant land will be including the outlays that the taxpayer has reported throughout

the time when the land was in possession of the taxpayer will be added with the purchase

price. The capital gains from the empty land will be included for assessment purpose.

Introduction:

Capital gains tax functions by the considering the taxable income during the tax year

in which the asset is sold or else disposed to the taxpayer (Engelmann et al. 2017). If the

individual taxpayer is the company, then in such a situation the company should pay 30% on

the net amount of capital gains. If the person is the individual, the tax rate will be similar to

that of the individual tax rate during the year.

Answer to question 1:

Vacant Land:

The treatment of tax for the land and the profits from the sales of those land is in

general reliant on whether it is treated as the capital asset or the matter of business or the

business transactions. Capital gains tax is taken into the account as vacant land is the capital

asset. Still, when the transactions of land are assumed as the element of the business activity,

the sale proceeds of the land may be treated as the ordinary income and might be subjected to

GST (Tanzi 2014). A capital gains tax liability will arise if a vacant land is acquired by the

person. The vacant land sums up as the capital asset. But when an individual purchase the

land to use it in the business or for making revenue then the person is dealing in the activity

of land. The sale proceeds of the land are the ordinary income where the taxpayer will be

compelled to register under the goods and service tax.

Selling the block of empty land at $320,000 amounts to capital gains tax. The cost

base of the vacant land will be including the outlays that the taxpayer has reported throughout

the time when the land was in possession of the taxpayer will be added with the purchase

price. The capital gains from the empty land will be included for assessment purpose.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Antique Bed:

As per the “section 149-10 of the ITAA 1997” a pre-CGT asset that is owned by a person

only when the person last purchased the asset before the 20 September 1985 (Mares and

Queralt 2015). All the assets that is purchased since capital gains tax started on the September

1985 there will be the CGT unless it is specifically excluded. The example of the CGT is

applied to the real estate, leases or goodwill, foreign currency, collectables as well as the

personal usage assets that are further than the certain value.

When there is loss or destruction of the CGT asset there is a CGT event C1 under “SECT

104.20 of ITAA 1997” (Genovese, Scheve and Stasavage 2016). CGT event C1 happens if

the CGT asset that a person owned is lost or destroyed. This event is generally applying to a

portion of the CGT asset under the section 108-5 when the time of the event is;

a. When the person obtains the compensation for the loss or the destruction or;

b. If there is no compensation received following the discovery or destruction taking

place.

A person makes the capital gains if the capital proceeds obtained from the loss or

destruction of the assets is greater than the cost base of the assets. simultaneously, a person

makes capital loss if the capital proceeds is lower than the reduced cost base of the assets

(Ábrahám, Koehne and Pavoni 2016). The antique bed is the collectables that is beyond the

certain value. A CGT event C1 happened when the compensation amounting to $11,000 for

the loss of stolen antique bed was received.

Painting:

Antique Bed:

As per the “section 149-10 of the ITAA 1997” a pre-CGT asset that is owned by a person

only when the person last purchased the asset before the 20 September 1985 (Mares and

Queralt 2015). All the assets that is purchased since capital gains tax started on the September

1985 there will be the CGT unless it is specifically excluded. The example of the CGT is

applied to the real estate, leases or goodwill, foreign currency, collectables as well as the

personal usage assets that are further than the certain value.

When there is loss or destruction of the CGT asset there is a CGT event C1 under “SECT

104.20 of ITAA 1997” (Genovese, Scheve and Stasavage 2016). CGT event C1 happens if

the CGT asset that a person owned is lost or destroyed. This event is generally applying to a

portion of the CGT asset under the section 108-5 when the time of the event is;

a. When the person obtains the compensation for the loss or the destruction or;

b. If there is no compensation received following the discovery or destruction taking

place.

A person makes the capital gains if the capital proceeds obtained from the loss or

destruction of the assets is greater than the cost base of the assets. simultaneously, a person

makes capital loss if the capital proceeds is lower than the reduced cost base of the assets

(Ábrahám, Koehne and Pavoni 2016). The antique bed is the collectables that is beyond the

certain value. A CGT event C1 happened when the compensation amounting to $11,000 for

the loss of stolen antique bed was received.

Painting:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Capital gains or the capital loss for the pre-CGT asset must be ignored if the asset is

purchased before 20 September 1985. “SECT 108.10 of ITAA 1997” states that at the time of

working out the net capital gains or the net capital loss during the income year, capital loss

from the collectables can be used to lower down the capital gains from the collectables

(Kabatek, Van Soest and Stancanelli 2014). A CGT exemption is given to the leases, shares,

improvements made to land that are bought or acquired before the 20 September 1985.

The painting here is the pre-CGT collectables that is purchased before the start of the

capital gains tax. As a result, the taxpayer here will be exempted from the capital gains that is

made because the asset is the Pre-CGT asset.

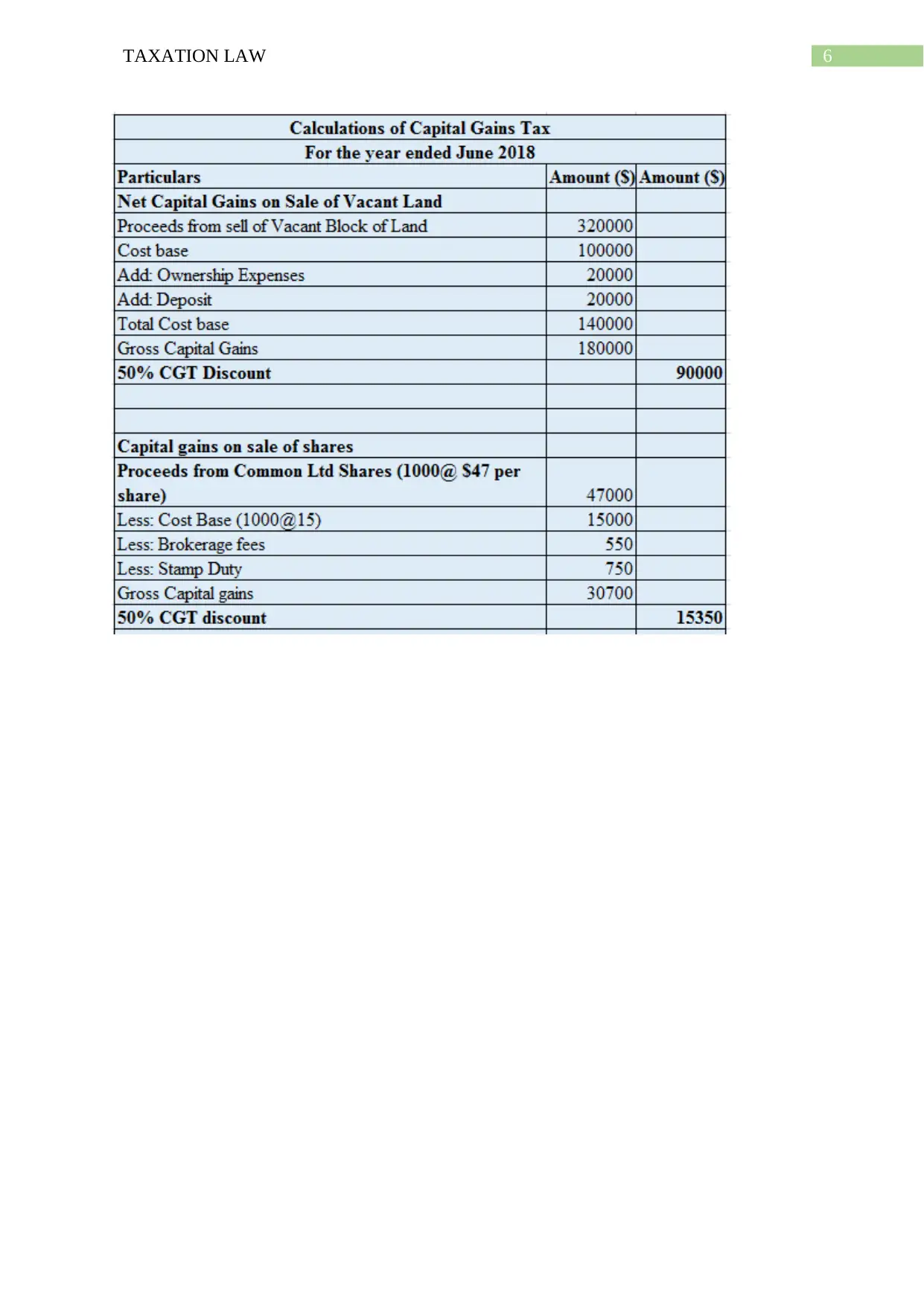

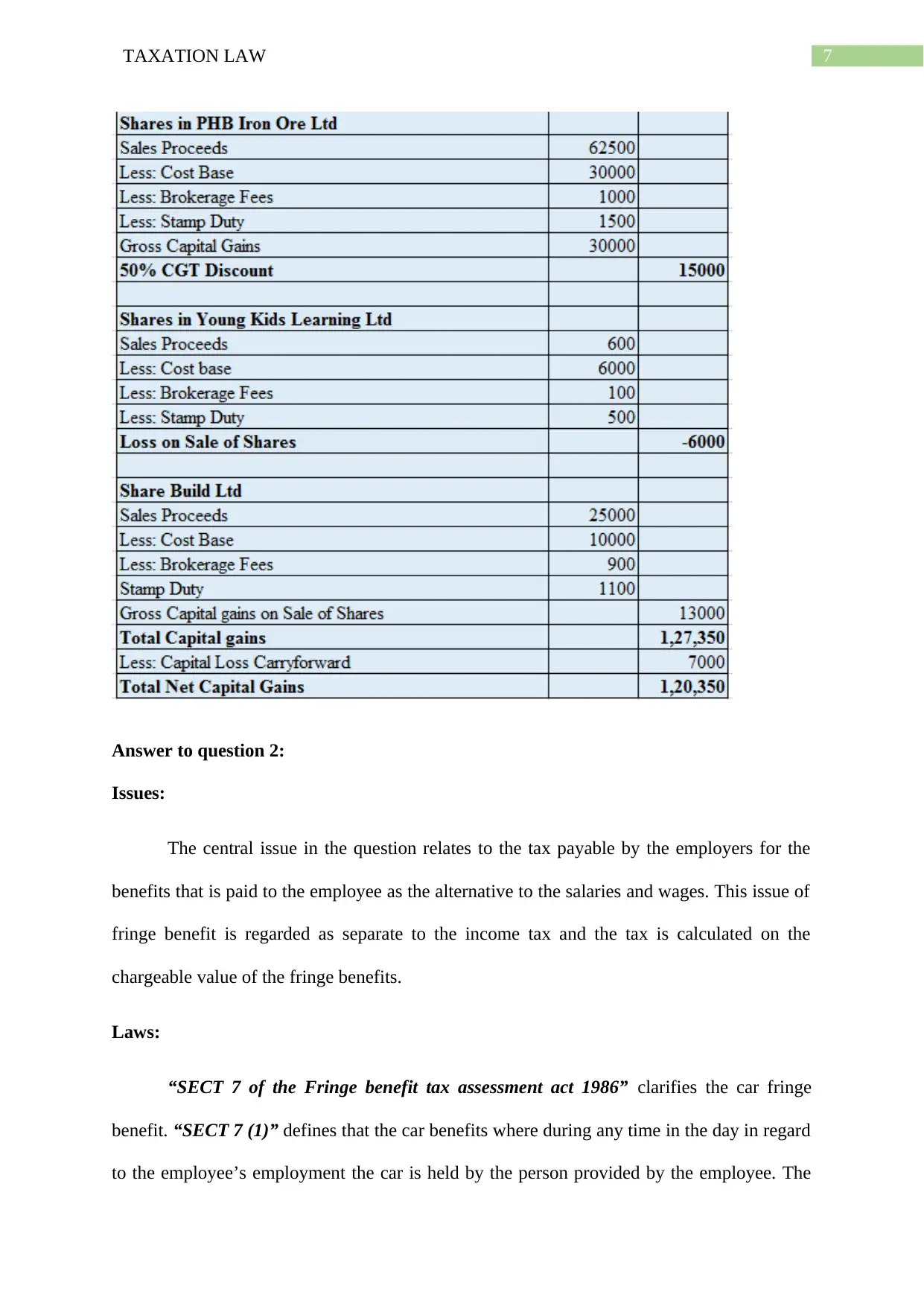

Shares:

The purpose of the “SECT 115.45 of the ITAA 1997” a CGT event happens when the

shares are sold. A capital gain is not the discounted capital gains when the capital gains from

the CGT event happens to the shares in the company or unit (Apps and Rees 2015). As per

the “SECT 104.10 of the ITAA 1997” a CGT event A1 gives rise when the disposal of the

asset results in the change in the ownership occurring to the taxpayer or to other entity.

However, the change in ownership does not takes place when a person stops being the owner

of the asset but remains the beneficial owner. A person can make the gains when the shares in

the company are disposed or the interest in the trust that is purchased.

For the purpose of the “SECT 104.10 of the ITAA 1997” a CGT event C1 happened

when the shares of the common bank ltd, iron ore ltd and share build ltd (Apps, Van Long

and Rees 2014). These shares yielded capital gains to the taxpayer whereas the capital loss

from the shares of young kids were made. The capital loss can be offset from the capital gains

yielded from the above stated shares.

Violin:

Capital gains or the capital loss for the pre-CGT asset must be ignored if the asset is

purchased before 20 September 1985. “SECT 108.10 of ITAA 1997” states that at the time of

working out the net capital gains or the net capital loss during the income year, capital loss

from the collectables can be used to lower down the capital gains from the collectables

(Kabatek, Van Soest and Stancanelli 2014). A CGT exemption is given to the leases, shares,

improvements made to land that are bought or acquired before the 20 September 1985.

The painting here is the pre-CGT collectables that is purchased before the start of the

capital gains tax. As a result, the taxpayer here will be exempted from the capital gains that is

made because the asset is the Pre-CGT asset.

Shares:

The purpose of the “SECT 115.45 of the ITAA 1997” a CGT event happens when the

shares are sold. A capital gain is not the discounted capital gains when the capital gains from

the CGT event happens to the shares in the company or unit (Apps and Rees 2015). As per

the “SECT 104.10 of the ITAA 1997” a CGT event A1 gives rise when the disposal of the

asset results in the change in the ownership occurring to the taxpayer or to other entity.

However, the change in ownership does not takes place when a person stops being the owner

of the asset but remains the beneficial owner. A person can make the gains when the shares in

the company are disposed or the interest in the trust that is purchased.

For the purpose of the “SECT 104.10 of the ITAA 1997” a CGT event C1 happened

when the shares of the common bank ltd, iron ore ltd and share build ltd (Apps, Van Long

and Rees 2014). These shares yielded capital gains to the taxpayer whereas the capital loss

from the shares of young kids were made. The capital loss can be offset from the capital gains

yielded from the above stated shares.

Violin:

5TAXATION LAW

In “SECT 118.10 of the ITAA 1997” a capital gains or the capital loss that is made

from the collectables is overlooked if the first element of the cost base or the expenses

relating to the depreciating asset is lesser than the $500. Any capital gains that they make

from the assets that is used personally is overlooked and not taken into the considerations if

the first element of the assets costs base or the first element of its cost base of the

depreciating asset is $10,000 or below (Burton 2017). “Subsection 108-20 (1), ITAA 1997”

clarifies the taxpayer that makes the capital loss from the personal use assets should be

disregarded.

The violin is the personal use assets because the taxpayer used the violin for its

personal enjoyment and usage. The cost of the violin is $5500 which is below the prescribed

limit given in “SECT 118.10 ITAA 1997” (Pinto and Evans 2018). The capital gains that is

yielded upon the disposal of the violin should be ignored because the violin is the personal

use asset and there cannot be any kind of capital gains tax in this regard.

In “SECT 118.10 of the ITAA 1997” a capital gains or the capital loss that is made

from the collectables is overlooked if the first element of the cost base or the expenses

relating to the depreciating asset is lesser than the $500. Any capital gains that they make

from the assets that is used personally is overlooked and not taken into the considerations if

the first element of the assets costs base or the first element of its cost base of the

depreciating asset is $10,000 or below (Burton 2017). “Subsection 108-20 (1), ITAA 1997”

clarifies the taxpayer that makes the capital loss from the personal use assets should be

disregarded.

The violin is the personal use assets because the taxpayer used the violin for its

personal enjoyment and usage. The cost of the violin is $5500 which is below the prescribed

limit given in “SECT 118.10 ITAA 1997” (Pinto and Evans 2018). The capital gains that is

yielded upon the disposal of the violin should be ignored because the violin is the personal

use asset and there cannot be any kind of capital gains tax in this regard.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issues:

The central issue in the question relates to the tax payable by the employers for the

benefits that is paid to the employee as the alternative to the salaries and wages. This issue of

fringe benefit is regarded as separate to the income tax and the tax is calculated on the

chargeable value of the fringe benefits.

Laws:

“SECT 7 of the Fringe benefit tax assessment act 1986” clarifies the car fringe

benefit. “SECT 7 (1)” defines that the car benefits where during any time in the day in regard

to the employee’s employment the car is held by the person provided by the employee. The

Answer to question 2:

Issues:

The central issue in the question relates to the tax payable by the employers for the

benefits that is paid to the employee as the alternative to the salaries and wages. This issue of

fringe benefit is regarded as separate to the income tax and the tax is calculated on the

chargeable value of the fringe benefits.

Laws:

“SECT 7 of the Fringe benefit tax assessment act 1986” clarifies the car fringe

benefit. “SECT 7 (1)” defines that the car benefits where during any time in the day in regard

to the employee’s employment the car is held by the person provided by the employee. The

8TAXATION LAW

car benefits are applicable relating to the private usage by the employee or the associate of

the employee (Motro 2016). Under “SECT 7 (1) (b)” car benefits happen when the specific

conditions are fulfilled.

This includes either the car provider is the employer or the car is made available

under the arrangement amid the provider or the another person. It is notable that the associate

of the employer or the employer of the employee provides the car during the day in regard to

the employment, a car benefit would eventually arise under “SECT 7 (1)”. “SECT 9 of the

FBTAA 1986” explains that the taxable value of the car benefit is calculated by using the

statutory formula (Rogers and Weller 2014). While the taxpayer can use the “SECT 10 of the

FBTAA 1986” to determine the assessable value of the car fringe benefit under the cost basis

method.

“SECT 20” provides the description of expanse payment benefits under “FBTAA

1986”. Under this section where the person makes the payment in discharge either in whole

or in part as the obligation of the other person to pay the expenses to the third party in regard

to the expenditure occurred by the recipient (Cremer and Roeder 2018). The expense

payment benefit is also regarded as the benefit when another person is reimbursed in whole

or the part in relation to the sum of expenses that is occurred by the recipient.

The reimbursement of the expenses under this section will be taken to constitute the

provision of benefit by the employer to the employee. “SECT 23 of the FBTAA 1986”

defines that the chargeable value in regard to the year of taxation of the expenditure payment

fringe benefit given the amount of payment that is referred is reimbursed by the provider

(Bagger et al. 2018).

car benefits are applicable relating to the private usage by the employee or the associate of

the employee (Motro 2016). Under “SECT 7 (1) (b)” car benefits happen when the specific

conditions are fulfilled.

This includes either the car provider is the employer or the car is made available

under the arrangement amid the provider or the another person. It is notable that the associate

of the employer or the employer of the employee provides the car during the day in regard to

the employment, a car benefit would eventually arise under “SECT 7 (1)”. “SECT 9 of the

FBTAA 1986” explains that the taxable value of the car benefit is calculated by using the

statutory formula (Rogers and Weller 2014). While the taxpayer can use the “SECT 10 of the

FBTAA 1986” to determine the assessable value of the car fringe benefit under the cost basis

method.

“SECT 20” provides the description of expanse payment benefits under “FBTAA

1986”. Under this section where the person makes the payment in discharge either in whole

or in part as the obligation of the other person to pay the expenses to the third party in regard

to the expenditure occurred by the recipient (Cremer and Roeder 2018). The expense

payment benefit is also regarded as the benefit when another person is reimbursed in whole

or the part in relation to the sum of expenses that is occurred by the recipient.

The reimbursement of the expenses under this section will be taken to constitute the

provision of benefit by the employer to the employee. “SECT 23 of the FBTAA 1986”

defines that the chargeable value in regard to the year of taxation of the expenditure payment

fringe benefit given the amount of payment that is referred is reimbursed by the provider

(Bagger et al. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Where during any specific time when the car is held by the person that being the

employer, associate of the employer or the person to whom the arrangement of the car is

available at the garage of the employee then it would give rise to car benefits.

As per the “SECT 16 of the FBTAA 1986” where the person or the loan provider

makes the loan to the recipient (Ono and Uchida 2018). The making of such loan will be

constituting the benefit that is given by the provider to the recipient and that the benefit will

be taken to have been provided in relation to every tax year. The loan amount may be

provided as the whole or part of which the recipient is obligatory required to refund the either

any or the portion of the loan. For the purpose of the this act the person is under the

obligation of paying the amount to another person.

As per the “SECT 18 of the FBTAA 1986” there results in the taxable fringe benefit

of the loan (Benczúr et al. 2014). Subject to this provision under “SECT 18 (1) of the

FBTAA 1986” the loan fringe benefit rendered in relation to the year of taxation it represents

the amount through which the notional sum of interest in relation to the notional amount of

interest that is accrued for the loan during the year of tax.

Very generally, the car parking benefit might come into the existence during each of

the day in which the provider of the car also gives the recipient with the space for parking

that is exclusively for the use of the employee. Definitely, the car parking benefit will be

arising in the fringe benefit year only under the below given conditions;

a. A car that is parked at the premises that is owned by the owner of the car or under the

control of the provider generally not the employer.

b. Inside the radius of the one kilometre of the premises where the parking of the car is

made at the commercial parking station that takes the fees for the full day parking.

c. The parking of the car is given to the employee when they are under the employment.

Where during any specific time when the car is held by the person that being the

employer, associate of the employer or the person to whom the arrangement of the car is

available at the garage of the employee then it would give rise to car benefits.

As per the “SECT 16 of the FBTAA 1986” where the person or the loan provider

makes the loan to the recipient (Ono and Uchida 2018). The making of such loan will be

constituting the benefit that is given by the provider to the recipient and that the benefit will

be taken to have been provided in relation to every tax year. The loan amount may be

provided as the whole or part of which the recipient is obligatory required to refund the either

any or the portion of the loan. For the purpose of the this act the person is under the

obligation of paying the amount to another person.

As per the “SECT 18 of the FBTAA 1986” there results in the taxable fringe benefit

of the loan (Benczúr et al. 2014). Subject to this provision under “SECT 18 (1) of the

FBTAA 1986” the loan fringe benefit rendered in relation to the year of taxation it represents

the amount through which the notional sum of interest in relation to the notional amount of

interest that is accrued for the loan during the year of tax.

Very generally, the car parking benefit might come into the existence during each of

the day in which the provider of the car also gives the recipient with the space for parking

that is exclusively for the use of the employee. Definitely, the car parking benefit will be

arising in the fringe benefit year only under the below given conditions;

a. A car that is parked at the premises that is owned by the owner of the car or under the

control of the provider generally not the employer.

b. Inside the radius of the one kilometre of the premises where the parking of the car is

made at the commercial parking station that takes the fees for the full day parking.

c. The parking of the car is given to the employee when they are under the employment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

d. The employee uses the car given by the employer for traveling between the place of

home and work for a minimum of once in a day.

e. The car is parked or leased at the primary place of the employment during the day.

Application:

The central issue of the case is here determining the fringe benefit tax for the Rapid

Heat all through the FBT year. The benefit here in the current case provided to Jasmine

holding employer employee relationship with the Rapid Heat Pty Ltd. Jasmine in regard to

the employer employee relationship is provided with the fringe benefit during the year

(Bernheim and Scheuer 2014). This includes the car that is solely provided to Jasmine in

order to meet the work related travelling obligations.

The traveling or use of the car was not limited to the employment but it is also

available for the private use. Using the car by Jasmine given by the Rapid Heat Pty resulted

in the car benefit under “SECT 7 of the Fringe benefit tax assessment act 1986”. The car

benefits are applicable for Rapid Heat for making the car available relating to the private

usage of the employee (Seto 2017). Employing the “SECT 9 of the FBTAA 1986” the

taxable value of the car benefit can be calculated by Rapid Heat by using the statutory

formula.

The events that were unfolded from the case study suggest that minor repairing

expenses were occurred by Jasmine for the car. Referring to “SECT 20” the description of

expense payment by Rapid Heat gave rise to the expense payment fringe benefit. The minor

repairing expenses that has been reimbursed by the employer has given rise to the fringe

benefit of expense payment for Rapid Heat (Boadway and Pestieau 2018). The expenses that

was occurred was in the employee course of the employment which was eventually

reimbursed therefore this give rise to the expense payment benefit.

d. The employee uses the car given by the employer for traveling between the place of

home and work for a minimum of once in a day.

e. The car is parked or leased at the primary place of the employment during the day.

Application:

The central issue of the case is here determining the fringe benefit tax for the Rapid

Heat all through the FBT year. The benefit here in the current case provided to Jasmine

holding employer employee relationship with the Rapid Heat Pty Ltd. Jasmine in regard to

the employer employee relationship is provided with the fringe benefit during the year

(Bernheim and Scheuer 2014). This includes the car that is solely provided to Jasmine in

order to meet the work related travelling obligations.

The traveling or use of the car was not limited to the employment but it is also

available for the private use. Using the car by Jasmine given by the Rapid Heat Pty resulted

in the car benefit under “SECT 7 of the Fringe benefit tax assessment act 1986”. The car

benefits are applicable for Rapid Heat for making the car available relating to the private

usage of the employee (Seto 2017). Employing the “SECT 9 of the FBTAA 1986” the

taxable value of the car benefit can be calculated by Rapid Heat by using the statutory

formula.

The events that were unfolded from the case study suggest that minor repairing

expenses were occurred by Jasmine for the car. Referring to “SECT 20” the description of

expense payment by Rapid Heat gave rise to the expense payment fringe benefit. The minor

repairing expenses that has been reimbursed by the employer has given rise to the fringe

benefit of expense payment for Rapid Heat (Boadway and Pestieau 2018). The expenses that

was occurred was in the employee course of the employment which was eventually

reimbursed therefore this give rise to the expense payment benefit.

11TAXATION LAW

There was the instance in the case where the employee Jasmine was out of the state

and parked the car at the airport. The car was additionally parked for five additional days for

the yearly repairs. In this aspect there was no car parking fringe benefit as the car was not

parked at the premises that is owned by the owner of the car or under the control of the

provider. The car was not within the radius of the one kilometre of the premises where the

parking of the car is made (Ludwig and Krueger 2016). Therefore, there cannot be any car

parking fringe benefit in this respect for Rapid Heat Pty Ltd.

The events that were occurred in the case study it is understood that the Rapid Heat

gave Jasmine with the loan of $500,000. The interest of the loan was below the statutory rate

of interest and as result of this there was the loan benefit of the Rapid Heat under the “SECT

16 of the FBTAA 1986”. The making of such loan by Rapid Heat will be constituting the

benefit that is given by the provider to the recipient and that the benefit will be taken to have

been provided in relation to every tax year (Boadway and Pestieau 2018). The taxable value

of the loan benefit under the “SECT 18 of the FBTAA 1986” stating that the amount of

difference that is presented in the notional interest rate from the actual rate of interest. The

employer Rapid heat can consider opting for claiming income tax deductions for the benefit

given to employee during the FBT year.

There was the instance in the case where the employee Jasmine was out of the state

and parked the car at the airport. The car was additionally parked for five additional days for

the yearly repairs. In this aspect there was no car parking fringe benefit as the car was not

parked at the premises that is owned by the owner of the car or under the control of the

provider. The car was not within the radius of the one kilometre of the premises where the

parking of the car is made (Ludwig and Krueger 2016). Therefore, there cannot be any car

parking fringe benefit in this respect for Rapid Heat Pty Ltd.

The events that were occurred in the case study it is understood that the Rapid Heat

gave Jasmine with the loan of $500,000. The interest of the loan was below the statutory rate

of interest and as result of this there was the loan benefit of the Rapid Heat under the “SECT

16 of the FBTAA 1986”. The making of such loan by Rapid Heat will be constituting the

benefit that is given by the provider to the recipient and that the benefit will be taken to have

been provided in relation to every tax year (Boadway and Pestieau 2018). The taxable value

of the loan benefit under the “SECT 18 of the FBTAA 1986” stating that the amount of

difference that is presented in the notional interest rate from the actual rate of interest. The

employer Rapid heat can consider opting for claiming income tax deductions for the benefit

given to employee during the FBT year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.