Taxation Law: Understanding Taxable Income and Capital Gains Tax

VerifiedAdded on 2023/06/11

|13

|3040

|217

AI Summary

This article provides a detailed explanation of taxable income and capital gains tax under the ITA Act 1997. It covers different scenarios and provides examples to help readers understand the rules and regulations. The article also includes answers to common questions and is a comprehensive guide to Taxation Law.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

Reference List:.........................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to question 2:.................................................................................................................6

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................8

Reference List:.........................................................................................................................11

3TAXATION LAW

Answer to question 1:

Issue:

Are the monies that received for providing services amounts to reward from service

and would such kind of amount would be liable for tax with respect to the “section 6-5 of the

ITA Act 1997”?

Rule:

The rule here in “section 6-1 of the ITA Act 1997” explains that a person that obtains

the income their private effort is regarded as income that has been obtained by the person

from the private exertion (Travers 2014). Under the income from the private exertion the

income that are derived are the wages that is paid to the taxpayer or the salaries that is

received from the personal exertion. This also include the payment which is received as the

fees or pensions, gratuities, allowances or an individual taxpayer deriving revenue from the

business that is carried on by himself or in partnership.

The general rule of the “section 6-5 of the ITA Act 1997” provides an explanation of

the ordinary income as the income which is determined as per the ordinary concepts (Becker,

Reimer and Rust 2015). In an important explanation that has been in the example case of

“Commissioner of Taxation v Scott (1935)” that it is necessary to determine whether the

amount that is derived is treated as income according to the ordinary concepts.

There is an important explanation of the “section 6-5 of the ITA Act 1997” monies

that is received by the taxpayer as the reward for the services is would be considered for

taxation purpose (Peiros and Smyth 2017). Any kind of receipt from the media relating to the

narration of life story is regarded as the reward for service and money that is obtained from

the such reward through media is taxable under the “section 6-5 of the ITA Act 1997”

Answer to question 1:

Issue:

Are the monies that received for providing services amounts to reward from service

and would such kind of amount would be liable for tax with respect to the “section 6-5 of the

ITA Act 1997”?

Rule:

The rule here in “section 6-1 of the ITA Act 1997” explains that a person that obtains

the income their private effort is regarded as income that has been obtained by the person

from the private exertion (Travers 2014). Under the income from the private exertion the

income that are derived are the wages that is paid to the taxpayer or the salaries that is

received from the personal exertion. This also include the payment which is received as the

fees or pensions, gratuities, allowances or an individual taxpayer deriving revenue from the

business that is carried on by himself or in partnership.

The general rule of the “section 6-5 of the ITA Act 1997” provides an explanation of

the ordinary income as the income which is determined as per the ordinary concepts (Becker,

Reimer and Rust 2015). In an important explanation that has been in the example case of

“Commissioner of Taxation v Scott (1935)” that it is necessary to determine whether the

amount that is derived is treated as income according to the ordinary concepts.

There is an important explanation of the “section 6-5 of the ITA Act 1997” monies

that is received by the taxpayer as the reward for the services is would be considered for

taxation purpose (Peiros and Smyth 2017). Any kind of receipt from the media relating to the

narration of life story is regarded as the reward for service and money that is obtained from

the such reward through media is taxable under the “section 6-5 of the ITA Act 1997”

4TAXATION LAW

because without providing service money cannot be received. A leading explanation of

“Brent v Federal Commissioner of Taxation (1971)” can be explained where it was noticed

that the wife of the train robber has received income from the personal service that was

rendered for telling her life story to media publication was considered having the nature of

income (Smith 2015). These income would be classified as ordinary income and with respect

to “section 6-5 of the ITA Act 1997” it is taxable.

Taking into the consideration the “Housden (Inspector of Taxes v Marshall (1958)”

an explanation can be provided that taxpayer in the present situation decided to make the

Jockey experience available (Van Rensburg 2015). As a result of this the photographs that

were taken by the taxpayer and the cuttings relating to the newspaper was sold. The money

which is obtained from the sale of the photographs and cuttings of newspaper is regarded as

income according to the ordinary concepts and taxable with respect to the provision of the

“section 6-5 of the ITA Act 1997”.

Selling of autobiographies that is written by the taxpayer and obtaining income from

such sale of autobiographies would be counted as the Royalty which is taxable under

provision of the “section 6-5 of the ITA Act 1997” (Mintz 2016). Leading example of

“Hobbs v Hussy (1942) TC 153)” provides an explanation that criminal who was notorious

derived $1500 from selling his autobiographies to newspaper article for publications. The

money that was received should be classified as income and taxable under provision of the

“section 6-5 of the ITA Act 1997”.

Applications:

The applications of the above stated principles can be in the situation of Hilary who

was the famous mountain climber and one occasion after being approached by the Newspaper

to tell the life story she agreed to write the book to narrate her experience in exchange for a

because without providing service money cannot be received. A leading explanation of

“Brent v Federal Commissioner of Taxation (1971)” can be explained where it was noticed

that the wife of the train robber has received income from the personal service that was

rendered for telling her life story to media publication was considered having the nature of

income (Smith 2015). These income would be classified as ordinary income and with respect

to “section 6-5 of the ITA Act 1997” it is taxable.

Taking into the consideration the “Housden (Inspector of Taxes v Marshall (1958)”

an explanation can be provided that taxpayer in the present situation decided to make the

Jockey experience available (Van Rensburg 2015). As a result of this the photographs that

were taken by the taxpayer and the cuttings relating to the newspaper was sold. The money

which is obtained from the sale of the photographs and cuttings of newspaper is regarded as

income according to the ordinary concepts and taxable with respect to the provision of the

“section 6-5 of the ITA Act 1997”.

Selling of autobiographies that is written by the taxpayer and obtaining income from

such sale of autobiographies would be counted as the Royalty which is taxable under

provision of the “section 6-5 of the ITA Act 1997” (Mintz 2016). Leading example of

“Hobbs v Hussy (1942) TC 153)” provides an explanation that criminal who was notorious

derived $1500 from selling his autobiographies to newspaper article for publications. The

money that was received should be classified as income and taxable under provision of the

“section 6-5 of the ITA Act 1997”.

Applications:

The applications of the above stated principles can be in the situation of Hilary who

was the famous mountain climber and one occasion after being approached by the Newspaper

to tell the life story she agreed to write the book to narrate her experience in exchange for a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5TAXATION LAW

sum of $10,000. With reference to the “section 6-1 of the ITA Act 1997” these amount is an

income from the personal exertion. (Contractor 2016) Mentioning the example of

“Commissioner of Taxation v Scott (1935)” the sum of $10,000 should viewed as ordinary

income and liable for taxation under “section 6-5 of the ITA Act 1997”. The amount received

by Hilary is a personal service reward and the instances of “Brent v Federal Commissioner

of Taxation (1971)” can be applied to consider the sum of $10,000 for taxation purpose under

“section 6-5 of the ITA Act 1997” as the ordinary concept income.

Later Hilary sold the photographs and the manuscripts to the library for $5,000 and

$2,000 respectively. With respect to the illustration made in “Housden (Inspector of Taxes v

Marshall (1958)” the money received from selling the photographs and manuscripts is

taxable as an ordinary income under the provision of “section 6-5 of the ITAA 1997”.

If Hilary decides to write the book herself then the money received from the sale of

autobiographies would be held as royalty income. Referring to the illustrations of the “Hobbs

v Hussy (1942) TC 153)” these sale of books written by Hilary and obtaining the income

from the selling of autobiographies is taxable income as per the ordinary concepts explained

under the provision of “section 6-5 of the ITAA 1997”.

Conclusion:

After analysing the case of Hilary the amount of $10,000 as well as the money

received sale of photographs and manuscripts should be considered as private exertion

income. These amounts are taxable as per the ordinary concepts of “section 6-5 of the ITAA

1997”.

sum of $10,000. With reference to the “section 6-1 of the ITA Act 1997” these amount is an

income from the personal exertion. (Contractor 2016) Mentioning the example of

“Commissioner of Taxation v Scott (1935)” the sum of $10,000 should viewed as ordinary

income and liable for taxation under “section 6-5 of the ITA Act 1997”. The amount received

by Hilary is a personal service reward and the instances of “Brent v Federal Commissioner

of Taxation (1971)” can be applied to consider the sum of $10,000 for taxation purpose under

“section 6-5 of the ITA Act 1997” as the ordinary concept income.

Later Hilary sold the photographs and the manuscripts to the library for $5,000 and

$2,000 respectively. With respect to the illustration made in “Housden (Inspector of Taxes v

Marshall (1958)” the money received from selling the photographs and manuscripts is

taxable as an ordinary income under the provision of “section 6-5 of the ITAA 1997”.

If Hilary decides to write the book herself then the money received from the sale of

autobiographies would be held as royalty income. Referring to the illustrations of the “Hobbs

v Hussy (1942) TC 153)” these sale of books written by Hilary and obtaining the income

from the selling of autobiographies is taxable income as per the ordinary concepts explained

under the provision of “section 6-5 of the ITAA 1997”.

Conclusion:

After analysing the case of Hilary the amount of $10,000 as well as the money

received sale of photographs and manuscripts should be considered as private exertion

income. These amounts are taxable as per the ordinary concepts of “section 6-5 of the ITAA

1997”.

6TAXATION LAW

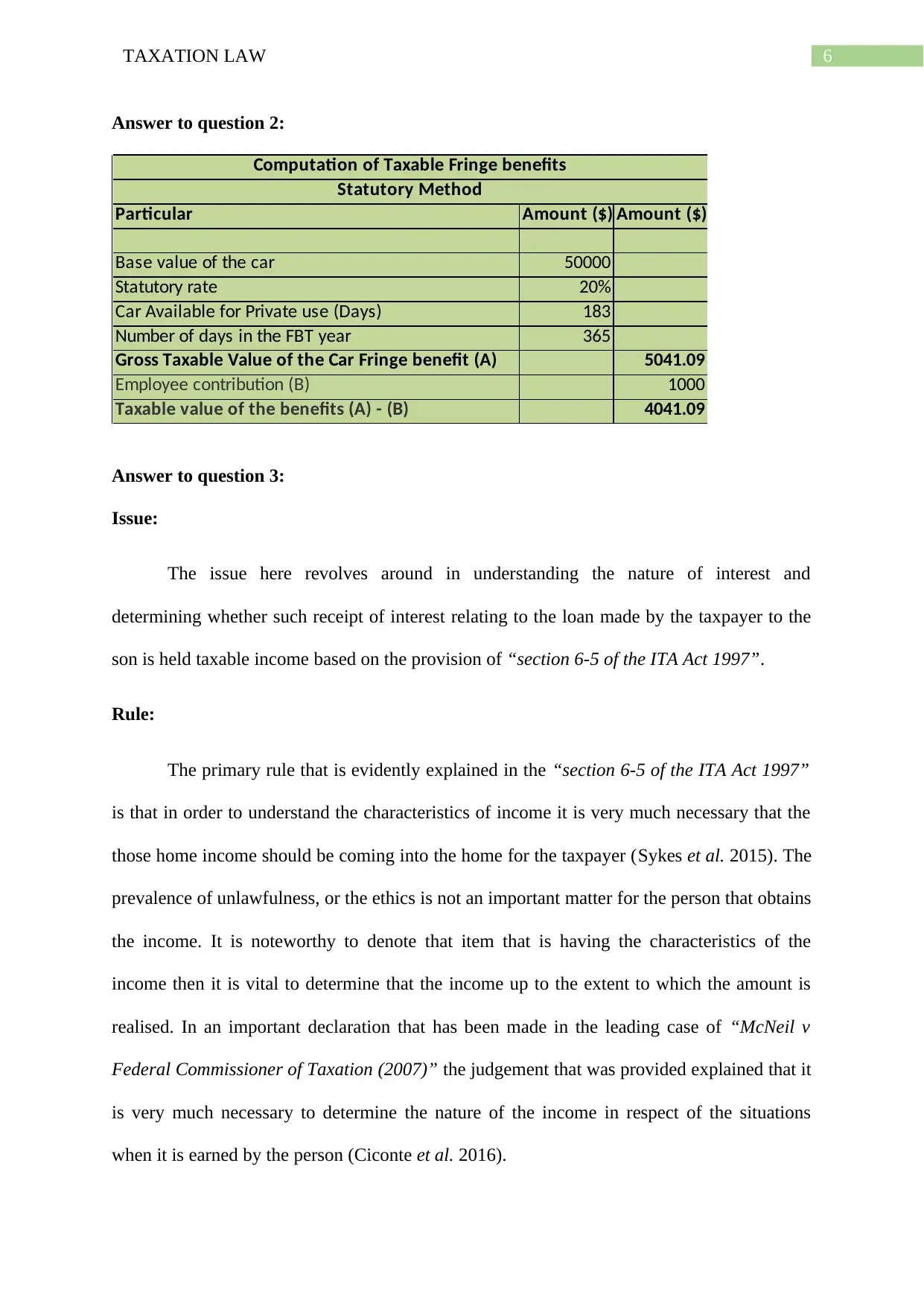

Answer to question 2:

Particular Amount ($) Amount ($)

Base value of the car 50000

Statutory rate 20%

Car Available for Private use (Days) 183

Number of days in the FBT year 365

Gross Taxable Value of the Car Fringe benefit (A) 5041.09

Employee contribution (B) 1000

Taxable value of the benefits (A) - (B) 4041.09

Computation of Taxable Fringe benefits

Statutory Method

Answer to question 3:

Issue:

The issue here revolves around in understanding the nature of interest and

determining whether such receipt of interest relating to the loan made by the taxpayer to the

son is held taxable income based on the provision of “section 6-5 of the ITA Act 1997”.

Rule:

The primary rule that is evidently explained in the “section 6-5 of the ITA Act 1997”

is that in order to understand the characteristics of income it is very much necessary that the

those home income should be coming into the home for the taxpayer (Sykes et al. 2015). The

prevalence of unlawfulness, or the ethics is not an important matter for the person that obtains

the income. It is noteworthy to denote that item that is having the characteristics of the

income then it is vital to determine that the income up to the extent to which the amount is

realised. In an important declaration that has been made in the leading case of “McNeil v

Federal Commissioner of Taxation (2007)” the judgement that was provided explained that it

is very much necessary to determine the nature of the income in respect of the situations

when it is earned by the person (Ciconte et al. 2016).

Answer to question 2:

Particular Amount ($) Amount ($)

Base value of the car 50000

Statutory rate 20%

Car Available for Private use (Days) 183

Number of days in the FBT year 365

Gross Taxable Value of the Car Fringe benefit (A) 5041.09

Employee contribution (B) 1000

Taxable value of the benefits (A) - (B) 4041.09

Computation of Taxable Fringe benefits

Statutory Method

Answer to question 3:

Issue:

The issue here revolves around in understanding the nature of interest and

determining whether such receipt of interest relating to the loan made by the taxpayer to the

son is held taxable income based on the provision of “section 6-5 of the ITA Act 1997”.

Rule:

The primary rule that is evidently explained in the “section 6-5 of the ITA Act 1997”

is that in order to understand the characteristics of income it is very much necessary that the

those home income should be coming into the home for the taxpayer (Sykes et al. 2015). The

prevalence of unlawfulness, or the ethics is not an important matter for the person that obtains

the income. It is noteworthy to denote that item that is having the characteristics of the

income then it is vital to determine that the income up to the extent to which the amount is

realised. In an important declaration that has been made in the leading case of “McNeil v

Federal Commissioner of Taxation (2007)” the judgement that was provided explained that it

is very much necessary to determine the nature of the income in respect of the situations

when it is earned by the person (Ciconte et al. 2016).

7TAXATION LAW

The necessary explanation was also made by the court by providing the necessary

declaration in the leading case of “Hochstrasser v Mayes (1960)” that an individual is under

the obligations of classifying the income that is having the vital characteristics of gain

(Stiglitz and Rosengard 2015). It is noteworthy to denote that the decision that was stated by

the court relatively provided an explanation that there is no type of gain until and unless the

item is beneficially derived by a person.

Application:

In the instances that is gained from going through the case study of the client it is

learnt that the parents in this case study has made loan to their son for the purpose of

developing house. It is worth mentioning that the parents did not charged with any kind of

interest from the son while the conditions of the loan contained that the son will repay the

principle amount of the loan inside the span of five years after taking such loan. In the later

evidences that has been gained following the study that the principle amount of the loan that

was made by the son was paid to the parents but only within the span of two years. The loan

principle amount was repaid but also accompanied the current market value interest for the

loan that was taken by the son. A reference should be made regarding the example of

“Federal Commissioner of Taxation v McNeil (2007)” that the amount of interest that was

paid by the son to the parents possessed the necessary characteristics of income (Auerbach

and Hassett 2015).

Taking into the consideration the evidences that has been made after making a

detailed analysis of the case is that the situation of “Hochstrasser v Mayes (1960)” can be

implemented to arrive at the decision that the interest that was obtained by the taxpayer has

the necessary element of the gain (Bronfenbrenner 2017). Taking into the considerations that

necessary explanation of the provision “6-5 of the ITA Act 1997” the interest that is obtained

The necessary explanation was also made by the court by providing the necessary

declaration in the leading case of “Hochstrasser v Mayes (1960)” that an individual is under

the obligations of classifying the income that is having the vital characteristics of gain

(Stiglitz and Rosengard 2015). It is noteworthy to denote that the decision that was stated by

the court relatively provided an explanation that there is no type of gain until and unless the

item is beneficially derived by a person.

Application:

In the instances that is gained from going through the case study of the client it is

learnt that the parents in this case study has made loan to their son for the purpose of

developing house. It is worth mentioning that the parents did not charged with any kind of

interest from the son while the conditions of the loan contained that the son will repay the

principle amount of the loan inside the span of five years after taking such loan. In the later

evidences that has been gained following the study that the principle amount of the loan that

was made by the son was paid to the parents but only within the span of two years. The loan

principle amount was repaid but also accompanied the current market value interest for the

loan that was taken by the son. A reference should be made regarding the example of

“Federal Commissioner of Taxation v McNeil (2007)” that the amount of interest that was

paid by the son to the parents possessed the necessary characteristics of income (Auerbach

and Hassett 2015).

Taking into the consideration the evidences that has been made after making a

detailed analysis of the case is that the situation of “Hochstrasser v Mayes (1960)” can be

implemented to arrive at the decision that the interest that was obtained by the taxpayer has

the necessary element of the gain (Bronfenbrenner 2017). Taking into the considerations that

necessary explanation of the provision “6-5 of the ITA Act 1997” the interest that is obtained

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8TAXATION LAW

by the parents will be classified as income with respect to the ordinary conceptions. The

taxpayer in the current case is not required to consider the principle amount of loan as income

because it was having the element of capital while the income that is received in the form

interest is necessary required to be held for assessment purpose (Stantcheva 2017). The

taxpayer is include those receipt of interest in the taxable income which is taxable under the

provision of “6-5 of the ITA Act 1997”.

Conclusion:

On arriving at the conclusion of the above stated case, it can be bought forward that

loan interest that was received by the taxpayer from son was carrying the necessary element

of income and taxable under “section 6-5 of the ITA Act 1997”.

Answer to question 4:

Answer to A:

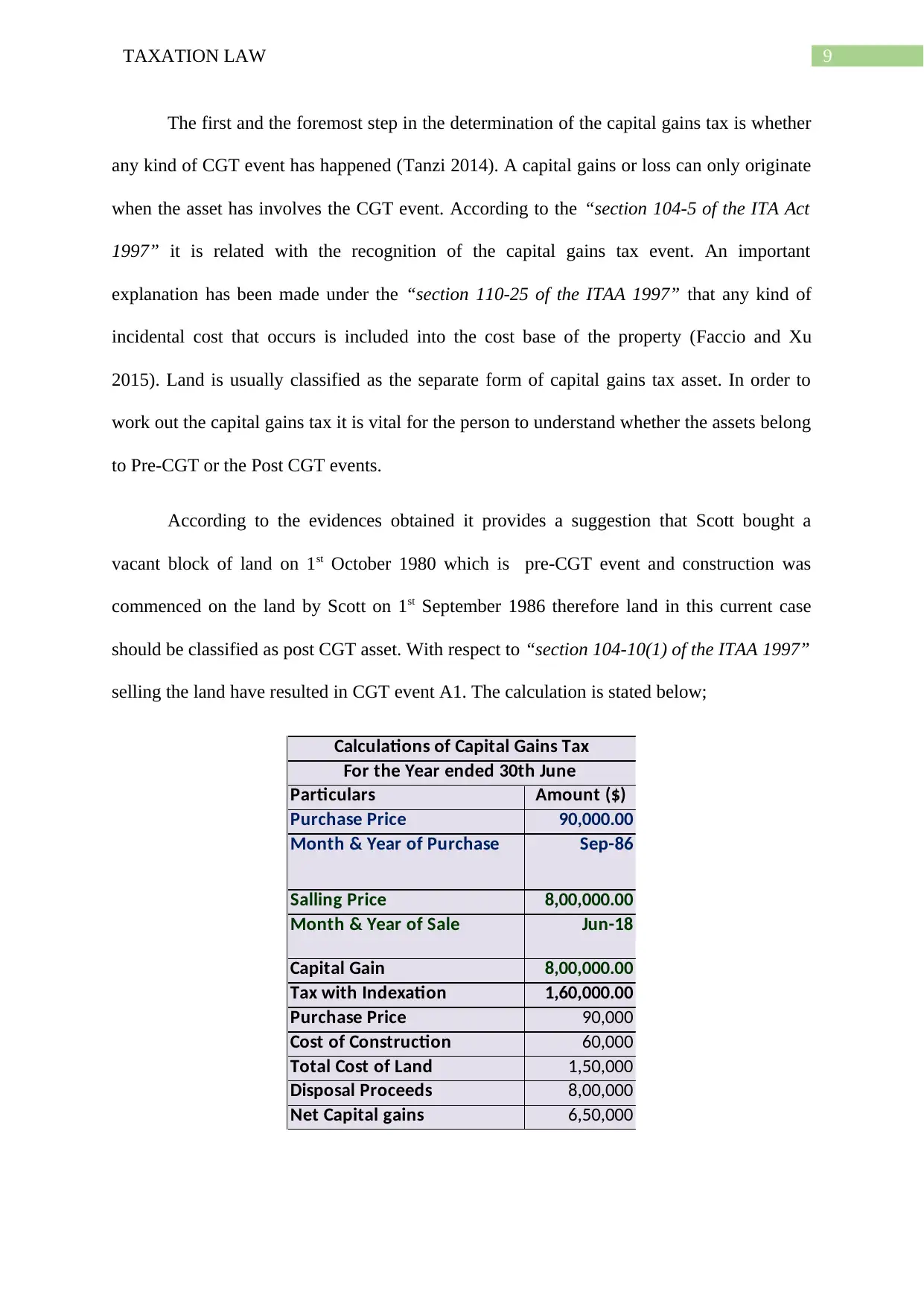

The situation opens with the conditions that Scott is owner of the vacant land that was

purchased by him on 1st September 1980. Later Scott, undertook the construction on the land

during 1st October 1986. The property was employed by Scott as the income producing

element and used the property for a period of thirty years before finally selling the property.

Capital gains tax is only applied to determine the assets that is obtained or acquired

during or after the 20 September 1985 (Jacob 2018). It is worth mentioning that the terms of

the pre-CGT and the Post CGT is used commonly for the assets that has been acquired after

the events or situations that are happening before or after the date. The system of capital

gains tax is based on the realised amount of capital gains or losses that is made from the sale

of the property or the assets or from any other specified events.

by the parents will be classified as income with respect to the ordinary conceptions. The

taxpayer in the current case is not required to consider the principle amount of loan as income

because it was having the element of capital while the income that is received in the form

interest is necessary required to be held for assessment purpose (Stantcheva 2017). The

taxpayer is include those receipt of interest in the taxable income which is taxable under the

provision of “6-5 of the ITA Act 1997”.

Conclusion:

On arriving at the conclusion of the above stated case, it can be bought forward that

loan interest that was received by the taxpayer from son was carrying the necessary element

of income and taxable under “section 6-5 of the ITA Act 1997”.

Answer to question 4:

Answer to A:

The situation opens with the conditions that Scott is owner of the vacant land that was

purchased by him on 1st September 1980. Later Scott, undertook the construction on the land

during 1st October 1986. The property was employed by Scott as the income producing

element and used the property for a period of thirty years before finally selling the property.

Capital gains tax is only applied to determine the assets that is obtained or acquired

during or after the 20 September 1985 (Jacob 2018). It is worth mentioning that the terms of

the pre-CGT and the Post CGT is used commonly for the assets that has been acquired after

the events or situations that are happening before or after the date. The system of capital

gains tax is based on the realised amount of capital gains or losses that is made from the sale

of the property or the assets or from any other specified events.

9TAXATION LAW

The first and the foremost step in the determination of the capital gains tax is whether

any kind of CGT event has happened (Tanzi 2014). A capital gains or loss can only originate

when the asset has involves the CGT event. According to the “section 104-5 of the ITA Act

1997” it is related with the recognition of the capital gains tax event. An important

explanation has been made under the “section 110-25 of the ITAA 1997” that any kind of

incidental cost that occurs is included into the cost base of the property (Faccio and Xu

2015). Land is usually classified as the separate form of capital gains tax asset. In order to

work out the capital gains tax it is vital for the person to understand whether the assets belong

to Pre-CGT or the Post CGT events.

According to the evidences obtained it provides a suggestion that Scott bought a

vacant block of land on 1st October 1980 which is pre-CGT event and construction was

commenced on the land by Scott on 1st September 1986 therefore land in this current case

should be classified as post CGT asset. With respect to “section 104-10(1) of the ITAA 1997”

selling the land have resulted in CGT event A1. The calculation is stated below;

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Tax with Indexation 1,60,000.00

Purchase Price 90,000

Cost of Construction 60,000

Total Cost of Land 1,50,000

Disposal Proceeds 8,00,000

Net Capital gains 6,50,000

Calculations of Capital Gains Tax

For the Year ended 30th June

The first and the foremost step in the determination of the capital gains tax is whether

any kind of CGT event has happened (Tanzi 2014). A capital gains or loss can only originate

when the asset has involves the CGT event. According to the “section 104-5 of the ITA Act

1997” it is related with the recognition of the capital gains tax event. An important

explanation has been made under the “section 110-25 of the ITAA 1997” that any kind of

incidental cost that occurs is included into the cost base of the property (Faccio and Xu

2015). Land is usually classified as the separate form of capital gains tax asset. In order to

work out the capital gains tax it is vital for the person to understand whether the assets belong

to Pre-CGT or the Post CGT events.

According to the evidences obtained it provides a suggestion that Scott bought a

vacant block of land on 1st October 1980 which is pre-CGT event and construction was

commenced on the land by Scott on 1st September 1986 therefore land in this current case

should be classified as post CGT asset. With respect to “section 104-10(1) of the ITAA 1997”

selling the land have resulted in CGT event A1. The calculation is stated below;

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Tax with Indexation 1,60,000.00

Purchase Price 90,000

Cost of Construction 60,000

Total Cost of Land 1,50,000

Disposal Proceeds 8,00,000

Net Capital gains 6,50,000

Calculations of Capital Gains Tax

For the Year ended 30th June

10TAXATION LAW

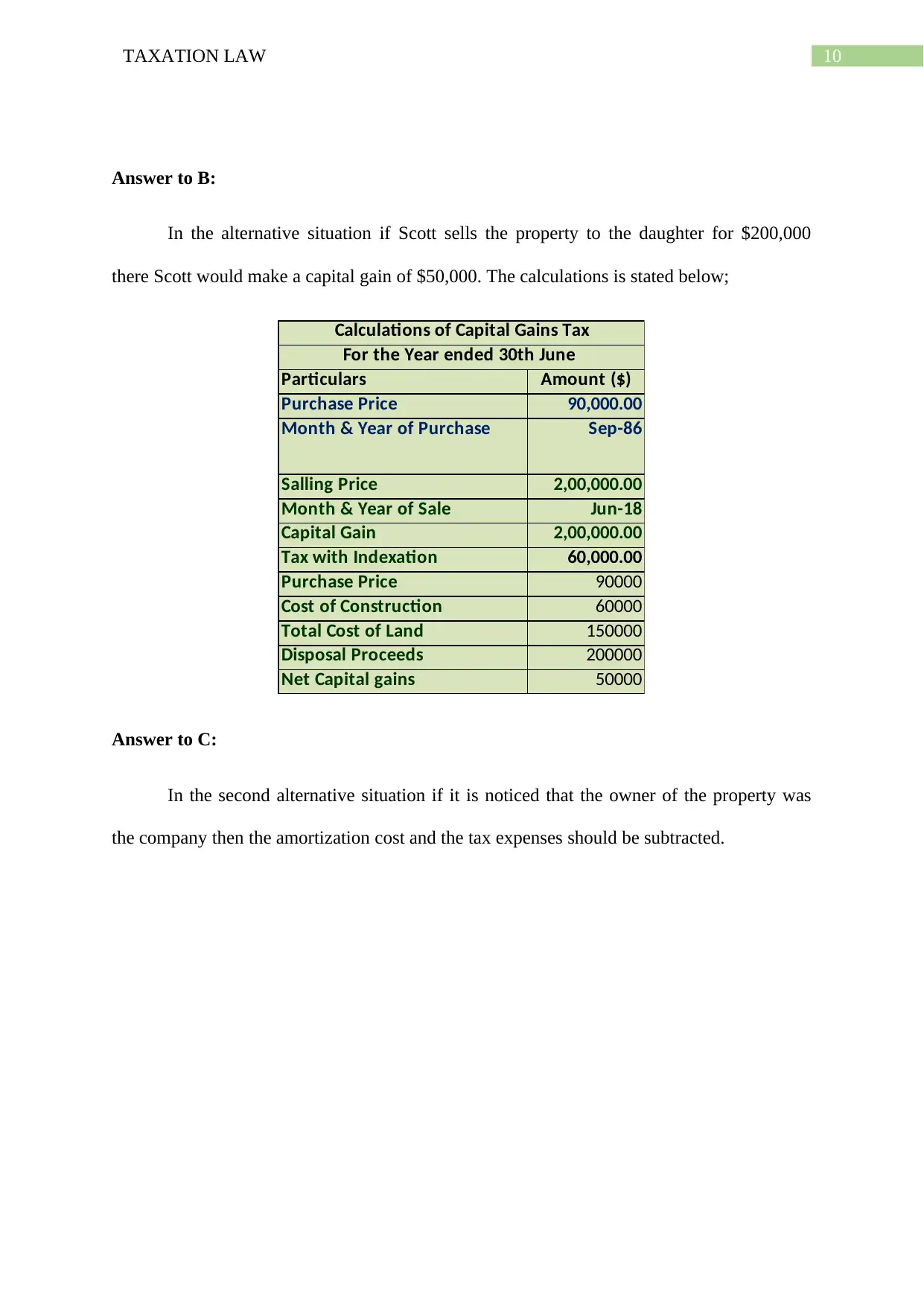

Answer to B:

In the alternative situation if Scott sells the property to the daughter for $200,000

there Scott would make a capital gain of $50,000. The calculations is stated below;

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 2,00,000.00

Month & Year of Sale Jun-18

Capital Gain 2,00,000.00

Tax with Indexation 60,000.00

Purchase Price 90000

Cost of Construction 60000

Total Cost of Land 150000

Disposal Proceeds 200000

Net Capital gains 50000

Calculations of Capital Gains Tax

For the Year ended 30th June

Answer to C:

In the second alternative situation if it is noticed that the owner of the property was

the company then the amortization cost and the tax expenses should be subtracted.

Answer to B:

In the alternative situation if Scott sells the property to the daughter for $200,000

there Scott would make a capital gain of $50,000. The calculations is stated below;

Particulars Amount ($)

Purchase Price 90,000.00

Month & Year of Purchase Sep-86

Salling Price 2,00,000.00

Month & Year of Sale Jun-18

Capital Gain 2,00,000.00

Tax with Indexation 60,000.00

Purchase Price 90000

Cost of Construction 60000

Total Cost of Land 150000

Disposal Proceeds 200000

Net Capital gains 50000

Calculations of Capital Gains Tax

For the Year ended 30th June

Answer to C:

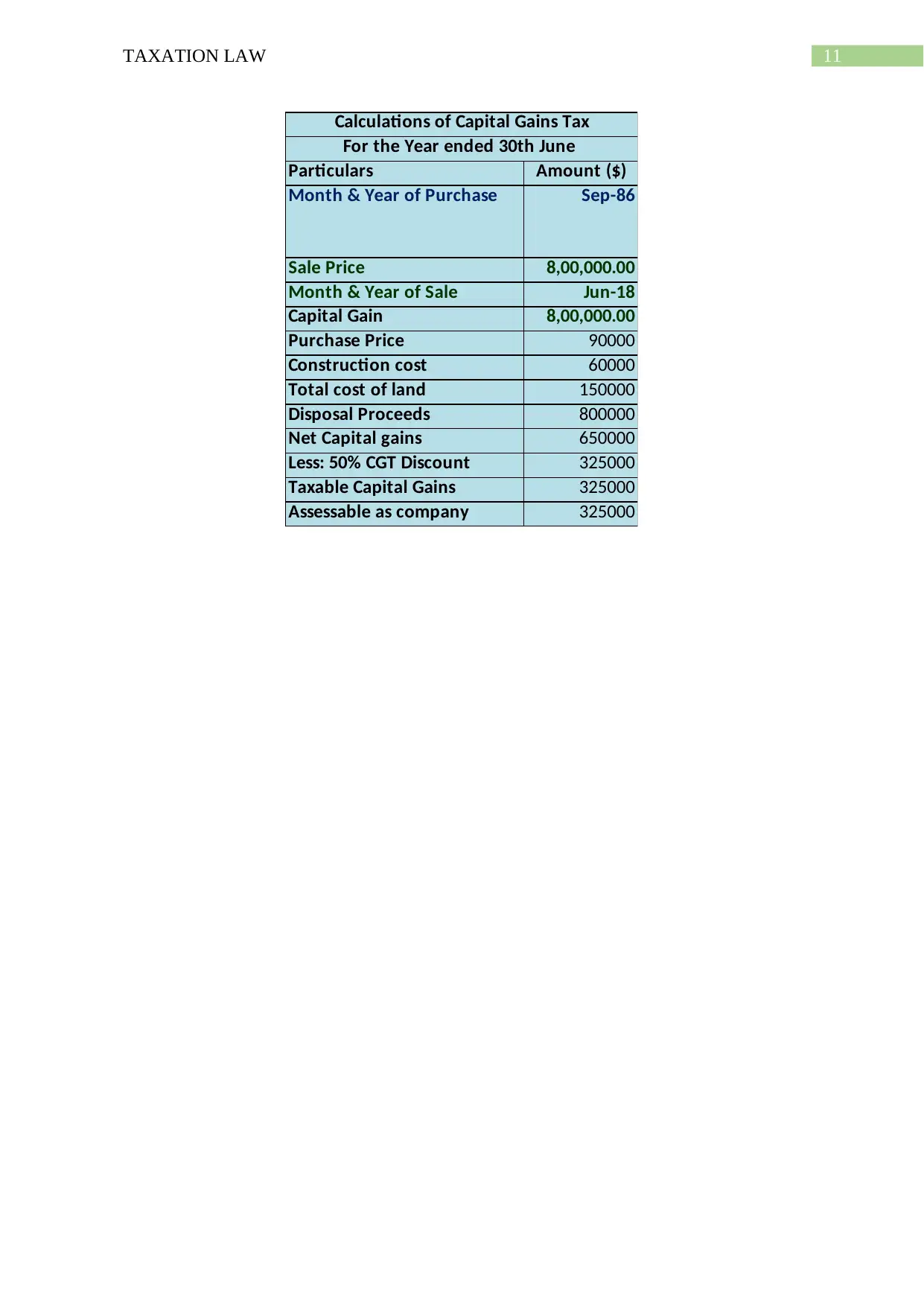

In the second alternative situation if it is noticed that the owner of the property was

the company then the amortization cost and the tax expenses should be subtracted.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11TAXATION LAW

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

Particulars Amount ($)

Month & Year of Purchase Sep-86

Sale Price 8,00,000.00

Month & Year of Sale Jun-18

Capital Gain 8,00,000.00

Purchase Price 90000

Construction cost 60000

Total cost of land 150000

Disposal Proceeds 800000

Net Capital gains 650000

Less: 50% CGT Discount 325000

Taxable Capital Gains 325000

Assessable as company 325000

Calculations of Capital Gains Tax

For the Year ended 30th June

12TAXATION LAW

Reference List:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bronfenbrenner, M., 2017. Income distribution theory. Routledge.

Ciconte, W., Donohoe, M., Lisowsky, P. and Mayberry, M., 2016. Predictable uncertainty:

The relation between unrecognized tax benefits and future income tax cash outflows.

Contractor, F.J., 2016. Tax avoidance by multinational companies: Methods, policies, and

ethics.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Mintz, J., 2016. Taxes, Royalties and Cross-Border Investments. International Taxation and

the Extractive Industries.

Peiros, K. and Smyth, C., 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), p.394.

Smith, J.P., 2015. Australian state income taxation: a historical perspective. Austl. Tax F., 30,

p.679.

Stantcheva, S., 2017. Optimal taxation and human capital policies over the life cycle. Journal

of Political Economy, 125(6), pp.1931-1990.

Reference List:

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Bronfenbrenner, M., 2017. Income distribution theory. Routledge.

Ciconte, W., Donohoe, M., Lisowsky, P. and Mayberry, M., 2016. Predictable uncertainty:

The relation between unrecognized tax benefits and future income tax cash outflows.

Contractor, F.J., 2016. Tax avoidance by multinational companies: Methods, policies, and

ethics.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Mintz, J., 2016. Taxes, Royalties and Cross-Border Investments. International Taxation and

the Extractive Industries.

Peiros, K. and Smyth, C., 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), p.394.

Smith, J.P., 2015. Australian state income taxation: a historical perspective. Austl. Tax F., 30,

p.679.

Stantcheva, S., 2017. Optimal taxation and human capital policies over the life cycle. Journal

of Political Economy, 125(6), pp.1931-1990.

13TAXATION LAW

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Sykes, J., Križ, K., Edin, K. and Halpern-Meekin, S., 2015. Dignity and dreams: What the

Earned Income Tax Credit (EITC) means to low-income families. American Sociological

Review, 80(2), pp.243-267.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

Travers, G., 2014. Personal services income. Tax Adviser's Guide to Part IVA: A Practical

Guide to the Application of the General Anti-avoidance Rule, The, p.49.

Van Rensburg, E.J., 2015. The origins and development of the general deduction formula in

income tax legislation of the Cape Colony. SA Mercantile Law Journal= SA Tydskrif vir

Handelsreg, 27(1), pp.92-127.

Stiglitz, J.E. and Rosengard, J.K., 2015. Economics of the Public Sector: Fourth International

Student Edition. WW Norton & Company.

Sykes, J., Križ, K., Edin, K. and Halpern-Meekin, S., 2015. Dignity and dreams: What the

Earned Income Tax Credit (EITC) means to low-income families. American Sociological

Review, 80(2), pp.243-267.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

Travers, G., 2014. Personal services income. Tax Adviser's Guide to Part IVA: A Practical

Guide to the Application of the General Anti-avoidance Rule, The, p.49.

Van Rensburg, E.J., 2015. The origins and development of the general deduction formula in

income tax legislation of the Cape Colony. SA Mercantile Law Journal= SA Tydskrif vir

Handelsreg, 27(1), pp.92-127.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.