Taxation Law: Income Assessment, CGT, and Fringe Benefits - HA3042

VerifiedAdded on 2023/06/12

|11

|2226

|398

Homework Assignment

AI Summary

This assignment solution delves into various aspects of taxation law, addressing questions related to assessable income, capital gains tax (CGT), and fringe benefits tax (FBT). It examines whether monies received by a mountain climber for her life story and related publications constitute assessable income under Section 6-5 of the ITAA 1997, applying relevant case law such as Scott v Commissioner of Taxation and Federal Commissioner of Taxation v Brent. The assignment also calculates taxable fringe benefits using the statutory method and analyzes the tax implications of an interest-free loan made to a family member. Furthermore, it discusses the CGT implications of selling land purchased before 1985, referencing Section 105-55 (2) of the ITAA 1997. The document provides detailed explanations and legal references to support its conclusions, offering a comprehensive overview of the taxation principles involved.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................5

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................7

Answer to A:..............................................................................................................................7

Answer to B:..............................................................................................................................7

Answer to C:..............................................................................................................................8

Reference List:.........................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................5

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................7

Answer to A:..............................................................................................................................7

Answer to B:..............................................................................................................................7

Answer to C:..............................................................................................................................8

Reference List:.........................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Are the monies that are received by the taxpayer for the exclusive media publications

assessable income under “section 6-5 of the ITAA 1997”?

Rule:

As stated under the “section 6-1 of the ITAA 1936” income derived from the personal

exertion or the income that is earned from the personal exertion represents the income that

includes wages, salaries, commissions, fees, bonuses, pensions, gratuities which is received

by the persons or the proceeds that is obtained by an individual for the business carried on.

According to the “section 6-1 of the ITAA 1997” an individual that derives the amount from

the personal exertion is held as income which is included in the taxable income as the

statutory or the ordinary income (Woellner et al. 2016).

Under “section 6-5 of the ITAA 1997” taxable income comprises of the income in

accordance with the ordinary concepts. Usually most of the income that comes in to the

taxpayer is held as ordinary income (Mumford 2017). The commissioner in “Scott v

Commissioner of Taxation (1935)” explained that receipts must be treated as income and

should be determined in agreement with the ordinary income concepts.

Payments that are received for media publications may or may not be held as the

taxable income. A reward relating to the provision of service is dependent facts of the

particular case (Pogge and Mehta 2016). This includes that the quantum of the payment that

is made to the taxpayer should be significant and should not merely be the nominal amount to

just cover the cost or inconvenience of the taxpayer. The taxpayer is required to provide the

service in order to receive the money.

Answer to question 1:

Issues:

Are the monies that are received by the taxpayer for the exclusive media publications

assessable income under “section 6-5 of the ITAA 1997”?

Rule:

As stated under the “section 6-1 of the ITAA 1936” income derived from the personal

exertion or the income that is earned from the personal exertion represents the income that

includes wages, salaries, commissions, fees, bonuses, pensions, gratuities which is received

by the persons or the proceeds that is obtained by an individual for the business carried on.

According to the “section 6-1 of the ITAA 1997” an individual that derives the amount from

the personal exertion is held as income which is included in the taxable income as the

statutory or the ordinary income (Woellner et al. 2016).

Under “section 6-5 of the ITAA 1997” taxable income comprises of the income in

accordance with the ordinary concepts. Usually most of the income that comes in to the

taxpayer is held as ordinary income (Mumford 2017). The commissioner in “Scott v

Commissioner of Taxation (1935)” explained that receipts must be treated as income and

should be determined in agreement with the ordinary income concepts.

Payments that are received for media publications may or may not be held as the

taxable income. A reward relating to the provision of service is dependent facts of the

particular case (Pogge and Mehta 2016). This includes that the quantum of the payment that

is made to the taxpayer should be significant and should not merely be the nominal amount to

just cover the cost or inconvenience of the taxpayer. The taxpayer is required to provide the

service in order to receive the money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

To support the treatment of the payment as the income it can be noticed in the case of

“Federal Commissioner of Taxation v Brent (1971) ATC 4195” (Jones and Rhoades-

Catanach 2015). It was noticed in the case that the wife of the greatest robber of train was

held by the commissioner of taxation to have obtained the taxation income when she was

awarded with money of telling the story of her life to the newspaper publications.

In another example the decision that was made in the case of “Housden (Inspector of

Taxes v Marshall (1958)” the taxpayer in an agreement decided to make the experiences as

the Jockey available (Barkoczy 2016). This included the taxpayer’s photographs and the

newspaper articles cuttings. The amount that was received constituted reward for personal

service which is taxable under “section 6-5 of the ITAA 1997” as income from ordinary

concepts.

Income that are derived from the sale of the autobiographies are regarded as the

royalties’ income. According to the decision that was made in the case of “Hobbs v Hussy

(1942) TC 153)” the taxpayer who was apparently considered as one of the notorious

criminal received an amount of £1500 for the serial rights of the autobiographies that was

published in the newspaper (Christie 2015). Therefore, it can be stated that amount derived

constituted royalty income which was taxable under ordinary concept of “section 6-5 of the

ITAA 1997”.

Applications:

The case scenario that is obtained from the case study suggest that Hilary was the

famous mountain climber. On being approached by the local Newspaper she agreed to write

the book and the sell the interest to the newspaper company. After the services were rendered

the newspaper company paid Hilary with a sum of $10,000. Citing the reference of “Scott v

Commissioner of Taxation (1935)” the receipts must be treated as income and should be

To support the treatment of the payment as the income it can be noticed in the case of

“Federal Commissioner of Taxation v Brent (1971) ATC 4195” (Jones and Rhoades-

Catanach 2015). It was noticed in the case that the wife of the greatest robber of train was

held by the commissioner of taxation to have obtained the taxation income when she was

awarded with money of telling the story of her life to the newspaper publications.

In another example the decision that was made in the case of “Housden (Inspector of

Taxes v Marshall (1958)” the taxpayer in an agreement decided to make the experiences as

the Jockey available (Barkoczy 2016). This included the taxpayer’s photographs and the

newspaper articles cuttings. The amount that was received constituted reward for personal

service which is taxable under “section 6-5 of the ITAA 1997” as income from ordinary

concepts.

Income that are derived from the sale of the autobiographies are regarded as the

royalties’ income. According to the decision that was made in the case of “Hobbs v Hussy

(1942) TC 153)” the taxpayer who was apparently considered as one of the notorious

criminal received an amount of £1500 for the serial rights of the autobiographies that was

published in the newspaper (Christie 2015). Therefore, it can be stated that amount derived

constituted royalty income which was taxable under ordinary concept of “section 6-5 of the

ITAA 1997”.

Applications:

The case scenario that is obtained from the case study suggest that Hilary was the

famous mountain climber. On being approached by the local Newspaper she agreed to write

the book and the sell the interest to the newspaper company. After the services were rendered

the newspaper company paid Hilary with a sum of $10,000. Citing the reference of “Scott v

Commissioner of Taxation (1935)” the receipts must be treated as income and should be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

determined in agreement with the ordinary income concepts (Sharkey and Murray 2016).

With reference to “section 6-1 of the ITAA 1997” the amount of $10,000 that was obtained

from the newspaper company was an income from the personal exertion.

Additionally, the quantum of the payment that is made to Hilary was be significant.

Hilary was required to provide the service in order to receive the money. To support the

treatment of the payment as the income reference can be made to the case of “Federal

Commissioner of Taxation v Brent (1971) ATC 4195” where the amount for narrating the

story of her life to the newspaper publications (De Wispelaere and Pacolet 2015).

In later instances it was noticed that payment of $5,000 and $2,000 was received by

Hilary for the selling the photographs and manuscripts would be classified as income from

personal exertion as well (Lang 2014). Mentioning the reference to the court’s decision in

“Housden (Inspector of Taxes v Marshall (1958)” the payment that was received would be

held as ordinary income and it is taxable under “section 6-5 of the ITAA 1997” as income

from ordinary concepts.

Considering an alternative decision of writing the book is undertaken by Hilary the

receipts of money from the sale of boo would be classified as the royalty income. By

referring to the case of “Hobbs v Hussy (1942) TC 153)” sale of books written by her would

lead to autobiographies and income derived would be held as royalty income which was

taxable under ordinary concept of “section 6-5 of the ITAA 1997” (Fleurbaey and Maniquet

2017).

Conclusion:

Accordingly, in the above stated case of Hilary the income earned would be classified

as the personal exertion income for the providing the personal service. The income would be

determined in agreement with the ordinary income concepts (Sharkey and Murray 2016).

With reference to “section 6-1 of the ITAA 1997” the amount of $10,000 that was obtained

from the newspaper company was an income from the personal exertion.

Additionally, the quantum of the payment that is made to Hilary was be significant.

Hilary was required to provide the service in order to receive the money. To support the

treatment of the payment as the income reference can be made to the case of “Federal

Commissioner of Taxation v Brent (1971) ATC 4195” where the amount for narrating the

story of her life to the newspaper publications (De Wispelaere and Pacolet 2015).

In later instances it was noticed that payment of $5,000 and $2,000 was received by

Hilary for the selling the photographs and manuscripts would be classified as income from

personal exertion as well (Lang 2014). Mentioning the reference to the court’s decision in

“Housden (Inspector of Taxes v Marshall (1958)” the payment that was received would be

held as ordinary income and it is taxable under “section 6-5 of the ITAA 1997” as income

from ordinary concepts.

Considering an alternative decision of writing the book is undertaken by Hilary the

receipts of money from the sale of boo would be classified as the royalty income. By

referring to the case of “Hobbs v Hussy (1942) TC 153)” sale of books written by her would

lead to autobiographies and income derived would be held as royalty income which was

taxable under ordinary concept of “section 6-5 of the ITAA 1997” (Fleurbaey and Maniquet

2017).

Conclusion:

Accordingly, in the above stated case of Hilary the income earned would be classified

as the personal exertion income for the providing the personal service. The income would be

5TAXATION LAW

classified as income under ordinary concepts and taxable under “section 6-5 of the ITAA

1997”.

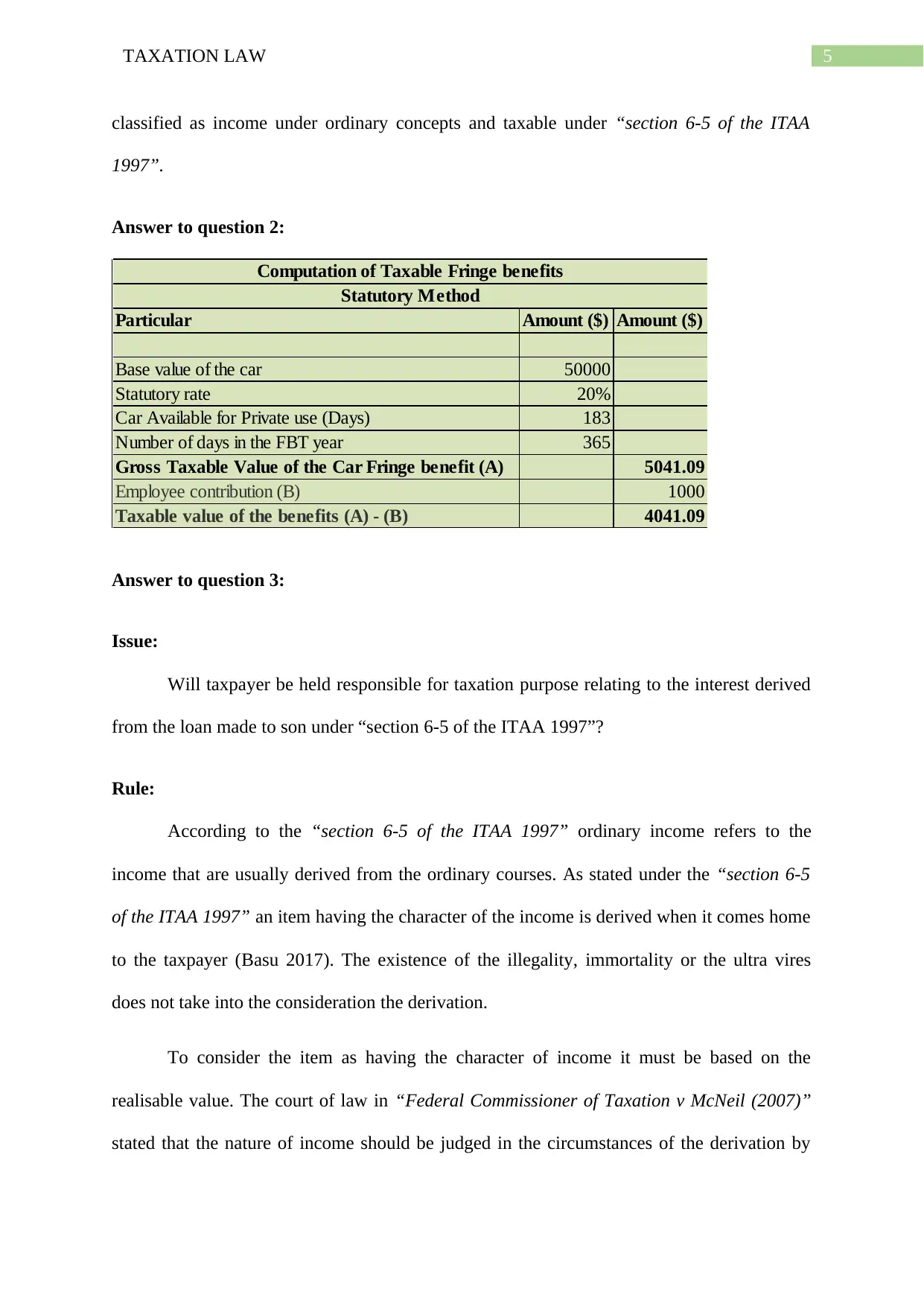

Answer to question 2:

Particular Amount ($) Amount ($)

Base value of the car 50000

Statutory rate 20%

Car Available for Private use (Days) 183

Number of days in the FBT year 365

Gross Taxable Value of the Car Fringe benefit (A) 5041.09

Employee contribution (B) 1000

Taxable value of the benefits (A) - (B) 4041.09

Computation of Taxable Fringe benefits

Statutory Method

Answer to question 3:

Issue:

Will taxpayer be held responsible for taxation purpose relating to the interest derived

from the loan made to son under “section 6-5 of the ITAA 1997”?

Rule:

According to the “section 6-5 of the ITAA 1997” ordinary income refers to the

income that are usually derived from the ordinary courses. As stated under the “section 6-5

of the ITAA 1997” an item having the character of the income is derived when it comes home

to the taxpayer (Basu 2017). The existence of the illegality, immortality or the ultra vires

does not take into the consideration the derivation.

To consider the item as having the character of income it must be based on the

realisable value. The court of law in “Federal Commissioner of Taxation v McNeil (2007)”

stated that the nature of income should be judged in the circumstances of the derivation by

classified as income under ordinary concepts and taxable under “section 6-5 of the ITAA

1997”.

Answer to question 2:

Particular Amount ($) Amount ($)

Base value of the car 50000

Statutory rate 20%

Car Available for Private use (Days) 183

Number of days in the FBT year 365

Gross Taxable Value of the Car Fringe benefit (A) 5041.09

Employee contribution (B) 1000

Taxable value of the benefits (A) - (B) 4041.09

Computation of Taxable Fringe benefits

Statutory Method

Answer to question 3:

Issue:

Will taxpayer be held responsible for taxation purpose relating to the interest derived

from the loan made to son under “section 6-5 of the ITAA 1997”?

Rule:

According to the “section 6-5 of the ITAA 1997” ordinary income refers to the

income that are usually derived from the ordinary courses. As stated under the “section 6-5

of the ITAA 1997” an item having the character of the income is derived when it comes home

to the taxpayer (Basu 2017). The existence of the illegality, immortality or the ultra vires

does not take into the consideration the derivation.

To consider the item as having the character of income it must be based on the

realisable value. The court of law in “Federal Commissioner of Taxation v McNeil (2007)”

stated that the nature of income should be judged in the circumstances of the derivation by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

the taxpayer (Fleurbaey and Maniquet 2017). In another example of “Hochsrasser v Mayes

(1960)” the court stated that to possess the character of income it should have the nature of

gain for the taxpayer that derives it. There cannot be any form of gain unless the taxpayer

derives it beneficially.

Applications:

As evident in the current situation, it was noticed that she made an interest free loan to

the son for commercial house purpose. The agreed term of loan repayment was five years by

the son. But it was later noticed that the loan was repaid by the son inside the span of two

years and also paid the parent with the interest amount.

Referring to the explanation stated in the case of “Federal Commissioner of Taxation

v McNeil (2007)” it is necessary to determine the nature of interest that is received by the

parent. Citing the decision that has been made in the case of “Hochsrasser v Mayes (1960)”

the interest derived from the loan by the parent was regarded as having the character of

income (De Wispelaere and Pacolet 2015). The interest income that was received by the

mother had the nature of gain for the taxpayer since it was derived beneficially. Therefore,

the amount that was derived by the mother was regarded as income under the ordinary

concepts which is taxable under “section 6-5 of the ITAA 1997”. However, the loan principle

cannot be classified as having the nature of income since it was capital in nature.

Conclusion:

The amount of interest will be considered taxable under “section 6-5 of the ITAA

1997” since it constituted gain. The amount would be held as income derived from the

ordinary concepts.

the taxpayer (Fleurbaey and Maniquet 2017). In another example of “Hochsrasser v Mayes

(1960)” the court stated that to possess the character of income it should have the nature of

gain for the taxpayer that derives it. There cannot be any form of gain unless the taxpayer

derives it beneficially.

Applications:

As evident in the current situation, it was noticed that she made an interest free loan to

the son for commercial house purpose. The agreed term of loan repayment was five years by

the son. But it was later noticed that the loan was repaid by the son inside the span of two

years and also paid the parent with the interest amount.

Referring to the explanation stated in the case of “Federal Commissioner of Taxation

v McNeil (2007)” it is necessary to determine the nature of interest that is received by the

parent. Citing the decision that has been made in the case of “Hochsrasser v Mayes (1960)”

the interest derived from the loan by the parent was regarded as having the character of

income (De Wispelaere and Pacolet 2015). The interest income that was received by the

mother had the nature of gain for the taxpayer since it was derived beneficially. Therefore,

the amount that was derived by the mother was regarded as income under the ordinary

concepts which is taxable under “section 6-5 of the ITAA 1997”. However, the loan principle

cannot be classified as having the nature of income since it was capital in nature.

Conclusion:

The amount of interest will be considered taxable under “section 6-5 of the ITAA

1997” since it constituted gain. The amount would be held as income derived from the

ordinary concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

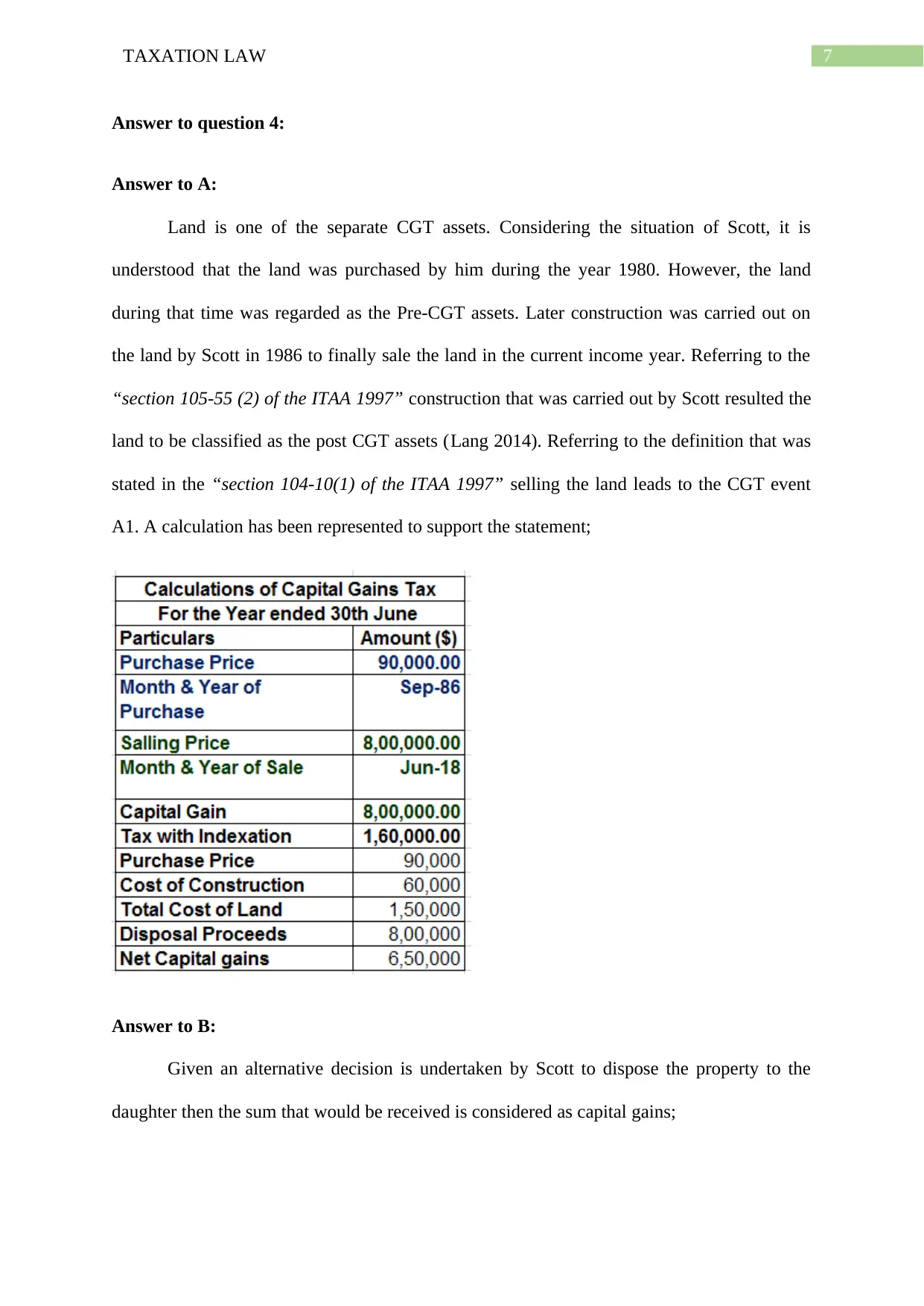

Answer to question 4:

Answer to A:

Land is one of the separate CGT assets. Considering the situation of Scott, it is

understood that the land was purchased by him during the year 1980. However, the land

during that time was regarded as the Pre-CGT assets. Later construction was carried out on

the land by Scott in 1986 to finally sale the land in the current income year. Referring to the

“section 105-55 (2) of the ITAA 1997” construction that was carried out by Scott resulted the

land to be classified as the post CGT assets (Lang 2014). Referring to the definition that was

stated in the “section 104-10(1) of the ITAA 1997” selling the land leads to the CGT event

A1. A calculation has been represented to support the statement;

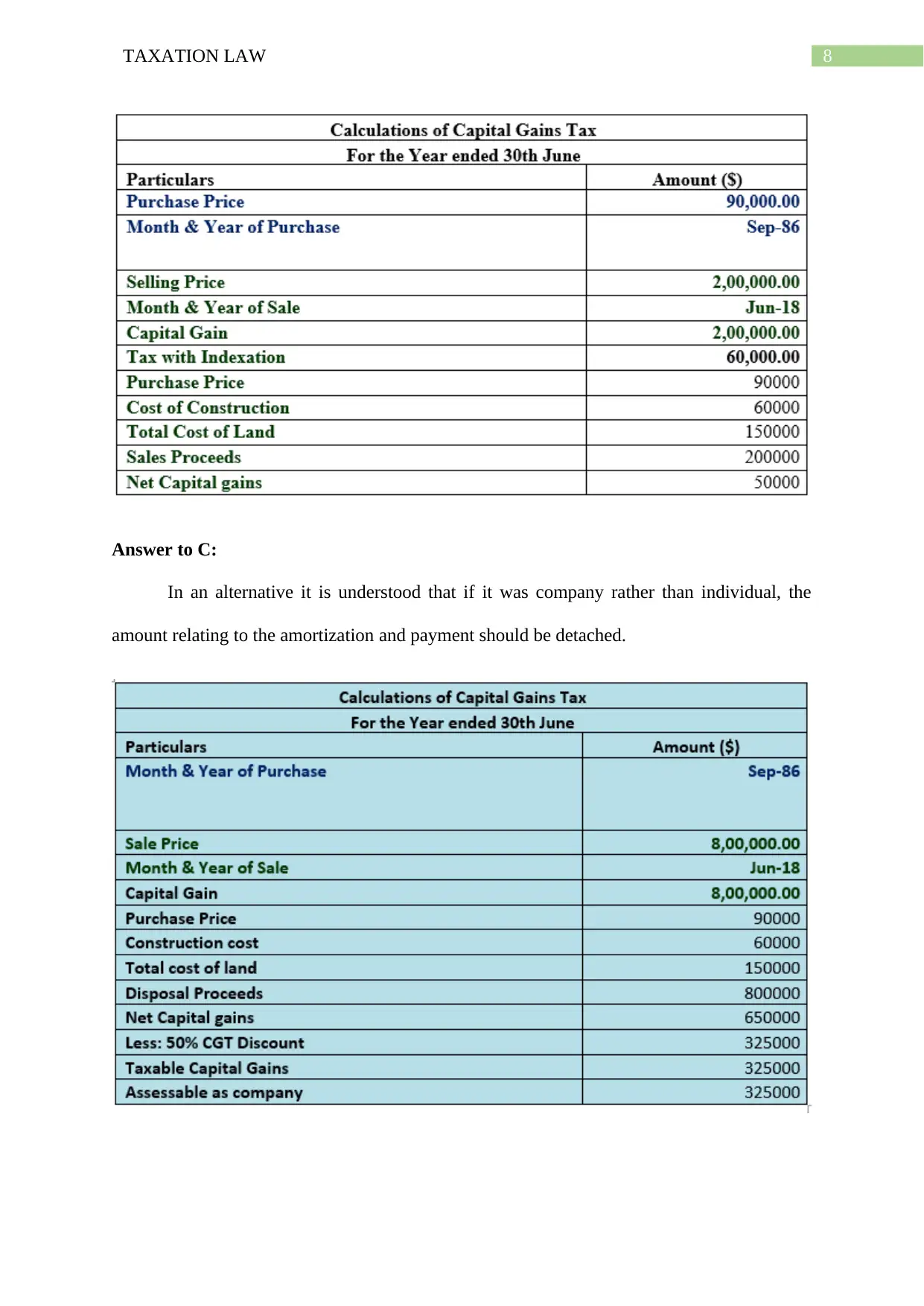

Answer to B:

Given an alternative decision is undertaken by Scott to dispose the property to the

daughter then the sum that would be received is considered as capital gains;

Answer to question 4:

Answer to A:

Land is one of the separate CGT assets. Considering the situation of Scott, it is

understood that the land was purchased by him during the year 1980. However, the land

during that time was regarded as the Pre-CGT assets. Later construction was carried out on

the land by Scott in 1986 to finally sale the land in the current income year. Referring to the

“section 105-55 (2) of the ITAA 1997” construction that was carried out by Scott resulted the

land to be classified as the post CGT assets (Lang 2014). Referring to the definition that was

stated in the “section 104-10(1) of the ITAA 1997” selling the land leads to the CGT event

A1. A calculation has been represented to support the statement;

Answer to B:

Given an alternative decision is undertaken by Scott to dispose the property to the

daughter then the sum that would be received is considered as capital gains;

8TAXATION LAW

Answer to C:

In an alternative it is understood that if it was company rather than individual, the

amount relating to the amortization and payment should be detached.

Answer to C:

In an alternative it is understood that if it was company rather than individual, the

amount relating to the amortization and payment should be detached.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Basu, S., 2017. International Direct Taxation and E-Commerce: A Catalyst for

Reform. NUJS L. Rev., 10, p.19.

Christie, M., 2015. Principles of Taxation Law 2015.

De Wispelaere, F. and Pacolet, J., 2015. Posting of workers: the impact of social security

coordination and income taxation law on welfare states.

Fleurbaey, M. and Maniquet, F., 2017. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature.

Herdegen, M., 2016. Principles of international economic law. Oxford University Press.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law principles. Austl.

Tax F., 31, p.63.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Basu, S., 2017. International Direct Taxation and E-Commerce: A Catalyst for

Reform. NUJS L. Rev., 10, p.19.

Christie, M., 2015. Principles of Taxation Law 2015.

De Wispelaere, F. and Pacolet, J., 2015. Posting of workers: the impact of social security

coordination and income taxation law on welfare states.

Fleurbaey, M. and Maniquet, F., 2017. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature.

Herdegen, M., 2016. Principles of international economic law. Oxford University Press.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Pogge, T. and Mehta, K. eds., 2016. Global tax fairness. Oxford University Press.

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law principles. Austl.

Tax F., 31, p.63.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.