GST and Business Tax Calculations

VerifiedAdded on 2020/03/28

|13

|1825

|447

AI Summary

This taxation assignment involves several problem-solving tasks. It requires applying the Goods and Services Tax (GST) ruling 'GSTR 2006/3' to a scenario involving Big Bank Ltd.'s advertisement expenses. Further, it demands calculating Angelo's taxable income and the net income of a partnership. The document includes detailed explanations and computations for each task.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Answer to question 1.4:..............................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Answer to question 1.4:..............................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

2TAXATION LAW

Rule:...........................................................................................................................................7

Applications:..............................................................................................................................7

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to question 4:...............................................................................................................10

References................................................................................................................................12

Rule:...........................................................................................................................................7

Applications:..............................................................................................................................7

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................8

Answer to question 4:...............................................................................................................10

References................................................................................................................................12

3TAXATION LAW

Answer to Question 1.1:

Issue:

Based on the given case the issue has been found in terms of whether allowable

deductions needs to be charged on moving the machine to a new location.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “British Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

The taxpayer needs to be entitled for the various types of allowable deductions which

have taken place as per the income accessible. Based on “Section 8-1 of the ITAA”, the

activity of moving the machine has been identified as an inflated cost of asset. Based on the

present condition it has been seen that the cost of moving the machine shall not be considered

under permissible deductions. The main rationale for it is due to increased asset cost.

As stated in “British Insulated & Helsby Cables”, the cost of transport lay down at

seven evidence by showing consistent advantage for the business enterprises in relocating the

depreciable asset/machinery in a new place. As per “Taxation ruling of TD 92/126” the cost

incurred at the outset of setting new machinery is considered as the revenue for the business

as this cost is generally considered under cost of capital and cannot be entitled for allowable

deductions (Pyrmont 2014).

Conclusion:

Henceforth, it can be discerned that the cost incurred in moving the machinery is not

entitled under allowable deduction as this kind of cost is considered under cost of capital.

Answer to Question 1.1:

Issue:

Based on the given case the issue has been found in terms of whether allowable

deductions needs to be charged on moving the machine to a new location.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “British Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

The taxpayer needs to be entitled for the various types of allowable deductions which

have taken place as per the income accessible. Based on “Section 8-1 of the ITAA”, the

activity of moving the machine has been identified as an inflated cost of asset. Based on the

present condition it has been seen that the cost of moving the machine shall not be considered

under permissible deductions. The main rationale for it is due to increased asset cost.

As stated in “British Insulated & Helsby Cables”, the cost of transport lay down at

seven evidence by showing consistent advantage for the business enterprises in relocating the

depreciable asset/machinery in a new place. As per “Taxation ruling of TD 92/126” the cost

incurred at the outset of setting new machinery is considered as the revenue for the business

as this cost is generally considered under cost of capital and cannot be entitled for allowable

deductions (Pyrmont 2014).

Conclusion:

Henceforth, it can be discerned that the cost incurred in moving the machinery is not

entitled under allowable deduction as this kind of cost is considered under cost of capital.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Answer to question 1.2:

Issue:

The main issue has been identified whether the revaluation of asset for the insurance

cover is to be entitled as per the permissible deductions as per “Section 8-1 of the ITAA

1997”.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

based on the present issue it can be certain that the cost of asset revaluation as a result

of insurance cover needs to be entitled for the allowable deductions as per “Section 8-1 of

the ITAA 1997” due to its repeatability in nature. The outlay incurred for the revaluation of

asset is further based on a straight-line method relating to the fixed asset. The cost incurred

signifies an impertinent nature of advantage which is predictive in nature henceforth it needs

to be considered for the deductions as per “Section 8-1 of the ITAA 1997” (Aktaev et al.

2015).

Conclusion:

as mentioned in the given case the cost for the revolution of asset new to the insurance

cover needs to be entitled for the deductions as per “Section 8-1 of the ITAA 1997”.

Answer to question 1.3:

Issue:

The given case raises the issue whether the legal expenditure incurred by individual

taxpayer for opposing the winding up of petition is to be considered for permissible

deductions.

Answer to question 1.2:

Issue:

The main issue has been identified whether the revaluation of asset for the insurance

cover is to be entitled as per the permissible deductions as per “Section 8-1 of the ITAA

1997”.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

based on the present issue it can be certain that the cost of asset revaluation as a result

of insurance cover needs to be entitled for the allowable deductions as per “Section 8-1 of

the ITAA 1997” due to its repeatability in nature. The outlay incurred for the revaluation of

asset is further based on a straight-line method relating to the fixed asset. The cost incurred

signifies an impertinent nature of advantage which is predictive in nature henceforth it needs

to be considered for the deductions as per “Section 8-1 of the ITAA 1997” (Aktaev et al.

2015).

Conclusion:

as mentioned in the given case the cost for the revolution of asset new to the insurance

cover needs to be entitled for the deductions as per “Section 8-1 of the ITAA 1997”.

Answer to question 1.3:

Issue:

The given case raises the issue whether the legal expenditure incurred by individual

taxpayer for opposing the winding up of petition is to be considered for permissible

deductions.

5TAXATION LAW

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

Based on the given issue it can be certain whether the winding up of businesses

usually treated as an outlay of the business function and not considered under “Section 8-1 of

the ITAA 1997” for the various types of allowable deductions. As stated in “Taxation

ruling of ID 2004/367” various types of the costs are legally related for execution of the

business operations and henceforth the cost borne by the taxpayer is used in producing

assessable income.

As per the “FC of T v Snowden and Wilson Pty Ltd (1958)”, the main form of

outlay of the expenses have taken place in the ordinary course of business and individual

taxpayer were needed to outlay that state of affairs to prevented any sort of expense which is

considered for admission or deduction (Barkoczy 2016).

Despite of the cost qualifying with the positive limbs, it cannot be held deductible due

to the fact that the expenses incurred owns the features associated to cost of capital.

Conclusion:

As noted from the aforementioned discussion it can be asserted that cost

involved in opposing the petition cannot be considered claimable under the allowable

deductions as per “Section 8-1 of the ITAA 1997”.

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

Based on the given issue it can be certain whether the winding up of businesses

usually treated as an outlay of the business function and not considered under “Section 8-1 of

the ITAA 1997” for the various types of allowable deductions. As stated in “Taxation

ruling of ID 2004/367” various types of the costs are legally related for execution of the

business operations and henceforth the cost borne by the taxpayer is used in producing

assessable income.

As per the “FC of T v Snowden and Wilson Pty Ltd (1958)”, the main form of

outlay of the expenses have taken place in the ordinary course of business and individual

taxpayer were needed to outlay that state of affairs to prevented any sort of expense which is

considered for admission or deduction (Barkoczy 2016).

Despite of the cost qualifying with the positive limbs, it cannot be held deductible due

to the fact that the expenses incurred owns the features associated to cost of capital.

Conclusion:

As noted from the aforementioned discussion it can be asserted that cost

involved in opposing the petition cannot be considered claimable under the allowable

deductions as per “Section 8-1 of the ITAA 1997”.

6TAXATION LAW

Answer to question 1.4:

Issue:

The aforementioned issue is able to state on whether expense determination is in

relation to the service of the solicitor and whether it needs to be taken into consideration as

per funds will deductions stated in “Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

Applications:

Based on the aforementioned ruling the legal expenditure relating to the trading

activities needs to be considered for the admissible deductions. It is so further noted that as

per “Section 8-1 of the ITAA 1997” in case the expenditure is found to be domestic,

personal and capital in nature it cannot be considered as non-exemption, non-admissible and

non-assessable deduction. However, to qualify for the deductions the legal expenditure has

been associated to a revenue producing activity. Based on the given issue the taxpayer has

borne the expenditure for taking service of solicitor in undertaking business function and

shall be entitled for deductions as per “Section 8-1 of the ITAA 1997” (May 2016).

Conclusion:

there is of the aforementioned legal expenditure for the service of the solicitor in

discharging the business functions needs to be taken into consideration as per “Section 8-1 of

the ITAA 1997” as the legal expenditure is related to a revenue generating activity.

Answer to question 1.4:

Issue:

The aforementioned issue is able to state on whether expense determination is in

relation to the service of the solicitor and whether it needs to be taken into consideration as

per funds will deductions stated in “Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

Applications:

Based on the aforementioned ruling the legal expenditure relating to the trading

activities needs to be considered for the admissible deductions. It is so further noted that as

per “Section 8-1 of the ITAA 1997” in case the expenditure is found to be domestic,

personal and capital in nature it cannot be considered as non-exemption, non-admissible and

non-assessable deduction. However, to qualify for the deductions the legal expenditure has

been associated to a revenue producing activity. Based on the given issue the taxpayer has

borne the expenditure for taking service of solicitor in undertaking business function and

shall be entitled for deductions as per “Section 8-1 of the ITAA 1997” (May 2016).

Conclusion:

there is of the aforementioned legal expenditure for the service of the solicitor in

discharging the business functions needs to be taken into consideration as per “Section 8-1 of

the ITAA 1997” as the legal expenditure is related to a revenue generating activity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Answer to question 2:

Issue:

The aforementioned issue is able to consider the determination of input tax credit

subjected to GST supplies made under “GST Act 1999”.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

Applications:

The aforementioned case of Big Bank is mainly associated in determining that GST

supplies which has been made along with the determination of input tax credit as for the

advertisement expenditure. Based on the ruling is provided in “Chapter 2 of the GST Act

1999” any commercial unit shall be permitted to claim the input tax which has been incurred

by the organisation in normal course of business. Although it needs to be noted that the

expenditure should be inclusive of the total amount of GST charged. Based on the present

case Big Bank Ltd. has been able to put forward the financial services in more than 50

branches throughout the country (Millar 2014).

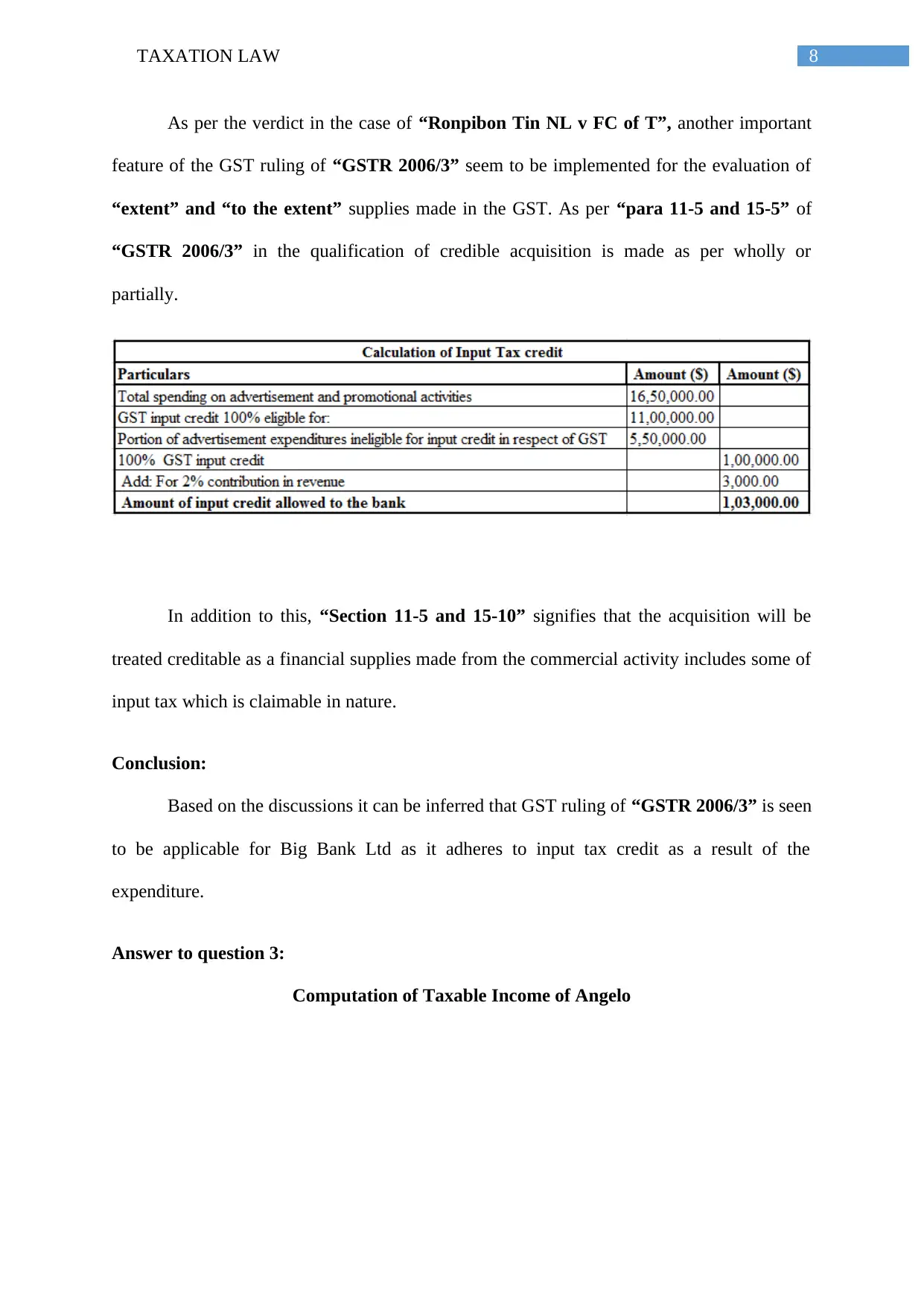

As per “division 11-15 and 129 of the GST Act 1999” the total amount of credible

acquisition has been identified in previously mentioned. It has been further discerned that the

ruling of “GSTR 2006/3” is seen to be mainly applicable for the business concerns exceeding

the financial limit of acquisition in terms of acquisition of input tax credit. Based on the given

context big bank has incurred the advertisement expenses which is inclusive of the GST

amount henceforth GST ruling of “GSTR 2006/3” is applicable (Datt, Nienaber and Tran-

Nam 2017).

Answer to question 2:

Issue:

The aforementioned issue is able to consider the determination of input tax credit

subjected to GST supplies made under “GST Act 1999”.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

Applications:

The aforementioned case of Big Bank is mainly associated in determining that GST

supplies which has been made along with the determination of input tax credit as for the

advertisement expenditure. Based on the ruling is provided in “Chapter 2 of the GST Act

1999” any commercial unit shall be permitted to claim the input tax which has been incurred

by the organisation in normal course of business. Although it needs to be noted that the

expenditure should be inclusive of the total amount of GST charged. Based on the present

case Big Bank Ltd. has been able to put forward the financial services in more than 50

branches throughout the country (Millar 2014).

As per “division 11-15 and 129 of the GST Act 1999” the total amount of credible

acquisition has been identified in previously mentioned. It has been further discerned that the

ruling of “GSTR 2006/3” is seen to be mainly applicable for the business concerns exceeding

the financial limit of acquisition in terms of acquisition of input tax credit. Based on the given

context big bank has incurred the advertisement expenses which is inclusive of the GST

amount henceforth GST ruling of “GSTR 2006/3” is applicable (Datt, Nienaber and Tran-

Nam 2017).

8TAXATION LAW

As per the verdict in the case of “Ronpibon Tin NL v FC of T”, another important

feature of the GST ruling of “GSTR 2006/3” seem to be implemented for the evaluation of

“extent” and “to the extent” supplies made in the GST. As per “para 11-5 and 15-5” of

“GSTR 2006/3” in the qualification of credible acquisition is made as per wholly or

partially.

In addition to this, “Section 11-5 and 15-10” signifies that the acquisition will be

treated creditable as a financial supplies made from the commercial activity includes some of

input tax which is claimable in nature.

Conclusion:

Based on the discussions it can be inferred that GST ruling of “GSTR 2006/3” is seen

to be applicable for Big Bank Ltd as it adheres to input tax credit as a result of the

expenditure.

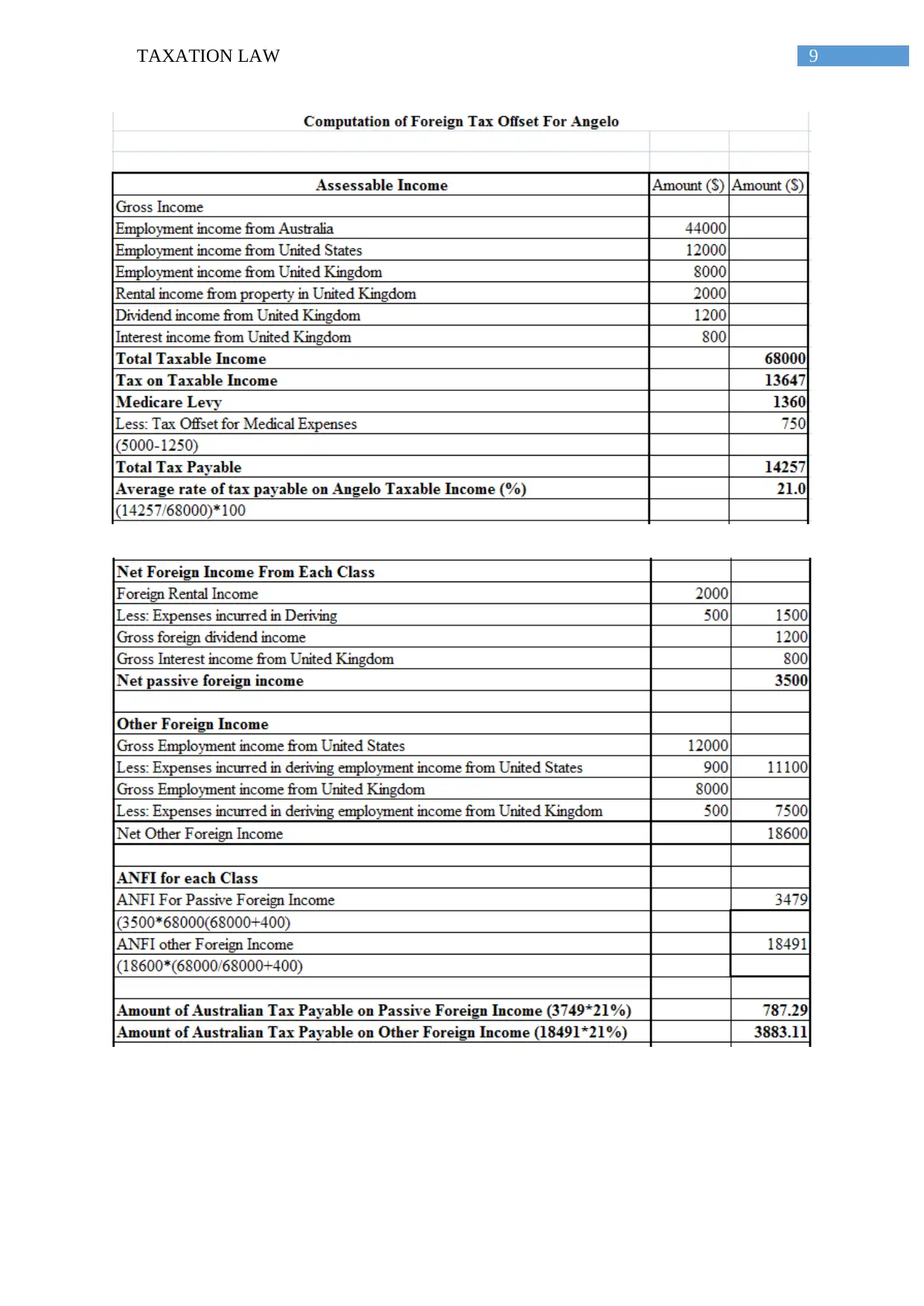

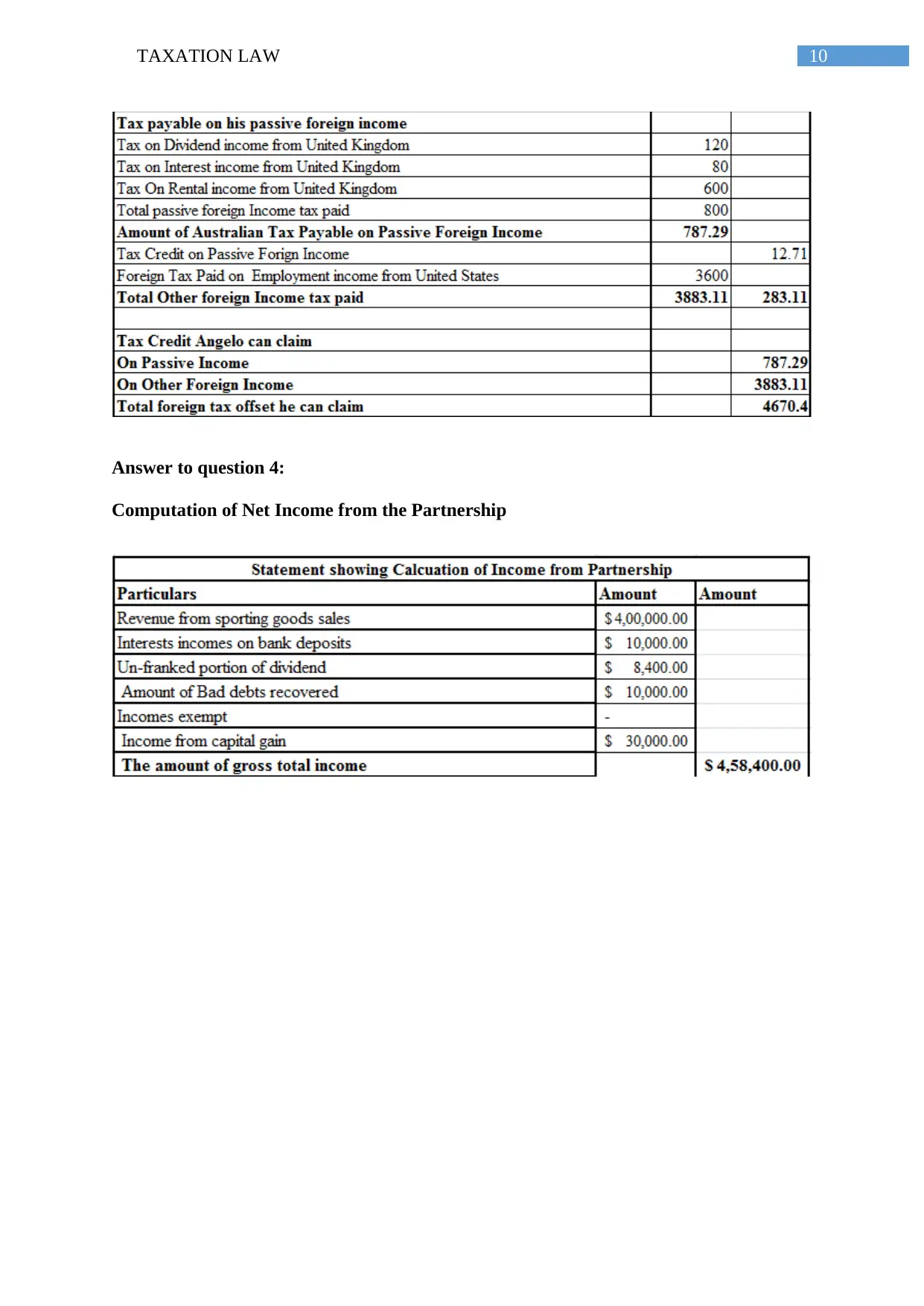

Answer to question 3:

Computation of Taxable Income of Angelo

As per the verdict in the case of “Ronpibon Tin NL v FC of T”, another important

feature of the GST ruling of “GSTR 2006/3” seem to be implemented for the evaluation of

“extent” and “to the extent” supplies made in the GST. As per “para 11-5 and 15-5” of

“GSTR 2006/3” in the qualification of credible acquisition is made as per wholly or

partially.

In addition to this, “Section 11-5 and 15-10” signifies that the acquisition will be

treated creditable as a financial supplies made from the commercial activity includes some of

input tax which is claimable in nature.

Conclusion:

Based on the discussions it can be inferred that GST ruling of “GSTR 2006/3” is seen

to be applicable for Big Bank Ltd as it adheres to input tax credit as a result of the

expenditure.

Answer to question 3:

Computation of Taxable Income of Angelo

9TAXATION LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

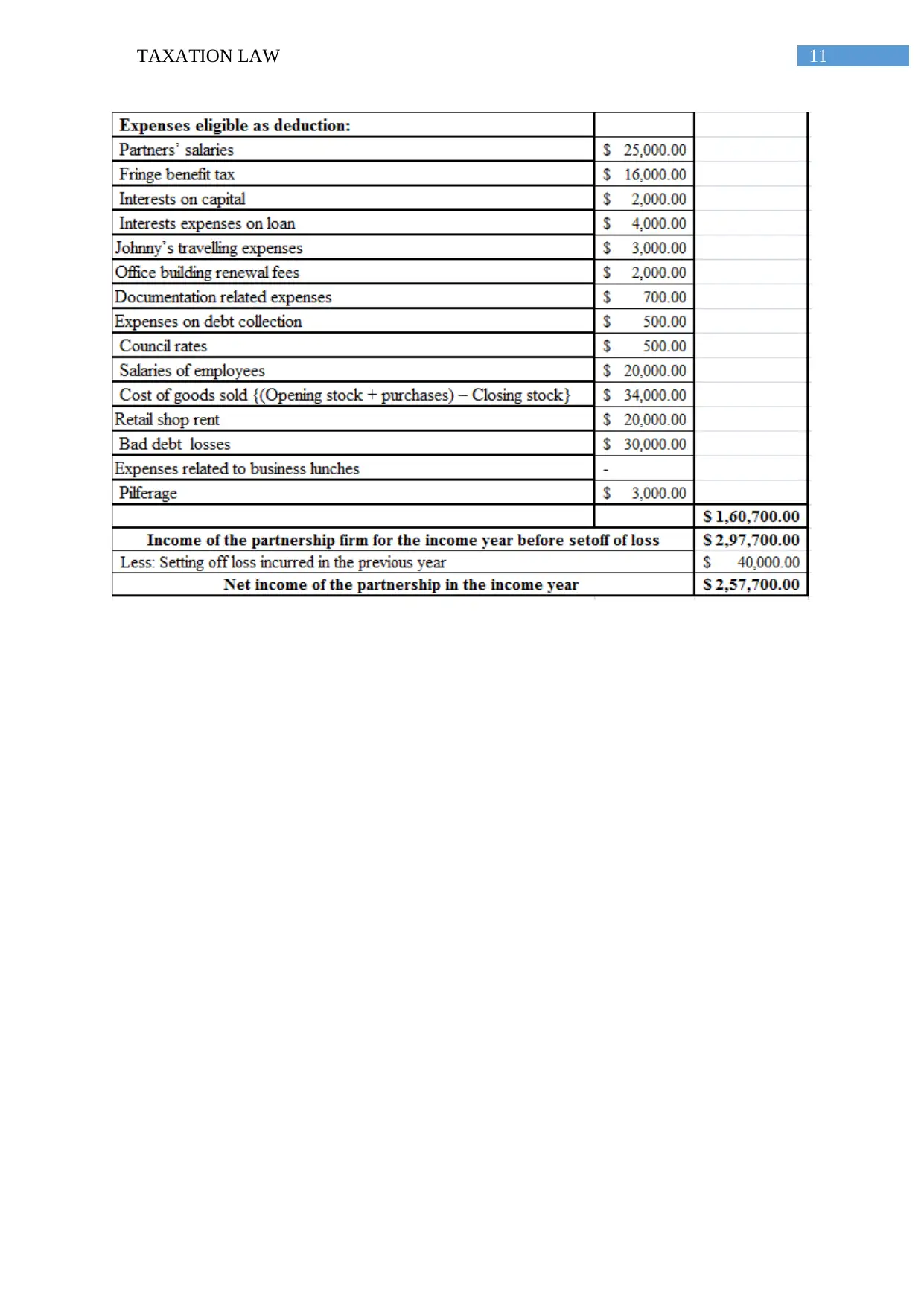

Answer to question 4:

Computation of Net Income from the Partnership

Answer to question 4:

Computation of Net Income from the Partnership

11TAXATION LAW

12TAXATION LAW

References

Aktaev, N.E., Bannova, K.A., Balandina, A.S., Dolgih, I.N., Pokrovskaia, N.V., Rumina,

U.A., Zhdanova, A.B. and Akhmadeev, K.N., 2015. Optimization criteria for entry into the

consolidated group of taxpayers in order to create an effective tax mechanism and improve

the social, economic development of regions in the Russian Federation. Procedia-Social and

Behavioral Sciences, 166, pp.30-35.Grange, J., Jover-Ledesma, G. and Maydew, G.

(n.d.). 2014 principles of business taxation.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and South

Africa. In Australian Tax Forum (Vol. 32, No. 2, p. 377). Tax Institute.

May, S., 2016. Applying the GST to imported digital products and services: Problems and

solutions. Tax Specialist, 19(3), p.110.

Millar, R., 2014. Grappling with basic VAT concepts in the Australian GST: the meaning of

‘supply for consideration’. World Journal of VAT/GST Law, 3(1), pp.1-31.

Pyrmont, (2014). Australian Taxation Law Cases 2014. NSW: Thomson Reuters.

References

Aktaev, N.E., Bannova, K.A., Balandina, A.S., Dolgih, I.N., Pokrovskaia, N.V., Rumina,

U.A., Zhdanova, A.B. and Akhmadeev, K.N., 2015. Optimization criteria for entry into the

consolidated group of taxpayers in order to create an effective tax mechanism and improve

the social, economic development of regions in the Russian Federation. Procedia-Social and

Behavioral Sciences, 166, pp.30-35.Grange, J., Jover-Ledesma, G. and Maydew, G.

(n.d.). 2014 principles of business taxation.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Datt, K., Nienaber, G. and Tran-Nam, B., 2017. GST/VAT general anti-avoidance

approaches: Some preliminary findings from a comparative study of Australia and South

Africa. In Australian Tax Forum (Vol. 32, No. 2, p. 377). Tax Institute.

May, S., 2016. Applying the GST to imported digital products and services: Problems and

solutions. Tax Specialist, 19(3), p.110.

Millar, R., 2014. Grappling with basic VAT concepts in the Australian GST: the meaning of

‘supply for consideration’. World Journal of VAT/GST Law, 3(1), pp.1-31.

Pyrmont, (2014). Australian Taxation Law Cases 2014. NSW: Thomson Reuters.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.