HA3042 Taxation Law Assignment: Income, FBTAA & Capital Gains Tax

VerifiedAdded on 2023/06/11

|8

|2345

|193

Homework Assignment

AI Summary

This taxation law assignment addresses several key issues. It analyzes whether payments received by a mountaineer are income from personal exertion, applying relevant case law to determine if payments for her story and photos are capital receipts. The assignment also computes the taxable value of car fringe benefits using the statutory formula under FBTAA 1986, and discusses the tax treatment of a parent receiving principal and interest payments from a loan to their son, considering potential gift implications. Finally, it examines capital gains tax implications for property sales, including scenarios involving sales to family members and transfers to a company, using both discount and indexation methods for calculation. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The given case is concerned with a famous mountaineer Hilary who has received certain

payments. The main issue is to assess if these payments can be considered as income arising

on account of personal exertion under the ambit of s. 6(5).

Payment from newspaper

Hilary was approached by the local newspaper that paid $ 10,000 to her for writing her story.

The key fact to notice here is that Hilary does not have writing experience nor is she known

for her writing skills. Anything written by Hilary would not have any value commercially.

Then, the key question which arises is as to why the payment was made to Hilary. The only

explanation that would arise is that the money was paid to Hilary so that the information

about her life can be obtained by the newspaper. Clearly, this information would be of

interest to the newspaper considering the fact that Hilary was famous and thus people would

be interested in knowing about her life and mountaineering expeditions. The act of writing

had served only a medium which enabled the transfer of information but did not produce any

commercial good or service (Barkoczy, 2015).

The consideration of writing as mere medium is validated by the decision pronounced by the

honourable court in the Brent vs Federal Commissioner of Taxation (1971) 125 case. In this

case also the wife of a famous robber was given money to reveal details about their marital

life. The mode of collection of this information was interviews and these continued for about

2 weeks. However, the court held that the interview session acted as merely the mode of

transfer of the pivotal information which is the asset (Woellner, 2014). The details of the

given case closely resemble that of present situation. As a result, the $ 10,000 payment would

not be labelled as personal exertion based income. The payment is essentially capital receipt

earned through exchange of information.

Payment from Library

The manuscript of the story along with some expedition photographs have been sold to the

library. In relation to the manuscript, it is imperative to consider that the museum is not

paying for the manuscript since Hilary has written it. Any literary work by Hilary would not

have worth considering Hilary does not have necessary skills for the same. However, the

1

The given case is concerned with a famous mountaineer Hilary who has received certain

payments. The main issue is to assess if these payments can be considered as income arising

on account of personal exertion under the ambit of s. 6(5).

Payment from newspaper

Hilary was approached by the local newspaper that paid $ 10,000 to her for writing her story.

The key fact to notice here is that Hilary does not have writing experience nor is she known

for her writing skills. Anything written by Hilary would not have any value commercially.

Then, the key question which arises is as to why the payment was made to Hilary. The only

explanation that would arise is that the money was paid to Hilary so that the information

about her life can be obtained by the newspaper. Clearly, this information would be of

interest to the newspaper considering the fact that Hilary was famous and thus people would

be interested in knowing about her life and mountaineering expeditions. The act of writing

had served only a medium which enabled the transfer of information but did not produce any

commercial good or service (Barkoczy, 2015).

The consideration of writing as mere medium is validated by the decision pronounced by the

honourable court in the Brent vs Federal Commissioner of Taxation (1971) 125 case. In this

case also the wife of a famous robber was given money to reveal details about their marital

life. The mode of collection of this information was interviews and these continued for about

2 weeks. However, the court held that the interview session acted as merely the mode of

transfer of the pivotal information which is the asset (Woellner, 2014). The details of the

given case closely resemble that of present situation. As a result, the $ 10,000 payment would

not be labelled as personal exertion based income. The payment is essentially capital receipt

earned through exchange of information.

Payment from Library

The manuscript of the story along with some expedition photographs have been sold to the

library. In relation to the manuscript, it is imperative to consider that the museum is not

paying for the manuscript since Hilary has written it. Any literary work by Hilary would not

have worth considering Hilary does not have necessary skills for the same. However, the

1

manuscript becomes valuable owing to the subject matter which relates to Hilary and since

she is famous, thus the manuscript becomes valuable (Gilders et. al., 2016).

In relation to the expedition pictures, the worth of pictures does not come from the activity of

clicking photos since Hilary is not any famed photographer whose work is sought after. But

again the subject matter is imperative. This is because the photos depict the various

photographs related to the expeditions carried out by Hilary which is valuable since she is

known as a mountain climber. Thus, the photograph skills do not have any role to play in the

value of the photographs. Owing to this, the income derived from the sale of photos is not

related to the activity of clicking photographs. Thus, the income would be termed as personal

exertion based income and instead would be termed as capital receipt (Gilders et. a., 2016).

Intention Change

If the story is now written based on self-satisfaction instead of the motive to earn money, then

also the appropriate tax treatment would essentially remain the same. This is because the

central activity of writing is not related to income as it does not lead to anything productive.

Based on the explanation above, writing is just a means of asset transfer and thus, the

underlying intention does not real matter. The underlying intention would become useful

when the act of writing was contribution to proceeds which is not the case here (Sadiq et. al.,

2016).

Question 2

Section 9, FBTAA 1986 highlights the formula to be deployed in computing the car fringe

benefit related taxable value. This is given below (Woellner, 2014).

The key inputs denoted as A, B, C,D & E can be computed based on the information

provided coupled with the relevant FBTAA provisions as highlighted as follows (Barkoczy,

2015).

2

she is famous, thus the manuscript becomes valuable (Gilders et. al., 2016).

In relation to the expedition pictures, the worth of pictures does not come from the activity of

clicking photos since Hilary is not any famed photographer whose work is sought after. But

again the subject matter is imperative. This is because the photos depict the various

photographs related to the expeditions carried out by Hilary which is valuable since she is

known as a mountain climber. Thus, the photograph skills do not have any role to play in the

value of the photographs. Owing to this, the income derived from the sale of photos is not

related to the activity of clicking photographs. Thus, the income would be termed as personal

exertion based income and instead would be termed as capital receipt (Gilders et. a., 2016).

Intention Change

If the story is now written based on self-satisfaction instead of the motive to earn money, then

also the appropriate tax treatment would essentially remain the same. This is because the

central activity of writing is not related to income as it does not lead to anything productive.

Based on the explanation above, writing is just a means of asset transfer and thus, the

underlying intention does not real matter. The underlying intention would become useful

when the act of writing was contribution to proceeds which is not the case here (Sadiq et. al.,

2016).

Question 2

Section 9, FBTAA 1986 highlights the formula to be deployed in computing the car fringe

benefit related taxable value. This is given below (Woellner, 2014).

The key inputs denoted as A, B, C,D & E can be computed based on the information

provided coupled with the relevant FBTAA provisions as highlighted as follows (Barkoczy,

2015).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A – The original purchase price of the car would be fed here since no depreciation

would be charged just now on the car considering only 2nd year is in progress and it is

charged only after 3 or 4 years. Therefore the value of A is $ 50,000.

B – The statutory percentage before 2011 used to depend on distance but for vehicles

purchased after 2011, the percentage is applied without any consideration of the

underlying distance. Therefore, the value of B is 20%.

C – This refers to the days of availability for personal car usage for which data has

already been provided in the question. Therefore, the value of C is 183.

D – This refers to the number of days that are present in the tax assessment year

which is under consideration. Therefore, the value of D is 365.

E – As indicated, the statutory formula does allow for deduction based on the

expenses incurred by employees relating to the vehicle. However, for deduction a key

necessary condition is that the concerned employees must have all supporting

documentation to establish that the money claimed has actually been spent in

accordance with s.10A. This condition is fulfilled in this case. Therefore, the value of

E is $ 10,000.

The inputs highlighted in the above discussion are out in the formula set out in section 9

which leads to the following computation.

Question 3

The case facts represent that a financial assistance of $ 40,000 was given to the son and there

was no desire to derive any interest income out of this which was clearly stated at the time of

providing the money. Also, there was no legal documentation or security taken to back the

loan and thus it was given on mere trust. Further, the parent wanted that the money should be

returned after five years. However, the son is able to return the principle after two years only

and further also provided 5% interest for 2 years which works out as $ 4,000. In wake of

these payments received by the parent, the appropriate tax treatment of this payment on the

end of the parent needs to be discussed.

For the purposes of analysis of the payment received, it makes sense to sub-divide the

payment into two tranches namely the principal and interest.

3

would be charged just now on the car considering only 2nd year is in progress and it is

charged only after 3 or 4 years. Therefore the value of A is $ 50,000.

B – The statutory percentage before 2011 used to depend on distance but for vehicles

purchased after 2011, the percentage is applied without any consideration of the

underlying distance. Therefore, the value of B is 20%.

C – This refers to the days of availability for personal car usage for which data has

already been provided in the question. Therefore, the value of C is 183.

D – This refers to the number of days that are present in the tax assessment year

which is under consideration. Therefore, the value of D is 365.

E – As indicated, the statutory formula does allow for deduction based on the

expenses incurred by employees relating to the vehicle. However, for deduction a key

necessary condition is that the concerned employees must have all supporting

documentation to establish that the money claimed has actually been spent in

accordance with s.10A. This condition is fulfilled in this case. Therefore, the value of

E is $ 10,000.

The inputs highlighted in the above discussion are out in the formula set out in section 9

which leads to the following computation.

Question 3

The case facts represent that a financial assistance of $ 40,000 was given to the son and there

was no desire to derive any interest income out of this which was clearly stated at the time of

providing the money. Also, there was no legal documentation or security taken to back the

loan and thus it was given on mere trust. Further, the parent wanted that the money should be

returned after five years. However, the son is able to return the principle after two years only

and further also provided 5% interest for 2 years which works out as $ 4,000. In wake of

these payments received by the parent, the appropriate tax treatment of this payment on the

end of the parent needs to be discussed.

For the purposes of analysis of the payment received, it makes sense to sub-divide the

payment into two tranches namely the principal and interest.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1) Principal Repayment– It is known that financial assistance to the tune of $ 40,000 was

extended to the son and hence the receipt of this amount from the son would not be

income but rather repayment of capital. As a result, the receipts would not be revenue

but capital nature and hence non-taxable (CCH, 2013).

2) Interest amount – For the $ 4,000 amount received under aegis of interest, the

explanation using various possible statutes and tax ruling ought to be attempted. The

first possibility is that the payment is income as per s.6(5). But for ordinary income to

arise, this cash flow has to be regular which would imply that the parent is operating a

business where lending on interest is a common practice. The given information does

not suggest the same and the unprofessional manner in which the money was lent

provides apparent evidence that the given payment is outside the purview of s.6(5)

(Woellner, 2014).

Another possibility is that the transaction in which the loan was given to son was an

isolated transaction and interest income may be taxable under s. 15(15) ITAA 1997.

However, for the interest income to be taxable, key condition to be met is that the loan

should have been extended by the parent driven by the intention to profit through the

interest income. But the case facts suggest a contrary situation here as the parent

highlighted that she did not want any interest and hence profit motive is clearly

absent. Thus, the given payment is outside the purview of s. 15(25) (Gilders et. al.,

2016).

Since the above two approaches have failed, then it is likely that the incremental

amount given as interest is gift. This can be shown through the following facts which

are in line with the demands of gift as stated in TR2005/13 (ATO, 2005).

Since cheque has been passed on to the parent, the transfer of money has concluded.

This money has been given despite the parent not wanting it at the first place which is

indicative of voluntary nature.

Owing to the nominal amount transfer, it is highly unlikely that any expectations

would arise on the part of son.

Gratitude is driving this transfer from son to the parent.

4

extended to the son and hence the receipt of this amount from the son would not be

income but rather repayment of capital. As a result, the receipts would not be revenue

but capital nature and hence non-taxable (CCH, 2013).

2) Interest amount – For the $ 4,000 amount received under aegis of interest, the

explanation using various possible statutes and tax ruling ought to be attempted. The

first possibility is that the payment is income as per s.6(5). But for ordinary income to

arise, this cash flow has to be regular which would imply that the parent is operating a

business where lending on interest is a common practice. The given information does

not suggest the same and the unprofessional manner in which the money was lent

provides apparent evidence that the given payment is outside the purview of s.6(5)

(Woellner, 2014).

Another possibility is that the transaction in which the loan was given to son was an

isolated transaction and interest income may be taxable under s. 15(15) ITAA 1997.

However, for the interest income to be taxable, key condition to be met is that the loan

should have been extended by the parent driven by the intention to profit through the

interest income. But the case facts suggest a contrary situation here as the parent

highlighted that she did not want any interest and hence profit motive is clearly

absent. Thus, the given payment is outside the purview of s. 15(25) (Gilders et. al.,

2016).

Since the above two approaches have failed, then it is likely that the incremental

amount given as interest is gift. This can be shown through the following facts which

are in line with the demands of gift as stated in TR2005/13 (ATO, 2005).

Since cheque has been passed on to the parent, the transfer of money has concluded.

This money has been given despite the parent not wanting it at the first place which is

indicative of voluntary nature.

Owing to the nominal amount transfer, it is highly unlikely that any expectations

would arise on the part of son.

Gratitude is driving this transfer from son to the parent.

4

Based on the arguments that have been stated above with regards to the principal and interest

tax treatment, it would be correct to assume that no tax would arise on parent’s behalf based

on the amount paid by son.

Question 4

a) Scott who is an accountant by profession has bought a vacant land in Brisbane in 1980. It

is noteworthy that capital gains tax came into existence only on September 20, 1985 and

hence all assets purchased before this period are exempt from any taxation of capital gains.

Further, in 1986, Scott started construction of a house on the vacant land which was

completed in 1986. Also, it is known that the house was given by rent ever since

construction and therefore would not qualify for main residence exemption under Division

119B (CCH, 2013).

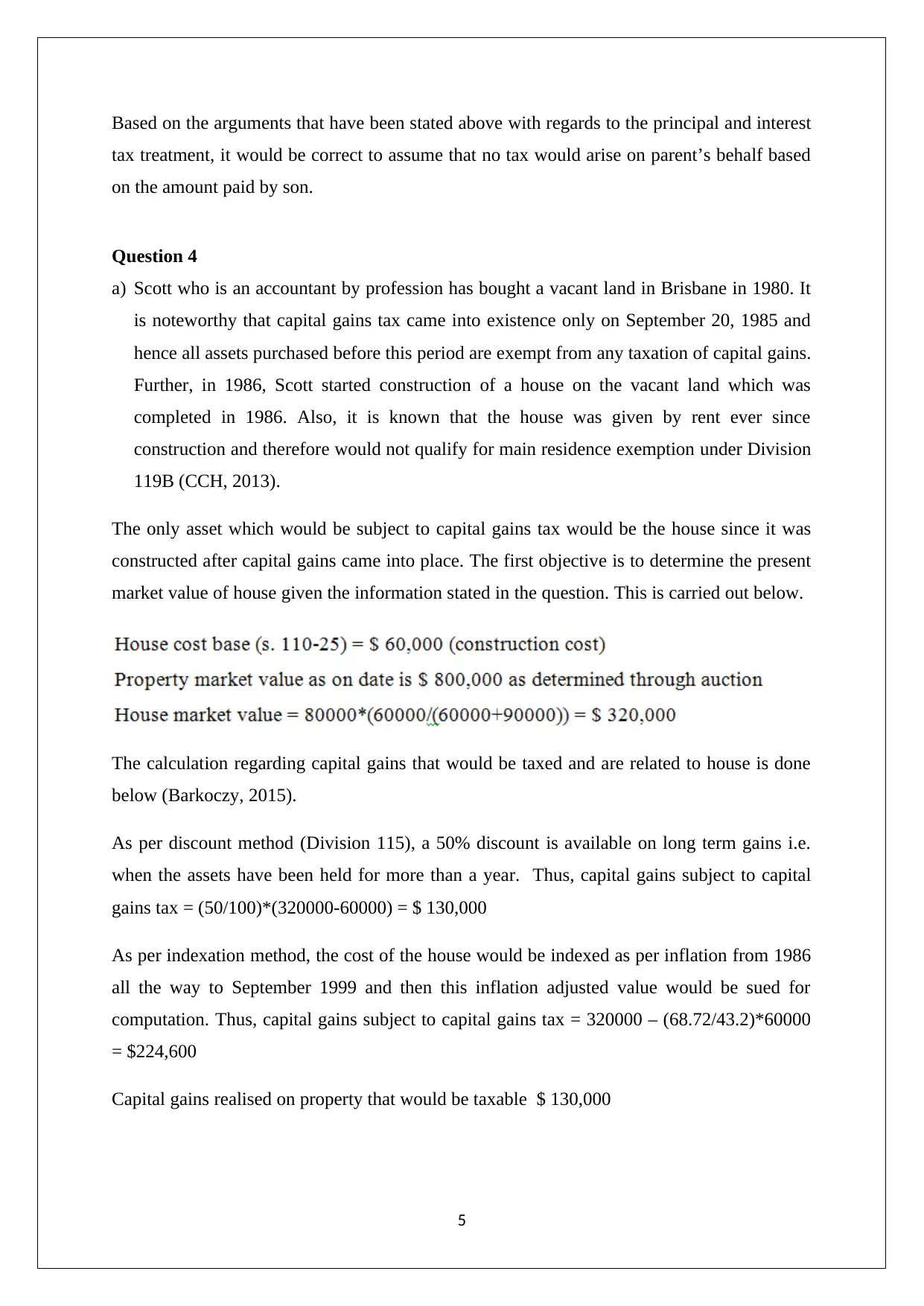

The only asset which would be subject to capital gains tax would be the house since it was

constructed after capital gains came into place. The first objective is to determine the present

market value of house given the information stated in the question. This is carried out below.

The calculation regarding capital gains that would be taxed and are related to house is done

below (Barkoczy, 2015).

As per discount method (Division 115), a 50% discount is available on long term gains i.e.

when the assets have been held for more than a year. Thus, capital gains subject to capital

gains tax = (50/100)*(320000-60000) = $ 130,000

As per indexation method, the cost of the house would be indexed as per inflation from 1986

all the way to September 1999 and then this inflation adjusted value would be sued for

computation. Thus, capital gains subject to capital gains tax = 320000 – (68.72/43.2)*60000

= $224,600

Capital gains realised on property that would be taxable $ 130,000

5

tax treatment, it would be correct to assume that no tax would arise on parent’s behalf based

on the amount paid by son.

Question 4

a) Scott who is an accountant by profession has bought a vacant land in Brisbane in 1980. It

is noteworthy that capital gains tax came into existence only on September 20, 1985 and

hence all assets purchased before this period are exempt from any taxation of capital gains.

Further, in 1986, Scott started construction of a house on the vacant land which was

completed in 1986. Also, it is known that the house was given by rent ever since

construction and therefore would not qualify for main residence exemption under Division

119B (CCH, 2013).

The only asset which would be subject to capital gains tax would be the house since it was

constructed after capital gains came into place. The first objective is to determine the present

market value of house given the information stated in the question. This is carried out below.

The calculation regarding capital gains that would be taxed and are related to house is done

below (Barkoczy, 2015).

As per discount method (Division 115), a 50% discount is available on long term gains i.e.

when the assets have been held for more than a year. Thus, capital gains subject to capital

gains tax = (50/100)*(320000-60000) = $ 130,000

As per indexation method, the cost of the house would be indexed as per inflation from 1986

all the way to September 1999 and then this inflation adjusted value would be sued for

computation. Thus, capital gains subject to capital gains tax = 320000 – (68.72/43.2)*60000

= $224,600

Capital gains realised on property that would be taxable $ 130,000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Scott sells the property to her daughter for only $ 200,000 while the market value is $

800,000. But, s. 116-30 clearly states that in case of non-convergence between the market

value and sales proceeds of the asset, the higher ought to be used for CGT purposes (Sadiq

et. al.,2016). The higher value is the market value of $ 800,000.

Hence, capital gains realised on property that would be taxable $ 130,000

c) The property owner is no more an individual but a company. This would have a

implication for capital gains tax computation since discount method cannot be availed by

companies (CCH, 2013). Hence, the capital gains would be computed in accordance with

indexation method that has been demonstrated in part (a).

Hence, capital gains realised on property that would be taxable - $224,600

6

800,000. But, s. 116-30 clearly states that in case of non-convergence between the market

value and sales proceeds of the asset, the higher ought to be used for CGT purposes (Sadiq

et. al.,2016). The higher value is the market value of $ 800,000.

Hence, capital gains realised on property that would be taxable $ 130,000

c) The property owner is no more an individual but a company. This would have a

implication for capital gains tax computation since discount method cannot be availed by

companies (CCH, 2013). Hence, the capital gains would be computed in accordance with

indexation method that has been demonstrated in part (a).

Hence, capital gains realised on property that would be taxable - $224,600

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

ATO (2005), Tax Ruling TR 2005/13, [online] available at

http://law.ato.gov.au/atolaw/view.htm?Docid=TXR/TR200513/NAT/ATO/00001

Barkoczy, S. (2015) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016) Australian tax

handbook. 8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016. 9th ed. Sydney: LexisNexis/Butterworths.

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont: Thomson Reuters

Woellner, R (2014), Australian taxation law 2014 7th ed. North Ryde: CCH Australia

7

ATO (2005), Tax Ruling TR 2005/13, [online] available at

http://law.ato.gov.au/atolaw/view.htm?Docid=TXR/TR200513/NAT/ATO/00001

Barkoczy, S. (2015) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University

Press.

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016) Australian tax

handbook. 8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation

law 2016. 9th ed. Sydney: LexisNexis/Butterworths.

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont: Thomson Reuters

Woellner, R (2014), Australian taxation law 2014 7th ed. North Ryde: CCH Australia

7

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.