Taxation Law: Personal Exertion Income, Car Fringe Benefit, Capital Gains Tax, and Gift Tax

Added on 2023-06-11

7 Pages1900 Words277 Views

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Question 1

It is known based on the facts presented that payment has been received by Hilary on account

of three main sources i.e. story, photographs and manuscript. The ley issue is to ascertain if

any of these payments can be categorised as personal exertion related income under s. 6(5).

Story payment

The newspaper offered $ 10,000 to Hilary to write her story despite being aware of her scant

experience in writing. Offering such a significant sum to a person lacking writing skills

clearly highlight that the interest lays elsewhere and in this case it would be on the

information about Hilary. This information would have commercial worth since this would

pertain to Hilary who is a well-known mountaineer. Also, this information can only be

extracted from Hilary. The story is just acting as means to extract the information which

already exists. Hence, the action of writing does not have any commercial value owing to

lack of writing skills by Hilary. This understanding is endorsed by the ruling in the Brent vs

Federal Commissioner of Taxation (1971) 125 (Woellner, 2014). Thus, the payment of

$10,000 derived in this case cannot be considered as personal exertion related income since

writing activity does not act as source of income.

Manuscript payment

Taking a cue from the above, it is apparent that writing does not lead to any income being

produced. As a result, manuscript has commercial value not because of Hilary writing the

same as her writing skills are not sought after. However, the subject matter is important

which provides intrinsic value to the manuscript which is responsible for purchase by the

buyer. Therefore, considering the role of writing as only a mechanism to transfer information

coupled with lack of writing skills on part of Hilary, it is clear that proceeds are not

considered as personal exertion related income (Gilders et. a., 2016).

Photograph related payment

Hilary is famous as a mountain climber and not as a photographer. Hence the activity of

clicking photos has no special significance and on that count, there is not worth of the

pictures. However, these photos capture moments from Hilary expeditions which makes them

1

It is known based on the facts presented that payment has been received by Hilary on account

of three main sources i.e. story, photographs and manuscript. The ley issue is to ascertain if

any of these payments can be categorised as personal exertion related income under s. 6(5).

Story payment

The newspaper offered $ 10,000 to Hilary to write her story despite being aware of her scant

experience in writing. Offering such a significant sum to a person lacking writing skills

clearly highlight that the interest lays elsewhere and in this case it would be on the

information about Hilary. This information would have commercial worth since this would

pertain to Hilary who is a well-known mountaineer. Also, this information can only be

extracted from Hilary. The story is just acting as means to extract the information which

already exists. Hence, the action of writing does not have any commercial value owing to

lack of writing skills by Hilary. This understanding is endorsed by the ruling in the Brent vs

Federal Commissioner of Taxation (1971) 125 (Woellner, 2014). Thus, the payment of

$10,000 derived in this case cannot be considered as personal exertion related income since

writing activity does not act as source of income.

Manuscript payment

Taking a cue from the above, it is apparent that writing does not lead to any income being

produced. As a result, manuscript has commercial value not because of Hilary writing the

same as her writing skills are not sought after. However, the subject matter is important

which provides intrinsic value to the manuscript which is responsible for purchase by the

buyer. Therefore, considering the role of writing as only a mechanism to transfer information

coupled with lack of writing skills on part of Hilary, it is clear that proceeds are not

considered as personal exertion related income (Gilders et. a., 2016).

Photograph related payment

Hilary is famous as a mountain climber and not as a photographer. Hence the activity of

clicking photos has no special significance and on that count, there is not worth of the

pictures. However, these photos capture moments from Hilary expeditions which makes them

1

valuable. Hence, the real source of value for the photos is the subject matter due to which

proceeds are not considered as personal exertion related income (Deustch et. al., 2016).

Change in Intention

If the underlying intention behind writing the story varies, it would not make any difference

to the tax treatment decided in the above case. This is because the writing activity is not the

creator of income and the proceeds are being derived owing to the access to information. This

information has not been created through writing but has only been communicated in this

means. Thus, the underlying motive and the presence of profit or not does not matter since

the activity does not produce any income anyways (Sadiq et. al., 2016).

Question 2

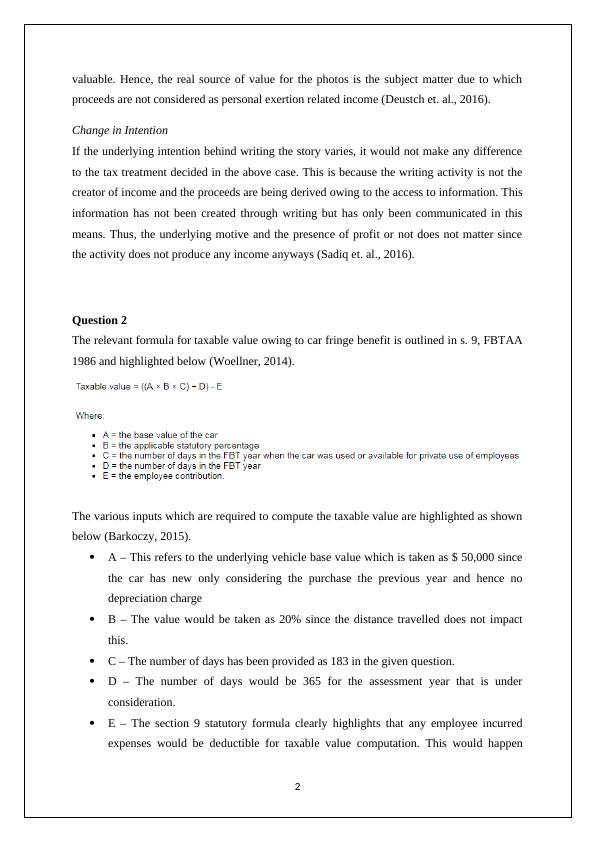

The relevant formula for taxable value owing to car fringe benefit is outlined in s. 9, FBTAA

1986 and highlighted below (Woellner, 2014).

The various inputs which are required to compute the taxable value are highlighted as shown

below (Barkoczy, 2015).

A – This refers to the underlying vehicle base value which is taken as $ 50,000 since

the car has new only considering the purchase the previous year and hence no

depreciation charge

B – The value would be taken as 20% since the distance travelled does not impact

this.

C – The number of days has been provided as 183 in the given question.

D – The number of days would be 365 for the assessment year that is under

consideration.

E – The section 9 statutory formula clearly highlights that any employee incurred

expenses would be deductible for taxable value computation. This would happen

2

proceeds are not considered as personal exertion related income (Deustch et. al., 2016).

Change in Intention

If the underlying intention behind writing the story varies, it would not make any difference

to the tax treatment decided in the above case. This is because the writing activity is not the

creator of income and the proceeds are being derived owing to the access to information. This

information has not been created through writing but has only been communicated in this

means. Thus, the underlying motive and the presence of profit or not does not matter since

the activity does not produce any income anyways (Sadiq et. al., 2016).

Question 2

The relevant formula for taxable value owing to car fringe benefit is outlined in s. 9, FBTAA

1986 and highlighted below (Woellner, 2014).

The various inputs which are required to compute the taxable value are highlighted as shown

below (Barkoczy, 2015).

A – This refers to the underlying vehicle base value which is taken as $ 50,000 since

the car has new only considering the purchase the previous year and hence no

depreciation charge

B – The value would be taken as 20% since the distance travelled does not impact

this.

C – The number of days has been provided as 183 in the given question.

D – The number of days would be 365 for the assessment year that is under

consideration.

E – The section 9 statutory formula clearly highlights that any employee incurred

expenses would be deductible for taxable value computation. This would happen

2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Analysis of Payments under Taxation Lawlg...

|8

|2342

|172

Taxation Law: Income Assessment, Car Fringe Benefit, Loan Tax Treatment, Capital Gains Taxlg...

|8

|2345

|193

Assignment - Taxation Law (Solution)lg...

|7

|1892

|87

Taxation Law: Payments from personal exertion, car fringe benefit, financial assistance, and CGT computationlg...

|7

|1916

|196

Taxation Law Issues: Assignmentlg...

|8

|1915

|44

Taxation Law ITAA 1997 - Doclg...

|6

|1596

|50