Taxation Law ITAA 1997 - Doc

Added on 2021-06-17

6 Pages1596 Words50 Views

TAXATION LAWSTUDENT ID:[Pick the date]

Question 1As per the given information, it is known that Hilary is a famous mountain climber who hasreceived payment for writing an autobiography, selling the manuscript and also expeditionphotographs. The tax treatment of these receipts need to be discussed in the wake of s.6(5)ITAA 1997 which has one component as income from personal exertion.Payment (Autobiography)The pertinent question to debate is whether the money extended by the newspaper was for thewriting skill of Hilary. In order to answer the same, consideration needs to be given to thefact that Hilary has never written anything of significance but still got an unsolicited offer of$ 10,000 from a local newspaper. Thus, it is apparent that the newspaper through theautobiography wants to gain access to the copyrighted information regarding Hilary’s life.This information has commercial value owing to the famed status of Hilary. Further, the actof writing does not produce anything useful but acts as the mechanism which facilitates thetransfer of key information from Hilary to newspaper. This understanding is in line with theverdict given in Brent vs Federal Commissioner of Taxation(1971) 125 CLR case. Theproceeds are for asset purchase and hence are capital receipts. Thus, proceeds are not derivedfrom personal exertion (Barkoczy, 2015).Payment (Manuscript & Photograph)The rationale that is established above can also be extended to related payments. Thephotograph does not derive any commercial worth from the photography skills of Hilary andthus the act of photography does not produce any assessable income. Similarly, themanuscript does not derive any commercial worth from the writing skills of Hilary and hencethe act of writing does not produce any assessable income. Thus, proceeds are not derivedfrom personal exertion (Sadiq et. al., 2015).Change in intentThe change of intent behind writing the book becomes pivotal when the act of writing isyielding something which has commercial worth. However, this is not true in the given caseas the worth of book is only because of the information contained. Hence, irrespective of thepresence of motive to profit or not, the proceeds would not be categorised as personalexertion related income (Deustch et. al., 2016).1

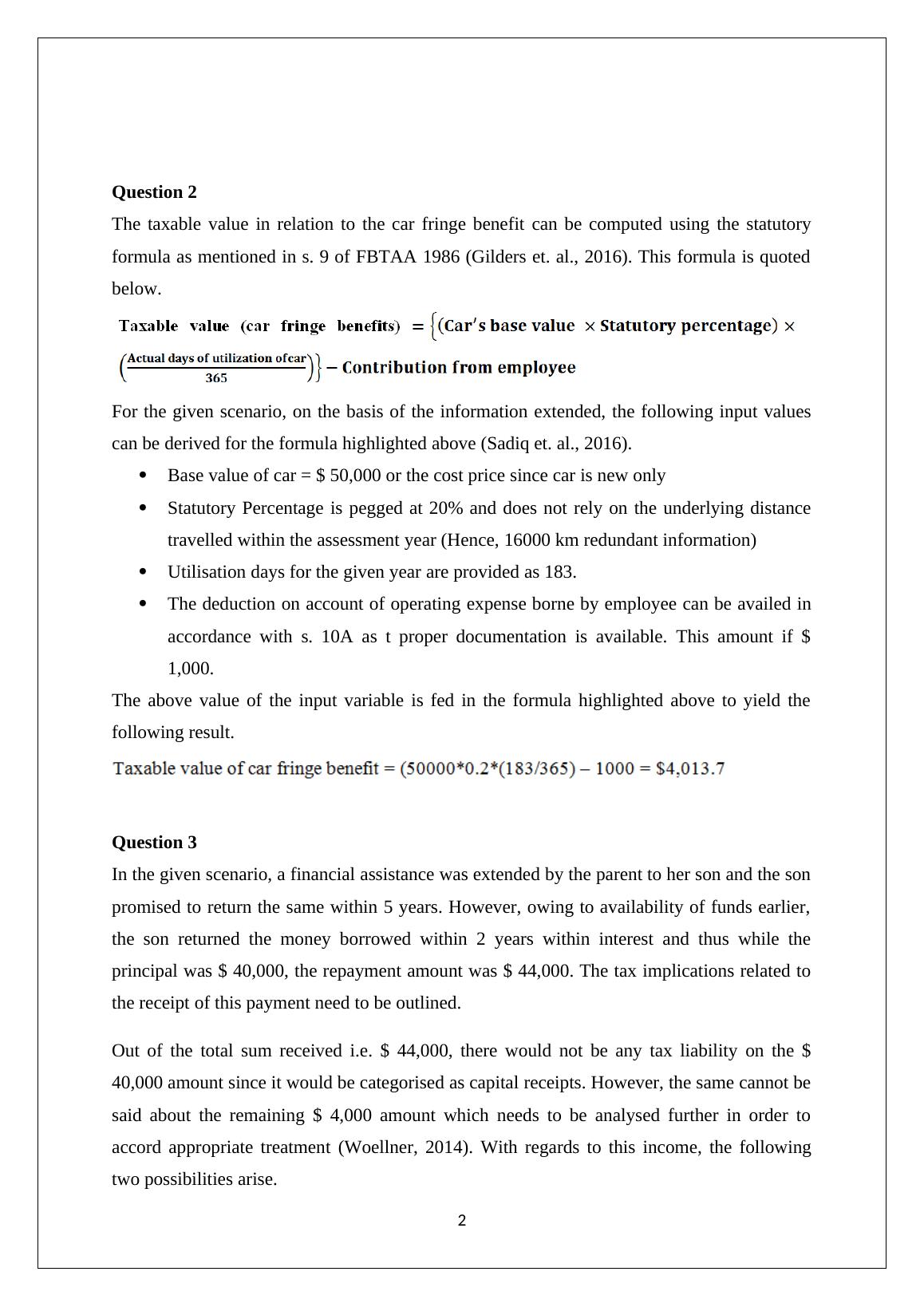

Question 2The taxable value in relation to the car fringe benefit can be computed using the statutoryformula as mentioned in s. 9 of FBTAA 1986 (Gilders et. al., 2016). This formula is quotedbelow.For the given scenario, on the basis of the information extended, the following input valuescan be derived for the formula highlighted above (Sadiq et. al., 2016).Base value of car = $ 50,000 or the cost price since car is new onlyStatutory Percentage is pegged at 20% and does not rely on the underlying distancetravelled within the assessment year (Hence, 16000 km redundant information)Utilisation days for the given year are provided as 183.The deduction on account of operating expense borne by employee can be availed inaccordance with s. 10A as t proper documentation is available. This amount if $1,000.The above value of the input variable is fed in the formula highlighted above to yield thefollowing result.Question 3In the given scenario, a financial assistance was extended by the parent to her son and the sonpromised to return the same within 5 years. However, owing to availability of funds earlier,the son returned the money borrowed within 2 years within interest and thus while theprincipal was $ 40,000, the repayment amount was $ 44,000. The tax implications related tothe receipt of this payment need to be outlined.Out of the total sum received i.e. $ 44,000, there would not be any tax liability on the $40,000 amount since it would be categorised as capital receipts. However, the same cannot besaid about the remaining $ 4,000 amount which needs to be analysed further in order toaccord appropriate treatment (Woellner, 2014). With regards to this income, the followingtwo possibilities arise. 2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Law: Analysis of Payments, Car Fringe Benefit, Capital Gains Computationlg...

|6

|1254

|306

Taxation Law: Payments from personal exertion, car fringe benefit, financial assistance, and CGT computationlg...

|7

|1916

|196

Taxation Law - Study Material with Solved Assignments, Essays, Dissertationlg...

|6

|1330

|437

Assignment - Taxation Law (Solution)lg...

|7

|1892

|87

Taxation Law Issues: Assignmentlg...

|8

|1915

|44

Taxation Law: Personal Exertion Income, Car Fringe Benefit, Capital Gains Tax, and Gift Taxlg...

|7

|1900

|277