HA3042 Taxation Law Assignment: FBT and Capital Gains Implications

VerifiedAdded on 2023/03/23

|9

|2658

|50

Homework Assignment

AI Summary

This assignment solution addresses two key questions in Taxation Law. The first question involves calculating the Fringe Benefits Tax (FBT) liability for Spiceco Pty Ltd for providing a car to their employee, Lucinda, for private use, detailing the depreciation, interest, operating costs, and taxable value calculations using both the cost basis and statutory formula methods, ultimately determining the FBT liability. The second question analyzes the net capital gains or losses made by Daniel from various transactions in 2018/2019, including the sale of a house (assessing main residence exemption), a painting (considering CGT implications for collectibles), a luxury yacht (evaluating personal use asset rules), and shares (calculating cost base and capital losses), to determine his taxable capital gains and the implications of capital gains or losses in the given financial year. Desklib provides a platform to access similar solved assignments and past papers for students.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The key objective is to ascertain the FBT liability that would arise for Spiceco Pty Ltd on

account of providing a car to their employee Lucinda for private use. The key aspects

related to the computation of car fringe benefit have been discussed below in wake of

the information provided.

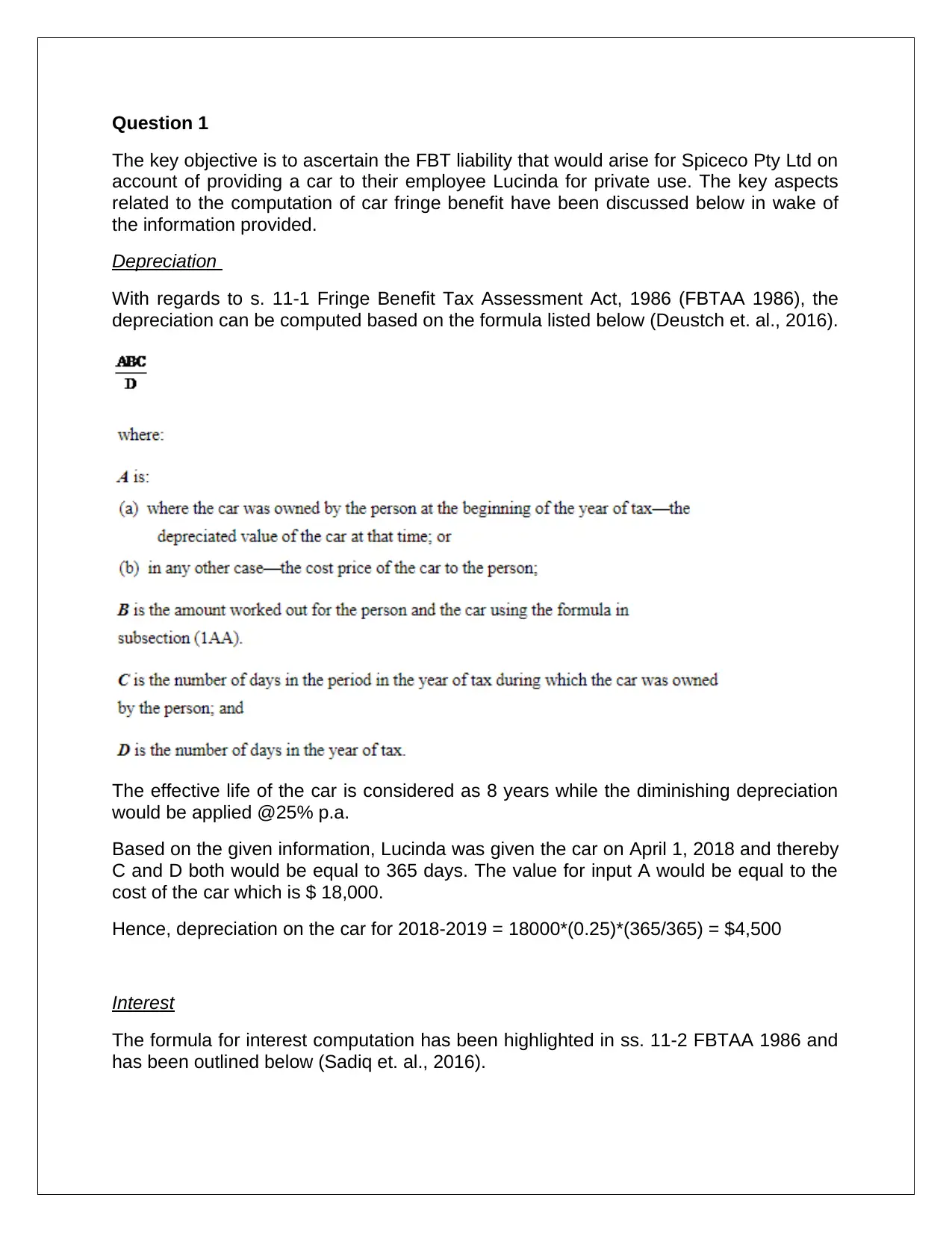

Depreciation

With regards to s. 11-1 Fringe Benefit Tax Assessment Act, 1986 (FBTAA 1986), the

depreciation can be computed based on the formula listed below (Deustch et. al., 2016).

The effective life of the car is considered as 8 years while the diminishing depreciation

would be applied @25% p.a.

Based on the given information, Lucinda was given the car on April 1, 2018 and thereby

C and D both would be equal to 365 days. The value for input A would be equal to the

cost of the car which is $ 18,000.

Hence, depreciation on the car for 2018-2019 = 18000*(0.25)*(365/365) = $4,500

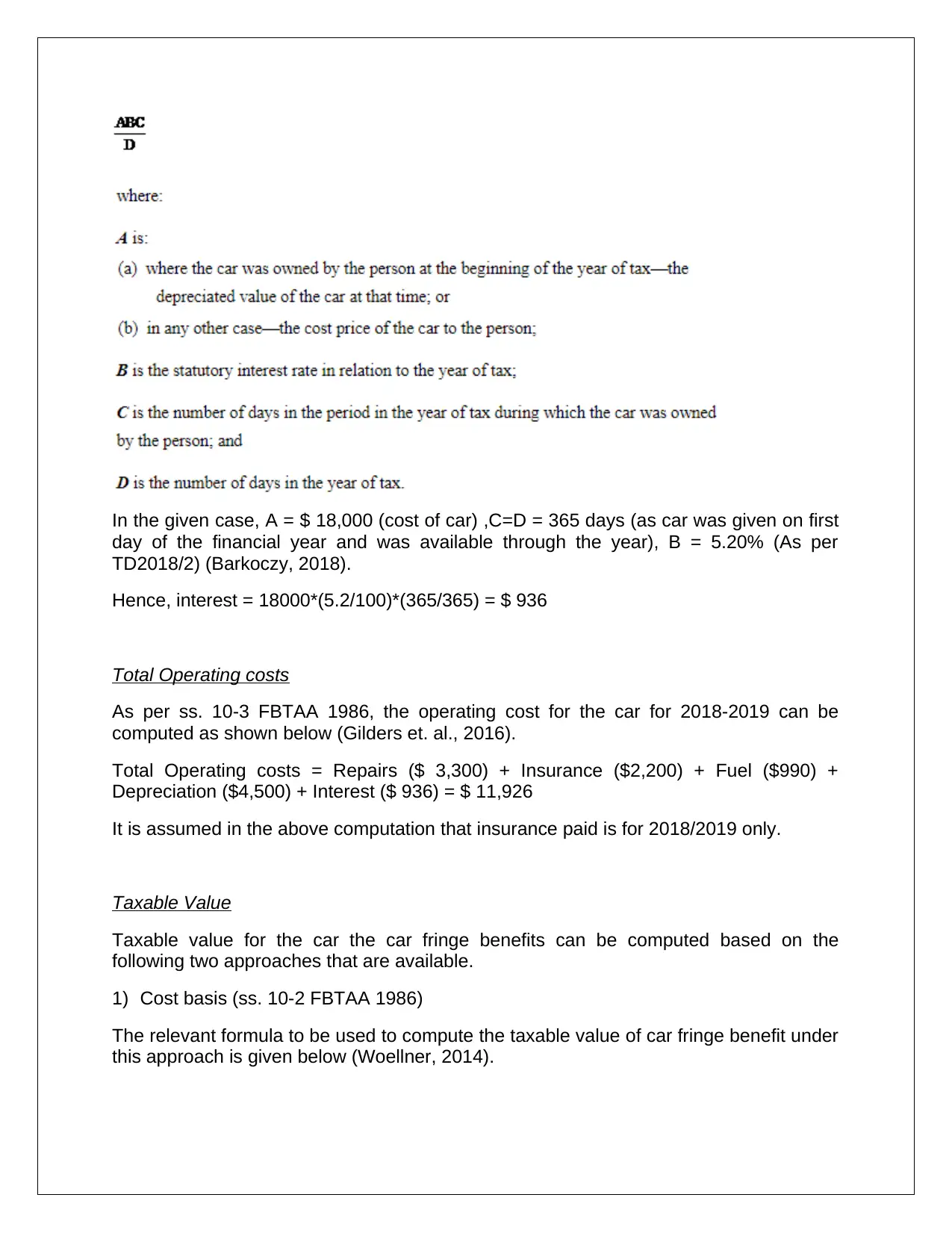

Interest

The formula for interest computation has been highlighted in ss. 11-2 FBTAA 1986 and

has been outlined below (Sadiq et. al., 2016).

The key objective is to ascertain the FBT liability that would arise for Spiceco Pty Ltd on

account of providing a car to their employee Lucinda for private use. The key aspects

related to the computation of car fringe benefit have been discussed below in wake of

the information provided.

Depreciation

With regards to s. 11-1 Fringe Benefit Tax Assessment Act, 1986 (FBTAA 1986), the

depreciation can be computed based on the formula listed below (Deustch et. al., 2016).

The effective life of the car is considered as 8 years while the diminishing depreciation

would be applied @25% p.a.

Based on the given information, Lucinda was given the car on April 1, 2018 and thereby

C and D both would be equal to 365 days. The value for input A would be equal to the

cost of the car which is $ 18,000.

Hence, depreciation on the car for 2018-2019 = 18000*(0.25)*(365/365) = $4,500

Interest

The formula for interest computation has been highlighted in ss. 11-2 FBTAA 1986 and

has been outlined below (Sadiq et. al., 2016).

In the given case, A = $ 18,000 (cost of car) ,C=D = 365 days (as car was given on first

day of the financial year and was available through the year), B = 5.20% (As per

TD2018/2) (Barkoczy, 2018).

Hence, interest = 18000*(5.2/100)*(365/365) = $ 936

Total Operating costs

As per ss. 10-3 FBTAA 1986, the operating cost for the car for 2018-2019 can be

computed as shown below (Gilders et. al., 2016).

Total Operating costs = Repairs ($ 3,300) + Insurance ($2,200) + Fuel ($990) +

Depreciation ($4,500) + Interest ($ 936) = $ 11,926

It is assumed in the above computation that insurance paid is for 2018/2019 only.

Taxable Value

Taxable value for the car the car fringe benefits can be computed based on the

following two approaches that are available.

1) Cost basis (ss. 10-2 FBTAA 1986)

The relevant formula to be used to compute the taxable value of car fringe benefit under

this approach is given below (Woellner, 2014).

day of the financial year and was available through the year), B = 5.20% (As per

TD2018/2) (Barkoczy, 2018).

Hence, interest = 18000*(5.2/100)*(365/365) = $ 936

Total Operating costs

As per ss. 10-3 FBTAA 1986, the operating cost for the car for 2018-2019 can be

computed as shown below (Gilders et. al., 2016).

Total Operating costs = Repairs ($ 3,300) + Insurance ($2,200) + Fuel ($990) +

Depreciation ($4,500) + Interest ($ 936) = $ 11,926

It is assumed in the above computation that insurance paid is for 2018/2019 only.

Taxable Value

Taxable value for the car the car fringe benefits can be computed based on the

following two approaches that are available.

1) Cost basis (ss. 10-2 FBTAA 1986)

The relevant formula to be used to compute the taxable value of car fringe benefit under

this approach is given below (Woellner, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The relevant input values are as follows.

C = $ 11,926, BP = 70%, R = $1,000

Hence, taxable value of car fringe benefit = 11926*(100%-70%) – 1000 = $ 2,578

2) Statutory Formula (s. 9 FBTAA 1986)

The relevant formula to be used to compute the taxable value of car fringe benefit under

this approach is given below (CCH, 2013).

Base value of the car = $ 18,000

Contribution by employee (Lucinda) = $ 1,000

Hence, taxable value of the car fringe benefit =(0.2*18,000*(365/365)) - $ 1,000 = $

2,600

Considering that FBT taxable value is lower for cost basis method, hence it would be

used tor computation of the FBT liability.

C = $ 11,926, BP = 70%, R = $1,000

Hence, taxable value of car fringe benefit = 11926*(100%-70%) – 1000 = $ 2,578

2) Statutory Formula (s. 9 FBTAA 1986)

The relevant formula to be used to compute the taxable value of car fringe benefit under

this approach is given below (CCH, 2013).

Base value of the car = $ 18,000

Contribution by employee (Lucinda) = $ 1,000

Hence, taxable value of the car fringe benefit =(0.2*18,000*(365/365)) - $ 1,000 = $

2,600

Considering that FBT taxable value is lower for cost basis method, hence it would be

used tor computation of the FBT liability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FBT

The taxable value of the car fringe benefit needs to be multiplied by the relevant gross

up factor so as to determine the grossed up taxable value of the car fringe benefit.

Considering that GST is applicable on car, hence it would be recognized as a Type 1

good with the corresponding gross up rate as 2.0802 (ATO, 2019).

Hence, grossed up taxable car fringe benefit = 2578 *2.0802 = $ 5,362.34

FBT liability

For the year ending on March 31, 2019, the FBT rate is 47% (ATO, 2019).

Hence, FBT liability on the employer = $ 5,362.34 * 0.47 = $ 2,520.3

Therefore, the employer needs to pay $ 2,520.3 as FBT with regards to the car fringe

benefit provided to Lucinda.

Question 2

(a) Based on the given information, the objective is to outline the net capital

gains/(losses) made by Daniel on account of the various transactions which he has

entered during the year2018/2019 in order to raise capital for funding his super fund.

The implications of each of the transactions have been discussed in the light of the

applicable statutory law.

1) Sale of house

In relation to sale of house, a key CGT concession that is available is the main

residence exemption that has been outlined in Sub-division 118-B. As per this rule,

100% exemption of CGT may be availed on any capital gains that arise on sale of

house provided the house has been termed as main residence for the whole duration of

the ownership period. The key conditions to be fulfilled in this regards are outlined

below (Gilders et. al., 2016).

Underlying residence must serve as home or main residence for the entire

ownership period (ss. 118-10(1)(b) ITAA 1997)

The dwelling should not have been used for assessable income production

Consider that Daniel has lived in the Doncaster based house for the whole ownership

period of about 30 years, hence it would be fair to conclude that the given house is main

residence and also does not have been used for income production. Therefore, the

capital gains from the house are non-taxable. Also, the payment of $ 85,000 in the form

of advance payment forfeited later would contribute to the capital gains only which

would not have any CGT implication (Nethercott, Richardson and Devos, 2016).

2) Sale of Painting

The taxable value of the car fringe benefit needs to be multiplied by the relevant gross

up factor so as to determine the grossed up taxable value of the car fringe benefit.

Considering that GST is applicable on car, hence it would be recognized as a Type 1

good with the corresponding gross up rate as 2.0802 (ATO, 2019).

Hence, grossed up taxable car fringe benefit = 2578 *2.0802 = $ 5,362.34

FBT liability

For the year ending on March 31, 2019, the FBT rate is 47% (ATO, 2019).

Hence, FBT liability on the employer = $ 5,362.34 * 0.47 = $ 2,520.3

Therefore, the employer needs to pay $ 2,520.3 as FBT with regards to the car fringe

benefit provided to Lucinda.

Question 2

(a) Based on the given information, the objective is to outline the net capital

gains/(losses) made by Daniel on account of the various transactions which he has

entered during the year2018/2019 in order to raise capital for funding his super fund.

The implications of each of the transactions have been discussed in the light of the

applicable statutory law.

1) Sale of house

In relation to sale of house, a key CGT concession that is available is the main

residence exemption that has been outlined in Sub-division 118-B. As per this rule,

100% exemption of CGT may be availed on any capital gains that arise on sale of

house provided the house has been termed as main residence for the whole duration of

the ownership period. The key conditions to be fulfilled in this regards are outlined

below (Gilders et. al., 2016).

Underlying residence must serve as home or main residence for the entire

ownership period (ss. 118-10(1)(b) ITAA 1997)

The dwelling should not have been used for assessable income production

Consider that Daniel has lived in the Doncaster based house for the whole ownership

period of about 30 years, hence it would be fair to conclude that the given house is main

residence and also does not have been used for income production. Therefore, the

capital gains from the house are non-taxable. Also, the payment of $ 85,000 in the form

of advance payment forfeited later would contribute to the capital gains only which

would not have any CGT implication (Nethercott, Richardson and Devos, 2016).

2) Sale of Painting

In accordance with ss.108-10(15) ITAA 1997, painting belongs to an asset class known

as “collectibles”. This particular asset class is recognized as CGT(Capital Gains Tax)

asset. As a result, in accordance with ss. 104-5 ITAA 1997, a A1 CGT event would be

triggered once this asset would be sold. Also, in accordance with the relevant approach

mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be deployed for

determining the extent of capital gains or losses is given below (CCH, 2013).

Capital Gains/(Losses) = Sales proceeds from asset liquidation – Cost base of the

liquidated asset

Another key aspect to note is that as per ss. 149-10 ITAA 1997, no CGT implications

would arise for pre-CGT assets. As a result any capital gains or losses realised on pre-

CGT assets are ignored as these would not be taxed. Pre-CGT assets refer to those

assets which have been purchased before CGT was introduced. The threshold date in

this regards is September 20, 1985 and thereby any assets bought before this cutoff

date would be termed as pre-CGT assets and not levied any CGT (Gilders et. al., 2016).

The painting under consideration has been bought on September 20, 1985 and thereby

would not be considered as a pre-CGT asset. As a result, the capital gains /(losses) on

this painting would be computed in accordance with the formula stated under ss. 104-

10.

Sale proceeds from painting disposal = $ 125,000

Purchase price of painting = $ 15,000

Hence, capital gains realised on painting disposal = $125,000 - $15,000 = $ 110,000

Consider that the holding period of the asset exceeds one year, hence discount method

under Division 15 can be availed which would reduce the taxable value of the capital

gains by 50% but the same would be applied after adjusted of all capital losses from the

current year as well as previous years (CCH, 2013).

3) Sale of luxury yacht

It is evident that the luxury yacht was not a business asset but an asset which was

meant for personal use and enjoyment of Daniel and his associates. As a result, it

would be recognized as a personal use asset as per ss. 108-20(2) ITAA 1997

(Nethercott, Richardson and Devos, 2016).. There are certain specific rules applicable on

computation of capital gains/(losses) for personal use assets. One of these is that the

capital gains derived from personal use assets would be subject to CGT only if the

purchase price of the underlying asset exceeds $ 10,000. Also, in accordance with ss.

108-20(1) ITAA 1997, any capital losses that are made on the disposal of the personal

use asset would be ignored for CGT computation and cannot be used to offset

assessable income or capital gains from any asset class (Deutsch et. al., 2016).. For

the luxury yacht, the purchase price exceeds $ 10,000 and thereby the capital gains

derived on the sale of this asset would be levied CGT. Also, in accordance with the

relevant approach mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be

deployed for determining the extent of capital gains or losses is given below.

as “collectibles”. This particular asset class is recognized as CGT(Capital Gains Tax)

asset. As a result, in accordance with ss. 104-5 ITAA 1997, a A1 CGT event would be

triggered once this asset would be sold. Also, in accordance with the relevant approach

mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be deployed for

determining the extent of capital gains or losses is given below (CCH, 2013).

Capital Gains/(Losses) = Sales proceeds from asset liquidation – Cost base of the

liquidated asset

Another key aspect to note is that as per ss. 149-10 ITAA 1997, no CGT implications

would arise for pre-CGT assets. As a result any capital gains or losses realised on pre-

CGT assets are ignored as these would not be taxed. Pre-CGT assets refer to those

assets which have been purchased before CGT was introduced. The threshold date in

this regards is September 20, 1985 and thereby any assets bought before this cutoff

date would be termed as pre-CGT assets and not levied any CGT (Gilders et. al., 2016).

The painting under consideration has been bought on September 20, 1985 and thereby

would not be considered as a pre-CGT asset. As a result, the capital gains /(losses) on

this painting would be computed in accordance with the formula stated under ss. 104-

10.

Sale proceeds from painting disposal = $ 125,000

Purchase price of painting = $ 15,000

Hence, capital gains realised on painting disposal = $125,000 - $15,000 = $ 110,000

Consider that the holding period of the asset exceeds one year, hence discount method

under Division 15 can be availed which would reduce the taxable value of the capital

gains by 50% but the same would be applied after adjusted of all capital losses from the

current year as well as previous years (CCH, 2013).

3) Sale of luxury yacht

It is evident that the luxury yacht was not a business asset but an asset which was

meant for personal use and enjoyment of Daniel and his associates. As a result, it

would be recognized as a personal use asset as per ss. 108-20(2) ITAA 1997

(Nethercott, Richardson and Devos, 2016).. There are certain specific rules applicable on

computation of capital gains/(losses) for personal use assets. One of these is that the

capital gains derived from personal use assets would be subject to CGT only if the

purchase price of the underlying asset exceeds $ 10,000. Also, in accordance with ss.

108-20(1) ITAA 1997, any capital losses that are made on the disposal of the personal

use asset would be ignored for CGT computation and cannot be used to offset

assessable income or capital gains from any asset class (Deutsch et. al., 2016).. For

the luxury yacht, the purchase price exceeds $ 10,000 and thereby the capital gains

derived on the sale of this asset would be levied CGT. Also, in accordance with the

relevant approach mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be

deployed for determining the extent of capital gains or losses is given below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital Gains/(Losses) = Sales proceeds from asset liquidation – Cost base of the

liquidated asset

Sales proceeds from luxury yacht disposal = $ 60,000

Cost base of luxury yacht = $ 110,000

Since the sales proceeds are lower than the cost base, hence it can be concluded that

Daniel would realise capital losses on the sale of luxury yacht which would be discarded

and would have no CGT implication.

4) Sale of shares

Share is a CGT asset whose disposal would result in trigger in the form of A1 CGT

event as per ss.104-5 ITAA 1997. Also, in accordance with the relevant approach

mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be deployed for

determining the extent of capital gains or losses is given below.

Capital Gains/(Losses) = Sales proceeds from asset liquidation – Cost base of the

liquidated asset

The various elements of cost base of a given asset have been outlined in s. 110-25(2)

ITAA 1997. The five elements in this regards are summarized below (Barkoczy, 2018).

Amount paid to acquire the asset

Incidental costs related to buying or selling of asset

Any cost that have been incurred with regards to retaining the asset ownership

such as interest costs, taxes etc.

Capital expenditure incurred in enhancing the asset value or to move the same.

Capital expenditure that has been incurred with regards to maintaining the legal

title over the asset.

In view of the above five elements of cost base, the cost base for the BHP shares ought

to be outlined which has been carried out as shown below.

Purchase price = $ 75,000

Incidental cost related to buying and selling of asset = $ 250 (Stamp Duty) + $ 750

(Brokerage) = $1,000

Costs related to share ownership = Interest cost to be tune of $ 5,000 which is

otherwise non-deductible

Hence, cost base of BHP shares = $ 75,000 + $ 1,000 + $ 5,000 = $ 81,000

Sales proceeds from BHP shares liquidation = $ 80,000

Capital losses from sale of shares = $ 81,000 - $ 80,000 = $ 1,000

liquidated asset

Sales proceeds from luxury yacht disposal = $ 60,000

Cost base of luxury yacht = $ 110,000

Since the sales proceeds are lower than the cost base, hence it can be concluded that

Daniel would realise capital losses on the sale of luxury yacht which would be discarded

and would have no CGT implication.

4) Sale of shares

Share is a CGT asset whose disposal would result in trigger in the form of A1 CGT

event as per ss.104-5 ITAA 1997. Also, in accordance with the relevant approach

mentioned in ss. 104-10 ITAA 1997, the appropriate formula to be deployed for

determining the extent of capital gains or losses is given below.

Capital Gains/(Losses) = Sales proceeds from asset liquidation – Cost base of the

liquidated asset

The various elements of cost base of a given asset have been outlined in s. 110-25(2)

ITAA 1997. The five elements in this regards are summarized below (Barkoczy, 2018).

Amount paid to acquire the asset

Incidental costs related to buying or selling of asset

Any cost that have been incurred with regards to retaining the asset ownership

such as interest costs, taxes etc.

Capital expenditure incurred in enhancing the asset value or to move the same.

Capital expenditure that has been incurred with regards to maintaining the legal

title over the asset.

In view of the above five elements of cost base, the cost base for the BHP shares ought

to be outlined which has been carried out as shown below.

Purchase price = $ 75,000

Incidental cost related to buying and selling of asset = $ 250 (Stamp Duty) + $ 750

(Brokerage) = $1,000

Costs related to share ownership = Interest cost to be tune of $ 5,000 which is

otherwise non-deductible

Hence, cost base of BHP shares = $ 75,000 + $ 1,000 + $ 5,000 = $ 81,000

Sales proceeds from BHP shares liquidation = $ 80,000

Capital losses from sale of shares = $ 81,000 - $ 80,000 = $ 1,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net capital gains/(losses) for Daniel for 2018-2019

Taxable Capital gains from disposal of painting = $ 110,000

Capital losses from BHP shares sale = $ 1,000

Losses forwarded on AZJ shares from 2017-2018 = $ 10,000

Hence, net capital gains after offsetting capital losses on shares = 110,000 – $10,000 -

$ 1,000 = $ 99,000

Considering that capital gains on the painting is long term, hence based on the discount

method, a 50% rebate would be available to individual taxpayer Daniel which would

reduce the taxable capital gains (CCH, 2013).

Taxable capital gains for Daniel in 2018-2019 = (50/100)*99,000 = $ 44,500

(b) In case of a capital gain in the given financial year, Daniel would need to pay capital

gains tax which would be levied at the marginal tax rate which would apply on him

based on his taxable income from other sources. It is imperative that the capital

gains should be adjusted using the discount method which can potentially reduce

the CGT liability of individual taxpayers like Daniel by 50%. The use of this provision

has been exhibited in the previous part (Woellner, 2014).

(c) In case of a capital loss in the given financial year, then the same needs to be carry

forwarded in the next year so that it can be offset against potential capital gains in

the future years. It is imperative to note that any capital loss cannot be used to offset

assessable income based on revenue receipts. Additionally, capital losses cannot be

used to demand any tax refunds since they can only be adjusted against capital

gains. Thereby if requisite capital gains are not available in the current year for

offsetting , then these would be carried forward each year till the same if offset. Also,

for certain asset classes such as collectible, capital losses can be offset against

capital gains arising from capital gains on collectibles only (Deutsch et. al., 2016).

Taxable Capital gains from disposal of painting = $ 110,000

Capital losses from BHP shares sale = $ 1,000

Losses forwarded on AZJ shares from 2017-2018 = $ 10,000

Hence, net capital gains after offsetting capital losses on shares = 110,000 – $10,000 -

$ 1,000 = $ 99,000

Considering that capital gains on the painting is long term, hence based on the discount

method, a 50% rebate would be available to individual taxpayer Daniel which would

reduce the taxable capital gains (CCH, 2013).

Taxable capital gains for Daniel in 2018-2019 = (50/100)*99,000 = $ 44,500

(b) In case of a capital gain in the given financial year, Daniel would need to pay capital

gains tax which would be levied at the marginal tax rate which would apply on him

based on his taxable income from other sources. It is imperative that the capital

gains should be adjusted using the discount method which can potentially reduce

the CGT liability of individual taxpayers like Daniel by 50%. The use of this provision

has been exhibited in the previous part (Woellner, 2014).

(c) In case of a capital loss in the given financial year, then the same needs to be carry

forwarded in the next year so that it can be offset against potential capital gains in

the future years. It is imperative to note that any capital loss cannot be used to offset

assessable income based on revenue receipts. Additionally, capital losses cannot be

used to demand any tax refunds since they can only be adjusted against capital

gains. Thereby if requisite capital gains are not available in the current year for

offsetting , then these would be carried forward each year till the same if offset. Also,

for certain asset classes such as collectible, capital losses can be offset against

capital gains arising from capital gains on collectibles only (Deutsch et. al., 2016).

References

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/ [Assessed May 25, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications, pp. 156, 190, 271

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer, pp.

178, 228-229

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax

handbook 8th ed., Pymont: Thomson Reuters, pp.223, 267-268

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding

taxation law 2016, 9th ed., Sydney: LexisNexis/Butterworths, pp. 173, 224

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual

2016, 4th ed., Sydney: Oxford University Press, pp. 167, 234

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters, pp. 232-

233, 289

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

pp. 167, 245, 312

ATO (2019) Fringe benefits tax – rates and thresholds, [online] Available at

https://www.ato.gov.au/Rates/FBT/ [Assessed May 25, 2019]

Barkoczy, S. (2018), Foundation of Taxation Law 2018, 9thed.,NorthRyde: CCH

Publications, pp. 156, 190, 271

CCH (2013), Australian Master Tax Guide 2013, 51st ed., Sydney: Wolters Kluwer, pp.

178, 228-229

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2016), Australian tax

handbook 8th ed., Pymont: Thomson Reuters, pp.223, 267-268

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016), Understanding

taxation law 2016, 9th ed., Sydney: LexisNexis/Butterworths, pp. 173, 224

Nethercott, L., Richardson, G. and Devos, K. (2016), Australian Taxation Study Manual

2016, 4th ed., Sydney: Oxford University Press, pp. 167, 234

Sadiq, K, Coleman, C, Hanegbi, R, Jogarajan, S, Krever, R, Obst, W, and Ting, A

(2016) , Principles of Taxation Law 2016, 8th ed., Pymont:Thomson Reuters, pp. 232-

233, 289

Woellner, R (2014), Australian taxation law 2014, 7th ed., North Ryde: CCH Australia,

pp. 167, 245, 312

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.