Holmes Institute Taxation Law Assignment - HA3042, T2 2019, Australia

VerifiedAdded on 2022/10/14

|12

|2918

|291

Homework Assignment

AI Summary

This taxation law assignment addresses two key questions. The first question analyzes the capital gains tax (CGT) implications for an individual, Jasmine, who is departing from Australia. It covers the sale of her main home (pre-CGT asset), a car (personal use asset), a cleaning business (small business), furniture, and paintings (collectables), assessing the applicability of CGT and small business concessions. The second question focuses on depreciation, specifically whether a taxpayer, John, who is a producer of BMW motor parts, can claim the decline in value of a CNC machine. The analysis considers the relevant income tax laws, depreciating assets, cost base elements, and assessable purposes to determine the eligibility for depreciation deductions. The assignment provides detailed explanations, legal references, and applications of tax principles to specific scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Response A: Sale of main home:

The broader concept of the CGT comprises of making the comparison against the

capital proceeds and the cost base of the asset. The taxpayers are required to denote that

capital gains or loss must be ascertained by subtracting the correct cost base associated to the

asset or any other associated events that is rising from the proceeds following the sale of

assets (Allerdice 2014). As a common rule, the application of taxing capital gains is usually

made in those circumstances when the CGT event happens after the 20 sept. 1985. This

contributes to the fact there are terms such as pre and post CGT is very commonly used for

referring the assets that is purchased or events that are taking place before that date. The

taxpayer is required to understand that the system of CGT is completely dependent on the

capital gains or loss that are happening from selling of assets.

To ascertain the capital gains tax liability of Jasmine, it is eminent that she is

departing from Australia on a permanent basis but prior to her departure there were numerous

assets which she has decided to sell. Eminently, Jasmine sells her home for $3,00,000 that

she has been using from a long time. In the year 1981 Jasmine buys it for $40,000. As a

matter of fact, the asset must be treated as the pre-CGT asset and the capital gains which

Jasmine has realised from selling the main residence will be excluded from tax.

Response B: Sale of Car

The primary step associated to the determination of the CGT is to know whether there

has been any occurrence of CGT event. More specially a “CGT event A1” under “sec 104-10

(1), ITA Act 97” is applied on the capital gains or loss derived from at the time of event

(Middleton 2018). The explanation regarding the personal use asset (PUA’s) is made in “Sub

Div 108-C”. Considering, “sec.108.20 (2)”, personal use asset is recognized as non-

Answer to question 1:

Response A: Sale of main home:

The broader concept of the CGT comprises of making the comparison against the

capital proceeds and the cost base of the asset. The taxpayers are required to denote that

capital gains or loss must be ascertained by subtracting the correct cost base associated to the

asset or any other associated events that is rising from the proceeds following the sale of

assets (Allerdice 2014). As a common rule, the application of taxing capital gains is usually

made in those circumstances when the CGT event happens after the 20 sept. 1985. This

contributes to the fact there are terms such as pre and post CGT is very commonly used for

referring the assets that is purchased or events that are taking place before that date. The

taxpayer is required to understand that the system of CGT is completely dependent on the

capital gains or loss that are happening from selling of assets.

To ascertain the capital gains tax liability of Jasmine, it is eminent that she is

departing from Australia on a permanent basis but prior to her departure there were numerous

assets which she has decided to sell. Eminently, Jasmine sells her home for $3,00,000 that

she has been using from a long time. In the year 1981 Jasmine buys it for $40,000. As a

matter of fact, the asset must be treated as the pre-CGT asset and the capital gains which

Jasmine has realised from selling the main residence will be excluded from tax.

Response B: Sale of Car

The primary step associated to the determination of the CGT is to know whether there

has been any occurrence of CGT event. More specially a “CGT event A1” under “sec 104-10

(1), ITA Act 97” is applied on the capital gains or loss derived from at the time of event

(Middleton 2018). The explanation regarding the personal use asset (PUA’s) is made in “Sub

Div 108-C”. Considering, “sec.108.20 (2)”, personal use asset is recognized as non-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

collectable asset. These type of asset is used by taxpayer chiefly for own amusement. The list

of assets under this heads include the boats, furniture, electrical goods, vehicles and domestic

use assets. If a circumstances arises where a PUA’s is disposed on loss, no offset can be

claimed by the taxpayer in this regard from the capital gains. Under “sec 108.20 (1)” the loss

is clearly ignored.

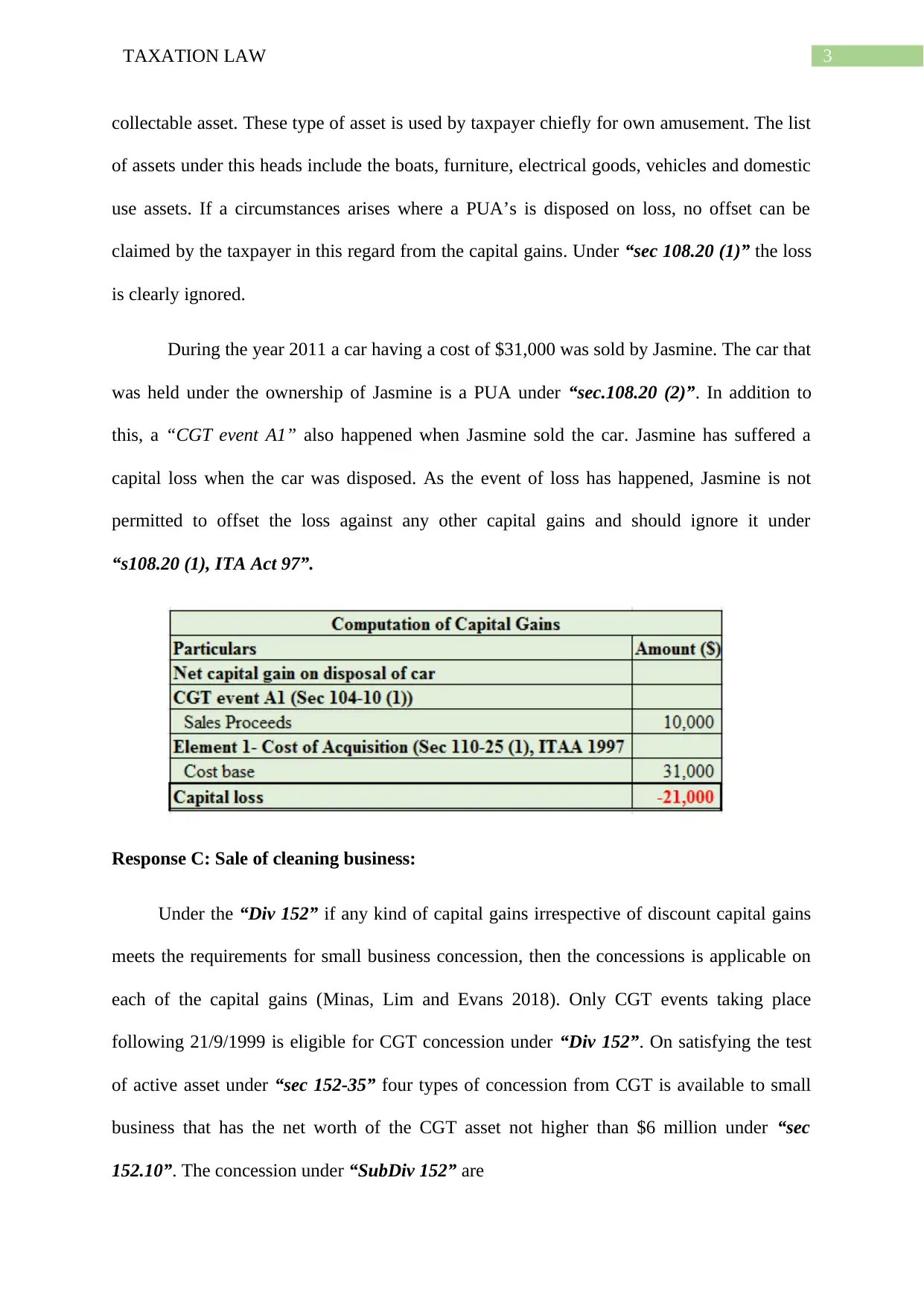

During the year 2011 a car having a cost of $31,000 was sold by Jasmine. The car that

was held under the ownership of Jasmine is a PUA under “sec.108.20 (2)”. In addition to

this, a “CGT event A1” also happened when Jasmine sold the car. Jasmine has suffered a

capital loss when the car was disposed. As the event of loss has happened, Jasmine is not

permitted to offset the loss against any other capital gains and should ignore it under

“s108.20 (1), ITA Act 97”.

Response C: Sale of cleaning business:

Under the “Div 152” if any kind of capital gains irrespective of discount capital gains

meets the requirements for small business concession, then the concessions is applicable on

each of the capital gains (Minas, Lim and Evans 2018). Only CGT events taking place

following 21/9/1999 is eligible for CGT concession under “Div 152”. On satisfying the test

of active asset under “sec 152-35” four types of concession from CGT is available to small

business that has the net worth of the CGT asset not higher than $6 million under “sec

152.10”. The concession under “SubDiv 152” are

collectable asset. These type of asset is used by taxpayer chiefly for own amusement. The list

of assets under this heads include the boats, furniture, electrical goods, vehicles and domestic

use assets. If a circumstances arises where a PUA’s is disposed on loss, no offset can be

claimed by the taxpayer in this regard from the capital gains. Under “sec 108.20 (1)” the loss

is clearly ignored.

During the year 2011 a car having a cost of $31,000 was sold by Jasmine. The car that

was held under the ownership of Jasmine is a PUA under “sec.108.20 (2)”. In addition to

this, a “CGT event A1” also happened when Jasmine sold the car. Jasmine has suffered a

capital loss when the car was disposed. As the event of loss has happened, Jasmine is not

permitted to offset the loss against any other capital gains and should ignore it under

“s108.20 (1), ITA Act 97”.

Response C: Sale of cleaning business:

Under the “Div 152” if any kind of capital gains irrespective of discount capital gains

meets the requirements for small business concession, then the concessions is applicable on

each of the capital gains (Minas, Lim and Evans 2018). Only CGT events taking place

following 21/9/1999 is eligible for CGT concession under “Div 152”. On satisfying the test

of active asset under “sec 152-35” four types of concession from CGT is available to small

business that has the net worth of the CGT asset not higher than $6 million under “sec

152.10”. The concession under “SubDiv 152” are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

15-year exemption from CGT

50% reduction from CGT

Retirement exemption from CGT

Roll-over concession from CGT when purchasing replacement asset from that

proceeds.

As it has been noticed in the case of Jasmine it is found that prior to her leaving

Australia, Jasmine was operating a small business of cleaning. On finding a buyer the

business was sold for a deal of $125,000. The business of Jasmine qualifies as the small

entity under “sec 152.10, ITA Act 97” (Mangioni 2015). Additionally, the business of

Jasmine also meets the active asset test under “sec 152.35, ITA Act 1997”. Referring to “sec

152-10” the net value of Jasmine’s business assets is not more than $6 million.

Jasmine is eligible for claiming the 15-year exemption under “Sub div 152-B” from

the capital gains made for the reason that all the assets were owned by her for a minimum of

15 years. She is also entitled to retirement exemption under “Sub div 152-D” since she is

retiring from her small cleaning business.

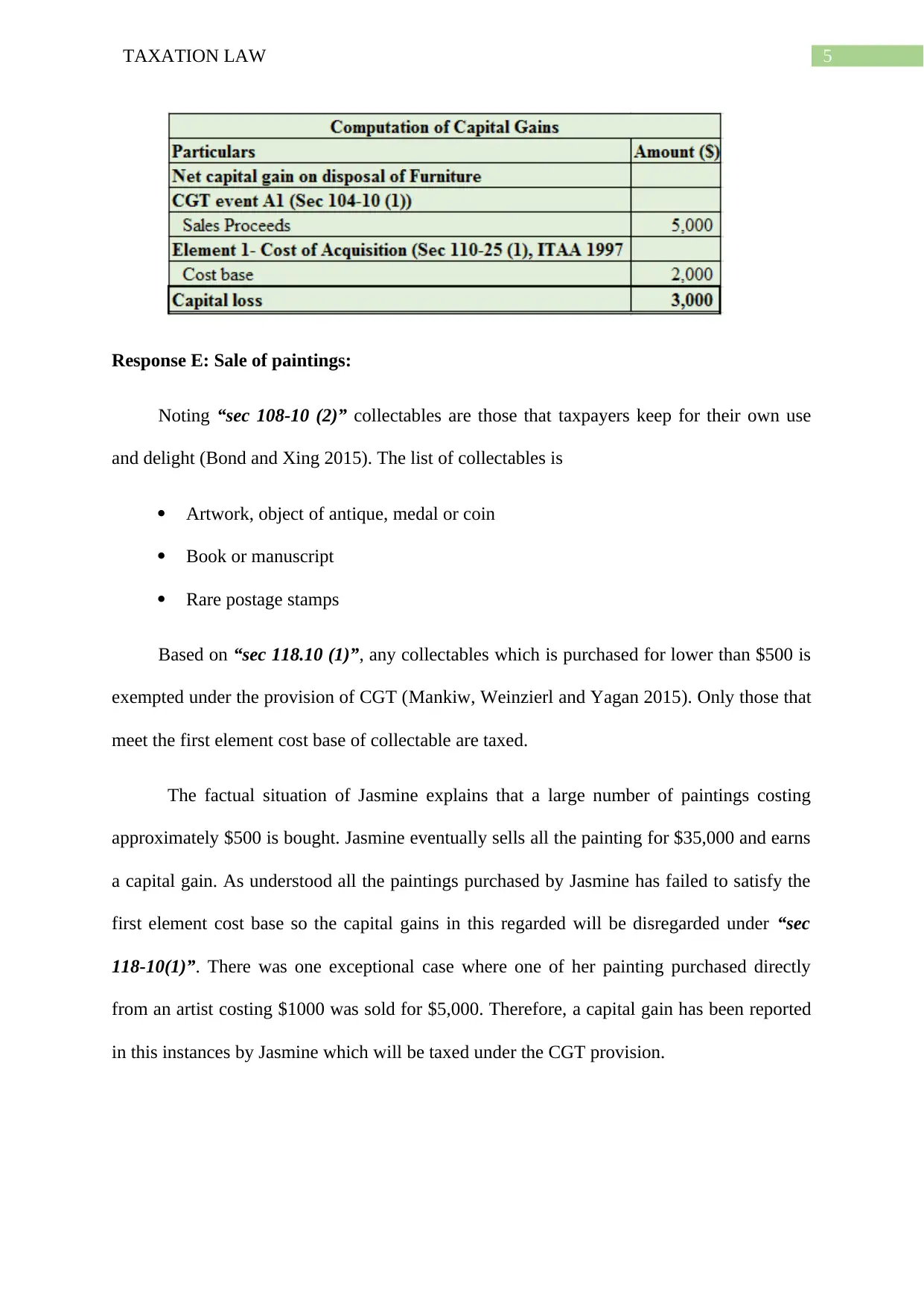

Response D: Sale of Furniture:

As explained in the “sec 118.10 (3), ITA Act 1997” capital gains that is yielded from

the PUA’s that is having the purchase value of $10,000 or lower have to be purely ignored

(Mclaren 2015). This implies that the taxpayer is under the obligation of keeping the details

of the asset which is purchased for greater than $10,000. As a matter of fact, a furniture that

was the acquisition price of $2,000 was disposed for $5,000 by Jasmine. It can be stated from

the fact that Jasmine has realised a capital gain from selling the furniture. But it must be

noted that capital gains will be ignored under “sec 118.10 (3)”, because the furniture has fail

to meet the first element cost base of $10,000.

15-year exemption from CGT

50% reduction from CGT

Retirement exemption from CGT

Roll-over concession from CGT when purchasing replacement asset from that

proceeds.

As it has been noticed in the case of Jasmine it is found that prior to her leaving

Australia, Jasmine was operating a small business of cleaning. On finding a buyer the

business was sold for a deal of $125,000. The business of Jasmine qualifies as the small

entity under “sec 152.10, ITA Act 97” (Mangioni 2015). Additionally, the business of

Jasmine also meets the active asset test under “sec 152.35, ITA Act 1997”. Referring to “sec

152-10” the net value of Jasmine’s business assets is not more than $6 million.

Jasmine is eligible for claiming the 15-year exemption under “Sub div 152-B” from

the capital gains made for the reason that all the assets were owned by her for a minimum of

15 years. She is also entitled to retirement exemption under “Sub div 152-D” since she is

retiring from her small cleaning business.

Response D: Sale of Furniture:

As explained in the “sec 118.10 (3), ITA Act 1997” capital gains that is yielded from

the PUA’s that is having the purchase value of $10,000 or lower have to be purely ignored

(Mclaren 2015). This implies that the taxpayer is under the obligation of keeping the details

of the asset which is purchased for greater than $10,000. As a matter of fact, a furniture that

was the acquisition price of $2,000 was disposed for $5,000 by Jasmine. It can be stated from

the fact that Jasmine has realised a capital gain from selling the furniture. But it must be

noted that capital gains will be ignored under “sec 118.10 (3)”, because the furniture has fail

to meet the first element cost base of $10,000.

5TAXATION LAW

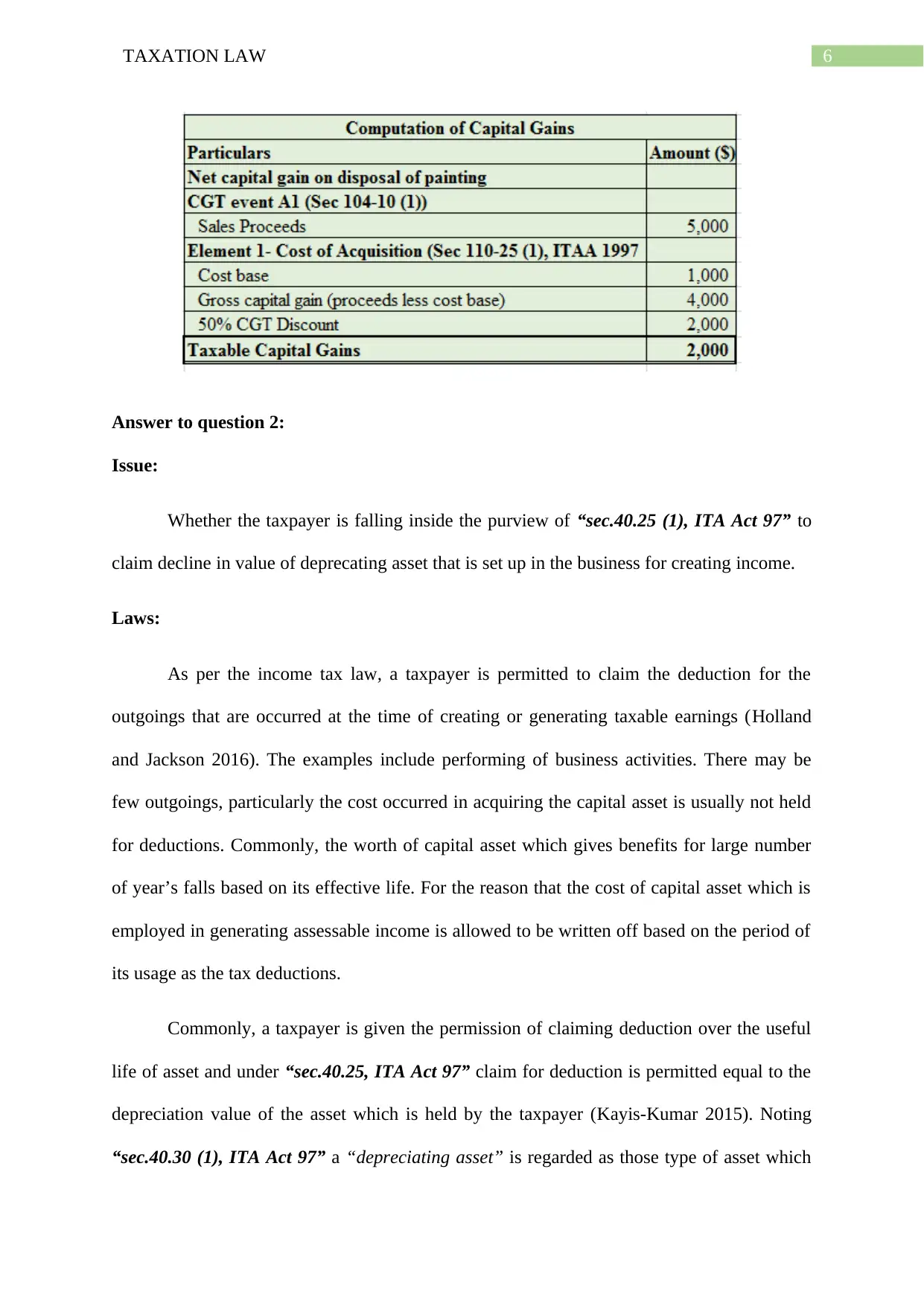

Response E: Sale of paintings:

Noting “sec 108-10 (2)” collectables are those that taxpayers keep for their own use

and delight (Bond and Xing 2015). The list of collectables is

Artwork, object of antique, medal or coin

Book or manuscript

Rare postage stamps

Based on “sec 118.10 (1)”, any collectables which is purchased for lower than $500 is

exempted under the provision of CGT (Mankiw, Weinzierl and Yagan 2015). Only those that

meet the first element cost base of collectable are taxed.

The factual situation of Jasmine explains that a large number of paintings costing

approximately $500 is bought. Jasmine eventually sells all the painting for $35,000 and earns

a capital gain. As understood all the paintings purchased by Jasmine has failed to satisfy the

first element cost base so the capital gains in this regarded will be disregarded under “sec

118-10(1)”. There was one exceptional case where one of her painting purchased directly

from an artist costing $1000 was sold for $5,000. Therefore, a capital gain has been reported

in this instances by Jasmine which will be taxed under the CGT provision.

Response E: Sale of paintings:

Noting “sec 108-10 (2)” collectables are those that taxpayers keep for their own use

and delight (Bond and Xing 2015). The list of collectables is

Artwork, object of antique, medal or coin

Book or manuscript

Rare postage stamps

Based on “sec 118.10 (1)”, any collectables which is purchased for lower than $500 is

exempted under the provision of CGT (Mankiw, Weinzierl and Yagan 2015). Only those that

meet the first element cost base of collectable are taxed.

The factual situation of Jasmine explains that a large number of paintings costing

approximately $500 is bought. Jasmine eventually sells all the painting for $35,000 and earns

a capital gain. As understood all the paintings purchased by Jasmine has failed to satisfy the

first element cost base so the capital gains in this regarded will be disregarded under “sec

118-10(1)”. There was one exceptional case where one of her painting purchased directly

from an artist costing $1000 was sold for $5,000. Therefore, a capital gain has been reported

in this instances by Jasmine which will be taxed under the CGT provision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 2:

Issue:

Whether the taxpayer is falling inside the purview of “sec.40.25 (1), ITA Act 97” to

claim decline in value of deprecating asset that is set up in the business for creating income.

Laws:

As per the income tax law, a taxpayer is permitted to claim the deduction for the

outgoings that are occurred at the time of creating or generating taxable earnings (Holland

and Jackson 2016). The examples include performing of business activities. There may be

few outgoings, particularly the cost occurred in acquiring the capital asset is usually not held

for deductions. Commonly, the worth of capital asset which gives benefits for large number

of year’s falls based on its effective life. For the reason that the cost of capital asset which is

employed in generating assessable income is allowed to be written off based on the period of

its usage as the tax deductions.

Commonly, a taxpayer is given the permission of claiming deduction over the useful

life of asset and under “sec.40.25, ITA Act 97” claim for deduction is permitted equal to the

depreciation value of the asset which is held by the taxpayer (Kayis-Kumar 2015). Noting

“sec.40.30 (1), ITA Act 97” a “depreciating asset” is regarded as those type of asset which

Answer to question 2:

Issue:

Whether the taxpayer is falling inside the purview of “sec.40.25 (1), ITA Act 97” to

claim decline in value of deprecating asset that is set up in the business for creating income.

Laws:

As per the income tax law, a taxpayer is permitted to claim the deduction for the

outgoings that are occurred at the time of creating or generating taxable earnings (Holland

and Jackson 2016). The examples include performing of business activities. There may be

few outgoings, particularly the cost occurred in acquiring the capital asset is usually not held

for deductions. Commonly, the worth of capital asset which gives benefits for large number

of year’s falls based on its effective life. For the reason that the cost of capital asset which is

employed in generating assessable income is allowed to be written off based on the period of

its usage as the tax deductions.

Commonly, a taxpayer is given the permission of claiming deduction over the useful

life of asset and under “sec.40.25, ITA Act 97” claim for deduction is permitted equal to the

depreciation value of the asset which is held by the taxpayer (Kayis-Kumar 2015). Noting

“sec.40.30 (1), ITA Act 97” a “depreciating asset” is regarded as those type of asset which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

carries a certain life. In “France v Yarmouth (1987)” a depreciating asset normally covers

the concept of plant under “sec 45.40”. The law court in its ordinary sense held that plant

usually includes any kind of apparatus which is used in business for conducting his business

activities (Elliot 2017). The “depreciating asset” is generally anticipated that it will fall in

value till the time the asset is utilized. Under “sec.40.25” depreciation is permitted for

“depreciating asset” only to the holder of the asset. In majority of the situation, the legal

owner of the depreciating asset would be treated as its holder.

Depreciation for the falling value of asset is only permitted as tax deduction when the

asset is used for taxable purpose under “sec.40.25 (2)” (Mcmahon and Mcgovern 2017). One

must denote that under “sec.40.25 (7)” an assessable purpose is most commonly seen when

the asset is utilized for the production of taxable earnings.

“Sub div.40-C” says that the taxpayers are required to denote that depreciation is

permitted on the “depreciating asset” in respect of its cost (Hopkins 2016). In most common

scenarios, the cost of the depreciating asset will not usually comprise of price paid for its

acquisition but would also comprise of the incidental cost involved in the installation as well

as deliver of the asset. The cost base of the “depreciating asset” includes two elements under

“sec.40.175”. These are as follows;

1st Element cost base: The first element cost base of the “depreciating asset” under “sec.

40.180” includes the consideration price which the taxpayer has paid for acquiring or holding

the asset (Pert et al. 2017).

2nd Element cost base: On a general note under “sec.40.190” this element comprises of the

consideration that is given by the taxpayer for setting up or bringing up the asset to its current

location and state based on time to time.

carries a certain life. In “France v Yarmouth (1987)” a depreciating asset normally covers

the concept of plant under “sec 45.40”. The law court in its ordinary sense held that plant

usually includes any kind of apparatus which is used in business for conducting his business

activities (Elliot 2017). The “depreciating asset” is generally anticipated that it will fall in

value till the time the asset is utilized. Under “sec.40.25” depreciation is permitted for

“depreciating asset” only to the holder of the asset. In majority of the situation, the legal

owner of the depreciating asset would be treated as its holder.

Depreciation for the falling value of asset is only permitted as tax deduction when the

asset is used for taxable purpose under “sec.40.25 (2)” (Mcmahon and Mcgovern 2017). One

must denote that under “sec.40.25 (7)” an assessable purpose is most commonly seen when

the asset is utilized for the production of taxable earnings.

“Sub div.40-C” says that the taxpayers are required to denote that depreciation is

permitted on the “depreciating asset” in respect of its cost (Hopkins 2016). In most common

scenarios, the cost of the depreciating asset will not usually comprise of price paid for its

acquisition but would also comprise of the incidental cost involved in the installation as well

as deliver of the asset. The cost base of the “depreciating asset” includes two elements under

“sec.40.175”. These are as follows;

1st Element cost base: The first element cost base of the “depreciating asset” under “sec.

40.180” includes the consideration price which the taxpayer has paid for acquiring or holding

the asset (Pert et al. 2017).

2nd Element cost base: On a general note under “sec.40.190” this element comprises of the

consideration that is given by the taxpayer for setting up or bringing up the asset to its current

location and state based on time to time.

8TAXATION LAW

The fall in value of the “depreciating asset” begins under “sec 40.60 (1)” when the

taxpayer makes the first use of the asset or they have installed the asset as ready to make its

usage for any purpose including the private purpose as well. This is generally referred as the

start time of “depreciating asset”.

Application:

The applicable of the above given laws can be made in the situation of John. The

taxpayer here is the producer of BMW motor parts. The activities of John involves the

manufacturing of vehicle parts and accessories. The taxpayer here John during 1st November

visited CNC factory in Germany to inspect about the CNC machine. Upon the successful

inspection he placed the order of buying the machine. The CNC machine under the laws of

“sec.40.30 (1)” amounts to the depreciating asset. Mentioning the factual situation of

“France v Yarmouth (1987)” in case of John the main reason for classifying the CNC

machine is mainly because it is having a reasonable effective lifespan (Beard and Lucas

2016). The CNC machine will fall in value based on its usage. Furthermore, under “sec 40.25

(7)”, John is permitted to claim the decline in value of CNC machine because the machine

was bought for taxable purpose only.

By referring to “Sub Div.40-C” to determine the depreciation of CNC machine for

capital allowance purpose it is important to take into the account the cost base (Kyle 2016).

The CNC machine bought by John has two cost base element under “sec 40.175”.

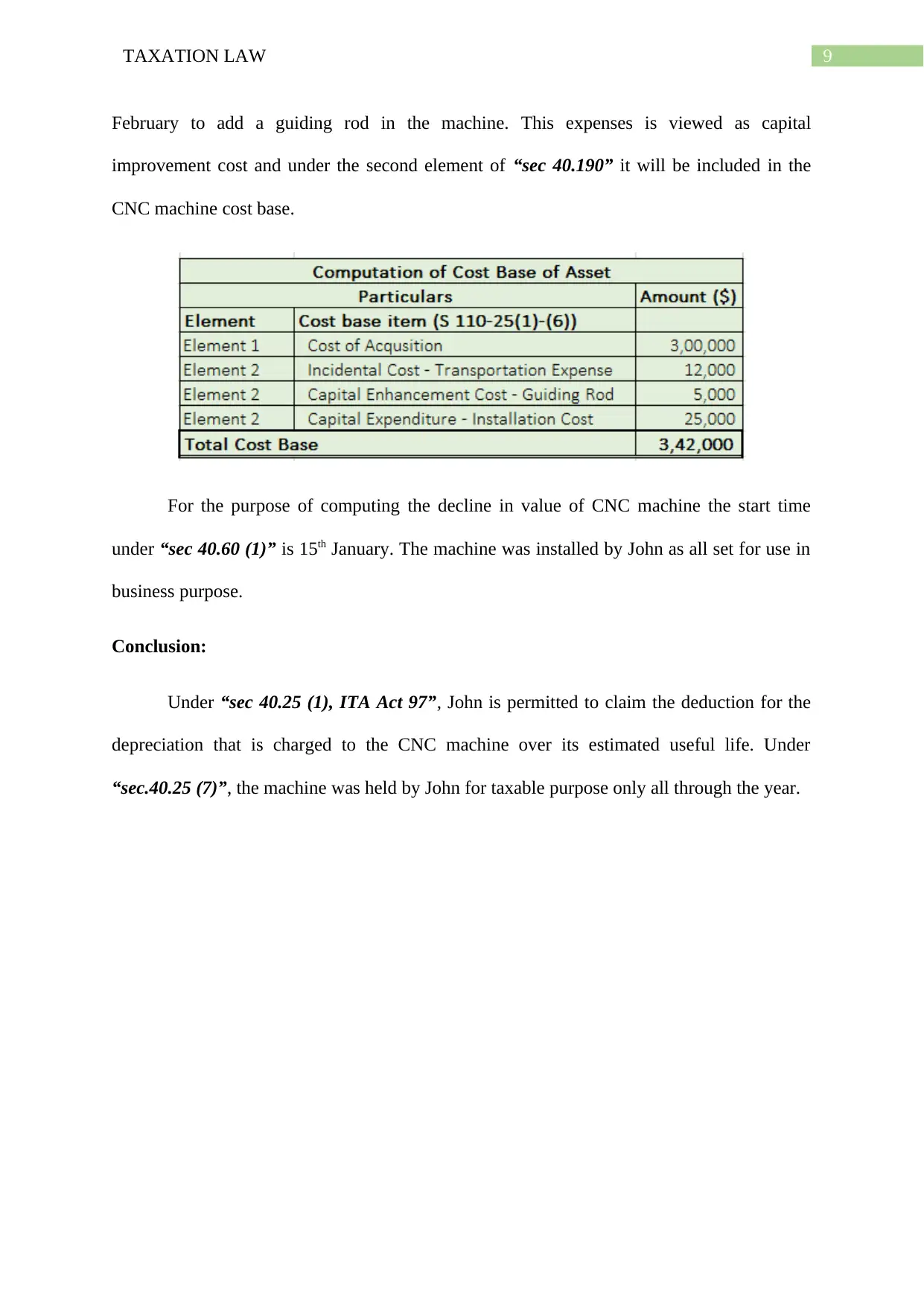

1st Element cost base: This includes under “sec.40.180” the purchase of $300,000 paid by

John as the consideration to hold the CNC machine.

2nd Element Cost base: Under “sec 40.180” the second element cost base of CNC machine

will include the installation expenses of $25,000 that is occurred by John in setting up the

CNC machine in his production factory. John also occurred further expense of $5,000 on 1st

The fall in value of the “depreciating asset” begins under “sec 40.60 (1)” when the

taxpayer makes the first use of the asset or they have installed the asset as ready to make its

usage for any purpose including the private purpose as well. This is generally referred as the

start time of “depreciating asset”.

Application:

The applicable of the above given laws can be made in the situation of John. The

taxpayer here is the producer of BMW motor parts. The activities of John involves the

manufacturing of vehicle parts and accessories. The taxpayer here John during 1st November

visited CNC factory in Germany to inspect about the CNC machine. Upon the successful

inspection he placed the order of buying the machine. The CNC machine under the laws of

“sec.40.30 (1)” amounts to the depreciating asset. Mentioning the factual situation of

“France v Yarmouth (1987)” in case of John the main reason for classifying the CNC

machine is mainly because it is having a reasonable effective lifespan (Beard and Lucas

2016). The CNC machine will fall in value based on its usage. Furthermore, under “sec 40.25

(7)”, John is permitted to claim the decline in value of CNC machine because the machine

was bought for taxable purpose only.

By referring to “Sub Div.40-C” to determine the depreciation of CNC machine for

capital allowance purpose it is important to take into the account the cost base (Kyle 2016).

The CNC machine bought by John has two cost base element under “sec 40.175”.

1st Element cost base: This includes under “sec.40.180” the purchase of $300,000 paid by

John as the consideration to hold the CNC machine.

2nd Element Cost base: Under “sec 40.180” the second element cost base of CNC machine

will include the installation expenses of $25,000 that is occurred by John in setting up the

CNC machine in his production factory. John also occurred further expense of $5,000 on 1st

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

February to add a guiding rod in the machine. This expenses is viewed as capital

improvement cost and under the second element of “sec 40.190” it will be included in the

CNC machine cost base.

For the purpose of computing the decline in value of CNC machine the start time

under “sec 40.60 (1)” is 15th January. The machine was installed by John as all set for use in

business purpose.

Conclusion:

Under “sec 40.25 (1), ITA Act 97”, John is permitted to claim the deduction for the

depreciation that is charged to the CNC machine over its estimated useful life. Under

“sec.40.25 (7)”, the machine was held by John for taxable purpose only all through the year.

February to add a guiding rod in the machine. This expenses is viewed as capital

improvement cost and under the second element of “sec 40.190” it will be included in the

CNC machine cost base.

For the purpose of computing the decline in value of CNC machine the start time

under “sec 40.60 (1)” is 15th January. The machine was installed by John as all set for use in

business purpose.

Conclusion:

Under “sec 40.25 (1), ITA Act 97”, John is permitted to claim the deduction for the

depreciation that is charged to the CNC machine over its estimated useful life. Under

“sec.40.25 (7)”, the machine was held by John for taxable purpose only all through the year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Allerdice, R., 2014. CGT provisions. Marks' Trusts & Estates: Taxation and Practice, p.213.

Beard, R. and Lucas, G.S., 2016. Federal income taxation. Mercer Law Review, 67(4),

pp.929–945.

Bond and Xing, 2015. Corporate taxation and capital accumulation: Evidence from sectoral

panel data for 14 OECD countries. Journal of Public Economics, 130(C), pp.15–31.

Elliot, W.D., 2017. Federal taxation: 2015-2016. Texas Tech Law Review, 49(3), pp.673–

684.

Holland, K. and Jackson, R.H.G., 2016. Taxation influences upon the market in venture

capital trust stocks: theory and practice. Accounting and Business Research, 41(1), pp.1–27.

Hopkins, B.R., 2016. The law of tax-exempt organizations 11th ed.,

Kayis-Kumar, Ann, 2015. Taxing cross-border intercompany transactions: Are financing

activities fungible? Australian Tax Forum, 30(3), pp.627–661.

Kyle, G. 2016. Election Seen As Opening For Federal Tax Reform. The Bond Buyer,

1(F363), pp.The Bond Buyer, April 22, 2016, Vol.1(F363).

Mangioni, V., 2015. A review of the practices of valuers in the assessment of land value for

taxation in Australia.(Statistical data), International Association of Assessing Officers.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2015. Optimal Taxation in Theory and Practice.

The Journal of Economic Perspectives, 23(4), pp.147–174.

Mclaren, J., 2015. The taxation of foreign investment in Australia by sovereign wealth funds:

why has Australia not passed laws enshrining the doctrine of sovereign immunity? Journal of

Australian Taxation, 17(1), p.53.

References:

Allerdice, R., 2014. CGT provisions. Marks' Trusts & Estates: Taxation and Practice, p.213.

Beard, R. and Lucas, G.S., 2016. Federal income taxation. Mercer Law Review, 67(4),

pp.929–945.

Bond and Xing, 2015. Corporate taxation and capital accumulation: Evidence from sectoral

panel data for 14 OECD countries. Journal of Public Economics, 130(C), pp.15–31.

Elliot, W.D., 2017. Federal taxation: 2015-2016. Texas Tech Law Review, 49(3), pp.673–

684.

Holland, K. and Jackson, R.H.G., 2016. Taxation influences upon the market in venture

capital trust stocks: theory and practice. Accounting and Business Research, 41(1), pp.1–27.

Hopkins, B.R., 2016. The law of tax-exempt organizations 11th ed.,

Kayis-Kumar, Ann, 2015. Taxing cross-border intercompany transactions: Are financing

activities fungible? Australian Tax Forum, 30(3), pp.627–661.

Kyle, G. 2016. Election Seen As Opening For Federal Tax Reform. The Bond Buyer,

1(F363), pp.The Bond Buyer, April 22, 2016, Vol.1(F363).

Mangioni, V., 2015. A review of the practices of valuers in the assessment of land value for

taxation in Australia.(Statistical data), International Association of Assessing Officers.

Mankiw, N.G., Weinzierl, M. and Yagan, D., 2015. Optimal Taxation in Theory and Practice.

The Journal of Economic Perspectives, 23(4), pp.147–174.

Mclaren, J., 2015. The taxation of foreign investment in Australia by sovereign wealth funds:

why has Australia not passed laws enshrining the doctrine of sovereign immunity? Journal of

Australian Taxation, 17(1), p.53.

11TAXATION LAW

Mcmahon, M.J.J. and Mcgovern, B.A., 2017. RECENT DEVELOPMENTS IN FEDERAL

INCOME TAXATION: THE YEAR 2016. Florida Tax Review, 20(3), pp.131–276.

Middleton, J., 2018. SME demergers and capital returns. Taxation in Australia, 53(4), p.177.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Pert, Alison, Chen, Helen and Carvosso, Rhys, 2017. 'Federal Commissioner of Taxation v

Seven Network Ltd' (2016) 241 FCR 1. Australian Year Book of International Law, 35,

pp.273–275.

Mcmahon, M.J.J. and Mcgovern, B.A., 2017. RECENT DEVELOPMENTS IN FEDERAL

INCOME TAXATION: THE YEAR 2016. Florida Tax Review, 20(3), pp.131–276.

Middleton, J., 2018. SME demergers and capital returns. Taxation in Australia, 53(4), p.177.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Pert, Alison, Chen, Helen and Carvosso, Rhys, 2017. 'Federal Commissioner of Taxation v

Seven Network Ltd' (2016) 241 FCR 1. Australian Year Book of International Law, 35,

pp.273–275.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.