Taxation Law Assignment: Car FBT, Income Tax, Barter System Analysis

VerifiedAdded on 2020/05/28

|11

|2284

|34

Homework Assignment

AI Summary

This taxation law assignment delves into various aspects of tax law, beginning with a case study on car fringe benefits tax (FBT) for an employee, Charlie, exploring the statutory and operating cost methods for calculating FBT. The assignment then addresses income tax implications for Alan, a locum doctor, who receives non-monetary gifts, such as wine, from patients, determining their inclusion in assessable income. It further analyzes the tax treatment of Betty's marmalade-making business and the criteria for distinguishing between a business and a hobby. Finally, the assignment examines the tax implications of a barter system used by Allan and Betty, considering GST and income tax liabilities. The document provides a comprehensive overview of relevant tax laws, rulings, and case precedents to support its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to requirement 1:...........................................................................................................2

Ascertainment of the Car FBT:..................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement B:..........................................................................................................6

Answer to requirement C:..........................................................................................................7

Answer to requirement D:..........................................................................................................8

Reference List:...........................................................................................................................9

Table of Contents

Answer to requirement 1:...........................................................................................................2

Ascertainment of the Car FBT:..................................................................................................2

Answer to question 2:.................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement B:..........................................................................................................6

Answer to requirement C:..........................................................................................................7

Answer to requirement D:..........................................................................................................8

Reference List:...........................................................................................................................9

2TAXATION LAW

Answer to requirement 1:

As defined in the “Subsection 136 (1) under Fringe Benefit Tax Assessment Act

1986” an employee that uses the car for his personal use and does not relates to the

employment income will constitute a personal use of the vehicle or car (Martin 2014). The

case study opens up with the situation where Charlie is the employee of Shiny Homes and

imparts his duties as the agent of real estate.

Shiny Homes on the other hand, executes the work of landscaping and as the part of

the employment Shiny Homes has provided Charlie with a car. An important consideration of

the section 7 of the FBTAA 1986 provides a that when an employee is provided with a car,

the employee would be liable to fringe benefit tax (Auerbach and Hassett 2015).

Ascertainment of the Car FBT:

The situation of Charlie describes that he was provided with car and has make use of

it for employment and private use. As depicted approximately thirty thousand kilometres

were travel for personal use with fifty thousand kilometres were used for business purpose. In

subsection 136 (1) Car usage by worker or employee will be taxable given that the employee

used the car personally (Tanzi 2014). Subsequently, “para 3 of the FBTAA 1986” puts

forward that cost that is occurred for the work purpose of the car should be mandatorily

logged in the log book as this will account for the kilometres that is travelled for work

purpose in determining the fringe benefit of the car under the operating cost method.

A statutory process can employed to obtain the FBT for car. An important legislation

that is useful in determining the taxable value of fringe benefit is “section 10A and Section

10 B of the FBTAA 1986” where operating method of costing is used (Gahvari and

Micheletto 2016). There has been relavant legislation of “Section 9 of the Miscellaneous

Taxation Ruling 2027” to know the amount of fringe benefit of car. A rate of twenty percent

Answer to requirement 1:

As defined in the “Subsection 136 (1) under Fringe Benefit Tax Assessment Act

1986” an employee that uses the car for his personal use and does not relates to the

employment income will constitute a personal use of the vehicle or car (Martin 2014). The

case study opens up with the situation where Charlie is the employee of Shiny Homes and

imparts his duties as the agent of real estate.

Shiny Homes on the other hand, executes the work of landscaping and as the part of

the employment Shiny Homes has provided Charlie with a car. An important consideration of

the section 7 of the FBTAA 1986 provides a that when an employee is provided with a car,

the employee would be liable to fringe benefit tax (Auerbach and Hassett 2015).

Ascertainment of the Car FBT:

The situation of Charlie describes that he was provided with car and has make use of

it for employment and private use. As depicted approximately thirty thousand kilometres

were travel for personal use with fifty thousand kilometres were used for business purpose. In

subsection 136 (1) Car usage by worker or employee will be taxable given that the employee

used the car personally (Tanzi 2014). Subsequently, “para 3 of the FBTAA 1986” puts

forward that cost that is occurred for the work purpose of the car should be mandatorily

logged in the log book as this will account for the kilometres that is travelled for work

purpose in determining the fringe benefit of the car under the operating cost method.

A statutory process can employed to obtain the FBT for car. An important legislation

that is useful in determining the taxable value of fringe benefit is “section 10A and Section

10 B of the FBTAA 1986” where operating method of costing is used (Gahvari and

Micheletto 2016). There has been relavant legislation of “Section 9 of the Miscellaneous

Taxation Ruling 2027” to know the amount of fringe benefit of car. A rate of twenty percent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

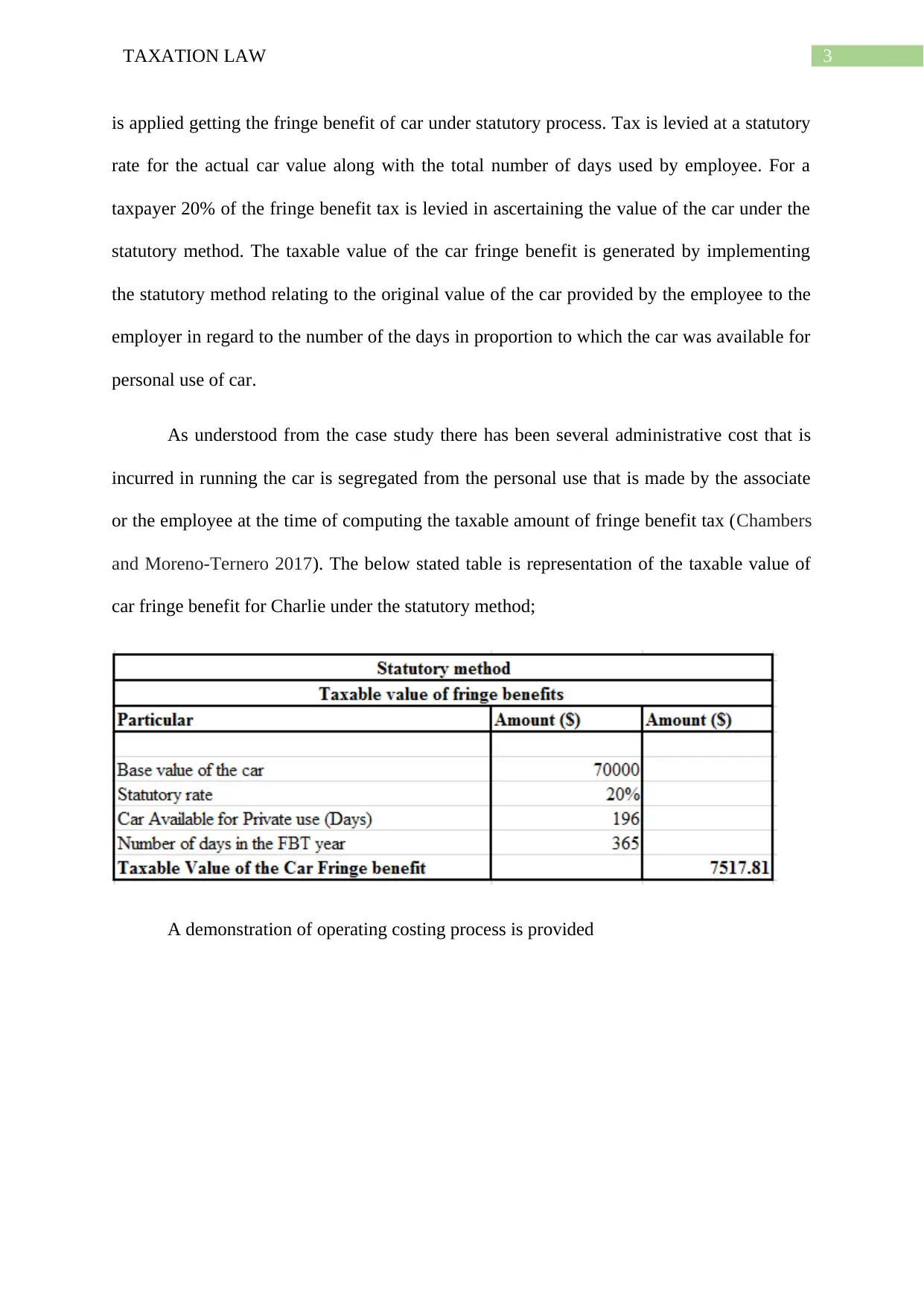

is applied getting the fringe benefit of car under statutory process. Tax is levied at a statutory

rate for the actual car value along with the total number of days used by employee. For a

taxpayer 20% of the fringe benefit tax is levied in ascertaining the value of the car under the

statutory method. The taxable value of the car fringe benefit is generated by implementing

the statutory method relating to the original value of the car provided by the employee to the

employer in regard to the number of the days in proportion to which the car was available for

personal use of car.

As understood from the case study there has been several administrative cost that is

incurred in running the car is segregated from the personal use that is made by the associate

or the employee at the time of computing the taxable amount of fringe benefit tax (Chambers

and Moreno-Ternero 2017). The below stated table is representation of the taxable value of

car fringe benefit for Charlie under the statutory method;

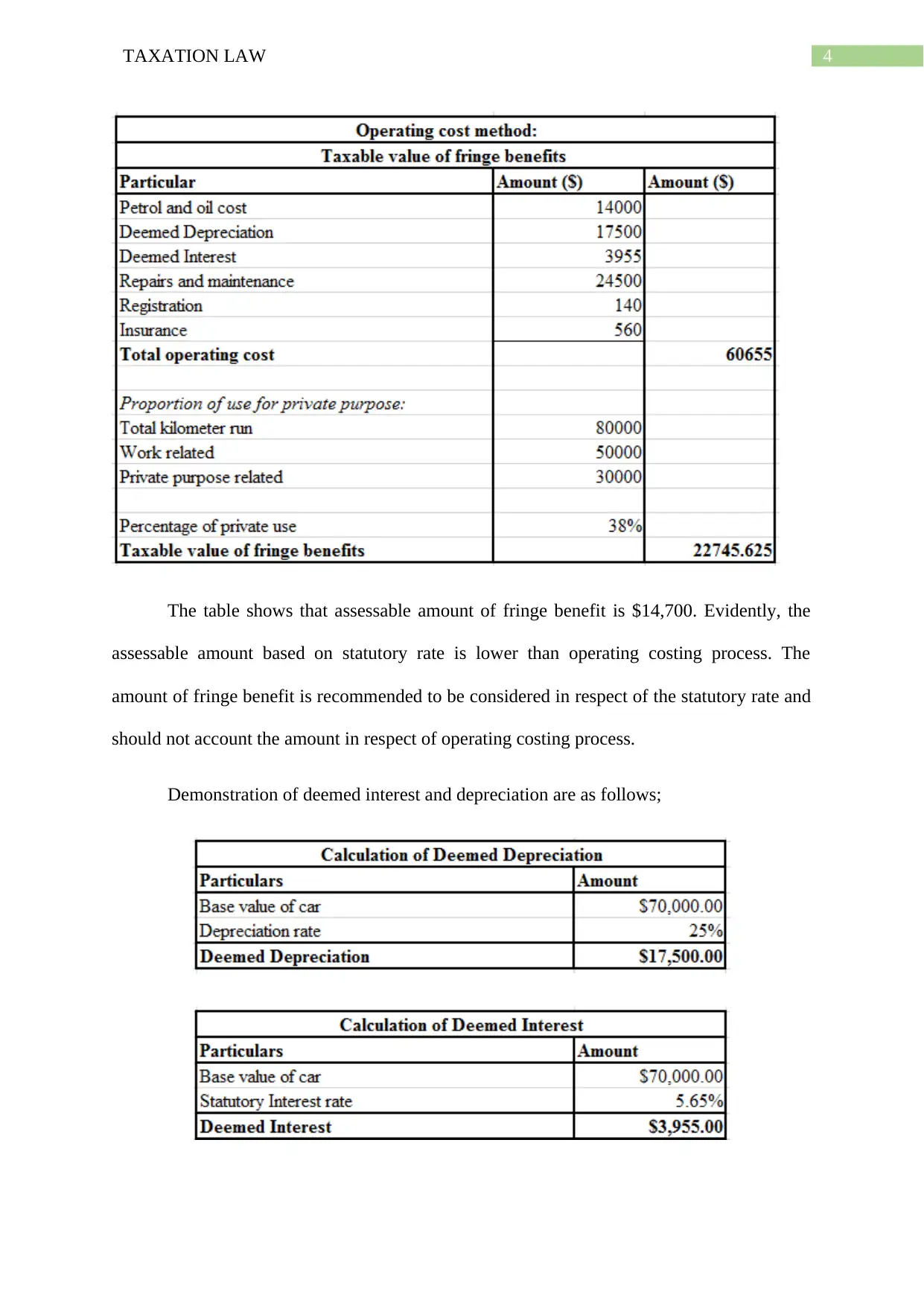

A demonstration of operating costing process is provided

is applied getting the fringe benefit of car under statutory process. Tax is levied at a statutory

rate for the actual car value along with the total number of days used by employee. For a

taxpayer 20% of the fringe benefit tax is levied in ascertaining the value of the car under the

statutory method. The taxable value of the car fringe benefit is generated by implementing

the statutory method relating to the original value of the car provided by the employee to the

employer in regard to the number of the days in proportion to which the car was available for

personal use of car.

As understood from the case study there has been several administrative cost that is

incurred in running the car is segregated from the personal use that is made by the associate

or the employee at the time of computing the taxable amount of fringe benefit tax (Chambers

and Moreno-Ternero 2017). The below stated table is representation of the taxable value of

car fringe benefit for Charlie under the statutory method;

A demonstration of operating costing process is provided

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The table shows that assessable amount of fringe benefit is $14,700. Evidently, the

assessable amount based on statutory rate is lower than operating costing process. The

amount of fringe benefit is recommended to be considered in respect of the statutory rate and

should not account the amount in respect of operating costing process.

Demonstration of deemed interest and depreciation are as follows;

The table shows that assessable amount of fringe benefit is $14,700. Evidently, the

assessable amount based on statutory rate is lower than operating costing process. The

amount of fringe benefit is recommended to be considered in respect of the statutory rate and

should not account the amount in respect of operating costing process.

Demonstration of deemed interest and depreciation are as follows;

5TAXATION LAW

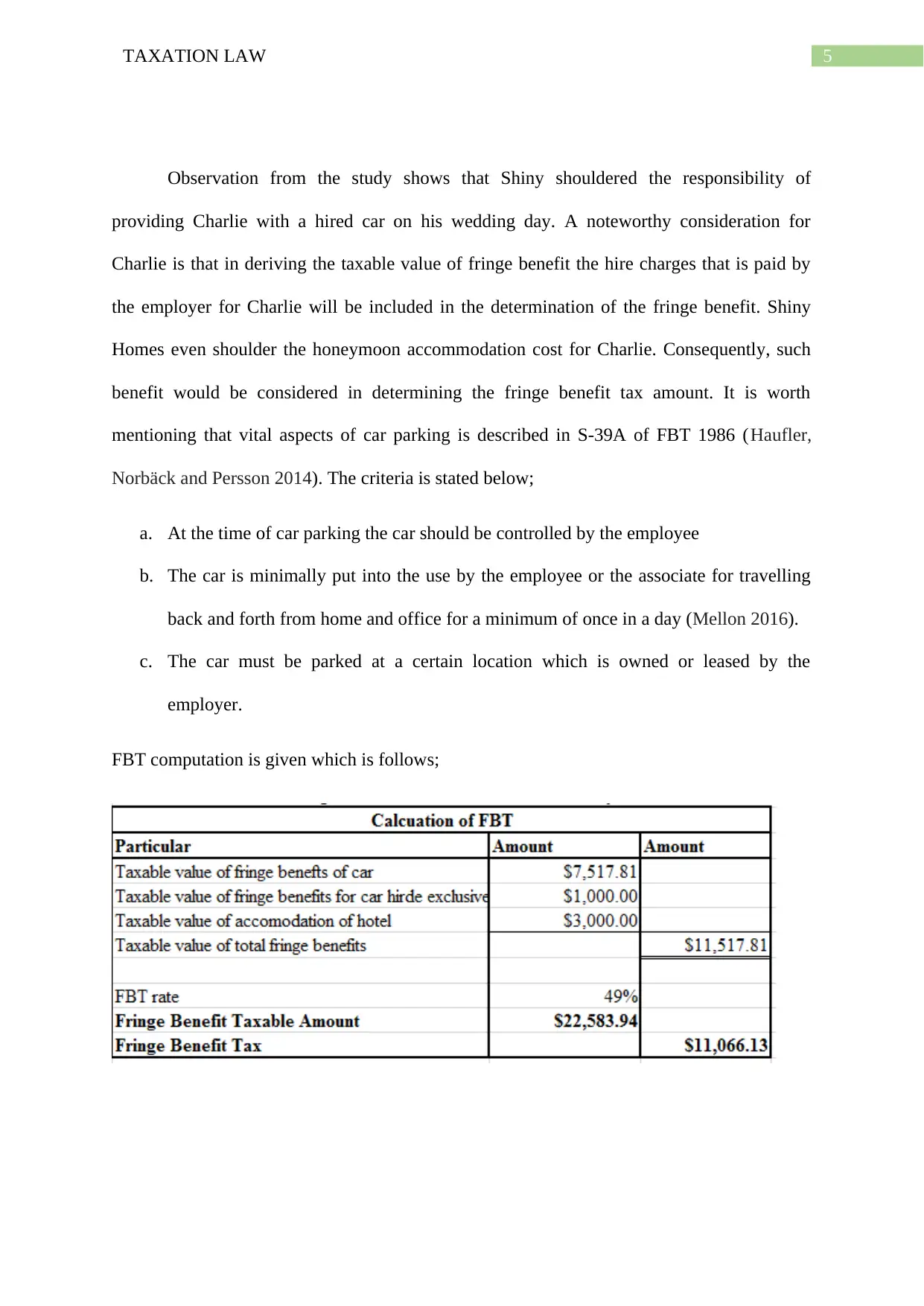

Observation from the study shows that Shiny shouldered the responsibility of

providing Charlie with a hired car on his wedding day. A noteworthy consideration for

Charlie is that in deriving the taxable value of fringe benefit the hire charges that is paid by

the employer for Charlie will be included in the determination of the fringe benefit. Shiny

Homes even shoulder the honeymoon accommodation cost for Charlie. Consequently, such

benefit would be considered in determining the fringe benefit tax amount. It is worth

mentioning that vital aspects of car parking is described in S-39A of FBT 1986 (Haufler,

Norbäck and Persson 2014). The criteria is stated below;

a. At the time of car parking the car should be controlled by the employee

b. The car is minimally put into the use by the employee or the associate for travelling

back and forth from home and office for a minimum of once in a day (Mellon 2016).

c. The car must be parked at a certain location which is owned or leased by the

employer.

FBT computation is given which is follows;

Observation from the study shows that Shiny shouldered the responsibility of

providing Charlie with a hired car on his wedding day. A noteworthy consideration for

Charlie is that in deriving the taxable value of fringe benefit the hire charges that is paid by

the employer for Charlie will be included in the determination of the fringe benefit. Shiny

Homes even shoulder the honeymoon accommodation cost for Charlie. Consequently, such

benefit would be considered in determining the fringe benefit tax amount. It is worth

mentioning that vital aspects of car parking is described in S-39A of FBT 1986 (Haufler,

Norbäck and Persson 2014). The criteria is stated below;

a. At the time of car parking the car should be controlled by the employee

b. The car is minimally put into the use by the employee or the associate for travelling

back and forth from home and office for a minimum of once in a day (Mellon 2016).

c. The car must be parked at a certain location which is owned or leased by the

employer.

FBT computation is given which is follows;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Taking into the considerations the concluding note of the present case study an

assertion can be bought forward by stating that Charlie would be liable for fringe benefit tax

under “FBTAA 1986”. Car was privately used by Charlie during employment course.

Answer to question 2:

Answer to requirement A:

The problem statement introduces the consequences of income tax for Alan. As

depicted from the case study Allan was the locum doctor and was very much well recognized

among his clients. When Alan cured his patients, he received home-produced cakes and

scones by his patients. Home grown foodstuff has no market worth and these component are

not accounted as taxable item.

Later, it was noticed that Allan received dozens of wine bottle from one of his client

as Allan treated his client’s dog from the snakebite. The retail value of the wine bottle in the

market is estimated to be $360. As a result of this the wine bottle will be included in the

taxable income of Allan since it has commercial value and will be considered in the

computation of the assessable income (Apps, Long and Rees 2014).

Answer to requirement B:

According to the “taxation ruling of TR 97/11” it helps in determining whether the

taxpayer is carrying on the business of the primary producer under “ITAA 1997” (Cohen,

Fedele and Panteghini 2016). The ruling serves as the guide in providing that whether an

individual is carrying on the business of the primary production. There are certain elements

that should be accounted in determining whether the person is indulgent in business or hobby;

a. If the person has more than just the objective of engaging in the business while hobby

hardly possess the intentions of engaging in business.

Taking into the considerations the concluding note of the present case study an

assertion can be bought forward by stating that Charlie would be liable for fringe benefit tax

under “FBTAA 1986”. Car was privately used by Charlie during employment course.

Answer to question 2:

Answer to requirement A:

The problem statement introduces the consequences of income tax for Alan. As

depicted from the case study Allan was the locum doctor and was very much well recognized

among his clients. When Alan cured his patients, he received home-produced cakes and

scones by his patients. Home grown foodstuff has no market worth and these component are

not accounted as taxable item.

Later, it was noticed that Allan received dozens of wine bottle from one of his client

as Allan treated his client’s dog from the snakebite. The retail value of the wine bottle in the

market is estimated to be $360. As a result of this the wine bottle will be included in the

taxable income of Allan since it has commercial value and will be considered in the

computation of the assessable income (Apps, Long and Rees 2014).

Answer to requirement B:

According to the “taxation ruling of TR 97/11” it helps in determining whether the

taxpayer is carrying on the business of the primary producer under “ITAA 1997” (Cohen,

Fedele and Panteghini 2016). The ruling serves as the guide in providing that whether an

individual is carrying on the business of the primary production. There are certain elements

that should be accounted in determining whether the person is indulgent in business or hobby;

a. If the person has more than just the objective of engaging in the business while hobby

hardly possess the intentions of engaging in business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

b. A business holds the significant commercial activity whereas the hobby does not has

any form of significant business activity

c. A business being carried on with the intention of making profit from the activity

whereas in hobby there is no such intention of making profit

d. Whether the business activity is carried on in the identical manner in respect of the

trade while hobby is carried on in the form of ad hoc manner (Peiros & Smyth, 2017).

e. A business activity is generally organized and it is carried on in the business-like

manner while hobby is not organized or executed in the normal business manner.

According to “FCT v Evans v (1989” decision made states that regards must be paid in

deciding nature of activity namely the business and hobby. (Snape and De Souza 2016). The

sum of revenue or income generated from the hobby cannot be regarded as the income.

Consequently, the profit generated from such hobby would be considered as executing the

activity of business.

Answer to requirement C:

Evidently “section 6 (1) of the ITAA 1997” is related to farming on land. For that

reason, the “taxation ruling TR 97/11” ascertains if an individual is executing trading or

primary production activity (Saad 2014). The court of law indicated that performing the trade

of primary production, the law court has stated whether the activity is well regarded as hobby

or any recreational activity. The case study depicts the situation that Betty has started making

marmalade which turned out to be widespread in her neighbours. A decision of opening stall

was made on every Sunday. Allan sold the excess amount to the supplier regularly.

The activities engaged in by Allan and Betty is having the characteristics of business

which is repetitive in nature. As held in the case of “Martin v. Federal Commissioner of

Taxation (1953)” the law court have placed emphasis that no single reflector could provide a

b. A business holds the significant commercial activity whereas the hobby does not has

any form of significant business activity

c. A business being carried on with the intention of making profit from the activity

whereas in hobby there is no such intention of making profit

d. Whether the business activity is carried on in the identical manner in respect of the

trade while hobby is carried on in the form of ad hoc manner (Peiros & Smyth, 2017).

e. A business activity is generally organized and it is carried on in the business-like

manner while hobby is not organized or executed in the normal business manner.

According to “FCT v Evans v (1989” decision made states that regards must be paid in

deciding nature of activity namely the business and hobby. (Snape and De Souza 2016). The

sum of revenue or income generated from the hobby cannot be regarded as the income.

Consequently, the profit generated from such hobby would be considered as executing the

activity of business.

Answer to requirement C:

Evidently “section 6 (1) of the ITAA 1997” is related to farming on land. For that

reason, the “taxation ruling TR 97/11” ascertains if an individual is executing trading or

primary production activity (Saad 2014). The court of law indicated that performing the trade

of primary production, the law court has stated whether the activity is well regarded as hobby

or any recreational activity. The case study depicts the situation that Betty has started making

marmalade which turned out to be widespread in her neighbours. A decision of opening stall

was made on every Sunday. Allan sold the excess amount to the supplier regularly.

The activities engaged in by Allan and Betty is having the characteristics of business

which is repetitive in nature. As held in the case of “Martin v. Federal Commissioner of

Taxation (1953)” the law court have placed emphasis that no single reflector could provide a

8TAXATION LAW

conclusive evidence and constantly involved overlapping indicators (Stewart, 2017). The

intention of profit was existing in the activities performed by Allan and Betty since their

activities accompanied business character. Conclusively Allan and Betty activities were of

business in nature and they will be liable for income tax.

Answer to requirement D:

There is a ruling relating to tax of “IT 2668” where transaction of barter system is

taxable as GST relating to cash and credit. Additionally, “Subsection 25 (1) of the ITAA

1936” lay down that revenue derived by an individual through barter system would be liable

for income tax. In the present case study of Allan and Betty the extent to which the nature of

the value received by them is dependent on the nature of the considerations in the recipient’s

hands (Jones, 2017).

The judgement of court in “F.C. of T. v. Cooke & Sherden 80 ATC 4140; 10 ATR

696” the considerations that is received as money by the Allan and Betty will attract tax

liability and it will additionally be liable for GST as well under the GSTR 1999 (Lang 2014).

The barter system that is set up by the Allan and Betty is considered equivalent to the cash or

credit and as a result of this it would attract tax liability.

conclusive evidence and constantly involved overlapping indicators (Stewart, 2017). The

intention of profit was existing in the activities performed by Allan and Betty since their

activities accompanied business character. Conclusively Allan and Betty activities were of

business in nature and they will be liable for income tax.

Answer to requirement D:

There is a ruling relating to tax of “IT 2668” where transaction of barter system is

taxable as GST relating to cash and credit. Additionally, “Subsection 25 (1) of the ITAA

1936” lay down that revenue derived by an individual through barter system would be liable

for income tax. In the present case study of Allan and Betty the extent to which the nature of

the value received by them is dependent on the nature of the considerations in the recipient’s

hands (Jones, 2017).

The judgement of court in “F.C. of T. v. Cooke & Sherden 80 ATC 4140; 10 ATR

696” the considerations that is received as money by the Allan and Betty will attract tax

liability and it will additionally be liable for GST as well under the GSTR 1999 (Lang 2014).

The barter system that is set up by the Allan and Betty is considered equivalent to the cash or

credit and as a result of this it would attract tax liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Reference List:

Apps, P., Long, N. and Rees, R., 2014. Optimal piecewise linear income taxation. Journal of

Public Economic Theory, 16(4), pp.523-545.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

American Economic Review, 105(5), pp.38-42.

Chambers, C.P. and Moreno-Ternero, J.D., 2017. Taxation and poverty. Social Choice and

Welfare, 48(1), pp.153-175.

Cohen, F., Fedele, A. and Panteghini, P.M., 2016. Corporate taxation and financial strategies

under asymmetric information. Economia Politica, 33(1), pp.9-34.

Gahvari, F. and Micheletto, L., 2016. Capital income taxation and the Atkinson–Stiglitz

theorem. Economics Letters, 147, pp.86-89.

Gevorkyan, A., Flaherty, M., Heine, D., Mazzucato, M., Radpour, S. and Semmler, W., 2016.

Financing Climate Policies through Carbon Taxation and Climate Bonds–Theory and

Empirics.

Haufler, A., Norbäck, P.J. and Persson, L., 2014. Entrepreneurial innovations and

taxation. Journal of Public Economics, 113, pp.13-31.

Jones, D., (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Martin, L. 2014. Taxation, loss aversion, and accountability: theory and experimental

evidence for taxation’s effect on citizen behavior. Unpublished paper, Yale

University, New Haven, CT.

Reference List:

Apps, P., Long, N. and Rees, R., 2014. Optimal piecewise linear income taxation. Journal of

Public Economic Theory, 16(4), pp.523-545.

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. The

American Economic Review, 105(5), pp.38-42.

Chambers, C.P. and Moreno-Ternero, J.D., 2017. Taxation and poverty. Social Choice and

Welfare, 48(1), pp.153-175.

Cohen, F., Fedele, A. and Panteghini, P.M., 2016. Corporate taxation and financial strategies

under asymmetric information. Economia Politica, 33(1), pp.9-34.

Gahvari, F. and Micheletto, L., 2016. Capital income taxation and the Atkinson–Stiglitz

theorem. Economics Letters, 147, pp.86-89.

Gevorkyan, A., Flaherty, M., Heine, D., Mazzucato, M., Radpour, S. and Semmler, W., 2016.

Financing Climate Policies through Carbon Taxation and Climate Bonds–Theory and

Empirics.

Haufler, A., Norbäck, P.J. and Persson, L., 2014. Entrepreneurial innovations and

taxation. Journal of Public Economics, 113, pp.13-31.

Jones, D., (2017). Tax and accounting income-Worlds apart?. Taxation in Australia, 52(1),

p.14.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Martin, L. 2014. Taxation, loss aversion, and accountability: theory and experimental

evidence for taxation’s effect on citizen behavior. Unpublished paper, Yale

University, New Haven, CT.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Peiros, K., & Smyth, C. (2017). Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), 394.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Stewart, M. (2017). Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41).

Springer, Cham.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Peiros, K., & Smyth, C. (2017). Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), 394.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Snape, J. and De Souza, J., 2016. Environmental taxation law: policy, contexts and practice.

Routledge.

Stewart, M. (2017). Australia’s Hybrid International Tax System: Limited Focus on Tax and

Development. In Taxation and Development-A Comparative Study (pp. 17-41).

Springer, Cham.

Tanzi, V., 2014. Inflation, indexation and interest income taxation. PSL Quarterly

Review, 29(116).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.