Taxation Law Assignment: Analysis of Income and Deductions (2019)

VerifiedAdded on 2023/01/18

|7

|1412

|75

Homework Assignment

AI Summary

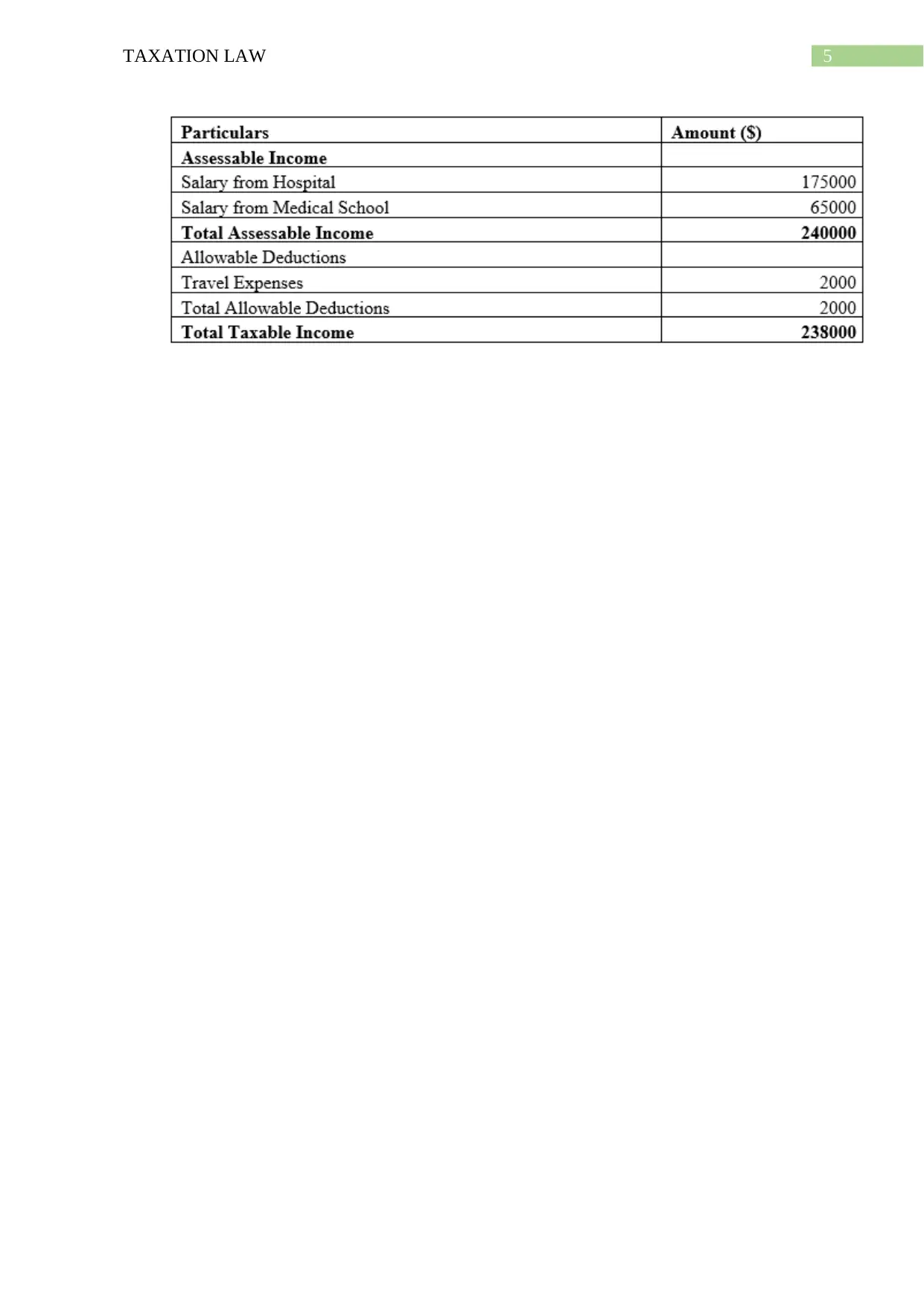

This document provides a detailed solution to a taxation law assignment, addressing a problem-style question with two parts. The assignment analyzes various aspects of income tax law, including the determination of assessable income from employment and part-time lecturing, referencing sections from the ITAA 1936 and ITAA 1997. It examines the deductibility of travel expenses, distinguishing between work-related travel and expenses for pursuing further education or negotiating contracts. Furthermore, the solution explores the treatment of repair expenses versus capital improvements, citing relevant case law such as Sun Newspapers Ltd v FC of T (1938). Finally, it covers the implications of capital gains tax (CGT) events, particularly the disposal of a CGT asset and the calculation of cost base, providing a comprehensive understanding of taxation principles. The solution also includes a references section with the relevant sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.