Taxation Law Tutorial 9 Assignment Solution - LAWS3101 Brisbane

VerifiedAdded on 2023/03/21

|6

|626

|70

Homework Assignment

AI Summary

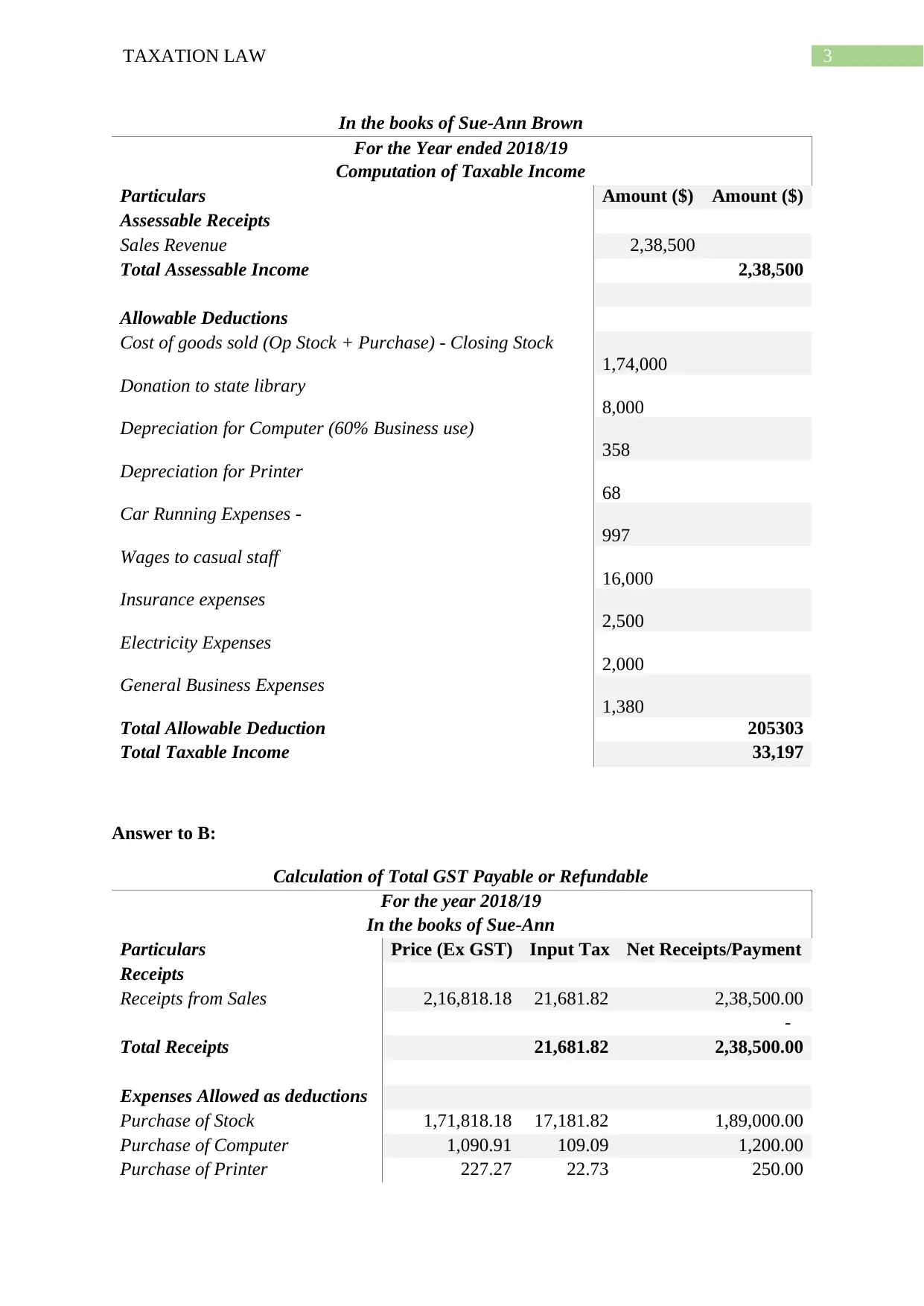

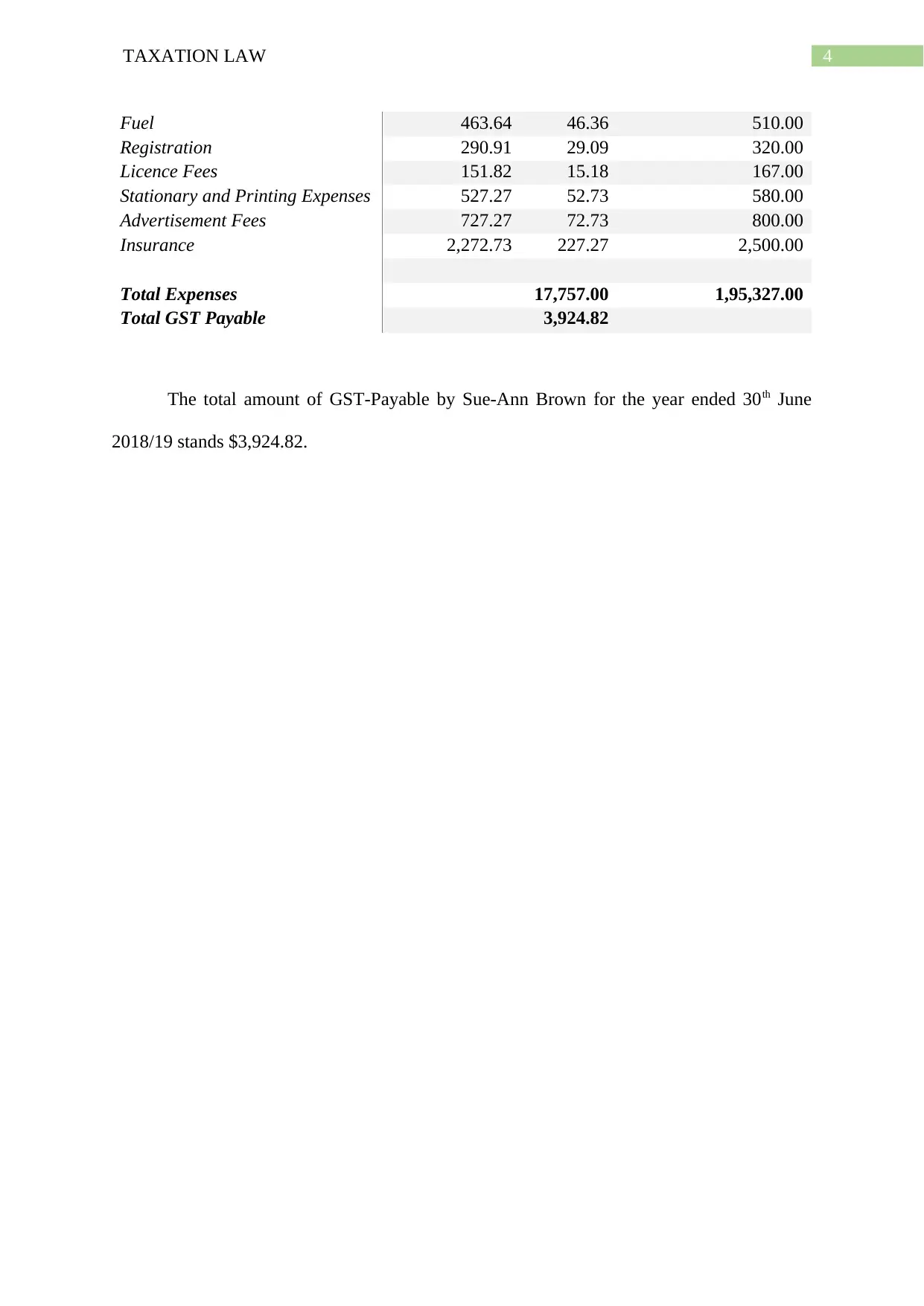

This assignment solution addresses the LAWS3101 Taxation Law Tutorial 9, focusing on the tax implications for Sue-Ann Brown's bookstore business. The solution calculates Sue-Ann's taxable income, considering sales revenue as assessable income, and details allowable deductions like cost of goods sold, donations, depreciation, wages, and various business expenses. It applies relevant sections of the ITAA 1997, such as section 6-5 for business receipts and division 30 for deductible gifts. Additionally, the solution computes the total GST payable by Sue-Ann, considering receipts, expenses, and input tax, providing a comprehensive understanding of her tax obligations. The assignment includes a detailed breakdown of the calculations, providing a clear understanding of taxation principles.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.