Taxation Law Assignment: FBT and CGT Calculations and Analysis

VerifiedAdded on 2023/03/23

|10

|2252

|59

Homework Assignment

AI Summary

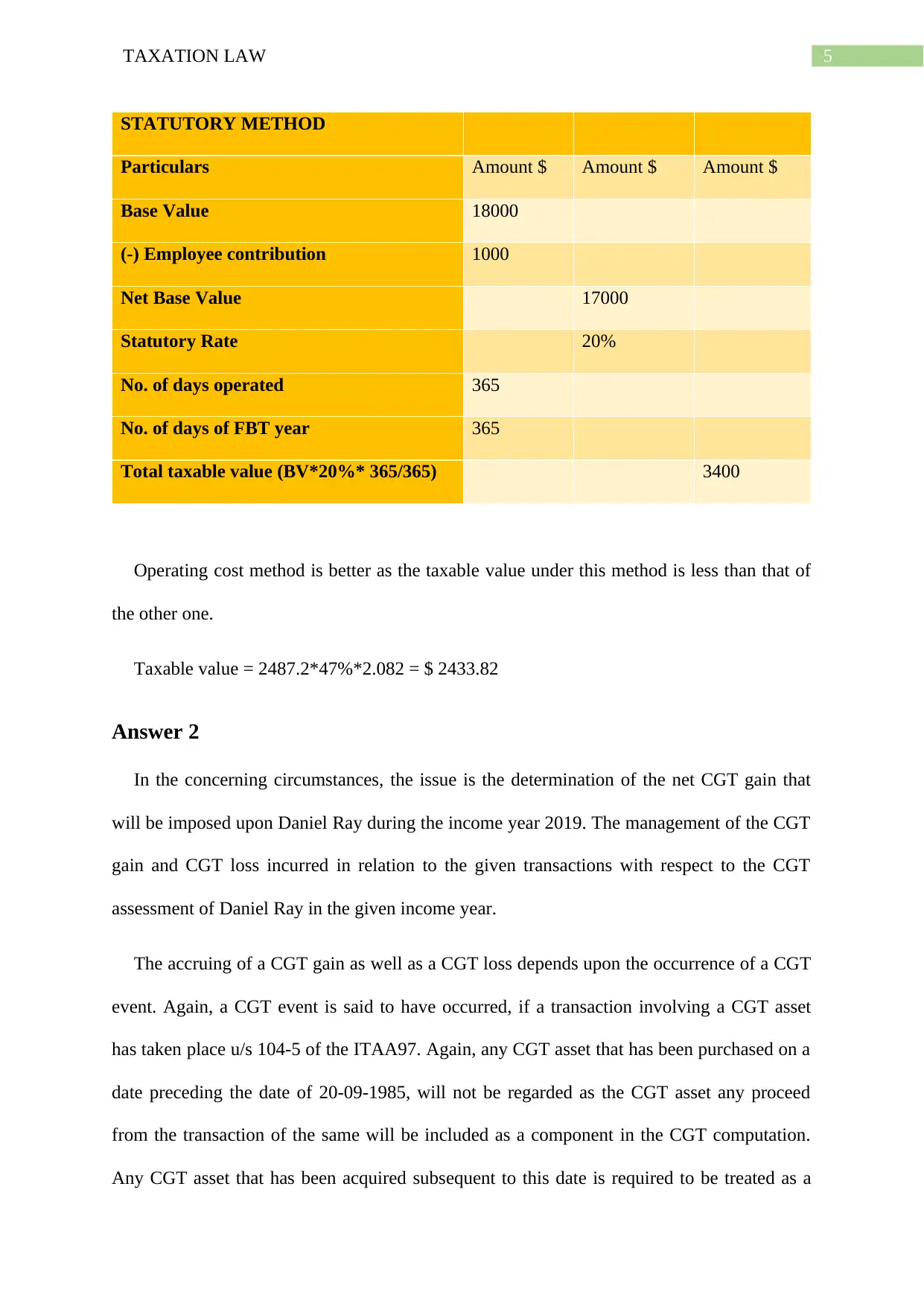

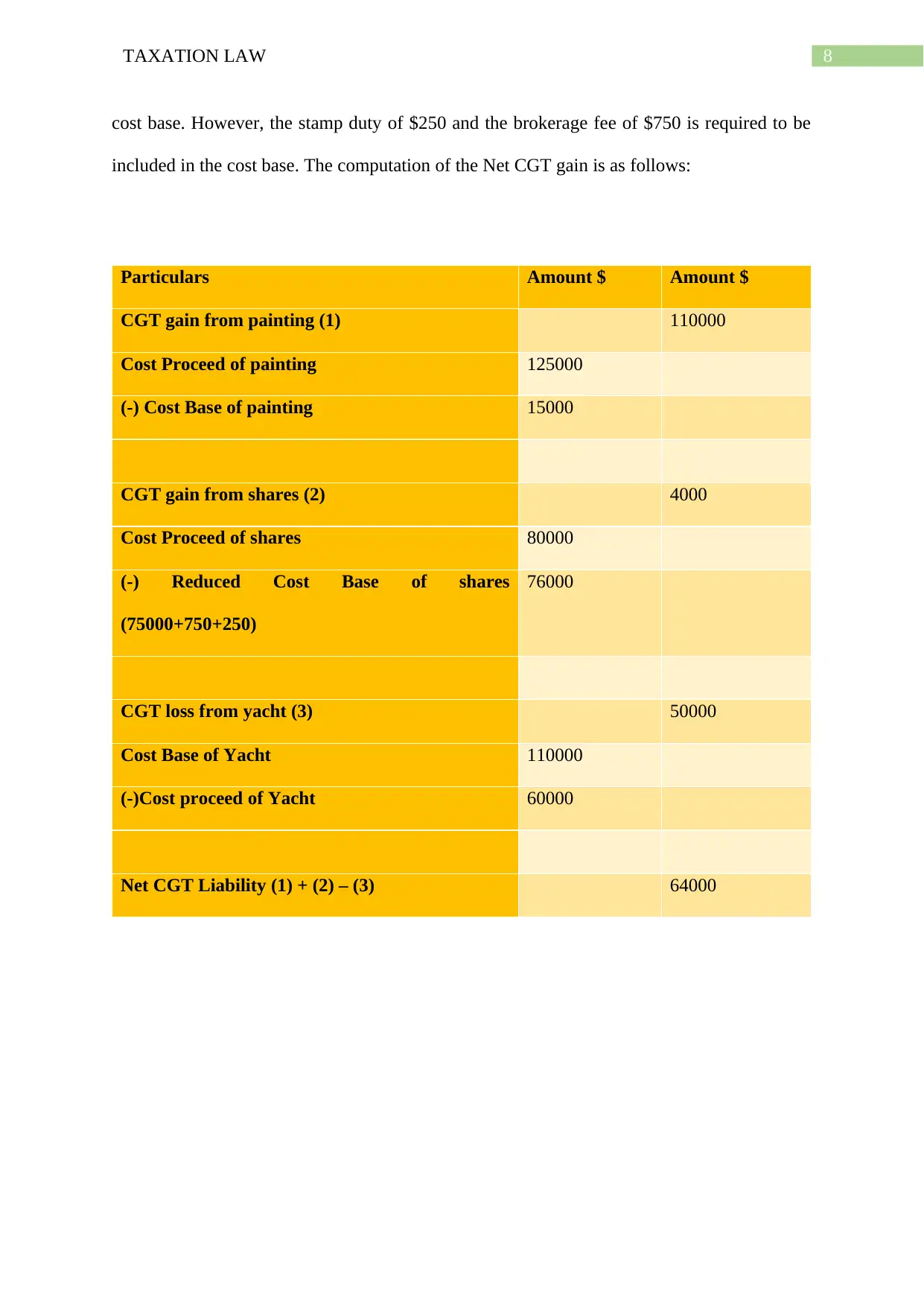

This assignment solution addresses a Taxation Law problem involving Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT). The first part focuses on calculating FBT liability for a car fringe benefit, comparing the statutory and operating cost methods. It analyzes the provided data, including the car's base value, employee contributions, and various expenses, to determine the taxable value under each method and recommends the most advantageous approach for minimizing tax liability. The second part deals with CGT, analyzing several transactions to determine the net CGT gain or loss for an individual. It covers the sale of a painting, shares, and a yacht, and the sale of a house. The solution applies relevant CGT rules, including the treatment of main residences, collectibles, and shares, considering acquisition costs, sale proceeds, and associated expenses. It calculates the CGT gain or loss for each transaction and determines the overall net CGT liability, including the exclusion of the main residence from CGT calculations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.