Taxation Law: Individual Assignment Solution Analysis - HA3042

VerifiedAdded on 2023/03/21

|11

|2374

|100

Homework Assignment

AI Summary

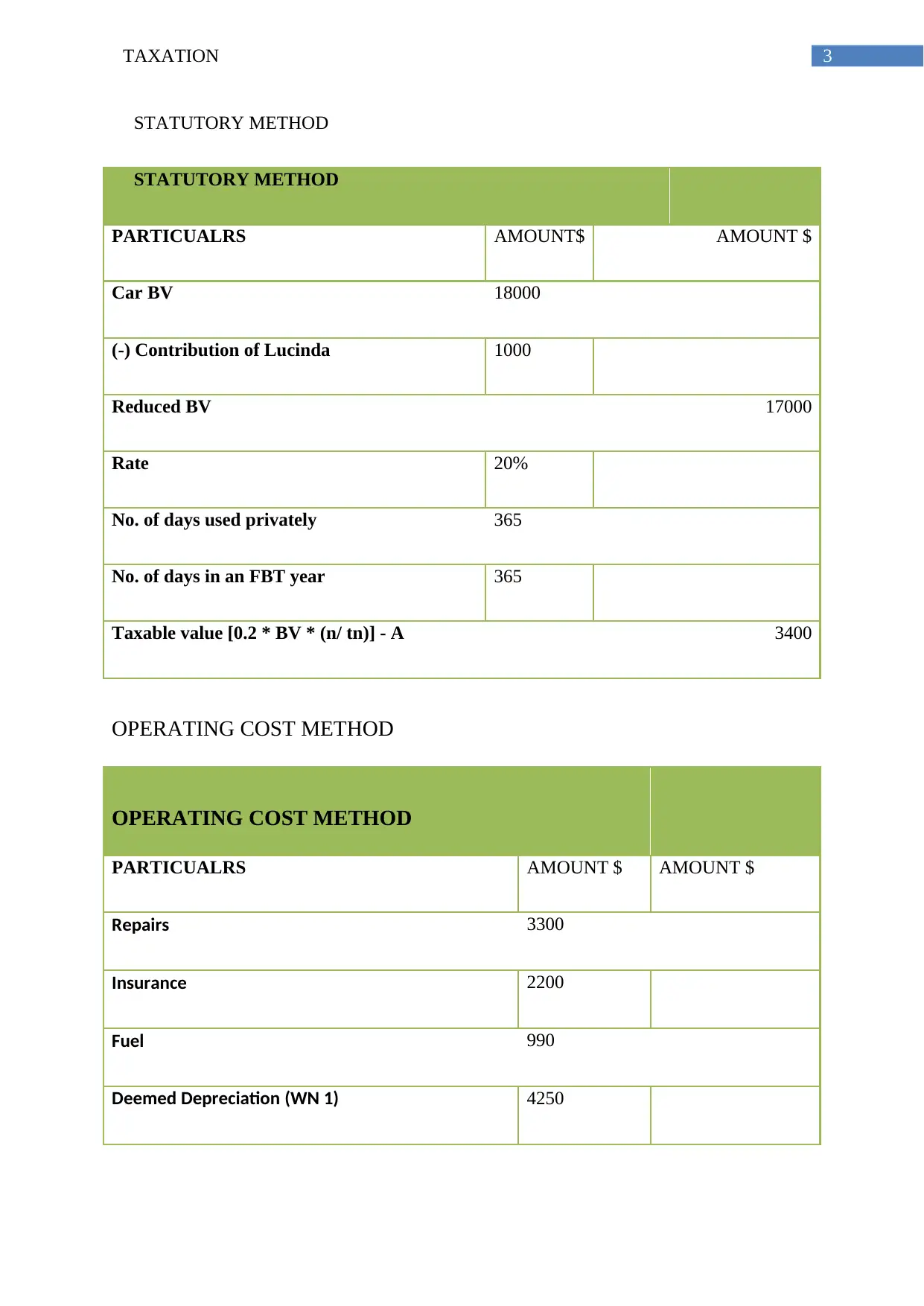

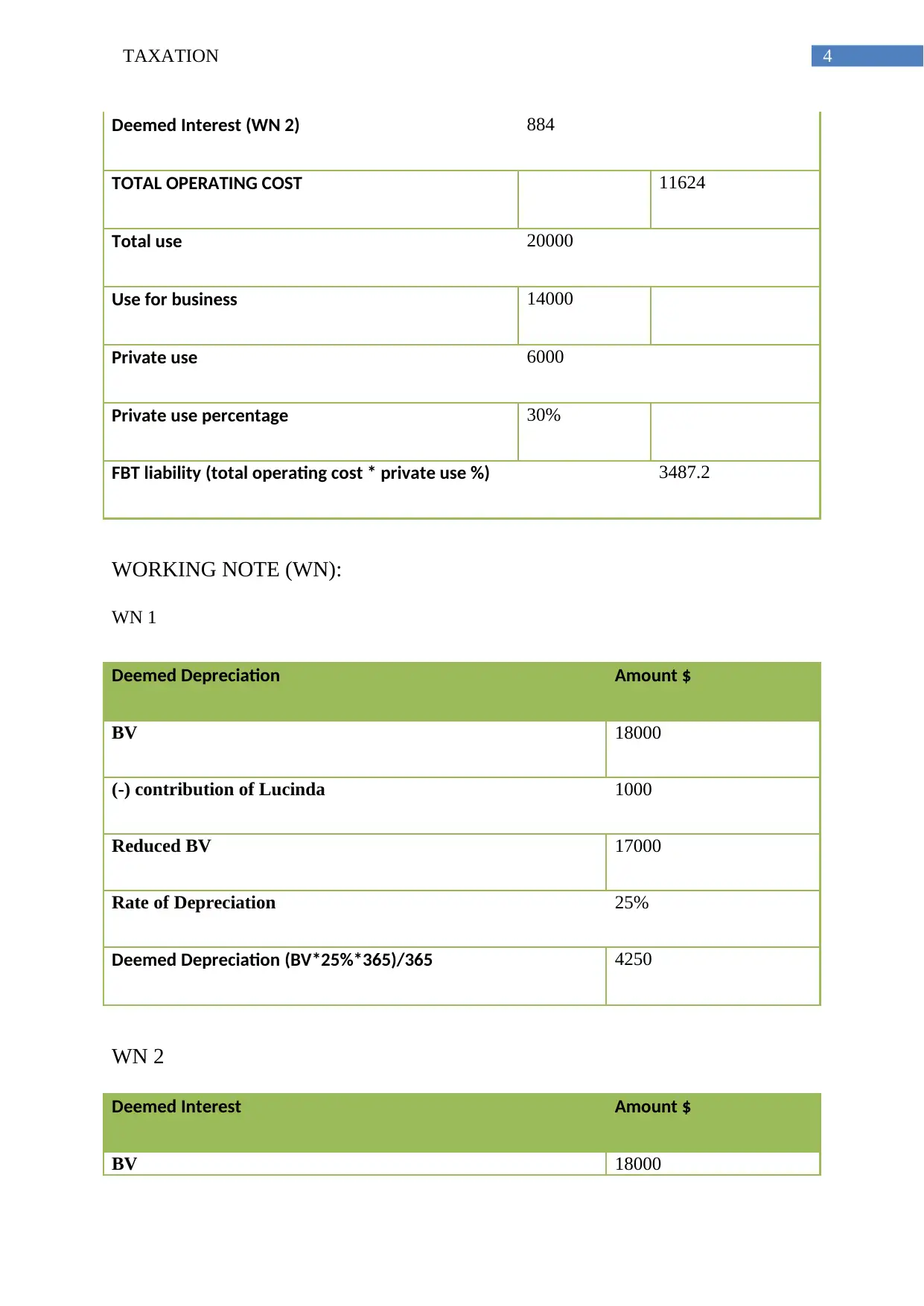

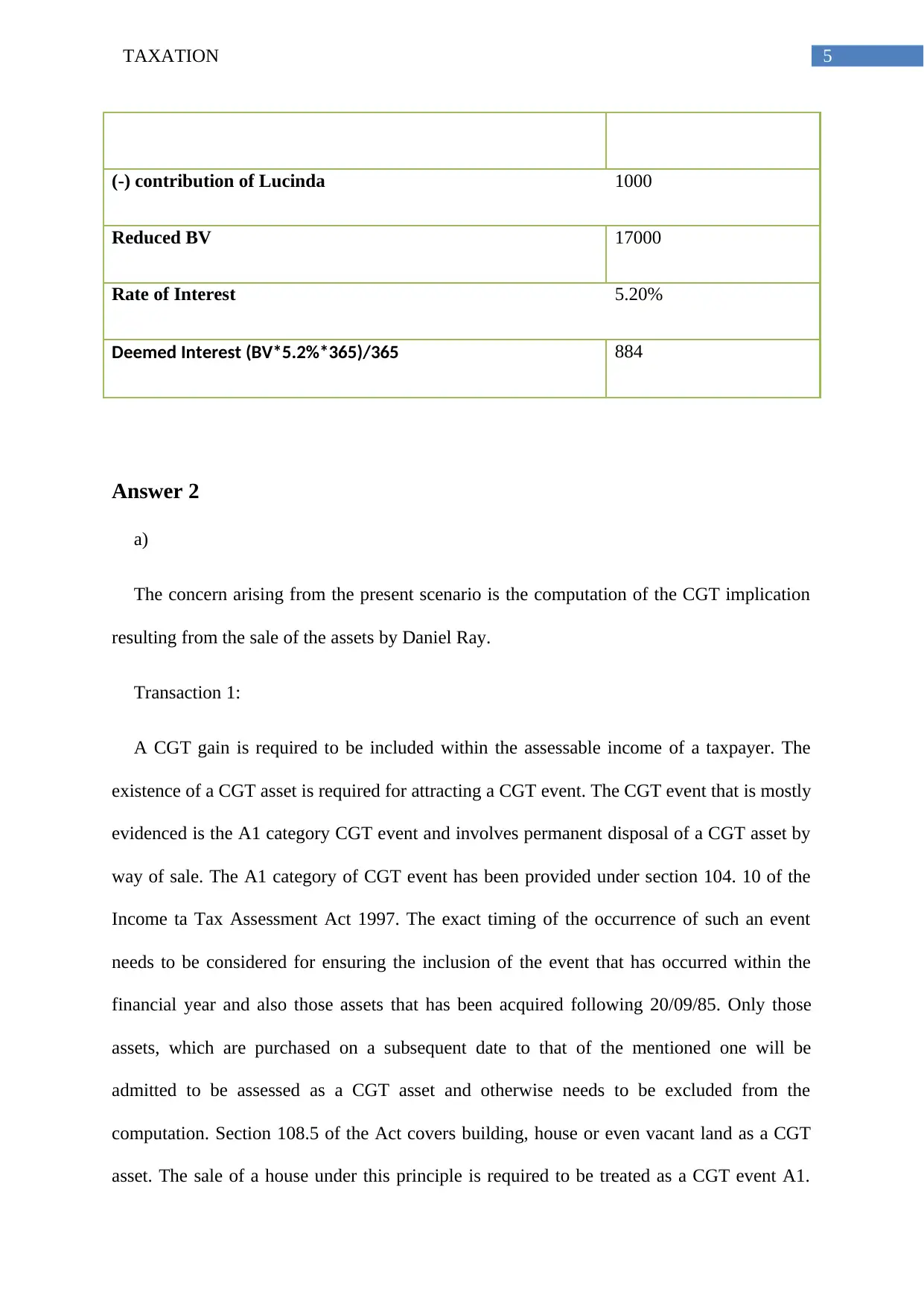

This assignment solution addresses two key areas of taxation: Fringe Benefit Tax (FBT) and Capital Gains Tax (CGT). The FBT section focuses on calculating the tax implications of providing a car to an employee, exploring both the statutory and operating cost methods. It includes detailed calculations and working notes to determine the taxable value and FBT liability. The CGT section analyzes four different transactions involving the sale of assets, including a house, a painting, a luxury yacht, and shares. It examines the application of CGT principles, including cost base, capital proceeds, and the potential for discounts and exemptions, providing a comprehensive understanding of CGT implications for each transaction. The solution incorporates relevant sections from the Fringe Benefit Tax Assessment Act 1986 and the Income Tax Assessment Act 1997, offering a practical application of tax law principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.