LAW 6001 Taxation Law Case Study: Client Advice on Tax Issues

VerifiedAdded on 2022/12/26

|12

|2884

|1

Case Study

AI Summary

This case study analyzes various aspects of Australian taxation law. It addresses questions related to the federation's legislative power in taxation, the role of the ATO, and the application of double taxation agreements. The study delves into capital gains tax (CGT) implications, particularly concerning pre-CGT assets and the main residence exemption. It examines the tax treatment of different scenarios, including property subdivision, trading stock, and the realization of capital assets. The case study further explores allowable deductions, such as interest on loans, and provides an analysis of home office expenses and the impact of ATO measures. Additionally, it examines the implications of removing refundable franking credits. The document offers practical tax advice based on the Income Tax Assessment Act (ITAA) 1936 and 1997, with references to relevant case law and articles. The study concludes with an analysis of the client's tax situation, providing recommendations based on the findings.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................5

Answer to question 6:.................................................................................................................7

Article 1: ATO measures on crackdown on home office expenses claims:...............................7

Article 2: ATO measures of removing “inequitable” inquiry:...................................................8

Answer to question 7:.................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................3

Part 1:.....................................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to part 2:........................................................................................................................4

Answer to question 4:.................................................................................................................4

Answer to question 5:.................................................................................................................5

Answer to question 6:.................................................................................................................7

Article 1: ATO measures on crackdown on home office expenses claims:...............................7

Article 2: ATO measures of removing “inequitable” inquiry:...................................................8

Answer to question 7:.................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Answer to A:

Australia is regarded as the federation and the legislative power is distributed among

the commonwealth and federations. The area that enumerates the areas of constitutional

power is section 51 (Graetz et al., 2015). These power are considered concurrent and the state

has the power to legislate on them or any other topic that is not specifically prohibited to

them by the constitution. According to the section 51 (ii) the commonwealth is allowed to

enact laws in relation to the taxation but it a manner that it does not discriminates between the

states or the parts of the states.

Answer to B:

The primary role of ATO is to administer the legislation relating to tax and

superannuation that is passed by the parliament. To carry-out this function, the ATO develops

the administrative arrangement to implement the taxation laws and provide advice to the

taxpayers regarding their rights and obligations, collecting of tax revenues and making sure

that it complies with the law (Lymer et al., 2013). The parliament and courts are accountable

for providing an overall improvement in the tax policy and the minister of treasury is

accountable for practically applying the laws. The court is responsible for making sure that

the tax policies and judicial procedure that provides an explanation in respect of the laws and

administrative features of tax system.

Answer to question 2:

According to the Double Taxation Agreement the business profits of a company that

is performing contractual obligation will be held liable for tax in that nation only excluding

the circumstances when the company in another contracting country is performing business

through permanent establishment (Chirelstein, 2015). A firm is only held as Australian

Answer to question 1:

Answer to A:

Australia is regarded as the federation and the legislative power is distributed among

the commonwealth and federations. The area that enumerates the areas of constitutional

power is section 51 (Graetz et al., 2015). These power are considered concurrent and the state

has the power to legislate on them or any other topic that is not specifically prohibited to

them by the constitution. According to the section 51 (ii) the commonwealth is allowed to

enact laws in relation to the taxation but it a manner that it does not discriminates between the

states or the parts of the states.

Answer to B:

The primary role of ATO is to administer the legislation relating to tax and

superannuation that is passed by the parliament. To carry-out this function, the ATO develops

the administrative arrangement to implement the taxation laws and provide advice to the

taxpayers regarding their rights and obligations, collecting of tax revenues and making sure

that it complies with the law (Lymer et al., 2013). The parliament and courts are accountable

for providing an overall improvement in the tax policy and the minister of treasury is

accountable for practically applying the laws. The court is responsible for making sure that

the tax policies and judicial procedure that provides an explanation in respect of the laws and

administrative features of tax system.

Answer to question 2:

According to the Double Taxation Agreement the business profits of a company that

is performing contractual obligation will be held liable for tax in that nation only excluding

the circumstances when the company in another contracting country is performing business

through permanent establishment (Chirelstein, 2015). A firm is only held as Australian

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

resident company if the company if the company is incorporated in Australia and majority of

its shareholders and control is located in Australia. As per the decision given under

“Malayan Shipping Company Ltd v FCT (1946)” the company was held to be austrlaian

resident because its central management and control was in Australia.

With respect to explanation made above, the profits that is made by the US base

company from the sales in Australia will be considered taxable in Australia. The main reason

for this is that the business profits are produced in Australia because the transaction has a

source in Australia.

Answer to question 3:

Part 1:

Answer to A:

According to “Section 102-5, ITAA 1997” the assessable income of the taxpayer also

includes the net amount of capital gains (Getches et al., 2014). In the current case of Indiana

has owned the property since 1st November 1976 then the land will be considered as the pre-

CGT profit. Subdividing and selling the land for profit will be exempted from tax since the

property was bought before the introduction of CGT regimes.

Answer to B:

First Option: If the property has been owned by Indiana from 1st November 1986 and she

decides to subdivide the property into 89 lots and later selling the undeveloped blocks to the

property developer then the land constitute trading stock. The capital gains will be taxable as

ordinary income under “section 6-5, ITAA 1997”.

Second Option: If Indiana takes the similar activities as mentioned above and holds the

auction of all the 80 blocks land to sell it to the highest bidder then it will amount to capital

resident company if the company if the company is incorporated in Australia and majority of

its shareholders and control is located in Australia. As per the decision given under

“Malayan Shipping Company Ltd v FCT (1946)” the company was held to be austrlaian

resident because its central management and control was in Australia.

With respect to explanation made above, the profits that is made by the US base

company from the sales in Australia will be considered taxable in Australia. The main reason

for this is that the business profits are produced in Australia because the transaction has a

source in Australia.

Answer to question 3:

Part 1:

Answer to A:

According to “Section 102-5, ITAA 1997” the assessable income of the taxpayer also

includes the net amount of capital gains (Getches et al., 2014). In the current case of Indiana

has owned the property since 1st November 1976 then the land will be considered as the pre-

CGT profit. Subdividing and selling the land for profit will be exempted from tax since the

property was bought before the introduction of CGT regimes.

Answer to B:

First Option: If the property has been owned by Indiana from 1st November 1986 and she

decides to subdivide the property into 89 lots and later selling the undeveloped blocks to the

property developer then the land constitute trading stock. The capital gains will be taxable as

ordinary income under “section 6-5, ITAA 1997”.

Second Option: If Indiana takes the similar activities as mentioned above and holds the

auction of all the 80 blocks land to sell it to the highest bidder then it will amount to capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

gains which will be taxable as ordinary income from the profit making undertaking or

scheme.

Third option: If Indiana does not decides to subdivide the land and sell the land to the

property developer then it will amount to mere realisation of the capital asset, The capital

gains derived will not be taxable as ordinary income for Indiana.

Answer to part 2:

Option A:

If the land is subdivided and results in mere realisation of the capital asset by the

Indiana then the capital gains that is made will be regarded as gain that is obtained

beneficially from land development. The capital gain will be regarded as income from the

revenue asset and will be held taxable under “section 6-5, ITAA 1997” as ordinary income

(Mumford, 2017).

Option B:

If Indiana takes the decision of sub-division of land then the undivided block of land

would amount to trading stock. The 80 blocks of land will be considered as trading stock

from the time the subdivision began. She will be considered taxable for the capital gains

made from the land because a commercial approach was undertaken to sell the land at present

market value. The capital gains that is made from the land is an ordinary income under

“section 6-5, ITAA 1997”.

Option C:

In the third option if Indiana simply decides to not divide the land and sell it to the

property development company then the receipts derived from the land will be treated as

gains which will be taxable as ordinary income from the profit making undertaking or

scheme.

Third option: If Indiana does not decides to subdivide the land and sell the land to the

property developer then it will amount to mere realisation of the capital asset, The capital

gains derived will not be taxable as ordinary income for Indiana.

Answer to part 2:

Option A:

If the land is subdivided and results in mere realisation of the capital asset by the

Indiana then the capital gains that is made will be regarded as gain that is obtained

beneficially from land development. The capital gain will be regarded as income from the

revenue asset and will be held taxable under “section 6-5, ITAA 1997” as ordinary income

(Mumford, 2017).

Option B:

If Indiana takes the decision of sub-division of land then the undivided block of land

would amount to trading stock. The 80 blocks of land will be considered as trading stock

from the time the subdivision began. She will be considered taxable for the capital gains

made from the land because a commercial approach was undertaken to sell the land at present

market value. The capital gains that is made from the land is an ordinary income under

“section 6-5, ITAA 1997”.

Option C:

In the third option if Indiana simply decides to not divide the land and sell it to the

property development company then the receipts derived from the land will be treated as

5TAXATION LAW

mere realisation of the capital asset and Indiana will not be held assessable for the gains

made.

Answer to question 4:

Under the two positive limbs the taxpayers are permitted to obtain deduction from

their assessable income for the any sum of loss or outgoings up to the extent that the

expenditure is occurred in gaining the assessable income or it is necessarily incurred in

performing the business with the objective of earning taxable income (Heffron, 2018).

Expenditure that happen after the business is ceased may be allowed for deduction given the

situation of loss or outgoing is noticed in the business operation that was previously

conducted by taxpayer with the objective of gaining assessable income. The federal

commissioner in “Placer Pacific Management Pty Ltd v FCT (1995)” held that situation of

outgoing was evidenced during the business operation which was aimed at producing the

assessable income (Listokin, 2017). The commissioner allowed the taxpayer with the

deduction for the business arrangement which the taxpayer entered into with the customer for

supply of conveyor belt.

Preceding from the case study of Amity it is found that the she occurred an interest on

loan that was directed towards the development of accommodation business for three years’

time. Referring the case of “Placer Pacific Management Pty Ltd v FCT (1995)” it is

understood that interest on loan was incurred by Amity which was aimed at producing the

assessable income (Miller & Oats, 2016). Consequently, Amity is permitted to obtain the

allowable deduction for the interest on loan because the event of loss or outgoing was related

to the business procedure entered into by Amity and her business partner Archie.

mere realisation of the capital asset and Indiana will not be held assessable for the gains

made.

Answer to question 4:

Under the two positive limbs the taxpayers are permitted to obtain deduction from

their assessable income for the any sum of loss or outgoings up to the extent that the

expenditure is occurred in gaining the assessable income or it is necessarily incurred in

performing the business with the objective of earning taxable income (Heffron, 2018).

Expenditure that happen after the business is ceased may be allowed for deduction given the

situation of loss or outgoing is noticed in the business operation that was previously

conducted by taxpayer with the objective of gaining assessable income. The federal

commissioner in “Placer Pacific Management Pty Ltd v FCT (1995)” held that situation of

outgoing was evidenced during the business operation which was aimed at producing the

assessable income (Listokin, 2017). The commissioner allowed the taxpayer with the

deduction for the business arrangement which the taxpayer entered into with the customer for

supply of conveyor belt.

Preceding from the case study of Amity it is found that the she occurred an interest on

loan that was directed towards the development of accommodation business for three years’

time. Referring the case of “Placer Pacific Management Pty Ltd v FCT (1995)” it is

understood that interest on loan was incurred by Amity which was aimed at producing the

assessable income (Miller & Oats, 2016). Consequently, Amity is permitted to obtain the

allowable deduction for the interest on loan because the event of loss or outgoing was related

to the business procedure entered into by Amity and her business partner Archie.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 5:

Capital gains tax began during 20th September 1985 and takes into the account the

receipts under the tax base (Sikka, 2017). Basic exemption is permitted to the taxpayer from

the capital gains derived from main residence where the CGT was forms the dwelling and the

taxpayer is regarded as an individual. Under “section 118-110 (1)”, the main residence

exemption is only applicable when the dwelling was the main residence of the taxpayer all

through the period of ownership. Under “section 118-190 ITAA 1997”, partial exemption for

the CGT event takes place when the main residence was not the portion of ownership and the

dwelling was used for producing income (Cole, 2015). Maurice purchased a home during

February 1989 and sold the same on March 2018. All through the period of ownership the

residence was used by Maurice for dwelling purpose only. Therefore, under “section 118-

110 (1)” capital gains from the main residence will be exempted.

Assets that are acquired before the introduction of the CGT regime are not considered

for taxation purpose. Instead these assets are treated as pre-CGT asset and capital gains made

from such asset is exempted from tax (Jones & Rhoades-Catanach, 2015). Maurice purchased

shares in FUL Pty Ltd on 10th April 1984 and these shares were sold on 1st May 2018. As

evident the shares were bought by Maurice prior to the introduction of CGT system. As a

result the shares will be considered as Pre-CGT asset and capital gains that is made is

exempted from tax.

“Section 108-20 (2), ITAA 1997” defines the personal use asset as those that are used

by the taxpayers for their private use (Sharkey & Murray, 2016). There are special rules that

are applicable to personal use assets under “section 118-10 (3), ITAA 1997”. This includes

that any capital gains or loss made is ignored under the first element when the cost base is

less than $10,000 (Basu, 2016). Maurice reports that she bought a furniture 20th May 2010

Answer to question 5:

Capital gains tax began during 20th September 1985 and takes into the account the

receipts under the tax base (Sikka, 2017). Basic exemption is permitted to the taxpayer from

the capital gains derived from main residence where the CGT was forms the dwelling and the

taxpayer is regarded as an individual. Under “section 118-110 (1)”, the main residence

exemption is only applicable when the dwelling was the main residence of the taxpayer all

through the period of ownership. Under “section 118-190 ITAA 1997”, partial exemption for

the CGT event takes place when the main residence was not the portion of ownership and the

dwelling was used for producing income (Cole, 2015). Maurice purchased a home during

February 1989 and sold the same on March 2018. All through the period of ownership the

residence was used by Maurice for dwelling purpose only. Therefore, under “section 118-

110 (1)” capital gains from the main residence will be exempted.

Assets that are acquired before the introduction of the CGT regime are not considered

for taxation purpose. Instead these assets are treated as pre-CGT asset and capital gains made

from such asset is exempted from tax (Jones & Rhoades-Catanach, 2015). Maurice purchased

shares in FUL Pty Ltd on 10th April 1984 and these shares were sold on 1st May 2018. As

evident the shares were bought by Maurice prior to the introduction of CGT system. As a

result the shares will be considered as Pre-CGT asset and capital gains that is made is

exempted from tax.

“Section 108-20 (2), ITAA 1997” defines the personal use asset as those that are used

by the taxpayers for their private use (Sharkey & Murray, 2016). There are special rules that

are applicable to personal use assets under “section 118-10 (3), ITAA 1997”. This includes

that any capital gains or loss made is ignored under the first element when the cost base is

less than $10,000 (Basu, 2016). Maurice reports that she bought a furniture 20th May 2010

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

which was sold for $5,000 on May 2018. The cost base of the furniture is less than $10k so

the capital loss made by her is disregarded.

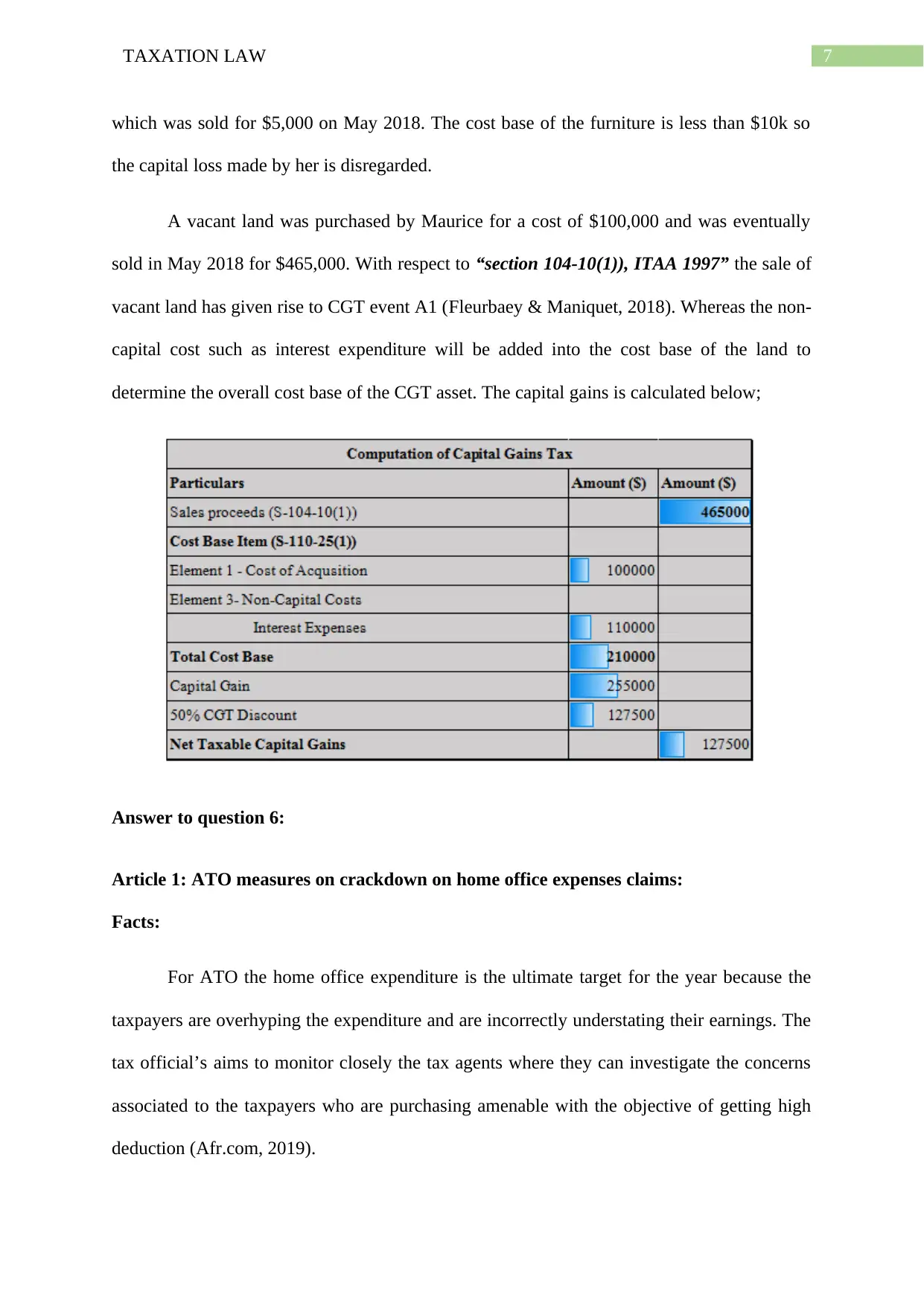

A vacant land was purchased by Maurice for a cost of $100,000 and was eventually

sold in May 2018 for $465,000. With respect to “section 104-10(1)), ITAA 1997” the sale of

vacant land has given rise to CGT event A1 (Fleurbaey & Maniquet, 2018). Whereas the non-

capital cost such as interest expenditure will be added into the cost base of the land to

determine the overall cost base of the CGT asset. The capital gains is calculated below;

Answer to question 6:

Article 1: ATO measures on crackdown on home office expenses claims:

Facts:

For ATO the home office expenditure is the ultimate target for the year because the

taxpayers are overhyping the expenditure and are incorrectly understating their earnings. The

tax official’s aims to monitor closely the tax agents where they can investigate the concerns

associated to the taxpayers who are purchasing amenable with the objective of getting high

deduction (Afr.com, 2019).

which was sold for $5,000 on May 2018. The cost base of the furniture is less than $10k so

the capital loss made by her is disregarded.

A vacant land was purchased by Maurice for a cost of $100,000 and was eventually

sold in May 2018 for $465,000. With respect to “section 104-10(1)), ITAA 1997” the sale of

vacant land has given rise to CGT event A1 (Fleurbaey & Maniquet, 2018). Whereas the non-

capital cost such as interest expenditure will be added into the cost base of the land to

determine the overall cost base of the CGT asset. The capital gains is calculated below;

Answer to question 6:

Article 1: ATO measures on crackdown on home office expenses claims:

Facts:

For ATO the home office expenditure is the ultimate target for the year because the

taxpayers are overhyping the expenditure and are incorrectly understating their earnings. The

tax official’s aims to monitor closely the tax agents where they can investigate the concerns

associated to the taxpayers who are purchasing amenable with the objective of getting high

deduction (Afr.com, 2019).

8TAXATION LAW

Concise explanation of taxation concepts:

A taxpayer is only allowed to claim the home office expenditure where the taxpayer

has set up a portion of their home for producing income and get deductions relating to the

running and occupancy expenditure. The taxpayers are under obligation of keeping the

records in a timely manner for their home office expenditure.

Explanation of connection between concepts and indicators of good tax policy:

With the aim of meeting the criteria of good tax policy, the ATO has constantly

placed its emphasis on inappropriate claims relating to deduction and underreporting of

income (Afr.com, 2019). As per the ATO about $8 billion has already been claimed by

taxpayer as home office deduction by approximately 6.7 billion taxpayer while filing 2016-17

returns.

Article 2: ATO measures of removing “inequitable” inquiry:

Facts:

The preliminary inquiry that is done suggest that the labor policy relating to the

eliminating the refundable franking credit for the persons and SMSF is viewed as faulty. The

committee after the taking into account the labor proposal concerning the exclusion of

franking credit for the persons and SMSF is highly unfair and deeply defective policy.

Concise explanation of taxation concepts:

As per the enquiry that was set up by the coalition government it has in its reports

submitted that removing the refundable franking credit would be entirely an injustice to the

middle income group people.

Concise explanation of taxation concepts:

A taxpayer is only allowed to claim the home office expenditure where the taxpayer

has set up a portion of their home for producing income and get deductions relating to the

running and occupancy expenditure. The taxpayers are under obligation of keeping the

records in a timely manner for their home office expenditure.

Explanation of connection between concepts and indicators of good tax policy:

With the aim of meeting the criteria of good tax policy, the ATO has constantly

placed its emphasis on inappropriate claims relating to deduction and underreporting of

income (Afr.com, 2019). As per the ATO about $8 billion has already been claimed by

taxpayer as home office deduction by approximately 6.7 billion taxpayer while filing 2016-17

returns.

Article 2: ATO measures of removing “inequitable” inquiry:

Facts:

The preliminary inquiry that is done suggest that the labor policy relating to the

eliminating the refundable franking credit for the persons and SMSF is viewed as faulty. The

committee after the taking into account the labor proposal concerning the exclusion of

franking credit for the persons and SMSF is highly unfair and deeply defective policy.

Concise explanation of taxation concepts:

As per the enquiry that was set up by the coalition government it has in its reports

submitted that removing the refundable franking credit would be entirely an injustice to the

middle income group people.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Description of link between concepts and indicators of good tax policy:

On eliminating the refundable franking credit it would result in the creation of

situation where the middle income group citizens may be adversely impacted and majority of

those citizens are not going to return to work for covering the loss of income (Afr.com,

2019). A recommendation stated by the report suggest that these kind of policy can be treated

as the element of equal set for promoting overall tax improvement.

Answer to question 7:

The role of tax agent advisors is as follows;

a. The tax agent is responsible for assuring that the clients make the well-informed

decision and seek the advice of tax agent to indulge in the legal arrangement of tax

which does not create an impact on reputation of tax advisors (Igt.gov.au, 2019).

b. The tax advisors are responsible for helping the clients to adhere with the

responsibilities of tax laws and enable them to make a full use of the rights that are

associated to tax matters.

c. The tax agent play an important role in making sure that the clients respect the law.

This comprises of the case laws and unwritten laws which identifies the legal

principles.

Description of link between concepts and indicators of good tax policy:

On eliminating the refundable franking credit it would result in the creation of

situation where the middle income group citizens may be adversely impacted and majority of

those citizens are not going to return to work for covering the loss of income (Afr.com,

2019). A recommendation stated by the report suggest that these kind of policy can be treated

as the element of equal set for promoting overall tax improvement.

Answer to question 7:

The role of tax agent advisors is as follows;

a. The tax agent is responsible for assuring that the clients make the well-informed

decision and seek the advice of tax agent to indulge in the legal arrangement of tax

which does not create an impact on reputation of tax advisors (Igt.gov.au, 2019).

b. The tax advisors are responsible for helping the clients to adhere with the

responsibilities of tax laws and enable them to make a full use of the rights that are

associated to tax matters.

c. The tax agent play an important role in making sure that the clients respect the law.

This comprises of the case laws and unwritten laws which identifies the legal

principles.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Basu, S. (2016). Global perspectives on e-commerce taxation law. Routledge.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/

Chirelstein, M. A. (2015). Federal income taxation: a law student's guide to the leading cases

and concepts. Foundation Press.

Cole, A. (2015). Estate and inheritance taxes around the world. Tax Foundation

https://taxfoundation. org/estateand-inheritance-taxes-around-world.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Getches, D. H., Wilkinson, C. F., Williams Jr, R. A., & Fletcher, M. L. (2014). Cases and

materials on federal Indian law.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., ... & Keyes, K.

(2015). Federal Income Taxation, Principles and Policies (University Casebook

Series). Foundation Press/West Academic.

Heffron, R. J. (2018). The application of distributive justice to energy taxation utilising

sovereign wealth funds. Energy Policy, 122, 649-654.

References:

Basu, S. (2016). Global perspectives on e-commerce taxation law. Routledge.

Chapter 7: Tax practitioners and advisors | Inspector-General of Taxation. (2019). Retrieved

from http://igt.gov.au/publications/reports-of-reviews/use-of-compliance-risk-

assessment-tools/chapter-7-tax-practitioners-and-advisors/

Chirelstein, M. A. (2015). Federal income taxation: a law student's guide to the leading cases

and concepts. Foundation Press.

Cole, A. (2015). Estate and inheritance taxes around the world. Tax Foundation

https://taxfoundation. org/estateand-inheritance-taxes-around-world.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Franking credit removal 'inequitable': inquiry. (2019). Retrieved from

https://www.afr.com/personal-finance/tax/franking-credit-removal-inequitable-and-

deeply-flawed-inquiry-20190404-p51az9

Getches, D. H., Wilkinson, C. F., Williams Jr, R. A., & Fletcher, M. L. (2014). Cases and

materials on federal Indian law.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., ... & Keyes, K.

(2015). Federal Income Taxation, Principles and Policies (University Casebook

Series). Foundation Press/West Academic.

Heffron, R. J. (2018). The application of distributive justice to energy taxation utilising

sovereign wealth funds. Energy Policy, 122, 649-654.

11TAXATION LAW

Jones, S., & Rhoades-Catanach, S. (2015). Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education.

Listokin, D. (2017). Landmarks Preservation and the Property Tax: Assessing Landmark

Buildings for Real Taxation Purposes. Routledge.

Lymer, A., & Hasseldine, J. (Eds.). (2013). The international taxation system. Springer

Science & Business Media.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Mumford, A. (2017). Taxing culture: towards a theory of tax collection law. Routledge.

Sharkey, N., & Murray, I. (2016). Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law

principles. Austl. Tax F., 31, 63.

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Jones, S., & Rhoades-Catanach, S. (2015). Principles of Taxation for Business and

Investment Planning 2016 Edition. McGraw-Hill Education.

Listokin, D. (2017). Landmarks Preservation and the Property Tax: Assessing Landmark

Buildings for Real Taxation Purposes. Routledge.

Lymer, A., & Hasseldine, J. (Eds.). (2013). The international taxation system. Springer

Science & Business Media.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Mumford, A. (2017). Taxing culture: towards a theory of tax collection law. Routledge.

Sharkey, N., & Murray, I. (2016). Reinventing administrative leadership in Australian

taxation: beware the fine balance of social psychological and rule of law

principles. Austl. Tax F., 31, 63.

Sikka, P. (2017, December). Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.